631 DYNAMIC SCORING, FISCAL POLICY, AND THE SHORT-RUN BEHAVIOR OF THE MACROECONOMY EILEEN MAUSKOPF * & DAVE REIFSCHNEIDER * Abstract - Currently, the near-term budgetary consequences of proposed changes to tax laws or federal spending are estimated under the implicit assump- tion that such changes have no measur- able impact on output, prices, interest rates, or income. Consequently, feed- back from the macroeconomy to federal expenditures and the tax base is ignored in scoring tax and spending proposals. This paper considers the advantages and complications involved in dynamic scoring of budget proposals. Such a procedure requires decisions concerning the appropriate macroeconomic model to use and the likely responses of both monetary policy and the public’s expectations to the fiscal initiative. INTRODUCTION In estimating the budgetary impact of tax proposals, it has long been a common practice of the Office of Management and Budget (OMB), the Congressional Budget Office (CBO), and the Joint Committee on Taxation (JCT) to take account of a limited set of economic effects. For instance, if a hike in the federal tax on motor fuels is under consideration, the scoring of its budgetary consequences would typically include the probable fall in the con- sumption of gasoline, based on an estimated price elasticity. Similarly, in the past, proposed reductions in the capital gains tax rate have been as- sumed to speed up capital gains realizations, increasing tax receipts to the Treasury (at least initially). Quantify- ing the revelant elasticity in order to make these microeconomic adjustments can be difficult and controversial. But, in many instances, empirical studies using various types of microlevel data are available to support the choice of one elasticity over another, and, by clarifying the assumptions and method- ology used in deriving the elasticity estimate, these studies can reduce the level of controversy associated with the choice. * Federal Reserve Board, Washington, D.C. 20551.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DYNAMIC SCORING

631

DYNAMIC SCORING,FISCAL POLICY, ANDTHE SHORT-RUNBEHAVIOR OF THEMACROECONOMYEILEEN MAUSKOPF * &DAVE REIFSCHNEIDER *

Abstract - Currently, the near-termbudgetary consequences of proposedchanges to tax laws or federal spendingare estimated under the implicit assump-tion that such changes have no measur-able impact on output, prices, interestrates, or income. Consequently, feed-back from the macroeconomy to federalexpenditures and the tax base is ignoredin scoring tax and spending proposals.This paper considers the advantages andcomplications involved in dynamicscoring of budget proposals. Such aprocedure requires decisions concerningthe appropriate macroeconomic modelto use and the likely responses of bothmonetary policy and the public’sexpectations to the fiscal initiative.

INTRODUCTION

In estimating the budgetary impact oftax proposals, it has long been a

common practice of the Office ofManagement and Budget (OMB), theCongressional Budget Office (CBO), andthe Joint Committee on Taxation (JCT)to take account of a limited set ofeconomic effects. For instance, if a hikein the federal tax on motor fuels isunder consideration, the scoring of itsbudgetary consequences would typicallyinclude the probable fall in the con-sumption of gasoline, based on anestimated price elasticity. Similarly, inthe past, proposed reductions in thecapital gains tax rate have been as-sumed to speed up capital gainsrealizations, increasing tax receipts tothe Treasury (at least initially). Quantify-ing the revelant elasticity in order tomake these microeconomic adjustmentscan be difficult and controversial. But,in many instances, empirical studiesusing various types of microlevel dataare available to support the choice ofone elasticity over another, and, byclarifying the assumptions and method-ology used in deriving the elasticityestimate, these studies can reduce thelevel of controversy associated with thechoice.*Federal Reserve Board, Washington, D.C. 20551.

NATIONAL TAX JOURNAL VOL. L NO. 3

632

Changes to tax laws and spendingprograms can also influence themacroeconomic environment, and theseeconomic effects—by altering tax basesand effective tax rates—feed back tothe flow of revenues to the Treasury.They also can affect governmentexpenditures by changing the cost ofentitlement programs and governmentcompensation; for instance, food stampand Medicaid outlays vary with bothaggregate unemployment and the pricelevel. Finally, changes in the aggregateeconomy influence the cost of servicingthe federal debt—directly throughchanges in interest rates and indirectlythrough changes in the level of indebt-edness caused by variations in taxreceipts and government spending. Anyprocedure for evaluating the budgetaryconsequences of a tax or spendingproposal that takes into account suchmacroeconomic feedback effects is anexample of dynamic scoring. Thechange in the budget deficit induced bythese macroeconomic feedbacks hasbeen termed the fiscal dividend. This isthe extra measure of deficit change overand above that due directly to the policychange.

It has not been standard practice to takeaccount of macroeconomic feedbackeffects or to calculate the fiscal dividendwhen scoring individual budget propos-als. For example, CBO budget estimatesare derived using a forecast of grossdomestic product (GDP), inflation, andinterest rates, conditioned on a “cur-rent-services” projection of outlays andtax rates. Historically, these macroeco-nomic projections have been heldunchanged even as the CBO evaluatedthe budgetary consequences of differingproposals.1 The staff of the JCT haveused the same fixed macroeconomicassumptions to evaluate the effect ofvarious tax changes. Only since 1995

has the CBO departed from pastpractice by presenting a second forecastbased on an alternative fiscal assump-tion—a program to gradually balancethe budget. This second forecast, whencompared with the current-servicesprojection, can be used to compute theCBO’s estimate of the feedback effectsof the policy proposal to real output,aggregate income, interest rates, andthe budget itself (U.S. CongressionalBudget Office, April, 1995, August,1995, December, 1995, May, 1996, andJanuary, 1997).

The ground rules of Congressionalbudget debate also have typicallyinvolved agreeing on a common fixedset of macroeconomic assumptions—usually those of the CBO—to be used inscoring tax and spending proposals.Thus, up until 1995, the Congress’sbudget estimates also were based on animplicit invariance of output, the taxbase, interest rates, and so forth tochanges in fiscal policy. Moreover, evensince 1995, the dynamic element in thebudget scoring process has beenlimited: Neither the Congress nor theCBO has attempted to adjust theestimated macroeconomic effect ofdeficit reduction for variations in thespecifics of balanced-budget proposals,even though the details should influ-ence the projected path of theeconomy.2

In contrast to conditioning a forecast ona current-services assumption, theadministration—more precisely, theOMB, the Council of Economic Advisers,and the Treasury—has always presenteda budget forecast that is contingent onthe passage of the President’s tax andspending proposals. That is, both thedeficit projection and the economicoutlook assume enactment of theadministration’s budget proposals. (Mid-

DYNAMIC SCORING

633

1

2

1

2

year updates take account of incomingeconomic data and changes in policy.)This is the only forecast the administra-tion presents: No current-servicesforecast is available from which onecould determine the administration’sestimate of macroeconomic feedbackeffects of budget proposals, althoughfeedback effects are implicit in theadministration estimates and arediscussed in the staff preparation of theforecast.

It is clear that systematic budget-scoringprocedures, that incorporatemacroeconomic feedback effects,require the use of a full-blown model(or models) of the economy. Suchmodels exist, but they are not easy touse, their predictions can be hard tounderstand even for economists trainedin their use, and no one model or classof models is favored by everyone. Mostimportantly, as discussed below, thesemodels differ in their predictions inquantitatively significant ways. Ifmacroeconomic dynamic scoring wereadopted, such differences could greatlycomplicate budget discussions unlessall participants agreed to use the samemodel or agreed to weight the resultsof different models in the same manner.

Nevertheless, dynamic scoring usingmodels is by no means impossible, asevidenced by the CBO’s recent analysesof the economic and budgetary implica-tions of balancing the deficit (U.S.Congressional Budget Office, April,1995 and January, 1997). In theseanalyses, the CBO considered resultsfrom a variety of macroeconometricstudies to estimate the likely size of thefiscal dividend associated with theimplementation of a program of deficitreduction. Aside from deficit reduction,there also has been interest on the partof the Congress in the feasibility of

using macroeconomic models toestimate the aggregate effects ofreplacing the current income tax systemwith a flat tax or a value-added tax(VAT). For example, the JCT recentlysponsored a symposium on this topic(Engen, Gravelle, and Smetters, 1997).

The remainder of this paper considersthe advisability of dynamic scoring fromseveral perspectives. The followingsection discusses in general terms thepractical difficulties of usingmacromodels in the budget estimationprocess. Chief among these difficulties isthe lack of a consensus model and theresultant need to weight the forecastsof alternative macroeconomic models.The third section assesses the quantita-tive importance of alternative modelspecification, by using several structuralmodels of the U.S. economy to simulatethe macroeconomic and budgetaryeffects of changes in taxation andspending. On balance, economicfeedback effects appear to vary substan-tially across models, even when thesemodels are quite similar in design. Thefourth section considers the implicationsfor dynamic scoring of a factor that isindependent of model design—monetary policy—and uses the FederalReserve Board staff’s econometricmodel, FRB/US, to simulate the effectsof a multi-year program to balance thefederal budget under alternativemonetary policies. This analysis suggeststhat not only the magnitude, but thesign, of the fiscal dividend can varyacross reasonable characterizations ofmonetary policy. Another source ofextra-model uncertainty, the public’sexpectations, is taken up in the follow-ing section. Again using the FRB/USmodel, it is shown that variations in theway expectations are formed—especiallyas regards the initial credibility of amultiyear deficit reduction package—

NATIONAL TAX JOURNAL VOL. L NO. 3

634

influence the short-run response of theeconomy and the budget to the fiscalinitiative.

DYNAMIC SCORING—CAVEATS TO THEUSE OF MACROMODELS

As an abstract proposition, the logic ofdynamically scoring comprehensive fiscalinitiatives would seem impeccable:Budget estimates should be based onthe most accurate available forecast ofaggregate economic conditions, and, ifchanges in fiscal policy have predictableand measurable effects on prices,output, and income, these should betaken into account by policymakers. Ofcourse, policymakers typically confrontnot one but multiple estimates of thelikely macroeconomic effect of a givenchange in fiscal policy. However, from atheoretical standpoint, the existence ofalternative forecasts is not a problemper se; if there are competing models ofthe economy, the “best” forecast issome average of the various predictions.In computing this average, greaterweight might be given to some modelsthan to others on the basis of superiorpredictive accuracy. Given data on thehistorical forecasting errors of thecompeting models, optimal weightscould be derived using standardstatistical pooling techniques, such asthose suggested by Bates and Granger(1969).

