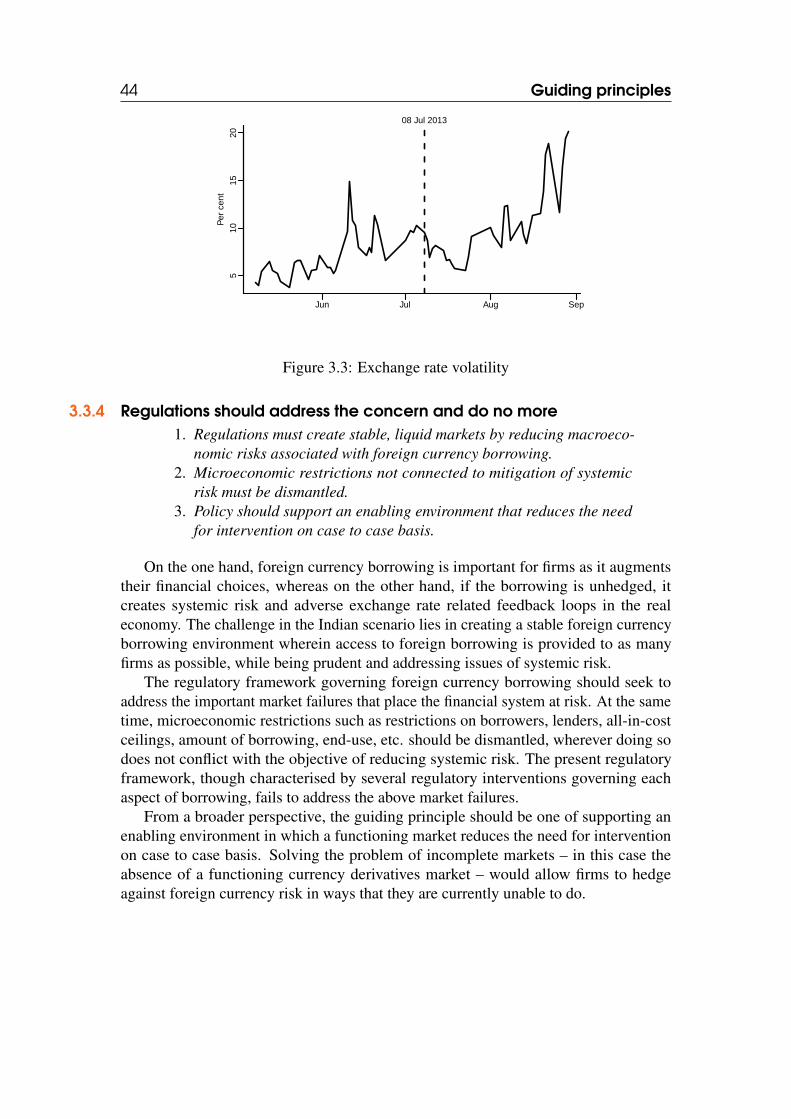

Report of the Committee to Review the Framework of Access to Domestic and Overseas Capital Markets (Phase II, Part II: Foreign Currency Borrowing) (Report III) Ministry of Finance Government of India February, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Report of the Committee to Review the Framework of Access to Domestic and Overseas Capital Markets

(Phase II, Part II: Foreign Currency Borrowing) (Report III)

Ministry of FinanceGovernment of India

February, 2015

Report of the Committee to Review the Framework of Access to Domestic and Overseas Capital Markets

(Phase II, Part II: Foreign Currency Borrowing) (Report III)

Ministry of FinanceGovernment of India

February, 2015

COMMITTEE TO REVIEW THE FRAMEWORK OFACCESS TO DOMESTIC ANDOVERSEAS CAPITAL MARKETS

New DelhiFebruary 24, 2015

Shri Arun JaitleyHon'ble Union Minister for Finance,Corporate Affairs, andInformation & BroadcastingGovernment of IndiaNew Delhi – 110 001

Dear Minister,

In continuation of its report in respect of Indian Depository Receipts submitted on June 9, 2014, theCommittee to review the framework of access to domestic and overseas capital markets, constitutedvide order F. No. 9/1/2013 – ECB dated January 1, 2014/January 10, 2014/February 5, 2014, herebypresents its report in respect of foreign currency borrowings to the Government of India.

Yours sincerely,

(M. S. Sahoo)Chairman

(S. Ravindran) (Ajay Shah)Member Member

(Manoj Joshi)Member

(Pratik Gupta)Member

(Sanjeev Kaushik)Member Convener

(Somasekhar Sundaresan)Member

Contents

Acronyms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

Acknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vii

1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1.1 Constitution of the Committee 3

1.2 Scope of work 4

1.3 Process followed 5

1.4 Structure of the report 5

2 Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

2.1 The extant legal framework 82.1.1 Evolution of the framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82.1.2 The extant framework for ECB . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92.1.3 The extant framework for hybrid instruments . . . . . . . . . . . . . . . . . . . . . 12

2.2 Description of outcomes 152.2.1 Dominant part of India’s external debt . . . . . . . . . . . . . . . . . . . . . . . . . . 152.2.2 Predominance of the automatic route . . . . . . . . . . . . . . . . . . . . . . . . . . 162.2.3 Increasing borrowing of longer maturity . . . . . . . . . . . . . . . . . . . . . . . . . 162.2.4 Dominance of non-resident foreign banks . . . . . . . . . . . . . . . . . . . . . . . 172.2.5 All-in-cost ceilings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.2.6 Expanding end-uses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.2.7 Broad pattern . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.3 Deficiencies in the extant arrangement 192.3.1 Complexity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 192.3.2 Prescriptive . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 202.3.3 Non-neutrality . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 222.3.4 Discretionary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 232.3.5 Currency mismatch . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 242.3.6 Deficiencies summed up . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

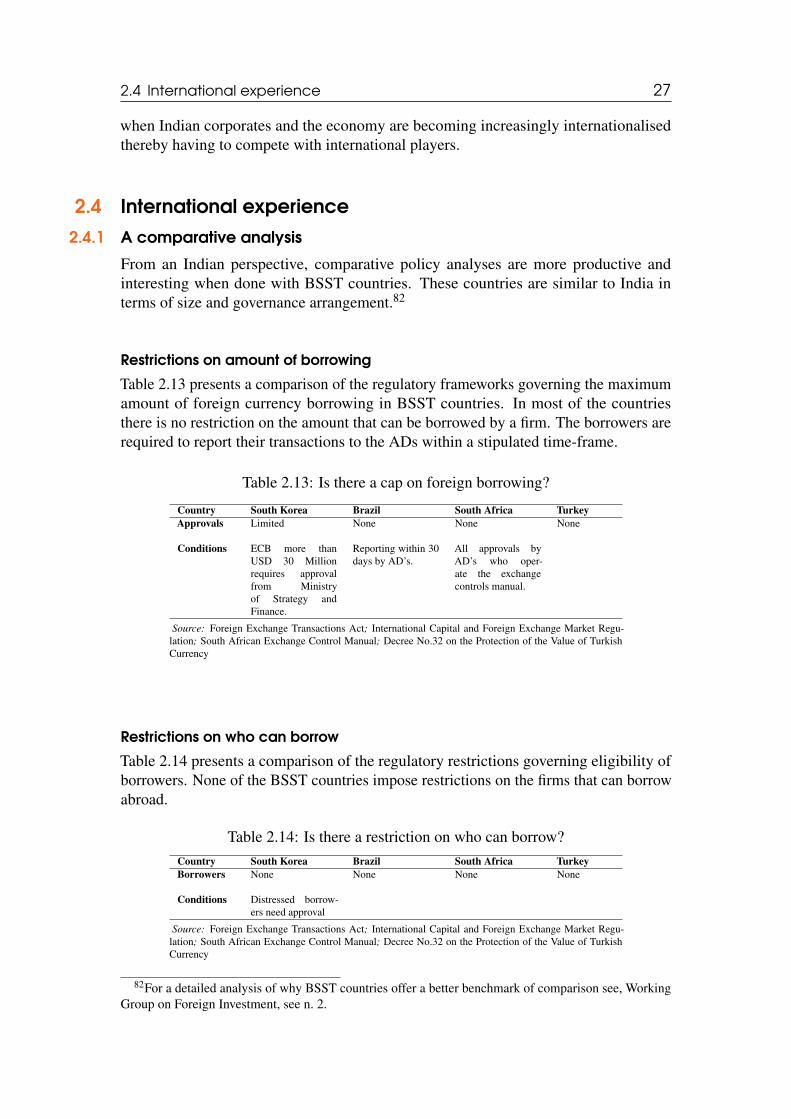

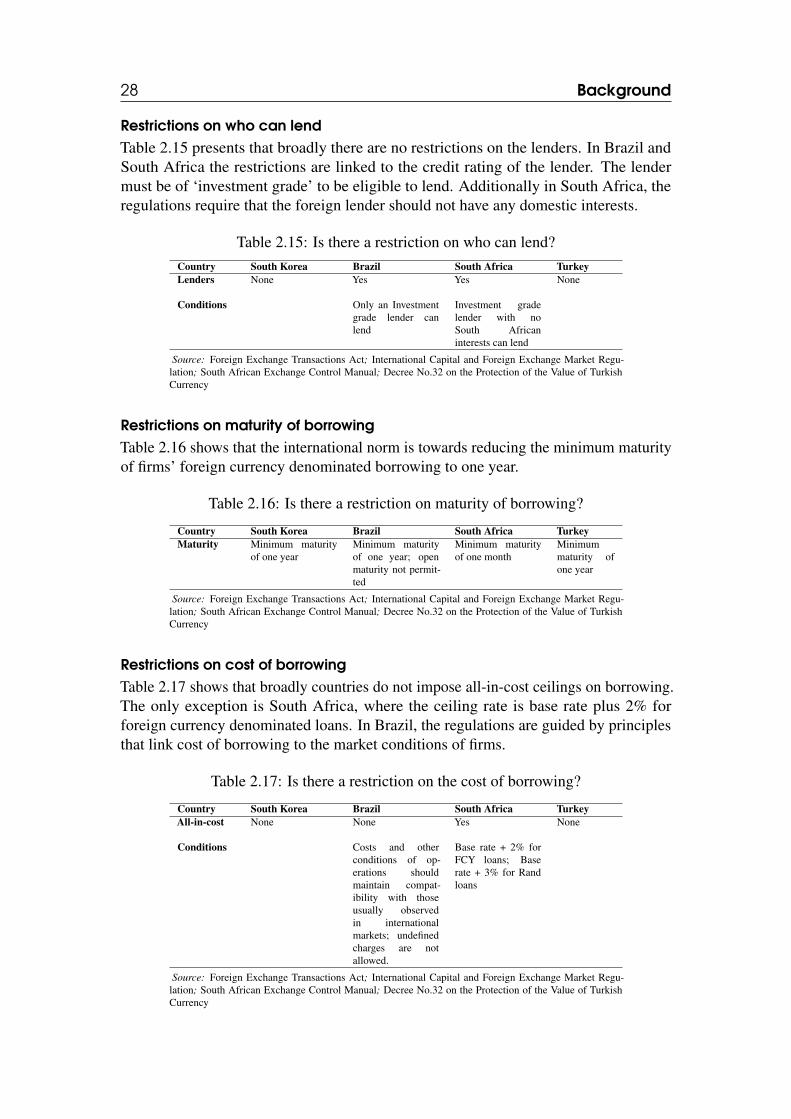

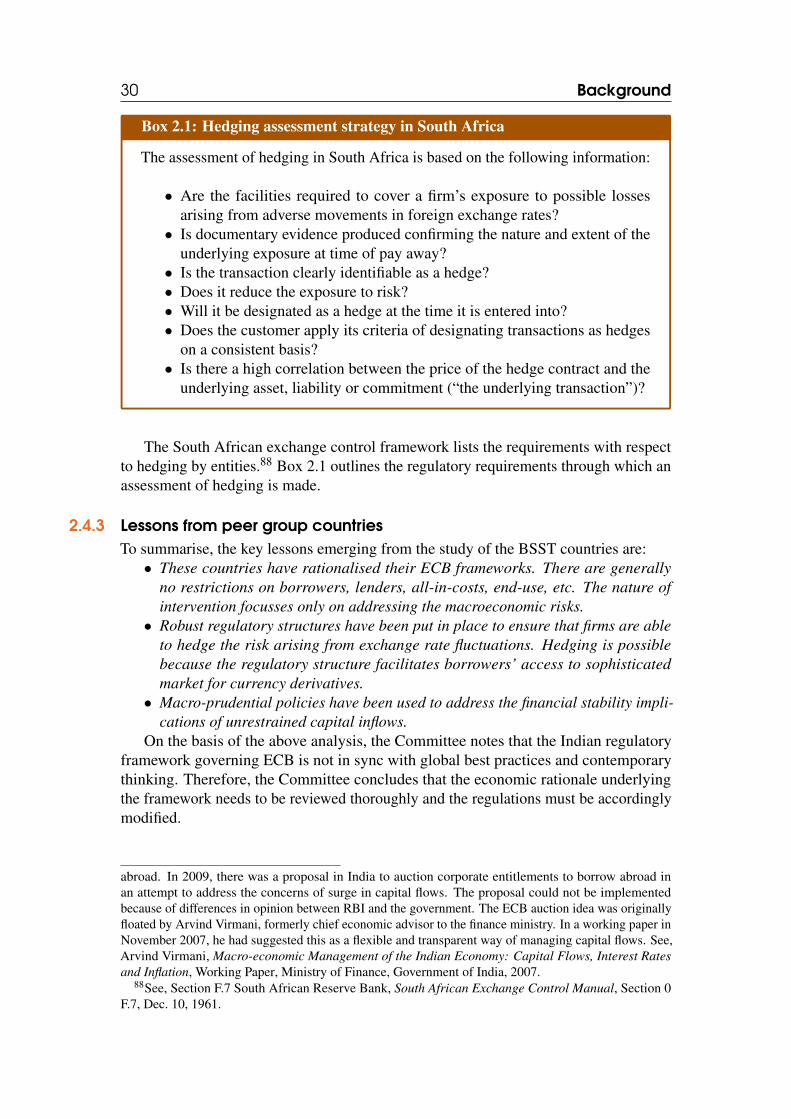

2.4 International experience 272.4.1 A comparative analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 272.4.2 Hedging facility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 292.4.3 Lessons from peer group countries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

3 Guiding principles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

3.1 Market failure 313.1.1 Sources and nature of currency exposure . . . . . . . . . . . . . . . . . . . . . . . 313.1.2 Is there a market failure? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 323.1.3 Experience with unhedged foreign currency exposure . . . . . . . . . . . . 33

