DEVELOPING MACRO-STRESS TESTS: HOW TO IDENTIFY SYSTEMIC RISK SESSION 10 MINDAUGAS LEIKA 1

DEVELOPING MACRO-STRESS TESTS: HOW TO IDENTIFY SYSTEMIC RISK SESSION 10 MINDAUGAS LEIKA 1.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

DEVELOPING MACRO-STRESS TESTS: HOW TO IDENTIFY SYSTEMIC RISKSESSION 10MINDAUGAS LEIKA

2

MACROPRUDENTIAL POLICY FRAMEWORK

I. Macroprudential policy definition, targets, policy transmission channels and relationships with other policies (Monday)

II. Institutional structure (Tuesday)

III. Policy tools (Tuesday)

IV. Risk identification and quantification: stress testing (This lecture)

AGENDA

How to identify systemic risk: role of stress testing

Advances in systemic risk research and monitoring

3

4

WHERE IS STRESS TESTING? (I)

Data Availability

• National accounts data• Property prices data• Data on cross border exposures• Supervisory data: loan write offs, defaults• Financial soundness indicators• Meetings with financial institutions, surveys etc.

Financial stability analysis

• Risk identification and scenario design

• Financial stability review• Regional Financial Stability review• Stress testing• Early warning indicators

Risk mitigation policies

• Focus on more risky banks and financial institutions

• Dialog with financial institutions

• Macroprudential instruments

5

WHERE IS STRESS TESTING? (II)

Systemic Risk identification

Systemic Risk quantification

Macroprudential policy tools

Macro Stress testing

6

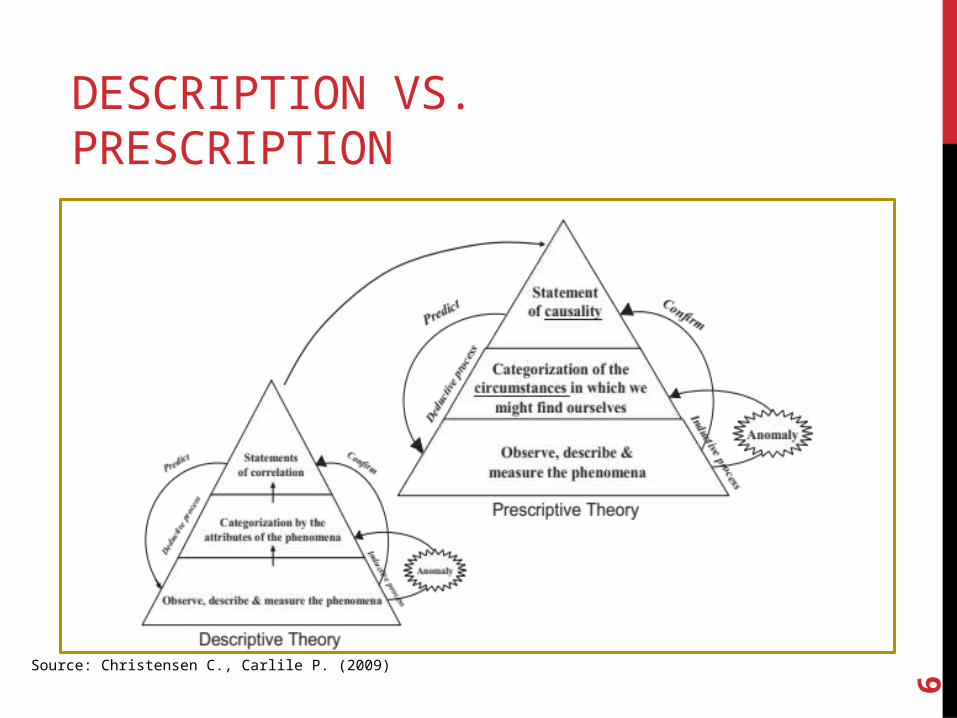

DESCRIPTION VS. PRESCRIPTION

Source: Christensen C., Carlile P. (2009)

7

STRESS TESTING CHALLENGES

-Data availability

-Data complexity

-Data relevancy

-Model uncertainty

-Scenario uncertainty

8

WHAT IS SYSTEMIC RISK?

