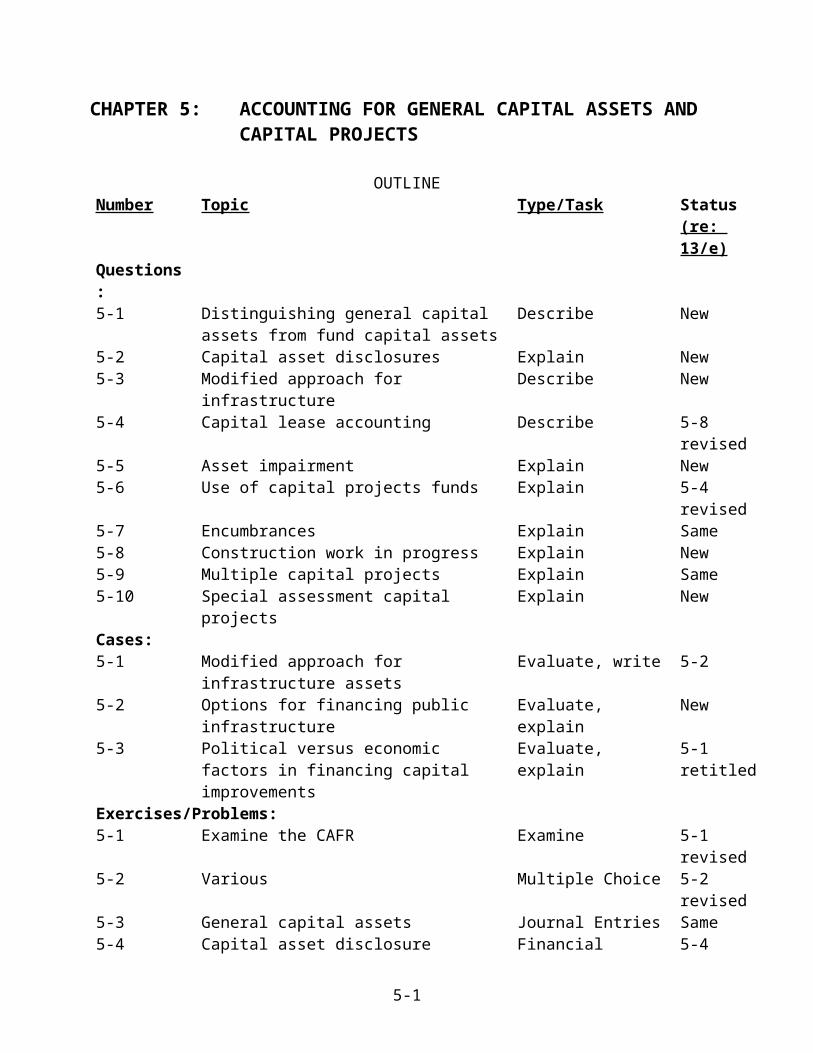

CHAPTER 5: ACCOUNTING FOR GENERAL CAPITAL ASSETS AND CAPITAL PROJECTS OUTLINE Number Topic Type/Task Status (re: 13/e) Questions : 5-1 Distinguishing general capital assets from fund capital assets Describe New 5-2 Capital asset disclosures Explain New 5-3 Modified approach for infrastructure Describe New 5-4 Capital lease accounting Describe 5-8 revised 5-5 Asset impairment Explain New 5-6 Use of capital projects funds Explain 5-4 revised 5-7 Encumbrances Explain Same 5-8 Construction work in progress Explain New 5-9 Multiple capital projects Explain Same 5-10 Special assessment capital projects Explain New Cases: 5-1 Modified approach for infrastructure assets Evaluate, write 5-2 5-2 Options for financing public infrastructure Evaluate, explain New 5-3 Political versus economic factors in financing capital improvements Evaluate, explain 5-1 retitled Exercises/Problems: 5-1 Examine the CAFR Examine 5-1 revised 5-2 Various Multiple Choice 5-2 revised 5-3 General capital assets Journal Entries Same 5-4 Capital asset disclosure Financial 5-4 5-1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER 5: ACCOUNTING FOR GENERAL CAPITAL ASSETS AND CAPITAL PROJECTS

OUTLINE Number Topic Type/Task Status

(re: 13/e)

Questions:5-1 Distinguishing general capital assets from fund

capital assetsDescribe New

5-2 Capital asset disclosures Explain New5-3 Modified approach for infrastructure Describe New5-4 Capital lease accounting Describe 5-8 revised5-5 Asset impairment Explain New5-6 Use of capital projects funds Explain 5-4 revised5-7 Encumbrances Explain Same5-8 Construction work in progress Explain New5-9 Multiple capital projects Explain Same5-10 Special assessment capital projects Explain New

Cases:5-1 Modified approach for infrastructure assets Evaluate, write 5-25-2 Options for financing public infrastructure Evaluate, explain New5-3 Political versus economic factors in financing

capital improvementsEvaluate, explain 5-1 retitled

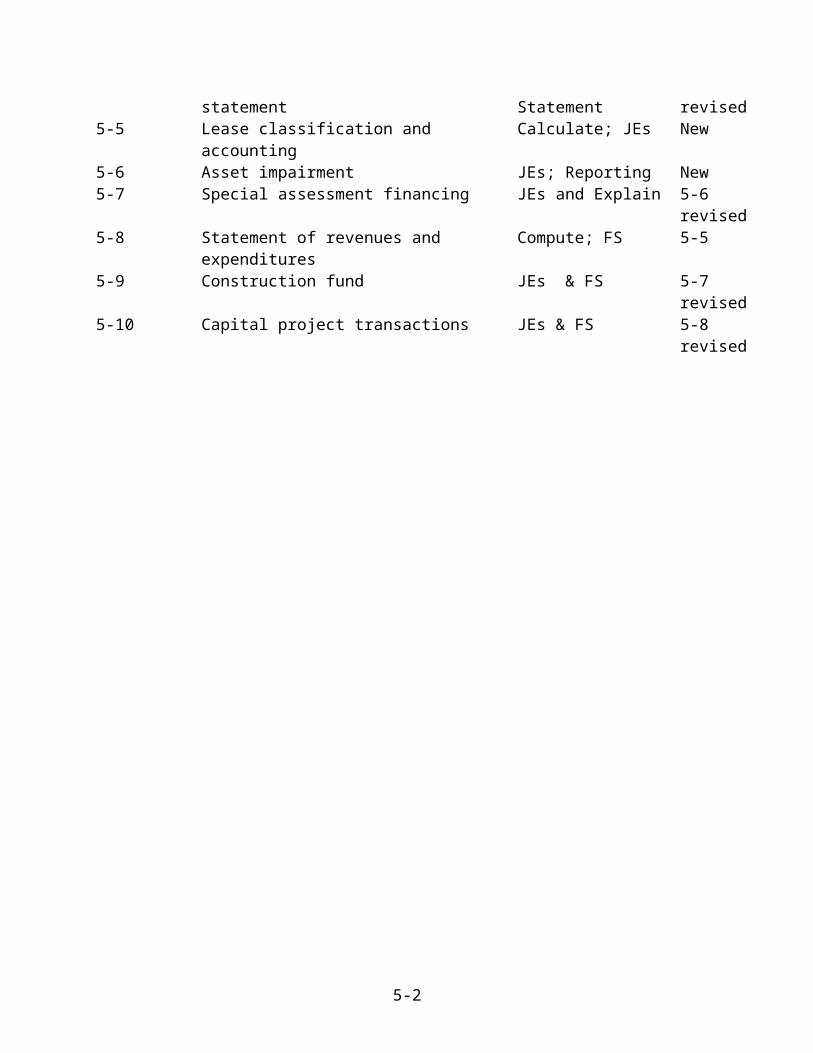

Exercises/Problems:5-1 Examine the CAFR Examine 5-1 revised5-2 Various Multiple Choice 5-2 revised5-3 General capital assets Journal Entries Same5-4 Capital asset disclosure statement Financial Statement 5-4 revised 5-5 Lease classification and accounting Calculate; JEs New5-6 Asset impairment JEs; Reporting New5-7 Special assessment financing JEs and Explain 5-6 revised5-8 Statement of revenues and expenditures Compute; FS 5-5 5-9 Construction fund JEs & FS 5-7 revised5-10 Capital project transactions JEs & FS 5-8 revised

5-1

CHAPTER 5: ACCOUNTING FOR GENERAL CAPITAL ASSETS AND CAPITAL PROJECTS

Answers to Questions

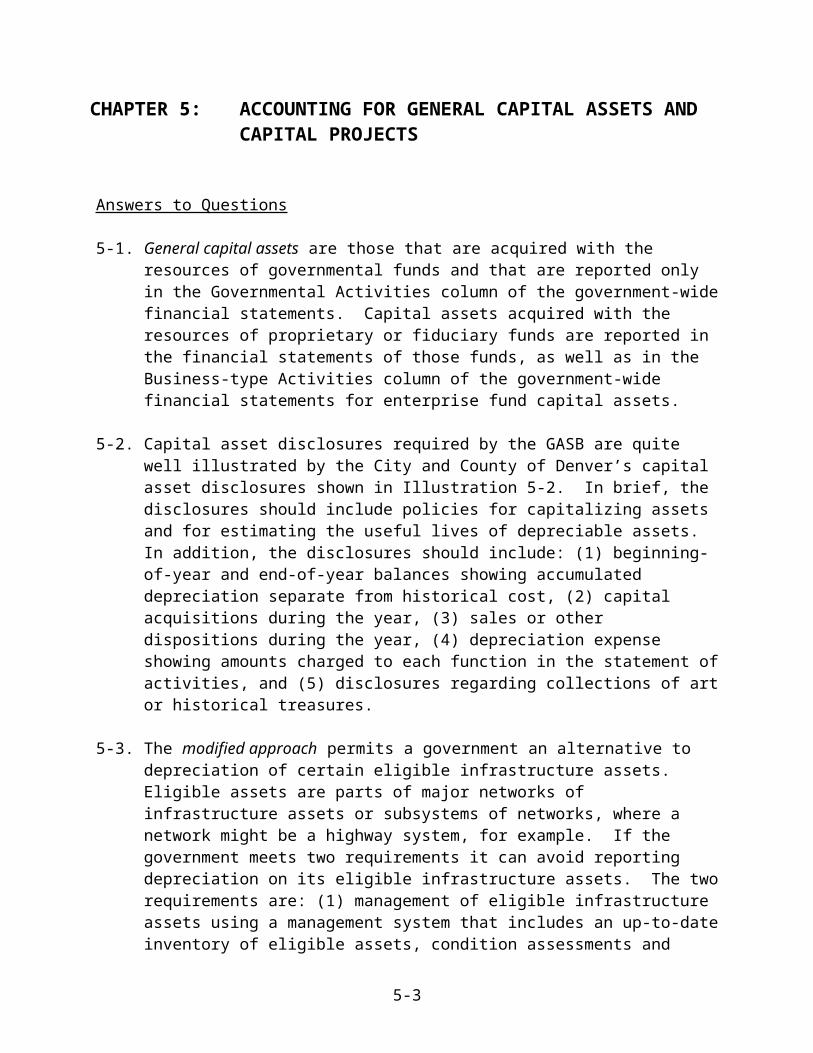

5-1. General capital assets are those that are acquired with the resources of governmental funds and that are reported only in the Governmental Activities column of the government-wide financial statements. Capital assets acquired with the resources of proprietary or fiduciary funds are reported in the financial statements of those funds, as well as in the Business-type Activities column of the government-wide financial statements for enterprise fund capital assets.

