WEALTH MANAGEMENT Eyes Wide Open CIO Office Investment Outlook 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

WEALTH MANAGEMENT

Eyes Wide Open

CIO OfficeInvestment Outlook 2018

OPPORTUNITIES TO INSPIRE 1

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

2017 Disruption and Rally

We began 2017 with a thematicfocus on disruption: an insightfulplay but wholly underestimatedacross the board.

It is now clear that 2017 markedsome of the most significant, tangibleand transformational disruptions wehave seen in over fifty years. Frompolitics to economics, nothing wasexempt.

While the past decade heralded theTech Age, 2017 was truly thebreakout year for disruptivetechnology. Traditional industrieswere put in defence mode. Financefor example, a sector previouslycoddled as untouchable, had tocompete with the onslaught ofinnovative technology: fromblockchain to digital asset managers,finance as we once knew it hasforever changed.

At the forefront of this disruption isthe human experience: frombanking to shopping, politics topersonal, Amazon to AI; TechnologyLiving is now the new normal.

With such momentous changecomes empowerment; the previouslyunheard voices arise, and the powershifts. The rise of nationalism inEurope and the surge of populism inthe US saw the greatest disruptionto the status quo in decades.

Nowhere was this change morepalpable in the GCC than in SaudiArabia, where historic social changeis afoot, and political power isevolving in line with an increasinglydiversifying economy and theconcentration of the youthdemographic. Critically, it was thisyouth demographic - the millennials

globally - which drove overwhelmingchange in 2017.

From Austria to Australia, SaudiArabia to South Africa, millennialsare now having their say inGovernment and making theirinfluence known.

2017 witnessed the EmergingMarkets (EM), particularly India, risefrom the shadows of the traditionallyfavoured Developed Markets (DM).EM economies held their own in2017, with most outperforming theirDM counterparts on multiple fronts.

The widely anticipated negativeeffect of a Trump presidency did notin fact materialize and marketsglobally reacted positively to aRepublican reformist taking office.

Global debt, however, continues torise and is now at record levels –more than 325% of global GDP.This is in part due to central bankpolicies after the 2008 recession,but at these levels, central banksare likely to start reining in thisliquidity with the inevitable resultingtension in global markets.

2018 Conviction and Persistence

We start 2018 with a healthy dose ofoptimism: cautious optimism. The2018 investor must be discerning,focused, agile and adaptable. Theyear of rallying returns off the back ofcomplacent investing is behind us.

That said, provided the rightconditions are met, we do expectcertain markets to have robust yearsahead. India and Saudi Arabiaremain our favourite markets from amulti-asset-rally perspective. Bothcountries are driving changes thatwill have significant global impact.

If Modi can wrestle command of theIndian Government in the upcomingelections, and oil remains below USD65/b, this should allow him tocontinue to reform and boost theIndian economy further.

For Saudi Arabia, we would expectpositive performance in both bondsand equities alongside theanticipated MSCI upgrade andcontinued focus on social andeconomic reform. A rally in theKingdom would also enhanceperformance in the UAE andBahrain.

We intend to remain overweightequities for the first half of 2018 andwill continue to focus on thetechnology sector, which presentssubstantial upside opportunity. USand Indian equities continue to haveour particular attention.

US equities have experiencedremarkable returns over the pastdecade and are now on course forthe longest positive streak everrecorded. We do, however, expectan increase in volatility as theimpact of multiple fed rate increases(albeit from historically record lows)take hold, and the inevitable “soul-searching” in the latter half of theyear hits as the benefits of taxreform and healthy economic databegin to wane.

Indian equities should continue tooutperform DM and EM, even withthe substantial rally in corporatevaluations over the past twelvemonths.

For the bond market, it is a tale oftwo halves: we expect DM bonds tocontinue to deliver negative to flatreturns and for EM bonds tocontinue to deliver alpha.

CIO Statement

Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

GCC bonds present opportunities asthe benefits of recent reforms andthe relatively neutral performanceover the past 12 months signal anupward trend. US Governmentbonds remain appealing and webelieve that they may sustain arange of 2.5% to 2.75%.

EM debt is appealing and our focusis on the UAE, India, China,Indonesia, Russia, Mexico, Turkeyand the KSA.

Blockchain technology andcryptocurrencies have theinvestment community divided.Blockchain encompasses the veryessence of disruptive technology;while it has certainly changed theway that certain industries dobusiness, as it relates tocryptocurrencies, its potential todisplace fiat currencies remains thecreed of the crypto believers. Thelack of regulation and resultantinability to “cash-out” on anymeaningful scale into fiat currencylimits cryptocurrency utilisation tothe “pump-and-dump” price arbitragingjaunts in a virtual world. For now.

It remains to be seen whethercryptocurrencies can in factpenetrate real economies and indoing so, compel governments andregulators to adapt.

With US corporates expected to seesignificant surpluses in light of taxreform, the US dollar is expected to

continue its slide against the euroand GBP. GBP, albeit still exposed tothe uncertainty of the Brexit outcome,may etch close to USD 1.42.

With widespread uncertainty onthe strength and stability ofmarkets throughout 2018, holdinga position in gold is likely topreserve overall portfolio returnsand help mitigate against volatilityand potential shocks.

In the US, as fervor builds aroundSenate and Congressional electionsin Q4 2018, the US President willface a real challenge in securingRepublican command of bothHouses, and as a result, risksweakening his legislative agenda.

In Europe, Italians go to the polls inwhat could become a barometer forthe nationalist movement sweepingEurope. In Germany, Angela Merkelis expected to struggle to keep thecoalition together (at least in thebackground) which may spell anothergeneral election and a resultingtremble in the EU administration.

In the GCC, markets will look tosignals around continued reformand the Saudi Arabian MSCIupgrade, both of which shouldboost markets.

2018 will be an interesting year forinvestors; a year for steadfast focus,diversification and continuousconsidered scrutiny.

Tariq Bin Hendi, PhDActing Chief Investment Officer

OPPORTUNITIES TO INSPIRE 2Emirates NBD CIO-Office Year Ahead 2018

CIO Statement

OPPORTUNITIES TO INSPIRE

A Look Back on Our 2017 StrategiesTechnology was the winner in equity markets. EM assets performedacross all asset classes.

5GCC Macro Economic OutlookThe outlook for the GCC economies at the start of 2018 is constructive. 7Oil OutlookWe forecast Brent Oil Futures at an average of USD 56/b in 2018.8Equity Strategy Expect high single digit returns in the US and low teen returns in EMs.Synchronised global growth and upwards earning revisions aresupportive of equity performance. In the GCC, high yielding stocksremain in favour.

10

Equity Strategy – Emerging MarketsThe bulging young demographic is supportive of consumption. Asiahas the highest corporate profitability and economic growth globally.India and China remain the dominant economies.

17

3

Contents

Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

BlockchainThe decentralisation of transaction-linked information is the underpinning ofblockchain technology. It may prove to be the catalyst for change across globalindustries, from accounting to manufacturing.

23Fixed Income Strategy Finding value in a risk environment: despite tighter valuations across the fixedincome asset class, stretched valuations have become the norm with theabundance of liquidity.

25Portfolio Strategy Diversification benefits of traditional asset classes are limited. Alternativestrategies enhance a portfolios risk/return trade-off.

29UK Real Estate StrategyThe search for yield and excess liquidity is driving UK commercial propertyinvestment.

33Global Risks to Our 2018 OutlookWe outline the risks that may come to pass in 2018.35

Contents

OPPORTUNITIES TO INSPIRE 4Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

OPPORTUNITIES TO INSPIRE 5

A Look Back on Our 2017 Strategies

Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

We successfully executedour “sustainable business”investment strategy:“Only those companies that arecontinually evolving and recreatingtheir businesses will survive. Whatleads to a sustainable business?Companies need to invest andinnovate, to be environmentallyconscious and ethical, expand intonew markets and adopt disruptivetechnology.” (Source: Emirates NBDWealth Management InvestmentOutlook 2017)

Our Long Term DM SustainablePortfolio ended 2017 up 24.7% andto complement the 2017 strategywe will be launching a SustainableEquity Portfolio for EM in 2018.

Our 2017 Equity strategy was to:

Overweight the US, and thetechnology, industrials andfinance sectors: The S&P 500ended 2017 with total returns of21%, driven by the technologysector, with the semiconductorsector a stand out. 7 out of 12sectors in the Index returned over20%. The rally was paired withhistorically low volatility. Ouroverweight calls on US technology,finance, industrials and healthcarepaid off as did our underweight onconsumer staples and telecom. Thetechnology sector has not only beenthe highest gainer, but contributedto more than 40% of the gains in theS&P 500 Index.

Overweight EM:The MSCI EM Indexended 2017 up 34%. Our overweighton India has been unchanged for 3years, riding both the waves andfallouts from the demonetisation andGST implementation. The IndianSensex Index ended 2017 up 28%.

Overweight Europe exporters;underweight the UK:Though the strong euro was a drag,the Stoxx Eurozone Exporters Indexended 2017 up 9.8%, outperformingthe broader benchmark.

Neutral the GCC:Though oil prices rallied, the GCCmarkets did not keep pace with eitheroil or EM, ending 2017 flat (incl.dividends). Geopolitical concernsweighed on sentiment.

Underweight certain sectors: Brick and mortar retail, non–onlinepay TV, telecom and the traditionalauto (internal combustion engine)industries: as expected, these werethe laggards in 2017.

Sector Sustainability Driver

0% 10% 20% 30% 40% 50% 60%

GCC

Eurostoxx

Japan Nikkei

Healthcare

S&P 500

MSCI World

India Sensex

MSCI EM

Technology

Semiconductors

Robotics

Genomics

AI

Lithium

Exhibit 2: Our 2017 technology strategy yielded highest returns

Exhibit 1: Focused sectors and their key drivers

Source: Bloomberg. Dec 2017

Source: Emirates NBD CIO Office. Dec 2017

Innovative Healthcare R&D

Social media User base

Internet search Mobile ads

Robotics/ AI Industrial use

Ecommerce AI

Digital banking Big data

Global payments EM

Health “Wellness"

Lifestyle Millennials

Renewables Consumer preference

A Look Back on Our 2017 Strategies

OPPORTUNITIES TO INSPIRE 6Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Our 2017 Fixed Income strategywas to:

The search for yield remained thekey driver for our overall strategy oflong-only and excessive duration bets.

