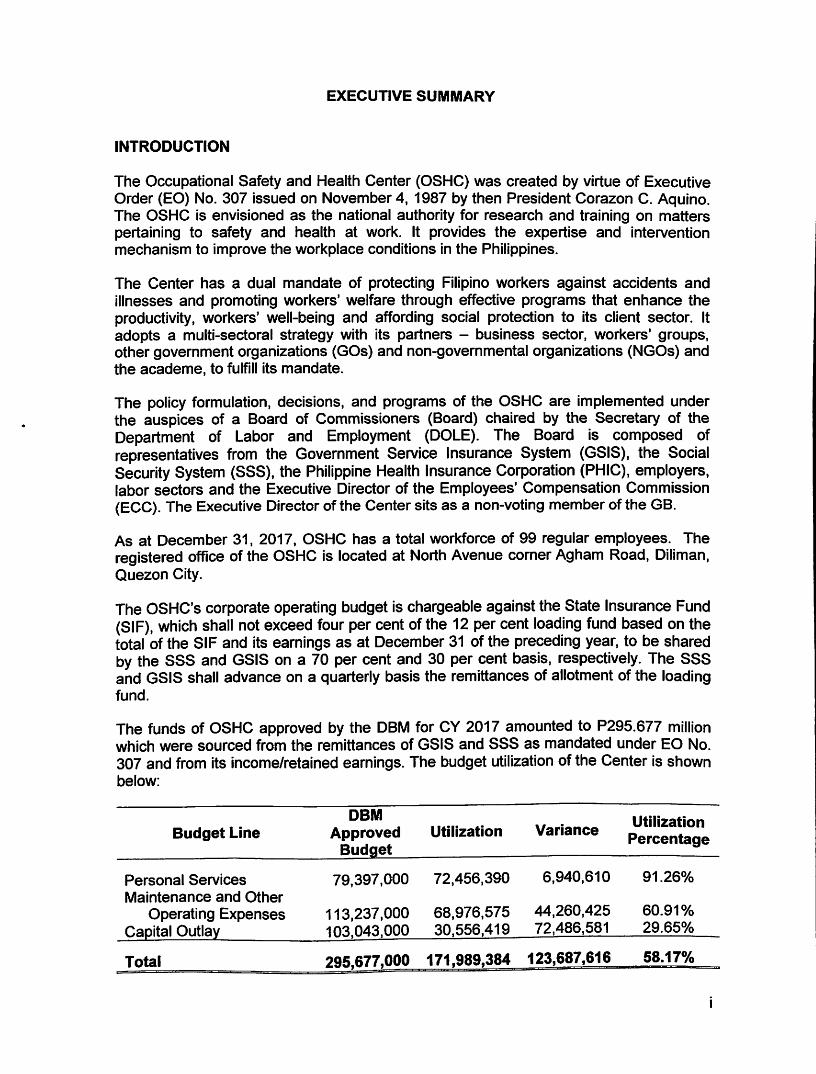

EXECUTIVE SUMMARY INTRODUCTION The Occupational Safety and Health Center (GSHO) was created by virtue of Executive Order (EO) No. 307 issued on November 4, 1987 by then President Corazon 0. Aquino. The OSHC is envisioned as the national authority for research and training on matters pertaining to safety and health at work. It provides the expertise and intervention mechanism to improve the workplace conditions in the Philippines. The Center has a dual mandate of protecting Filipino workers against accidents and illnesses and promoting workers' welfare through effective programs that enhance the productivity, workers' well-being and affording social protection to its client sector. It adopts a multi-sectoral strategy with its partners - business sector, workers' groups, other government organizations (GOs) and non-governmental organizations (NGOs) and the academe, to fulfill its mandate. The policy formulation, decisions, and programs of the OSHC are implemented under the auspices of a Board of Commissioners (Board) chaired by the Secretary of the Department of Labor and Employment (DOLE). The Board is composed of representatives from the Government Service Insurance System (GSIS), the Social Security System (SSS), the Philippine Health Insurance Corporation (PHIC), employers, labor sectors and the Executive Director of the Employees' Compensation Commission (ECC). The Executive Director of the Center sits as a non-voting member of the GB. As at December 31, 2017, OSHC has a total workforce of 99 regular employees. The registered office of the OSHC is located at North Avenue corner Agham Road, Diliman, Quezon City. The OSHC's corporate operating budget is chargeable against the State Insurance Fund (SIF), which shall not exceed four per cent of the 12 per cent loading fund based on the total of the SIF and its earnings as at December 31 of the preceding year, to be shared by the SSS and GSIS on a 70 per cent and 30 per cent basis, respectively. The SSS and GSIS shall advance on a quarterly basis the remittances of allotment of the loading fund. The funds of OSHC approved by the DBM for CY 2017 amounted to P295.677 million which were sourced from the remittances of GSIS and SSS as mandated under EO No. 307 and from its income/retained earnings. The budget utilization of the Center is shown below: Budget Line DBM Approved Budget Utilization Variance Utilization Percentage Personal Services Maintenance and Other Operating Expenses Capital Outlay 79,397,000 113,237,000 103.043.000 72,456,390 68,976,575 30,556,419 6,940,610 44,260,425 72.486,581 91.26% 60.91% 29.65% Total 295,677,000 171,989,384 123,687,616 58.17%

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

EXECUTIVE SUMMARY

INTRODUCTION

The Occupational Safety and Health Center (GSHO) was created by virtue of ExecutiveOrder (EO) No. 307 issued on November 4, 1987 by then President Corazon 0. Aquino.The OSHC is envisioned as the national authority for research and training on matterspertaining to safety and health at work. It provides the expertise and interventionmechanism to improve the workplace conditions in the Philippines.

