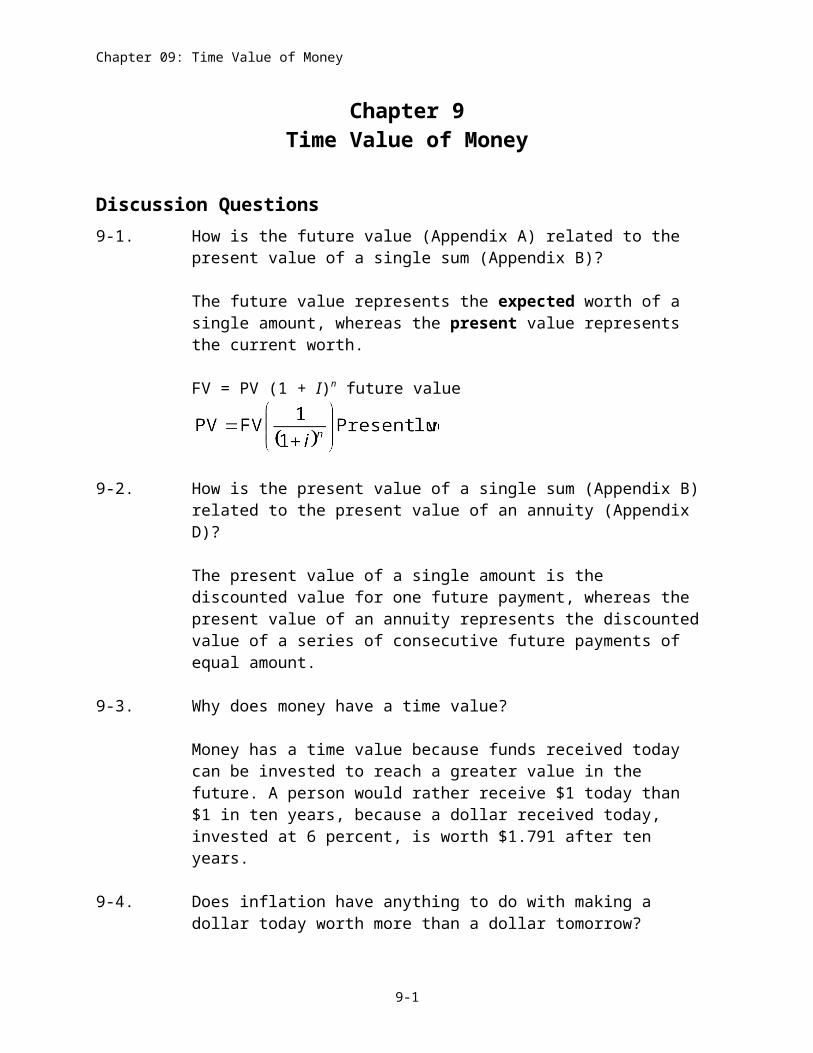

Chapter 09: Time Value of Money Chapter 9 Time Value of Money Discussion Questions 9-1. How is the future value (Appendix A) related to the present value of a single sum (Appendix B)? The future value represents the expected worth of a single amount, whereas the present value represents the current worth. FV = PV (1 + I) n future value 9-2. How is the present value of a single sum (Appendix B) related to the present value of an annuity (Appendix D)? The present value of a single amount is the discounted value for one future payment, whereas the present value of an annuity represents the discounted value of a series of consecutive future payments of equal amount. 9-3. Why does money have a time value? Money has a time value because funds received today can be invested to reach a greater value in the future. A person would rather receive $1 today than $1 in ten years, because a dollar received today, invested at 6 percent, is worth $1.791 after ten years. 9-4. Does inflation have anything to do with making a dollar today worth more than a dollar tomorrow? 9-1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 09: Time Value of Money

Chapter 9Time Value of Money

Discussion Questions9-1. How is the future value (Appendix A) related to the present value of a single

sum (Appendix B)?

The future value represents the expected worth of a single amount, whereas the present value represents the current worth.

FV = PV (1 + I)n future value

9-2. How is the present value of a single sum (Appendix B) related to the present value of an annuity (Appendix D)?

The present value of a single amount is the discounted value for one future payment, whereas the present value of an annuity represents the discounted value of a series of consecutive future payments of equal amount.

9-3. Why does money have a time value?

Money has a time value because funds received today can be invested to reach a greater value in the future. A person would rather receive $1 today than $1 in ten years, because a dollar received today, invested at 6 percent, is worth $1.791 after ten years.

9-4. Does inflation have anything to do with making a dollar today worth more than a dollar tomorrow?

Inflation makes a dollar today worth more than a dollar in the future. Because inflation tends to erode the purchasing power of money, funds received today will be worth more than the same amount received in the future.

9-1

Chapter 09: Time Value of Money

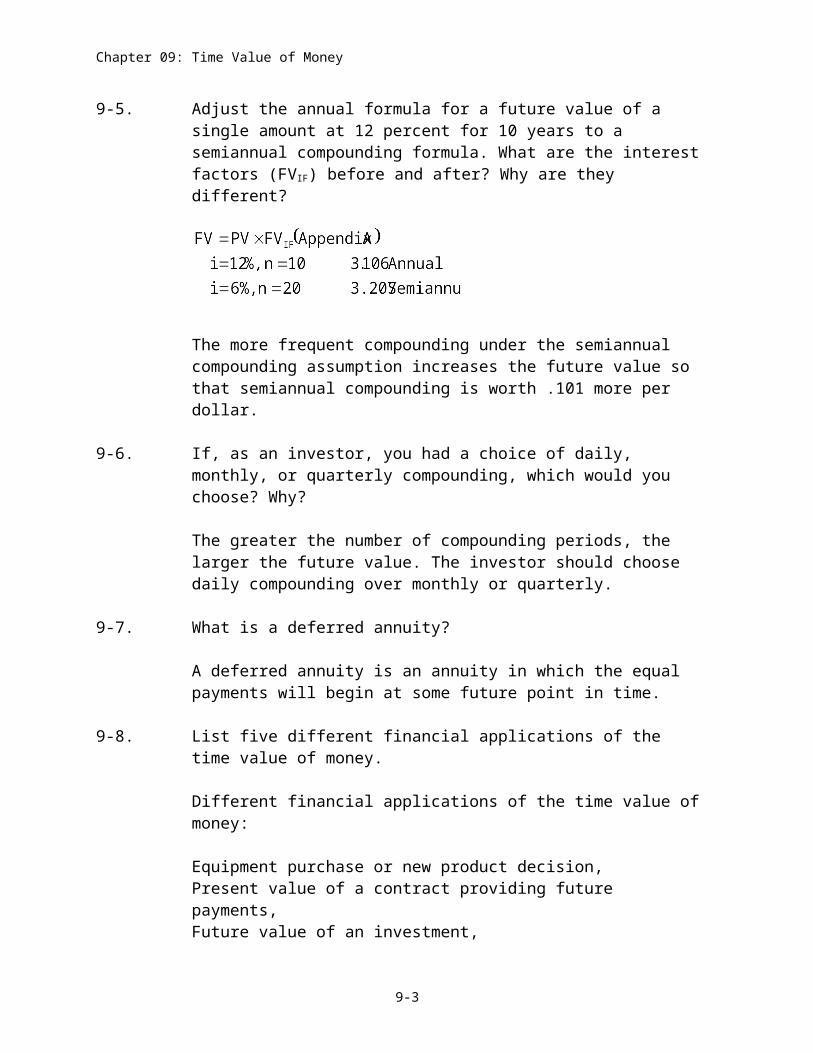

9-5. Adjust the annual formula for a future value of a single amount at 12 percent for 10 years to a semiannual compounding formula. What are the interest factors (FVIF) before and after? Why are they different?

The more frequent compounding under the semiannual compounding assumption increases the future value so that semiannual compounding is worth .101 more per dollar.

9-6. If, as an investor, you had a choice of daily, monthly, or quarterly compounding, which would you choose? Why?

The greater the number of compounding periods, the larger the future value. The investor should choose daily compounding over monthly or quarterly.

9-7. What is a deferred annuity?

A deferred annuity is an annuity in which the equal payments will begin at some future point in time.

9-8. List five different financial applications of the time value of money.

Different financial applications of the time value of money:

Equipment purchase or new product decision,Present value of a contract providing future payments,Future value of an investment,Regular payment necessary to provide a future sum,Regular payment necessary to amortize a loan,Determination of return on an investment,Determination of the value of a bond.

Chapter 9

Problems

1. Future value (LO2) You invest $2,500 a year for three years at 8 percent.a. What is the value of your investment after one year? Multiply $2,500 × 1.08.b. What is the value of your investment after two years? Multiply your answer to part a

by 1.08.