Unfortunately, the practical difficulties inimplementing such a methodologywould be considerable. For example,consider the weighting of competingforecasts from alternative models.Looking across the different types ofmacroeconomic models used byeconomists, data on historical forecast-ing errors from which optimal poolingweights could be derived, in general, arenot available. In the case of real businesscycle, overlapping generations, and

other theory-driven calibrated models,no forecasting record exists because themodels were designed for policy analysisand are rarely, if ever, used for forecast-ing. Another type of macromodel—vector autoregression models (VARs)—iswidely used in forecasting, but thesesystems typically have a structure toosimple to be useful for estimating theaggregate feedback effects of fiscalpolicy. Even in the case of commercialmodels such as that maintained by DataResources Incorporated (DRI), wheredata on historical forecasting perfor-mance are available, their relevancy isquestionable: The published forecastswere generated by judgmentallyadjusting a large-scale macroecono-metric model, and so the companies’track records reflect both their modelsand the expertise of their staffs.

Without data on forecasting perfor-mance, it would thus be necessary toweight models according to othercriteria, such as the perceived theoreticaland empirical rigor of their design. More-over, a judgmental weighting scheme ofthis sort might be necessary even if suchdata were generally available, as thereare situations in which historical forecast-ing accuracy would be irrelevant. In part-icular, where tax or spending proposalswould change incentives and other keyaspects of the economy in innovativeand unprecedented ways (such as a shiftto a flat tax), past forecasting accuracymight be a poor indicator of futurepredictive performance.

Even for a disinterested panel of experts,such a judgmental weighting problemwould be difficult because of the manydimensions across which models vary,including theoretical paradigm(Keynesian and classical); macroeco-nomic scope (general versus partialequilibrium and detailed treatment ofshort-run dynamics versus steady-state

DYNAMIC SCORING

635

focus); fiscal detail (many versus fewchannels for government policy toinfluence the economy); theoretical rigor(degree to which a model’s structure isderived from theory); and empiricalmethodology (calibration versusestimation). Given the lack of profes-sional consensus on the appropriate wayto model the macroeconomy, theweight assigned to various predictionswould invariably have a certain arbitraryaspect. Any given weighting schememight be difficult to defend, particularlyin a political context in which changes inweights may have quantitativelyimportant effects on budget estimates.

Some observers may argue that theproblem is considerably more tractablethan suggested here, because there is agood deal of agreement amongeconomists about the effects of manyaspects of government policy. Forexample, consider the case of taxreform. As Engen, Gravelle, andSmetters (1997) note, while predictionsof the long-run supply-side effects ofreplacing the current income tax systemwith a flat tax or a VAT vary acrossmodels, the differences can be traced toa few key differences in design andparameterization. Thus, it can be arguedthat a consensus estimate of long-termeffects is within reach, because furtherresearch should be able to settle thesenarrow specification issues. However,while this potential for consensus maybe real, its relevance to the issue athand—quantifying the near-termbudgetary impacts of changes to fiscalpolicy—is minimal. Disagreement aboutnear-term effects stems not only fromdifferent views about the speed withwhich the supply-side effects emerge—generally acknowledged to be slow—but more importantly from uncertaintyabout the magnitude of the response ofaggregate demand to fiscal change.3

There simply is no consensus among

economists on the importance ofadjustment costs, accelerator effects,and the other sources of dynamicbehavior, including expectations, thatwill condition the path of output in thepresence of a change to the fiscalstance.

At one end of the spectrum are theproponents of traditional large-scalestructural models, such as the DRImodel and Washington UniversityMacro Model (WUMM), as well as theFederal Reserve’s MPS model. This typeof model has several strengths, includ-ing an ability to fit historical data, long-run properties tied to steady-stateneoclassical theory, and structure richenough in detail to be useful in policyanalysis. Nonetheless, many economistsview these models as seriously deficientbecause they fail to distinguish betweenthe sources of dynamic behavior(adjustment costs versus expectations)and because they implicitly assume thatexpectations are formed adaptively(thus subjecting them to the Lucascritique).4

A new generation of structural models,including the Federal Reserve Board’sFRB/US model, has attempted to addressthese concerns through the use ofrational expectations and other innova-tions.5 So too have Leeper and Sims(1994) in an ambitious project todevelop a theory-based general equilib-rium model rigorously fit to historicaldata. Nonetheless, these efforts will notlikely generate an early consensus onthe best way to conduct policy analysisin the framework of a dynamic empiricalmodel.

This concern over modeling short-rundynamics would be misplaced if thebudgetary consequences of such effectswere small. As demonstrated below,however, many changes to fiscal policy

NATIONAL TAX JOURNAL VOL. L NO. 3

636

give rise to substantial fluctuations inaggregate output and budget out-comes, at least in the class of modelsconsidered. Furthermore, these budget-ary effects persist even if it is (unrealisti-cally) assumed that monetary policyperfectly stabilizes the real economy inthe short run. In general, the moreactive monetary policy is in keepingactual GDP at potential, the greater willbe the volatility in interest rates. Hence,changes in nominal income (and associ-ated tax revenue) are minimized at theexpense of changes in interest rates andthe cost of servicing the federal debt.

A final caveat concerns factors impor-tant to the short-run behavior of theeconomy that are independent of theactual model or models of the economyused in dynamic scoring. One suchfactor is the response of monetary policyto changes in economic conditions.Although monetary policy determinesonly the aggregate price level andinflation rate in the long run, in theshort run it can also influence both realinterest rates and the level of realactivity. Thus, policymakers can choosenot only the long-run rate of inflation,but also how much emphasis to placeon stable employment and inflation inthe short run. Alterations to thesechoices will have near-term budgetaryconsequences.

Public reaction to a change in fiscalpolicy is a second factor which cannotbe determined a priori. For example,consider a proposed multiyear programto balance the budget. Under somecircumstances, such a policy might beregarded as highly credible by the publicand would lead to a significant revisiontoday—even before enactment of theprogram—in expectations of long-runeconomic conditions. Under othercircumstances, the full implementationof such a program could be heavily

discounted. These two alternativeexpectational assumptions would havequite different implications for theshort-run behavior of the economy andthe budget.

MODEL UNCERTAINTY

As noted in the previous section, thepredicted macroeconomic consequencesof any fiscal proposal may vary substan-tially across different models. Toillustrate the quantitative importance todynamic scoring of this source ofuncertainty, simulations of simplechanges in fiscal policy are presentedbelow using different structural modelsof the U.S. economy. Four econometricmodels are used in this analysis. Two ofthe models—the DRI model and theWUMM—are currently in use and, withperiodic revisions, have been around forseveral decades. One—the MPSmodel—has only recently been retired atthe Federal Reserve after roughly a 25-year run. The fourth is the FRB/USmodel, which replaced the MPS modelin 1996 as the Federal Reserve Boardstaff’s main model of the domesticeconomy.

The design of these four models is quitesimilar. Their long-run properties areneoclassical, with output growthdetermined in steady state by popula-tion growth and rate of technologicalprogress. The long-run level of outputdepends on the production technology,the amount of labor hours supplied, andlabor productivity, where the lattervaries positively with the capital-laborratio. Fiscal policy, by affecting theaggregate saving rate as well as theafter-tax cost of capital, influences theamount of capital available per worker,and thus the long-run level of outputand income.6 Through the after-tax realwage, fiscal policy also influencespotential output via the long-run supply

DYNAMIC SCORING

637

of labor. This latter effect is important inthe WUMM and DRI models, but is ofminor importance or is nonexistent inthe other two models.

The short-run behavior of all fourmodels is Keynesian, implying thattransitory movements in the level ofoutput and employment are driven byfluctuations in aggregate demand(including that of the government). Thatoutput may deviate from potentialoutput in the short run is a consequenceof various costs of adjustment, as wellas the adaptive nature of expectations (acharacteristic of expectations in all butthe FRB/US model). Wages and prices donot move instantaneously to clear laborand goods markets. Instead, the rate ofwage and price inflation depends onpast wage and price inflation and thedegree of slack in labor and productmarkets, in a manner consistent with anaccelerationist view of the inflationprocess. All four models incorporate anon-accelerating inflation rate ofunemployment (NAIRU) to whichunemployment must converge in thelong run if inflation is to stabilize.7

The models are also similar with respectto estimation methodology. For ex-ample, the models are not calibratedbut are estimated (typically using single-equation least-squares methods),although to varying degrees, the modelsimpose coefficient values based ontheoretical priors about steady-staterelationships. The DRI, WUMM, andMPS models are also alike in thatexpected values of future variables aregenerally implicit, rather than explicit. Asa result, in these models it is notpossible to decompose the sources ofinertia in economic behavior into thosestemming from expectations versusother frictions impeding adjustment. Bycontrast, the FRB/US model employs amore complex estimation methodology

designed to clearly separate the role ofexpectations from other sources ofsluggish adjustment. This approach alsoallows the FRB/US model to be simu-lated under alternative expectationalassumptions, including model-consistentexpectations. Nonetheless, the specifica-tions of many important economicrelationships are similar to thoseembedded in the MPS model.