The Center has a dual mandate of protecting Filipino workers against accidents andillnesses and promoting workers' welfare through effective programs that enhance theproductivity, workers' well-being and affording social protection to its client sector. Itadopts a multi-sectoral strategy with its partners - business sector, workers' groups,other government organizations (GOs) and non-governmental organizations (NGOs) andthe academe, to fulfill its mandate.

The policy formulation, decisions, and programs of the OSHC are implemented underthe auspices of a Board of Commissioners (Board) chaired by the Secretary of theDepartment of Labor and Employment (DOLE). The Board is composed ofrepresentatives from the Government Service Insurance System (GSIS), the SocialSecurity System (SSS), the Philippine Health Insurance Corporation (PHIC), employers,labor sectors and the Executive Director of the Employees' Compensation Commission(ECC). The Executive Director of the Center sits as a non-voting member of the GB.

As at December 31, 2017, OSHC has a total workforce of 99 regular employees. Theregistered office of the OSHC is located at North Avenue corner Agham Road, Diliman,Quezon City.

The OSHC's corporate operating budget is chargeable against the State Insurance Fund(SIF), which shall not exceed four per cent of the 12 per cent loading fund based on thetotal of the SIF and its earnings as at December 31 of the preceding year, to be sharedby the SSS and GSIS on a 70 per cent and 30 per cent basis, respectively. The SSSand GSIS shall advance on a quarterly basis the remittances of allotment of the loadingfund.

The funds of OSHC approved by the DBM for CY 2017 amounted to P295.677 millionwhich were sourced from the remittances of GSIS and SSS as mandated under EO No.307 and from its income/retained earnings. The budget utilization of the Center is shownbelow:

Budget LineDBM

ApprovedBudget

Utilization VarianceUtilization

Percentage

Personal Services

Maintenance and Other

Operating ExpensesCapital Outlay

79,397,000

113,237,000103.043.000

72,456,390

68,976,57530,556,419

6,940,610

44,260,42572.486,581

91.26%

60.91%

29.65%

Total 295,677,000 171,989,384 123,687,616 58.17%

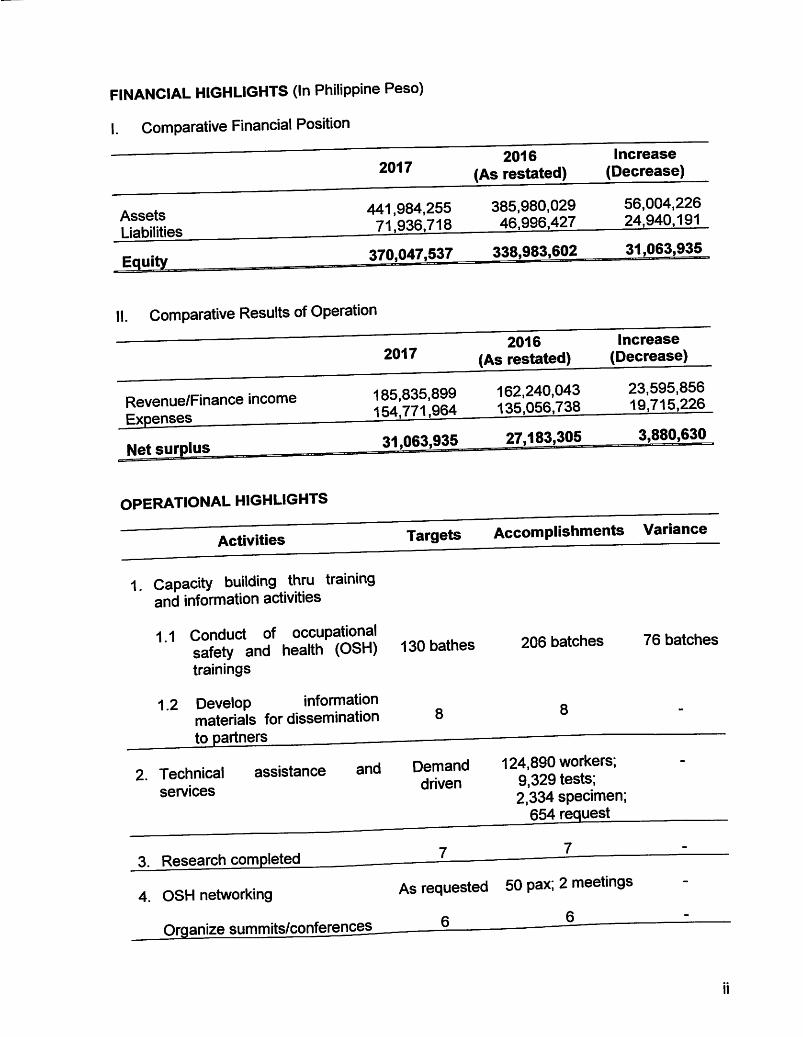

FINANCIAL HIGHLIGHTS (In Philippine Peso)

1. Comparative Financial Position

20172016

(As restated)Increase

(Decrease)

Assets

Liabilities

441.984.25571.936.718

385.980.02946.996.427

56.004.22624.940.191

Equity370,M7,537 _ 338j983j602 31.063.935

II. Comparative Results of Operation

Revenue/Finance incomeExpenses

Net surplus

2017

185,835,899154.771.964

31,063.935

2016

(As restated)

162.240.043135.056.738

27.183.305

Increase

(Decrease)