5-2. Capital asset disclosures required by the GASB are quite well illustrated by the City and County of Denver’s capital asset disclosures shown in Illustration 5-2. In brief, the disclosures should include policies for capitalizing assets and for estimating the useful lives of depreciable assets. In addition, the disclosures should include: (1) beginning-of-year and end-of-year balances showing accumulated depreciation separate from historical cost, (2) capital acquisitions during the year, (3) sales or other dispositions during the year, (4) depreciation expense showing amounts charged to each function in the statement of activities, and (5) disclosures regarding collections of art or historical treasures.

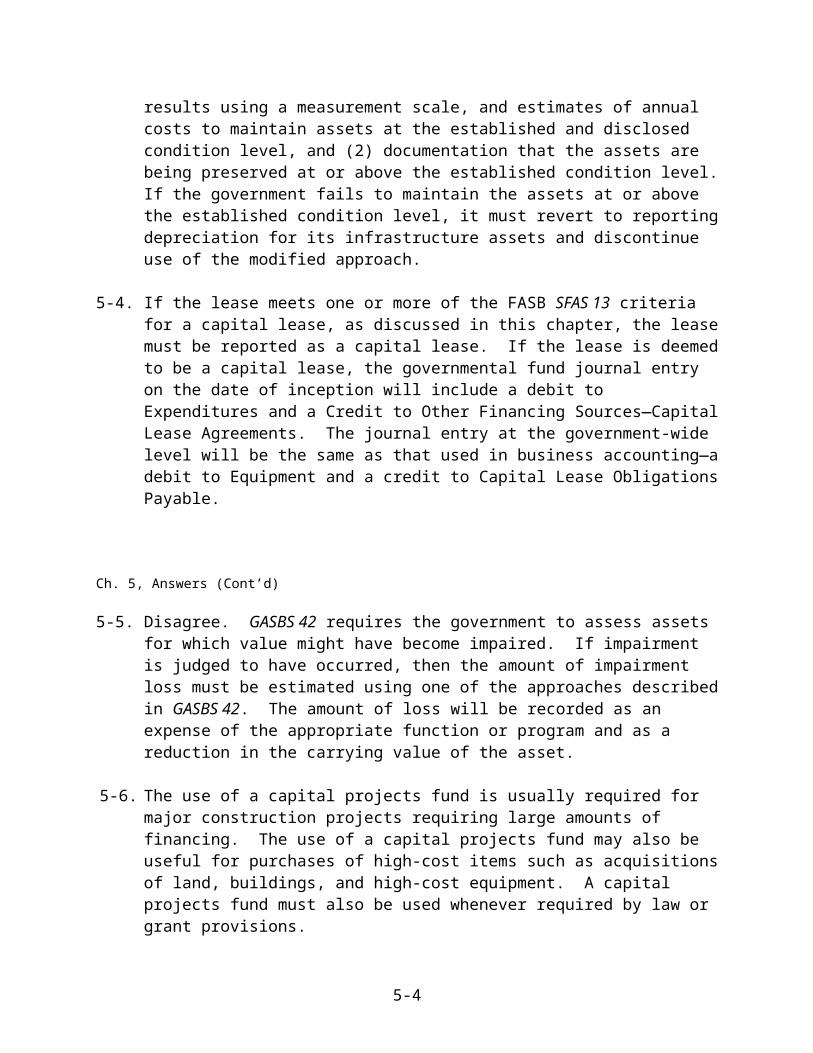

5-3. The modified approach permits a government an alternative to depreciation of certain eligible infrastructure assets. Eligible assets are parts of major networks of infrastructure assets or subsystems of networks, where a network might be a highway system, for example. If the government meets two requirements it can avoid reporting depreciation on its eligible infrastructure assets. The two requirements are: (1) management of eligible infrastructure assets using a management system that includes an up-to-date inventory of eligible assets, condition assessments and results using a measurement scale, and estimates of annual costs to maintain assets at the established and disclosed condition level, and (2) documentation that the assets are being preserved at or above the established condition level. If the government fails to maintain the assets at or above the established condition level, it must revert to reporting depreciation for its infrastructure assets and discontinue use of the modified approach.

5-4. If the lease meets one or more of the FASB SFAS 13 criteria for a capital lease, as discussed in this chapter, the lease must be reported as a capital lease. If the lease is deemed to be a capital lease, the governmental fund journal entry on the date of inception will include a debit to Expenditures and a Credit to Other Financing Sources—Capital Lease Agreements. The journal entry at the government-wide level will be the same as that used in business accounting—a debit to Equipment and a credit to Capital Lease Obligations Payable.

5-2

Ch. 5, Answers (Cont’d)

5-5. Disagree. GASBS 42 requires the government to assess assets for which value might have become impaired. If impairment is judged to have occurred, then the amount of impairment loss must be estimated using one of the approaches described in GASBS 42. The amount of loss will be recorded as an expense of the appropriate function or program and as a reduction in the carrying value of the asset.

5-6. The use of a capital projects fund is usually required for major construction projects

requiring large amounts of financing. The use of a capital projects fund may also be useful for purchases of high-cost items such as acquisitions of land, buildings, and high-cost equipment. A capital projects fund must also be used whenever required by law or grant provisions.

5-7. To facilitate preparation of financial statements at the end of the fiscal year, all operating and budgetary accounts should be closed, including Encumbrances. However, since the project is still underway and contractual commitments still exist to pay contractors when billed, it is essential that Encumbrances be reestablished at the beginning of the next year in order to maintain budgetary control over outstanding commitments.

5-8. All ordinary and necessary costs to construct the asset are appropriately reported as construction work in progress. This includes all legal costs, engineering and architectural services, site preparation, materials used, and billings from contractors, among other items. Interest incurred during construction is not capitalized for general capital assets, however. Construction Work in Progress is found in the ledger for governmental activities at the government-wide level for general capital assets, and not in the ledger for the capital projects fund. In the capital projects fund, all capitalizable items are debited to Construction Expenditures.

5-9. For a multiple-projects fund, encumbrances and construction expenditures should be identified in a manner that will indicate to which project each applies. This can be accomplished by adding a project identifier to the Encumbrances and Construction Expenditures accounts, such as EncumbrancesStreet Project or Construction ExpendituresProject No. 10. Identifying encumbrances and expenditures by project facilitates comparisons to budget for particular projects and presentation of cash and expenditure statements for multi-project operations. For example, the City of Smithville Continuous Computerized Problem that accompanies this text has two capital projects funds named the Springer Street Project and the Alzmann Street Project.

5-10. Capital projects fund accounting for special assessments is virtually identical in both of these situations. The only difference is that the credit entry for issuance of special assessment bonds is to Other Financing Sources—Contribution from Property Owners if the government assumes no responsibility for the debt, rather than to Other Financing Sources—Proceeds of Special Assessment Bonds with Governmental Commitment.

5-3

Solutions to Cases

5-1. a. Discuss with students various methods of obtaining financial statements and getting “benchmark” data to make comparisons across entities. Professional associations such as the Government Finance Officers Association, National Association of State Auditors, Controllers and Treasurers, and Association of School Business Officials publish “best practices” for various areas of public finance, accounting, and financial reporting. Since each student will have a different list of cities, ask them to compare their results with other students and look for patterns in which types and sizes of governments make similar choices in accounting methods, particularly, in this case, regarding choice of infrastructure asset accounting methods.

b. An important communication skill for students to master is to convey technical financial accounting information in an effective way so that decision makers find the information useful for making informed decisions. You may wish to ask students to show their memo or essay to a finance director of a city and get their opinion about whether the student has captured the fundamental issues relating to infrastructure and communicated it in a professional and informative manner.

c. During the implementation years of GASBS 34, the GFOA and some state auditors released policy statements indicating to governments that they did not have to capitalize infrastructure assets to meet minimum standards for the GFOA’s Certificate of Achievement for Excellence in Financial Reporting or the states’ reporting compliance regulations. Despite such statements, most governments that sought a “clean” audit opinion voluntarily developed inventories of infrastructure and followed GAAP for infrastructure reporting. For most general purpose governments, omitting infrastructure assets would cause their statement of net assets to be materially misstated resulting in a qualified or adverse audit opinion—likely the latter. A government receiving an adverse audit opinion may experience a downgrading of its bond rating and thus face considerably higher cost of borrowing.

5-2 a. Option (1), the sales tax approach, offers the advantage of spreading the burden for infrastructure improvements across a larger number of taxpayers, including many non-residents who visit or shop in Desert City. From an equity standpoint, the sales tax approach has appeal because infrastructure improvements enhance the city for visitors and shoppers, as well as for residents. Disadvantages of this approach are the necessity of scheduling and conducting a special election and the political risk of advocating for a tax increase.

Option (2), the development fee approach, has the advantage of being relatively “invisible” to the public and efficient to administer since the number of developers will be relatively small. Although real estate developers can be expected to pass the development fee to new homeowners and businesses, property values may be increased by enhanced infrastructure (e.g., improved streets and highways, adequate storm drainage, and so forth). As a result, taxpayers may recoup a portion of the development fee. The main disadvantage is the potential inequity of the development

5-4

Ch. 5, Solutions, Case 5-2 (Cont’d)

fee since a relatively high financial burden is imposed on new homeowners and new businesses for infrastructure expansion and improvement that may substantially benefit the entire city.

A city council member may prefer the development fee approach since it holds less political risk than asking residents to approve a tax increase. The city manager may prefer the sales tax approach as retail sales may be less volatile than new construction, which can be strongly impacted by the local, regional, and national economies. Since the city manager is responsible for ensuring that infrastructure stays abreast of population and new development, he or she may prefer a more stable source of infrastructure financing. Current homeowners and businesses might be expected to prefer the development fee approach since those fees would not directly impact on their property and would place the incidence of the tax on others. It would be surprising if new homeowners or new businesses favored the development fee approach as they would probably view it as inequitable.

b. Accounting and financial reporting would be minimally impacted by which option is ultimately chosen. Either way, there is revenue to be recognized in a capital projects fund (a tax in one case and development fee in the other). Accounting for infrastructure construction would not be affected by the source of financing.

5-3. a. Regardless of how a student voted, he or she had plenty of company. With a record voter turnout for such an election, the half-cent sales tax was barely approved. Only 51.7 percent of the voters in Brown County voted for the tax. As expected, 56.5 percent of the voters in the City of Brownville voted against it. Except for a few precincts in other cities and towns, voters outside Brownville voted overwhelmingly in support of the tax. While there is no "right" answer to this question, each student should have provided a rationale similar to one of the arguments provided in the case. A few students may develop unique arguments in support of their vote. Generally, the students who voted for the proposed tax must have thought the county-wide benefits of improved roads and bridges were worth the extra tax costs and outweighed the possible detrimental effects on the City's financial flexibility. Those who voted against it presumably did so using the rationale expressed by some voters in exit polls, "why should I pay more for roads that will benefit rural county residents more than me."

b. Although some students may profess an altruistic motivation for their vote, most are expected to reflect economic rationality. That is, they would likely vote for the sales tax increase if they were an owner of a large commercial or manufacturing property, and would therefore realize a net economic benefit from the property tax rollback and sales tax increase. Even then some students may justify the "yes" vote on the basis of the county-wide benefits of improved infrastructure rather than their financial self-interest.