Each of the four models was simulatedto trace the effects of a change in fiscalpolicy on real output and the federaldeficit over a short horizon (two years).Two policy changes were considered—adecrease in federal purchases of goodsand services and a lump-sum increase infederal personal income taxes, whereboth were calibrated to be worth onepercent of baseline nominal GDP. Thatis, absent feedback effects to aggregatespending and income, and ignoring thereduced interest expense associatedwith the cumulation of smaller deficits,these changes would cause the federalbudget deficit to decline by one percentof baseline GDP. In these simulations,federal outlays—other than interestpayments on the debt and the cyclicallysensitive components of transferpayments—were treated as exogenousin real terms.8

In all cases, monetary policy wasassumed to hold the nominal federalfunds rate at baseline values. Such anonaccommodative monetary policyresponse is not realistic for any but theshortest time periods, given its destabi-lizing properties in these models. (Thispoint is discussed further in the nextsection.) However, it is a useful assump-tion for illustrative purposes, in that iteliminates a potential source of budget-ary difference for the models—differ-ences in the projected path of interestrates. Alternatively, a common monetaryreaction function, such as unemploy-

NATIONAL TAX JOURNAL VOL. L NO. 3

638

ment targeting, could have beenimposed on all models. Such a policyrule would have reduced the variation inoutput simulated across the fourmodels, but would have increased thedisparity in the predicted response ofinterest rates. As a result, it is impossibleto know a priori whether the budgetdifferences across the models would belarger or smaller.

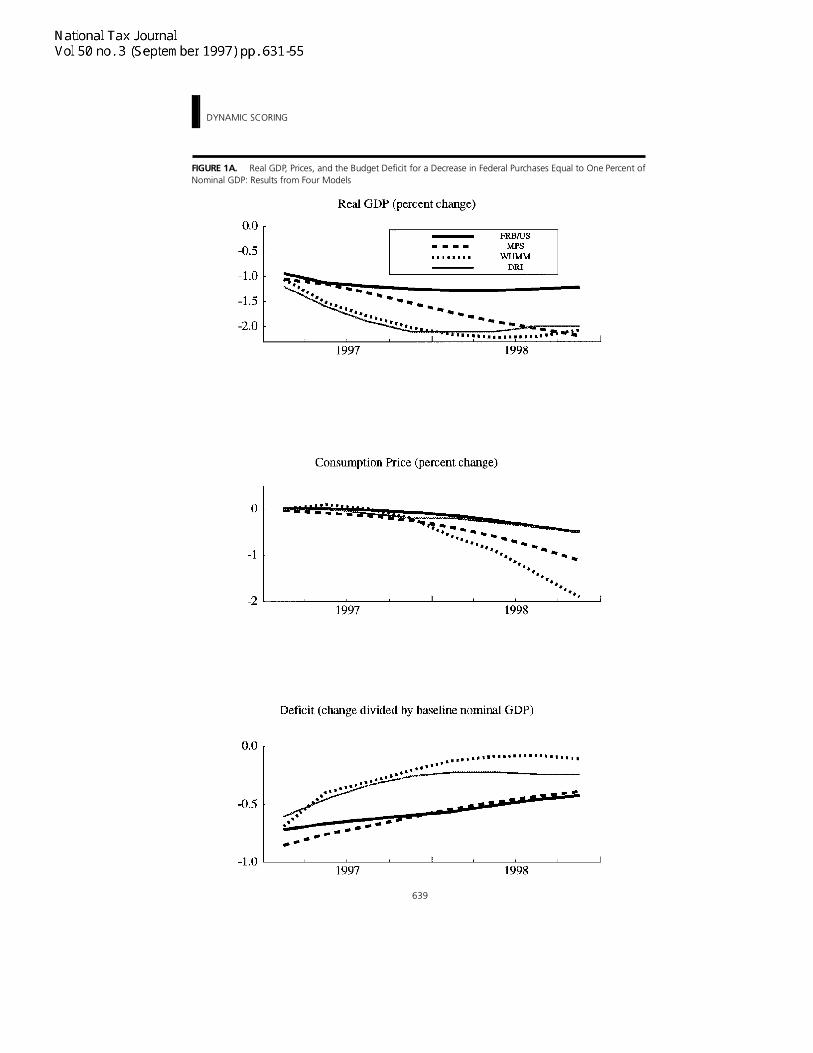

Figure 1A presents simulation results forthe reduction in government purchases.One year after the cuts were imple-mented, real GDP relative to baselinehad fallen by a minimum of 1.25percent (FRB/US) to a maximum of justover 2 percent (DRI). After two years,output is only 1.25 percent lower inFRB/US, but between 2 and 2.25percent lower in the other three models.The smaller contraction in FRB/USderives from the fact that householdsand businesses anticipate an easing inmonetary policy, based on the historicalrelationship between changes to thefederal funds rate and the deviationbetween actual and potential output. Asa result, the public projects the federalfunds rate to decline in the future andthereby to offset the projected weak-ness in activity. This belief helps tosustain expectations of future sales andincome growth, supporting aggregatedemand today.

Even among the three models that showsimilar paths of real output, the conse-quences for prices and the budgetdeficit are quite different. By the end ofthe second year, the simulated decline inconsumption prices varies considerablyacross models—down almost 2 percentin WUMM, about 1 percent in MPS, andonly 0.5 percent in DRI. As for thedeficit, although all models suggest aparing away of initial budget savingsowing to the decline in aggregateincome (and thus taxes), the extent of

the shortfall in budget savings is notreadily predictable from the simulatedchanges to real output and prices. Forinstance, in WUMM, where the com-bined effect on output and prices isultimately the largest, the predictedimprovement in the budget deficit isalmost zero by the end of two years. InMPS, with a smaller price decline, thereduction in the deficit is less than 0.5percent of baseline GDP, but, for DRI,with the smallest price decline of thethree, the deficit reduction is about 0.25percent.

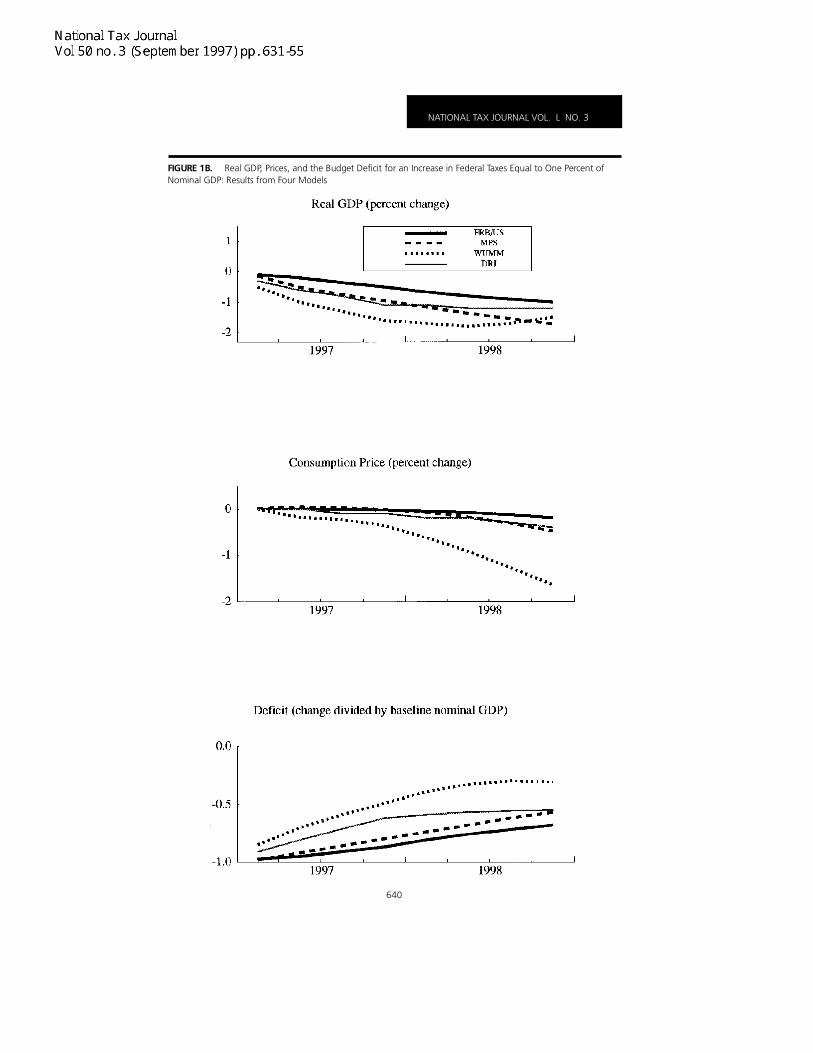

The simulation results for an increase inpersonal income taxes, shown in Figure1B, are no more supportive of aconsensus view for budget savings.Estimates of real output effects at atwo-year horizon range from a declineof 1 percent (FRB/US) to that of 1.75percent (MPS). Again, the limited effectof higher taxes in the FRB/US simulationreflects its expectational structure, inwhich the public believes that theFederal Reserve will ultimately interveneto offset the weakness in demand.Predicted budget outcomes are similarlydiffuse: The improvement in the deficitranges from a high of 0.75 percent(FRB/US) to a low of 0.25 percent(WUMM) relative to baseline nominalGDP.

These simulations show that the rangeof budget outcomes is substantial evenwhen the fiscal initiative under consider-ation is easy to characterize and whenthe macroeconomic models used toscore the initiative are similar in theirbasic design. Outcomes would almostcertainly be more disparate were morecomplicated fiscal initiatives considered—for instance, a change to marginalincome tax rates, which significantlyaffects labor supply decisions in somemodels and not in others. Similarly, evenfor the simplest of fiscal initiatives, the

DYNAMIC SCORING

639

FIGURE 1A. Real GDP, Prices, and the Budget Deficit for a Decrease in Federal Purchases Equal to One Percent ofNominal GDP: Results from Four Models

NATIONAL TAX JOURNAL VOL. L NO. 3

640

FIGURE 1B. Real GDP, Prices, and the Budget Deficit for an Increase in Federal Taxes Equal to One Percent ofNominal GDP: Results from Four Models

DYNAMIC SCORING

641

overlap would likely be small betweenresults generated by these types ofmodels, with their short-run Keynesianfeatures, and those produced byequilibrium business cycle models, withtheir Ricardian households and lack ofsignificant adjustment and expectationallags.