9-2

Chapter 09: Time Value of Money

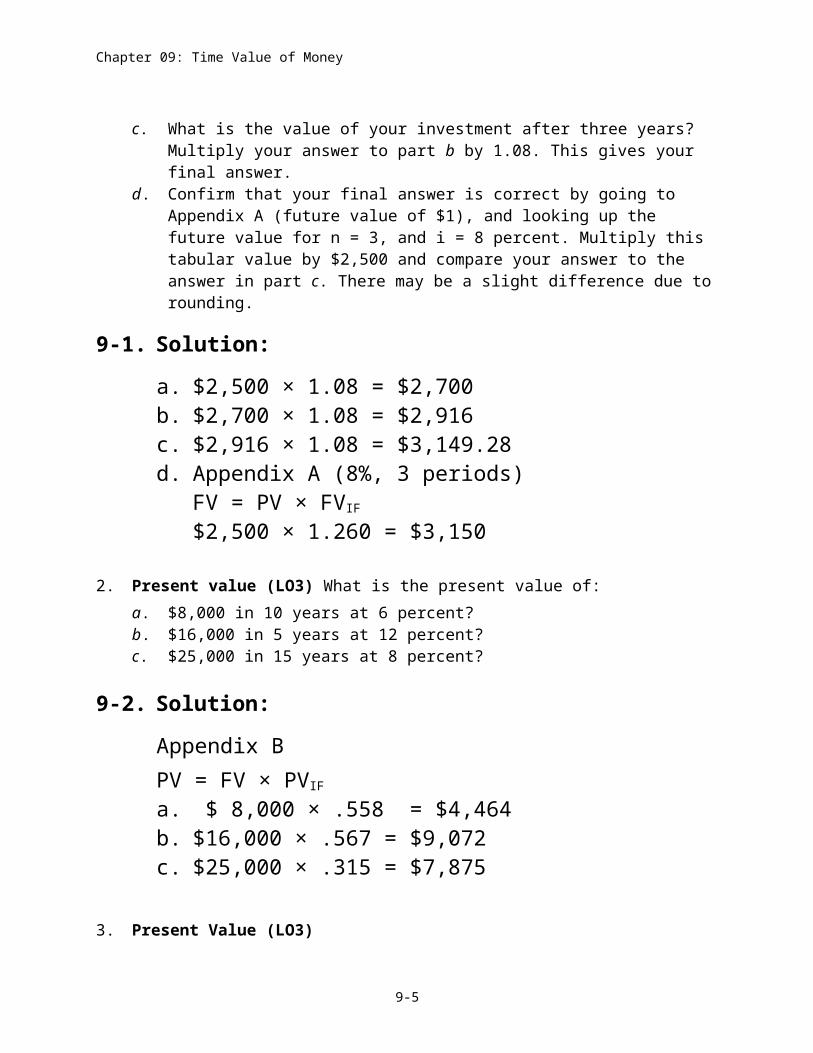

c. What is the value of your investment after three years? Multiply your answer to part b by 1.08. This gives your final answer.

d. Confirm that your final answer is correct by going to Appendix A (future value of $1), and looking up the future value for n = 3, and i = 8 percent. Multiply this tabular value by $2,500 and compare your answer to the answer in part c. There may be a slight difference due to rounding.

9-1. Solution:

a. $2,500 × 1.08 = $2,700b. $2,700 × 1.08 = $2,916c. $2,916 × 1.08 = $3,149.28d. Appendix A (8%, 3 periods)

FV = PV × FVIF

$2,500 × 1.260 = $3,150

2. Present value (LO3) What is the present value of:a. $8,000 in 10 years at 6 percent?b. $16,000 in 5 years at 12 percent?c. $25,000 in 15 years at 8 percent?

9-2. Solution:

Appendix BPV = FV × PVIF

a. $ 8,000 × .558 = $4,464b. $16,000 × .567 = $9,072c. $25,000 × .315 = $7,875

3. Present Value (LO3) a. What is the present value of $100,000 to be received after 40 years with an

18 percent discount rate?b. Would the present value of the funds in part a be enough to buy a $125 concert

ticket?

9-3. Solution:

9-3

Chapter 09: Time Value of Money

Appendix BPV = FV × PVIF (18%, 40 periods)

a. $100,000 × .001 = $100b. NO. You only have $100 in present value.

4. Present Value (LO4) You will receive $4,000 three years from now. The discount rate is 10 percent.a. What is the value of your investment two years from now? Multiply $4,000 × .909

(one year’s discount rate at 10 percent).b. What is the value of your investment one year from now? Multiply your answer to

part a by .909 (one year’s discount rate at 10 percent).c. What is the value of your investment today? Multiply your answer to part b by .909

(one year’s discount rate at 10 percent).d. Confirm that your answer to part c is correct by going to Appendix B (present value

of $1) for n = 3 and i = 10%. Multiply this tabular value by $4,000 and compare your answer to part c. There may be a slight difference due to rounding.

9-4. Solution:

a. $4,000 × .909 = $3,636b. $3,636 × .909 = $3,305.12c. $3,305.12 × .909 = $3,004.35d. Appendix B (10%, 3 periods)

FV = FV × PVIF

$4,000 ×.751 = $3,004.00

5. Future value (LO2) If you invest $12,000 today, how much will you have:a. In 6 years at 7 percent?b. In 15 years at 12 percent?c. In 25 years at 10 percent?d. In 25 years at 10 percent (compounded semiannually)?

9-5. Solution:

Appendix AFV = PV × FVIF

9-4

Chapter 09: Time Value of Money

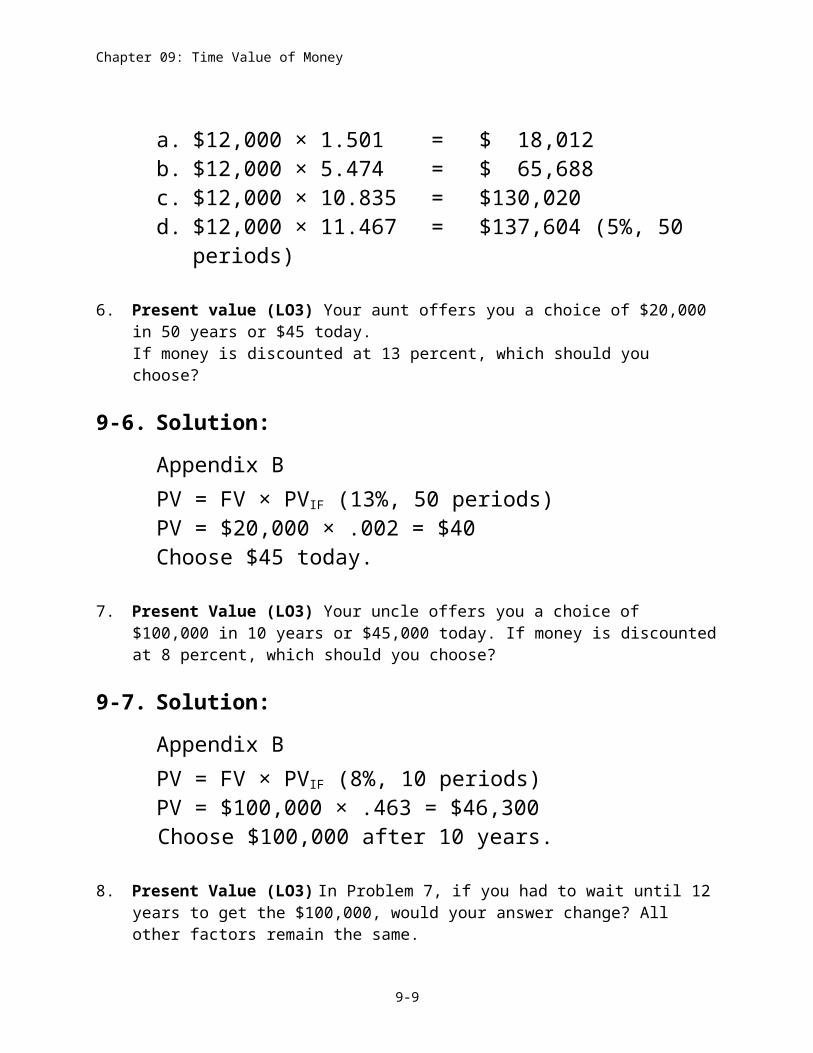

a. $12,000 × 1.501 = $ 18,012b. $12,000 × 5.474 = $ 65,688c. $12,000 × 10.835 = $130,020d. $12,000 × 11.467 = $137,604 (5%, 50 periods)

6. Present value (LO3) Your aunt offers you a choice of $20,000 in 50 years or $45 today. If money is discounted at 13 percent, which should you choose?

9-6. Solution:

Appendix BPV = FV × PVIF (13%, 50 periods)PV = $20,000 × .002 = $40Choose $45 today.

7. Present Value (LO3) Your uncle offers you a choice of $100,000 in 10 years or $45,000 today. If money is discounted at 8 percent, which should you choose?

9-7. Solution:

Appendix BPV = FV × PVIF (8%, 10 periods)PV = $100,000 × .463 = $46,300Choose $100,000 after 10 years.

8. Present Value (LO3) In Problem 7, if you had to wait until 12 years to get the $100,000, would your answer change? All other factors remain the same.