Our 2017 outlook on globalsustainability and structuralconcerns, subdued inflation, and

geopolitics supported our play onglobal high yield paper, investmentgrade bonds, EM debt, and selectpositioning on GCC credits.

In summary, the strategy was a purebeta play, taking directional bets insearch of yield and focusing onsectors which were aligned withcommodities and energy.

To some extent, technical factorsoutpaced fundamentals on thisquest for return. The second lowestdefault rates in the bond markets,coupled with robust demand forprimary bond issuances, whet theappetite for high yield bonds in thefixed income asset class.

US Government

Global DM Sovereign Bonds

Corporate Investment Grade

GCC Debt

Global High yield

USD Emerging Market

Local EM Sovereign

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

2.0%

2.1%

5.9%

7.5%

7.8%

8.0%

15.5%

Exhibit 4: Benchmark performance on the fixed income assetclass for 2017

Source: Bloomberg. Dec 2017

Exhibit 3: Estimates on bond yields and spreads (as per 2017 strategy)

Option-Adjusted spread using Treasuries for risk free rate. 5-Year US Treasuries being used for the above table limiting duration to 4 to 5 years.* Germany 5-year Bunds referenced for yield/spread calculationsSource: ENBD CIO Office. Dec 2017

Short term Sustainable medium2017/F term valuations (3yr-5yr)

Bonds Yield Spread Yield Spread Yield / Spread

10 - Year US Government Bond 2.50% 0 2.50% to 2.75% 0 2.25% to 2.50%Developed MarketsGlobal Developed Sovereign Bonds 0.92% 19 1.10% - 1.35% 40 25 bps to 50 bpsGlobal Investment Grade 2.58% 121 2.75% - 3.00% 125 100 bps to 150bpsHigh YieldUS High Yield 6.30% 434 6% - 6.50% 450 450 bps to 550 bpsEuropean HY Bond* 3.33% 353 3.50% - 4.00% 350 300 bps to 350 bpsGlobal High Yield 5.85% 423 6.25% - 6.50% 475 400 bps to 500 bpsEmerging MarketsSovereign Bonds 5.03% 282 4.75% - 5.25% 300 250bps to 300 bpsCorporate Bonds 5.24% 333 5.25% - 5.75% 350 350 bps to 400 bpsGCC Bonds 4.24% 210 4.40% - 4.70% 250 225 bps to 275 bps

Current

OPPORTUNITIES TO INSPIRE 7

GCC Macro Economic Outlook

Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Following an eventful 2017, we seethe outlook for the GCC economies atthe start of this year as constructive.

Following two years of relativeausterity in regional budgets, whichsaw the introduction of new taxes aswell as cuts to energy and othersubsidies, governments havesignalled a more expansionaryfiscal stance in their 2018 budgets.While Saudi Arabia has recentlyannounced public sector wageincreases and bonuses tocompensate for further fuel andelectricity price hikes and theintroduction of Value Added Tax(VAT) this year, most GCC budgetshave increased their allocations forinfrastructure spending, despiteusing relatively conservative oilprice assumptions for 2018. Thisshould underpin non-oil sectorgrowth this year, even ashouseholds’ spending is likely toremain somewhat constrained.

Oil prices have also started this yearhigher, which has helped to boostsentiment, although we are cautiousabout whether these prices will besustained for the full year. Ouraverage forecast for Brent oil is USD56 in 2018, not much higher than theaverage for 2017. However, even atthis seemingly conservative oil priceassumption, there is room for GCCgovernments to increase spendingwhile continuing to narrow theirbudget deficits.

After contracting in 2017 on OPECagreed production cuts, we alsoexpect the oil sector in most GCCeconomies to contribute positivelyto GDP growth this year, to varyingdegrees. Saudi Arabia had cutproduction by more than agreedwith OPEC last year, allowing theKingdom room to boost crudeoutput in 2018 while still remaining

compliant with OPEC limits. As aresult of both stronger oil and non-oil sector growth, we expect(weighted) average real GDPgrowth in the GCC to accelerate to2.8% in 2018 from an estimated0.6% in 2017.

Within the GCC, the UAE is likely toremain the outperformer in terms ofgrowth, with real GDP expanding3.4% this year, up from an estimated2.0% in 2017. The public sector isexpected to be the main engine ofgrowth this year however, withinfrastructure spending set to pickup as the country prepares to hostExpo 2020, and some public sectorwage growth likely as well.However, household consumption islikely be constrained by higher costsof living (petrol prices will rise with oilprices and VAT has been applied tofood and utilities as well as morediscretionary items) while there islittle indication yet that wages in theprivate sector will rise this year. TheEmirates NBD PMI survey datashowed that firms in the UAE did notincrease hiring much last year evenon the back of record growth inoutput and new work, and that staffcosts have also seen little growth.

Consumers in Saudi Arabia shouldfare slightly better, as the

Government has already put inplace a cash grant to help mitigatethe impact of fuel and energysubsidy cuts on lower incomehouseholds, and also announcedpublic sector wage increases andbonuses at the start of this year. Weexpect Saudi GDP growth toaccelerate to 2.5% this year from-0.5% in 2017.

2014 2015 2016 2017e 2018f0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

3.23.6

2.5

0.6

2.8

Source: Bloomberg. Dec 2017

Exhibit 1: GCC weighted average real GDP growth, % YoY

Oil prices havealso started this

year higher, whichhas helped to

boost sentiment

Oil Outlook

OPPORTUNITIES TO INSPIRE 8Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Oil markets begin 2018 on a strongfooting. OPEC production cuts arehelping to bring down excessinventories while a positive outlookfor the global economy should helpkeep demand afloat. Political riskhas also come back to the fore in oilmarkets, even if a material impact onproduct appears remote. There arestill some challenging fundamentalsfor oil to overcome in 2018 but pricesshould settle on a higher and moresustainable level than 2017.

Oil demand is expected to grow by1.3mn b/d in 2018, a slower rate thanthe buoyant growth of more than1.5mn b/d estimated for 2017.Consumption growth will be at afaster pace than long-term averagesbut will be wholly dependent on EM.After three consecutive years ofgrowth, OECD oil demand is set toflatline in 2018 thanks to acontraction in demand growth inOECD Asia (mostly Japan). Oilconsumption in EM will accelerate in2018 to 1.3mn b/d from 1.1mn b/d asmost economies will remain on asolid footing in 2018. Oil demandgrowth in China will slow next yearbut the decline will be offset by stronggrowth in India (over 300k b/d).

Non-OPEC production will recoverstrongly in 2018, expanding by over1.5mn b/d compared with growth of0.63mn b/d in 2017. The strongestgains will be seen in North Americaand Brazil. Oil production in the UShas recovered all of the decline inproduction from 2015 to mid-2016and has managed to expand tonear record high levels. Totalproduction in mid-November ofover 9.6m b/d is not far off historichighs of just over 10m b/d (hit in theearly 1970s) and even if the USgrows at the slower end of marketestimates production there is set tohit a new record high this year.

As demand growth slows and non-OPEC supply growth accelerates,the burden of balancing markets willfall heavily on OPEC producers. Atthe end of last year, OPEC and itspartners agreed to extend theirproduction cut deal for all of 2018with a review of market conditionsmid-year.

The improvement in oil prices in2017 was likely enough to keepmember countries on board with thedeal but ensuring compliance withthe terms of the cuts will be crucialto prevent the oil market fromblowing back into surplus.Production estimates from the IEApins overall compliance among theOPEC producers that are party tothe cuts at more than 100% onaverage for most of 2017, a farbetter level than any marketobserver had been expecting.However, with compliance alreadyso high, the potential for furtherimprovement appears slim.

The strong aggregate levels ofcompliance has been achieved bysome countries over-cutting andtaking on more than their expectedshare of the burden. Saudi Arabia’saverage compliance in 2017 hasbeen around 120% as it hasslashed output to less than 10m b/d

for several months, while Angolahas also been an over-achiever,although this is largely down tonaturally declining output at olderfields. Compliance across the restof MENA has been more mixed,ranging from effectively 100% inKuwait and Qatar to low levels inthe UAE and Iraq.

Market balance (mn b/d, lhs) OECD stocks: days of demand (rhs)

Jan-14

Apr-14

Jul-14

Oct-14

Jan-15

Apr-15

Jul-15

Oct-15

Jan-16

Apr-16

Jul-16

Oct-16

Jan-17

Apr-17

Jul-17

Oct-17

Jan-18

Apr-18

Jul-18

Oct-18

-1.5-1.0

-0.50.0

0.5

1.01.5

2.02.5

55

57

59

61

63

65

67

Source: Bloomberg. Dec 2017

Exhibit 1: Market balance and OECD stocks

Consumptiongrowth will be at afaster pace than

long-term averages

OPPORTUNITIES TO INSPIRE 9

Oil Outlook

Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

We expect to see an increase in oilproduction from most OPECproducers as they seek to supportgrowth in domestic economies andthe risk of losing more market shareto alternative producers is acute. Asa consequence we forecast the oilmarket returning to surplus in 2018and for inventories to resume theirupward climb. The surplus will benarrower than what the marketendured in 2014-16 but willnevertheless unwind some of thesuccess OPEC had in drawingdown stocks in 2017.

The major unknown variable foroil prices in 2018 remains politicalrisk. Starting with theindependence referendum by theKurdistan Regional Government,US President Donald Trump de-certifying Iran’s compliance withthe nuclear deal and extending tothe corruption investigationsunderway in Saudi Arabia, oilfutures have reincorporated

political risk in a way that hadlargely been absent from 2014-16.However, political risk is achallenging and nebulousdynamic and in reality impossibleto price correctly. At the momentwe see no direct, significantchallenge to oil production as aresult of current geopoliticaltensions in the Middle East.