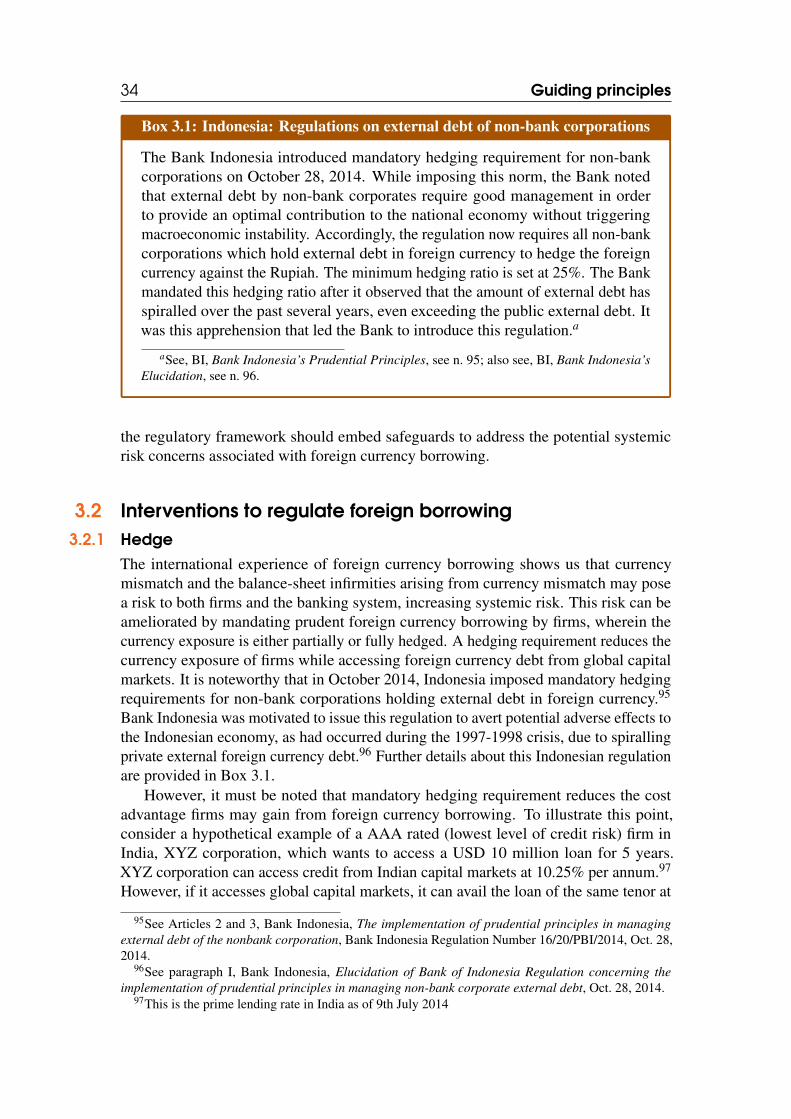

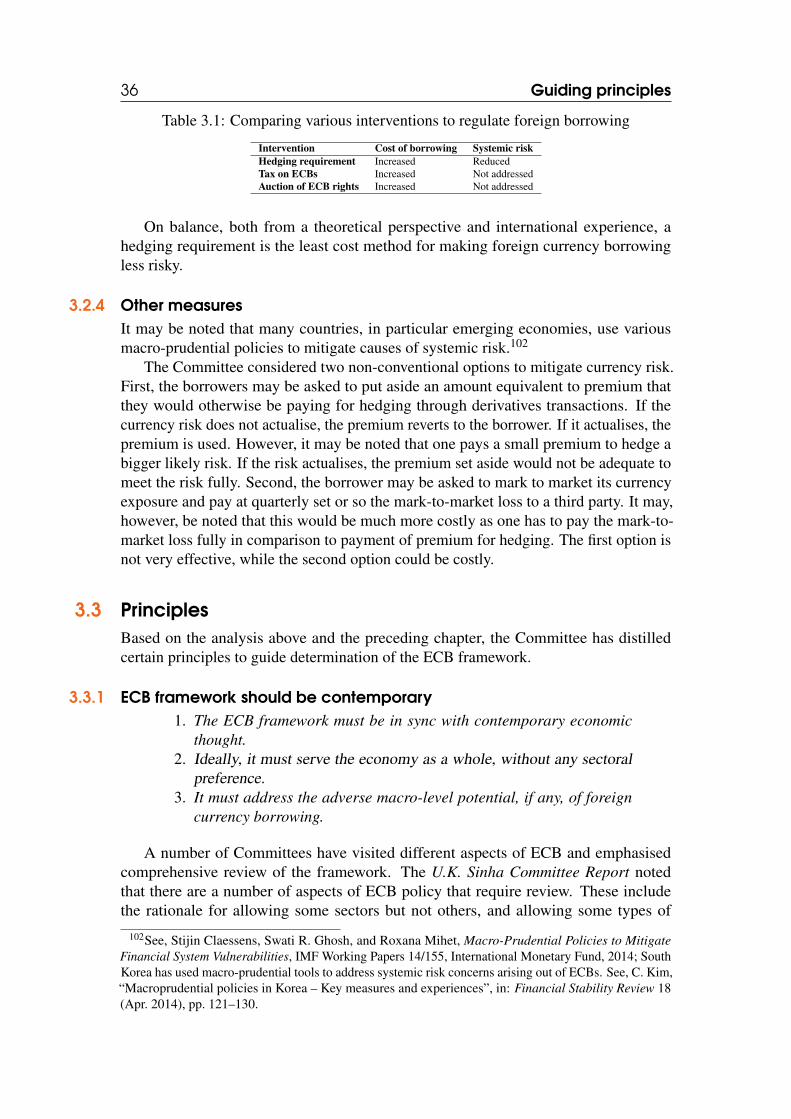

3.2 Interventions to regulate foreign borrowing 343.2.1 Hedge . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 343.2.2 Tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 353.2.3 Auction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 353.2.4 Other measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

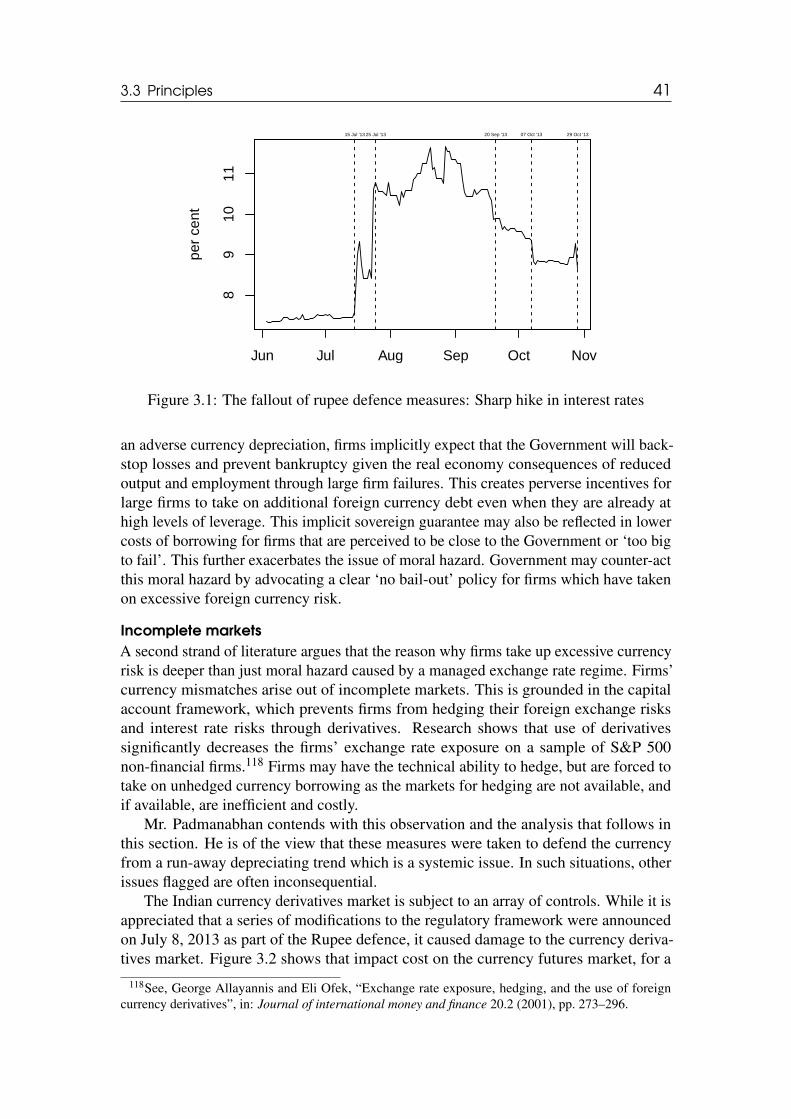

3.3 Principles 363.3.1 ECB framework should be contemporary . . . . . . . . . . . . . . . . . . . . . . . . 363.3.2 Regulations should address market failure . . . . . . . . . . . . . . . . . . . . . . . 373.3.3 Regulations should be informed by analysis of systemic risk . . . . . . . . 393.3.4 Regulations should address the concern and do no more . . . . . . . . . 44

4 Issues and responses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

4.1 What should be the objective of the ECB framework? 45

4.2 Who can borrow in foreign currency? 47

4.3 Who can lend in foreign currency? 48

4.4 Should the amount of ECB be regulated? 49

4.5 Should the maturity structure be regulated? 50

4.6 Should the cost of borrowing be regulated? 50

4.7 Should end-uses of ECB be regulated? 51

4.8 Should an ECB transaction require approval? 52

4.9 Should there be a special dispensation for PSUs? 52

4.10 Should there be a special dispensation for infrastructure? 53

4.11 How can systemic concerns arising from ECB be addressed? 54

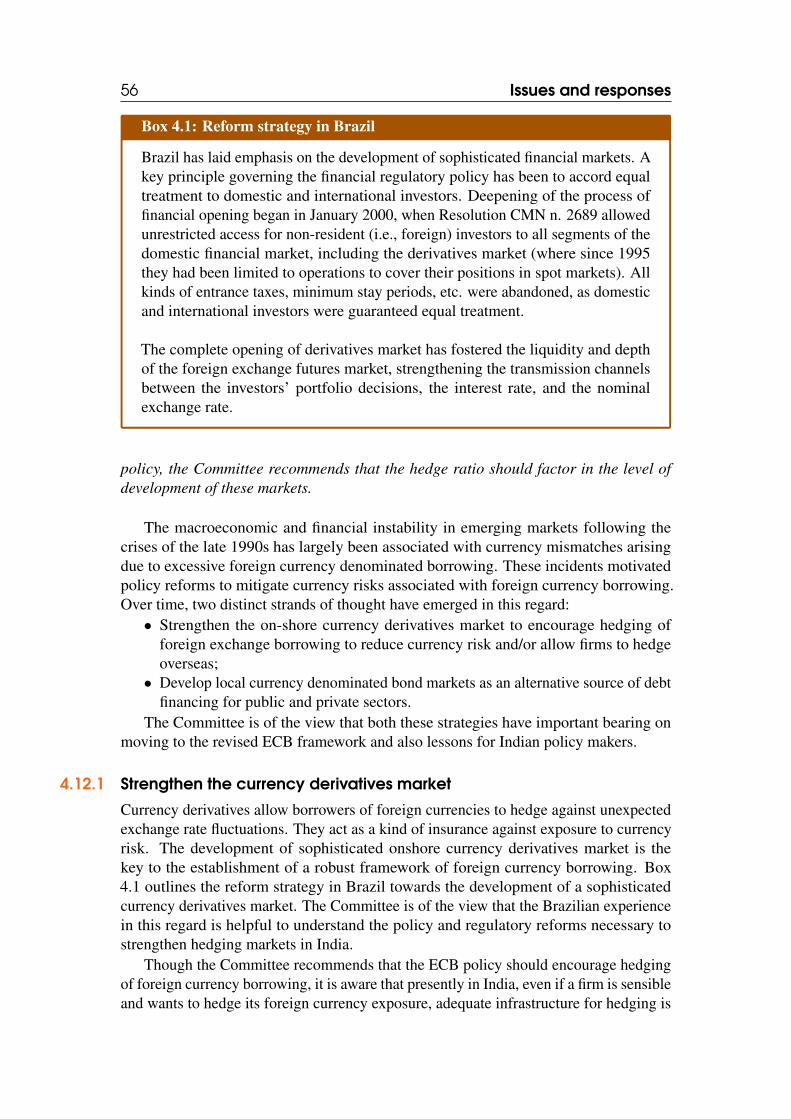

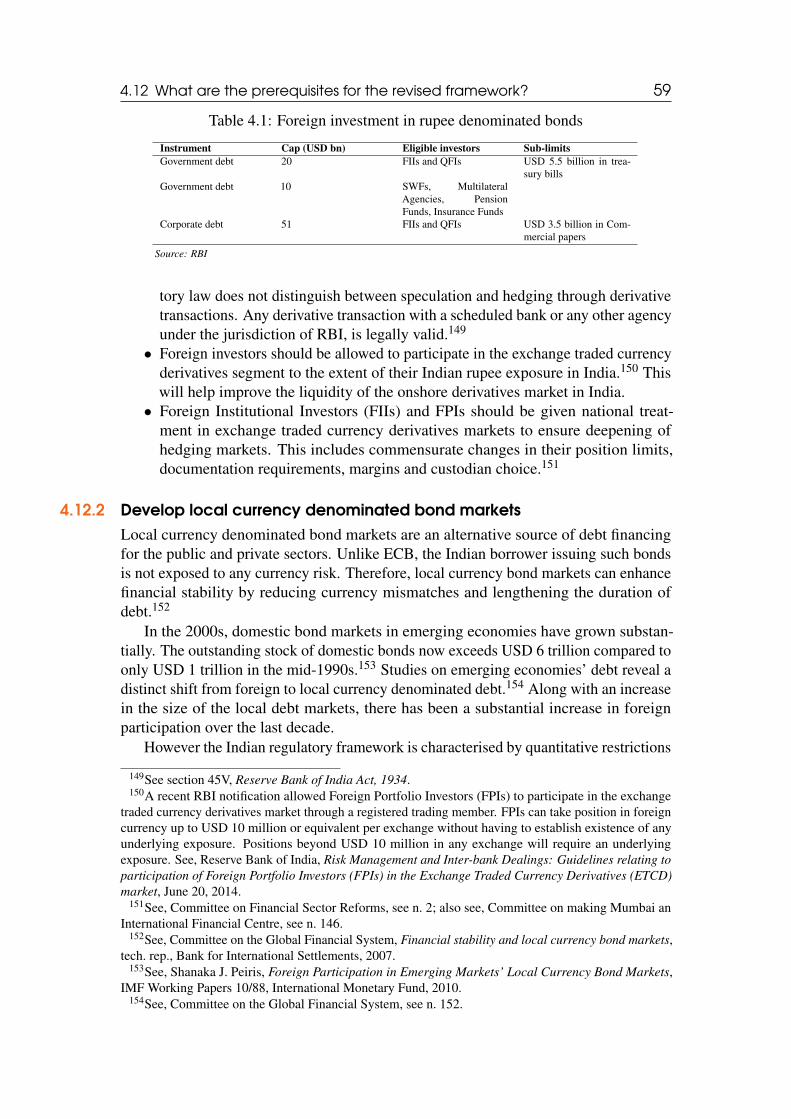

4.12 What are the prerequisites for the revised framework? 554.12.1 Strengthen the currency derivatives market . . . . . . . . . . . . . . . . . . . . . . 564.12.2 Develop local currency denominated bond markets . . . . . . . . . . . . . 59

4.13 Can the revised framework be implemented right away? 60

4.14 How to deal with FCCBs? 61

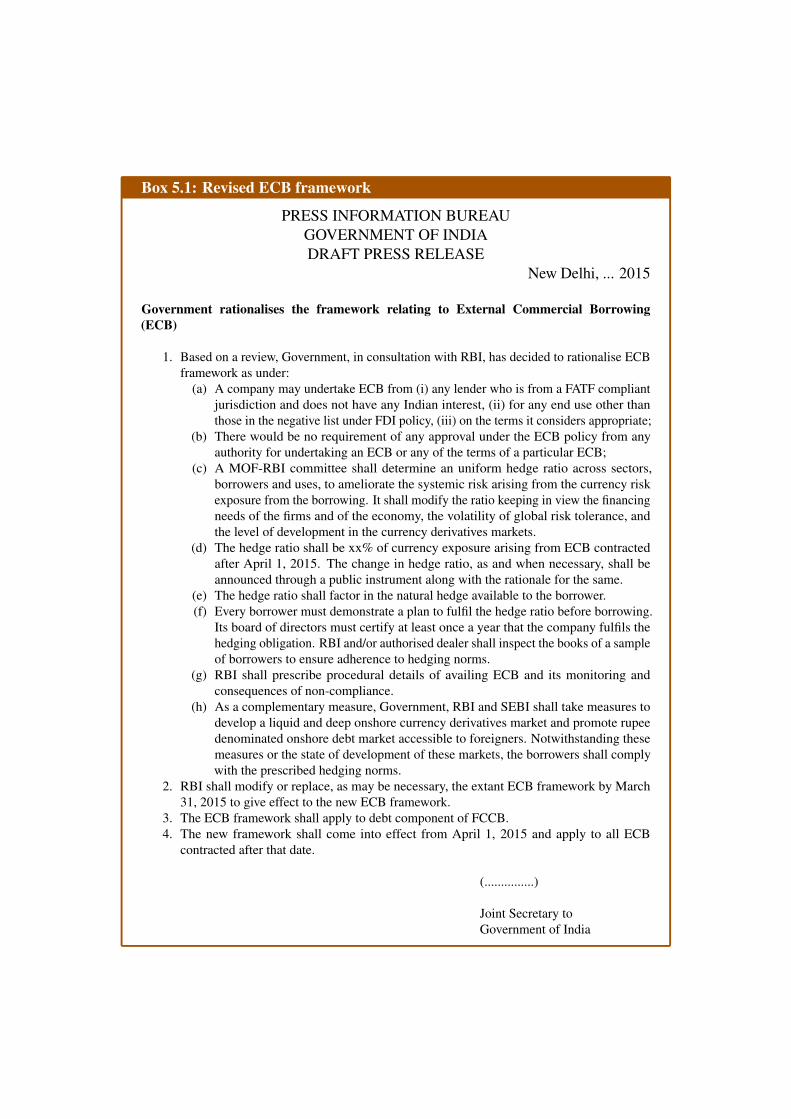

5 Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

5.1 Learning 65

5.2 Principles 66

5.3 Recommendations 67

Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Articles 71

Reports 72

Laws 74

Annexure-A1: Ministry of Finance order dated Septem-ber 23, 2013 constituting the Committee . . . . . . . . . . . . . 77

Annexure-A2: Ministry of Finance order dated January01, 2014 modifying the terms and the constitution of theCommittee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