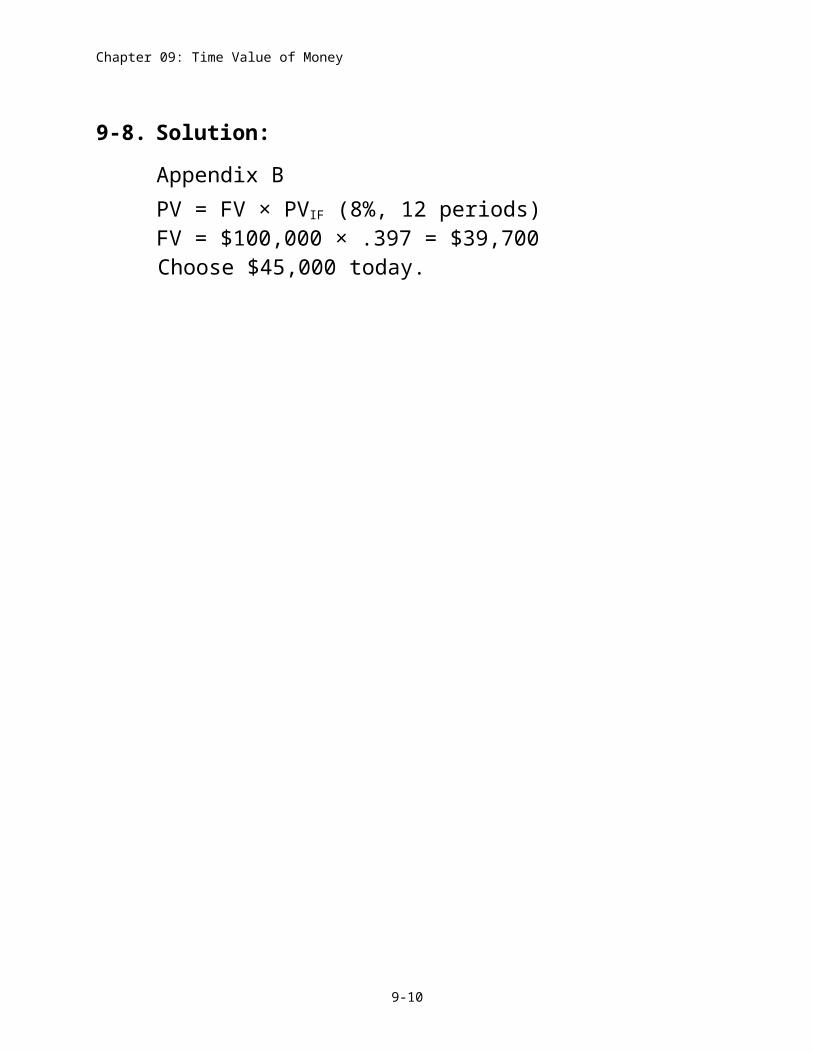

9-8. Solution:

Appendix BPV = FV × PVIF (8%, 12 periods)FV = $100,000 × .397 = $39,700Choose $45,000 today.

9-5

Chapter 09: Time Value of Money

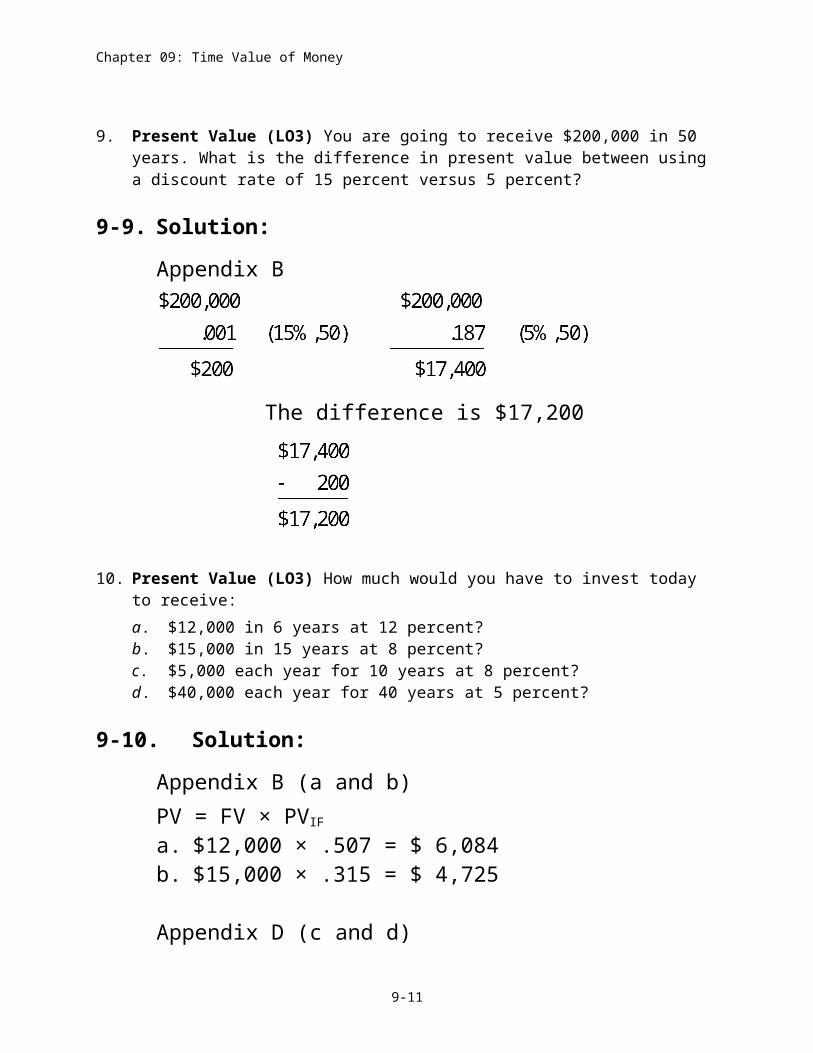

9. Present Value (LO3) You are going to receive $200,000 in 50 years. What is the difference in present value between using a discount rate of 15 percent versus 5 percent?

9-9. Solution:

Appendix B

The difference is $17,200

10. Present Value (LO3) How much would you have to invest today to receive:a. $12,000 in 6 years at 12 percent?b. $15,000 in 15 years at 8 percent?c. $5,000 each year for 10 years at 8 percent?d. $40,000 each year for 40 years at 5 percent?

9-10. Solution:

Appendix B (a and b)PV = FV × PVIF

a. $12,000 × .507 = $ 6,084b. $15,000 × .315 = $ 4,725

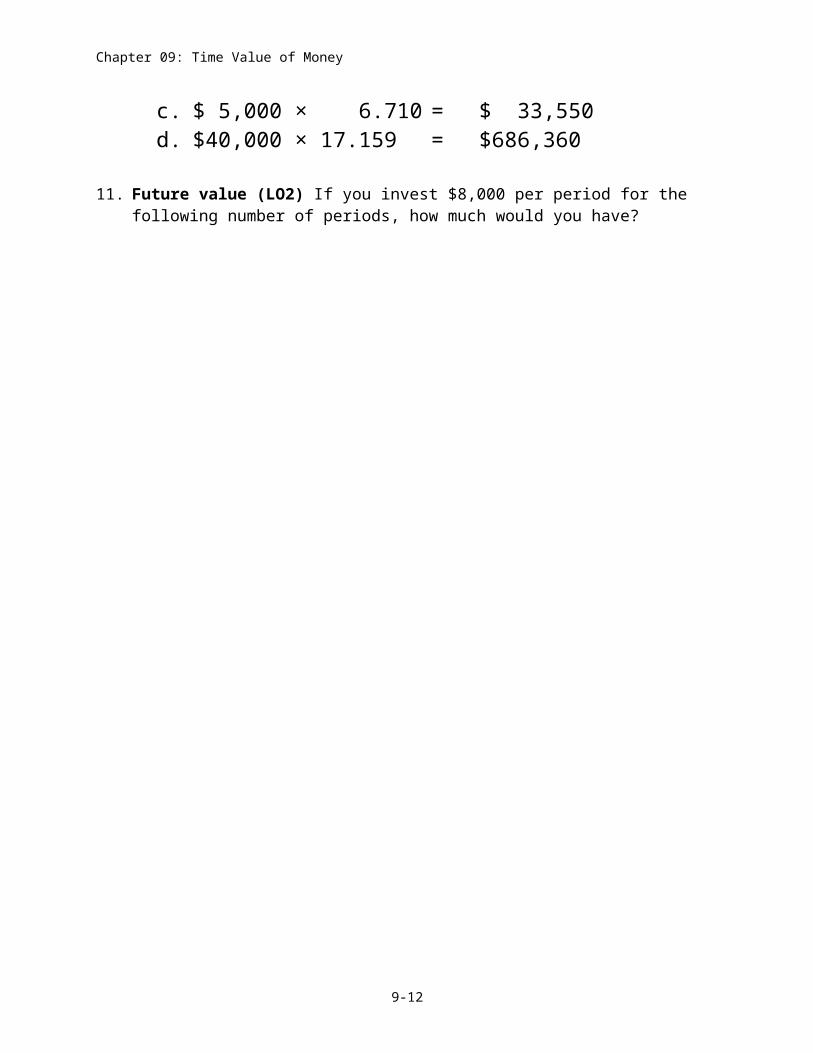

Appendix D (c and d)c. $ 5,000 × 6.710 = $ 33,550d. $40,000 × 17.159 = $686,360

11. Future value (LO2) If you invest $8,000 per period for the following number of periods, how much would you have?

9-6

Chapter 09: Time Value of Money

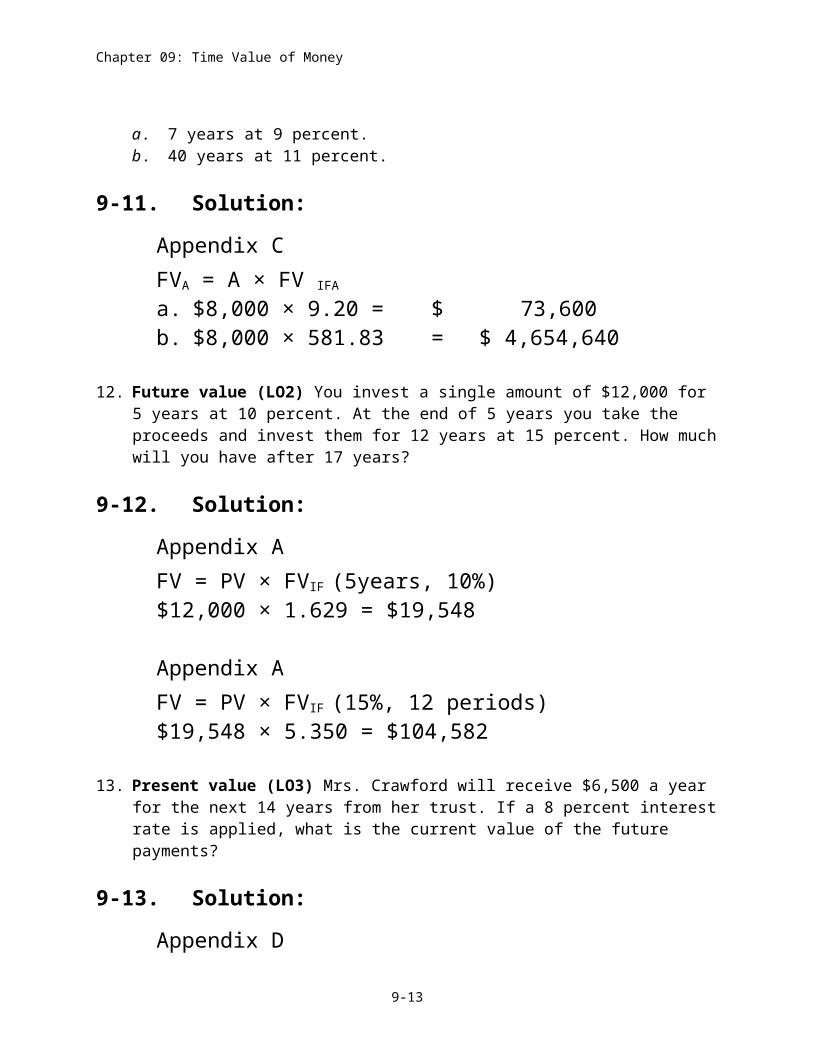

a. 7 years at 9 percent.b. 40 years at 11 percent.

9-11. Solution:

Appendix CFVA = A × FV IFA

a. $8,000 × 9.20 = $ 73,600b. $8,000 × 581.83 = $ 4,654,640

12. Future value (LO2) You invest a single amount of $12,000 for 5 years at 10 percent. At the end of 5 years you take the proceeds and invest them for 12 years at 15 percent. How much will you have after 17 years?

9-12. Solution:

Appendix AFV = PV × FVIF (5years, 10%)$12,000 × 1.629 = $19,548

Appendix AFV = PV × FVIF (15%, 12 periods)$19,548 × 5.350 = $104,582

13. Present value (LO3) Mrs. Crawford will receive $6,500 a year for the next 14 years from her trust. If a 8 percent interest rate is applied, what is the current value of the future payments?

9-13. Solution:

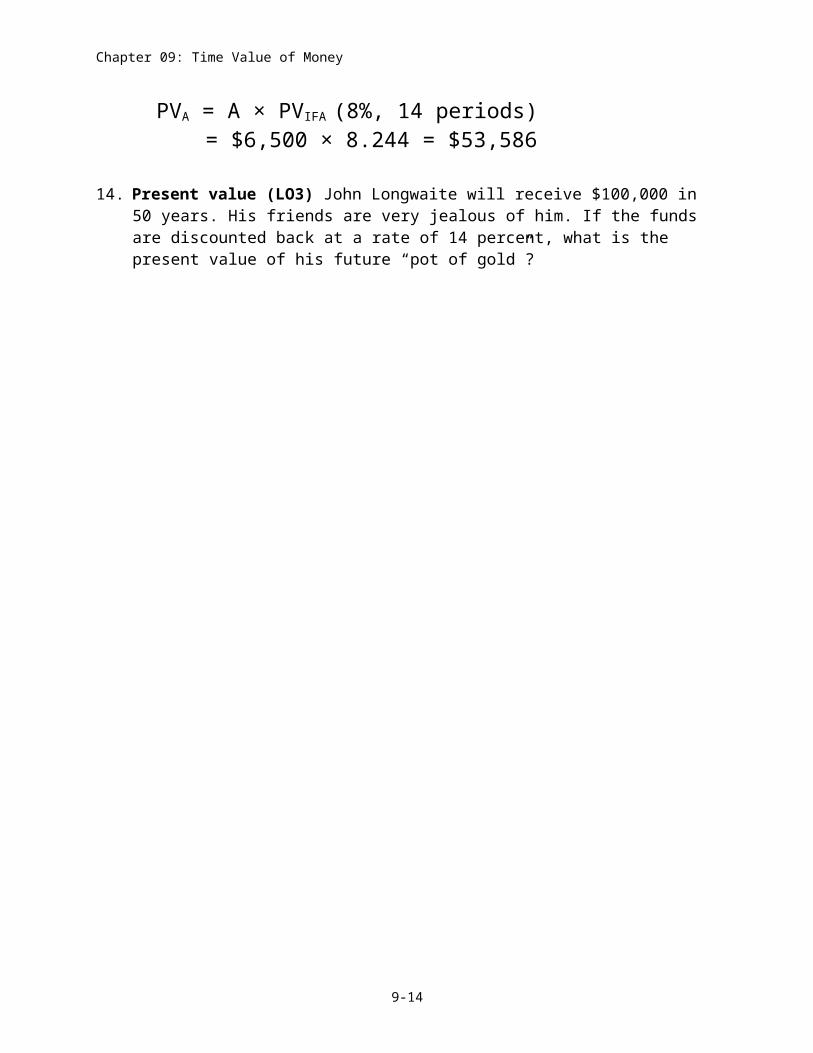

Appendix DPVA = A × PVIFA (8%, 14 periods)

= $6,500 × 8.244 = $53,586

14. Present value (LO3) John Longwaite will receive $100,000 in 50 years. His friends are very jealous of him. If the funds are discounted back at a rate of 14 percent, what is the present value of his future “pot of gold”?

9-7

Chapter 09: Time Value of Money

9-14. Solution:

Appendix BPV = FV × PVIF (14%, 50 periods)

= $100,000 × .001 = $100

15. Present Value (LO3) Sherwin Williams will receive $18,000 a year for the next 25 years as a result of a picture he has painted. If a discount rate of 10 percent is applied, should he be willing to sell out his future rights now for $160,000?

9-15. Solution:

Appendix DPVA = A × PVIFA (10%, 25 periods)PVA = $18,000 × 9.077 = $163,386No, the present value of the annuity is worth more than $160,000.

16. Present value (LO3) General Mills will receive $27,500 per year for the next 10 years as a payment for a weapon he invented. If a 12 percent rate is applied, should he be willing to sell out his future rights now for $160,000?

9-16. Solution:

Appendix DPVA = A × PVIFA (12%, 10 periods)PVA = $27,500 × 5.650 = $155,375Yes, the present value of the annuity is worth less than $160,000.

17. Present value (LO3) The Western Sweepstakes has just informed you that you have won $1 million. The amount is to be paid out at the rate of $50,000 a year for the next 20 years. With a discount rate of 12 percent, what is the present value of your winnings?

9-17. Solution:

Appendix DPVA = A × PVIFA (12%, 20 periods)PVA = $50,000 × 7.469 = $373,450

9-8

Chapter 09: Time Value of Money

18. Present value (LO3) Rita Gonzales won the $60 million lottery. She is to receive $1 million a year for the next 50 years plus an additional lump sum payment of $10 million after 50 years. The discount rate is 10 percent. What is the current value of her winnings?

9-18. Solution:

Appendix DPVA = A × PVIFA (10%, 50 periods)PVA = $1,000,000 × 9.915 = $9,915,000

Appendix BPV = FV × PVIF (10%, 50 periods)PV = $10,000,000 × .009 = $90,000

$ 9,915,000 90,000$10,005,000

19. Future value (LO2) Bruce Sutter invests $2,000 in a mint condition Nolan Ryan baseball card. He expects the card to increase in value 20 percent a year for the next five years. After that, he anticipates a 15 percent annual increase for the next three years. What is the projected value of the card after eight years?

9-19. Solution:

Appendix AFV = PV × FVIF (20%, 5 periods)

= $2,000 × 2.488 = $4,976FV = PV × FVIF (15%, 3 periods)

= $4,976 × 1.521 = $7,568.50

20. Future value (LO2) Christy Reed has been depositing $1,500 in her savings account every December since 2001. Her account earns 6 percent compounded annually. How much will she have in December 2010? (Assume that a deposit is made in December of 2010. Make sure to count the years carefully.)

9-9

Chapter 09: Time Value of Money

9-20. Solution:

Appendix CFVA = A × FVIFA (6%, n = 10)FVA = $1,500 × 13.181 = $19,771.50

21. Future value (LO2) At a growth (interest) rate of 8 percent annually, how long will it take for a sum to double? To triple? Select the year that is closest to the correct answer.