We forecast Brent oil futures at an

average of USD 56/b in 2018, animprovement from 2017 levels,and expect to see some short-termspikes higher. We would stressthat our price forecast is anaverage and would expect to seea wide swing in prices through2018 as the market responds touncertainties around OPEC’scommitment to the deal and thepotential for US production toupend markets once again.

Brent WTI

20

40

60

80

100

120

Jan-14

Apr-14

Jul-14

Oct-14

Jan-15

Apr-15

Jul-15

Oct-15

Jan-16

Apr-16

Jul-16

Oct-16

Jan-17

Apr-17

Jul-17

Oct-17

Jan-18

Apr-18

Jul-18

Oct-18

Source: Bloomberg. Dec 2017

Exhibit 2: Market balance and OECD stocks

Equity Strategy

OPPORTUNITIES TO INSPIRE 10Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

> Expect high single digit returns in DMs, low teen returns in EMs, complementing a great 2017

> Valuations of most markets at the higher end: endorse caution

> Volatility should revert to normal levels

> Global growth remains synchronous, with upwards earnings revisions supporting equity performance

Post a stellar performance of globalequity markets in 2017, backed bysynchronous economic growth, lowinterest rates and easy liquidityconditions, the total world marketcap is c. USD 100tn – tripling fromthe 2009 lows. Globally, equity ETFssaw a record USD 448bn of inflowsin 2017 (though, active managerssaw outflows of USD 153bn).

To a large extent, current valuationsreflect that equity markets havediscounted much of the expectedfuture profit growth. That limits theupside and is in line with the maturephase of the bull market. The MSCIWorld Index had positive absolutereturns in every month of 2017.

Volatility picks up a while before apeak is reached, so a big downturnis not imminent. Serious marketdownturns are usually preceded byrecessions, which still seem sometime away with 2018 looking likeanother year of strong economicgrowth. However, the liquidity boostfrom Central Banks is on its wayout, removing the strongest pillar ofequity performance in 2017.

MSCI World Growth Index

+56.5

+13.0

MSCI World Value Index

40

60

80

100

120

140

160

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Exhibit 1: Growth outperformed value since the 2008 Financial Crisis

Source: Bloomberg. Rebased to 100. Jan 2008

MSCI World 5Yr Zscore P/E 5Yr Zscore

-3

-2

-1

0

1

2

3

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Exhibit 2: Global markets are overvalued but not in bubble territory

Source: Bloomberg. Jan 2018

Growth has outperformed value since the 2008 Financial Crisis. We think that the majorcontinuing factor that will drive equity market performance is earnings growth. We areoperating in markets that are trading at valuations well above their 10 year average andinvestors need conviction on earnings visibility to remain invested.

OPPORTUNITIES TO INSPIRE 11

Equity Strategy

Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

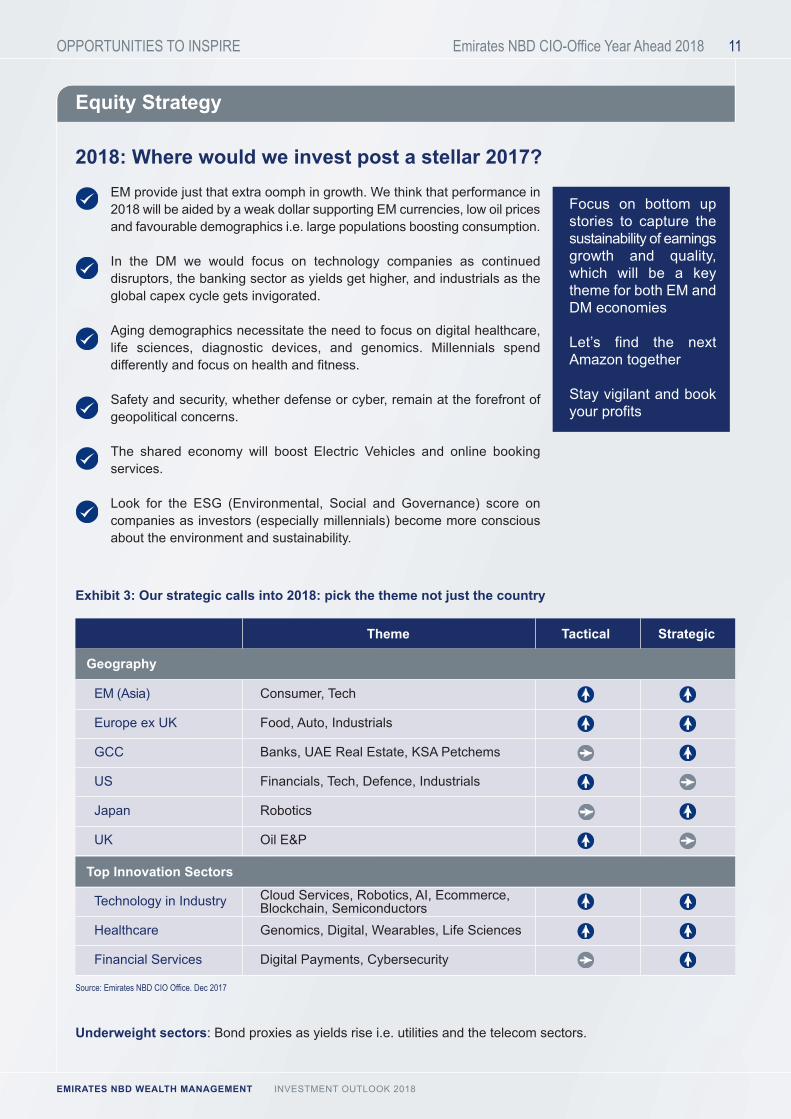

2018: Where would we invest post a stellar 2017? EM provide just that extra oomph in growth. We think that performance in2018 will be aided by a weak dollar supporting EM currencies, low oil pricesand favourable demographics i.e. large populations boosting consumption.

In the DM we would focus on technology companies as continueddisruptors, the banking sector as yields get higher, and industrials as theglobal capex cycle gets invigorated.

Aging demographics necessitate the need to focus on digital healthcare,life sciences, diagnostic devices, and genomics. Millennials spenddifferently and focus on health and fitness.

Safety and security, whether defense or cyber, remain at the forefront ofgeopolitical concerns.

The shared economy will boost Electric Vehicles and online bookingservices.

Look for the ESG (Environmental, Social and Governance) score oncompanies as investors (especially millennials) become more consciousabout the environment and sustainability.

Underweight sectors: Bond proxies as yields rise i.e. utilities and the telecom sectors.

Exhibit 3: Our strategic calls into 2018: pick the theme not just the country

Theme Tactical Strategic

Cloud Services, Robotics, AI, Ecommerce,Blockchain, Semiconductors

Focus on bottom upstories to capture thesustainability of earningsgrowth and quality,which will be a keytheme for both EM andDM economies

Let’s find the nextAmazon together

Stay vigilant and bookyour profits

Source: Emirates NBD CIO Office. Dec 2017

Geography

Top Innovation Sectors

EM (Asia) Consumer, Tech

Europe ex UK Food, Auto, Industrials

GCC Banks, UAE Real Estate, KSA Petchems

US Financials, Tech, Defence, Industrials

Japan Robotics

UK Oil E&P

Technology in Industry

Healthcare Genomics, Digital, Wearables, Life Sciences

Financial Services Digital Payments, Cybersecurity

OPPORTUNITIES TO INSPIRE 12Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Equity Strategy – US Equity Markets

Exceptional returns in 2017 (a broad-based rally) are not expected tocontinue into 2018 and neither is thelow volatility. The largest drawdownwas 3%, whilst the median over thelast 40 years was 10%. Continueinvesting in sustainable businessesto generate mid to high single digitreturns in 2018. It is the 9th year ofeconomic expansion in the US.Economic growth leads to corporateprofit growth and though late cycle,the economy is still in anexpansionary mode.

Positive catalysts> Earnings growth of c.10% for US

large caps in 2018 is achievablethrough tax cuts = 5% + Organicgrowth = 5%. The statutory taxrate has been reduced to 21%from 35%. The median tax ratepaid by S&P companies iscurrently 28%. Buybacks on thetax amnesty on repatriationwould further boost earningsgrowth. There is c. USD 900bn incash overseas with technologyand healthcare companies

> Higher capex spend

> Upwards earnings revisions andpositive forward guidance

> A slow tightening cycle

Risks: Valuations are lofty comparedto historical norms. The median stocktrades in the 98th Percentile (40years). As full employment isreached, higher labour costs coulddent profits. Confidence is near arecord high.

˃ Expect mid to high single digit returns in 2018, with H1 getting the lions share

˃ Overweight finance, technology and industrials (cyclical sectors)

˃ The S&P 500 has had positive total returns for 14 months, a first for the Index

Dec-17

Nov-17

Oct-17

Sep-17

Aug-17

Jul-17

Jun-17

May-17

Apr-17

Mar-17

Feb-17

Jan-17

Dec-16

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1.1

3.1

2.32.1

0.3

2.1

0.6

1.41.0

0.1

4.0

1.92.0

Exhibit 5: The S&P 500, % change each month

Exhibit 4: US indices valuations and growth

Source: Bloomberg. Dec 2017

TelecomEnergy

Real estateUtilities

Cons. StplIndustrials

S&P500HealthcareFinancials

Cons. DiscMaterials

Tech

-5% 0% 5% 10% 15% 20% 25% 30% 35% 40%

Exhibit 6: Technology the best performer

Source: Bloomberg. Dec 2017

2017 Forward LT EPSTotal Return P/E Growth

S&P 500 2,674 21.8% 20.0 12.9

RUSSELL 2000 1,536 14.6% 34.7 9.0

NASDAQ 6,903 29.7% 24.3 11.2

DOW JONES 24,719 28.1% 19.7 8.7

Source: Bloomberg. Dec 2017

Index Level

OPPORTUNITIES TO INSPIRE 13Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Equity Strategy – US Equity Markets

Sectors with the highest potentialgrowth:

US Financials: Banks earn 78% oftheir revenue domestically and willbenefit from the tax cuts andderegulation permitting higherdividend payouts. Interest ratehikes are earnings accretive andwith the fed expected to raise ratesat least thrice in 2018, the USbanks would benefit.