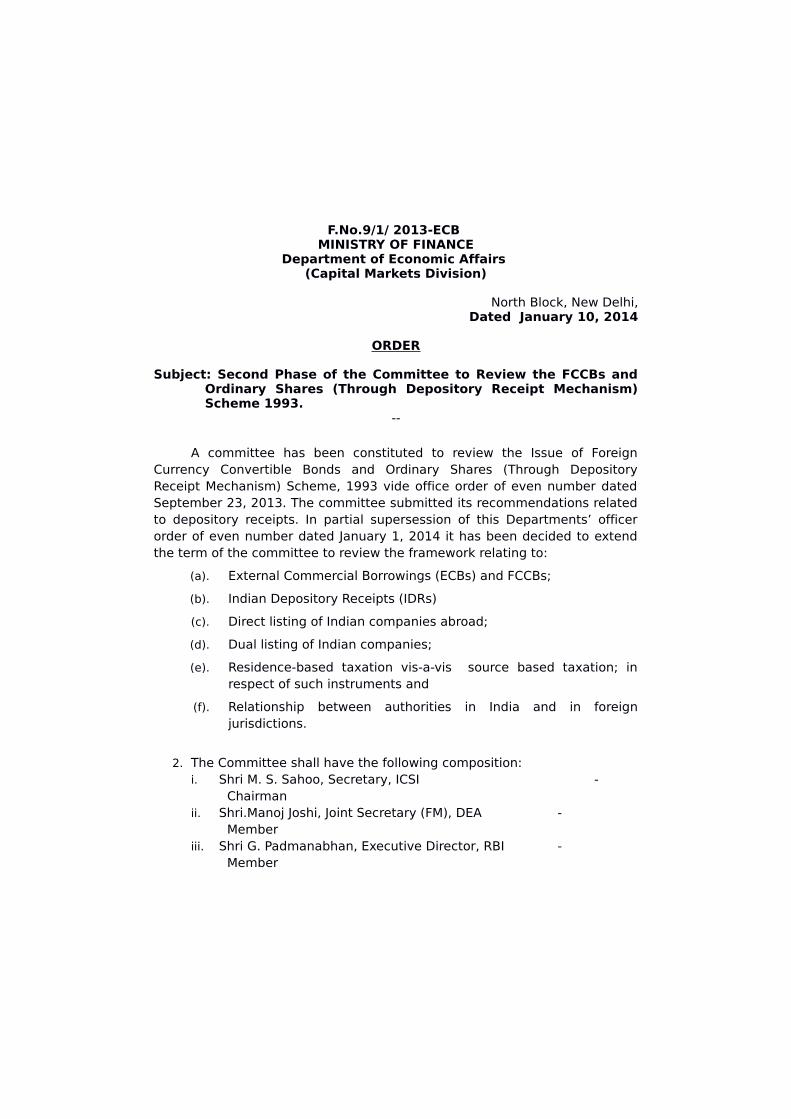

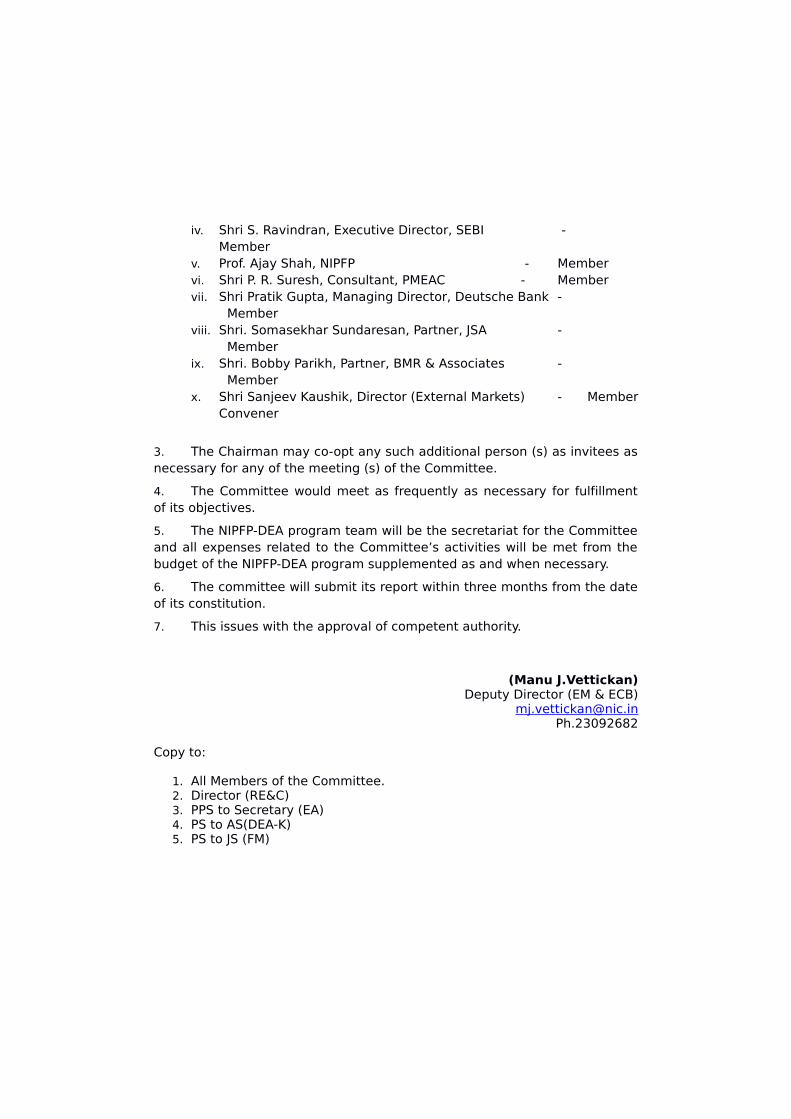

Annexure-A3: Ministry of Finance order dated January10, 2014 further modifying the earlier order . . . . . . . . . . 85

Annexure-A4: Ministry of Finance order dated February5, 2014 further modifying the earlier order . . . . . . . . . . . . 89

Annexure-B: List of stakeholders who engaged with theCommittee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

Acronyms

AD Authorised Dealer.ADB Asian Development Bank.ADR American Depository Receipt.AFC Asset Finance Company.

BhDR Bharat Depository Receipt.BSST countries Brazil, South Africa, South Korea, and Turkey.

CDC Commonwealth Development Corporation.CIC Core Investment Company.CMIE Centre for Monitoring Indian Economy Pvt. Ltd..CRR Cash Reserve Ratio.

DR Depository Receipt.

ECB External Commercial Borrowing.EME Emerging Market Economy.

FATF Financial Action Task Force.FCCB Foreign Currency Convertible Bond.FCEB Foreign Currency Exchangeable Bond.FDI Foreign Direct Investment.FEMA Foreign Exchange Management Act, 1999.FII Foreign Institutional Investor.FIPB Foreign Investment Promotion Board.FPI Foreign Portfolio Investor.FSLRC Financial Sector Legislative Reforms Commis-

sion.

GDP Gross Domestic Product.GDR Global Depository Receipt.

HFC Housing Finance Company.HLCECB High Level Committee on External Commercial

Borrowing.

ICSI Institute of Company Secretaries of India.IDR Indian Depository Receipt.IFC International Finance Corporation.IOF Financial Transactions Tax.IOSCO International Organization of Securities Commis-

sions.

LAF Liquidity Adjustment Facility.LIBOR London Interbank Offered Rate.LRN Loan Registration Number.

MFI Micro Finance Institution.MOF Ministry of Finance.MSF Marginal Standing Facility.MSME Micro Small and Medium Enterprise.

NBFC Non Banking Financial Company.NDF Non-Deliverable Forward.NDTL Net Demand and Time Liability.NGO Non Government Organization.NIPFP National Institute of Public Finance and Policy.

OTC Over The Counter.

PMEAC Economic Advisory Council to the Prime Minis-ter.

PSU Public Sector Undertaking.

QFI Qualified Foreign Investor.

RBI Reserve Bank of India.

SAT Securities Appellate Tribunal.SEBI Securities and Exchange Board of India.SEZ Special Economic Zone.SIDBI Small Industries Development Bank of India.SPV Special Purpose Vehicle.

Acknowledgements

Foreign currency borrowing, popularly known as External Commercial Borrowing(ECB), refers to commercial loans in foreign currency availed by persons resident inIndia from non-resident lenders. The Foreign Exchange Management Act, 1999 (FEMA)governs all transactions in foreign currency, including lending and borrowing in foreigncurrency. Government, at the advice of a High Level Committee on External Com-mercial Borrowing (HLCECB) formulates and reviews the ECB policy in consultationwith Reserve Bank of India (RBI) and announces the same through press releases orguidelines. While formulating or reviewing the policy, Government takes into accountthe macro-economic situation, the requirements of the corporate sector, the need tosupport certain end-uses, the state of external financial markets, the challenges facedin external sector management, and the experience gained so far in the administrationof the ECB policy and endeavours to provide flexibility in borrowing within prudentlimits. The policy so evolved is notified and administered by RBI through regulationsand circulars under FEMA.

Government has been liberalising the ECB policy from time to time to enable Indianfirms greater access to international capital markets. For example, it amended the policyin January 2005, June 2005, and January 2006 respectively to allow qualified NonGovernment Organizations (NGOs), Non Banking Financial Companies (NBFCs) andmulti-State co-operative societies to access ECB. It expanded the ambit of ‘infrastruc-ture’, which is a permissible end-use, in 2008 to include mining, exploration and refining,and in 2013 to include energy, communication, transport, water and sanitation, miningand social and commercial infrastructure.1 Similarly, Government has been streamliningthe procedure. It reduced layers of approval such as in-principle approval and taking onrecord of loan agreement from Government and FERA/FEMA approval and permissionto draw down from RBI. It delegated sanctioning authority to RBI over time while

1See, Reserve Bank of India, External Commercial Borrowings Policy - Liberalisation, RBI/2008-09/210 A.P. (DIR Series) Circular No. 20, Oct. 8, 2008; also see, Reserve Bank of India, ExternalCommercial Borrowings (ECB) Policy – Liberalisation of definition of Infrastructure Sector, RBI/2013-14/270 A.P. (DIR Series) Circular No. 48, Sept. 18, 2013.

vi

creating an automatic route under which a borrower can access ECB without requiringany approval from any authority. Generally, ECB allowed for a sector/end-use for thefirst time is kept under approval route for a while before being shifted to the automaticroute.

The ECB framework has been a product of its time. The basic structure remains thesame even though it is being refined continuously. In the meantime, Indian financialmarkets, and the legal and regulatory framework relating to financial markets andcorporate sector have become modern and contemporary. The policy stance towards theeconomy and capital flows has changed. A number of committees have brought in newthought and approach to regulation and design of financial markets. These developmentswarrant a fresh, comprehensive look at the framework of foreign currency borrowingto bring it in sync with the rest of the ecosystem. Many thought leaders have rightlyunderlined the need for a comprehensive review.2 The Committee thanks the Ministryof Finance (MOF) for providing an opportunity to do so.

I am grateful to each member of the Committee for putting in long hours of workand making significant contribution to the deliberation and drafting of this report:

1. Mr. G. Padmanabhan, Executive Director, RBI;2. Mr. S. Ravindran, Executive Director, Securities and Exchange Board of India

(SEBI);3. Dr. Ajay Shah, Professor, National Institute of Public Finance and Policy (NIPFP);4. Mr. P. R. Suresh, then Consultant, Economic Advisory Council to the Prime

Minister (PMEAC);5. Mr. Sunil Gupta, then Joint Secretary, Department of Revenue, MOF;6. Mr. Manoj Joshi, Joint Secretary, Department of Economic Affairs, MOF;7. Mr. Somasekhar Sundaresan, Partner, JSA;8. Mr. Pratik Gupta, Managing Director, Deutsche Bank;9. Mr. Bobby Parikh, Partner, BMR & Associates; and

10. Mr. Sanjeev Kaushik, then Director, Department of Economic Affairs, MOF.I am extremely grateful to Dr. Ila Patnaik, Principal Economic Adviser, Ministry of

Finance (then Professor, NIPFP) for supporting the Committee as a special invitee interms of research analysis and thought leadership.

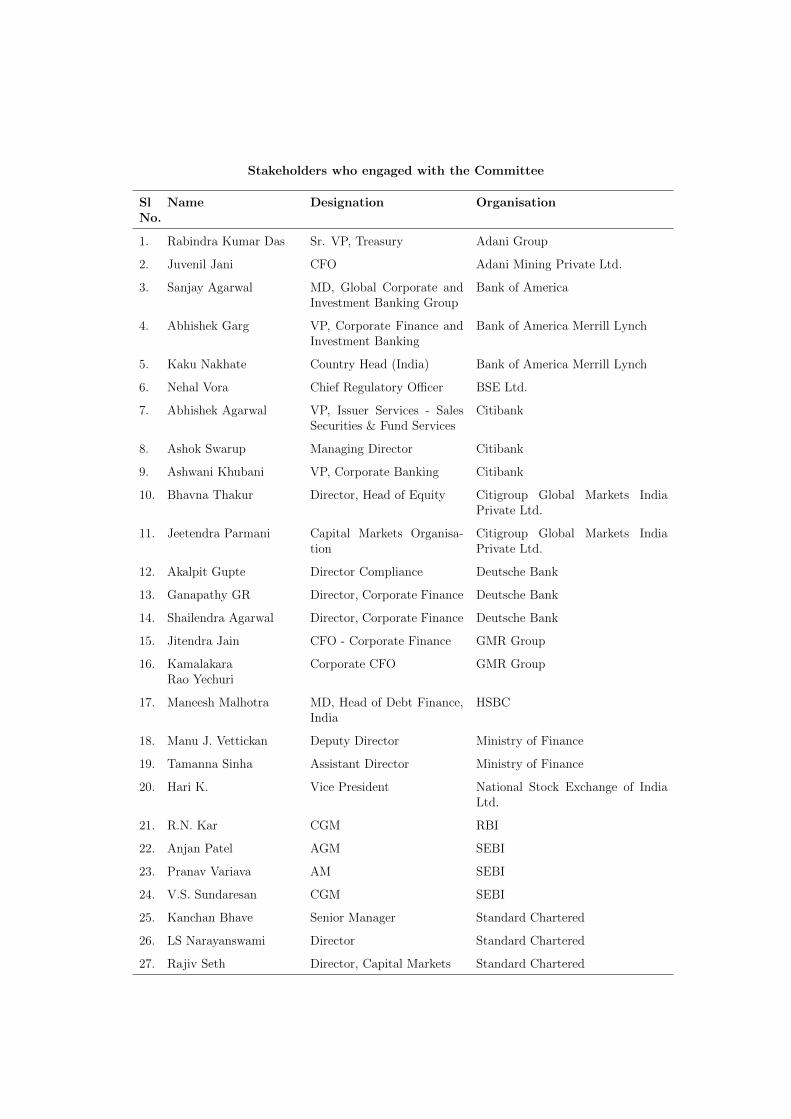

I am thankful to Mr. Rabindra Kumar Das of Adani Group; Mr. Juvenil Jani ofAdani Mining Private Ltd.; Mr. Sanjay Agarwal of Bank of America; Mr. AbhishekGarg and Ms. Kaku Nakhate of Bank of America Merrill Lynch; Mr. Abhishek Agarwal,Mr. Ashok Swarup and Mr. Ashwani Khubani of Citibank; Ms. Bhavna Thakur and Mr.Jeetendra Parmani of Citigroup Global Markets India Private Ltd.; Mr. Akalpit Gupte,Mr. Ganapathy GR and Mr. Shailendra Agarwal of Deutsche Bank; Mr. Jitendra Jainand Mr. Kamalakara Rao Yechuri of GMR Group; Mr. Maneesh Malhotra of HSBC;Mr. Nehal Vora of BSE Ltd.; Mr. Hari K. of National Stock Exchange of India Ltd.; Ms.Kanchan Bhave, Mr. LS Narayanswami and Mr. Rajiv Seth of Standard Chartered; Mr.

2See, Committee on Fuller Capital Account Convertibility, Report of the Committee on Fuller CapitalAccount Convertibility, tech. rep., Reserve Bank of India, 2006; Working Group on Foreign Investment,Report of the Working Group on Foreign Investment, tech. rep., Department of Economic Affairs, Ministryof Finance, July 30, 2010; Committee on Financial Sector Reforms, A Hundred Small Steps, Report ofthe Committee on Financial Sector Reforms, tech. rep., Planning Commission of India, Sept. 12, 2008;and G. Padmanabhan, Administering FEMA - Evolving Challenges, tech. rep., Inaugural address at theAuthorised Dealers’ Conference at Agra on November 30, 2013, 2013.

vii

Manu J. Vettickan and Ms. Tamanna Sinha of the Ministry of Finance; Mr. R. N. Karof RBI; and Mr. Anjan Patel, Mr. Pranav Variava and Mr. V. S. Sundaresan of SEBI,for engaging with the Committee and sharing their experiences, concerns, thoughts andperspectives.

The Secretariat for the Committee, the NIPFP Macro/Finance Group, deliveredoutstanding research support as it has been doing for numerous other Governmentprojects. Mr. Pratik Datta, the leader of this team, put in tireless efforts to prepare thefirst draft of the report and brought in significant insights into the issues. Dr. RadhikaPandey and Mr. Shekhar Harikumar of the team brought on the table their perspectiveson the complex issues for consideration of the Committee and provided research support.Mr. Mehtab Hans, Ms. Sanhita Sapatnekar and Ms. Apoorva Gupta assisted in reviewingthe report. Ms. Neena Jacob of NIPFP managed the process smoothly and flawlessly.

I acknowledge the support from SEBI and NIPFP for making their facilities availableto the Committee for holding extensive meetings and extending warm hospitality.

February 24, 2015 M. S. Sahoo

Executive Summary

Firms seek the lowest possible cost of capital for financing projects. When capital isavailable at lower cost, a larger set of projects become financially viable, and greaterinvestment takes place. The policy should, therefore, aim at making capital available tofirms at the lowest possible cost. Just as trade reforms has given Indian firms the abilityto buy the cheapest goods available globally, financial reforms should give Indian firmsthe ability to obtain the cheapest capital available on a global scale.