In performing these simulations, it ispossible that our relative ignoranceabout the WUMM and DRI modelscould have led to improper adjustmentsto the models in order to incorporatethe fiscal policy initiative. Thus, theresults may have been biased in favor offinding discord rather than consensusamong the simulations. Consultationswith the DRI and WUMM staffs suggestthat any “execution” bias on our part issmall. Nevertheless, this possibility doespoint out another danger in usingmodels to score fiscal policy changes.Who will run the models and how wellwill they understand the intricacies ofboth the models and the proposedchanges to policy? It is likely that thepolicy analysts who know theexcrutiating details of the various fiscalinitiatives will be ignorant about themanner in which to modify the modelsin order to capture the macroeconomiceffects, including the budgetaryconsequences. Likewise, the modelersare unlikely to know the ins and outs ofevery policy initiative. As a result, honestdifferences could arise across modelsimulations that are attributable toexperimental, not model, design.

MONETARY POLICY

As noted earlier, the budgetary conse-quences of a fiscal initiative depend onthe response of monetary policy. Theprevious section illustrated the range ofbudget outcomes from differentmacroeconometric models when

monetary policy was unresponsive tothe tightened stance of fiscal policy.However, policymakers would beunlikely to hold the federal funds rateconstant for long in the face of apermanent change in fiscal restraint. Asillustrated by the simulations, a policy ofnonaccommodation would lead to asustained fall in real output relative tobaseline levels. Although some oscilla-tory behavior may characterize the pathof real output, all these models suggestthat the long-run implication of such afiscal and monetary mix would be asustained and growing weakness inaggregate output.9

Models such as those considered in theprevious section suggest that a bettercourse for monetary policymakerswould be to allow changes in theeconomy to feed back to the federalfunds rate or to the growth rate ofsome monetary aggregate in order tostabilize the economy. A simple exampleof such a policy is the Taylor rule, wherethe nominal federal funds rate (i) is afunction of four variables: the estimatedequilibrium real interest rate (r*); therate of inflation (π); the target rate ofinflation, chosen by the monetaryauthority (π*); and the percentagedeviation of output from its potentiallevel, (y):

The Taylor rule stabilizes the economyby raising (lowering) the nominal fundsrate whenever inflation is above (below)its target level and aggregate demand isgreater (less) than potential output. Inthe long run, manipulating the fundsrate in line with the Taylor rule causesinflation to converge to its target rate

1

it = r* + 1.5πt – 0.5π* + 0.5yt

NATIONAL TAX JOURNAL VOL. L NO. 3

642

and eliminates the output gap, as longas the equilibrium real interest rate iscorrectly estimated.10

The Taylor rule is just one example of astabilizing policy reaction function. Manyothers are equally feasible, in the senseof being consistent with long-runinflation stability and full employment.For example, the coefficients of theTaylor rule can be altered to modifyeither the aggressiveness with whichpolicymakers seek to stabilize outputand/or inflation in the short run or thepolicymakers’ choice of a long-run targetfor the rate of inflation. Alternatively, therule can be generalized so that thecurrent setting of the funds rate dependsin part on past values of interest rates,inflation, and the output gap. Suchgeneralizations can dampen the short-run volatility of interest rates. Othermodifications of the rule can convert itinto a procedure for targeting the pricelevel or nominal income. Williams (1997)discusses these alternatives and theirimplications for macroeconomic stability.

Because the short-run response of themacroeconomy and the budget mayvary significantly under differentspecifications of the monetary policyrule, it would be convenient to knowexactly how monetary policy willproceed. Unfortunately, budget scorerswill likely have to do their jobs withsubstantial uncertainty about this aspectof the macroeconomy. Even if we knewin advance the relative weightspolicymakers would place on inflationversus output stabilization in the shortrun, all simple rules would at best beonly a crude approximation to the actualpolicy process, because policymakerstake account of a much wider range ofinformation. Indeed, the behavior of thefunds rate has at times deviatedsubstantially from the predictions ofthese simple estimated reaction func-

tions.11 Moreover, even when anestimated rule does a good job insummarizing the manner by whichpolicy responded to changes in inflationand output in the past, its usefulness asa guide to future policy decisions islimited: The economic climate may bedifferent, and the changing membershipof the Federal Open Market Committee(FOMC) may respond in new ways. Theonly elements in the process that onecan be certain about concern the longrun: the FOMC ultimately must ensure asetting for the federal funds rate that isconsistent with full employment andwith output growing in line withpotential growth, because only then isthe rate of inflation stable.

To illustrate the sensitivity of the budgetoutcome to the monetary policy stance,the FRB/US model is simulated allowingfor two alternative characterizations ofthe monetary policy response to a multi-year program to balance the federalbudget by 2002. The first characteriza-tion of policy, denoted “post-1979funds rate rule,” is a version of theTaylor rule estimated over the period1979:Q4 to 1995:Q4, generalized sothat past values of the funds rate, theinflation rate, and the output gapinfluence the choice of the currentfunds rate. The second characterizationof policy, labeled “unemploymenttargeting,” is one where policymakersaggressively adjust the funds rate toprevent the fiscal tightening fromhaving any effect on unemploymentover the simulation period.

In the simulations, the extent of baselinebudgetary imbalance is assumed to besimilar to that projected by the CBO inits January 1997 report—that is, roughlytwo percent of GDP in 2002. Twoalternative means of balancing thebudget are considered. In the first, fiscalpolicy is characterized by a phased-in

DYNAMIC SCORING

643

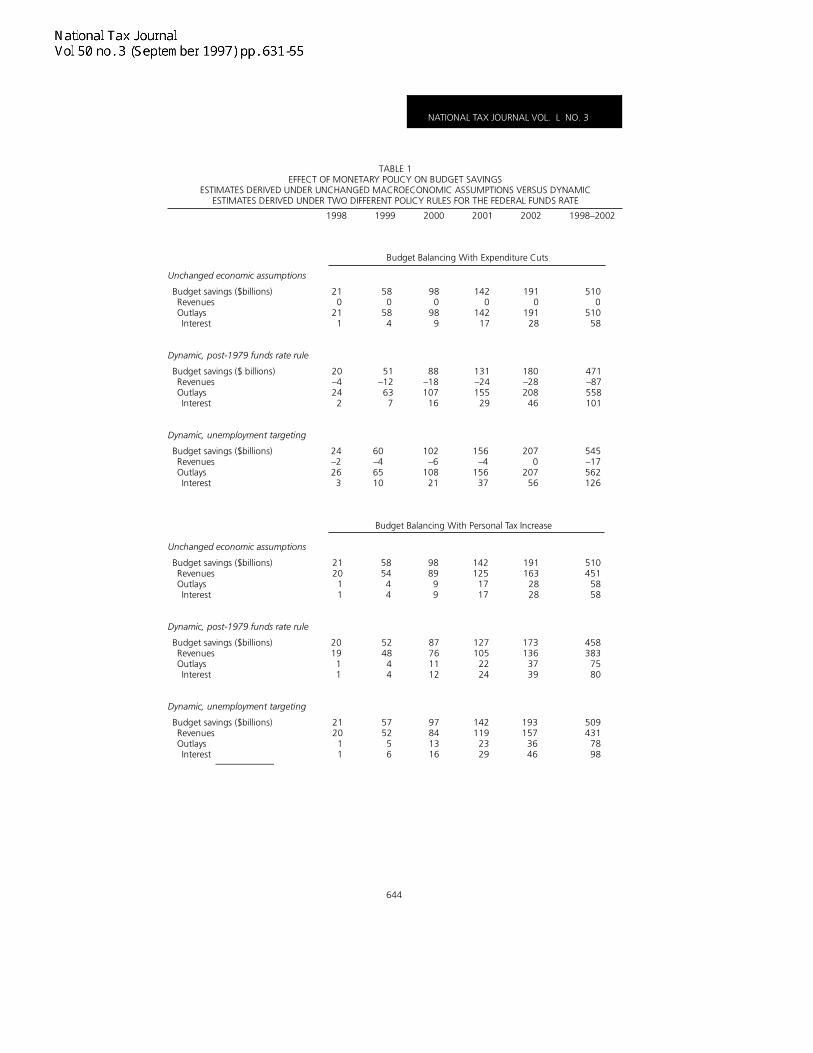

reduction in federal expenditures—halfin purchases of goods and services andhalf in personal transfer payments. Asshown in the top half of Table 1, thesize of the spending cut is calibrated tolead to budget balance by 2002 and tosave a cumulative $510 billion inexpenditures between 1998 and 2002,a portion of which reflects a reductionin the government’s interest paymentson its debt due to the cumulation ofsmaller deficits. The budget savings donot take into account any feedbackfrom the policy change to interest ratesor to the tax base through changes inthe level or composition of nominalincome and spending. The reductions intotal outlays and in interest expendituresare shown under the heading “un-changed economic assumptions.”