Industrials, aerospace & defense:Beneficiaries of Government spend.

Technology: High growth and highmargins should continue to provideupside though valuations are lofty.Technology is improving our lives inmore ways than ever and consumerenthusiasm is growing as quickly ascompanies can bring their innovationsto market. The smartphone marketis estimated at USD 63bn, digitalTV’s USD 22bn, wearables USD6.5bn and speakers at USD 4bn.

The FAAMGs dominated 2017 fora reason. (2017 returns: Facebookup 51%, Amazon up 55%, Apple up45%, Microsoft up 41% and Googleup 30%) contributed 37% of theS&P 500’s rise. Their disruptiveproperties and large cash balanceswill ensure earnings growth in theyears to come. Digital advertisinghas a 40% market share in the US,expected to grow by 5% p.a. (FBhas 25% of this share and Google

43%). Amazon will benefit fromprime subscriptions and Echo sales.Echo was the bestselling product onPrime Day 2017. Prime membersspend 4.5x as much as non-primemembers. Amazon controls almost50% of ecommerce sales in the US.

However, these monopolies faceglobal pressure on privacy issuesand the use of data as well as theirdominance in search engines.

Fed Funds rate (Rate % RHS)UST 10 yr (Spread bp LHS)

Trai

ling

12M

EP

S

Trailing 12M P

ofit Margin

1990 1993 1996 1999 2002 2005 2008 2011 2014 20170

20

40

60

80

100

120

140

0

5

10

15

20

25

30

Exhibit 7: Improving earnings and margins provide support tothe lofty valuations

Source: Bloomberg. Dec 2017

The tech giants domination The next Amazon? Which industry?

FacebookCash USD 38bn

AmazonCash USD 24bn

AppleCash USD 268bn

GoogleCash USD 107bn

Exhibit 8

Source: Emirates NBD CIO Office. Dec 2017

Microsoft Cash USD 125bn

2bn users

93% of US e-book sales

63% of high endsmartphone sales

78% of US internet ad spend

USD 20bn revenue from cloud services

BlockchainAICloud services Digital content Esport streamingChip makers for cryptosEV – battery makers Wearables for health GenomicsCyber securityRobotics

OPPORTUNITIES TO INSPIRE 14Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Equity Strategy – GCC Markets

> High yielding companies offer sustainable returns

˃ Regular free cash flows are translating to sustainable dividend pay outs

> The petrochemical companies have high margins on account of lower feedstock prices

> The real estate sector is generating sustainable income from malls and hotels

> The banking and telecom sectors have maintained their high dividend payout

MXGCC Index MXEF Index CO1 Comdty

20

40

60

80

100

120

140

160

Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Exhibit 9: On a 5 year basis the GCC markets match EM returns

Source: Bloomberg. Jan 2018

Real estateIndustrialMaterialsFinancials

MSCI GCCHealthcare

EnergyDisc.

StaplesTelecomUtilities

-10% -5% 0% 5% 10% 15% 20%

16.4%15.9%

11.8%10.5%

4.6%4.2%

2.9%2.1%

-0.9%-3.7%

-7.3%

Exhibit 10: MSCI GCC sector total returns 2017

Source: Bloomberg. Dec 2017

The GCC markets offer reasonablevaluations as they were theexception to the global rally of 2017.The UAE and KSA indices ended2017 flat, hence provide a bettercanvas than the global equitymarket. On a five year basis GCCmarkets performance has matchedthat of EM, but regional events keptinvestors sidelined in 2017. GCCmarkets are attractively valued– theUAE is trading at 10x 2018E Price toEarnings with a 4.9% yield, the SaudiIndex at 13.2x with a 3.7% yield vs13x for MSCI EM and a 2.8% yield,.However, geopolitical concerns needto be addressed to provide increasedliquidity and investor confidence inthe UAE and GCC markets.

In the GCC in 2017, real estate gainsin the Index were driven largely byone stock in the KSA i.e. Dar AlArkan (up 133%). Industrial gainswere driven by DP World (up 45%)and finance sector gains were led bybanks in the KSA. The materialssector had petrochemical companiesrally on higher petrochemical productprices. Financials and logisticcompanies were the best performerson the Dubai bourse. On the AbuDhabi bourse insurance and energycompanies were the outperformers. On a five year

basis GCC marketsperformance has

matched that of EM

OPPORTUNITIES TO INSPIRE 15Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Equity Strategy – GCC Markets

Banking: We remain positive banksin the GCC as higher interest rateswill translate to higher net interestmargins and higher earnings. NetInterest Margin expansion hascontinued for GCC banks in Q4.The Islamic banks in the GCCremain the best positioned tobenefit from higher global rates asthey have large proportions of non-interest bearing deposits.

2017 began with GCC banks facingtightening liquidity and deterioratingcredit quality issues in the SMEsector. 2018 looks better asimproved business and consumergrowth, supported by higher oilprices should accelerate economicgrowth. In the UAE the key catalystis expected to be the Expo 2020with the construction sector drivinggrowth. Also, banking consolidationwithin the UAE such as the FirstGulf Bank and the National Bank ofAbu Dhabi merger, are consideredto be at the forefront of a strategictransformation in the bankingsector, as this may compel smallerbanks to merge and remaincompetitive.

Real estate: Here the Dubai realestate sector would be our focus.The upcoming Expo 2020 isexpected to drive up demand andprices in 2018. Increasingly,individual investors and real estatefunds are investing in Dubai as themajor developers i.e. EmaarProperties, Dubai Properties andNakheel provide differentiatedproducts in the market. In the realestate sector developers remaincheaply valued and as off plandeliveries translate into revenue thesector should see a boost.

The sector remains well supportedby recurring revenue from malls and

hotels. Over the next three years,around 886,000 sq. meters (+22.0%)of new retail space is expected toenter the Dubai market, reaching4.1mn sq. meters of retail GLA.Dubai is targeting 20mn touristarrivals by 2020. Dubai has beenranked amongst the top three citiesin the world that are visited bytourists relative to its population size.

Logistics: Our focus is on the UAEhere. The UAE’s logistics sector isexpected to grow in 2018 fueled bynew investments and strong growthin the UAE’s air and sea freightmarkets. According to BMIResearch, UAE’s air freight marketis expected to expand by a CAGRof +4.8% over the 2017-2021period. The UAE’s two leadingairports have continued to invest inexpanding and enhancing facilitiesin recent years. Air freight volumesin the UAE are expected to increasewith the expansion of cold-chainlogistics services at both airports.Jebel Ali Port, managed by DPWorld, is investing USD 1.6bnwhich will further expand the portsin the UAE and develop its facilities.Abu Dhabi Ports Company plans toexpand Khalifa Port in terms ofcapacity in mid-2018 to keep pacewith rapid growth within the sectorand accommodate more industries.

These expansions will have ameaningful positive outcome formajor logistics-focused companiesin the UAE such as Air Arabia andAramex. The logistics industry willbenefit from the increased tourismand a pick-up in the economy.Synergies amongst the players andadoption of technology are leadingto efficiencies of scale.

Petrochemicals in the KSA: The rally could continue. As oil

hovers close to USD 70,petrochemical product prices willmove in line. We expect a continuedfocus on operational excellence toboost margins and FCF generation.Globally recognised players such asSABIC have clear strategies withthree major greenfield expansionsin upstream chemicals, to enhanceits geographical exposure andfeedstock diversity. Acquisitionswould strengthen its position in keyend markets and provide access tonew product technologies.

Capital markets: 2017 saw somesignificant IPO’s with Emaar listing20% of its development businessand raising AED 4.8bn in theprocess. ADNOC listed itsdistribution subsidiary, raising AED3.1bn off a 10% spinoff. The SaudiAramco IPO is expected to be thebiggest globally and in the region in2018. Tadawul is easing regulationson foreign investors to trade on thebourse in order to facilitate the IPOof Saudi Aramco. Tadawul’sindependent custody model (ICM)will be updated to enhanceQualified Foreign Investor (QFI)access to the market by providingfurther flexibility in trading limits.

The changes depict a positivetransformation as viewed byinternational institutions toenhance the growth of themarket. To facilitate inclusion inthe MSCI EM Index, Saudiregulators announced reformsincluding easing rules for foreigninstitutions to invest. Thisremains the biggest catalyst forthe KSA market as it would get2.5 to 3% share of the MSCI EMIndex with the correspondingpassive inflows boosting itsequity market.