23.595.85619.715.226

3.880.630

Targets Accomplishments Variance

OPERATIONAL HIGHLIGHTS

Activities

1 Capacity building thru trainingand information activities

1 1 Conduct of occupationalsafety and health (OSH) 130 bathestrainings

206 batches 76 batches

information1.2 Developmaterials for disseminationto partners

Demand

driven2. Technical

services

assistance124.890 workers;

9,329 tests;2.334 specimen;654 request

3. Research completed

As requested 50 pax; 2 meetings4. OSH networking

Organize summits/conferences

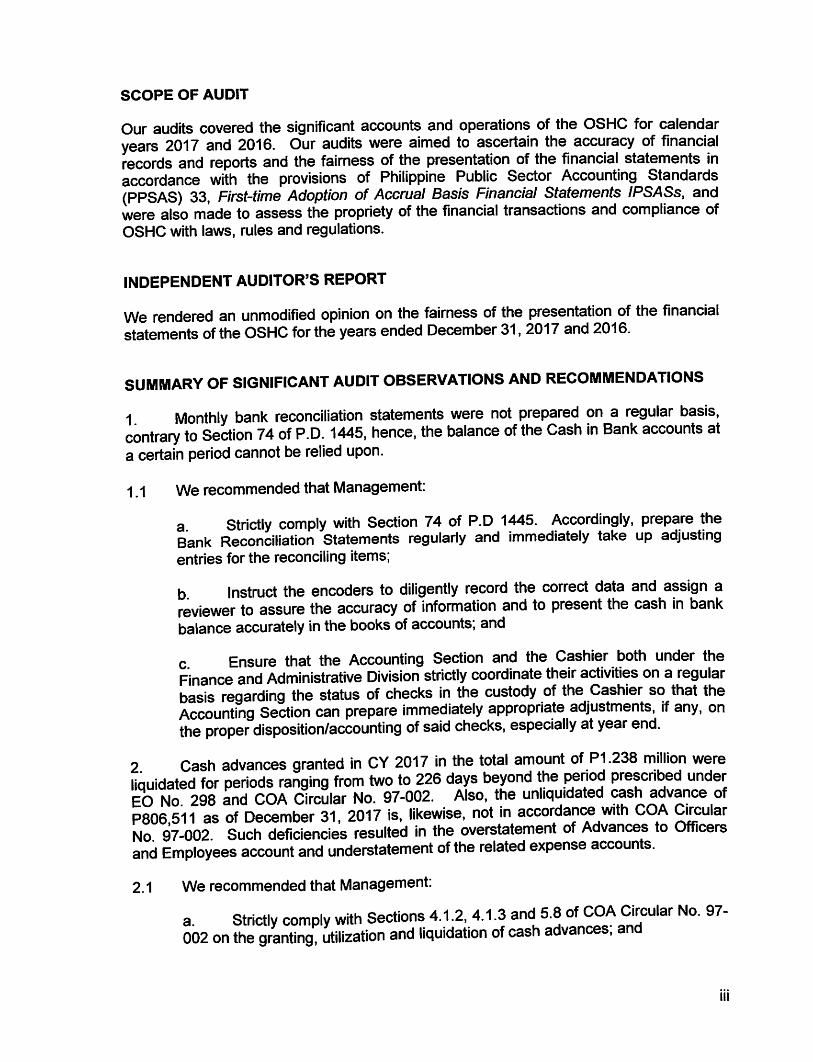

SCOPE OF AUDIT

Our audits covered the significant accounts and operations of the GSHO for calendaryears 2017 and 2016. Our audits were aimed to ascertain the accuracy of financialrecords and reports and the fairness of the presentation of the financial statements inaccordance with the provisions of Philippine Public Sector Accounting Standards(PPSAS) 33, First-time Adoption of Accrual Basis Financial Statements IPSASs, andwere also made to assess the propriety of the financial transactions and compliance ofOSHO with laws, rules and regulations.

INDEPENDENT AUDITOR'S REPORT

We rendered an unmodified opinion on the fairness of the presentation of the financialstatements of the OSHO for the years ended December 31, 2017 and 2016.

SUMMARY OF SIGNIFICANT AUDIT OBSERVATIONS AND RECOMMENDATIONS

1 Monthly bank reconciliation statements were not prepared on a regular basis,contrary to Section 74 of P.D. 1445, hence, the balance of the Cash in Bank accounts ata certain period cannot be relied upon.

1.1 We recommended that Management;

a Strictly comply with Section 74 of P.D 1445. Accordingly, prepare theBank Reconciliation Statements regularly and immediately take up adjustingentries for the reconciling items;

b. Instruct the encoders to diligently record the correct data and assign areviewer to assure the accuracy of information and to present the cash in bankbalance accurately in the books of accounts; and

c Ensure that the Accounting Section and the Cashier both under theFinance and Administrative Division strictly coordinate their activities on a regularbasis regarding the status of checks in the custody of the Cashier so that theAccounting Section can prepare immediately appropriate adjustments, if any, onthe proper disposition/accounting of said checks, especially at year end.

2. Cash advances granted in CY 2017 in the total amount of PI .238 million wereliquidated for periods ranging from two to 226 days beyond the prescribed underEO No 298 and COA Circular No. 97-002. Also, the unliquidated cash advance ofP806,511 as of December 31, 2017 is, likewise, not in accordanc^ with COA ̂ cularNo. 97-002. Such deficiencies resulted in the overstatement of Advances to Officersand Employees account and understatement of the related expense accounts.

2.1 We recommended that Management:

a. Strictly comply with Sections 4.1.2, 4.1.3 and 5.8 of COA Circular No. 97-002 on the granting, utilization and liquidation of cash advances, ana

III

b. Limit the grant of cash advances for specific purpose and amount bebased on the approved activity/program budget to avoid the excess amountsubject to refund.