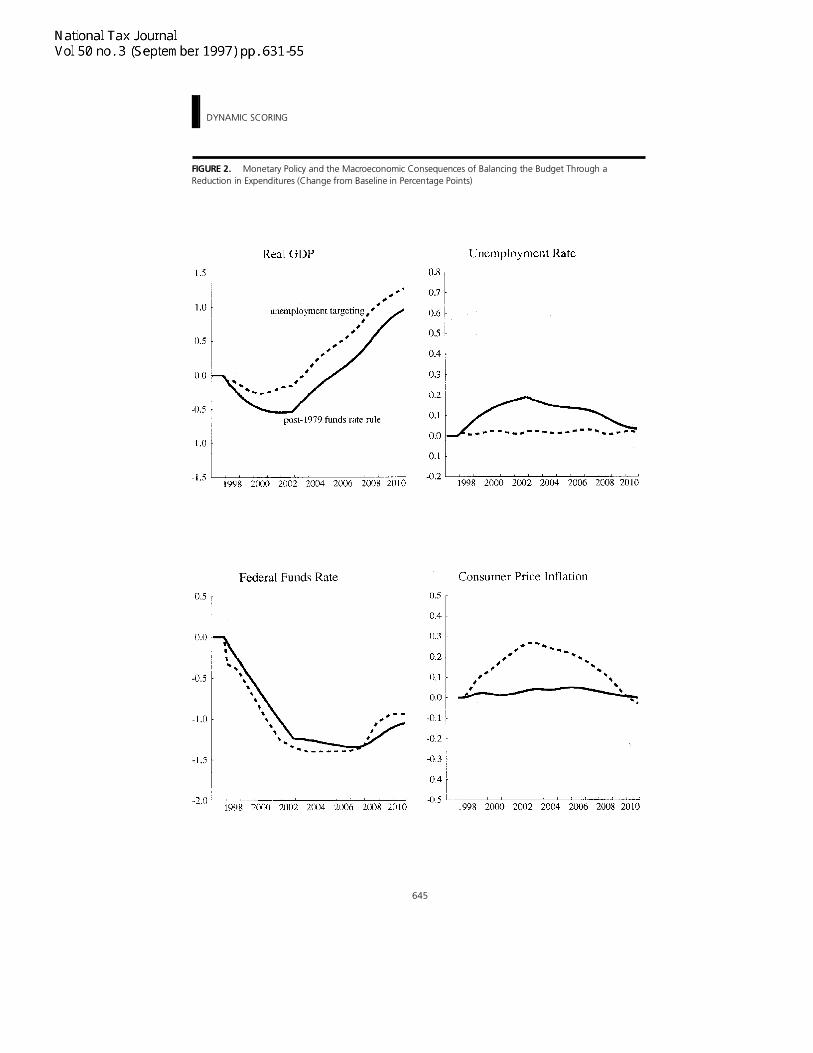

The sensitivity of the estimated budgetsavings from this course of expenditurereduction to the conduct of monetarypolicy can be gauged from the otherpanels in the top half of Table 1. Underthe post-1979 funds rate rule, thecumulative budget savings are $471billion, almost eight percent less thanwhen scored assuming unchangedeconomic conditions. Under unemploy-ment targeting, the savings are $545billion, close to seven percent more thanwhen scored assuming no change tomacroeconomic variables. Figure 2shows the factors that contribute to thedisparity in estimated budget savings—lower interest rates and higher realoutput under unemployment targetingthan under the post-1979 rule. Inaddition, unemployment targeting leadsto a higher inflation rate than does thepost-1979 rule, in part because theformer policy is consistent with a greaterlevel of resource utilization and in partbecause this policy is associated with alarger depreciation of the exchangerate. All told, unemployment targetingleads to higher nominal income (and

income tax revenues) as well as lowerinterest expenditures compared to thepost-1979 rule.

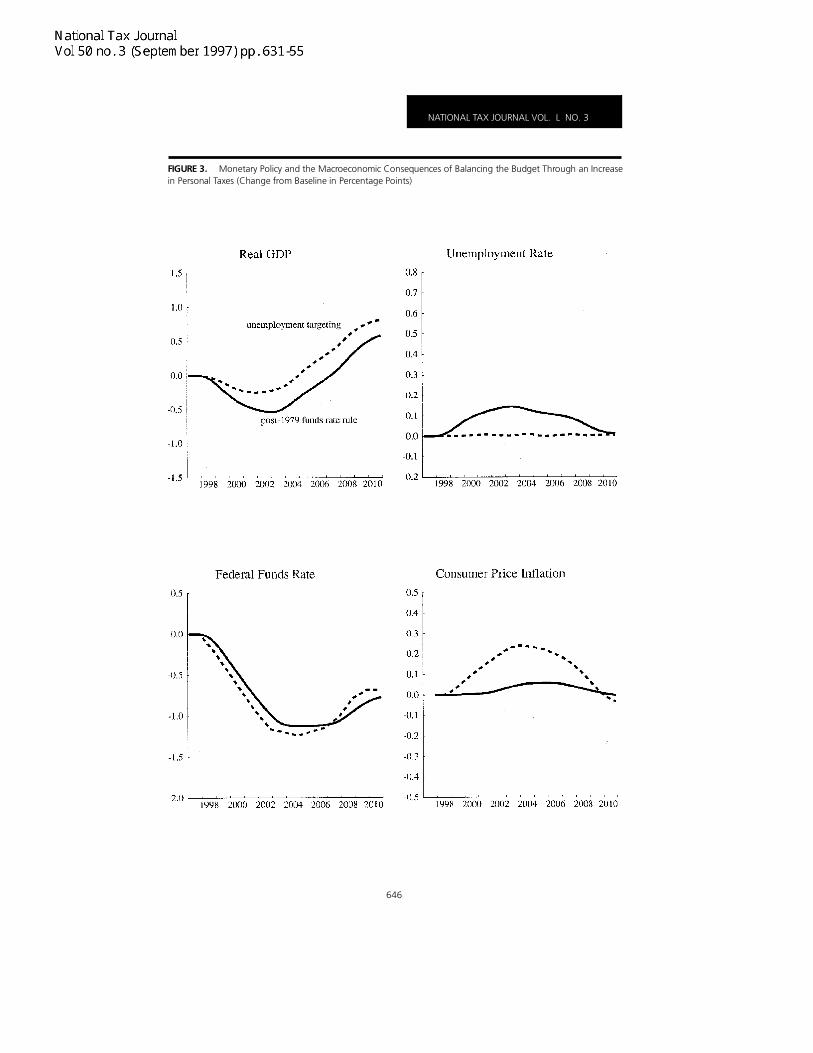

The bottom half of Table 1 and Figure 3present the estimated budget savingsand effects on output, interest rates,and inflation for a fiscal contractionenacted through a lump-sum increase inpersonal taxes. The tax increase and theassociated savings on interest expendi-tures, scored assuming no macroeco-nomic consequences, mirror the budgetsavings from the policy of expenditurecuts described above. This time,following the post-1979 funds rate ruleresults in cumulative budget savings of$459 billion, ten percent less than whenscored ignoring macroeconomicfeedback effects. Targeting the unem-ployment rate results in $509 billioncumulative savings, almost identical tothe estimated savings under unchangedeconomic assumptions.

As suggested by these simulationresults, the range of estimated budgetsavings generated by alternativespecifications for monetary policy is notinvariant to the details of the fiscalpolicy initiative. For instance, considerthe imposition of an excise tax thatraises as much tax revenue as the lump-sum income tax when both are scoredignoring macroeconomic feedbackeffects. Absent a change in the fundsrate, the imposition of the excise taxaffects the rate of inflation in two ways.The direct effect of the tax is to raise therate of inflation at the time the tax isfirst imposed, while the subsequent lossof disposable income reduces outputand reduces the pressure on prices.Under the post-1979 rule, the jump ininflation may warrant a rise in the fundsrate, at least initially, further weakeningreal output but moderating the directinflationary impact of the excise tax.But, under the unemployment targeting

NATIONAL TAX JOURNAL VOL. L NO. 3

644

TABLE 1EFFECT OF MONETARY POLICY ON BUDGET SAVINGS

ESTIMATES DERIVED UNDER UNCHANGED MACROECONOMIC ASSUMPTIONS VERSUS DYNAMICESTIMATES DERIVED UNDER TWO DIFFERENT POLICY RULES FOR THE FEDERAL FUNDS RATE

1998 1999 2000 2001 2002 1998–2002

Unchanged economic assumptions

Budget savings ($billions)RevenuesOutlaysInterest

Dynamic, post-1979 funds rate rule

Budget savings ($ billions)RevenuesOutlaysInterest

Dynamic, unemployment targeting

Budget savings ($billions)RevenuesOutlaysInterest

Unchanged economic assumptions

Budget savings ($billions)RevenuesOutlaysInterest

Dynamic, post-1979 funds rate rule

Budget savings ($billions)RevenuesOutlaysInterest

Dynamic, unemployment targeting

Budget savings ($billions)RevenuesOutlaysInterest

Budget Balancing With Expenditure Cuts

5100

51058

1910

19128

1420

14217

980

989

580

584

210

211

471–87558101

180–28208

46

131–24155

29

88–18107

16

51–12637

20–4242

545–17562126

2070

20756

156–4

15637

102–6

10821

60–46510

24–2263

510451

5858

191163

2828

142125

1717

988999

585444

212011

458383

7580

173136

3739

127105

2224

87761112

524844

201911

509431

7898

193157

3646

142119

2329

97841316

575256

212011

Budget Balancing With Personal Tax Increase

DYNAMIC SCORING

645

FIGURE 2. Monetary Policy and the Macroeconomic Consequences of Balancing the Budget Through aReduction in Expenditures (Change from Baseline in Percentage Points)

NATIONAL TAX JOURNAL VOL. L NO. 3

646

FIGURE 3. Monetary Policy and the Macroeconomic Consequences of Balancing the Budget Through an Increasein Personal Taxes (Change from Baseline in Percentage Points)

DYNAMIC SCORING

647

rule, the funds rate would be unam-biguously reduced in order to preventdemand from falling. Conceivably, therange of budget savings consistent withalternative monetary policies widenswhen a change to excise taxes—whichhave direct consequences for the pricelevel and the rate of inflation—ratherthan income taxes is contemplated.

EXPECTATIONS

Perhaps the most uncertain element inpredicting how a particular change infiscal policy will influence the economyand the budget is the effect the changein policy has on the public’s expectationsabout the future course of the economy.The absence of reliable data on expecta-tions has led to a debate about the wayin which households and firms formexpectations, the scope of informationthat they use in forming expectations,and the speed with which they reviseexpectations in response to newinformation such as a change in policy.Nonetheless, although economists arefar from a consensus on the appropriateway to specify expectations or theprocess by which expectations areformed, there is widespread agreementthat expectations are critical to eco-nomic decisionmaking. In fact, they maybe the wild card in the short-runtransmission of monetary and fiscalpolicies to the economy.