GCC: High yielding sectors to invest in and capital market reform

OPPORTUNITIES TO INSPIRE 16Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

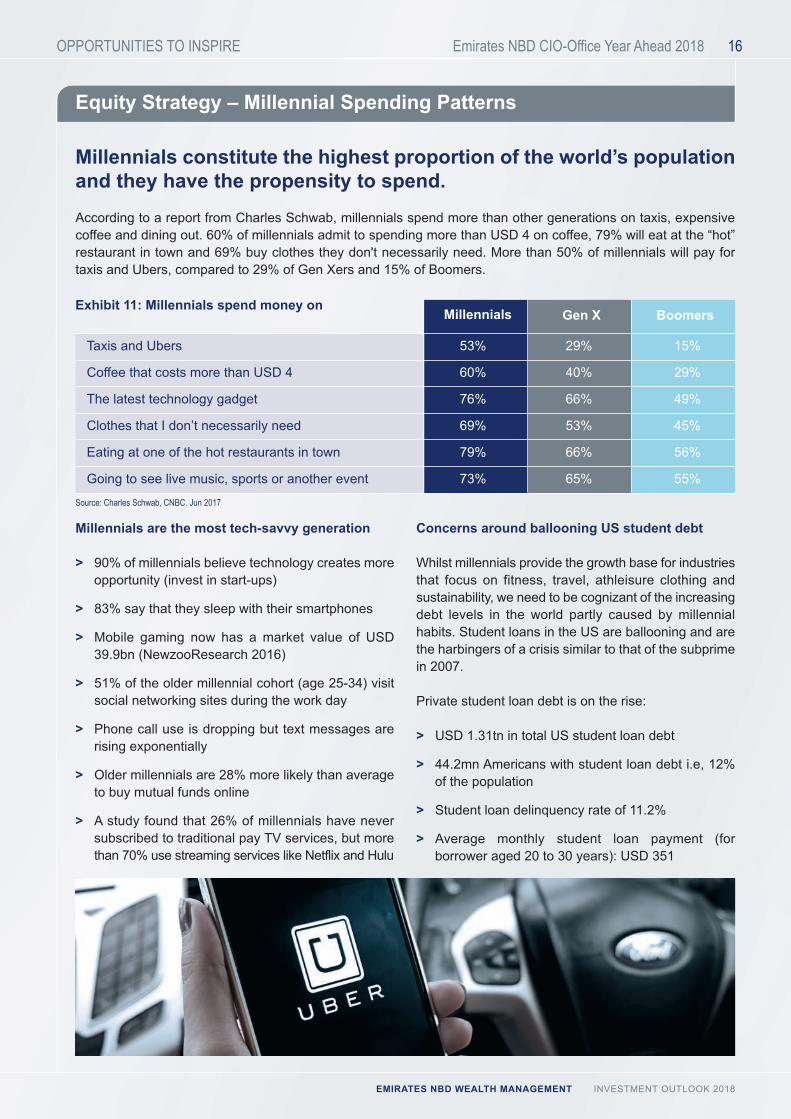

Equity Strategy – Millennial Spending Patterns

Millennials constitute the highest proportion of the world’s populationand they have the propensity to spend. According to a report from Charles Schwab, millennials spend more than other generations on taxis, expensivecoffee and dining out. 60% of millennials admit to spending more than USD 4 on coffee, 79% will eat at the “hot”restaurant in town and 69% buy clothes they don't necessarily need. More than 50% of millennials will pay fortaxis and Ubers, compared to 29% of Gen Xers and 15% of Boomers.

Millennials are the most tech-savvy generation

> 90% of millennials believe technology creates moreopportunity (invest in start-ups)

> 83% say that they sleep with their smartphones

> Mobile gaming now has a market value of USD39.9bn (NewzooResearch 2016)

> 51% of the older millennial cohort (age 25-34) visitsocial networking sites during the work day

> Phone call use is dropping but text messages arerising exponentially

> Older millennials are 28% more likely than averageto buy mutual funds online

> A study found that 26% of millennials have neversubscribed to traditional pay TV services, but morethan 70% use streaming services like Netflix and Hulu

Concerns around ballooning US student debt

Whilst millennials provide the growth base for industriesthat focus on fitness, travel, athleisure clothing andsustainability, we need to be cognizant of the increasingdebt levels in the world partly caused by millennialhabits. Student loans in the US are ballooning and arethe harbingers of a crisis similar to that of the subprimein 2007.

Private student loan debt is on the rise:

> USD 1.31tn in total US student loan debt

> 44.2mn Americans with student loan debt i.e, 12%of the population

> Student loan delinquency rate of 11.2%

> Average monthly student loan payment (forborrower aged 20 to 30 years): USD 351

Exhibit 11: Millennials spend money onMillennials Gen X Boomers

Taxis and Ubers 53% 29% 15%

Coffee that costs more than USD 4 60% 40% 29%

The latest technology gadget 76% 66% 49%

Clothes that I don’t necessarily need 69% 53% 45%

Eating at one of the hot restaurants in town 79% 66% 56%

Going to see live music, sports or another event 73% 65% 55%

Source: Charles Schwab, CNBC. Jun 2017

OPPORTUNITIES TO INSPIRE 17Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Equity Strategy – Emerging Markets

China OtherEM Asia Ex China

1.2%

0.9%

1.5%

Exhibit 12: Breakdown of 2017 global GDP growth between EMAsia and other countries

Source: IMF WEO. Oct 2017

Global economic trends have beennegatively affected by an agingworld population and, since the2008 Financial Crisis, by lowerproductivity, which have bothstarved the world for structuralgrowth and investors for returns andyield. Both factors have beennegative contributors to globalpotential growth and recentlytriggered speculation about apossible period of economicstagnation ahead.

According to the October 2017 IMFWorld Economic Outlook, globalGDP is forecast to rise onlymodestly to 3.8% by 2021 from3.7% in 2018, as output gaps in theadvanced economies are closedand their growth rates are expectedto decline. The IMF includesdeveloping economies anddescribes how the slack in globalGDP growth will be picked up bythese economies which areprojected to grow at 5% by the endof the forecast period.

What is even more relevant is thecontribution to incremental growthprovided by the region. In particular,within the emerging and developingeconomies, we think investorsshould focus their attention on thegeographical area accounting forthe bulk of global growth, which isEM Asia. EM Asia accounted for60% of world growth in 2017, hence58% of the 3.6% world expansionrate, with China making up 34% andother EM Asia 24% of it (Exhibit 12).

The structural drivers of suchdiverging performance between EMand DM economies are to be found indemographic and productivity trends,with both factors most supportivespecifically in EM Asia. Cyclically,increased stability in China, upsidein EM currencies, hence apotentially weaker dollar, play a rolein the favourable outlook as well.

Overall we hold the view that in EMAsia investors should focus theirattention on countries with dynamicdomestic economies, keeping inmind that exposure to global traderepresents a growing risk in thedays of ‘Trumpnomics’. A case inpoint is provided by India, where weretain a constructive view due to itsuntapped potential stemming fromthe huge consumer base.

EM Asia demographicsSupportive demographics in Asiaaccount for exceptional growth rates

of the labour force and of the middleclass, the latter being the populationcohort which has a relevant amountof discretionary income available,hence important for the sustainabledevelopment of a country.

According to the BrookingsInstitution, Asia will account for 90%of the next billion entrants in themiddle class globally, of which380mn are Indians and 350mnChinese. In Asia the middle class isforecast to grow at an impressiverate in the 2020-2030 decade, 72%,unrivalled for the same period inother regions of the world.

The above patterns are importantfor consumption expenditure, sincethe middle class represents themost important market segment forconsumer goods. Consumption isexpected for this cohort to grow by101% in the 2020-2030 decade inAsia, double the world rate.

> EM Asia offers an appealing growth profile

˃ Demographics and productivity above global average

˃ Consumption patterns boosted by growing middle class

˃ Stable China key to EM Asia outlook

˃ Growing US debt points to dollar peak

OPPORTUNITIES TO INSPIRE 18Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

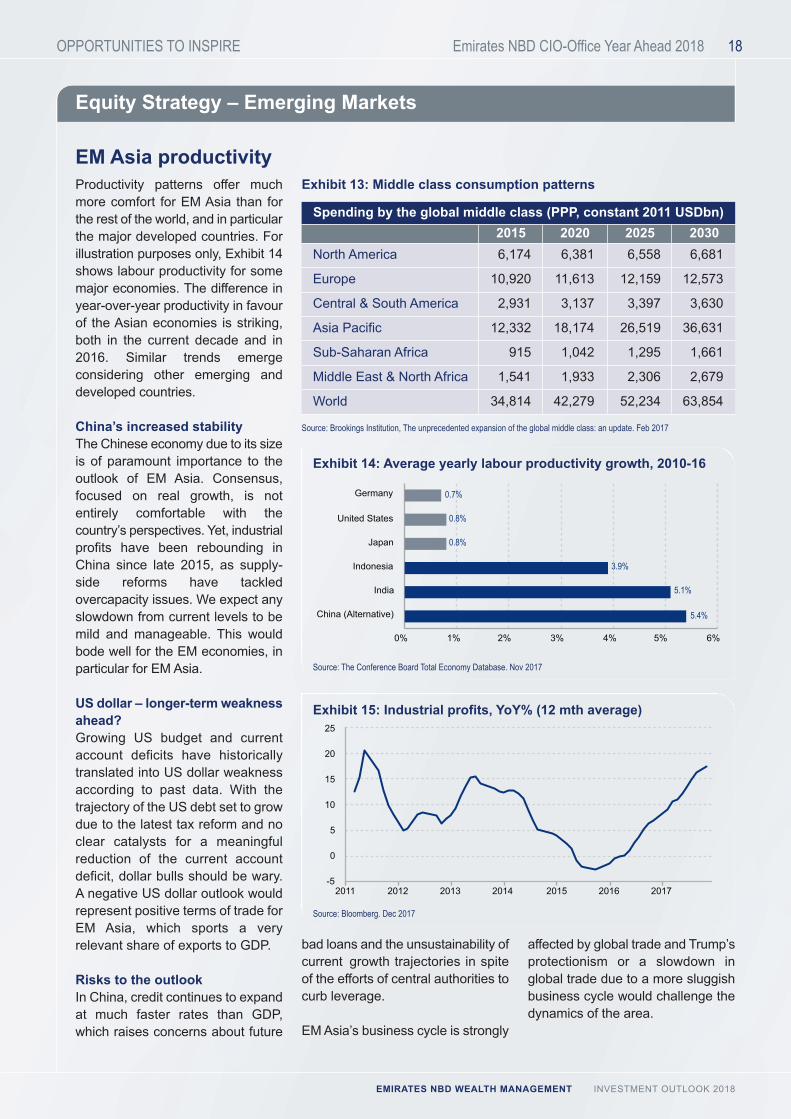

2015 2020 2025 2030Spending by the global middle class (PPP, constant 2011 USDbn)

North America 6,174 6,381 6,558 6,681

Europe 10,920 11,613 12,159 12,573

Central & South America 2,931 3,137 3,397 3,630

Asia Pacific 12,332 18,174 26,519 36,631

Sub-Saharan Africa 915 1,042 1,295 1,661

Middle East & North Africa 1,541 1,933 2,306 2,679

World 34,814 42,279 52,234 63,854

Equity Strategy – Emerging Markets

Productivity patterns offer muchmore comfort for EM Asia than forthe rest of the world, and in particularthe major developed countries. Forillustration purposes only, Exhibit 14shows labour productivity for somemajor economies. The difference inyear-over-year productivity in favourof the Asian economies is striking,both in the current decade and in2016. Similar trends emergeconsidering other emerging anddeveloped countries.