STATUS OF IMPLEMENTATION OF PRIOR YEARS' AUDIT RECOMMENDATIONS

Out of the 18 audit recommendations embodied in the prior years' Annual Audit Reports,12 were fully implemented, five were partially implemented and one were notimplemented. Details are presented in Part III of this Report.

IV

Republic of the PhilippinesCOMMISSION ON AUDIT

Commonweaith Avenue, Quezon City

INDEPENDENT AUDITOR^S REPORT

THE BOARD OF COMMISSIONERS

Occupational Safety and Health CenterNorth Avenue corner Agham RoadDiliman, Quezon City

Report on the Financial Statements

Opinion

We have audited the financial statements of Occupational Safety and Health Center(OSHC), which comprise the statements of financial position as at December 31, 2017and 2016, and the statements of financial performance, statements of changes in netassets/equity, statements of cash flows, statement of comparison of budget and actualamounts for the years then ended, and notes to the financial statements, including asummary of significant accounting policies.

In our opinion, the financial statements present fairly, in all material respects, thefinancial position of the OSHC as at December 31. 2017 and 2016, and its financialperformance and its cash flows for the years then ended in accordance with PhilippinePublic Sector Accounting Standards (PPSAS).

Basis for Opinion

We conducted our audits in accordance with International Standards of Supreme AuditInstitutions (ISSAIs). Our responsibilities under those standards are described in theAuditor's Responsibilities for the Audit of Financial Statements section of our report. Weare independent of the OSHC in accordance with the Code of Ethics for GovernmentAuditors in the Philippines (Code of Ethics) together with the ethical requirements thatare relevant to our audit of the financial statements, and we have fulfilled our otherethical responsibilities in accordance with these requirements and the Code of Ethics.We believe that the audit evidence we have obtained is sufficient and appropriate toprovide a basis for our opinion.

Responsibilities of Management and Those Charged with Governance for the FinancialStatements

Management is responsible for the preparation and fair presentation of the financialstatements in accordance with PPSAS, and for such internal control as Managementdetermines is necessary to enable the preparation of financial statements that are freefrom material misstatement, whether due to fraud or error. In preparing the financialstatements, Management is responsible for assessing the OSHCs ability to continue as

a going concern, disclosing, as applicable, matters related to going concern and usingthe going concern basis of accounting unless Management either intends to liquidate theOSHC or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the OSHC's financialreporting process.

Auditor's Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financialstatements as a whole are free from material misstatement, whether due to fraud orerror, and to issue an auditor's report that includes our opinion. Reasonable assuranceis a high level of assurance, but is not a guarantee that an audit conducted inaccordance with ISSAIs will always detect a material misstatement when it exists.Misstatements can arise from fraud or error and are considered material if, individually orin the aggregate, they could reasonably be expected to influence the economicdecisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISSAIs, we exercise professional judgment andmaintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial statements,whether due to fraud or error, design and perform audit procedures responsive tothose risks, and obtain audit evidence that is sufficient and appropriate to provide abasis for our opinion. The risk of not detecting a material misstatement resultingfrom fraud is higher than for one resulting from error, as fraud may involve collusion,forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to designaudit procedures that are appropriate in the circumstances, but not for the purposeof expressing an opinion on the effectiveness of the OSHC's internal control.

• Evaluate the appropriateness of accounting policies used and the reasonablenessof accounting estimates and related disclosures made by Management.

• Conclude on the appropriateness of the Management's use of the going concernbasis of accounting and, based on the audit evidence obtained, whether a materialuncertainty exists related to events or conditions that may cast significant doubt onthe OSHC's ability to continue as a going concern. If we conclude that a materialuncertainty exists, we are required to draw attention in our auditor's report to therelated disclosures in the financial statements or, if such disclosures areinadequate to modify our opinion. Our conclusions are based on the audit evidenceobtained up to the date of our auditor's report. However, future events or conditionsmay cause the OSHC to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial statements,including the disclosures, and whether the financial statements represent theunderlying transactions and events in a manner that achieves fair presentation.

We communicated with those charged with governance regarding, among other matters,the planned scope and timing of the audit and significant audit findings, including anysignificant deficiencies in internal control that we identify during our audit.

Report on Other Legal and Regulatory Requirements

Our audits were conducted for the purpose of forming an opinion on the basic financialstatements taken as a whole. The supplementary information for the year endedDecember 31, 2017 required by the Bureau of Internal Revenue as disclosed in Note 20to the financial statements is presented for purposes of additional analysis and is not arequired part of the basic financial statements prepared in accordance with PPSAS.Such supplementary information is the responsibility of Management. Thesupplementary information has been subjected to the auditing procedures applied in theaudit of the basic financial statements.

COMMISSION ON AUDIT

ELIZABETH M. SAVELLA

Supervising Auditor

June 28, 2018

OSHC

Republic of the PhilippinesDEPARTMENT OF LABOR AND EMPLOYMENTOCCUPATIONAL SAFETY AND HEALTH CENTER

Wowoi-Jww

! TOvnit^nwal i

STATEMENT OF MANAGEMENTS RESPONSIBILITYFOR FINANCIAL STATEMENTS

TTie management of OCCUPATIONAL SAFETY AND HEALTH CENTER (OSHC) isresponsible for the preparation and fair presentation of the financial statementsincluding the schedules attached therein, for the years ended December 31, 2017 andDecember 31, 2016 in accordance with tfie prescribed financial reporting ftameworkindicated therein, and for such internal control as management determines is necessaryto enable the preparation of financial statements that are free from materialmisstatement, whether due to fraud or error

In preparing the financial statements, management is responsible for assessing theOCCUPATIONAL SAFEFY AND HEALTH CENTER'S ability to continue as a goingconcern, disclosing, as applicable, matters related to going concern and using the goingconcern basis of accounting unless management either intends to RquklateOCCUPATIONAL SAFETY \ND HEALTH CENTER or to cease operations, or has norealistic attemative to do so.