Macroeconometric models that empha-size the short-run determination ofoutput have taken alternative routes todealing with expectations. The MPS,WUMM, and DRI models use adaptiveexpectations, whereby the forecast of aparticular variable depends on the samevariable’s behavior in the recent past.Lucas’s critique of adaptive expectationsled to the development of macroeco-nomic models with rational or model-consistent expectations, defined as

expectations that are equal to theforecasts of the complete model of theeconomy. Somewhere between thesetwo extremes is the notion that house-holds and firms make a significant effortto understand the economy, especiallyas regards those factors important totheir decision making, but that thiseffort falls short of a complete under-standing of the economy.

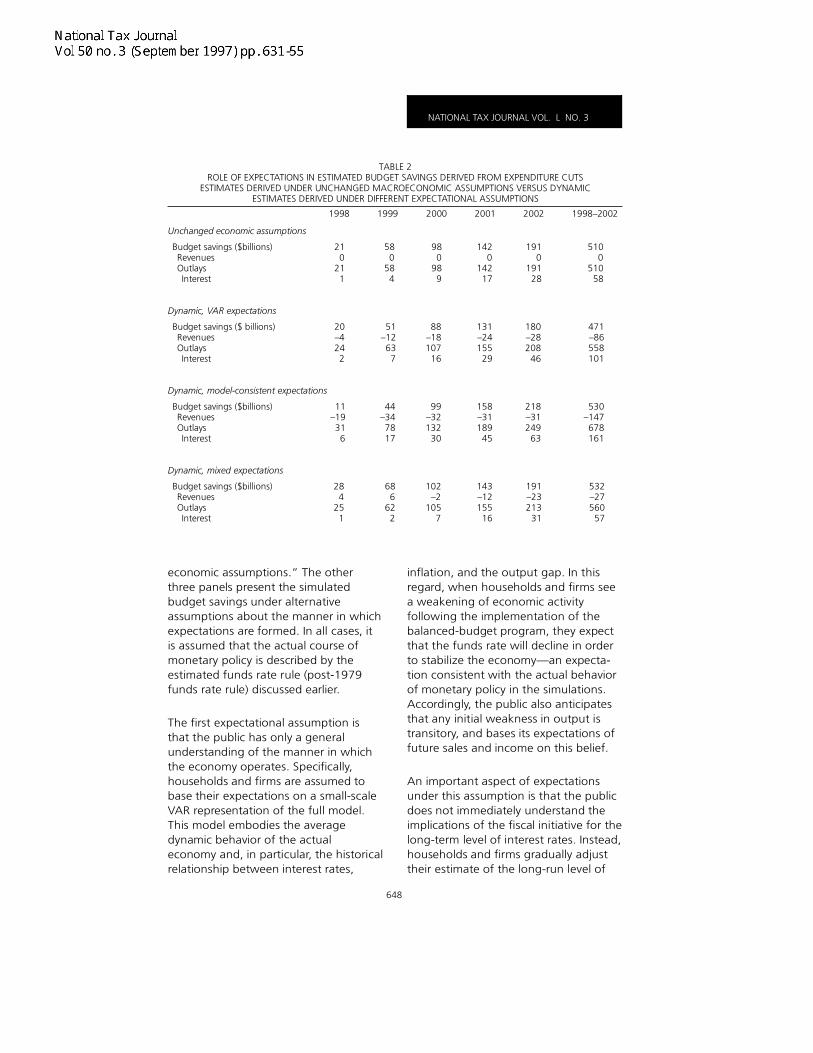

Just how important the expectationsprocess can be for the budgetaryconsequences of a change in fiscalpolicy is illustrated by simulations of theFRB/US model under alternative assump-tions about the manner in which thepublic forms its beliefs about the future.As noted earlier, in FRB/US, theeconomy’s dynamic behavior is decom-posed into two separately identifiablecomponents—one part attributable toexpectations and the other arising fromintrinsic frictions that give rise tosluggish adjustment. Because theexpectational channels have been clearlyidentified, the characterization ofexpectations can be altered—e.g., asregards what information is taken intoaccount in forming expectations andwhen expectations are revised inresponse to new information—withoutchanging the rest of the model’sdynamic structure.12

Tables 2 and 3 and Figures 4 and 5illustrate the sensitivity of macroeco-nomic and budget projections toalternative expectational assumptions.The fiscal initiatives considered here arethe same as those discussed in theprevious section—a gradual cut tofederal expenditures or a gradualincrease in personal income taxes,intended to lead to budget balance by2002. The scoring of the fiscal initiativeassuming no macroeconomic feedbackis given in the top panel of the tablesunder the heading “Unchanged

NATIONAL TAX JOURNAL VOL. L NO. 3

648

economic assumptions.” The otherthree panels present the simulatedbudget savings under alternativeassumptions about the manner in whichexpectations are formed. In all cases, itis assumed that the actual course ofmonetary policy is described by theestimated funds rate rule (post-1979funds rate rule) discussed earlier.

The first expectational assumption isthat the public has only a generalunderstanding of the manner in whichthe economy operates. Specifically,households and firms are assumed tobase their expectations on a small-scaleVAR representation of the full model.This model embodies the averagedynamic behavior of the actualeconomy and, in particular, the historicalrelationship between interest rates,

inflation, and the output gap. In thisregard, when households and firms seea weakening of economic activityfollowing the implementation of thebalanced-budget program, they expectthat the funds rate will decline in orderto stabilize the economy—an expecta-tion consistent with the actual behaviorof monetary policy in the simulations.Accordingly, the public also anticipatesthat any initial weakness in output istransitory, and bases its expectations offuture sales and income on this belief.

An important aspect of expectationsunder this assumption is that the publicdoes not immediately understand theimplications of the fiscal initiative for thelong-term level of interest rates. Instead,households and firms gradually adjusttheir estimate of the long-run level of

TABLE 2ROLE OF EXPECTATIONS IN ESTIMATED BUDGET SAVINGS DERIVED FROM EXPENDITURE CUTS

ESTIMATES DERIVED UNDER UNCHANGED MACROECONOMIC ASSUMPTIONS VERSUS DYNAMICESTIMATES DERIVED UNDER DIFFERENT EXPECTATIONAL ASSUMPTIONS

1998 1999 2000 2001 2002 1998–2002

Unchanged economic assumptions

Budget savings ($billions)RevenuesOutlaysInterest

Dynamic, VAR expectations

Budget savings ($ billions)RevenuesOutlaysInterest

Dynamic, model-consistent expectations

Budget savings ($billions)RevenuesOutlaysInterest

Dynamic, mixed expectations

Budget savings ($billions)RevenuesOutlaysInterest

5100

51058

1910

19128

1420

14217

980

989

580

584

210

211

471–86558101

180–28208

46

131–24155

29

88–18107

16

51–12637

20–4242

530–147678161

218–31249

63

158–31189

45

99–32132

30

44–347817

11–19316

532–27560

57

191–23213

31

143–12155

16

102–2

1057

686

622

284

251

DYNAMIC SCORING

649

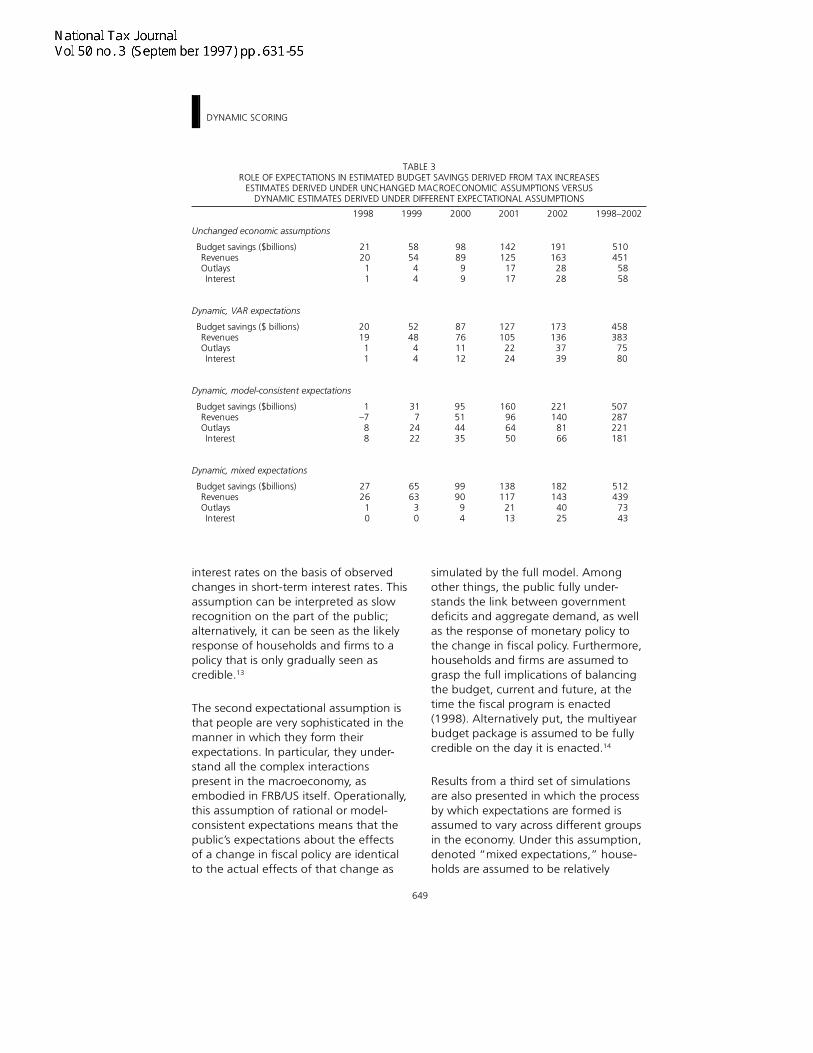

interest rates on the basis of observedchanges in short-term interest rates. Thisassumption can be interpreted as slowrecognition on the part of the public;alternatively, it can be seen as the likelyresponse of households and firms to apolicy that is only gradually seen ascredible.13