5-5

Ch. 5, Solutions, Case 5-3 (Cont’d)

c. Again, there is no right answer to this question. Students (Brownville voters) who voted against the tax probably would argue that residents who primarily benefit should pay for the improvements (i.e., special assessment financing should have been used). Those who voted for the tax probably would argue that the broader (county-wide) economic benefits of improved county infrastructure justifies financial support by all county residents. Some who voted for the tax may have preferred special assessment financing but possibly feared that failure to approve the sales tax would doom the needed improvements altogether.

d. The County's procedures for accounting for the financing and the capital projects activities will differ slightly for the option approved by the voters compared with those that would have been used if special assessment financing had been used. But, as explained in Chapter 5, the procedures for accounting for special assessment-financed capital projects are quite similar to those for other capital projects, especially when, as is often the case, the government is committed in some manner for repaying debt issued for the project. Since bond financing is typically used for special assessment capital projects, accounting for both special assessment taxes and debt service would have been required for an extended period, probably ten years or more. Whether these differences would be termed "significant" accounting issues is a matter of conjecture; they might be considered significant by the financial staff of the County.

Solutions to Exercises and Problems

5-1. Each student will have a different annual report, so he or she will have different answers to questions in this exercise. The various kinds of capital assets and capital projects, wide variety of financing mechanisms, and different accounting policies used in and by governments should generate interesting classroom discussions.

5-2. 1. a. 6. c.2. d. 7. d.3. c. 8. c.4. a 9. a.5. b. 10. c.

5-6

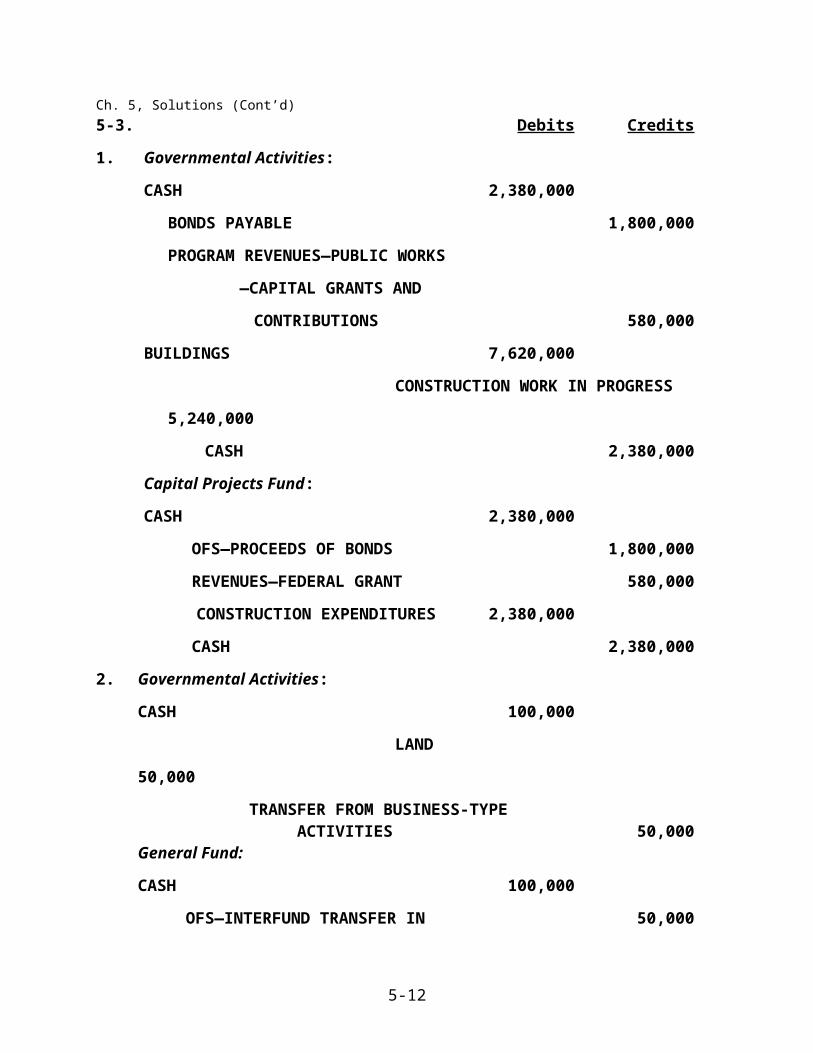

Ch. 5, Solutions (Cont’d)5-3. Debits Credits

1. Governmental Activities:

CASH 2,380,000

BONDS PAYABLE 1,800,000

PROGRAM REVENUES—PUBLIC WORKS

—CAPITAL GRANTS AND

CONTRIBUTIONS 580,000

BUILDINGS 7,620,000

CONSTRUCTION WORK IN PROGRESS 5,240,000

CASH 2,380,000

Capital Projects Fund:

CASH 2,380,000

OFS—PROCEEDS OF BONDS 1,800,000

REVENUES—FEDERAL GRANT 580,000

CONSTRUCTION EXPENDITURES 2,380,000

CASH 2,380,000

2. Governmental Activities:

CASH 100,000

LAND 50,000

TRANSFER FROM BUSINESS-TYPE ACTIVITIES 50,000

General Fund:

CASH 100,000

OFS—INTERFUND TRANSFER IN 50,000

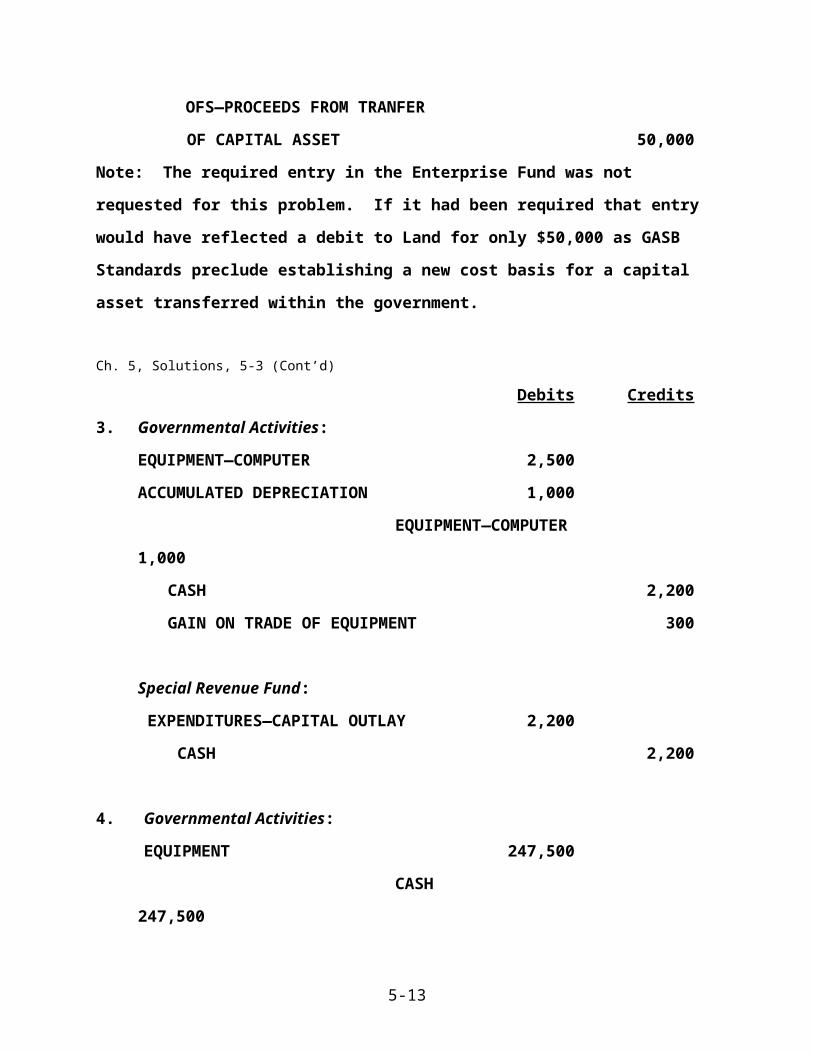

OFS—PROCEEDS FROM TRANFER

OF CAPITAL ASSET 50,000

Note: The required entry in the Enterprise Fund was not requested for this

problem. If it had been required that entry would have reflected a debit to Land

for only $50,000 as GASB Standards preclude establishing a new cost basis for a

capital asset transferred within the government.

5-7

Ch. 5, Solutions, 5-3 (Cont’d)

Debits Credits

3. Governmental Activities:

EQUIPMENT—COMPUTER 2,500

ACCUMULATED DEPRECIATION 1,000

EQUIPMENT—COMPUTER 1,000

CASH 2,200

GAIN ON TRADE OF EQUIPMENT 300

Special Revenue Fund:

EXPENDITURES—CAPITAL OUTLAY 2,200

CASH 2,200

4. Governmental Activities:

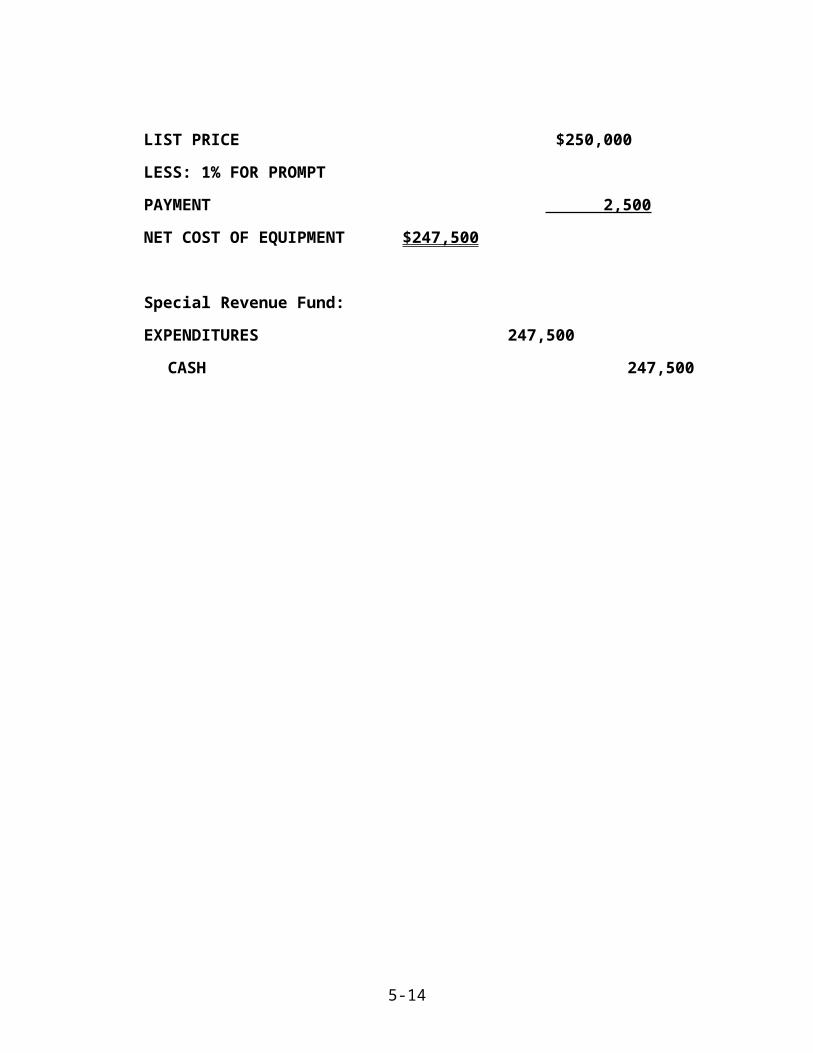

EQUIPMENT 247,500

CASH 247,500

LIST PRICE $250,000

LESS: 1% FOR PROMPT

PAYMENT 2,500

NET COST OF EQUIPMENT $247,500

Special Revenue Fund:

EXPENDITURES 247,500

CASH 247,500

5-8

Ch. 5, Solutions, 5-3 (Cont’d)

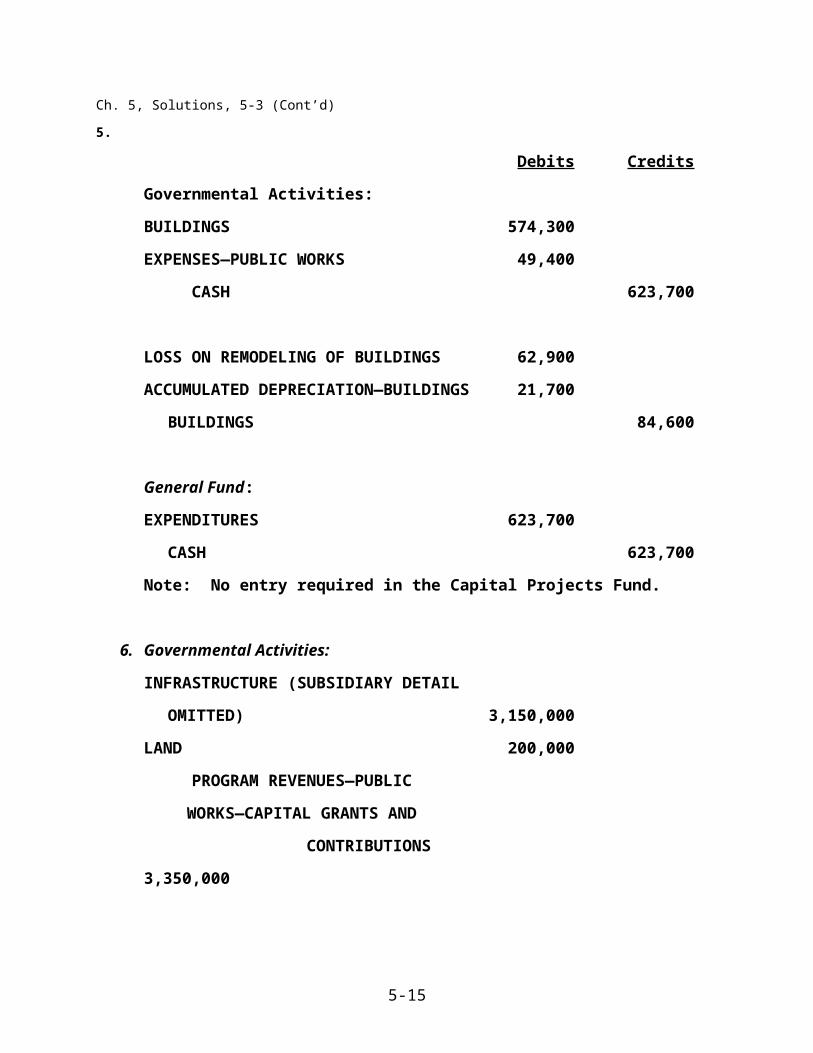

5.

Debits Credits

Governmental Activities:

BUILDINGS 574,300

EXPENSES—PUBLIC WORKS 49,400

CASH 623,700

LOSS ON REMODELING OF BUILDINGS 62,900

ACCUMULATED DEPRECIATION—BUILDINGS 21,700

BUILDINGS 84,600

General Fund:

EXPENDITURES 623,700

CASH 623,700

Note: No entry required in the Capital Projects Fund.

6. Governmental Activities:

INFRASTRUCTURE (SUBSIDIARY DETAIL

OMITTED) 3,150,000

LAND 200,000

PROGRAM REVENUES—PUBLIC

WORKS—CAPITAL GRANTS AND

CONTRIBUTIONS 3,350,000

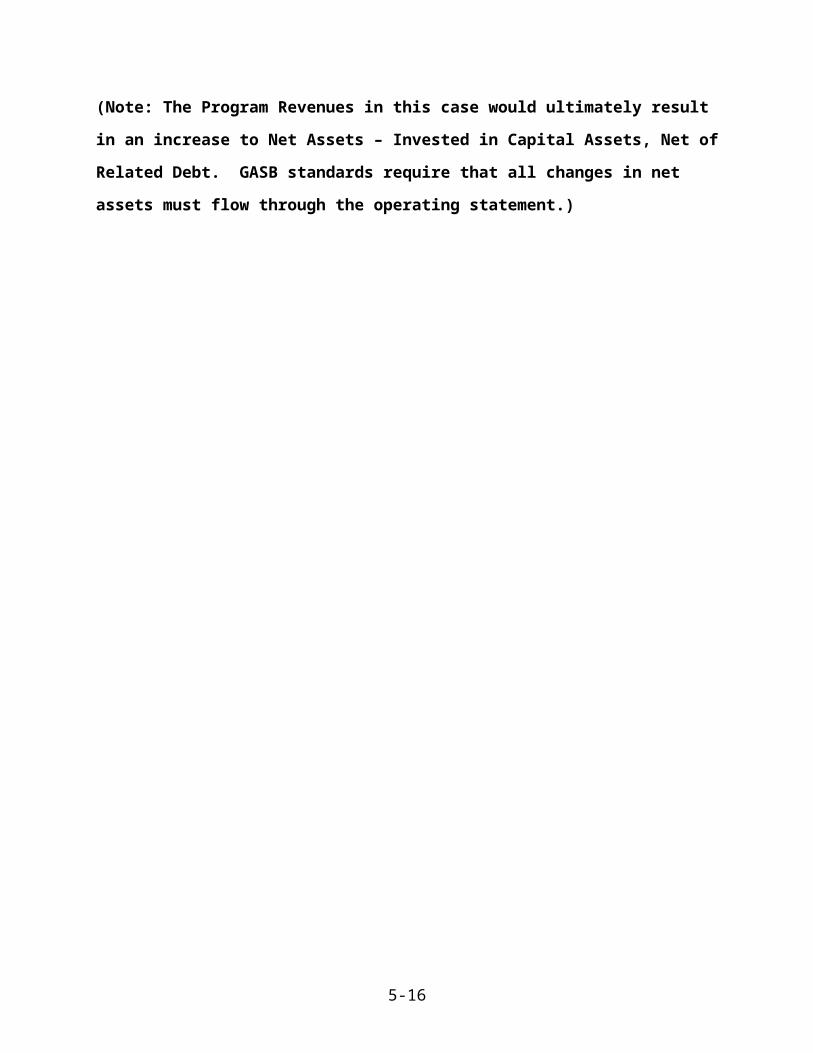

(Note: The Program Revenues in this case would ultimately result in an increase

to Net Assets – Invested in Capital Assets, Net of Related Debt. GASB standards

require that all changes in net assets must flow through the operating statement.)

5-9

Ch. 5, Solutions (Cont’d)

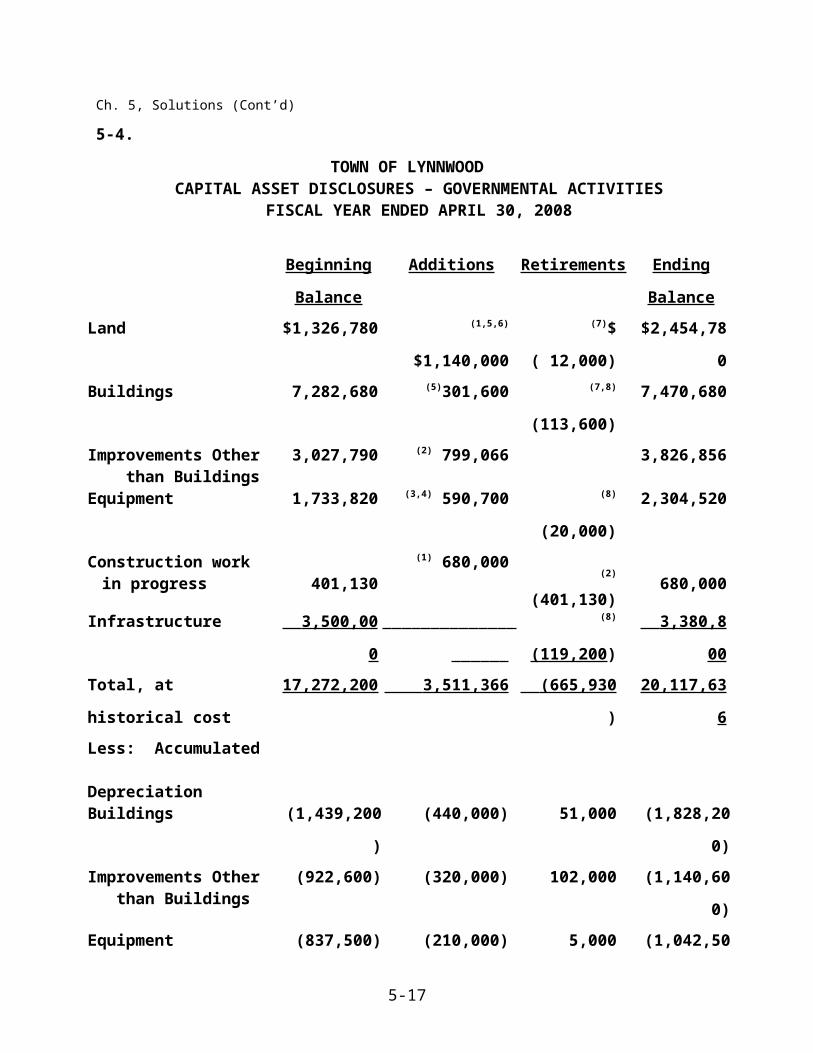

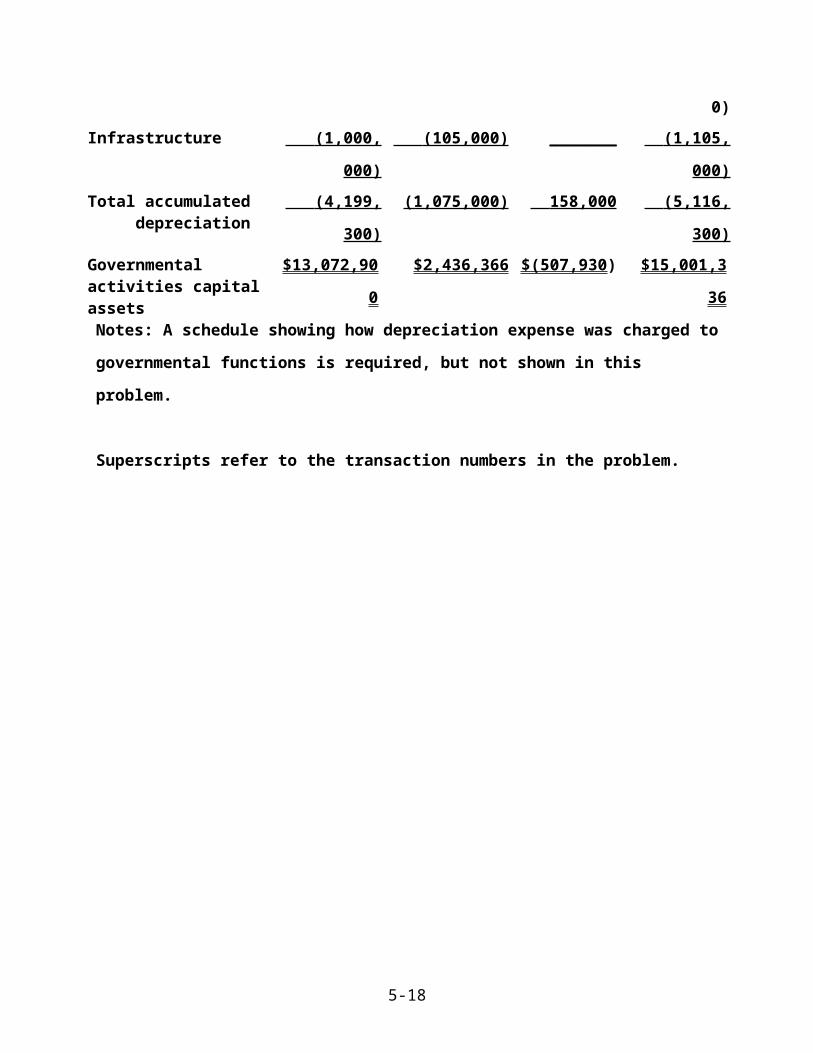

5-4.