The Board of Commissioners is responsible for overseeing the OCCUPATIONALSAFETY AND HEALTH CENTER'S financial reporting process.

The Board of Commissioners reviews and approves tie financial statements, including' the scfiedules attadied ttierein, and submits the same to the stocKtiolders or members.

The Commission on Audit, through its authorized representative, has examined thefinancial statements of the OSHC pursuant to Section 2, Article IX-D of the PhilippineConstitution and Section 28 of the Presidential Decree No. 1445, otherwise known asthe Government Auditing Code of the Philippines. The audit was corrducted inaccordance wifti the Intemalional Standards of Supreme Audit Institutions and theaudKor, in its report to the stockholders or members, has expressed its opinion on thefairness of presentation upon completion of such audit.

CIRIACO A. LAGOIKAD IIICHairman - Altemme

^J^K&^nag, ce^j^e^tive Director

RtYA-ESHLLOREC^ief, Finance and Administretive Division

Signed this 22™* day of June 2018

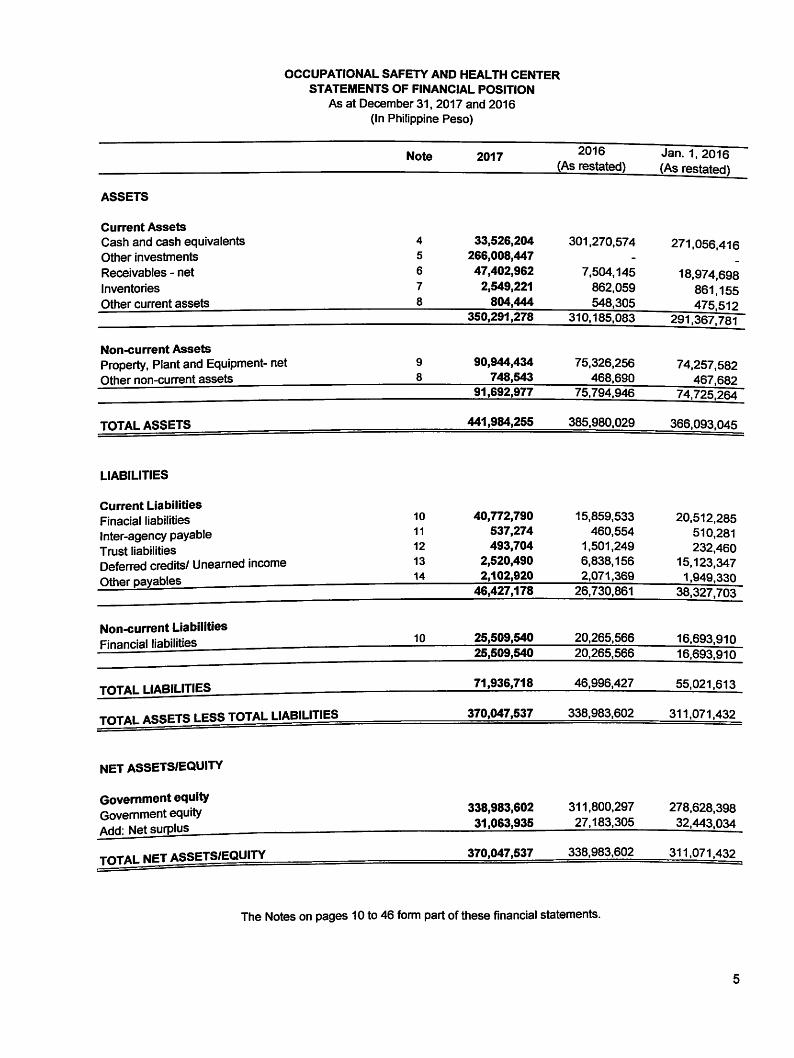

OCCUPATIONAL SAFETY AND HEALTH CENTER

STATEMENTS OF FINANCIAL POSITION

As at December 31, 2017 and 2016

(In Philippine Peso)

Note 20172016

(As restated)Jan. 1, 2016

(As restated^

ASSETS

Current Assets

Cash and cash equivalents

Other investments

Receivables - net

Inventories

Other current assets

4

5

6

7

8

33,526,204

266,008,447

47,402,962

2,549,221

804,444

301,270,574

7,504,145

862.059

548,305

271,056,416

18,974,698861,155475.512

350,291,278 310,185,083 291,367.781

Non-current Assets

Property, Plant and Equipment- netOther non-current assets

9

8

90,944,434

748,54375,326,256

468,69074,257.582

467.68291,692,977 75.794,946 74.725.264

TOTAL ASSETS 441,984,255 385,980,029 366,093.045

LIABILITIES

Current Liabilities

Finacial liabilities

Inter-agency payableTrust liabilities

Deferred credits/ Unearned incomeOther pavables

10

11

12

13

14

40,772,790

537,274

493,704

2,520,490

2,102,920

15,859,533

460,554

1,501,249

6,838,156

2,071,369

20,512,285510,281

232,460

15,123,3471,949.330

46,427,178 26,730,861 38,327.703

Non-current Liabilities

Financial liabilities10 25,509,540 20,265,566 16,693,910

25,509,540 20,265,566 16,693.910

TOTAL LIABILITIES71,936,718 46,996,427 55,021,613

TOTAL ASSETS LESS TOTAL LIABILITIES 370,047,537 338,983,602 311,071,432

NET ASSETS/EQUITY

Government equityGovernment equityAdd: Net surplus

338,983,602

31,063,935

311,800,297

27,183,305278,628.39832,443.034

t^tai MPT assets/equity 370,047,537 338,983,602 311,071,432

The Notes on pages 10 to 46 form part of these financial statements.