Every firm takes on various risks in the course of its business activities, and some ofthese risks generate losses. Idiosyncratic losses by some firms, and consequent failureof some firms, are of no concern to policy makers. However, when a firm undertakesforeign currency borrowing, its balance sheet is exposed to exchange rate fluctuations. Ifnumerous firms, who undertake foreign currency borrowing, do not hedge their currencyexposure, there is a possibility of correlated failure of these firms if there is a largeexchange rate movement. The negative impact of this movement on their balance sheetscould then hamper investment and the country’s Gross Domestic Product. This imposesnegative externalities upon the citizenry which constitutes a market failure.

The firms that borrow in foreign currency may not hedge their risks from currencyexposure fully or may even undertake excessive borrowing / risks. They do it generallyfor two main reasons. First, the firms may not be able to hedge their currency exposurebecause the onshore derivatives market is shallow and illiquid, and the firms do not haveaccess to the overseas derivatives market. Second, a managed / pegged exchange rategives an implicit guarantee that there would not be large fluctuations in exchange rates.This emboldens many firms to borrow more and to leave their foreign currency exposureunhedged. They free ride on the costs paid by the economy at large in pursuit of managedexchange rate policy. The Committee notes that this carries two kinds of problems,namely, (a) the problem of political economy, where the firms lobby in favour ofperpetuation of low volatility of the exchange rate; and (b) when the inevitable exchangerate adjustment ultimately takes place, many firms may suffer losses simultaneously.

The Committee notes that the extant ECB policy requires hedging for certain cate-gories of borrowing. It is of the firm view that the possibility of market failure arising

1

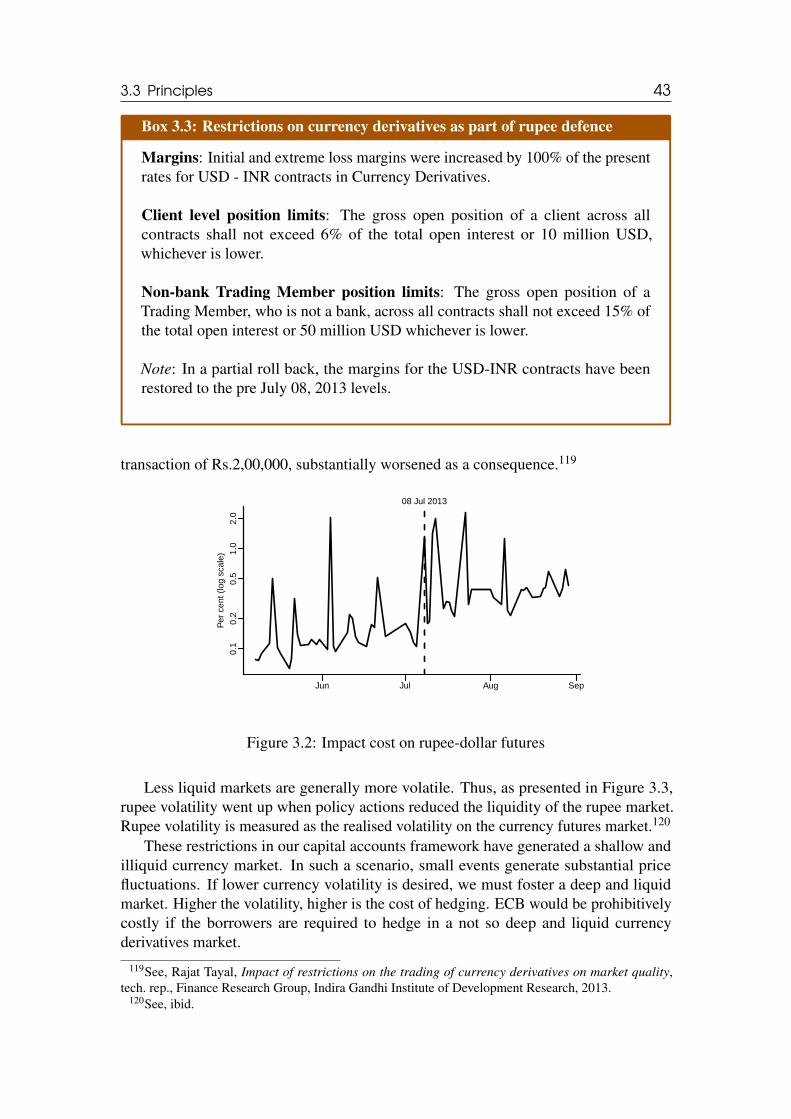

from ECB can be ameliorated by building on the existing strategy, that is, requiringfirms borrowing in foreign currency to hedge their exchange risk exposure. There canbe two kinds of hedges: natural hedges or hedging using financial derivatives. Naturalhedges arise when firms sell more tradeables than they consume. This generates thenet economic exposure of an exporter. The firms may use financial derivatives such ascurrency futures, currency options, etc. to hedge their currency exposure. The mainrecommendation of this report is that Indian firms should be able to borrow abroad,through foreign currency debt, while being subject to a capital control, which requiresthem to substantially hedge their foreign currency exposure, whether through financialderivatives or natural hedges.

The Committee is conscious of the fact that hedging involves cost and given thestate of the onshore currency derivatives market, the cost of hedging may make foreigncurrency debt unattractive. The Committee, therefore, recommends that measures betaken to develop a liquid and deep onshore derivatives market. Keeping the availability ofeffective facility for borrowers to hedge their currency exposures onshore, and financialneeds of the firms and of the economy, the authorities should specify and modify thehedge ratio (percentage of currency exposure to be hedged). However, they must ensurethat this ratio is uniform across sectors or borrowers.

There is a systemic concern arising from volatility in global risk tolerance which maycreate huge fluctuations in ECB flows unrelated to fundamentals. This concern requiresmeasures to moderate ECB flows. The second recommendation of the Committee,therefore, is that the authorities may modify the required hedge ratio in response tochanges in global conditions, whenever required.

At present, there is an array of other interventions into the process of foreign currencyborrowing. Most of these interventions were brought in to meet the specific needs of thehour and have outlived their utility. None of them seems to be addressing any identifiedmarket failure today. The Committee, therefore, recommends a complete removal ofthese interventions. It does not recommend interventions in the form of taxation orauction as advocated by some experts as these could reduce the volume of transactionsbut not address the identified market failure.

Mr. G. Padmanabhan and Mr. S. Ravindran, members of the Committee do not fullyconcur with some of the recommendations and observations in the report. These havebeen recorded in the relevant paragraphs in the report.

This is the third report (Report III) written by this Committee, the previous two beingon American Depository Receipt (ADR)/Global Depository Receipt (GDR) issuance(Report I) and on Indian Depository Receipt (IDR)/Bharat Depository Receipt (BhDR)issuance (Report II). The first of these reports has been substantially implementedthrough the new Depository Receipts Scheme, 2014. The union budget for 2014-15 hasproposed to completely revamp the IDR and introduce a much more liberal and ambitiousBhDR, which has been the recommendation of the second report. In all the three reports,the consistent intellectual strategy has been to identify market failures, if any, and addressthem, and to remove all other aspects of capital controls or administrative overhead. Thisyields a substantial reduction in the cost of doing business in India and improves India’sengagement with financial globalisation. The resulting frameworks are conceptuallyclear, involve reduced legal risk and reduce the need for private firms to interact with theauthorities and thereby improve the ease of doing business.

1 — Introduction

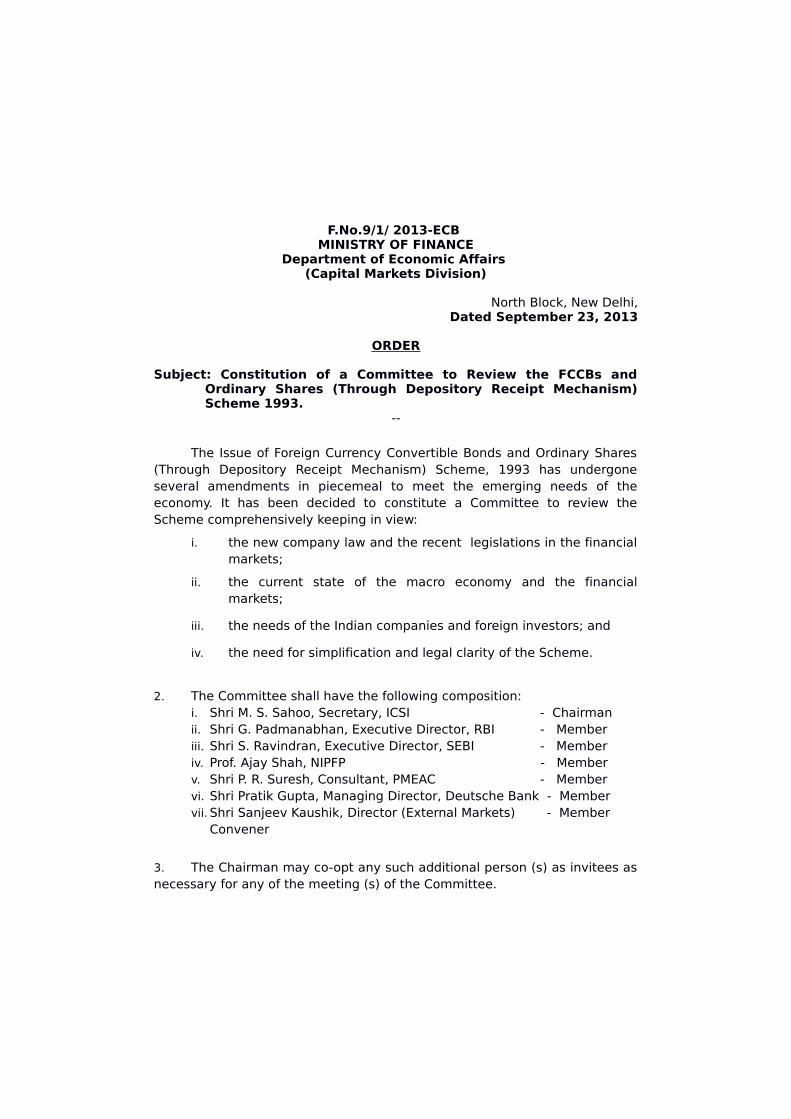

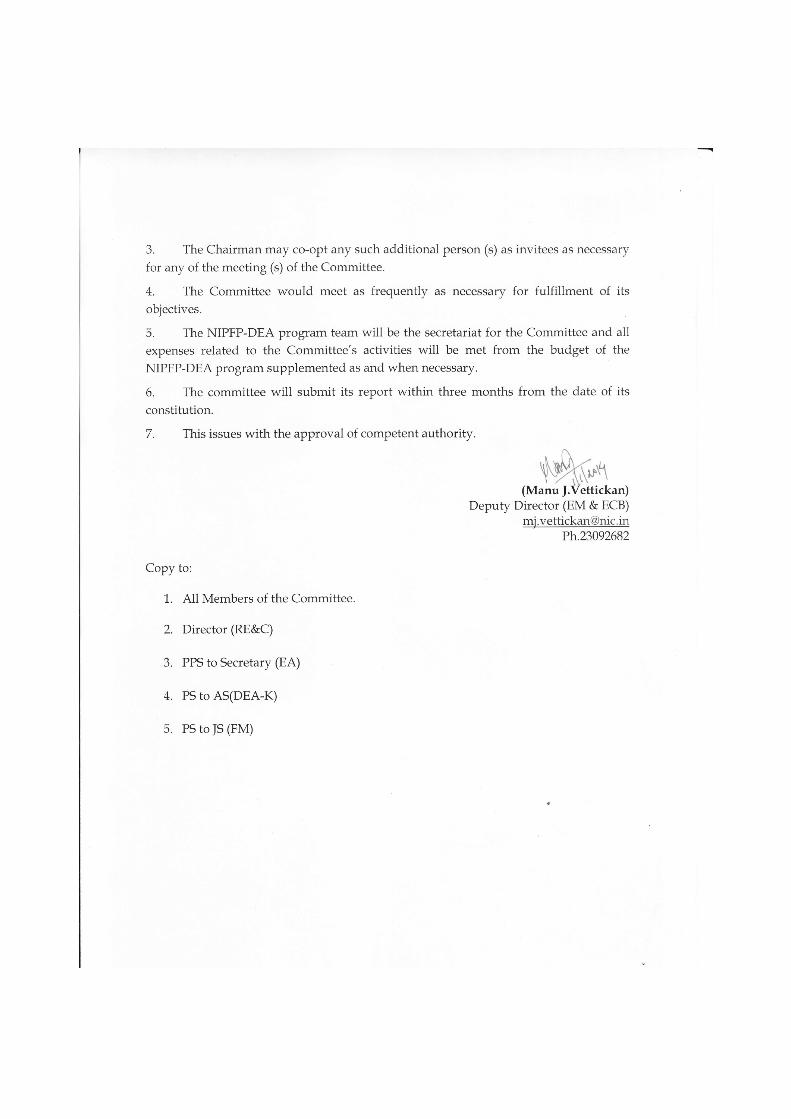

1.1 Constitution of the CommitteeMOF constituted a Committee, vide its Office Order dated September 23, 2013 (Annexure-A1), to comprehensively review the Foreign Currency Convertible Bonds and OrdinaryShares (Through Deposit Receipt Mechanism) Scheme, 1993. Accordingly, on Novem-ber 26, 2013, the Committee submitted to the MOF its report on Depository Receipts(DRs) along with a draft scheme in replacement of the extant scheme.3 This report ishereinafter referred to as the Report I. The draft scheme (except the portion relating totax) has been notified by MOF through a notification dated October 21, 2014.4 RBI hasalso amended FEMA 20 and inserted Schedule 10, pursuant to the recommendations ofthe Committee.5

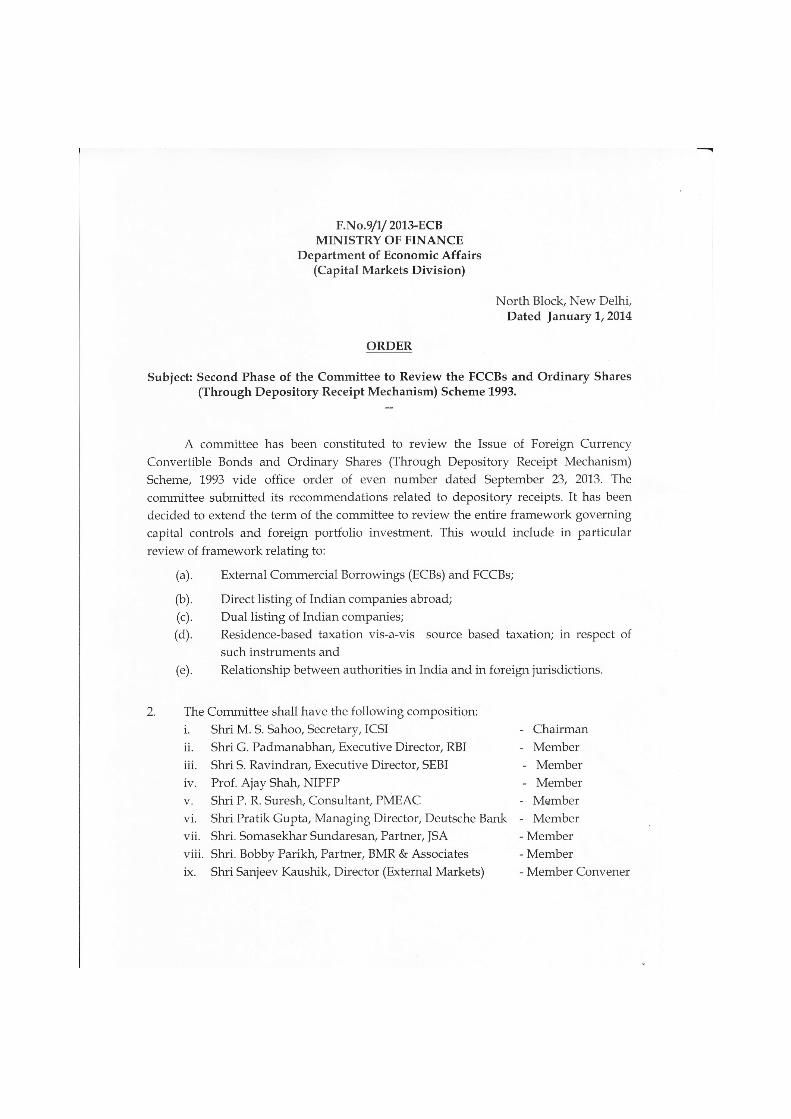

Subsequently, vide Office Orders dated January 1, 2014 (Annexure-A2), January 10,2014 (Annexure-A3) and February 5, 2014 (Annexure-A4), the MOF reconstituted theCommittee as under:

1. Mr. M. S. Sahoo, then Secretary, Institute of Company Secretaries of India (ICSI);2. Mr. G. Padmanabhan, Executive Director, RBI;3. Mr. S. Ravindran, Executive Director, SEBI;4. Dr. Ajay Shah, Professor, NIPFP;5. Mr. P. R. Suresh, then Consultant, PMEAC;6. Mr. Sunil Gupta, then Joint Secretary, Department of Revenue, MOF (since left

Government and did not participate in the process after some time);7. Mr. Manoj Joshi, Joint Secretary, Department of Economic Affairs, MOF;8. Mr. Somasekhar Sundaresan, Partner, JSA;

3See, Ministry of Finance, Report of the committee to review the FCCBs and Ordinary Shares (ThroughDepository Receipt Mechanism) Scheme, 1993, tech. rep., Ministry of Finance, Nov. 26, 2013.