TOWN OF LYNNWOODCAPITAL ASSET DISCLOSURES – GOVERNMENTAL ACTIVITIES

FISCAL YEAR ENDED APRIL 30, 2008

Beginning

Balance

Additions Retirements Ending

Balance

Land $1,326,780 (1,5,6) $1,140,000 (7)$( 12,000) $2,454,780

Buildings 7,282,680 (5)301,600 (7,8)(113,600) 7,470,680

Improvements Other than Buildings

3,027,790 (2) 799,066 3,826,856

Equipment 1,733,820 (3,4) 590,700 (8) (20,000) 2,304,520

Construction work in progress 401,130

(1) 680,000 (2) (401,130) 680,000

Infrastructure 3,500,000 (8) (119,200) 3,380,800

Total, at historical cost 17,272,200 3,511,366 (665,930 ) 20,117,636

Less: Accumulated DepreciationBuildings (1,439,200) (440,000) 51,000 (1,828,200)

Improvements Other than Buildings

(922,600) (320,000) 102,000 (1,140,600)

Equipment (837,500) (210,000) 5,000 (1,042,500)

Infrastructure (1,000,000) (105,000) _______ (1,105,000)

Total accumulated depreciation

(4,199,300) (1,075,000) 158,000 (5,116,300)

Governmental activities capital assets

$13,072,900 $2,436,366 $(507,930) $15,001,336

Notes: A schedule showing how depreciation expense was charged to

governmental functions is required, but not shown in this problem.

Superscripts refer to the transaction numbers in the problem.

5-10

Ch. 5, Solutions (Cont’d)

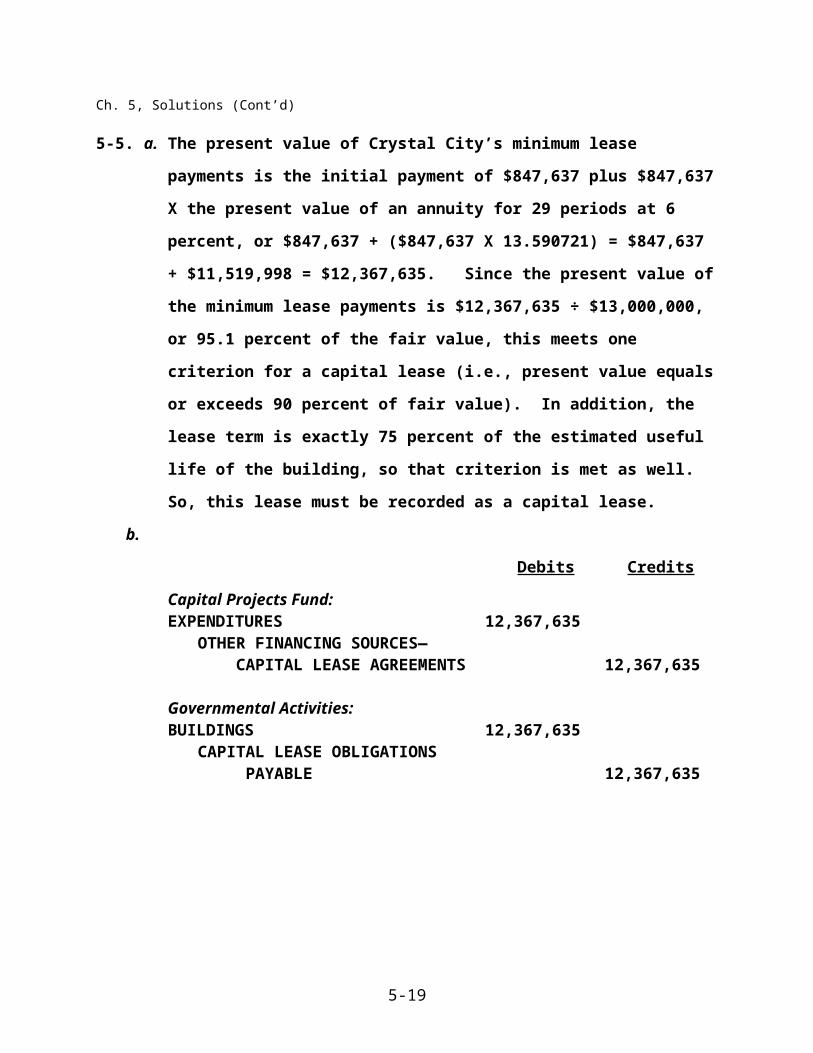

5-5. a. The present value of Crystal City’s minimum lease payments is the

initial payment of $847,637 plus $847,637 X the present value of an

annuity for 29 periods at 6 percent, or $847,637 + ($847,637 X 13.590721)

= $847,637 + $11,519,998 = $12,367,635. Since the present value of the

minimum lease payments is $12,367,635 ÷ $13,000,000, or 95.1 percent

of the fair value, this meets one criterion for a capital lease (i.e., present

value equals or exceeds 90 percent of fair value). In addition, the lease

term is exactly 75 percent of the estimated useful life of the building, so

that criterion is met as well. So, this lease must be recorded as a capital

lease.

b.

Debits Credits

Capital Projects Fund:EXPENDITURES 12,367,635

OTHER FINANCING SOURCES— CAPITAL LEASE AGREEMENTS 12,367,635

Governmental Activities:BUILDINGS 12,367,635

CAPITAL LEASE OBLIGATIONS PAYABLE 12,367,635

5-11

Chapter 5, Solutions (Cont’d)

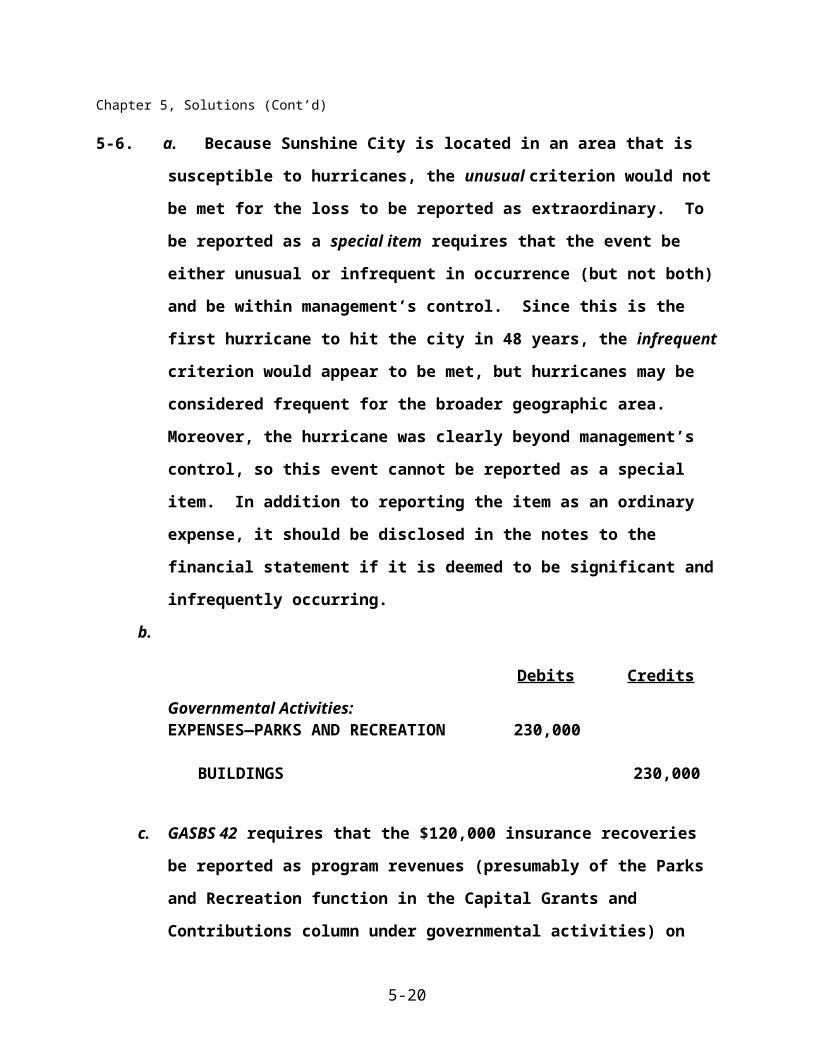

5-6. a. Because Sunshine City is located in an area that is susceptible to

hurricanes, the unusual criterion would not be met for the loss to be

reported as extraordinary. To be reported as a special item requires

that the event be either unusual or infrequent in occurrence (but not

both) and be within management’s control. Since this is the first

hurricane to hit the city in 48 years, the infrequent criterion would

appear to be met, but hurricanes may be considered frequent for the

broader geographic area. Moreover, the hurricane was clearly beyond

management’s control, so this event cannot be reported as a special

item. In addition to reporting the item as an ordinary expense, it should

be disclosed in the notes to the financial statement if it is deemed to be

significant and infrequently occurring.

b.

Debits Credits

Governmental Activities:EXPENSES—PARKS AND RECREATION 230,000

BUILDINGS 230,000

c. GASBS 42 requires that the $120,000 insurance recoveries be reported

as program revenues (presumably of the Parks and Recreation function

in the Capital Grants and Contributions column under governmental

activities) on the government-wide statement of activities. In addition, it

should be reported as an other financing source by the General Fund.