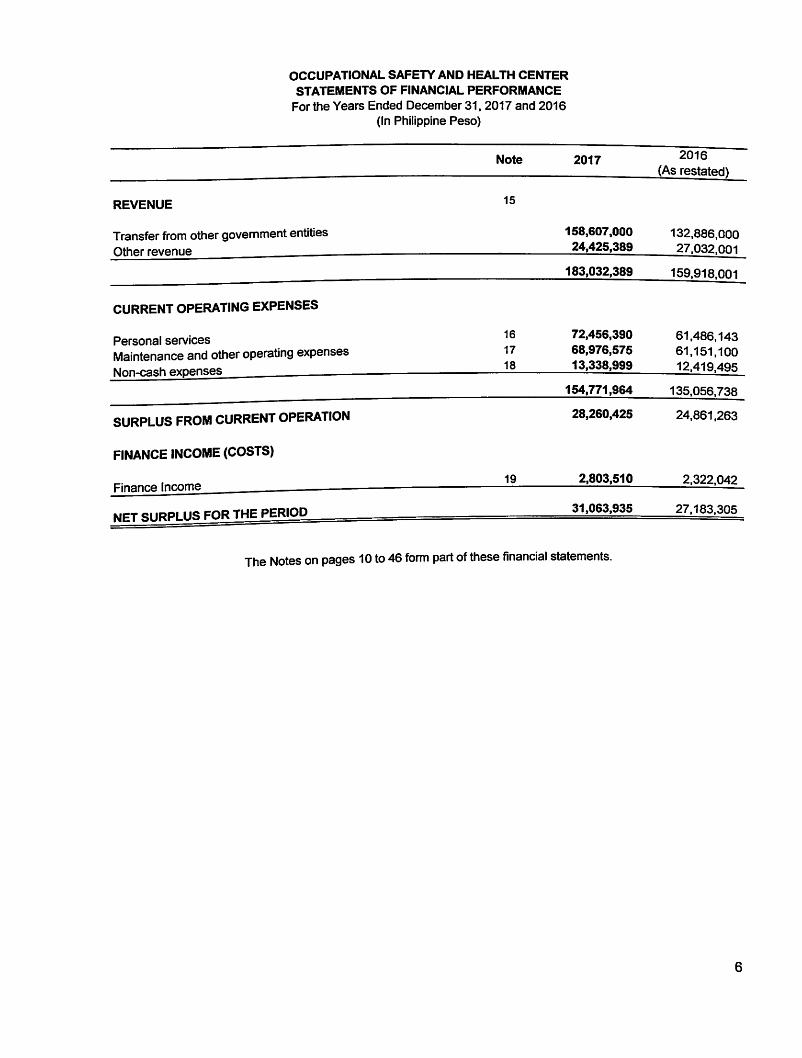

OCCUPATIONAL SAFETY AND HEALTH CENTER

STATEMENTS OF FINANCIAL PERFORMANCE

For the Years Ended December 31,2017 and 2016

(In Philippine Peso)

Note 2017 2016

(As restated)

REVENUE 15

Transfer from other government entitiesOther revenue

158,607,000

24,425,389132.886.000

27.032.001

183,032,389 159.918.001

CURRENT OPERATING EXPENSES

Personal services

Maintenance and other operating expensesNon-cash expenses

16

17

18

72,456,390

68,976,575

13,338,999

61.486.143

61.151.100

12.419.495

154,771,964 135.056.738

SURPLUS FROM CURRENT OPERATION 28,260,425 24.861.263

FINANCE INCOME (COSTS)

Finanre Income19 2,803,510 2.322,042

NET SURPLUS FOR THE PERIOD31,063,935 27.183.305

The Notes on pages 10 to 46 form part of these financial statements.