The second expectational assumption isthat people are very sophisticated in themanner in which they form theirexpectations. In particular, they under-stand all the complex interactionspresent in the macroeconomy, asembodied in FRB/US itself. Operationally,this assumption of rational or model-consistent expectations means that thepublic’s expectations about the effectsof a change in fiscal policy are identicalto the actual effects of that change as

simulated by the full model. Amongother things, the public fully under-stands the link between governmentdeficits and aggregate demand, as wellas the response of monetary policy tothe change in fiscal policy. Furthermore,households and firms are assumed tograsp the full implications of balancingthe budget, current and future, at thetime the fiscal program is enacted(1998). Alternatively put, the multiyearbudget package is assumed to be fullycredible on the day it is enacted.14

Results from a third set of simulationsare also presented in which the processby which expectations are formed isassumed to vary across different groupsin the economy. Under this assumption,denoted “mixed expectations,” house-holds are assumed to be relatively

TABLE 3ROLE OF EXPECTATIONS IN ESTIMATED BUDGET SAVINGS DERIVED FROM TAX INCREASES

ESTIMATES DERIVED UNDER UNCHANGED MACROECONOMIC ASSUMPTIONS VERSUSDYNAMIC ESTIMATES DERIVED UNDER DIFFERENT EXPECTATIONAL ASSUMPTIONS

1998 1999 2000 2001 2002 1998–2002

Unchanged economic assumptions

Budget savings ($billions)RevenuesOutlaysInterest

Dynamic, VAR expectations

Budget savings ($ billions)RevenuesOutlaysInterest

Dynamic, model-consistent expectations

Budget savings ($billions)RevenuesOutlaysInterest

Dynamic, mixed expectations

Budget savings ($billions)RevenuesOutlaysInterest

510451

5858

191163

2828

142125

1717

988999

585444

212011

458383

7580

173136

3739

127105

2224

87761112

524844

201911

507287221181

221140

8166

160966450

95514435

317

2422

1–788

512439

7343

182143

4025

138117

2113

999094

656330

272610

NATIONAL TAX JOURNAL VOL. L NO. 3

650

FIGURE 4. Expectations and the Macroeconomic Consequences of Balancing the Budget Through a Reduction inExpenditures (Change from Baseline in Percentage Points)

DYNAMIC SCORING

651

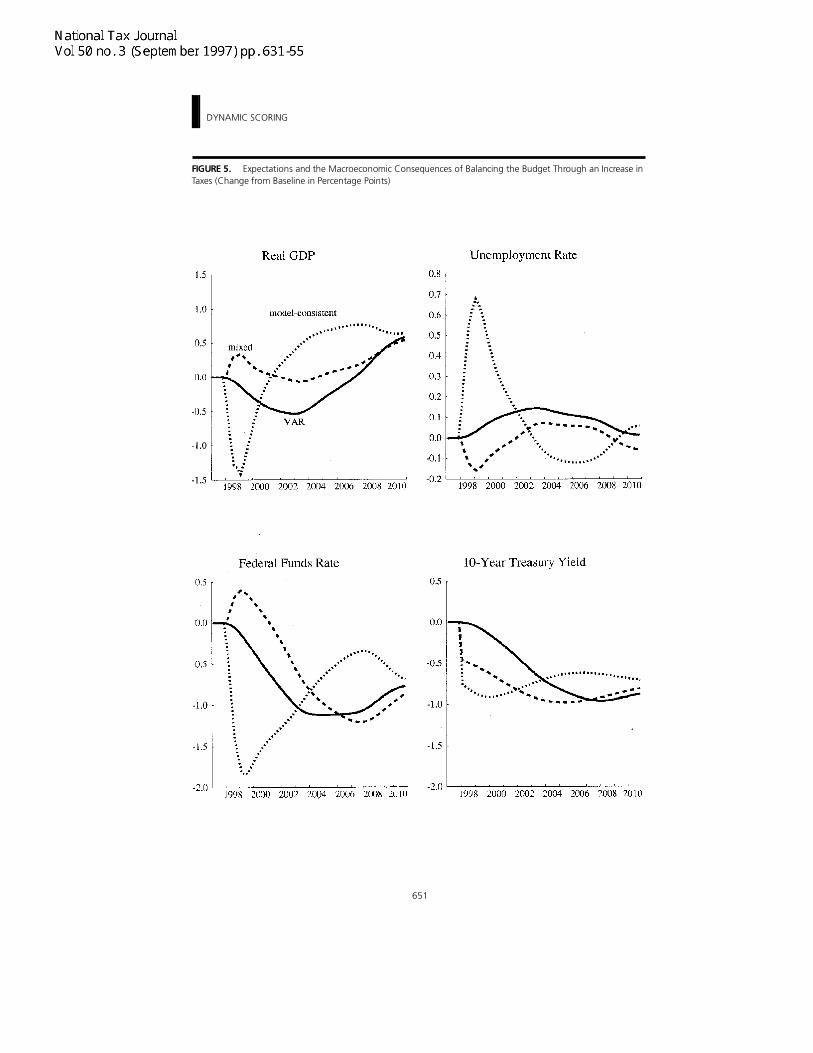

FIGURE 5. Expectations and the Macroeconomic Consequences of Balancing the Budget Through an Increase inTaxes (Change from Baseline in Percentage Points)

NATIONAL TAX JOURNAL VOL. L NO. 3

652

unsophisticated in their forecastingmethods, with their expectationsderived from small-scale VAR models. Incontrast, firms and investors areassumed to use sophisticated predictiontechniques and have model-consistentexpectations. Such a difference insophistication might arise because ofdifferences in expertise. Alternatively, itmay reflect a greater payoff to the lattergroup for accurate forecasting. Inaddition, households are assumed tolearn only gradually about the long-runeconomic implications of the change infiscal policy, whereas firms and investorsrecognize them immediately.

As can be seen in Tables 2 and 3, thesedifferences in expectational assumptionsyield significant variations in thedynamic scoring of the balanced budgetprogram. For example, under VARexpectations, cumulative budget savingsfrom the reduction in spending are eightpercent less than the estimate of savingsassuming no feedback, whereas theyare four percent higher under mixedexpectations. Cumulative budgetsavings under model-consistent expecta-tions are estimated to be similar tothose obtained under mixed expecta-tions, but savings in the first two yearsof the program are predicted to besmaller than those obtained undereither alternative assumption. As shownin Table 3, these differences are esti-mated to be even more pronounced ifbudget balance is achieved through taxincreases.

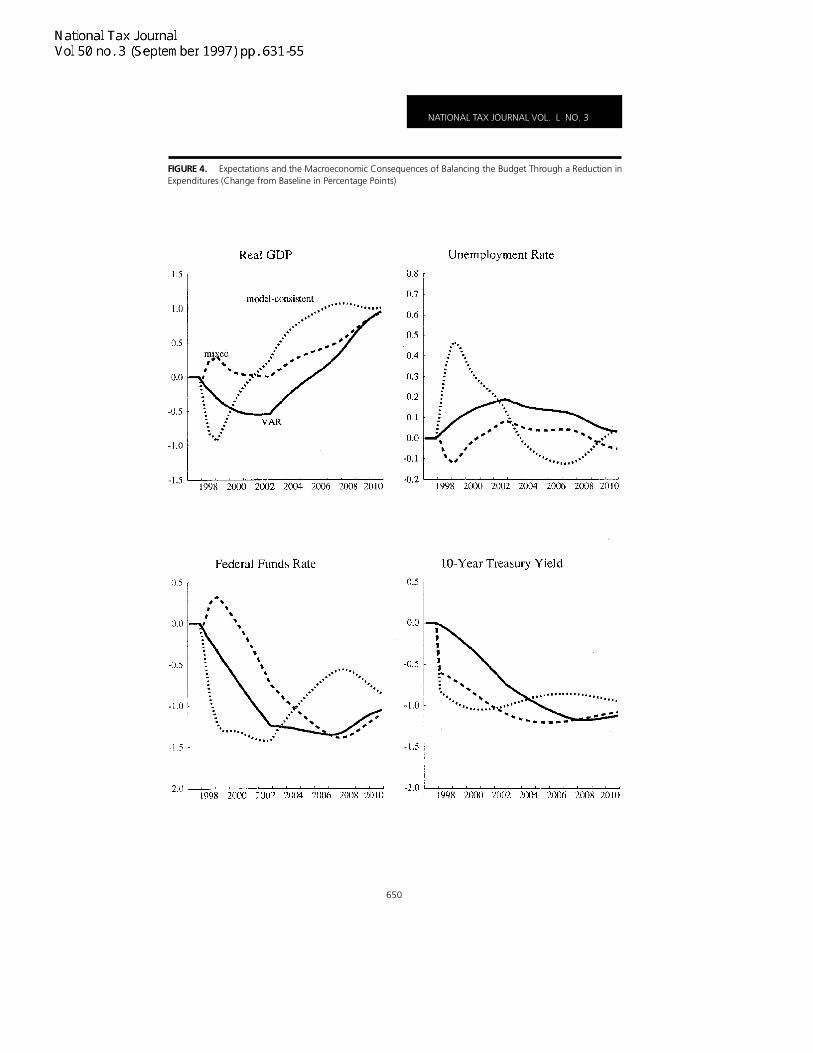

Figures 4 and 5 illustrate the macroeco-nomic forces underlying these differ-ences. Under either model-consistent ormixed expectations, bond yields dropimmediately upon enactment of theprogram because investors recognizethe implications of fiscal restraint for thelong-run level of real interest rates.Prompted by these same expectations,

the stock market rallies and the dollardepreciates. This anticipatory responseof financial markets, occurring as it doeswell before the bulk of the fiscalrestraint is in place, helps to sustainaggregate demand during the initialphase of the program by lowering thecost of borrowing, increasing householdwealth, and improving the internationalcompetitiveness of domestic firms.