4See, Department of Economic Affairs, Ministry of Finance, Depository Receipts Scheme, 2014,Oct. 21, 2014.

5See, Reserve Bank of India, Foreign Exchange Management (Transfer or issue of security by aperson resident outside India) (Seventeenth Amendment) Regulations, 2014, Notification No. FEMA330/2014-RB dated, Dec. 15, 2014.

4 Introduction

9. Mr. Pratik Gupta, Managing Director, Deutsche Bank;10. Mr. Bobby Parikh, Partner, BMR & Associates; and11. Mr. Sanjeev Kaushik, then Director, Department of Economic Affairs, MOF.

These orders mandate the Committee to review the entire framework of access todomestic and overseas capital markets and related aspects. These include the frameworksrelating to:

• Indian depository receipts (IDRs);• ECB and Foreign Currency Convertible Bonds (FCCBs);• Direct listing of Indian companies abroad;• Dual listing of Indian companies;• Residence-based taxation vis-a-vis source based taxation; and• Relationship between authorities in India and those in foreign jurisdictions.Pursuant to the above, the Committee undertook a review of the framework relating

to IDRs and submitted its report on the same along with the draft BhDR Guidelines tothe MOF on June 9, 2014.6 This report is hereinafter referred to as the Report II. Thisreport has been released by Government seeking comments from the public.7 On July10, 2014, the Finance Minister in his budget speech has proposed that Government will‘completely revamp the IDR and introduce a much more liberal and ambitious BhDR’.8

In continuation of the above, the Committee worked on ECB, which is the subjectmatter of this report. This report is hereinafter referred to as Report III.

1.2 Scope of workThe Committee has a very wide ranging terms of reference. While deliberating on these,its strategy has been to refocus the interventions of the State upon addressing marketfailures. This implies removing existing interventions that cannot be justified in terms ofmarket failures. The second element of the strategy has been the reinforcement of ruleof law into the working of capital controls in India.

The 1993 Scheme was one of the early moves to open up the Indian capital account.It allowed Indian issuers to raise capital from international capital markets through theDR route. The early motivation was to give foreign investors a mechanism to connectwith Indian companies without dealing with the problems of the Indian equity market.The reforms since 1993 have yielded a world class equities market in India. This changedthe purpose of DRs, from addressing the weaknesses of the domestic equity market toalleviating home bias faced by most Indian firms. The Report I brought in contemporarythinking in financial economic policy in India into this field. The Committee drafted anew scheme for DRs to replace the 1993 Scheme.9

Just as DR issuance connects foreign investors to Indian companies, IDR issuanceconnects foreign companies to Indian investors. While IDRs found place in the statute in2000, the development of the enabling framework took quite some time. Till date only

6See, Ministry of Finance, Report of the committee to review the framework of access to domestic andoverseas capital markets, tech. rep., Ministry of Finance, June 9, 2014.

7See, Press Information Bureau, Report of the Committee to Review the Framework of Access toDomestic and Overseas Capital Markets (Phase II, Part I: Indian Depository Receipts).

8See, Ministry of Finance, Budget Speech by Hon’ble Finance Minister, tech. rep., July 10, 2014.9This scheme was notified by the Ministry of Finance on October 21, 2014, with necessary modifica-

tions. See, DEA, Depository Receipts Scheme, 2014, see n. 4.

1.3 Process followed 5

one IDR issue has taken place. The Report II also brought in contemporary thinkingin financial economic policy in India into this field. The Committee recommendedstreamlining various regulations to address potential market failures in the IDR market.Along with the report, the Committee also submitted draft guidelines to assist theconcerned regulators in drafting the requisite regulations.

The third element of the work is in foreign currency borrowing by Indian firms,which is the subject of the instant report (Report III). The analysis of this report replicatesthe strategy of the previous two elements: bringing in contemporary thinking in financialeconomic policy in India to the question, which involves refocusing State interventionsupon market failures, reducing administrative overhead by removing interventions whichare not grounded in addressing market failures, and reinforcing the rule of law.

1.3 Process followedThe Committee had four meetings devoted to deliberations on ECB. During thesemeetings it consulted the stakeholders concerned, and delineated the relevant policyissues and deliberated extensively on the same. The deliberations of the Committee wereinformed by the research conducted by its secretariat, the NIPFP Macro/Finance Group.The research was based on relevant data collected by the NIPFP Macro/Finance Groupfrom various sources, including some of the stakeholders and RBI, and contemporarythought as reflected in recent policy decisions and committee reports. The list ofstakeholders who engaged with the Committee is at Annexure-B.

1.4 Structure of the reportThe report is structured as follows. Chapter 2 describes the design, outcome and defi-ciencies of the extant ECB framework. It also compares the extant ECB framework withthat of some of the peer countries to focus on the specific regulatory areas that need tobe redesigned. Chapter 3 attempts to understand market failures in the context of foreigncurrency borrowing and the interventions necessary to address the same. It distills thepolicy reforms strategies for foreign currency borrowing as articulated by previous expertcommittees, the economic rationale for regulating such activities and the principles thatmust guide the recommendations of the Committee in rationalising the regulations onECB. Chapter 4 focuses on the policy issues relevant to ECB and analyses them indepth, keeping in view the principles of economics, law and regulations enunciated inearlier chapters. Chapter 5 summarises the principles guiding the recommendations ofthe Committee and its recommendations based on the same.

2 — Background

Capital is a key input that shapes the competitiveness of firms. To be a low cost producerof steel in India, it is important to match the cost of capital obtained by the top steelcompanies of the world. Just as Indian steel companies have the choice of buying coal,iron ore or capital goods at the lowest cost, they must also have the choice of raisingcapital - debt or equity - abroad on competitive terms.

Firms have the option of raising capital in the form of equity or debt, locally orglobally, in domestic or foreign currency. There are limits on each mode of raisingcapital and there are reasons to prefer one option over another. For example, given thelevel of development of the bond market in India, it may not be possible to borrow hugeamounts domestically. This has, in fact, prompted firms to increasingly depend on bankcredit for debt needs. Given the stress in the banking system, there are concerns aboutthe extent to which the next wave of investment can obtain debt financing.

This calls for reforms in foreign capital inflows for debt financing. This can be donein two ways:

1. Onshore issuance of bonds denominated in rupees which are purchased by foreigninvestors operating in India. This channel places no currency exposure uponIndian persons and there is no market failure. This needs to be permitted, enabledand encouraged.

2. Overseas issuance of foreign currency denominated bonds by Indian firms. Thisinvolves certain policy concerns which is the focus of the present report.

This chapter provides the background necessary to appreciate the extant legal frame-work supporting ECB and the need for its review. It gives an overview of the regulationsgoverning this field, their outcomes and the difficulties with the present arrangement. Itthen looks at how Brazil, South Africa, South Korea, and Turkey (BSST countries) haveaddressed this through regulations. It concludes that the extant framework needs to bechanged to make it in sync with global best practices and contemporary policy thinkingin this field.

8 Background

2.1 The extant legal framework2.1.1 Evolution of the framework

From the 1950s to the early 1980s, Indian firms’ access to international capital marketswas restricted mainly to bilateral and multilateral assistance. In course of time, thesesources of finance were found inadequate and were supplemented with commercialborrowing through international capital markets. In the second half of the 1980s, thepolicy framework encouraged financial institutions and public sector undertakings toaccess the international market. With the introduction of economic reforms since thebalance of payments crisis, external assistance ceased to be an important element ofcapital inflows and private capital flows gained prominence. ECB rose significantly inthis period.10 In the following years, India pursued a regulatory approach of encouragingnon-debt creating flows and placing restrictions on debt creating flows.11 During initialyears, the MOF used to decide the ECB policy through guidelines and administer thesame.12 In course of time, the administration was fully transferred to RBI, while thepolicy is being determined by Government is consultation with RBI.

Section 6(3)(d) of the Foreign Exchange Management Act, 1999 empowers RBI toissue regulations governing any borrowing or lending in foreign exchange. Pursuant tothis provision, RBI has categorised various forms of foreign currency borrowing andissued regulations governing these categories:

1. External Commercial Borrowing: These are commercial loans in the form ofbank loans, buyers’ credit, suppliers’ credit, securitised instruments (like floatingrate notes and fixed rate bonds, non-convertible, optionally convertible or par-tially convertible preference shares) availed of from non-resident lenders with aminimum average maturity of three years. ECB is governed by FEMA 3.13

2. Foreign Currency Convertible Bonds: These are issued by an Indian companyand subscribed by non-residents. These are convertible into ordinary shares of theissuing company in any manner, either in whole, or in part. The issue of FCCBsis governed by the 1993 Scheme and the provisions of FEMA 120.14 The ECBregulations are applicable to the debt portion of FCCBs.

3. Preference shares: Preference shares of Indian companies (which may be non-convertible, optionally convertible or partially convertible) for issue of which fundshave been received on or after May 1, 2007 are considered as debt. Accordingly,these attract the ECB framework.

4. Foreign Currency Exchangeable Bonds: These are issued by an Indian com-

10See, Bhupal Singh, Corporate choice for overseas borrowings: The Indian evidence, MPRA Paper,University Library of Munich, Germany, 2007.

11This approach was advocated by the Rangarajan Committee. See, C. Rangarajan, Report of the HighLevel Committee on Balance of Payments, tech. rep., Government of India, 1993.

12See, Ministry of Finance, Government revises External Commercial Borrowings Policy, Nov. 12, 2003,URL: http://pib.nic.in/archieve/lreleng/lyr2003/rnov2003/12112003/r1211200314.html (visited on 09/12/2014).

13See, Reserve Bank of India, Foreign Exchange Management (Borrowing or lending in foreignexchange) Regulations, 2000, Notification No. FEMA 3/2000-RB dated 3rd May 2000, May 3, 2000.

14See, Department of Economic Affairs, Ministry of Finance, Issue of Foreign Currency ConvertibleBonds and Ordinary Shares (Through Depositary Receipt Mechanism) Scheme, 1993, GSR 700(E),Nov. 12, 1993; Reserve Bank of India, Foreign Exchange Management (Transfer or issue of any foreignsecurity) Regulations, 2004, Notification No. FEMA 120/RB-2004 dated July 7, 2004, July 7, 2004.

2.1 The extant legal framework 9

pany (called the ‘issuing company’) and subscribed by non-residents. These areconvertible into equity shares of another company, called the ‘offered company’.The ‘issuing company’ is part of the promoter group of the ‘offered company’and holds the equity shares offered at the time of issuance of Foreign CurrencyExchangeable Bond (FCEB). The FCEBs are governed by the 2008 Scheme.15

The regulations governing ECB also apply to FCEBs.RBI amends and modifies regulations through notifications. It also issues circulars

to clarify the legal position on various issues. In July every year, it brings up a mastercircular explaining the updated policy position, and consolidating all the relevant notifi-cations and circulars issued by it over the course of the previous year. The latest mastercircular provides the updated policy framework as on November 25, 2014 with regard toECB.16

2.1.2 The extant framework for ECB

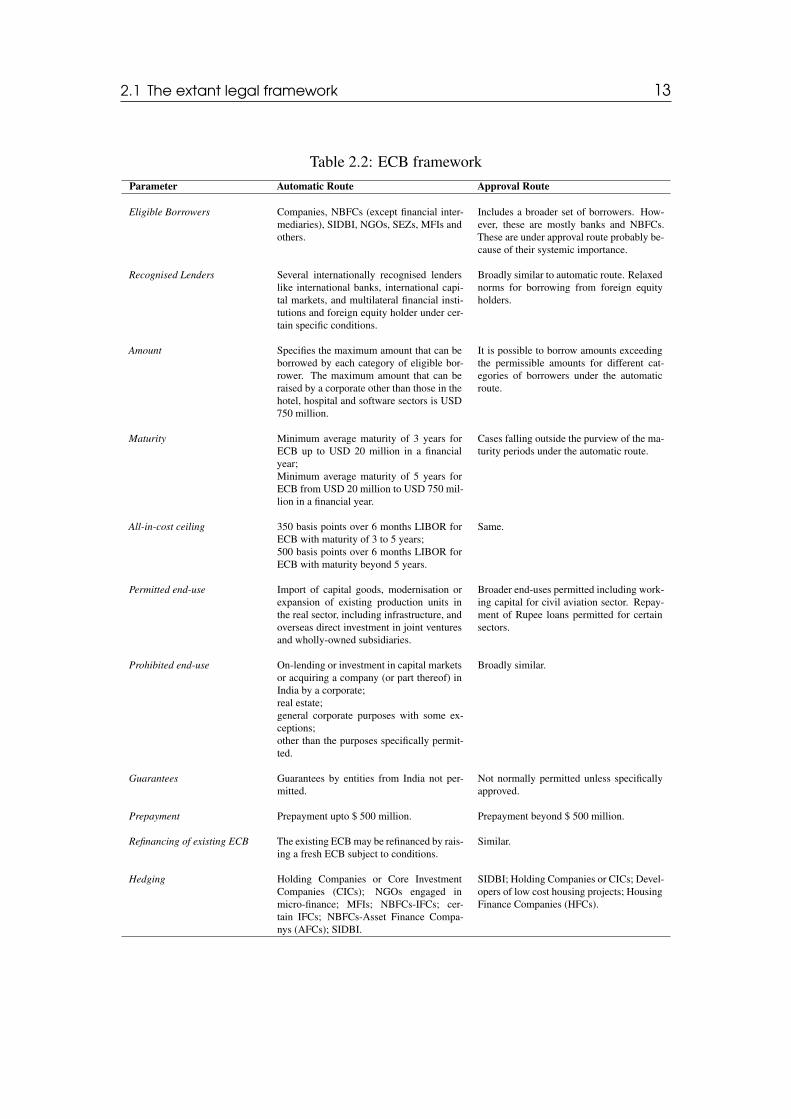

ECB can be accessed under the automatic route or the approval route. Under theautomatic route, no approval is needed to access ECB. Under the approval route, specificapproval from RBI is necessary. Broadly a borrowing not covered under automaticroute requires approval of RBI. Generally, ECB allowed for a sector or end-use for thefirst time is kept under the approval route before being shifted to the automatic route.Further, banks and financial institutions have relatively more restrictions on accessingECB. Borrowing, whether under the automatic or the approval route, are subject tonumerous restrictions, including restrictions on who can borrow, who can lend, the termsof the borrowing, the uses to which the borrowed amount can be put (‘end-use’), thecost of borrowing (‘all-in-cost’) and so on.17 This section describes these restrictions onautomatic and approval routes in detail. Table 2.2 provides a brief comparative overviewof the key parameters of these restrictions.

Automatic route• Eligible borrowers: Initially, only firms registered under the Companies Act, 1956,

except financial intermediaries, were allowed to borrow under this route. Overtime, the list of eligible borrowers has expanded to include certain categories ofNBFCs, NGOs, Special Economic Zones (SEZs), and Micro Finance Institutions(MFIs).18

• Recognised lenders: There are several internationally recognised lenders, suchas international banks, international capital markets, and multilateral financialinstitutions such as International Finance Corporation (IFC), Asian DevelopmentBank (ADB), and Commonwealth Development Corporation (CDC), export credit

15See, Department of Economic Affairs, Ministry of Finance, Issue of Foreign Currency ExchangeableBonds Scheme, 2008, GSR 89(E), Feb. 15, 2008.

16For the latest version, see, Reserve Bank of India, Master Circular on External Commercial Borrow-ings and Trade Credits, July 1, 2014.

17The cost of borrowing in the international capital markets is linked to the 6-month London InterbankOffered Rate (LIBOR) for the respective currencies in which the loan is raised. Referred to as the‘all-in-cost’, it includes rate of interest, other fees and expenses in foreign currency except commitmentfee, pre-payment fee, and fees payable in Indian Rupees. This is an important instrument in the hands ofthe regulator to modulate capital flows. See Part I I.(A) iv, ibid.

18See Part I(I)(A)(i), ibid.

10 Background

Table 2.1: All-in-cost ceilings over 6 month LIBOR (Basis points)

Date of RBI circulars ≥ 3 years ≤ 5 years ≥ 5 years ≤ 7 years ≥ 7 years31.01.2004 200 350 35021.05.2007 150 250 25029.05.2008 200 350 35022.09.2008 200 350 45022.10.2008 300 500 50009.12.2009 300 500 50023.11.2011 350 500 500

Source: RBI

agencies, suppliers of equipment, foreign collaborators and foreign equity holders.Overseas organisations and individuals with a certificate of due diligence fromoverseas bank adhering to host country regulations are allowed to lend under theautomatic route. Foreign equity holders are also recognised lenders under certainspecified conditions.19

• Amount: The framework specifies the maximum amount that can be borrowed byeach category of eligible borrower and for each purpose. As an example, whilethe maximum amount that can be borrowed by a firm is USD 750 million, firmsin specific sectors such as hotels, hospitals and software sector and miscellaneousservices are allowed to borrow up to USD 200 million. In some cases it is linkedto a percentage of its own funds.