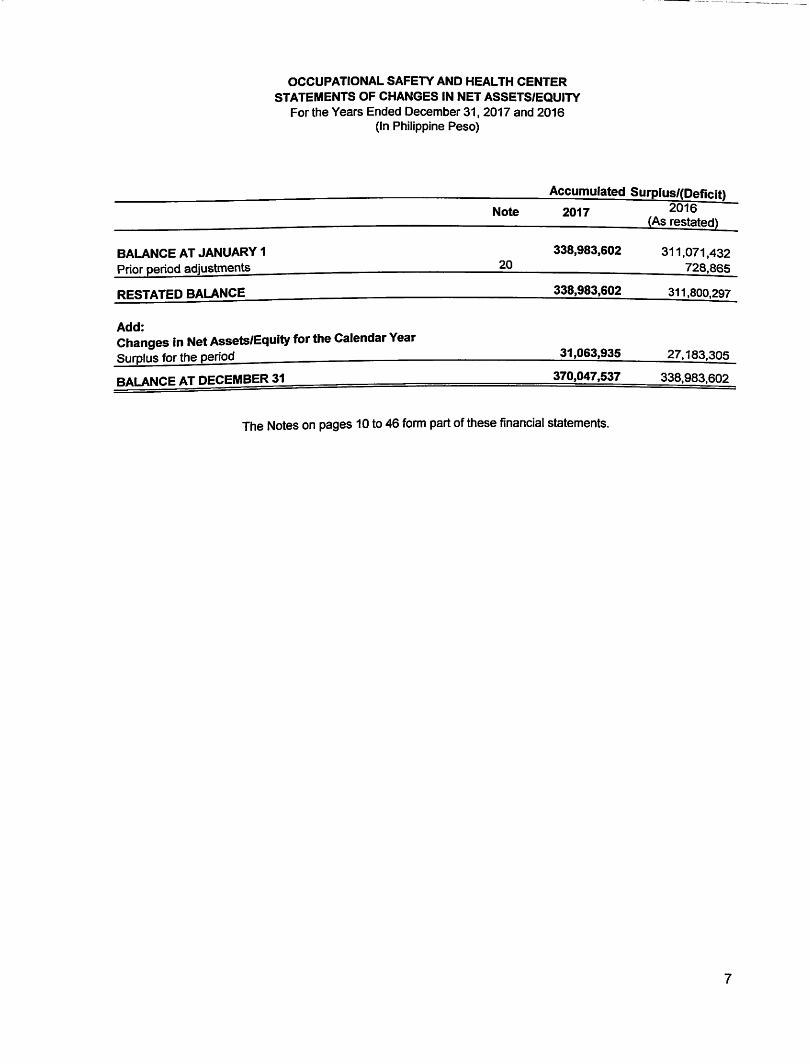

OCCUPATIONAL SAFETY AND HEALTH CENTER

STATEMENTS OF CHANGES IN NET ASSETS/EQUITY

For the Years Ended December 31,2017 and 2016(In Philippine Peso)

Note 2017 2016

(As restated)

BALANCE AT JANUARY 1

Prior period adjustments 20

338,983,602 311.071,432728.865

RESTATED BALANCE 338,983.602 311,800,297

Add:

Changes In Net Assets/Equity for the Calendar YearSurplus for the period 31,063,935 27,183.305

BALANCE AT DECEMBER 31 370,047,537 338,983.602

The Notes on pages 10 to 46 form part of these financial statements.

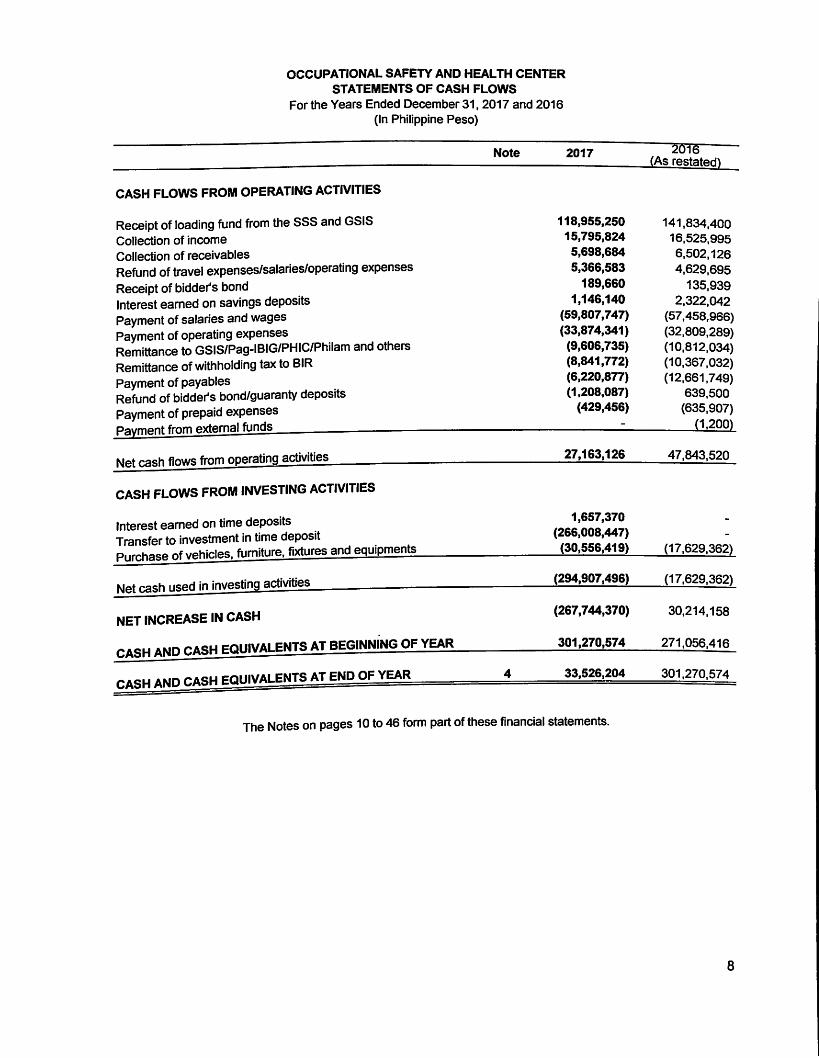

OCCUPATIONAL SAFETY AND HEALTH CENTER

STATEMENTS OF CASH FLOWS

For the Years Ended December 31, 2017 and 2016(In Philippine Peso)

Note 2017 20T6(As restated)

CASH FLOWS FROM OPERATING ACTIVITIES

Receipt of loading fund from the SSS and GSISCollection of income

Collection of receivables

Refund of travel expenses/salaries/operating expensesReceipt of bidder's bondInterest earned on savings depositsPayment of salaries and wagesPayment of operating expensesRemittance to GSIS/Pag-IBIG/PHIC/Philam and othersRemittance of withholding tax to BIRPayment of payablesRefund of bidder's bond/guaranty depositsPayment of prepaid expenses