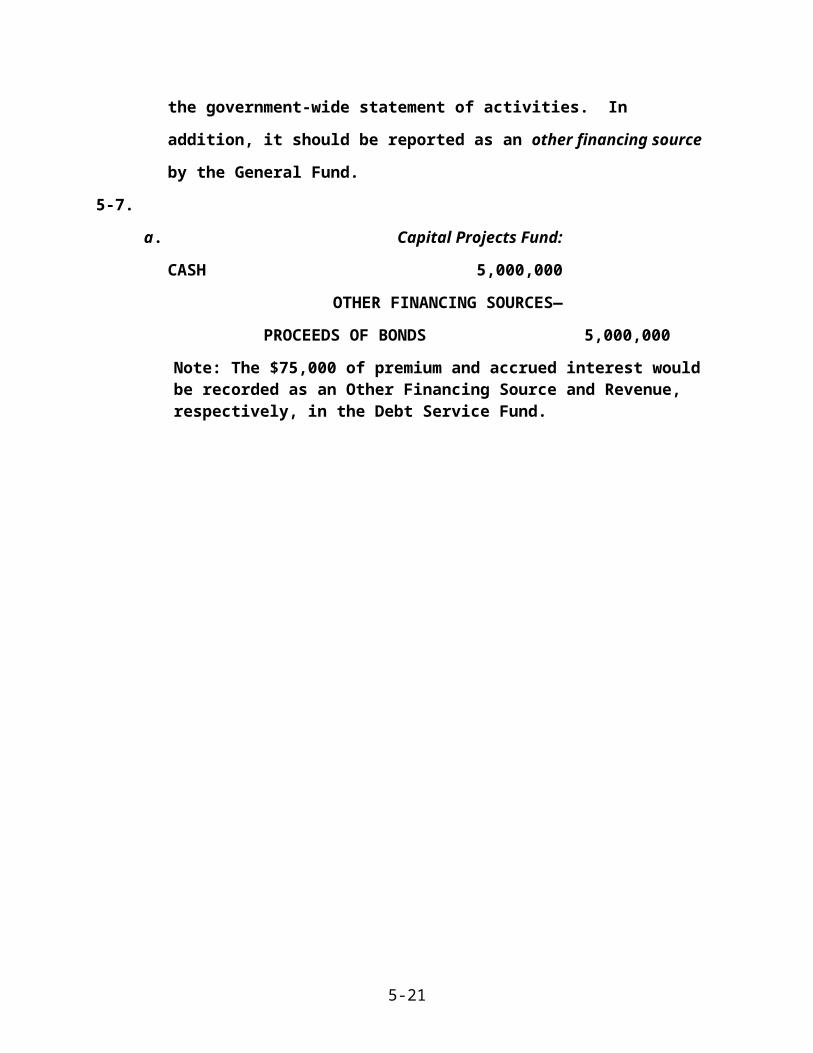

5-7.

a. Capital Projects Fund:

CASH 5,000,000

OTHER FINANCING SOURCES—

PROCEEDS OF BONDS 5,000,000

Note: The $75,000 of premium and accrued interest would be recorded as an Other Financing Source and Revenue, respectively, in the Debt Service Fund.

5-12

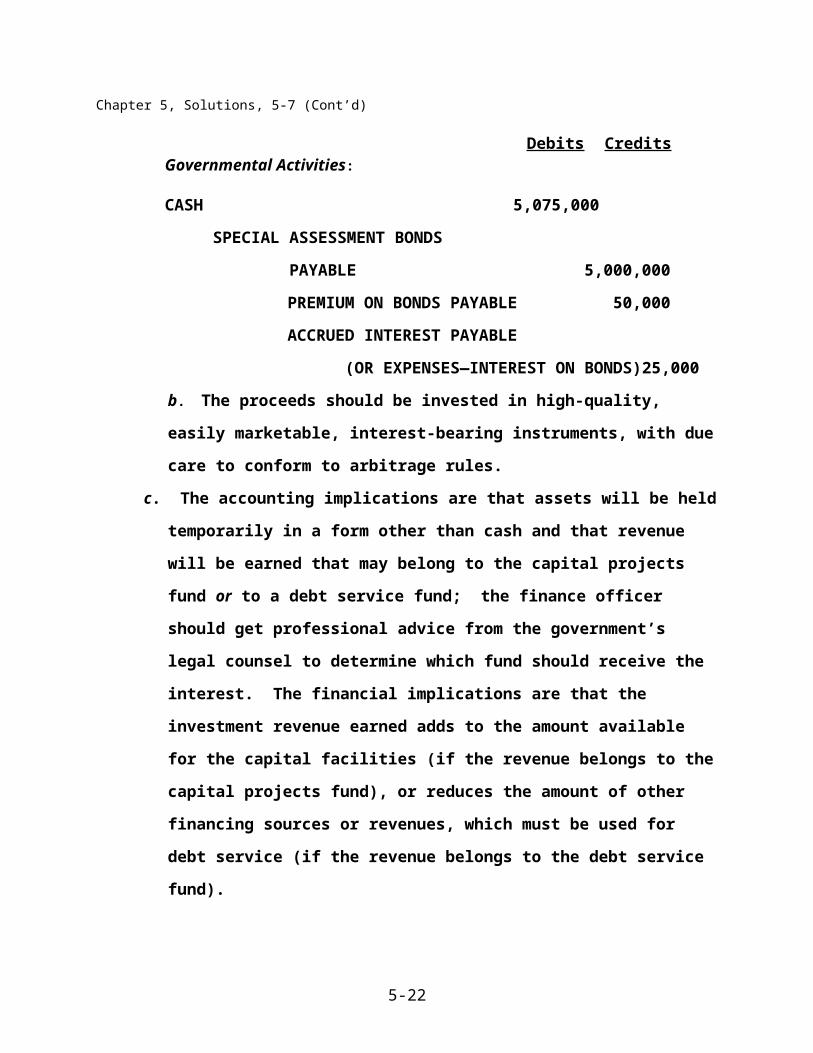

Chapter 5, Solutions, 5-7 (Cont’d)

Debits CreditsGovernmental Activities:

CASH 5,075,000

SPECIAL ASSESSMENT BONDS

PAYABLE 5,000,000

PREMIUM ON BONDS PAYABLE 50,000

ACCRUED INTEREST PAYABLE

(OR EXPENSES—INTEREST ON BONDS) 25,000

b. The proceeds should be invested in high-quality, easily marketable,

interest-bearing instruments, with due care to conform to arbitrage

rules.

c. The accounting implications are that assets will be held temporarily in a

form other than cash and that revenue will be earned that may belong to

the capital projects fund or to a debt service fund; the finance officer

should get professional advice from the government’s legal counsel to

determine which fund should receive the interest. The financial

implications are that the investment revenue earned adds to the amount

available for the capital facilities (if the revenue belongs to the capital

projects fund), or reduces the amount of other financing sources or

revenues, which must be used for debt service (if the revenue belongs

to the debt service fund).

5-13

Chapter 5, Solutions (Cont’d)

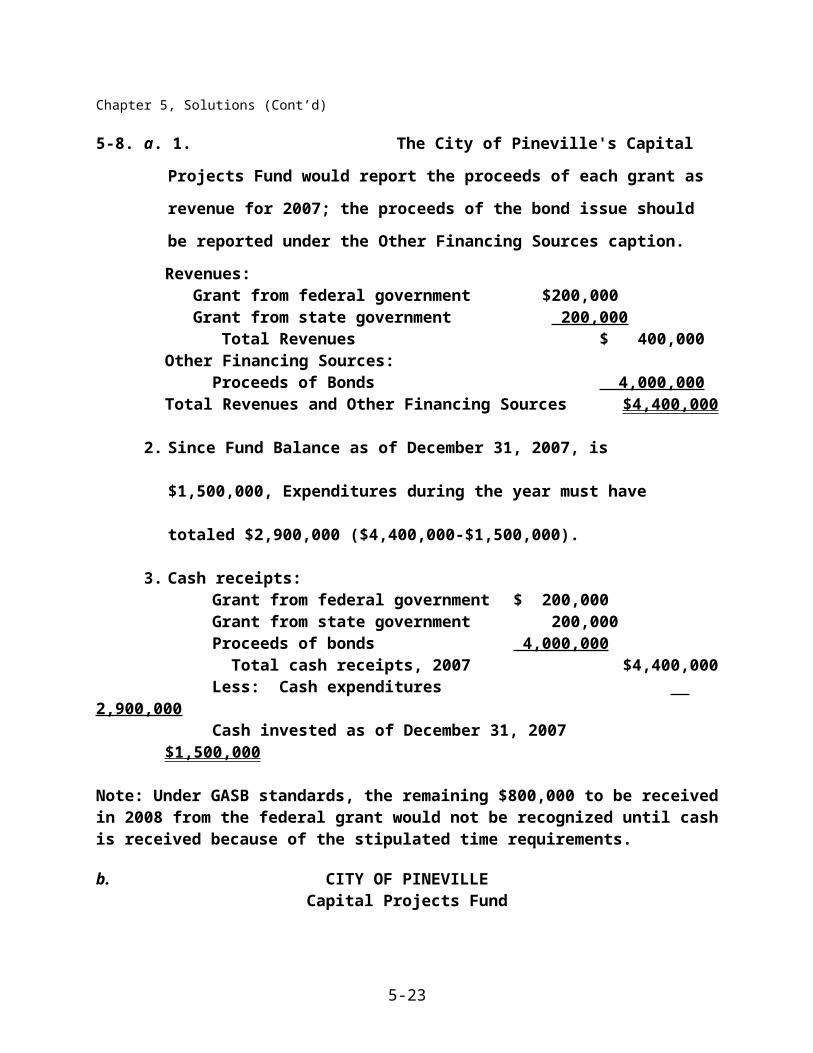

5-8. a. 1. The City of Pineville's Capital Projects Fund would report the proceeds

of each grant as revenue for 2007; the proceeds of the bond issue

should be reported under the Other Financing Sources caption.

Revenues:Grant from federal government $200,000 Grant from state government 200,000 Total Revenues $ 400,000

Other Financing Sources: Proceeds of Bonds 4,000,000

Total Revenues and Other Financing Sources $4,400,000

2. Since Fund Balance as of December 31, 2007, is $1,500,000,

Expenditures during the year must have totaled $2,900,000 ($4,400,000-

$1,500,000).

3. Cash receipts: Grant from federal government $ 200,000 Grant from state government 200,000 Proceeds of bonds 4,000,000 Total cash receipts, 2007 $4,400,000 Less: Cash expenditures 2,900,000 Cash invested as of December 31, 2007 $1,500,000

Note: Under GASB standards, the remaining $800,000 to be received in 2008 from the federal grant would not be recognized until cash is received because of the stipulated time requirements.

b. CITY OF PINEVILLECapital Projects Fund

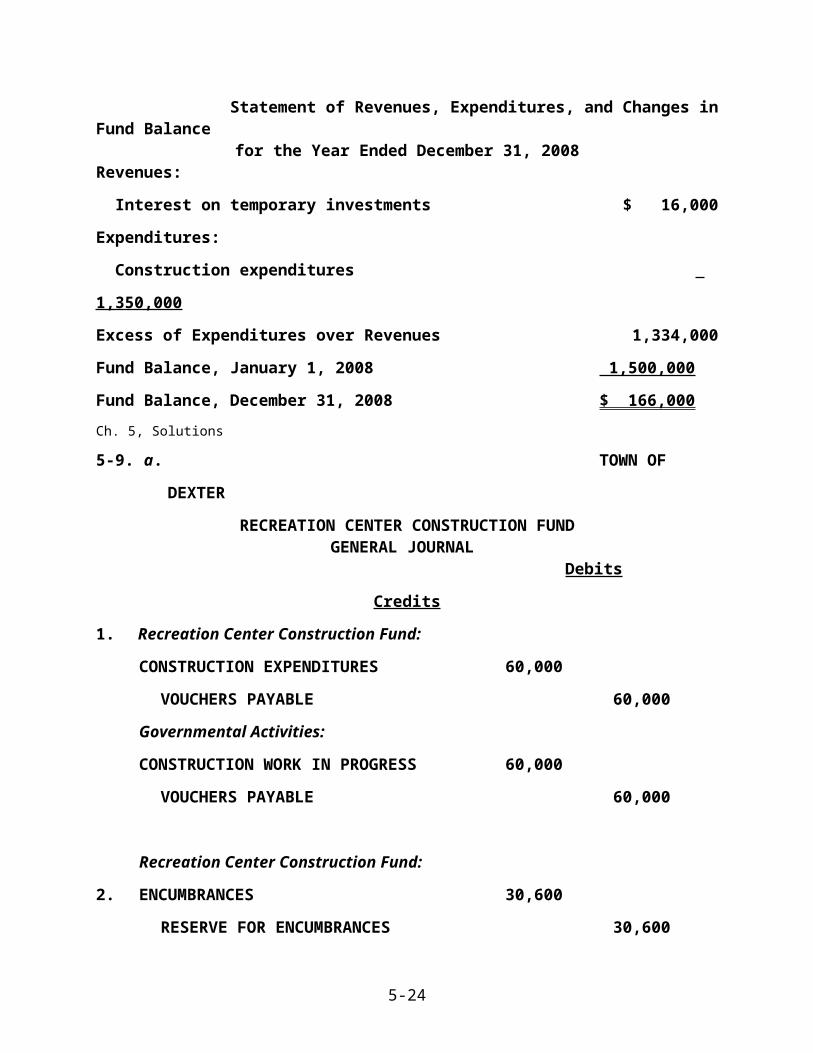

Statement of Revenues, Expenditures, and Changes in Fund Balance for the Year Ended December 31, 2008