• Maturity: ECB upto USD 20 million or its equivalent can be raised in a financialyear with minimum average maturity of 3 years. ECB above USD 20 million orequivalent and upto USD 750 million or its equivalent can be raised in a financialyear with a minimum average maturity of 5 years.20

• All-in-cost ceiling: The all-in-cost ceiling was reduced in May 2007 from 200basis points to 150 basis points over the six-month LIBOR for ECB of tenor ofthree to five years. For a tenor of more than five years, the cost ceiling was reducedfrom 350 basis points to 250 basis points over six-month LIBOR.21 Since then,there has been a progressive liberalisation of the spreads. Table 2.1 shows thechanges in the all-in-cost ceilings from 2004 onwards.22

• End-use restrictions: Borrowing is permitted for import of capital goods, mod-ernisation or expansion of existing production units in the real sector, includinginfrastructure, and overseas direct investment in joint ventures and wholly ownedsubsidiaries. Over time, the list of permissible activities has been expanded toenable certain categories of NBFCs to avail of ECB for on-lending and leasingto infrastructure projects. ECB is also allowed for general corporate purposes bycertain categories of eligible borrowers from direct foreign equity holders subjectto certain conditions.23 It is generally not permitted for on-lending or investmentin capital market, real estate, working capital, general corporate purpose andrepayment of existing rupee loans.

• Guarantees: Issuance of guarantee, standby letter of credit, letter of undertaking

19See Part I(I)(A)(ii), Reserve Bank of India, 2014 Master Circular, see n. 16.20See Part I(I)(A)(iii), ibid.21See, Reserve Bank of India, External Commercial Borrowings (ECB) – End-use and All-in-cost

ceilings - Revised, RBI/2006-2007/409 A. P. (DIR Series) Circular No. 60, May 21, 2007.22Also see Part I(I)(A)(iv), Reserve Bank of India, 2014 Master Circular, see n. 16.23See Part I (I)(A)(v), ibid.

2.1 The extant legal framework 11

or letter of comfort by banks, financial institutions and NBFCs from India relatingto ECB is not permitted.24

• Parking of ECB proceeds: If funds are borrowed for rupee expenditure, theyshould be repatriated immediately. In case of foreign currency expenditure, ECBproceeds may be retained abroad pending utilisation. When retained abroad, thefunds may be invested in prescribed assets.25

• Prepayment: Prepayment of ECB up to USD 500 million may be allowed by Au-thorised Dealer (AD) banks without prior approval of RBI, subject to compliancewith the stipulated minimum average maturity period as applicable to the loan.26

• Refinancing of an existing ECB: Borrowers are allowed to refinance their existingECB by raising a fresh ECB subject to the condition that the fresh ECB is raisedat a lower all-in-cost ceiling and the outstanding maturity of the original ECB ismaintained.27

• Procedural requirements: Borrowing firms are required to report details of loanagreements to the ADs for any amount of ECB in any category.28

Approval route

Generally, ECB beyond the amount (for example, USD 750 million by corporatesand SEZ, USD 200 million by hotel, hospital and software sector) permissible underautomatic route and ECB with maturities falling outside the limits under automatic routeare considered under approval route.

• Eligible borrowers: A variety of borrowers are permitted to access ECB under theapproval route. These include:29

– Banks and financial institutions which had participated in the textile or steelsector restructuring package;

– NBFCs undertaking ECB with a minimum average maturity of 5 years;– Housing finance companies undertaking FCCBs;– Special purpose vehicles or any other entity notified by RBI set up to finance

infrastructure companies/ projects;– Multi-state co-operative societies engaged in manufacturing activity;– Certain categories of NBFCs, SEZ developers, Small Industries Development

Bank of India (SIDBI).• Recognised lenders: The list of eligible lenders is broadly similar to the one

prescribed under the automatic route. Indirect equity holders and group companies

24See Part I(I)(A)(viii), ibid.25See Part I(I)(A)(x), ibid.26See Part I(I)(A)(xi), ibid.27See Part I(I)(A)(xii), ibid.28 This information is submitted in Form-83. See Annex I, Reserve Bank of India, External Commercial

Borrowings (ECB) – Rationalisation of Form-83, RBI/2011-12/620 A. P. (DIR Series) Circular No. 136,June 26, 2012; the AD has to certify that the borrowing company complies with the ECB regulationsand that the AD recommends the application for allotment of Loan Registration Number (LRN). Theborrower can draw-down the loan only after obtaining the LRN from RBI. In addition, borrowers arerequired to submit ECB-2 return certified by the designated AD bank on a monthly basis ensuring itreaches RBI within seven working days from the close of the month to which it relates. See Annex III,Reserve Bank of India, 2014 Master Circular, see n. 16.

29See Part I(I)(B)(i), Reserve Bank of India, 2014 Master Circular, see n. 16.

12 Background

can also lend under specified conditions.30

• Amount: Under the approval route, it is possible to borrow amounts exceedingthe amounts permissible for different categories of borrowers under the automaticroute.31

• Maturity: Under the approval route, it is possible to borrow for maturities fallingoutside the limits under the automatic route. The borrowers may avail of shortterm credit under the ECB in anticipation of it being replaced by long-term ECB.32

• All-in-cost ceilings: The all-in-cost ceilings under the approval route are similarto those under the automatic route.33

• End-use restrictions: Though broadly similar to those under automatic route, thereare several exceptions. While ECB for acquisition of a company is prohibitedunder the automatic route, it is permitted under the approval route for acquisitionby a IFC, EXIM bank, etc. Firms in the power sector are allowed to refinance rupeedenominated loans through ECB to a much greater extent than other infrastructurefirms.34 Civil aviation firms can use ECB for working capital requirements.35

• Guarantee: Issuance of guarantee, standby letter of credit, letter of undertaking orletter of comfort by banks, financial institutions and NBFCs relating to ECB isnot normally permitted. For some sectors, issuance of guarantees are consideredsubject to prudential norms.36

• Prepayment: Prepayment for amounts exceeding USD 500 million is considered.37

• Refinancing/Rescheduling of existing ECB: The existing ECB may be refinancedby raising a fresh ECB subject to the condition that the fresh ECB is raised at alower all-in-cost, the outstanding maturity of the original ECB is not reduced andthe amount of fresh ECB is beyond the eligible limit under the automatic route.Such refinance is not permitted by raising fresh ECB from overseas branches/sub-sidiaries of Indian banks.38

In addition to the regulatory framework governing firm’s borrowing, there is anaggregate soft cap on ECB which is decided by the HLCECB. The HLCECB is chairedby the Finance Secretary and has officials from RBI and MOF.

2.1.3 The extant framework for hybrid instruments

This section offers a brief overview of the extant framework for FCCBs and FCEBs.As hybrid instruments, these are subject to restrictions applicable to equities as well asdebt instruments. Further, FCCBs must conform to the Foreign Direct Investment (FDI)

30See Part I(I)(B)(ii), Reserve Bank of India, 2014 Master Circular, see n. 16.31See Part I(I)(B)(iii), ibid.32See Part I(I)(B)(v)(h), ibid.33See Part I(I)(B)(iv), ibid.34Indian companies which are in the infrastructure sector (except companies in the power sector), as

defined under the extant ECB regulations, are permitted to utilise 25% of the fresh ECB raised by themtowards refinancing of the Rupee loans availed by them from the domestic banking system, the companiesin the power sector are permitted to utilize up to 40% of the fresh ECB raised by them towards refinancingof the Rupee loans availed by them from the domestic banking system. See Part I(I)(B)(v)(f), ibid.

35See Part I(I)(B)(v)(i), ibid.36See Part I (I)(B)(x), ibid.37See Part I(I)(B)(xiii), ibid.38See Part I(I)(B)(xiv), ibid.

2.1 The extant legal framework 13

Table 2.2: ECB frameworkParameter Automatic Route Approval Route

Eligible Borrowers Companies, NBFCs (except financial inter-mediaries), SIDBI, NGOs, SEZs, MFIs andothers.

Includes a broader set of borrowers. How-ever, these are mostly banks and NBFCs.These are under approval route probably be-cause of their systemic importance.

Recognised Lenders Several internationally recognised lenderslike international banks, international capi-tal markets, and multilateral financial insti-tutions and foreign equity holder under cer-tain specific conditions.

Broadly similar to automatic route. Relaxednorms for borrowing from foreign equityholders.

Amount Specifies the maximum amount that can beborrowed by each category of eligible bor-rower. The maximum amount that can beraised by a corporate other than those in thehotel, hospital and software sectors is USD750 million.

It is possible to borrow amounts exceedingthe permissible amounts for different cat-egories of borrowers under the automaticroute.

Maturity Minimum average maturity of 3 years forECB up to USD 20 million in a financialyear;Minimum average maturity of 5 years forECB from USD 20 million to USD 750 mil-lion in a financial year.

Cases falling outside the purview of the ma-turity periods under the automatic route.

All-in-cost ceiling 350 basis points over 6 months LIBOR forECB with maturity of 3 to 5 years;500 basis points over 6 months LIBOR forECB with maturity beyond 5 years.

Same.

Permitted end-use Import of capital goods, modernisation orexpansion of existing production units inthe real sector, including infrastructure, andoverseas direct investment in joint venturesand wholly-owned subsidiaries.

Broader end-uses permitted including work-ing capital for civil aviation sector. Repay-ment of Rupee loans permitted for certainsectors.

Prohibited end-use On-lending or investment in capital marketsor acquiring a company (or part thereof) inIndia by a corporate;real estate;general corporate purposes with some ex-ceptions;other than the purposes specifically permit-ted.

Broadly similar.

Guarantees Guarantees by entities from India not per-mitted.

Not normally permitted unless specificallyapproved.

Prepayment Prepayment upto $ 500 million. Prepayment beyond $ 500 million.

Refinancing of existing ECB The existing ECB may be refinanced by rais-ing a fresh ECB subject to conditions.

Similar.

Hedging Holding Companies or Core InvestmentCompanies (CICs); NGOs engaged inmicro-finance; MFIs; NBFCs-IFCs; cer-tain IFCs; NBFCs-Asset Finance Compa-nys (AFCs); SIDBI.

SIDBI; Holding Companies or CICs; Devel-opers of low cost housing projects; HousingFinance Companies (HFCs).

14 Background

policy.39

Foreign Currency Convertible Bonds

Any company raising foreign funds through FCCBs must obtain permission fromMOF.40 As with all foreign currency borrowing, there are a number of restrictionsthat apply to these instruments.

The Foreign Exchange Management Act, 1999 prohibits issue or transfer of a foreignsecurity by a person resident in India unless specifically permitted by RBI.41 Accordingly,the 2014 Master Circular, FEMA 3 and FEMA 120 apply to the debt portion of theFCCBs. They permit issue of FCCBs subject to restrictions on the amount,42 maturity,43

all-in-cost ceilings,44 and hedging.

In addition, because these are hybrid instruments with equity component, additionalrestrictions apply regarding the jurisdictions in which they can be listed45 and theconversion price.46 The interest from FCCBs is subject to 10% taxation at source.47

However, conversion to equity and transfer of the FCCB abroad from one non-residentto another are not taxable.

Foreign Currency Exchangeable Bonds

FCEBs can be issued by any Indian company (‘issuing company’) eligible to raise fundsfrom Indian securities market. These instruments may be convertible into equity sharesof a listed company (‘offered company’), which is engaged in a sector eligible to receiveFDI and eligible to issue or avail of FCCB or ECB.48 Restrictions apply on maturity,49

39See, DEA, 1993 Scheme, see n. 14.40See, ibid.41See section 6(3)(a), Foreign Exchange Management Act, 1999.42The amount cannot exceed USD 750 million in a financial year through automatic route. Issue of

FCCBs beyond USD 750 million requires specific approval from RBI. See Schedule I, Reserve Bank ofIndia, FEMA 120, see n. 14.

43The maturity of these instruments cannot be more than 5 years. See, ibid.44The all-in-cost ceilings and end-use restrictions are aligned with those of ECB under FEMA 345If the company is unlisted, it can issue FCCBs only if they are listed in International Organization of

Securities Commissions (IOSCO) or Financial Action Task Force (FATF) compliant jurisdictions. BeforeOctober 11, 2013, unlisted companies were required to simultaneously list on an Indian stock exchange.See, Ministry of Finance, Issue of Foreign Currency Convertible Bonds and Ordinary Shares (ThroughDepositary Mechanism)(Amendment) Scheme, 2013, Notification No. GSR 684(E) [F.No.4/13/2012-ECB],Oct. 11, 2013.

46The conversion price of FCCBs into the underlying equity should not be less than the average of theweekly high and low of the closing prices of the related shares quoted on the stock exchange during thetwo weeks preceding the relevant date. See paragraphs 5(4)(ca) and 5(4)(e)(i), DEA, 1993 Scheme, seen. 14.

47See section 115AC, Income Tax Act, 1961.48See paragraph 3(1) and 3(2), DEA, 2008 Scheme, see n. 15.49The minimum average maturity of FCEB is five years.

2.2 Description of outcomes 15

exchange price,50 end-use,51 interest,52 and dividend payments.53 However, conversionto equity and transfer of the FCEBs abroad from one non-resident to another are nottaxable.

The subscriber to FCEBs is required to comply with the FDI policy and adhere tothe sectoral caps at the time of issuance of FCEBs. Prior approval of Foreign InvestmentPromotion Board (FIPB), wherever required under the FDI policy, should be obtained.54

The rate of interest payable on FCEB and the issue expenses incurred in foreign currencymust conform to the all-in-cost-ceilings prescribed by RBI under the ECB regulations.55

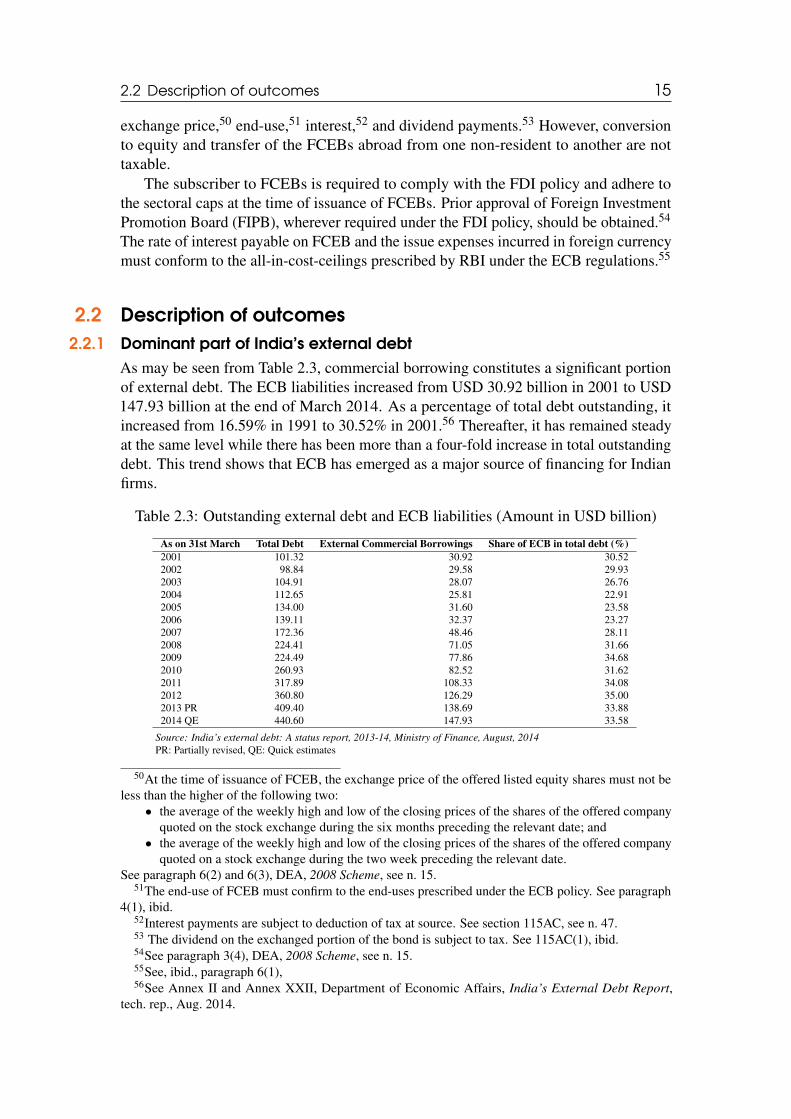

2.2 Description of outcomes2.2.1 Dominant part of India’s external debt

As may be seen from Table 2.3, commercial borrowing constitutes a significant portionof external debt. The ECB liabilities increased from USD 30.92 billion in 2001 to USD147.93 billion at the end of March 2014. As a percentage of total debt outstanding, itincreased from 16.59% in 1991 to 30.52% in 2001.56 Thereafter, it has remained steadyat the same level while there has been more than a four-fold increase in total outstandingdebt. This trend shows that ECB has emerged as a major source of financing for Indianfirms.

Table 2.3: Outstanding external debt and ECB liabilities (Amount in USD billion)

As on 31st March Total Debt External Commercial Borrowings Share of ECB in total debt (%)2001 101.32 30.92 30.522002 98.84 29.58 29.932003 104.91 28.07 26.762004 112.65 25.81 22.912005 134.00 31.60 23.582006 139.11 32.37 23.272007 172.36 48.46 28.112008 224.41 71.05 31.662009 224.49 77.86 34.682010 260.93 82.52 31.622011 317.89 108.33 34.082012 360.80 126.29 35.002013 PR 409.40 138.69 33.882014 QE 440.60 147.93 33.58

Source: India’s external debt: A status report, 2013-14, Ministry of Finance, August, 2014PR: Partially revised, QE: Quick estimates

50At the time of issuance of FCEB, the exchange price of the offered listed equity shares must not beless than the higher of the following two:

• the average of the weekly high and low of the closing prices of the shares of the offered companyquoted on the stock exchange during the six months preceding the relevant date; and

• the average of the weekly high and low of the closing prices of the shares of the offered companyquoted on a stock exchange during the two week preceding the relevant date.