China’s increased stabilityThe Chinese economy due to its sizeis of paramount importance to theoutlook of EM Asia. Consensus,focused on real growth, is notentirely comfortable with thecountry’s perspectives. Yet, industrialprofits have been rebounding inChina since late 2015, as supply-side reforms have tackledovercapacity issues. We expect anyslowdown from current levels to bemild and manageable. This wouldbode well for the EM economies, inparticular for EM Asia.

US dollar – longer-term weaknessahead?Growing US budget and currentaccount deficits have historicallytranslated into US dollar weaknessaccording to past data. With thetrajectory of the US debt set to growdue to the latest tax reform and noclear catalysts for a meaningfulreduction of the current accountdeficit, dollar bulls should be wary.A negative US dollar outlook wouldrepresent positive terms of trade forEM Asia, which sports a veryrelevant share of exports to GDP.

Risks to the outlookIn China, credit continues to expandat much faster rates than GDP,which raises concerns about future

China (Alternative)

India

Indonesia

Japan

United States

Germany

0% 1% 2% 3% 4% 5% 6%

5.4%

5.1%

3.9%

0.8%

0.8%

0.7%

Source: The Conference Board Total Economy Database. Nov 2017

Exhibit 14: Average yearly labour productivity growth, 2010-16

Source: Brookings Institution, The unprecedented expansion of the global middle class: an update. Feb 2017

Exhibit 13: Middle class consumption patterns

-5

0

5

10

15

20

25

2011 2012 2013 2014 2015 2016 2017

Source: Bloomberg. Dec 2017

Exhibit 15: Industrial profits, YoY% (12 mth average)

bad loans and the unsustainability ofcurrent growth trajectories in spiteof the efforts of central authorities tocurb leverage.

EM Asia’s business cycle is strongly

affected by global trade and Trump’sprotectionism or a slowdown inglobal trade due to a more sluggishbusiness cycle would challenge thedynamics of the area.

EM Asia productivity

OPPORTUNITIES TO INSPIRE 19Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Equity Strategy – Emerging Markets

The EMs remain an area ofappealing valuations vs DMs. Notonly do they offer the highesteconomic growth, corporate earningsgrowth is in the mid-teens, which ismuch higher than that of the DMs.

Domestic demand drives consumptionin these denser economies whichalso boast a young populationwhich will enter the workforce andboost productivity further.

EMs are not a homogeneous groupand besides covering severalgeographies i.e. Asia, SouthAmerica and Central Europe, theyalso can be classified into oilimporters and exporters.

India is the world’s largestdemocracy, seen to be politicallystable and China is now becominga hub of technological innovation.

China dominates the world with730mn internet users, andTencent’s WeChat has exceeded700mn users. China also leads theworld in adoption of electric vehiclesin a move to reduce pollution.

> Driven by the youth and the growing middle class

> A widening EM – DM growth differential will support EM assets

> Stable macro conditions should reinforce recovering earning trends

> Increasing spending power as the working population increases

> Low penetration of consumer goods offers a blank canvas

2017 2030 2050

4.11

0.82

4.74

0.79

5.39

0.75

0

2

4

6

1

3

5

Less Developed Region Developed Region

Exhibit 16: EMs are witnessing growth in the work force vs. adecline in the DMs

Source: United Nations Population Division, 15-64 age group ( in mn). Dec 2017Developed regions comprise Europe, Northern America, Australia/New Zealand and JapanLess Developed Regions comprise all regions of Africa, Asia (ex. Japan), Latin America and the Caribbean plusMelanesia, Micronesia and Polynesia

We focus here on just two themes that we like in the EM space,in the economies which offer the highest growth globally:

> China which is transitioning into an innovative, digitally ledeconomy

> India where under penetration of digital services and arising middle class provide ample scope for growth ofconsumer good companies

OPPORTUNITIES TO INSPIRE 20Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Equity Strategy – China Technology

Achieving dominance in emergingtechnologies is the world’s mostimportant battle for economicpower. China and the US are theleaders on investment in technologyand AI. In the US, the private sectorleads, and in China it is theGovernment, which aligns with thecountry’s tech monoliths to ensurethe people and the state remain insync. The pace of technologicalbreakthroughs is quickening and willplay an important role for globalmarkets in 2018. The convergenceof AI, big data, and ultra-fastnetworks is the game changer.Connectivity through the internetand smartphones is the key toeconomic potential.

The rise of the BATs (Baidu +39%,Alibaba +95% and Tencent +114%in 2017)is due to the accessibility of thesecompanies to the data of a largeconsumer base. Today AIpermeates all their applicationsallowing them to personaliseofferings and provide the cuttingcompetitive edge to ensure theyretain a monopoly. On Singles Day,Alibaba used AI to generate 400mnpersonalised ads; Chatbots answered

Exhibit 17: US vs China

3.5mn customer queries. TheChinese social media andecommerce companies’ advantageover the US is the 1bn plus Chinapopulation. Chinese consumershave embraced facial recognitionand mobile payments much fasterthan their Western counterparts.

The cashless society has arrived– but it’s in Asia.Internet titans Alibaba and Tencenthave sidelined the banks to take agrowing role in daily commerce.Their success offers a glimpse of afuture where technology firms driveinnovations in finance just as theyhave in retailing, auto and the media

sectors. WeChat and rival Alipayhave about 90% of the mobile-payment market in China.

For Alibaba and Tencent, thetransaction fees come second to theconsumer data collected, which cantransform their apps into marketingplatforms for a wide variety ofservices. While using the customerdata within their ecosystems, bothinternet giants say they don’t sell it toothers. The problem for banks isthat the payment processors oftenknow more about their customersthan they do.

Started more than a decade ago asa copy of PayPal, Alibaba’s Alipaypassed PayPal in 2013 as thelargest mobile-payment platform.That same year, Tencent linked amobile-payment system to itspopular WeChat instant-messagingapp. Tencent and AntFinancialservices are forming partnershipswith payment processing companiesacross Europe and investing inmobile-payment firms in India,Thailand and other countries.

Internet Users 246mn 773mn

Supercomputers (500 most powerful) 2017 143 202

Operational Robots 2017 250,000 340,000

Top AI start ups 75 8

Mobile payments volume 2016 USD 112bn USD 5.5tn

Source: Eurasia Group “Top Risks 2018”

Dec-2011 Dec-2012 Dec-2013

CAGR (2011-2016): 72.7%

Dec-2014 Dec-2015 Dec-20160

100

200

300

400

500

3155

125

217

358

469

Exhibit 18: Number of mobile payment users in China (mn)

Source: China Internet Network Information Centre. Dec 2017

US China

OPPORTUNITIES TO INSPIRE 21Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Equity Strategy – India

Indian equities are expected todeliver some of the highestearnings growth across majormarkets in 2018. Corporate earningswill be supported by the USD 32bnbank recapitalisation which will boostcredit and consumer spending. Weexpect more fiscal stimulus ahead ofthe 8 State elections in 2018.

Domestic stock market liquiditycontinues to be a strong support forIndian equities along with FIIinflows. Near-term growth recovery,positive domestic sentiment, arating upgrade by Moody’s, andlong-term demographic supportmake staying invested in India anattractive proposition.

Domestic Institutional Investors(DIIs) were net investors to the tuneof USD 14bn in 2017. ForeignInstitutional Investors (FIIs) alsosupported the markets with netinvestments of USD 7.5bn into theIndian equity markets.

Domestic mutual-fund inflows are atrecord levels. Low inflation and lowreturns on property and gold boostedequity inflows. Financial savingsincreased to 54% of annual savingsin 2017 versus 40% in 2012. In 2017,equity participation was 10-12% offinancial savings, mostly via mutualfunds. Risks are a potential high-end-property-market revival andchanges in taxation on capital gains.

The disruption from 2017’s “bigbang” reforms should wane andfocus a return to pushing growth.One of the key concerns in 2017 was

that the Indian market was notsupported by strong earnings growth.Corporate earnings look set for arecovery, which would support thecurrent lofty valuations. The NiftyIndex is trading 10% below 2007’speak valuation and is 1.5sd above its10-year average. High valuationsclearly factor in easy liquidity in globalmarkets. Current market consensusis for 20%+ earnings growth for 2018.

This earnings recovery is aconfluence of the macro polices and

reforms agenda, the boost toinfrastructure spending, the exportgrowth supported by strong globalgrowth, and robust consumerdemand (including improvement inrural demand). A nascent recoveryin private capex would boostearnings over the longer period.

Cash in the hand of the middle andlower income population will lead tohigher consumption as will India’sstrong economic growth and thepower of the Government to spend.

Smartphone Connection (mn) Smartphone Penetration

2014 2015 2016 2017 2018 2019 20200

100

200

300

400

500

600

700

800

0%

10%

20%

30%

40%

50%

60%

157239

340451

544629 702

17%

24%

32%

40%46%

51%55%

Exhibit 19: Smartphone penetration in India

Source: COAI Annual Report. Dec 2017

Jun-16 Sep-16 Dec-16 Mar-17 Jun-170

100

200

300

400

500

330

21

346

21

370

22

401

22

410

22

Wireless Internet Subscribers Wired Internet Subscribers

Exhibit 20: Total internet subscribers (mn)

Source: TRAI. Dec 2017

> India is young and growing – the cycle is at its beginning

> Indian corporate earnings growth is in the high teens

> The Indian middle class is set to become globally significant

> Capital markets’ expansion will add to breadth

> Domestic flows providing sustainable liquidity

OPPORTUNITIES TO INSPIRE 22Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Equity Strategy – India

India provides the demographicsfor increasing ecommerce anddigitisation

India is currently the 2nd largesttelecommunication market globallyand has the 3rd highest number ofinternet users in the world.