Revenues:

Interest on temporary investments $ 16,000

Expenditures:

Construction expenditures 1,350,000

Excess of Expenditures over Revenues 1,334,000

Fund Balance, January 1, 2008 1,500,000

Fund Balance, December 31, 2008 $ 166,000

5-14

Ch. 5, Solutions

5-9. a. TOWN OF DEXTER

RECREATION CENTER CONSTRUCTION FUNDGENERAL JOURNAL

Debits Credits

1. Recreation Center Construction Fund:

CONSTRUCTION EXPENDITURES 60,000

VOUCHERS PAYABLE 60,000

Governmental Activities:

CONSTRUCTION WORK IN PROGRESS 60,000

VOUCHERS PAYABLE 60,000

Recreation Center Construction Fund:

2. ENCUMBRANCES 30,600

RESERVE FOR ENCUMBRANCES 30,600

Governmental Activities:

NO ENTRY REQUIRED

Recreation Center Construction Fund:

3. ENCUMBRANCES 2,500,000

RESERVE FOR ENCUMBRANCES 2,500,000

Governmental Activities:

NO ENTRY REQUIRED

4. Recreation Center Construction Fund:

RESERVE FOR ENCUMBRANCES 30,600

CONSTRUCTION EXPENDITURES 30,500

ENCUMBRANCES 30,600

VOUCHERS PAYABLE 30,500

Governmental Activities:

CONSTRUCTION WORK IN PROGRESS 30,500

VOUCHERS PAYABLE 30,500

5-15

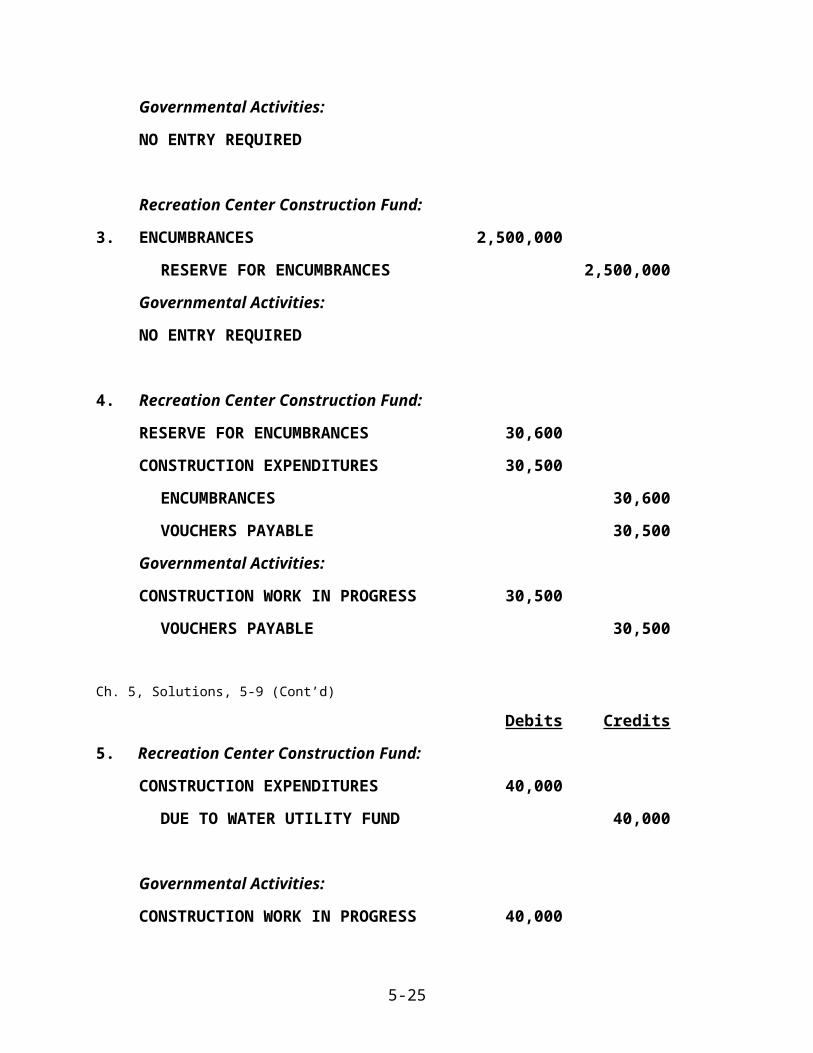

Ch. 5, Solutions, 5-9 (Cont’d)

Debits Credits

5. Recreation Center Construction Fund:

CONSTRUCTION EXPENDITURES 40,000

DUE TO WATER UTILITY FUND 40,000

Governmental Activities:

CONSTRUCTION WORK IN PROGRESS 40,000

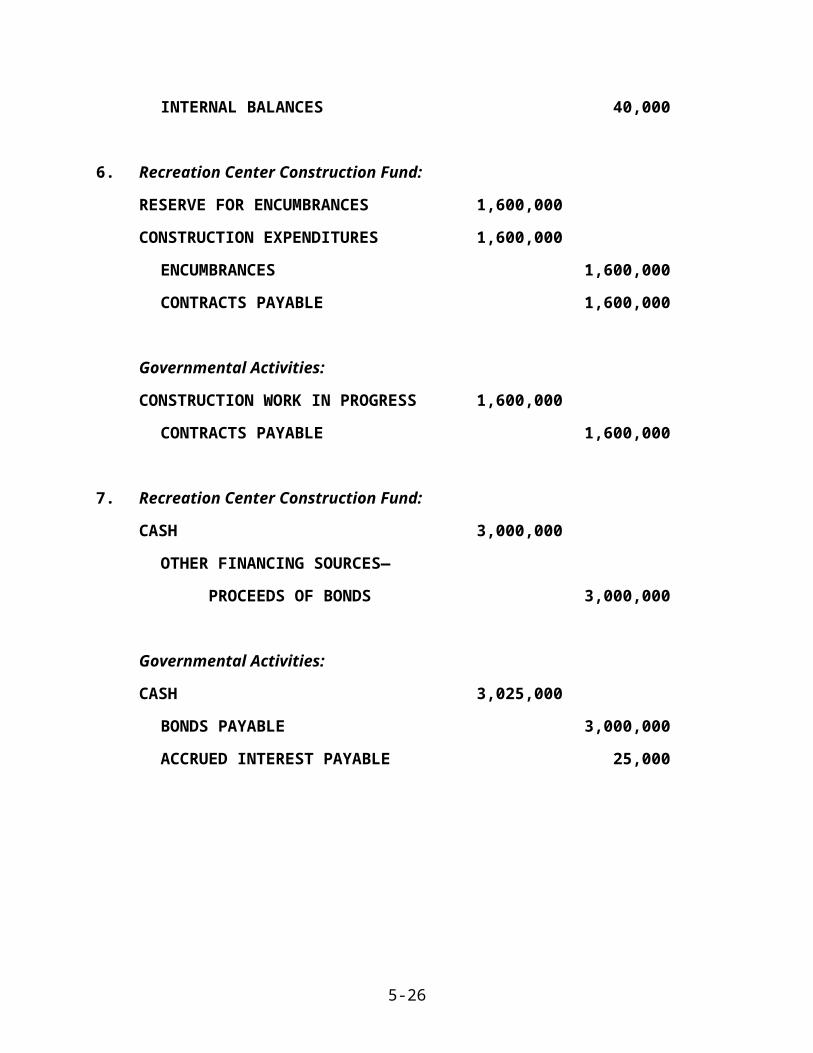

INTERNAL BALANCES 40,000

6. Recreation Center Construction Fund:

RESERVE FOR ENCUMBRANCES 1,600,000

CONSTRUCTION EXPENDITURES 1,600,000

ENCUMBRANCES 1,600,000

CONTRACTS PAYABLE 1,600,000

Governmental Activities:

CONSTRUCTION WORK IN PROGRESS 1,600,000

CONTRACTS PAYABLE 1,600,000

7. Recreation Center Construction Fund:

CASH 3,000,000

OTHER FINANCING SOURCES—

PROCEEDS OF BONDS 3,000,000

Governmental Activities:

CASH 3,025,000

BONDS PAYABLE 3,000,000

ACCRUED INTEREST PAYABLE 25,000

5-16

Ch. 5, Solutions, 5-9 (Cont’d)

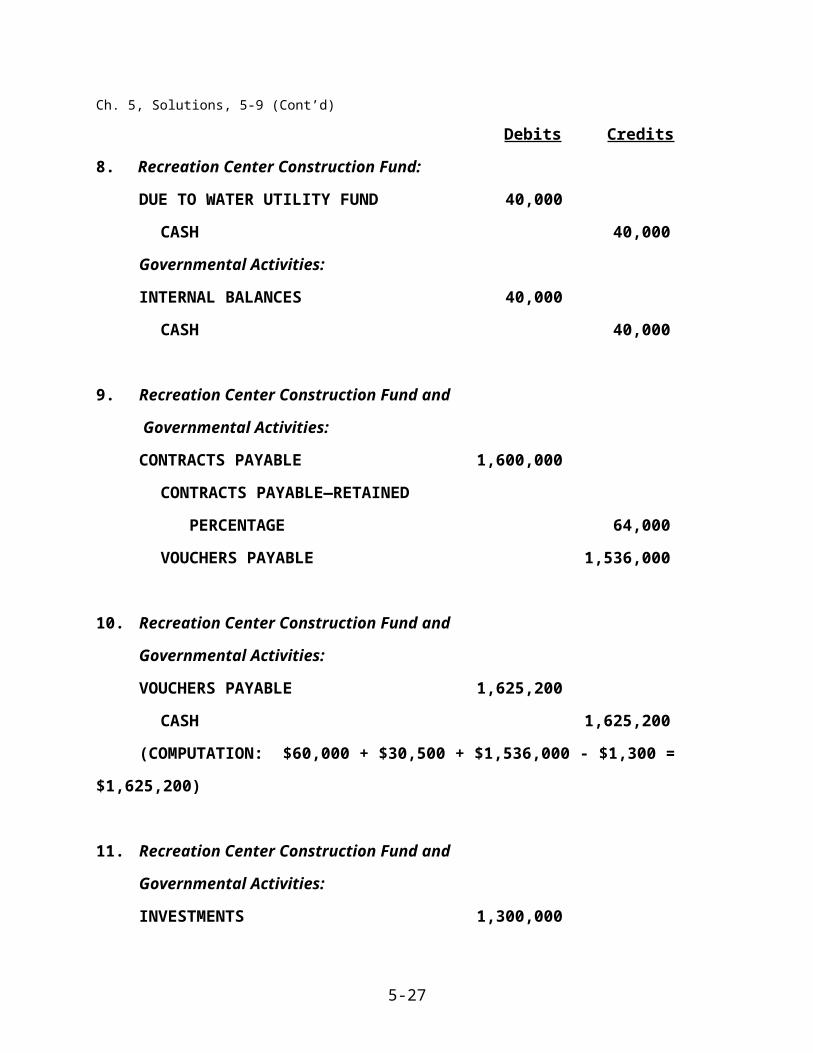

Debits Credits

8. Recreation Center Construction Fund:

DUE TO WATER UTILITY FUND 40,000

CASH 40,000

Governmental Activities:

INTERNAL BALANCES 40,000

CASH 40,000

9. Recreation Center Construction Fund and

Governmental Activities:

CONTRACTS PAYABLE 1,600,000

CONTRACTS PAYABLE—RETAINED

PERCENTAGE 64,000

VOUCHERS PAYABLE 1,536,000

10. Recreation Center Construction Fund and

Governmental Activities:

VOUCHERS PAYABLE 1,625,200

CASH 1,625,200

(COMPUTATION: $60,000 + $30,500 + $1,536,000 - $1,300 = $1,625,200)

11. Recreation Center Construction Fund and

Governmental Activities:

INVESTMENTS 1,300,000

CASH 1,300,000

5-17

Ch. 5, Solutions, 5-9 (Cont’d)

Debits Credits

12. Recreation Center Construction Fund:

OFS—PROCEEDS OF BONDS 3,000,000

CONSTRUCTION EXPENDITURES 1,730,500

ENCUMBRANCES 900,000

FUND BALANCE 369,500

Governmental Activities:

NO CLOSING ENTRY REQUIRED AS THERE ARE NO TEMPORARY

ACCOUNT BALANCES. IF SUFFICIENT INFORMATION HAD BEEN GIVEN,

IT WOULD HAVE BEEN APPROPRIATE TO ACCRUE ADDITIONAL

INFORMATION ON THE BONDS PAYABLE. BUT SINCE NO SUCH

INFORMATION IS PROVIDED, THAT ENTRY IS IGNORED.

5-18

Ch. 5, Solutions, 5-9 (Cont’d)

TOWN OF DEXTER

RECREATION CENTER CONSTRUCTION FUNDGENERAL LEDGER (NOT REQUIRED)

CASH CONTRACTS PAYABLE

(7) 3,000,000 (8) 40,000 (9) 1,600,000 (6) 1,600,000

(10) 1,625,200

(11) 1,300,000

INVESTMENTS VOUCHERS PAYABLE

(11) 1,300,000 (10) 1,625,200 (1) 60,000

(4) 30,500

(9) 1,536,000

CONTRACTS PAYABLE

DUE TO WATER UTILITY FUND RETAINED PERCENTAGE

(8) 40,000 (5) 40,000 (9) 64,000

FUND BALANCE ENCUMBRANCES

(12) 369,500 (2) 30,600 (4) 30,600

(3) 2,500,000

(6) 1,600,000

(12) 900,000

RESERVE FOR ENCUMBRANCES

(4) 30,600 (2) 30,600

(6) 1,600,000 (3) 2,500,000

CONSTRUCTION EXPENDITURES OFS—Proceeds of Bonds

(1) 60,000 (12) 1,730,500 (12) 3,000,000 (7A) 3,000,000

(4) 30,500

(5) 40,000

5-19

(6) 1,600,000

5-20

Ch. 5, Solutions, 5-9 (Cont’d)

b. TOWN OF DEXTER

RECREATION CENTER CONSTRUCTION FUND

BALANCE SHEET

DECEMBER 31, 2008

ASSETS

CASH $ 34,800

INVESTMENTS 1,300,000

TOTAL ASSETS $1,334,800

LIABILITIES AND FUND BALANCES

LIABILITIES:

VOUCHERS PAYABLE $ 1,300

CONTRACTS PAYABLE RETAINED PERCENTAGE 64,000

TOTAL LIABILITIES 65,300

FUND BALANCES:

RESERVED FOR ENCUMBRANCES 900,000

FUND BALANCE 369,500

TOTAL FUND BALANCES 1,269,500

TOTAL LIABILITIES AND FUND BALANCES $1,334,800

5-21

Ch. 5, Solutions, 5-9 (Cont’d)

c. TOWN OF DEXTER

RECREATION CENTER CONSTRUCTION FUND

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES

IN FUND BALANCE

FOR THE PERIOD ENDED DECEMBER 31, 2008

EXPENDITURES:

CONSTRUCTION EXPENDITURES $ 1,730,500

EXCESS OF REVENUES OVER (UNDER) EXPENDITURES (1,730,500)

OTHER FINANCING SOURCES:

PROCEEDS OF BONDS 3,000,000

EXCESS OF REVENUES AND OTHER

FINANCING SOURCES OVER EXPENDITURES 1,269,500

FUND BALANCES, JANUARY 1, 2008 -0-

FUND BALANCES, DECEMBER 31, 2008 $ 1,269,500

d. In the Governmental Activities column of the statement of net assets, the

construction expenditures of $1,730,500 for this year will appear in the

capital assets, net of depreciation row. The capital assets disclosure in the

notes to the financial statements will break this total down by class, such

as construction work in progress (in this case) if the project is not yet

complete, or specific amounts for buildings, equipment and land

improvement. The Governmental Activities column of the statement of

activities will show the depreciation expense on the recreation center when

it is completed, most likely in the functional expense category (row) called

parks and recreation.

5-22

Ch. 5, Solutions

5-10. a. FALTS CITY

STREET IMPROVEMENT FUND

JOURNAL ENTRIES FOR 2008

Debits Credits

1. CASH 100,000

OTHER FINANCING SOURCES—PROCEEDS

OF BOND ANTICIPATION NOTES 100,000

2. DUE FROM FEDERAL GOVERNMENT 750,000

REVENUES 750,000

Note: the $750,000 to be received the following year is a time requirement and

would not be accrued (per GASBS 33).

3. ENCUMBRANCES 2,700,000

RESERVE FOR ENCUMBRANCES 2,700,000

4. CONSTRUCTION EXPENDITURES 60,000

DUE TO OTHER FUNDS 60,000

5. CONSTRUCTION EXPENDITURES 69,000

CASH 69,000

6. CONSTRUCTION EXPENDITURES 18,500

VOUCHERS PAYABLE 18,500

7. RESERVE FOR ENCUMBRANCES 1,000,000

CONSTRUCTION EXPENDITURES 1,000,000

ENCUMBRANCES 1,000,000

CONTRACTS PAYABLE 1,000,000

5-23

Ch. 5, Solutions, 5-10 (Cont’d)

Debits Credits

8. CASH 3,250,000

DUE FROM FEDERAL GOVERNMENT 750,000

OTHER FINANCING SOURCES—

PROCEEDS OF BONDS 2,500,000

9. OTHER FINANCING USES—REPAYMENT OF BANs 100,000

INTEREST EXPENDITURES (NOTE A) 3,000

CASH 103,000

(BANs = BOND ANTICIPATION NOTES)

NOTE A: INTEREST DUE IS CALCULATED AS FOLLOWS:

$100,000 x .06 x 180/360 = $3,000; PER GASBS 37,

INTEREST IS NOT CAPITALIZED FOR GENERAL

CAPITAL ASSETS.

10. CONTRACTS PAYABLE 1,000,000

CONTRACTS PAYABLE—RETAINED PERCENTAGE 50,000

CASH 950,000

11. INVESTMENTS 1,800,000

CASH 1,800,000

5-24

Ch. 5, Solutions, 5-10 (Cont’d)

Debits Credits

12. OTHER FINANCING SOURCES—

PROCEEDS OF BONDS 2,500,000

OTHER FINANCING SOURCES—

PROCEEDS OF BANs 100,000

REVENUES 750,000

FUND BALANCE 399,500

ENCUMBRANCES 1,700,000

OTHER FINANCING USES—REPAYMENT OF BANs 100,000

CONSTRUCTION EXPENDITURES 1,147,500

INTEREST EXPENDITURES 3,000

5-25

Ch. 5, Solutions, 5-10 (Cont’d)

FALTS CITY

STREET IMPROVEMENT FUNDGENERAL LEDGER (NOT REQUIRED)

CASH

(1) 100,000 (5) 69,000

(8) 3,250,000 (9) 103,000

(10) 950,000

(11) 1,800,000

INVESTMENTS

(11) 1,800,000

DUE FROM FEDERAL GOVERNMENT

(2) 750,000 (8) 750,000

VOUCHERS PAYABLE

(6) 18,500

CONTRACTS PAYABLE

(10) 1,000,000 (7) 1,000,000

CONTRACTS PAYABLE RETAINED PERCENTAGE

(10) 50,000

DUE TO OTHER FUNDS

(4) 60,000

5-26

Ch. 5, Solutions, 5-10 (Cont’d)

FUND BALANCE

(12) 399,500

REVENUES

(12) 750,000 (2) 750,000

OFS—PROCEEDS OF BONDS

(12) 2,500,000 (8) 2,500,000

OFS—PROCEEDS OF BOND ANTICIPATION NOTES

(9) 100,000 (1) 100,000

ENCUMBRANCES

(3) 2,700,000 (7) 1,000,000

(12) 1,700,000

RESERVE FOR ENCUMBRANCES

(7) 1,000,000 (3) 2,700,000

CONSTRUCTION EXPENDITURES

(4) 60,000 (12) 1,147,500

(5) 69,000

(6) 18,500

(7) 1,000,000

INTEREST EXPENDITURES

(9) 3,000 (12) 3,000

OTHER FINANCING USES—REPAYMENT OF BANs _ _______

(9) 100,000 (12) 100,000

5-27

Ch. 5, Solutions, 5-10 (Cont’d)

b. FALTS CITY

STREET IMPROVEMENT FUND

BALANCE SHEET, DECEMBER 31, 2008

ASSETS

CASH $ 428,000

INVESTMENTS 1,800,000

TOTAL ASSETS $2,228,000

LIABILITIES AND FUND BALANCES

LIABILITIES:

VOUCHERS PAYABLE $ 18,500

DUE TO OTHER FUNDS 60,000

CONTRACTS PAYABLERETAINED PERCENTAGE 50,000

TOTAL LIABILITIES 128,500

FUND BALANCES:

RESERVED FOR ENCUMBRANCES $1,700,000

FUND BALANCE 399,500

TOTAL FUND BALANCES 2,099,500

TOTAL LIABILITIES AND FUND BALANCES $2,228,000

5-28

Ch. 5, Solutions, 5-10 (Cont’d)

c. FALTS CITY

STREET IMPROVEMENT FUND

STATEMENT OF REVENUES, EXPENDITURES,

AND CHANGES IN FUND BALANCE

FOR THE PERIOD JULY 1, 2008 - DECEMBER 31, 2008

REVENUES:

FEDERAL GRANT $ 750,000

EXPENDITURES:

CONSTRUCTION EXPENDITURES 1,147,500

INTEREST EXPENDITURES 3,000

TOTAL EXPENDITURES 1,150,500

EXCESS OF REVENUES OVER (UNDER)

EXPENDITURES (400,500)

OTHER FINANCING SOURCES AND USES:

PROCEEDS OF BOND ANTICIPATION NOTES 100,000

OTHER FINANCING USES: REPAYMENT OF

BOND ANTICIPATION NOTES (100,000)

PROCEEDS OF BONDS SOLD 2,500,000 2,500,000

EXCESS OF REVENUES AND OTHER

SOURCES OVER EXPENDITURES 2,099,500

FUND BALANCES, JULY 1, 2008 -0-

FUND BALANCES, DECEMBER 31, 2008 $2,099,500

5-29