Imbalances

Correlated exposures

Excessive exposures

Spillovers to the real economy

Disruption of financial transactions, flow of funds

Capital flight

Bubbles, contagion

Bank closures

Various studies offer different measures of risk. However, what is relevant in one country might not be relevant in another one, and this is especially important in Africa: various advanced tools might be too premature to be employed.Many studies provide a good description of what happened in the past, but can they predict the future?

9

IDENTIFICATION: METRICSA. Lo at all (2012) provides an extensive list of various systemic risk measures and data requirements:

-Macroeconomic: asset price bubbles, credit, investment cycles; macroprudential regulation

-Granular and Network measures: default intensity, network analysis and systemic financial linkages; scenario analysis; risk and shock transmission; mark-to-market accounting and liquidity pricing;

-Forward looking risk measures: Contingent claim analysis, multivariate density estimation, housing sector simulations, principal component analysis etc.

-Stress test measures: macro stress tests

-Cross-Sectional Measures: CoVaR, expected shortfall etc.

-Illiquidity and insolvency: risk topography, leverage cycle, crowded trades, hedge fund trades etc.

10

IDENTIFICATION: DATA (1)

Asset price boom/bust cycles:

-National statistics and/or international data sources: IMF International Financial Statistics

-Macroeconomic indicators: national statistics office, national accounts data (e.g. financial accounts)

Bank funding risk and shock transmission:

-BIS locational banking statistics;

-Bank surveys (on financing terms); deposit statistics (interest rates);

-Refinancing schedule (timing of bonds to be redeemed, loans repaid etc.);

-Data on covenants (e.g. repayment obligation link with credit rating).

11

Corporate and consumer indebtedness:

- Banks’ proprietary data; credit register (both positive and negative ones);

- National accounts statistics: corporate and household leverage ratios;

Contingent claim analysis:

- Moody’s KMV, Bloomberg, MarkIt; CDS spreads;

CoVaR, currency trades, insurance premiums, etc.

- Market data, various service providers: Bollomberg, Reuters Datastream, Moody’s, S&Ps etc. However, in many cases this is not very relevant for African countries (dominated by plain vanilla banks), as many instruments are not available in local markets.

Identification: data (2)

12

RECOMMENDATIONS

Avoid “Sophistication trap”, i.e. the more sophisticated analysis is, the more credibility it has. This is wrong approach, especially in countries where simple financial systems dominate. Avoid sophisticated models, if data is not reliable and even not available.

Concentrate on data availability and timing issues: simple ratios can tell much more, than distance to default or first principal component.

Try to build simple models and for systemic risk, create network of individual exposures, observe common patterns.

13

EXAMPLE: FROM INDIVIDUAL BANK RUN TOWARDS SYSTEMIC CRISIS

14

INDIVIDUAL BANK RUN (1)As soon as even a small fraction of deposits is channeled towards illiquid assets (long-term loans, investments etc.) every bank won’t be able to meet its obligations towards creditors (depositors), hence there is always a risk of liquidity crisis.

Imagine, that we have a three period game: deposit D is placed at t=0 and can be withdrawn at t=1 (impatient depositors) and t=2 (patient depositors). Bank invest deposits into long term assets that yield rate of return R. R>1 at time period t=2, however R<1 at time period t=1. Hence, if bank needs to liquidate investment before it matures, it makes a loss (R<1) (e.g. fire-sale of assets). If bank knows the proportion of depositors who are impatient and withdraw at time t=1, it invests D share of deposits into liquid assets and (1- )D share of deposits into less liquid (long-term) assets.