However, under model-consistentexpectations, the spur to investment,consumption, and net exports from theimprovement in financial conditions isnot enough to prevent an initial declinein aggregate output and employment.This is because households understandthe implications of balancing the budgetfor their future income. In the FRB/USmodel, consumption today dependsupon expectations of future income,particularly income over the next fewyears. Although long-run income isincreased by the reduction in deficitspending—owing to increased capitalformation and other supply-side effects—in the first few years of the program,expected future after-tax income fallssubstantially, leading to a cutback inconsumer spending. The expecteddecline in income is more pronounced ifbudget savings are achieved solely atthe expense of households through anincrease in personal taxes, rather thanby having a portion of fiscal restraintoccur through a reduction in govern-ment purchases.

By contrast, if households do not initiallyrecognize the implications of deficitreduction for their future after-taxincome but firm and investor awarenessboosts the financial markets, the short-run response of the economy may bepositive, not negative. Under theseconditions, the stimulative effects ofrallies in the bond and stock market are

DYNAMIC SCORING

653

not offset by downward revisions toincome expectations, and aggregatedemand (particularly investment) rises.In fact, the strength of the economyleads to a temporary increase in thefederal funds rate, prompted by theneed to keep inflation in check duringthis early period. In the long run,however, the federal funds rate—as wellas other interest rates—declines underall expectational assumptions by aboutthe same amount.

Conclusions

This paper highlights some of thedifficulties encountered in assessing thelikely impact of fiscal policy decisions onthe economy and the feedback from theinduced changes in the economy to thefederal budget. Such an accounting ofthe macroeconomic impact is the criticalelement in formulating a more realisticassessment of the budgetary conse-quences of a proposed change to fiscalpolicy. To evaluate the impact of policychange on the dynamic path of theaggregate economy will involve acertain degree of controversy given thecurrent state of economic knowledge.First, there is a broad range of macro-economic models, which purport toaccurately represent the importantrelationships of the economy. It wasdemonstrated that, even among asomewhat narrow subset of thesemodels, substantial differences emergein the simulated response of theeconomy and the budget to relativelysimple fiscal initiatives. Yet, it will benecessary to choose among thesemodels or at least to choose a set ofweights to apply to the results of thedifferent models. Assumptions aboutthe probable response of monetarypolicy to the change in the fiscal stancewill also affect the results of dynamicscoring. Finally, the scoring requires thata judgment be made about how the

public’s expectations are formed,including the degree to which the publicanticipates the policy change and/orbelieves the announced policy iscredible. For all these reasons, achievingconsensus on the dynamic scoring of afiscal policy initiative will not be easy,and pursuing the status quo in budgetscoring may be the appropriate courseof action now. Nevertheless, it shouldbe realized that this is a second-bestsolution, and one that should bereplaced if and when the state ofeconomic knowledge permits a broaderconsensus regarding the macroeco-nomic consequences of fiscal policy.

ENDNOTES

The views expressed in this paper do notnecessarily reflect those of the Board of Governorsof the Federal Reserve System or its staff. Wewould like to thank the following individuals fortheir help and comments: Robert Anderson of theOMB; Glenn Follette of the Federal Reserve Board;Matthew Salomon of the CBO; Joel Prakken ofMacroeconomic Advisors; and Chris Probyn, MarkLasky, and David Wyss of DRI. We would also liketo thank Brian Doyle for his able researchassistance.

1 The CBO forecast is updated twice a year, at whichtime the CBO takes into account changes to botheconomic conditions and current-services law.

2 Estimates of the fiscal dividend associated withbalancing the budget have fallen since the CBOpublished its first comprehensive estimate inDecember 1995. But, this is mainly due to adecline in the actual and projected current servicesdeficit. See, for example, the CBO reports ofDecember, 1995, May, 1996, and January, 1997.

3 The slow response of aggregate supply reflects thedifficulty of altering the three factors thatdetermine the economy’s long-run productivepotential—multifactor productivity, capital stock,and labor force participation. For example,changes in government support for education andresearch can probably alter the rate of technologi-cal progress, but only very slowly given productgestation lags. Similarly, while government policiescan influence the capital stock through infrastruc-ture spending, tax investment incentives, andcompetition for the pool of private saving, thenature of capital accumulation ensures that thisprocess is slow. Based on standard estimates ofthe aggregate production function, an increase inpotential GDP of one percent would require a

NATIONAL TAX JOURNAL VOL. L NO. 3

654

three percent increase in the capital stock. To raisethe capital stock three percent in one year wouldrequire a thirty percent increase in the level ofinvestment—an increase that would be hard forpolicy to achieve, given the time it takes to developnew investment plans and to produce and installnew buildings and machinery. Finally, while it istheoretically possible to alter aggregate labor forceparticipation quickly through changes in the after-tax return to working, habit persistance,adjustment costs, and institutional rigidities makeit likely that such effects would manifestthemselves over a prolonged period of time.

4 An additional criticism of such models is that theirestimation involves arbitrary assumptions aboutwhich variables are included as direct determinantsof any given variable in the system.

5 For details on the new FRB/US model, see Braytonand Tinsley (1996). Other examples of rationalexpectation structural models include the Taylor(1993) multicountry macromodel and theInternational Monetary Fund’s MULTIMOD (Massonet al, 1988).

6 In the DRI model, fiscal policy also affects capitalavailability directly through government investmentin infrastructure.

7 The long-run inflation rate is determined by themonetary authority through its long-run setting formonetary growth.

8 In the DRI simulations, it was not possible toexogenize all expenditure components in realterms. One of these components—net subsidiesof government enterprises—was exogenized innominal terms, but, as its dollar value is quitesmall, the effect on the simulation results wasinconsequential. Two components of current-dollar transfer payments were also endogenous,but they were adjusted to keep their simulatedvalues close to baseline in real terms.

9 The source of this instability—illustrated moststarkly by the MPS results—is the implication ofthe policy for real interest rates: With the nominalfunds rate held constant, the contractionary effectof fiscal restraint reduces inflation and raises thereal interest rate, which, in turn, depresses realactivity and inflation further. As a result, realinterest rates increase again, setting in motion adownward spiral of the economy. The speed atwhich this spiral emerges is damped in the othermodels because of various factors—in FRB/US, forexample, by the public’s expectation that such anonaccommodative policy will not be pursued forlong. Nevertheless, such an unstable (andunrealistic) outcome would eventually emerge inlonger simulations of all four models, or in anymodel with an accelerationist view of inflation anda dependence of spending on the real interest rate.

10 This is not a stringent restriction, in that trendmovements in the observed real federal funds ratecan be used to update the estimated equilibrium

real funds rate. Such an updating rule is used inFRB/US to ensure that r* converges to theequilibrium real funds rate.

11 For example, the standard error of a one-step-ahead prediction of the federal funds rate over the1980–96 period is more than a percentage pointfor two of the estimated policy rules used in theFRB/US model.

12 Of course, the integrity of simulation resultsobtained under alternative expectational processesrests on the assumption that the underlyingstructural parameters of the economy have beenidentified. Without this assumption, it would notbe true that the model’s adjustment costs (i.e., itscoefficients) would remain invariant to changes inthe characterization of expectations.

13 Because this same expectational assumption wasused in the monetary policy experiments, theresults reported in Tables 2 and 3 and Figures 4and 5 under the heading “VAR expectations” areidentical to those reported in Table 1 and Figures 2and 3 under the label “post-1979 funds rate rule.”

14 It is worth noting that this pairing of model-consistent expectations and immediate recognitionis somewhat arbitrary. People could have model-consistent expectations but might not immediatelyreact to the long-run consequences of deficitreduction, perhaps because it is initially suspectedthat future elements of the multiyear package willnot be enacted or will be reversed at a later date.Alternatively, they could anticipate the policy’slong-run consequences and begin to react to themeven before the policy change is implemented.Similar variations are possible under VARexpectations as well. For a further discussion ofthis issue, see Brayton et al. (1997).

REFERENCES

Bates, John M., and Clive W. J. Granger.“The Combination of Forecasts.” OperationalResearch Quarterly 20 No. 4 (December, 1969):451–68.

Brayton, Flint, Eileen Mauskopf, DavidReifschneider, Peter Tinsley, and JohnWilliams. “The Role of Expectations in the FRB/US Macroeconomic Model.” Federal ReserveBulletin 83 (April, 1997): 227–45.

Brayton, Flint, and Peter Tinsley. “A Guide toFRB/US: A Macroeconomic Model of the UnitedStates.” Finance and Economics DiscussionSeries No. 1996-42. Washington, D.C.: Boardof Governors of the Federal Reserve, 1996.

Engen, Eric M., Jane Gravelle, and KentSmetters. “Dynamic Tax Models: Why They Dothe Things They Do. National Tax Journal 50 No.3 (September, 1997): 683–706.

Leeper, Eric, and Christopher A. Sims.“Toward a Modern Macroeconomic Model

DYNAMIC SCORING

655

Usable for Policy Analysis.” NBER ResearchWorking Paper No. 4761. Cambridge, MA:National Bureau of Economic Research, 1994.

Masson, Paul, Steven Symansky, Rick Haas,and Michael Dooley. “MULTIMOD: A Multi-Region Econometric Model.” Staff Studies forthe World Economic Outlook. Washington,D.C.: International Monetary Fund, 1988.

Taylor, John. Macroeconomic Policy in a WorldEconomy. New York: Norton, 1993.

U.S. Congressional Budget Office. AnAnalysis of the President’s Budgetary Proposalsfor Fiscal Year 1996. Washington, D.C., April,1995.

U.S. Congressional Budget Office. TheEconomic and Budget Outlook: An Update.Washington, D.C., August, 1995.

U.S. Congressional Budget Office. TheEconomic and Budget Outlook: December 1995Update. Washington, D.C., December, 1995.

U.S. Congressional Budget Office. TheEconomic and Budget Outlook: Fiscal Years1997–2006. Washington, D.C., May, 1996.

U.S. Congressional Budget Office. TheEconomic and Budget Outlook: Fiscal Years1998–2007. Washington, D.C., January, 1997.

Williams, John. “Simple Rules for MonetaryPolicy.” Federal Reserve Board. Mimeo, 1997.

Related Documents