9-21. Solution:

Appendix A

If the sum is doubling, then the tabular value must equal 2.

In Appendix A, looking down the 8% column, we find the factor closest to 2 (1.999) on the 9-year row. The factor closest to 3 (2.937) is on the 14-year row.

22. Present value (LO3) If you owe $30,000 payable at the end of five years, what amount should your creditor accept in payment immediately if she could earn 11 percent on her money?

9-22. Solution:

Appendix BPV = FV × PVIF (11%, 5 periods)PV = $30,000 × .593 = $17,790

23. Present value (LO3) Barney Smith invests in a stock that will pay dividends of $3.00 at the end of the first year; $3.30 at the end of the second year; and $3.60 at the end of the third year. Also, he believes that at the end of the third year he will be able to sell the stock for $50. What is the present value of all future benefits if a discount rate of 11 percent is applied? (Round all values to two places to the right of the decimal point.)

9-23. Solution:

9-10

Chapter 09: Time Value of Money

Appendix BPV = FV × PVIF

Discount rate = 11%

$ 3.00 × .901 = $ 2.70 3.30 × .812 = 2.68 3.60 × .731 = 2.63 50.00 × .731 = 36 .55

$44.56

24. Present value (LO3) Mr. Flint retired as president of Color Title Company but is currently on a consulting contract for $45,000 per year for the next 10 years.a. If Mr. Flint’s opportunity cost (potential return) is 10 percent, what is the present

value of his consulting contract?b. Assuming that Mr. Flint will not retire for two more years and will not start to receive

his 10 payments until the end of the third year, what would be the value of his deferred annuity?

9-24. Solution:

Using a Two Step Procedure

Appendix Da. PVA = A × PVIFA (i = 10%, 10 periods)

= $45,000 × 6.145 = $276,525

Appendix Bb. PV = FV × PVIF (i = 10%, 2 periods)

$276,525 × .826 = $228,410

Alternative SolutionAppendix Da. PVA = A × PVIFA (10%, 10 periods)

9-11

Chapter 09: Time Value of Money

PVA = $45,000 × 6.145 = $276,525

9-12

Chapter 09: Time Value of Money

b. Deferred annuity-Appendix DPVA = $45,000 (6.814 – 1.736) where n = 12; n = 2 and i = 10%

= $45,000(5.078) = $228,510 (or use a two step solution)

The answer is slightly different from the answer above due to rounding in the tables.

25 Quarterly compounding (LO5) Cousin Bertha invested $100,000 10 years ago at 12 percent, compounded quarterly. How much has she accumulated?

9-25. Solution:

Appendix AFV = PV × FVIF (3%, 40 periods)FV = $100,000 × 3.262 = $326,200

26. Special compounding (LO5) Determine the amount of money in a savings account at the end of five years, given an initial deposit of $3,000 and a 8 percent annual interest rate when interest is compounded (a) annually, (b) semiannually, and (c) quarterly.

9-26. Solution:

Appendix AFV = PV × FVIF

a. $3,000 × 1.469 = $4,407 (n=5; i=8%)b. $3,000 × 1.480 = $4,440 (n=10; i=4%)c. $3,000 × 1.486 = $4,458 (n=20; i=2%)

9-13

Chapter 09: Time Value of Money

27. Annuity due (LO4) As stated in the chapter, annuity payments are assumed to come at the end of each payment period (termed an ordinary annuity). However, an exception occurs when the annuity payments come at the beginning of each period (termed an annuity due). To find the present value of an annuity due, subtract 1 from n and add 1 to the tabular value. To find the future value of an annuity, add 1 to n and subtract 1 from the tabular value. For example, to find the future value of a $100 payment at the beginning of each period for five periods at 10 percent, go to Appendix C for n = 6 and i = 10 percent. Look up the value of 7.716 and subtract 1 from it for an answer of 6.716 or $671.60 ($100 × 6.716).

What is the future value of a 10-year annuity of $2,000 per period where payments come at the beginning of each period? The interest rate is 8 percent.

9-27. Solution:

Appendix CFVA = A × FVIFA

n = 11, i = 8% 16.645 – 1 = 15.645FVA = $2,000 × 15.645 = $31,290

28. Annuity due (LO4) Related to the discussion in problem 27, what is the present value of a 10-year annuity of $3,000 per period in which payments come at the beginning of each period? The interest rate is 12 percent.

9-28. Solution:

Appendix DPVA = A × PVIFA

n = 9, i = 12% 5.328 + 1 = 6.328PVA = $3,000 × 6.328 = $18,984

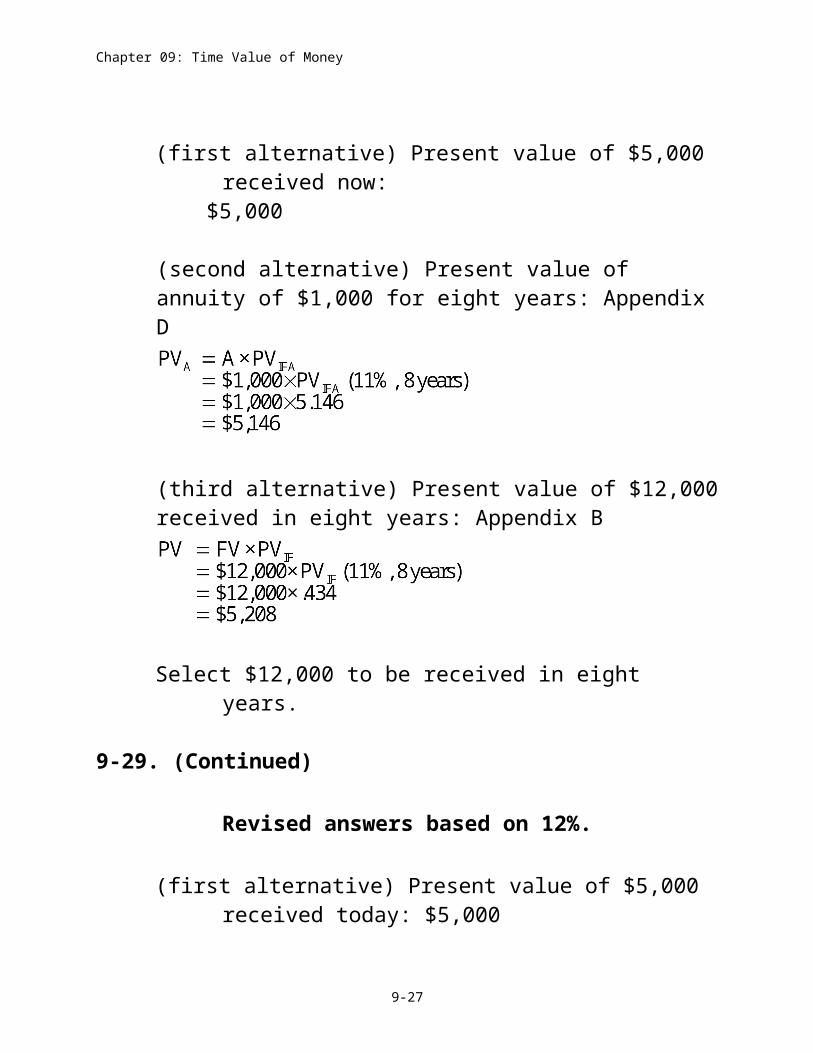

29. Present value alternative (LO3) Your grandfather has offered you a choice of one of the three following alternatives: $5,000 now; $1,000 a year for eight years; or $12,000 at the end of eight years. Assuming you could earn 11 percent annually, which alternative should you choose? If you could earn 12 percent annually, would you still choose the same alternative?

9-29. Solution:

9-14

Chapter 09: Time Value of Money

(first alternative) Present value of $5,000 received now: $5,000

(second alternative) Present value of annuity of $1,000 for eight years: Appendix D

(third alternative) Present value of $12,000 received in eight years: Appendix B

Select $12,000 to be received in eight years.

9-29. (Continued)

Revised answers based on 12%.