15

INDIVIDUAL BANK RUN (2)

This system is called a Fractional Reserve Banking system. In practice, banks need to make their own liquidity forecasts to obtain , or stick to minimum reserve and liquidity requirements imposed by regulators.

This system works well, if is stable, however is is higher than anticipated, the bank will have to liquidate higher proportion of assets under depressed prices and suffer loss. If this happens, patient depositors realize, that they won’t be able to get back their deposits at time t=2 in full amount. Bank run in this case is a rational strategy; depositors’ expectations are self-fulfilling.

Of course, there is a case when R is much higher than 1, so higher might not necessarily lead to bank liquidation.

16

INDIVIDUAL BANK RUN (3)These assumptions were incorporated in the classical Diamond-Dybvig framework.

If depositors type is observed, it is possible to prohibit early withdrawal (contract design or by law); otherwise banks need to rely on historical observations. However a lack of confidence in a given bank would lead to a coordination failure among depositors. Hence, the bank needs to obtain liquidity in the market and/or from a central bank or liquidate investments.

If interbank market is functional and liquidity needs are bank specific rather than system, bank might be able to obtain liquidity by borrowing. It is also possible, that the bank simply securitizes its long-term assets (the case of Northern Rock).

Due to inter-linkages among banks, other financial institutions, payment and settlement systems etc. individual bank run might lead to the general loss of confidence in the banking system and as a result – systemic crisis.

Alternative solutions: suspension of convertibility (also “bank holidays”), deposit insurance, debt-equity swap.

17

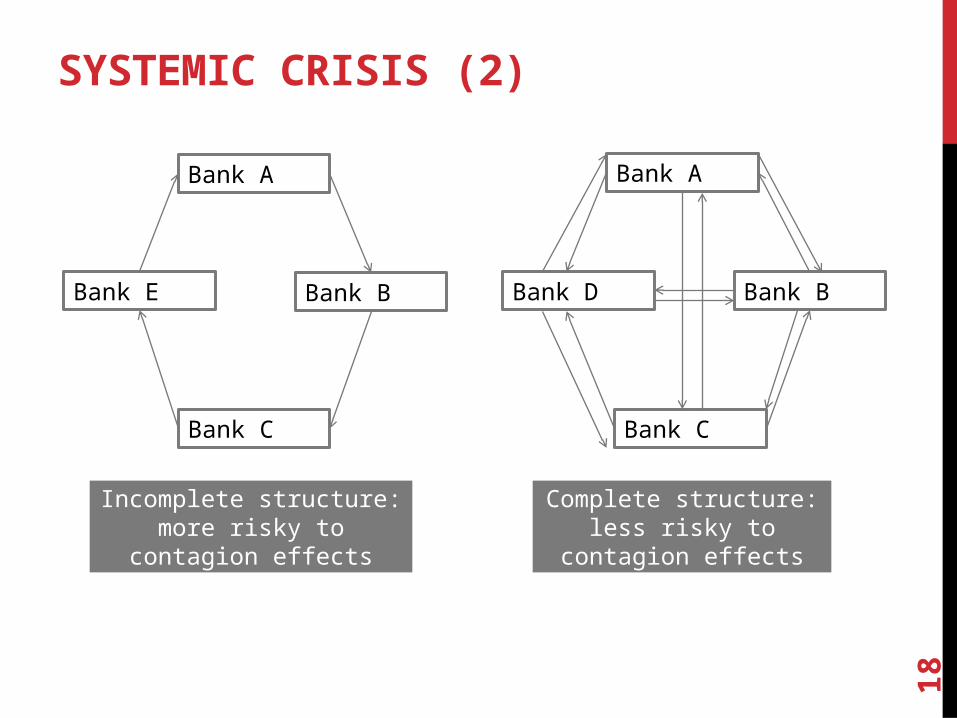

SYSTEMIC CRISIS (1)Due to inter-linkages among banks, other financial institutions, payment and settlement systems etc. individual bank run might lead to the general loss of confidence in the banking system and as a result – systemic crisis.