> Data usage on Indian telecomoperators' networks (excludingReliance Jio), doubled in sixmonths to 359 petabytes or3.7mn gigabytes per month as4G data usage share increasedto 34% by the end of June 2017

> The Government of India plansto provide wifi to 550,000 villagesby March 2019

The Indian market continues to bedriven by the affordable (<USD 100)and value for money (USD 100-400)smart phone segments.

Supported by rising smartphonepenetration, the launch of 4Gnetworks and increasing consumerwealth, the Indian e-commercemarket is expected to grow to USD200bn by 2026. E-commerce isincreasingly attracting customersfrom Tier 2 and 3 cities, wherepeople have limited access tobrands but have high aspirations.

Two-wheeler sales, tractor sales,diesel demand, rural wage growth,and demand for consumer non-durables – point towards morehouseholds entering the middleclass segment and an improvingrural economy. However, themonsoons in 2018 will remain keyfor a sustained improvement in ruraldemand.

Sectors that will benefit fromincreasing consumption and arecovery of the rural economy:

Autos: Strong demand exists tosustain a 10% sales growth over thenext three years in private andcommercial vehicles. Two-wheelersshould see a 7% CAGR over thesame period.

Consumer goods: Expect demandto pick up on improved consumersentiment, a low base and moreaffordable product prices after theGST “Goods & Services Tax”implementation led to lower taxrates. The rural consumption storyhalted in 2017 owing to severaldisruptive changes in the economy– demonetisation and GST – andpost consecutive droughts in 2014and 2015. The drivers for a ruralconsumption pick-up are now inplace.

Capital goods/infrastructure: TheGovernment is focusing on urbandevelopment and roads;engineering and construction is key.Urban infrastructure and roads isone of the Modi Government’s top-three capex themes.

Property: Demonetisation hasbrought prices to more reasonablelevels. Increased affordability shoulddrive volume recovery.

Private sector banks: Strongdemographics are supportive ofretail / consumer banking growth.With some signs of resolution oflarge ticket corporate NPLs, thecorporate private sector lenderswould likely benefit as credit costsmoderate and growth in corporatelending resumes.

Life insurance companies:A structural shift towards financialsavings which started as aconsequence of the demonetisationdrive should continue. Lifeinsurance companies which havebetter distribution franchises andstrong banc-assurance tie upswould benefit. With structuralimprovements in persistencytogether with higher growth, NewBusiness Premium (NBP) marginsare also likely to improve resultingin better profitability.

Key risks

> A sharp and sustained rise in oilprices

> A sustained spike in bond yieldscould impact the cost of capital

> Any political instability as a resultof the heavy election calendar of2018

OPPORTUNITIES TO INSPIRE 23Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Blockchain

So what is blockchain? At its core, itis a decentralised – yet incorruptible –digital ledger used to record atransaction. Any transaction. Itsbest-known application was increating cryptocurrency, but thetechnology has the capability todisrupt every industry across theboard: from banking to baking!Blockchain technology eliminatesreliance on single-location storageof information, permits public recordkeeping that is easily verifiedacross potentially millions ofsources, all the while preservingprivacy and anonymity. Think of itas sharing a single document withmillions of users, but where allusers can simultaneously accessand use the document, with no riskto data reliability.

Most importantly – and by design –the blockchain ecosystem preventsany single entity from controllinginformation; it has no single point offailure because information is storedin blocks with an interlinked chain(hence the name blockchain). Justlike the internet, the technology isbuilt to be robust. This technologyaddresses major global regulatoryissues because all information onthe blockchain is widely accessible.

A blockchain continues to grow asmore users (known as nodes oradministrators) voluntarily join itand verify information on theblockchain. So why volunteer?Depending on which underlyingblockchain is used, these nodes oradministrators are rewardedthrough gathering or “mining”tokens, known as cryptocurrencies.

Cryptocurrencies (cryptos) areeffectively digital tokens that areexchangeable for goods or services(i.e. a utility token) or tradeableagainst other cryptos (i.e. acurrency token or coin). Cryptos,just like blockchain technology,were designed to operate in adecentralised digital paymentsystem. The first of these wasBitcoin, which has now becomesynonymous with the cryptomovement. The staunch supportersof cryptos argue that they are nodifferent to your traditional (fiat)currencies sitting in a bank account;that effectively, both crypto and fiatcurrencies are limited entries in adatabase that cannot be changedwithout fulfilling specific conditions.

The consensus on blockchaintechnology is that it is a matter ofwhen - and not if - it is adopteduniversally. The only consensus oncryptos today, however, is that thereis no consensus; you either support

the underlying technology andperceived value or you don’t. Notunlike when the internet was firstintroduced, there will be those whoshun the technology and others whoembrace it. Only time will tell if theearly movers will have the edge, orif the crypto skeptics were right allalong. As with all technology, it isonly as good as it is useful: only atthat point in time when it becomespart of Technology Living will thedissenters be forced to adapt.

In keeping with our view that we are indeed living in Tech Age 2.0,blockchain technology presents boundless opportunity to continue todisrupt as it grows in its application across several sectors.

Just like theinternet, thetechnology is

built to be robust

Blockchain

OPPORTUNITIES TO INSPIRE 24Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Industries potentially disruptedby blockchain:

Financial Services & Payments:Complex, cross-border paymentsmay be more secure withblockchain. International paymentsystems such as SWIFT need safercross-border payments solutions: afully decentralised blockchain couldbe that solution. That said, spin-offtechnologies from blockchains alsopose a threat to the long-term viabilityof SWIFT. In fact, the US FederalReserve, which is the supervisor ofUS dollar payment, settlement andclearing systems, highlighted cross-border payments as a possible casefor blockchain use.

Leading global banks, alongsideMasterCard, Visa and IBM, aretenaciously exploring the ledgertechnology behind blockchain toimprove post-trade processing, to

make secure payments and tomaintain immutable records.

Online Retail: Sellers and buyerscan connect directly on blockchain,circumventing the middleman.Smart contracts embedded in theblockchain could establish scoresfor buyers and sellers to determinetheir reliability and quality.

The Internet of Things: Samsungand IBM are creating a decentralisednetwork of IoT devices.

Online Media and Music: Listenersand musicians can connect directly.

Online Marketing: Start-ups appearto support the decentralised systemof record keeping, and are alreadylooking to build platforms whichavoid the reliance on intermediaries:this could possibly mitigate againstclick-fraud.

Video Games: The virtual currenciesused in digital games could be"tokenised" and transferable,allowing people to make moneytrading them like "real" assets.Start-up houses, Gameflip andDMarket, are looking to developthis further.

eSports: Multiplayer video gamecompetitions are getting morepopular, and blockchain technologywill allow virtual asset purchases,among other benefits.

Cloud Storage: File storage couldbecome more secure and possiblycheaper.

Digital Wallets: E-Wallets couldmake it easier to pay for tolls,parking and other consumables.

(Source: Barron’s, Bloomberg, Morningstar)

Exhibit 1: Major technology transforming financial services

Technology Financial Services

Foundations Innovations

Machine Learning

PredictiveAnalytics

Distributed Ledger

(Blockchain)

SmartContractsBiometrics

APIsDigital Wallets

AIBig Data

DistributedComputing

Cryptography

Mobile AccessInternet

Pay

Investment Advice (Robots)Credit Decisions

Regtech, Fraud DetectionAsset Trading

Settle PaymentsB2B

Back-office and RecordingDigital Currencies

Automatic TransactionsSecurity

Identity ProtectionEasy to use Digital Wallets; Finance Dashboards; P2P

Crowd-fundingInter-operability and Expandability

Save Borrow Manage risks Get advice

Source: Morningstar. Dec 2017

OPPORTUNITIES TO INSPIRE 25

Fixed Income Strategy

Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Each year we examine thepotential catalysts which mayimpact returns on fixed income.2015 brought the “great rotation”;2017 followed with PresidentTrump’s “reflationary trade”; and2018 presents a dilemma. At theend of a decade long bull run,global central banks are graduallypulling the plug on stimulus – theso-called “easy money”.

It has become all too prevalenttoday that bond market sentiment isdriven by a series of glossy chartsand theories; but the fact remains:long term global growth has beenstagnant and inflation has beenstubbornly low.

Are we just complacent or beingnaïve trying to understand the realmof financial markets?

> On policy rates – Is this the“new normal” on rates?

> On Inflation – How muchmoney needs to be thrown in to

stimulate spending to igniteinflation?

> On global debt levels – Is thissustainable? Can we affordhigher rates and still servicesuch massive debt levels?Currently global debt is at arecord high of close to USD220tn or circa 325% of globalGDP output

> On expected returns – Are wecomplacent with the returns andrisks attached?

> On monetary and fiscalreforms – Were policy makerscredible? Did this create assetbubbles that led to the birth ofcryptocurrencies?

The most topical - The US yieldcurve being flat has raised manyconcerns as we move to perhaps alate extended economic cycle. Webelieve economic fundamentalsand the growth trajectory couldfurther support and maintain the

shape of the yield curve of furtherflattening to some inversion. Thesteady increase in shorter-termrates has been a major driver of theflattening of the yield curve.

With broad-based expectations forthree rate hikes by the FederalReserve in 2018, the spreaddifferential between the shorter-termtreasuries and their long-termmaturities could converge further.During the last four decades, theyield curve has flattened six times ofwhich 5 led to a recessionary periodfor the US with an average lag effectof about 1 to 2 years.