(first alternative) Present value of $5,000 received today: $5,000

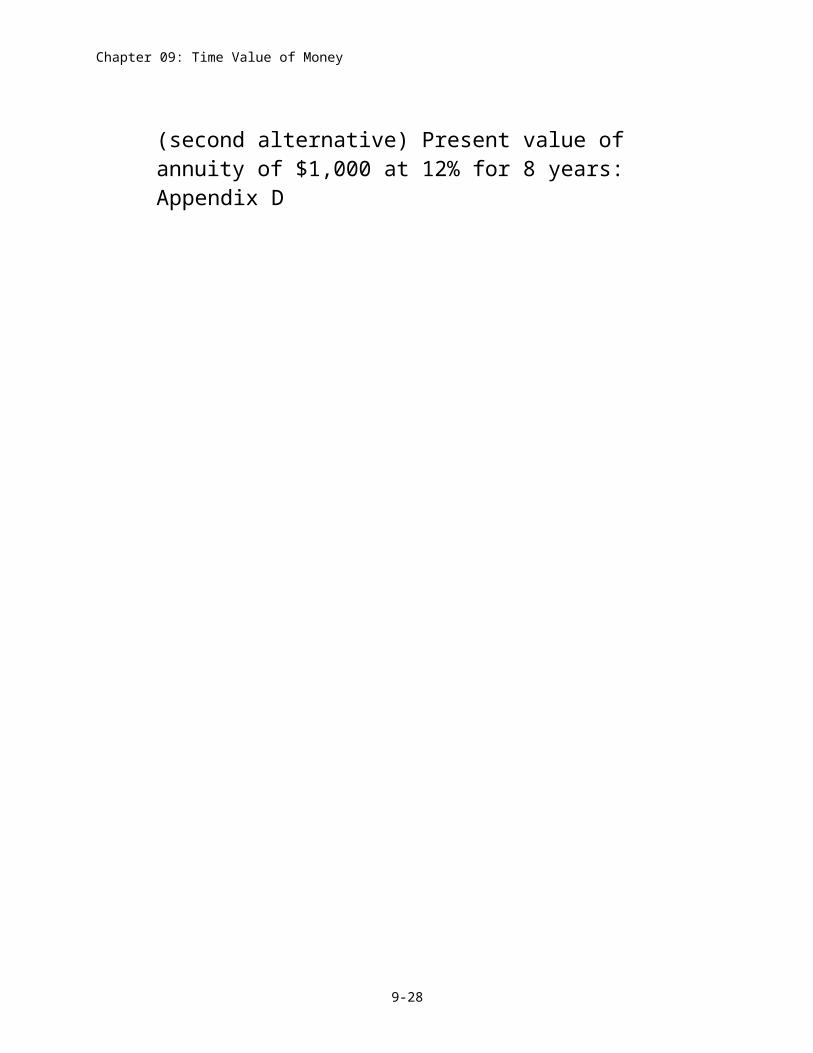

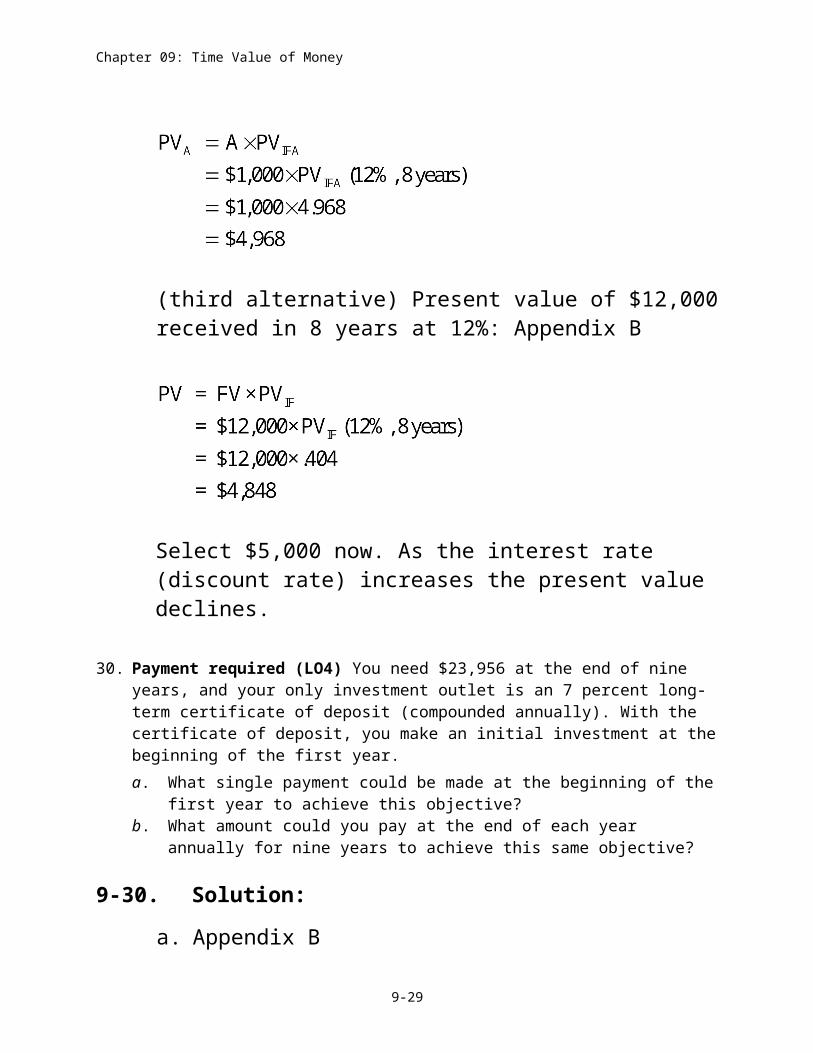

(second alternative) Present value of annuity of $1,000 at 12% for 8 years: Appendix D

9-15

Chapter 09: Time Value of Money

(third alternative) Present value of $12,000 received in 8 years at 12%: Appendix B

Select $5,000 now. As the interest rate (discount rate) increases the present value declines.

30. Payment required (LO4) You need $23,956 at the end of nine years, and your only investment outlet is an 7 percent long-term certificate of deposit (compounded annually). With the certificate of deposit, you make an initial investment at the beginning of the first year.a. What single payment could be made at the beginning of the first year to achieve this

objective?b. What amount could you pay at the end of each year annually for nine years to achieve

this same objective?

9-30. Solution:

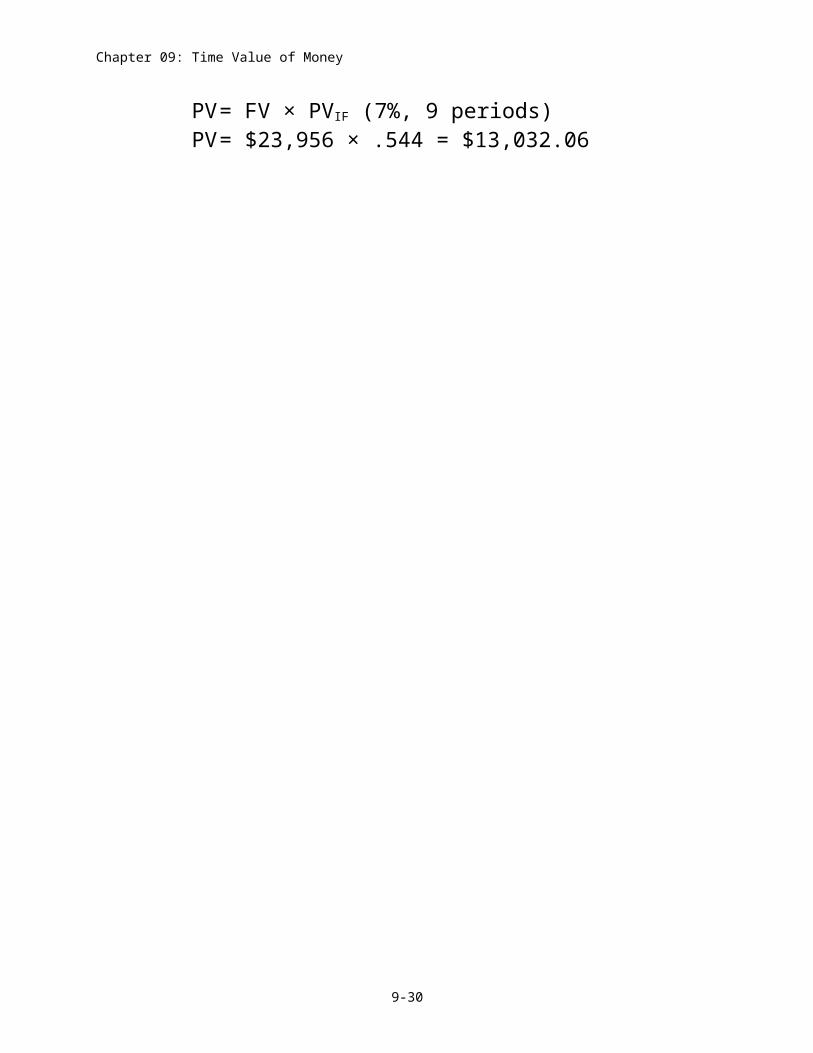

a. Appendix BPV= FV × PVIF (7%, 9 periods)PV= $23,956 × .544 = $13,032.06

9-16

Chapter 09: Time Value of Money

b. Appendix CA = FVA/FVIFA

A = $23,956/11.978 = $2,000 per year

31. Quarterly compounding (LO5) Beverly Hills started a paper route on January 1, 2004. Every three months, she deposits $300 in her bank account, which earns 8 percent annually but is compounded quarterly. On December 31, 2007, she used the entire balance in her bank account to invest in an investment at 12 percent annually. How much will she have on December 31, 2010?