Systemic crisis can be triggered via system of cross-holdings among banks.

Market topology is important: a system where each bank borrows from one or several banks is more fragile than a more diversified interbank system.

18

SYSTEMIC CRISIS (2)

Bank A Bank A

Bank E Bank D

Bank C

Bank B Bank B

Bank C

Incomplete structure: more risky to contagion effects

Complete structure: less risky to contagion effects

19

ORIGINS OF LIQUIDITY SHOCKS

Market eventsCross-border contagionLoss in confidenceSpeculations (rumors)Interbank contagion

Credit lossesOperational lossesChange in investors expectationsRating downgrade

Liquidity ratio below thresholdNegative cash flow

20

VICIOUS CIRCLE

1. Run on a bank

2. Liquidity crisis

3. Interbank interest rates, Real interest rate

4. Assets value, market prices

21

STRESS IN THE FEDWIRE

Source: Bech M. et all (2009)

22

ADVANCES IN SYSTEMIC RISK RESEARCH AND MONITORING

23

FROM INDIVIDUAL RISK TO SYSTEMIC RISK

Systemic risk

Bank C

Bank B

BankA

Most of the studies before the GFC focused on individual or firm level risks: VaR, portfolio concentration, diversification, credit ratings etc. There were studies on joint probability of default, but not on bank, but firm level

SR studies flourished during this crisis: CoVaR,measures of interconnectedness, spillover effects, risk transmission,deleveraging etc.

24

STUDIES (1)IMF Cross-Border contagion model. Utilizes BIS statistics and uses Input-Output type of matrices of cross-border exposures. http://www.imf.org/external/np/pp/eng/2010/090110.pdf

Adrian, Brunnermeier (2009) CoVaR. Co means: conditional, contagion, comovement. It is VaR of the whole financial sector conditional on institution i being in distress. http://www.princeton.edu/~markus/research/papers/CoVaR.pdf

Information cascades and Big data analytics. Abreu, Brunnermeier (2003). http://www.princeton.edu/~markus/research/papers/bubbles_crashes.pdf

25

STUDIES (2)

Goodhart, Segoviano (2009). Banking Stability Measures. Measures distress dependence among banks. http://www.imf.org/external/pubs/ft/wp/2009/wp0904.pdf

Abbe, Khandani, Lo (2011) Privacy-Preserving Methods for Sharing Financial Risk Exposures. Data collection: how to obtain aggregate number without disclosing individual exposure? http://bigdata.csail.mit.edu/node/23

26

EXAMPLE: REAL ESTATE LINKED LOANS (1)

Source: Abbe, Khandani, Lo (2011)