As far as tighter monetary policiesare concerned, higher rates do notalways translate nor stipulate theunderperformance on the fixedincome asset class directly. Today,the bond markets have evolved,and offer well diversifiedopportunities for investors. Thereare many ways to steer away fromthe most sensitive bonds from risingrates and position into the less

Fixed Income is core for every portfolio: finding value in a rich environment (perhaps the “New Normal”)

> DM Sovereign bonds portend negative to flat returns

> US Government bonds are appealing

> Remain overweight EM bonds – sovereigns, financials, consumer staples attractive

> GCC bond markets offer select opportunites across sovereigns and corporates

Fixed Income Positioning Current Expected Returns Risks toSub-Asset Class Tactical Strategic Yield for 2018 our Strategy

DM Sovereign Debt ▼ ■ 1.15% Flat

Corporate Investment Grade ▲ ■ 2.48% 2.5% to 3.5%

Corporate High Yield (Global) ■ ■ 5.23% 4.0% to 6.0%

EM Debt ▲ ▲ 4.52% 4.0% to 5.0%

GCC Bond/Sukuk ▲ ▲ 4.25% 3.5% to 4.5%

Overweight ▲ Neutral ■ Underweight ▼

Geo-politicalconcerns, inflationarypressures, fasterthan expectedmonetary policyactions, highersupply of bondissuance to fundfederal deficit, higherglobal growth thanexpected

Exhibit 1: Our preference and strategy across the fixed income sub asset class

Source: Fixed Income desk (CIO Office) projections. Dec 2017

Fixed Income Strategy

OPPORTUNITIES TO INSPIRE 26Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

sensitive, and still be investedprudently without compromising onquality of bond portfolios.

We believe bond markets areseasoned and ready for a gradualpace of policy rate hikes with the“well-telegraphed” unwinding ofcentral bank’s balance sheets. Afaster pace of US rate hikes areprobably the biggest risk to ourassessment, along with inflationovershooting. However, wesubscribe to the fact that policyrates are unrealistically low,especially as we move towards theend of an extended late-economic

cycle. In most of the past USeconomic cycles, the FederalReserve has had enough buffer ontheir monetary policy to drop rates.Failing to hike rates sufficientlyduring this cycle could posesignificant risks to the economyleaving the FED with limited tools tomaneuver monetary policies.

US-Government bonds areappealing given the macro-economic landscapeOur findings and thoughts on longterm valuations, give us comfort andconviction that yields on the US 10-year benchmark should be well

anchored between the 2.50% to2.75% range throughout 2018.While the current shape of the yieldcurve does depict some inversion,we see a low likelihood that long-term inflation expectations mayovershoot and pressure bond yieldsto rise.

Exhibit 2: Yield curve vs fed funds rate Exhibit 3: Economics vs reality: US benchmarkyields seem to be well anchored

Source: Bloomberg. Dec 2017

1997 2002 2007 2012 20170

1

2

3

4

5

6

7

-100

-50

0

50

100

150

200

250

300

Fed Funds TR - upper bound (%)5Y-30Y (Spread bp LHS) Fed Funds Rate (%)UST 10Y (Spread bp LHS)

2013 2014 2015 2016 20171.0

1.5

2.0

2.5

3.0

3.5First 25bp hike in Dec 2015; Start of the tightening cycle

Three 25bp hikesduring 2017

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Exhibit 4: University of Michigan expected changein prices over the next 5-10 years(median)

Exhibit 5: Negative or zero yields lure globalinvestors to US Government bonds

Source: Bloomberg. Dec 2017

Source: Bloomberg. Dec 2017

Source: Bloomberg. Dec 2017

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2014 2015 2016 20170

2000

4000

6000

8000

10000

12000

14000

Bill

ions

(US

D)

OPPORTUNITIES TO INSPIRE 27Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Fixed Income Strategy

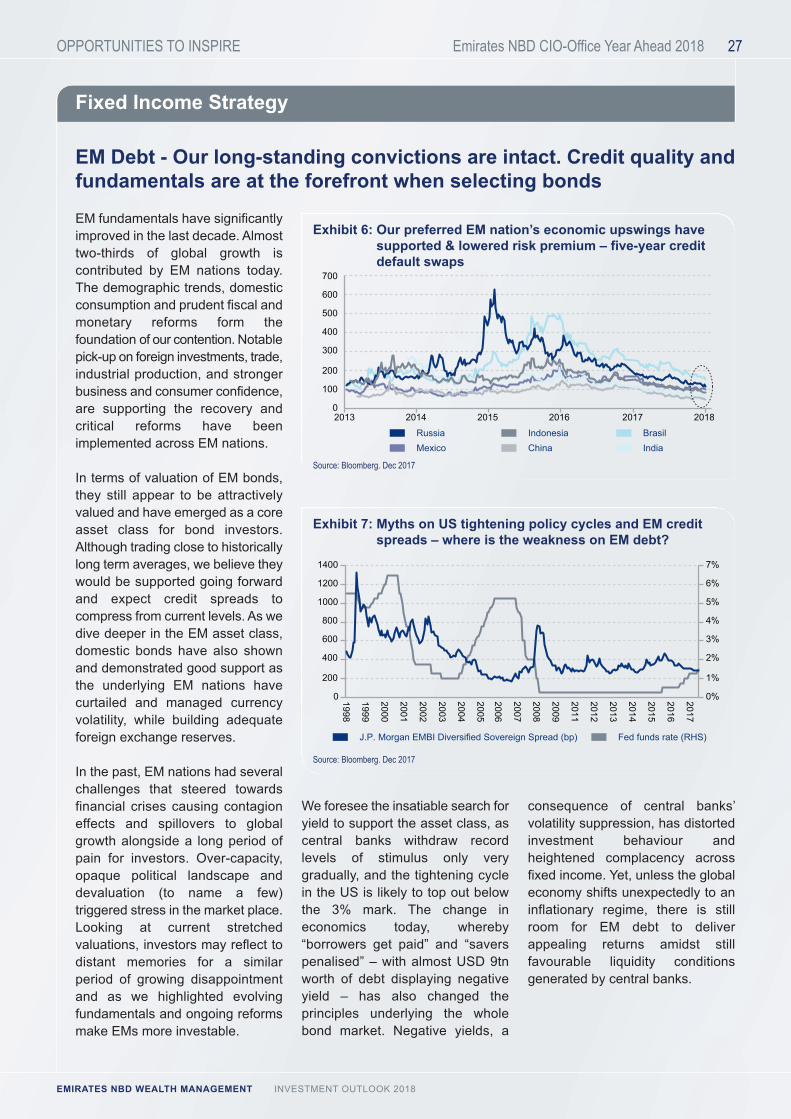

EM fundamentals have significantlyimproved in the last decade. Almosttwo-thirds of global growth iscontributed by EM nations today.The demographic trends, domesticconsumption and prudent fiscal andmonetary reforms form thefoundation of our contention. Notablepick-up on foreign investments, trade,industrial production, and strongerbusiness and consumer confidence,are supporting the recovery andcritical reforms have beenimplemented across EM nations.

In terms of valuation of EM bonds,they still appear to be attractivelyvalued and have emerged as a coreasset class for bond investors.Although trading close to historicallylong term averages, we believe theywould be supported going forwardand expect credit spreads tocompress from current levels. As wedive deeper in the EM asset class,domestic bonds have also shownand demonstrated good support asthe underlying EM nations havecurtailed and managed currencyvolatility, while building adequateforeign exchange reserves.

In the past, EM nations had severalchallenges that steered towardsfinancial crises causing contagioneffects and spillovers to globalgrowth alongside a long period ofpain for investors. Over-capacity,opaque political landscape anddevaluation (to name a few)triggered stress in the market place.Looking at current stretchedvaluations, investors may reflect todistant memories for a similarperiod of growing disappointmentand as we highlighted evolvingfundamentals and ongoing reformsmake EMs more investable.

We foresee the insatiable search foryield to support the asset class, ascentral banks withdraw recordlevels of stimulus only verygradually, and the tightening cyclein the US is likely to top out belowthe 3% mark. The change ineconomics today, whereby“borrowers get paid” and “saverspenalised” – with almost USD 9tnworth of debt displaying negativeyield – has also changed theprinciples underlying the wholebond market. Negative yields, a

consequence of central banks’volatility suppression, has distortedinvestment behaviour andheightened complacency acrossfixed income. Yet, unless the globaleconomy shifts unexpectedly to aninflationary regime, there is stillroom for EM debt to deliverappealing returns amidst stillfavourable liquidity conditionsgenerated by central banks.

EM Debt - Our long-standing convictions are intact. Credit quality andfundamentals are at the forefront when selecting bonds

IndonesiaRussia BrasilChinaMexico India

0

100

200

300

400

500

600

700

2013 2014 2015 2016 2017 2018

Exhibit 6: Our preferred EM nation’s economic upswings havesupported & lowered risk premium – five-year creditdefault swaps

Source: Bloomberg. Dec 2017

Fed funds rate (RHS)J.P. Morgan EMBI Diversified Sovereign Spread (bp)

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2011

2012

2013

2014

2015

2016

2017

0

200

400

600

800

1000

1200

1400

0%

1%

2%

3%

4%

5%

6%

7%

Exhibit 7: Myths on US tightening policy cycles and EM creditspreads – where is the weakness on EM debt?

Source: Bloomberg. Dec 2017

OPPORTUNITIES TO INSPIRE 28Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Fixed Income Strategy

50,000

100,000

150,000

200,000

250,000

300,000

2012 2013 2014 2015 2016 2017

Corporate

Record borrowing from EM debt issuers (USD mn) Record borrowing from Global debt issuers (USD mn)

Financial DM EMSovereign

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

2012 2013 2014 2015 2016 2017 2018

Exhibit 8: Borrowings through bond markets have surged over the years to record levels

Source: Bond Radar and Emirates NBD CIO Office. Dec 2017 Source: Bond Radar and Emirates NBD CIO Office. Dec 2017

Emerging market vulnerabilities have structurally declined and are nowmore diverse. Primary Eurobond sales were well received andsurpassed USD 675bn for 2017

OPPORTUNITIES TO INSPIRE 29Emirates NBD CIO-Office Year Ahead 2018

EMIRATES NBD WEALTH MANAGEMENT INVESTMENT OUTLOOK 2018

Portfolio Strategy

˃ Diversification benefits of traditional asset classes are limited