See paragraph 6(2) and 6(3), DEA, 2008 Scheme, see n. 15.51The end-use of FCEB must confirm to the end-uses prescribed under the ECB policy. See paragraph

4(1), ibid.52Interest payments are subject to deduction of tax at source. See section 115AC, see n. 47.53 The dividend on the exchanged portion of the bond is subject to tax. See 115AC(1), ibid.54See paragraph 3(4), DEA, 2008 Scheme, see n. 15.55See, ibid., paragraph 6(1),56See Annex II and Annex XXII, Department of Economic Affairs, India’s External Debt Report,

tech. rep., Aug. 2014.

16 Background

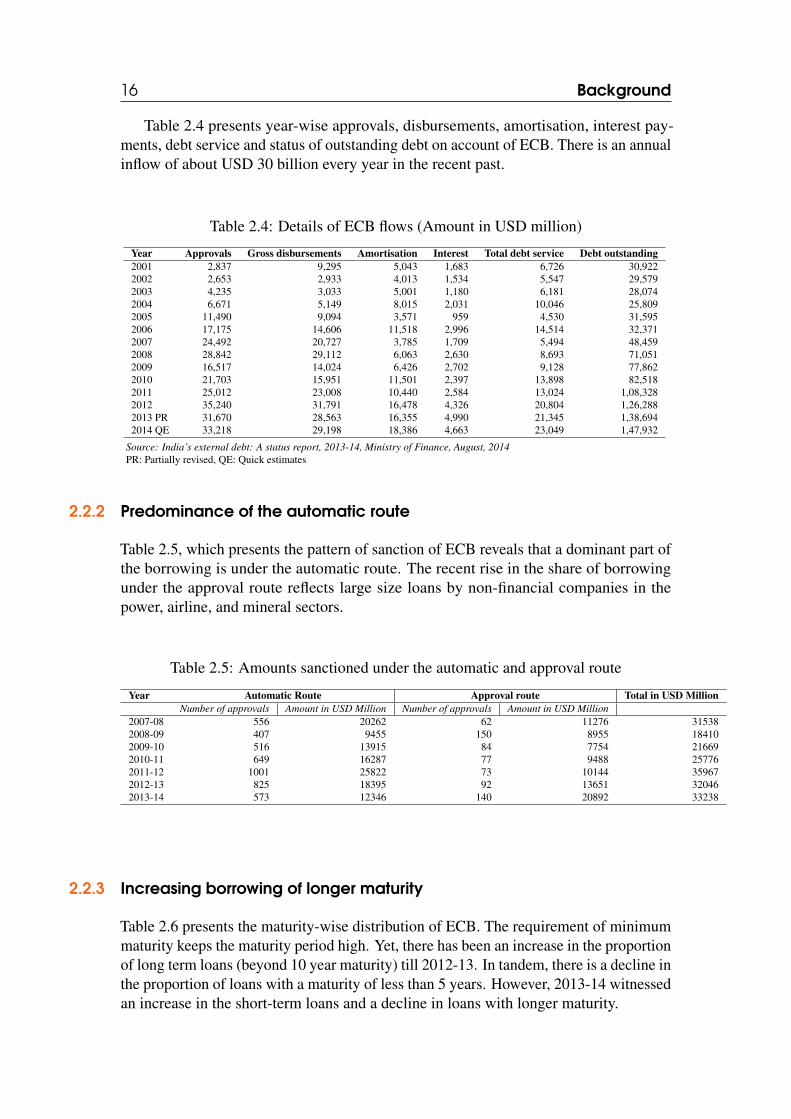

Table 2.4 presents year-wise approvals, disbursements, amortisation, interest pay-ments, debt service and status of outstanding debt on account of ECB. There is an annualinflow of about USD 30 billion every year in the recent past.

Table 2.4: Details of ECB flows (Amount in USD million)

Year Approvals Gross disbursements Amortisation Interest Total debt service Debt outstanding2001 2,837 9,295 5,043 1,683 6,726 30,9222002 2,653 2,933 4,013 1,534 5,547 29,5792003 4,235 3,033 5,001 1,180 6,181 28,0742004 6,671 5,149 8,015 2,031 10,046 25,8092005 11,490 9,094 3,571 959 4,530 31,5952006 17,175 14,606 11,518 2,996 14,514 32,3712007 24,492 20,727 3,785 1,709 5,494 48,4592008 28,842 29,112 6,063 2,630 8,693 71,0512009 16,517 14,024 6,426 2,702 9,128 77,8622010 21,703 15,951 11,501 2,397 13,898 82,5182011 25,012 23,008 10,440 2,584 13,024 1,08,3282012 35,240 31,791 16,478 4,326 20,804 1,26,2882013 PR 31,670 28,563 16,355 4,990 21,345 1,38,6942014 QE 33,218 29,198 18,386 4,663 23,049 1,47,932

Source: India’s external debt: A status report, 2013-14, Ministry of Finance, August, 2014PR: Partially revised, QE: Quick estimates

2.2.2 Predominance of the automatic route

Table 2.5, which presents the pattern of sanction of ECB reveals that a dominant part ofthe borrowing is under the automatic route. The recent rise in the share of borrowingunder the approval route reflects large size loans by non-financial companies in thepower, airline, and mineral sectors.

Table 2.5: Amounts sanctioned under the automatic and approval route

Year Automatic Route Approval route Total in USD MillionNumber of approvals Amount in USD Million Number of approvals Amount in USD Million

2007-08 556 20262 62 11276 315382008-09 407 9455 150 8955 184102009-10 516 13915 84 7754 216692010-11 649 16287 77 9488 257762011-12 1001 25822 73 10144 359672012-13 825 18395 92 13651 320462013-14 573 12346 140 20892 33238

2.2.3 Increasing borrowing of longer maturity

Table 2.6 presents the maturity-wise distribution of ECB. The requirement of minimummaturity keeps the maturity period high. Yet, there has been an increase in the proportionof long term loans (beyond 10 year maturity) till 2012-13. In tandem, there is a decline inthe proportion of loans with a maturity of less than 5 years. However, 2013-14 witnessedan increase in the short-term loans and a decline in loans with longer maturity.

2.2 Description of outcomes 17

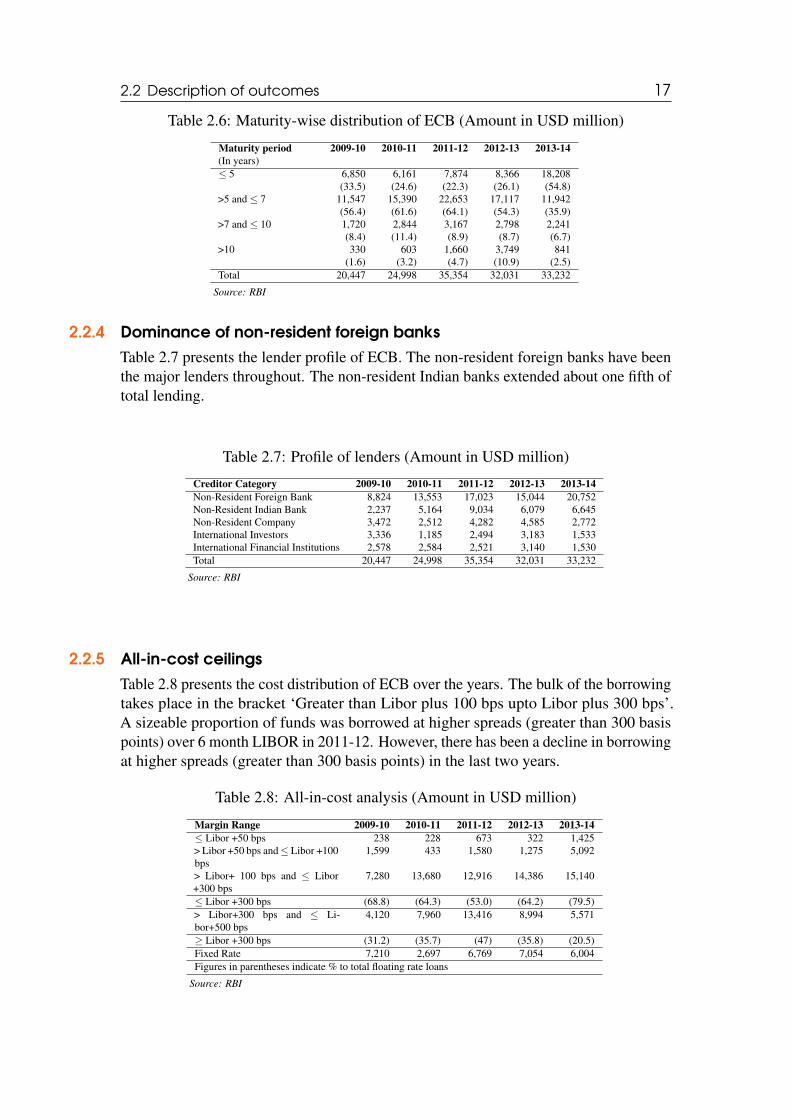

Table 2.6: Maturity-wise distribution of ECB (Amount in USD million)

Maturity period 2009-10 2010-11 2011-12 2012-13 2013-14(In years)≤ 5 6,850 6,161 7,874 8,366 18,208

(33.5) (24.6) (22.3) (26.1) (54.8)>5 and ≤ 7 11,547 15,390 22,653 17,117 11,942

(56.4) (61.6) (64.1) (54.3) (35.9)>7 and ≤ 10 1,720 2,844 3,167 2,798 2,241

(8.4) (11.4) (8.9) (8.7) (6.7)>10 330 603 1,660 3,749 841

(1.6) (3.2) (4.7) (10.9) (2.5)Total 20,447 24,998 35,354 32,031 33,232

Source: RBI

2.2.4 Dominance of non-resident foreign banksTable 2.7 presents the lender profile of ECB. The non-resident foreign banks have beenthe major lenders throughout. The non-resident Indian banks extended about one fifth oftotal lending.

Table 2.7: Profile of lenders (Amount in USD million)

Creditor Category 2009-10 2010-11 2011-12 2012-13 2013-14Non-Resident Foreign Bank 8,824 13,553 17,023 15,044 20,752Non-Resident Indian Bank 2,237 5,164 9,034 6,079 6,645Non-Resident Company 3,472 2,512 4,282 4,585 2,772International Investors 3,336 1,185 2,494 3,183 1,533International Financial Institutions 2,578 2,584 2,521 3,140 1,530Total 20,447 24,998 35,354 32,031 33,232

Source: RBI

2.2.5 All-in-cost ceilingsTable 2.8 presents the cost distribution of ECB over the years. The bulk of the borrowingtakes place in the bracket ‘Greater than Libor plus 100 bps upto Libor plus 300 bps’.A sizeable proportion of funds was borrowed at higher spreads (greater than 300 basispoints) over 6 month LIBOR in 2011-12. However, there has been a decline in borrowingat higher spreads (greater than 300 basis points) in the last two years.

Table 2.8: All-in-cost analysis (Amount in USD million)

Margin Range 2009-10 2010-11 2011-12 2012-13 2013-14≤ Libor +50 bps 238 228 673 322 1,425> Libor +50 bps and ≤ Libor +100bps

1,599 433 1,580 1,275 5,092

> Libor+ 100 bps and ≤ Libor+300 bps

7,280 13,680 12,916 14,386 15,140

≤ Libor +300 bps (68.8) (64.3) (53.0) (64.2) (79.5)> Libor+300 bps and ≤ Li-bor+500 bps

4,120 7,960 13,416 8,994 5,571

≥ Libor +300 bps (31.2) (35.7) (47) (35.8) (20.5)Fixed Rate 7,210 2,697 6,769 7,054 6,004Figures in parentheses indicate % to total floating rate loans

Source: RBI

18 Background

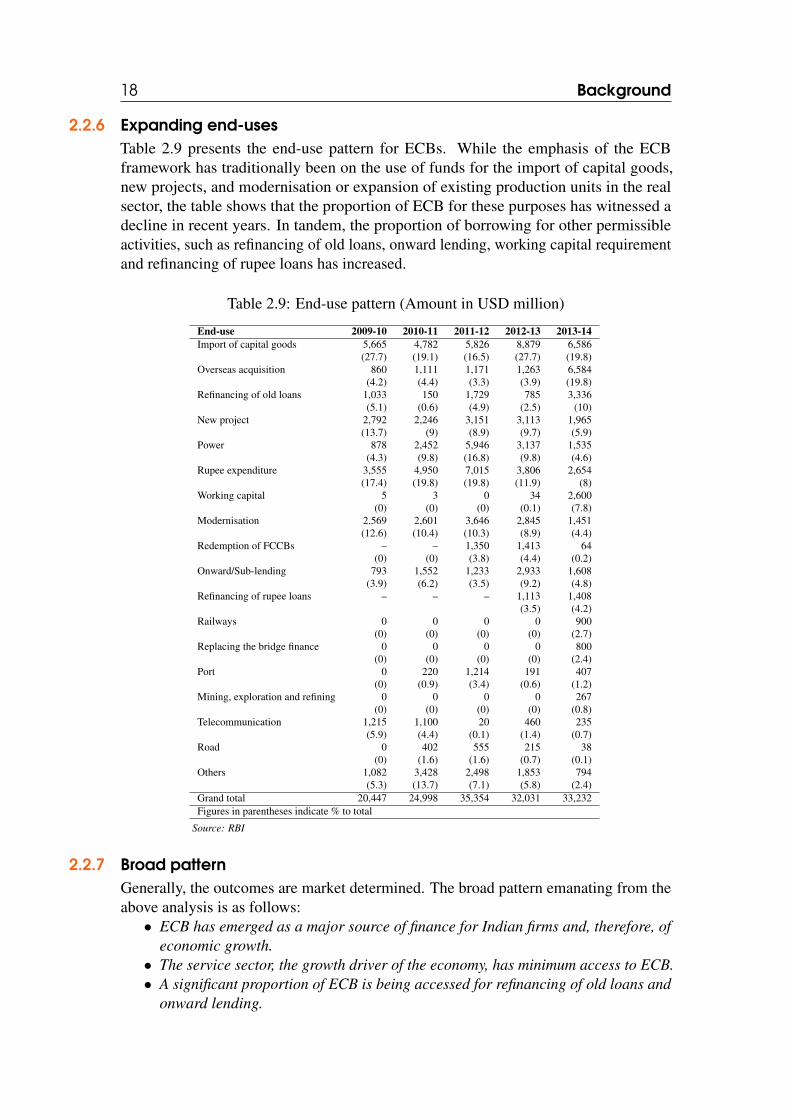

2.2.6 Expanding end-usesTable 2.9 presents the end-use pattern for ECBs. While the emphasis of the ECBframework has traditionally been on the use of funds for the import of capital goods,new projects, and modernisation or expansion of existing production units in the realsector, the table shows that the proportion of ECB for these purposes has witnessed adecline in recent years. In tandem, the proportion of borrowing for other permissibleactivities, such as refinancing of old loans, onward lending, working capital requirementand refinancing of rupee loans has increased.

Table 2.9: End-use pattern (Amount in USD million)

End-use 2009-10 2010-11 2011-12 2012-13 2013-14Import of capital goods 5,665 4,782 5,826 8,879 6,586

(27.7) (19.1) (16.5) (27.7) (19.8)Overseas acquisition 860 1,111 1,171 1,263 6,584

(4.2) (4.4) (3.3) (3.9) (19.8)Refinancing of old loans 1,033 150 1,729 785 3,336

(5.1) (0.6) (4.9) (2.5) (10)New project 2,792 2,246 3,151 3,113 1,965

(13.7) (9) (8.9) (9.7) (5.9)Power 878 2,452 5,946 3,137 1,535

(4.3) (9.8) (16.8) (9.8) (4.6)Rupee expenditure 3,555 4,950 7,015 3,806 2,654

(17.4) (19.8) (19.8) (11.9) (8)Working capital 5 3 0 34 2,600

(0) (0) (0) (0.1) (7.8)Modernisation 2,569 2,601 3,646 2,845 1,451

(12.6) (10.4) (10.3) (8.9) (4.4)Redemption of FCCBs – – 1,350 1,413 64

(0) (0) (3.8) (4.4) (0.2)Onward/Sub-lending 793 1,552 1,233 2,933 1,608

(3.9) (6.2) (3.5) (9.2) (4.8)Refinancing of rupee loans – – – 1,113 1,408

(3.5) (4.2)Railways 0 0 0 0 900

(0) (0) (0) (0) (2.7)Replacing the bridge finance 0 0 0 0 800

(0) (0) (0) (0) (2.4)Port 0 220 1,214 191 407

(0) (0.9) (3.4) (0.6) (1.2)Mining, exploration and refining 0 0 0 0 267

(0) (0) (0) (0) (0.8)Telecommunication 1,215 1,100 20 460 235

(5.9) (4.4) (0.1) (1.4) (0.7)Road 0 402 555 215 38

(0) (1.6) (1.6) (0.7) (0.1)Others 1,082 3,428 2,498 1,853 794

(5.3) (13.7) (7.1) (5.8) (2.4)Grand total 20,447 24,998 35,354 32,031 33,232Figures in parentheses indicate % to total

Source: RBI

2.2.7 Broad patternGenerally, the outcomes are market determined. The broad pattern emanating from theabove analysis is as follows:

• ECB has emerged as a major source of finance for Indian firms and, therefore, ofeconomic growth.