118,955,250

15,795,824

5,698,684

5,366,583

189,660

1,146,140

(59,807,747)

(33,874,341)

(9,606,735)(8,841,772)(6,220,877)(1,208,087)

(429,456)

141,834,40016,525,995

6,502,126

4,629,695

135,939

2,322,042(57,458,966)(32,809,289)(10,812,034)(10,367,032)(12,661,749)

639,500

(635,907)

rayiiiciii nwn — —

Net cash flows from operating activities^27,163,126 47,843,520

CASH FLOWS FROM INVESTING ACTIVITIES

Interest earned on time depositsTransfer to investment in time depositPurchase of vehicles, furniture, fixtures and equipments

1,657,370

(266,008,447)(30,556,419) (17,629,362)

Net cash used in investing activities(294,907,496) (17,629,362)

NET INCREASE IN CASH(267,744,370) 30,214,158

CASH AND CASH equivalents AT BEGINNING OF YEAR301,270,574 271,056,416

CASH AND CASH EQUIVALENTS AT END OF YEAR4 33,526,204 301,270,574

The Notes on pages 10 to 46 form part of these financial statements.

OCCUPATIONAL SAFETY AND HEALTH CENTER

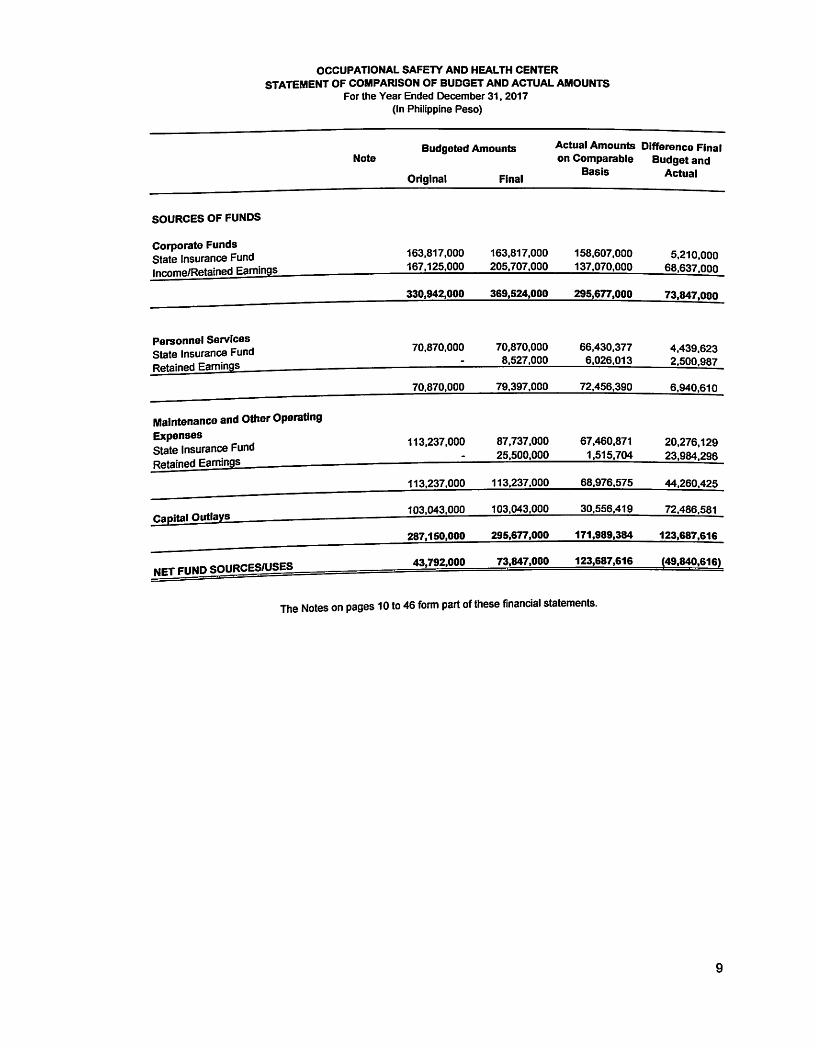

STATEMENT OF COMPARISON OF BUDGET AND ACTUAL AMOUNTSFor the Year Ended December 31, 2017

(In Philippine Peso)

NoteBudgeted Amounts

Original Finai

Actual Amounts Difference Finalon Comparable Budget and

Basis Actual

SOURCES OF FUNDS

Corporate FundsState Insurance Fundinmme/Retained Earnings

163.817,000

167,125,000

163,817,000

205,707,000

158,607,000

137,070,0005,210,000

68,637.000

330,942,000 369,524,000 295,677,000 73,847.000

Personnel ServicesState Insurance FundRetained Earnings

70,870.000 70,870,000

8,527,000

66,430,377

6,026,0134,439,623

2,500,987

70,870,000 79,397,000 72,456,390 6,940,610

Maintenance and Other OperatingExpenses

State Insurance FundRetained Earnings

113,237,000 87,737,000

25,500,000

67,460,871

1,515,704

20,276,129

23,984,296

113,237,000 113,237,000 68,976,575 44,260,425

Capital Outlays103.043,000 103,043,000 30,556,419 72,486,581

287.150.000 295,677,000 171,989,384 123,687,616

NET FUND^OB^^^^y£l^^=43,792,000 73,847,000 123,687,616 (49,840,616)

The Notes on pages 10 to 46 form part of these financial statements.

Related Documents

![02_POEA Casco - MLC-OSHC [Compatibility Mode]](https://static.cupdf.com/doc/110x72/54636c41b4af9f531c8b4c45/02poea-casco-mlc-oshc-compatibility-mode.jpg)