27

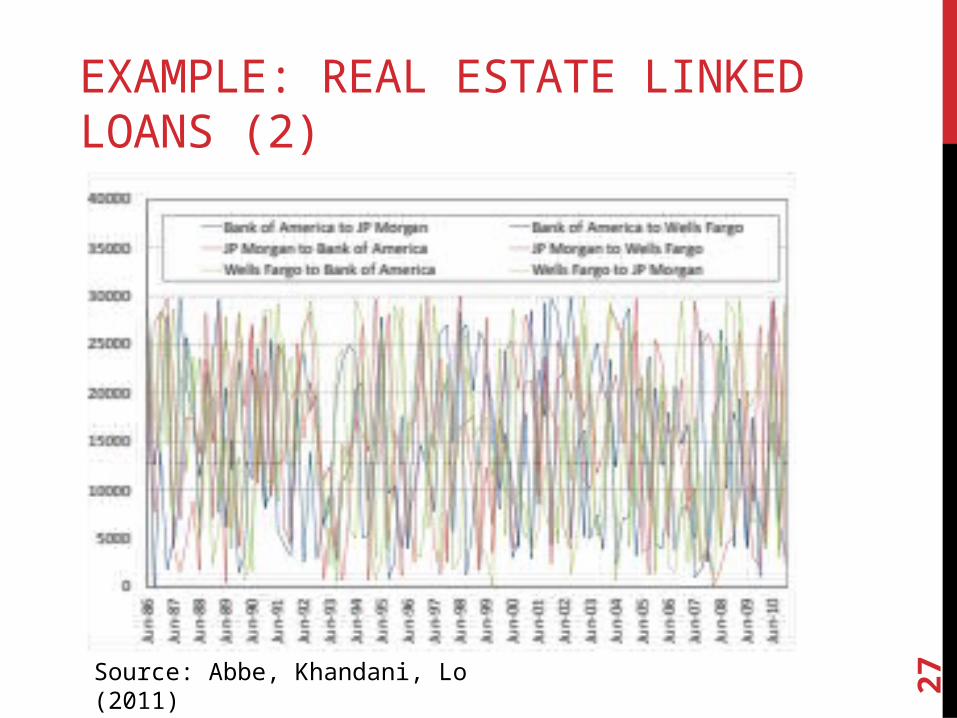

EXAMPLE: REAL ESTATE LINKED LOANS (2)

Source: Abbe, Khandani, Lo (2011)

28

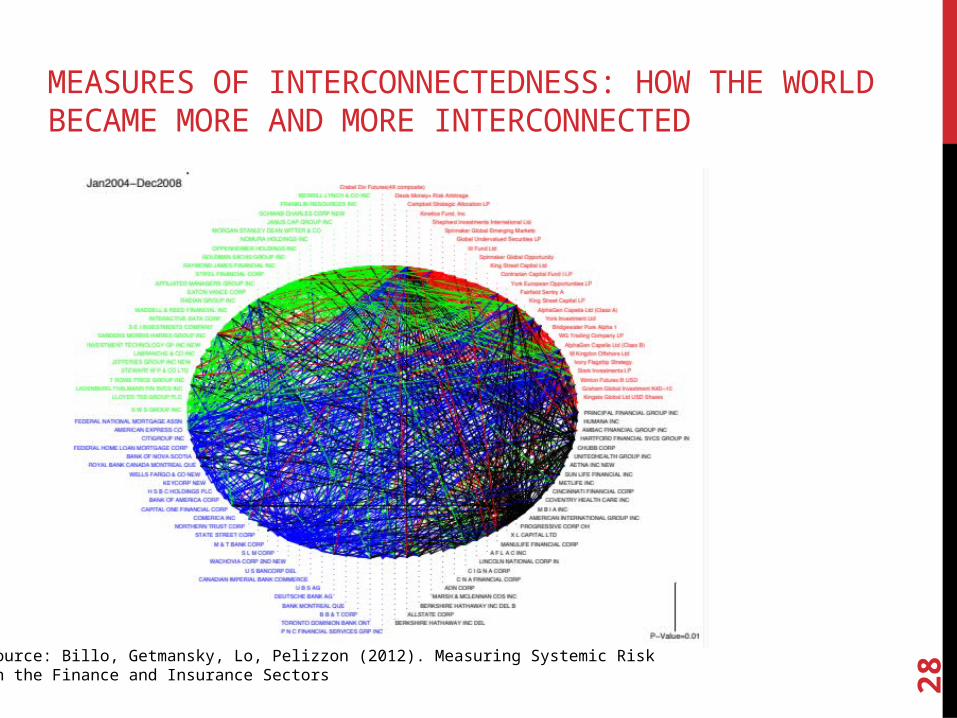

MEASURES OF INTERCONNECTEDNESS: HOW THE WORLD BECAME MORE AND MORE INTERCONNECTED

Source: Billo, Getmansky, Lo, Pelizzon (2012). Measuring Systemic Risk in the Finance and Insurance Sectors

Related Documents