• The service sector, the growth driver of the economy, has minimum access to ECB.• A significant proportion of ECB is being accessed for refinancing of old loans and

onward lending.

2.3 Deficiencies in the extant arrangement 19

• There is an increase in number of borrowing under the automatic route reflectingdecreasing intervention of State in individual transactions.

• Non-resident Indian banks extend a sizeable portion of ECB.• The bulk of borrowing is in the maturity bracket of 5-7 years reflecting currency

exposure over a longer time horizon.• There is a preference to borrow at floating rates indicating acceptance of market

determined outcomes.• The bulk of the borrowing happens at the lower end of the permissible cost

reflecting ability of the Indian firms to strike good deals.

2.3 Deficiencies in the extant arrangementThe stakeholders have brought up the following deficiencies in the extant regime govern-ing ECB to the notice of the Committee.

2.3.1 ComplexityThe 2014 Master Circular issued by RBI on ECB devotes twenty-four pages to specifyas to who can borrow, for what purposes it can borrow, from what sources it can borrow,what amount it can borrow, on what terms it can borrow and subject to what obligations.There are different eligibility norms for each firm wishing to borrow in foreign currencyand it can borrow on specified terms, from specified lenders, for specified purposesand with specified obligations. For example, a NBFC-Infrastructure Finance Companycan borrow up to 75% of its own funds for on-lending to infrastructure sector if ithedges 75% of its currency exposure. An NBFC-AFC can borrow up to 75% of its ownfunds subject to a maximum of USD 200 million per financial year with a minimummaturity of five years for financing of import of infrastructure equipment for leasing toinfrastructure projects provided it hedges the currency exposure in full. The purposesof borrowing are essentially the same in both the cases while the amount that can beborrowed, the terms (maturity) of borrowing and the hedging obligation are different.Take another example. A MFI registered as a society, trust or co-operative can borrowup to USD 10 million from international banks, multilateral financial institutions, exportcredit agencies, overseas organisations and individuals provided it has a satisfactoryborrowing relationship with a bank and its management committee is ‘fit and proper’.A NBFC-MFI can borrow from international banks, multilateral financial institutions,foreign equity holders and overseas organisations. While the end-use is essentially thesame in both the cases, the lenders, eligibility for borrowing, the amount that can beborrowed, and the status of fit and proper are different.

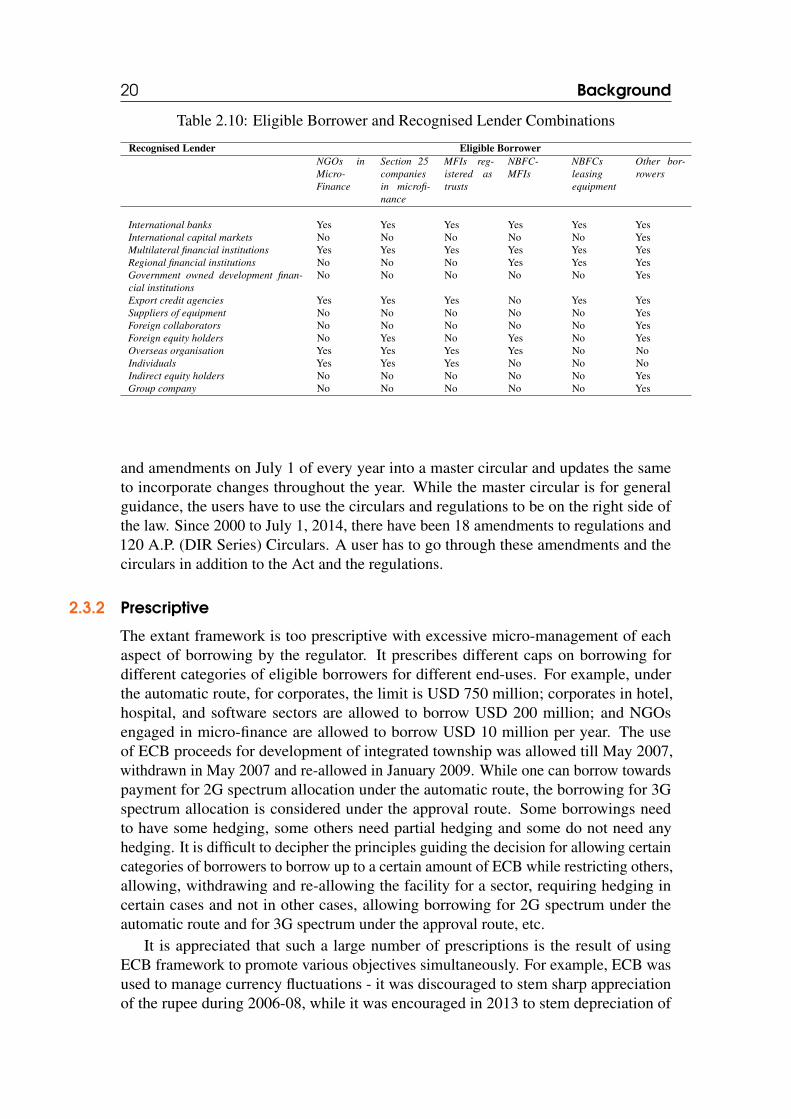

Table 2.10 presents an example of complexity where specified borrowers can borrowfrom specified lenders only. A section 25 company can borrow from international banksand not from government owned development financial institutions, while an exportcredit agency can lend to MFIs registered as trusts and not to NBFC-MFIs.

The Foreign Exchange Management Act, 1999 and the regulations made and circularsissued thereunder govern the ECB. RBI issues general directions through A.P. (DIRSeries) Circulars under section 10(4), section 11(1) and section 11(2) and amends theregulations like FEMA 3, FEMA 8 and FEMA 120 framed under the Foreign ExchangeManagement Act, 1999 to change the ECB framework. It consolidates these circulars

20 Background

Table 2.10: Eligible Borrower and Recognised Lender Combinations

Recognised Lender Eligible BorrowerNGOs inMicro-Finance

Section 25companiesin microfi-nance

MFIs reg-istered astrusts

NBFC-MFIs

NBFCsleasingequipment

Other bor-rowers

International banks Yes Yes Yes Yes Yes YesInternational capital markets No No No No No YesMultilateral financial institutions Yes Yes Yes Yes Yes YesRegional financial institutions No No No Yes Yes YesGovernment owned development finan-cial institutions

No No No No No Yes

Export credit agencies Yes Yes Yes No Yes YesSuppliers of equipment No No No No No YesForeign collaborators No No No No No YesForeign equity holders No Yes No Yes No YesOverseas organisation Yes Yes Yes Yes No NoIndividuals Yes Yes Yes No No NoIndirect equity holders No No No No No YesGroup company No No No No No Yes

and amendments on July 1 of every year into a master circular and updates the sameto incorporate changes throughout the year. While the master circular is for generalguidance, the users have to use the circulars and regulations to be on the right side ofthe law. Since 2000 to July 1, 2014, there have been 18 amendments to regulations and120 A.P. (DIR Series) Circulars. A user has to go through these amendments and thecirculars in addition to the Act and the regulations.

2.3.2 Prescriptive

The extant framework is too prescriptive with excessive micro-management of eachaspect of borrowing by the regulator. It prescribes different caps on borrowing fordifferent categories of eligible borrowers for different end-uses. For example, underthe automatic route, for corporates, the limit is USD 750 million; corporates in hotel,hospital, and software sectors are allowed to borrow USD 200 million; and NGOsengaged in micro-finance are allowed to borrow USD 10 million per year. The useof ECB proceeds for development of integrated township was allowed till May 2007,withdrawn in May 2007 and re-allowed in January 2009. While one can borrow towardspayment for 2G spectrum allocation under the automatic route, the borrowing for 3Gspectrum allocation is considered under the approval route. Some borrowings needto have some hedging, some others need partial hedging and some do not need anyhedging. It is difficult to decipher the principles guiding the decision for allowing certaincategories of borrowers to borrow up to a certain amount of ECB while restricting others,allowing, withdrawing and re-allowing the facility for a sector, requiring hedging incertain cases and not in other cases, allowing borrowing for 2G spectrum under theautomatic route and for 3G spectrum under the approval route, etc.

It is appreciated that such a large number of prescriptions is the result of usingECB framework to promote various objectives simultaneously. For example, ECB wasused to manage currency fluctuations - it was discouraged to stem sharp appreciationof the rupee during 2006-08, while it was encouraged in 2013 to stem depreciation of

2.3 Deficiencies in the extant arrangement 21

the rupee.57 Similarly, banks are not allowed to give guarantee and there are severalprohibitions, restrictions and restrictive permissions on banks and NBFCs for availingECB to maintain integrity of financial system.58 The use of ECB for development ofintegrated township was withdrawn in May 2007, keeping in view sharp rise in assetprices, especially property prices. As a sector specific measure, it was re-allowed inJanuary 2009.59 While some press releases indicate the objective of the prescription,often the objective is either not stated or vague. Ideally every provision prescribing arequirement should explicitly state the rationale for the same.60 The stakeholders mustknow whether a particular prescription addresses a market failure, promotes exchangerate stability, maintains integrity of the banking system or any other. Further, as theGovernment charts out its reforms strategy, its chances of success increases if it keepsthe assignment rule firmly in mind. It is efficient to assign a specific objective to eachinstrument of policy. The consequences of pursuing multiple objectives through oneinstrument can be adverse.61 The ECB policy should not be used, to the extent possible,to pursue so many objectives such as development of a particular sector.

Mr. Padmanabhan does not agree with the above observations and is of the viewthat the measures discussed above were implemented keeping in view larger macroobjectives. Further, the borrowing regime for financial sector entities like banks andNBFCs had always been accorded a different treatment for stability considerations.

Absence of clear principles for determining eligible borrowers leads to an additionof additional categories to the list of eligible borrowers, as and when a representationis received. There were only two broad categories of eligible borrowers in 2004.62

Over one decade, the list has turned into a complex document with sixteen categoriesof eligible borrowers ranging from NBFCs to HFCs, Special Purpose Vehicles (SPVs),co-operative societies, SIDBI, and service sector units. In addition, certain sectorsfacing financial difficulties are allowed ECB for working capital requirement for a fixedwindow.63 This creates problems of political economy. Sectors which are not allowed toavail ECB under the automatic route today keep on persuading the authorities to addthem to the list. Additionally, they apply under the approval category and persuadethe authorities to accede to their requests. This is antithetical to the rule of law andadds hugely to administrative workload and enforcement of law without addressing anymarket failure.

57See, Padmanabhan, see n. 2.58See Part I(I)(A)(viii), Reserve Bank of India, 2014 Master Circular, see n. 16.59See, Ministry of Finance, Review of External commercial borrowings (ECB) policy, Jan. 2, 2009, URL:

http://finmin.nic.in/press_room/2009/jan_details.asp?pageid=7#ECBPolicy02012009(visited on 12/10/2014).

60See, Supreme Court of India, Daiichi Sankyo Company Ltd. v. Jayaram Chigurupati and Ors. (2010)7 SCC 449.

61See, Subir Gokarn, You can’t kill two birds... Nov. 2, 2014, URL: http://www.business-standard . com / article / opinion / subir - gokarn - you - can - t - kill - two - birds -114110200711_1.html (visited on 12/09/2014).

62These were: (a) Financial institutions dealing exclusively with infrastructure and export finance; and(b) Banks and financial institutions which had participated in textile restructuring package subject toprudential norms imposed by RBI.

63See, Reserve Bank of India, 2014 Master Circular, see n. 16.

22 Background

2.3.3 Non-neutrality

The extant framework allows some sectors and not others, allows some companiesand not others, and generally restricts banks, financial institutions and service sectorto access ECB.64 It does not permit ECB for general corporate purposes, includingworking capital. However, it permits ECB for working capital in civil aviation sectorunder the approval route.65 Further, it allows infrastructure firms to utilise 25% of ECBproceeds towards refinancing of rupee loans. It, however, allows firms in the powersector to use 40% of ECB proceeds towards refinancing of rupee loans.66 The frameworkimposes different obligations, such as hedging, on different kinds of borrowers. Thisapproach obviously promotes certain sectors or end uses at the cost of others and therebycontributes to market failure in terms of resource allocation. In fact, a change in policyoccasionally carries a statement that it is a sector specific measure.67 Thus, all sectors ofthe economy do not have the same level playing field. Promotion of a particular sectorwas probably the objective at the relevant time, but is no more relevant today and doesnot gel with the contemporary economic thinking.

It is instructive to look at reforms in the capital market. The Capital Issues (Control)Act, 1947 empowered the authorities to determine the eligible firms to access thedomestic capital market and the terms of access. However, in sync with economicthought of the early 1990s, the Capital Issues (Control) Act, 1947 was repealed. Nowthere is no restriction on a firm to raise any amount for any purpose and it does soon terms acceptable to the market. No sector gets preferential treatment for raisingresources from market.

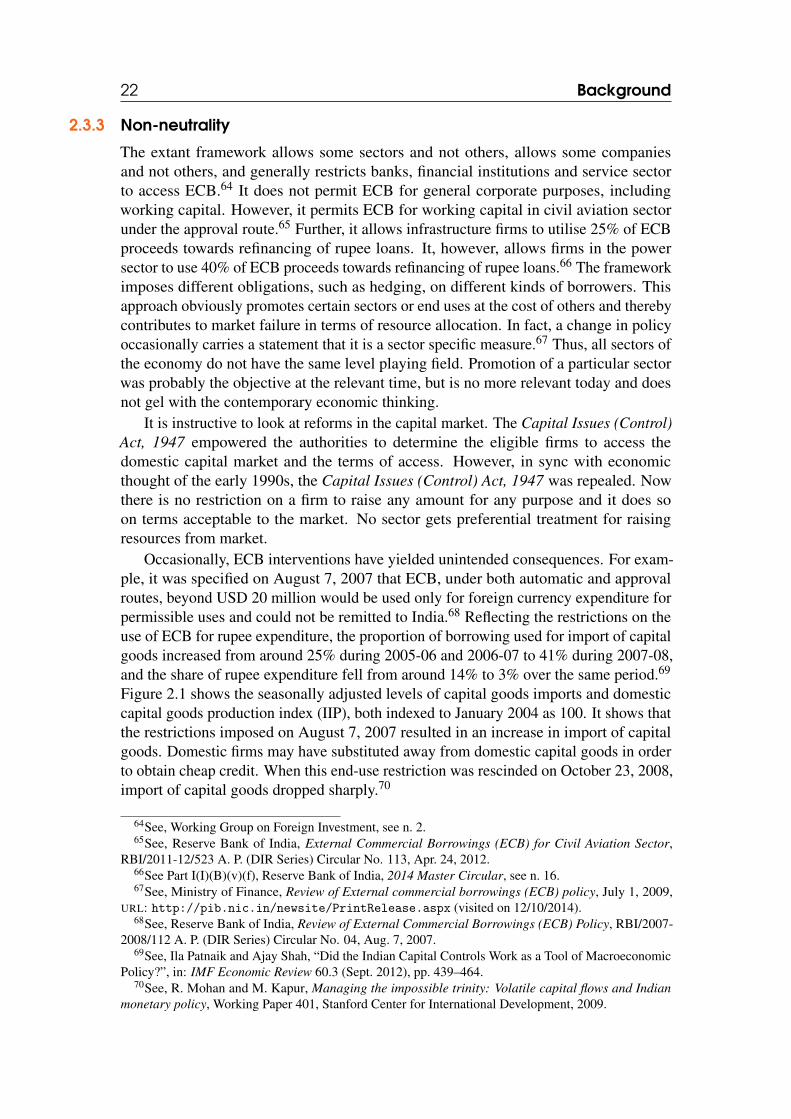

Occasionally, ECB interventions have yielded unintended consequences. For exam-ple, it was specified on August 7, 2007 that ECB, under both automatic and approvalroutes, beyond USD 20 million would be used only for foreign currency expenditure forpermissible uses and could not be remitted to India.68 Reflecting the restrictions on theuse of ECB for rupee expenditure, the proportion of borrowing used for import of capitalgoods increased from around 25% during 2005-06 and 2006-07 to 41% during 2007-08,and the share of rupee expenditure fell from around 14% to 3% over the same period.69

Figure 2.1 shows the seasonally adjusted levels of capital goods imports and domesticcapital goods production index (IIP), both indexed to January 2004 as 100. It shows thatthe restrictions imposed on August 7, 2007 resulted in an increase in import of capitalgoods. Domestic firms may have substituted away from domestic capital goods in orderto obtain cheap credit. When this end-use restriction was rescinded on October 23, 2008,import of capital goods dropped sharply.70

64See, Working Group on Foreign Investment, see n. 2.65See, Reserve Bank of India, External Commercial Borrowings (ECB) for Civil Aviation Sector,