9-31. Solution:

Appendix CFVA = A × FVIFA (2%, 16 periods)FVA = $300 × 18.639 = $5,591.70 after four years

Appendix AFV = PV × FVIF (12%, 3 periods)FV = $5,591.70 × 1.405FV = $7,856.34 after three more years

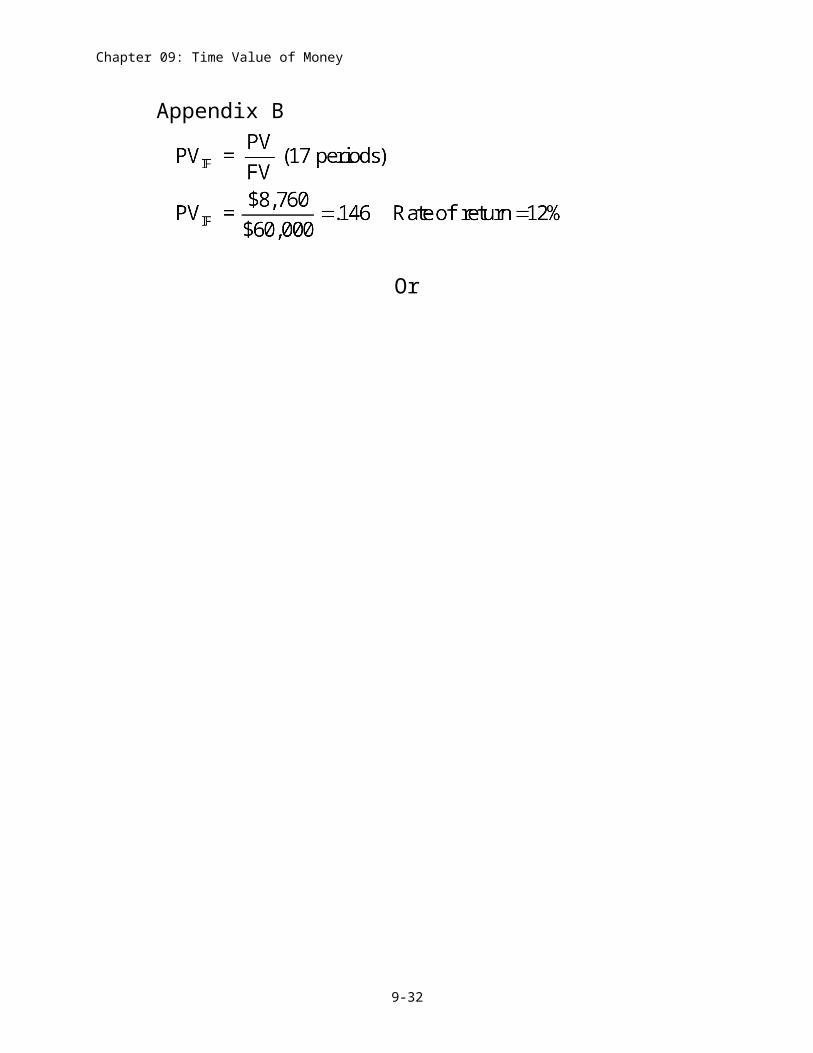

32. Yield (LO4) Franklin Templeton has just invested $8,760 for her son (age one). This money will be used for his son’s education 17 years from now. He calculates that he will need $60,000 by the time the boy goes to school. What rate of return will Mr. Templeton need in order to achieve this goal?

9-32. Solution:

Appendix B

Or

9-17

Chapter 09: Time Value of Money

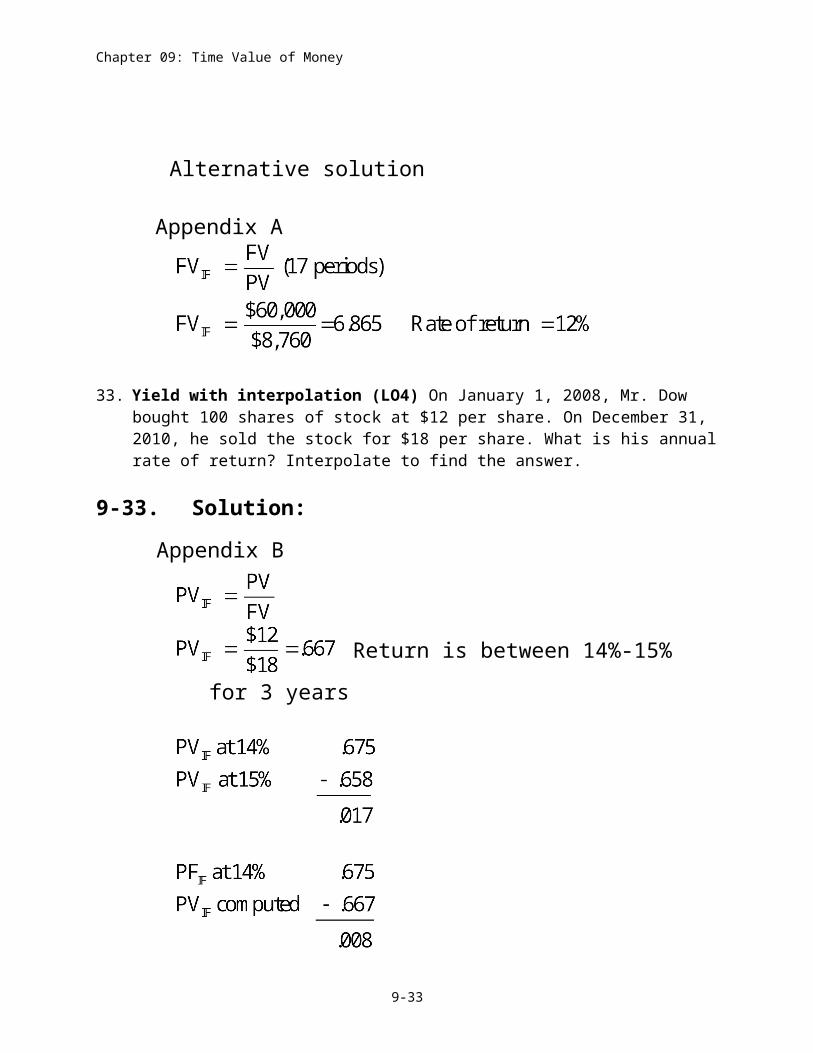

Alternative solution

Appendix A

33. Yield with interpolation (LO4) On January 1, 2008, Mr. Dow bought 100 shares of stock at $12 per share. On December 31, 2010, he sold the stock for $18 per share. What is his annual rate of return? Interpolate to find the answer.

9-33. Solution:

Appendix B

Return is between 14%-15% for 3 years

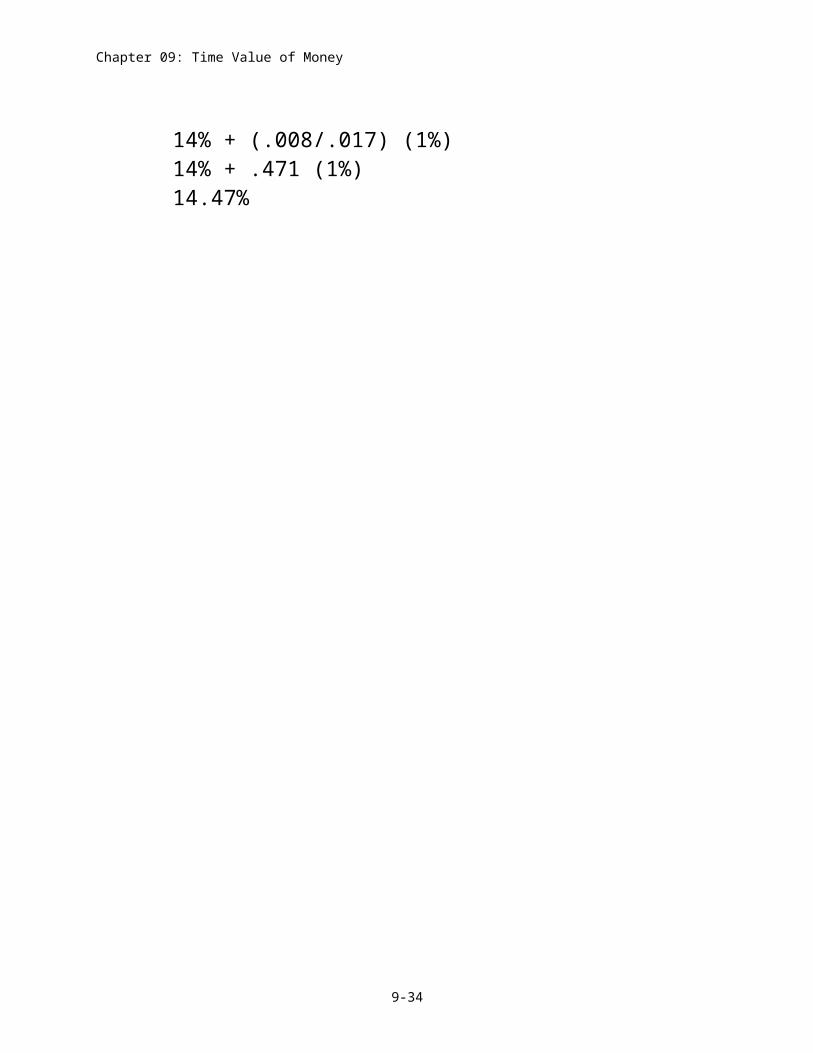

14% + (.008/.017) (1%)14% + .471 (1%)14.47%

9-18

Chapter 09: Time Value of Money

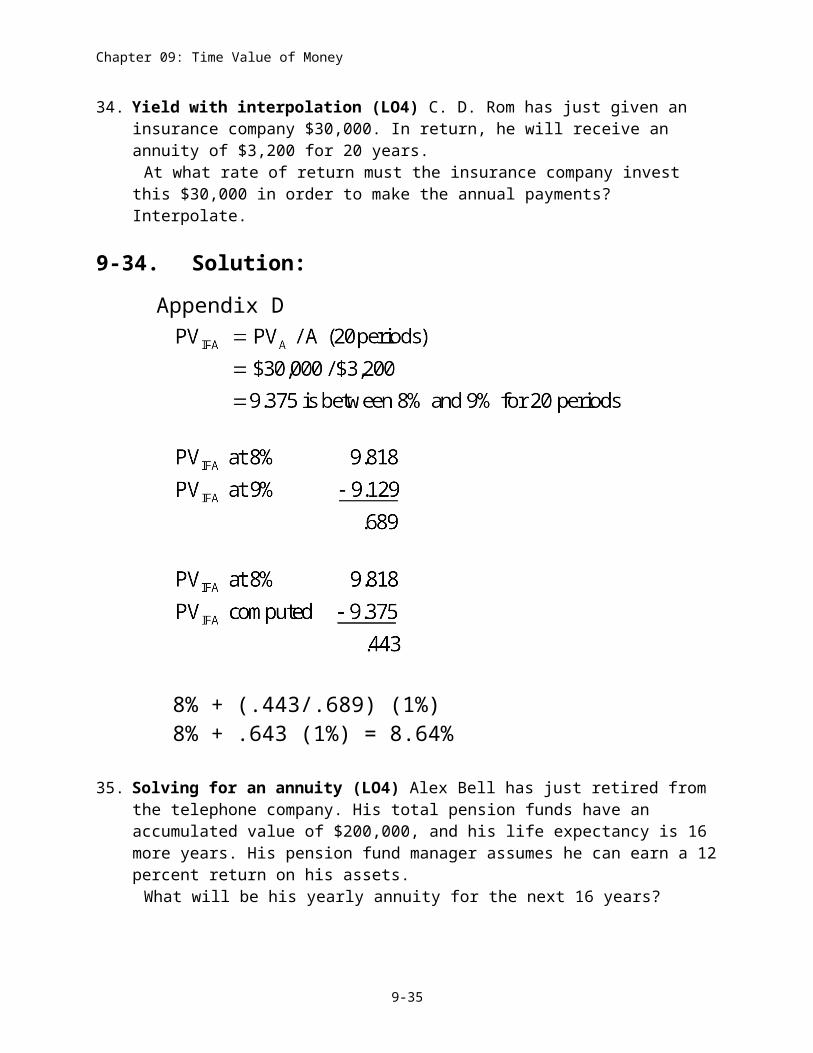

34. Yield with interpolation (LO4) C. D. Rom has just given an insurance company $30,000. In return, he will receive an annuity of $3,200 for 20 years.

At what rate of return must the insurance company invest this $30,000 in order to make the annual payments? Interpolate.

9-34. Solution:

Appendix D

8% + (.443/.689) (1%)8% + .643 (1%) = 8.64%

35. Solving for an annuity (LO4) Alex Bell has just retired from the telephone company. His total pension funds have an accumulated value of $200,000, and his life expectancy is 16 more years. His pension fund manager assumes he can earn a 12 percent return on his assets.

What will be his yearly annuity for the next 16 years?

9-35. Solution:

Appendix D

9-19

Chapter 09: Time Value of Money

36. Solving for an annuity (LO4) Dr. Oats, a nutrition professor, invests $80,000 in a piece of land that is expected to increase in value by 14 percent per year for the next five years. She will then take the proceeds and provide herself with a 10-year annuity. Assuming a 14 percent interest rate for the annuity, how much will this annuity be?

9-36. Solution:

Appendix AFV = PV × FVIF (14%, 5 periods)FV = $80,000 × 1.925 = $154,000

Appendix DA = PVA/PVIFA (14%, 10 periods)A = $154,000/5.216 = $29,524.54

37. Solving for an annuity (LO4) You wish to retire in 20 years, at which time you want to have accumulated enough money to receive an annual annuity of $12,000 for 25 years after retirement. During the period before retirement you can earn 8 percent annually, while after retirement you can earn 10 percent on your money.

What annual contributions to the retirement fund will allow you to receive the $12,000 annuity?

9-37. Solution:

Determine the present value of an annuity during retirement: Appendix D

To determine the annual deposit into an account earning 8% that is necessary to accumulate $108,924 after 20 years, use the Future Value of an Annuity table: Appendix C

9-20

Chapter 09: Time Value of Money

38. Deferred annuity (LO3) Rusty Steele will receive the following payments at the end of the next three years: $4,000, $7,000, and $9,000. Then from the end of the fourth year through the end of the tenth year, he will receive an annuity of $10,000. At a discount rate of 10 percent, what is the present value of all future benefits?

9-38. Solution:

First find the present value of the first three payments.

PV = FV × PVIF (Appendix B) i = 10%

1) $4,000 × .909 = $3,6362) 7,000 × .826 = 5,7823) 9,000 × .751 = 6,759

$16,177

Then find the present value of the deferred annuity.

Appendix D will give a factor for a seven period annuity (fourth year through the tenth year) at a discount rate of 10 percent. The value of the annuity at the beginning of the fourth year is:

This value at the beginning of year four (end of year three) must now be discounted back for three years to get the present value of the deferred annuity. Use Appendix B.

9-21

Chapter 09: Time Value of Money

Finally, find the total present value of all future payments.

Present value of first three payments $16,177Present value of the deferred annuity 36,559

$52,7369-38. (Continued)

OR

Take the PVIFA for 10 years at 10% and subtract the PVIFA for 3 years at 10% to end up with the 7 year deferred annuity.

PVIFA = 6.145 (10 years at 10%)

PVIFA = 2.487 ( 3 years at 10%)PVIFA = 3.658 (years 4 through 10 years at 10%)

$10,000 × 3.658 = $36,580

Present value of first three payments $16,177 Present value of the deferred annuity 36,580

$52,757

39. Present value (LO3) Kelly Greene has a contract in which she will receive the following payments for the next five years: $3,000, $4,000, $5,000, $6,000, and $7,000. She will then receive an annuity of $9,000 a year from the end of the sixth through the end of the 15th year. The appropriate discount rate is 13 percent. If she is offered $40,000 to cancel the contract, should she do it?

9-39. Solution:

First find the present value of the first five payments.

PV = FV × PVIF (Appendix B) i = 13%

9-22

Chapter 09: Time Value of Money

1) $3,000 × .885 = $ 2,6552) 4,000 × .783 = 3,1323) 5,000 × .693 = 3,4654) 6,000 × .613 = 3,6785) 7,000 × .543 = 3,801

$16,731

Then find the present value of the deferred annuity.

Appendix D will give a factor for a ten period annuity (sixth year through the fifteenth year) at a discount rate of 13 percent. The value of the annuity at the beginning of the sixth year is:

This value at the beginning of year six (end of year five) must now be discounted back for five years to get the present value of the deferred annuity. Use Appendix B.

9-39. (Continued)

Next, find the total present value of all future payments.

Present value of first three payments $16,731Present value of the deferred annuity 26,517

$43,248Since the present value of all future benefits under the contract is greater than $40,000, Kelly Greene should not accept this amount to cancel the contract.

9-23

Chapter 09: Time Value of Money

40. Deferred annuity (LO3) Kay Mart has purchased an annuity to begin payment at the end of 2113 (the date of the first payment). Assume it is now the beginning of 2011. The annuity is for $12,000 per year and is designed to last eight years. If the discount rate for the calculation is 11 percent, what is the most she should have paid for the annuity?

9-40. Solution:

Appendix D will give a factor for an 8 year annuity when the appropriate discount rate is 11 percent (5.146). The value of the annuity at the beginning of the year it starts (2113) is:

The present value at the beginning of 2011 is found using Appendix B (2 years at 11%). The factor is .812. Note we are discounting from the beginning of 2113 to the beginning of 2011.

The maximum that should be paid for the annuity is $50,142.62.

41. Yield (LO4) If you borrow $9,725 and are required to pay back the loan in five equal annual installments of $2,500, what is the interest rate associated with the loan?

9-41. Solution:

Appendix D

9-24

Chapter 09: Time Value of Money

Interest rate = 9 percent

Go across period 5 until you find 3.890. Go up to the percentage at the top of the column and find 9 percent.

42. Loan repayment (LO4) Tom Busby owes $20,000 now. A lender will carry the debt for four more years at 8 percent interest. That is, in this particular case, the amount owed will go up by 8 percent per year for four years. The lender then will require Busby to pay off the loan over 12 years at 11 percent interest. What will his annual payment be?

9-42. Solution:

Appendix A

Appendix D

43. Loan repayment (LO4) If your aunt borrows $50,000 from the bank at 10 percent interest over the eight-year life of the loan, what equal annual payments must be made to discharge the loan, plus pay the bank its required rate of interest (round to the nearest dollar)? How much of his first payment will be applied to interest? To principal? How much of her second payment will be applied to each?

9-43. Solution:

9-25

Chapter 09: Time Value of Money

Appendix D

First payment:$50,000 × .10 = $5,000 first year interest$9,372.07 – $5,000 = $4,372.07 applied to principal

Second payment: First determine remaining principal$50,000 – $4,372.07 = $45,627.93$45,627.93 × .10 = $4,562.79 second year interest$9,372.07 – $4,562.79 = $4,809.28 applied to principal

44. Loan repayment (LO4) Jim Thorpe borrows $70,000 toward the purchase of a home at 12 percent interest. His mortgage is for 30 years.a. How much will his annual payments be? (Although home payments are usually on a

monthly basis, we shall do our analysis on an annual basis for ease of computation. We will get a reasonably accurate answer.)

b. How much interest will he pay over the life of the loan?c. How much should he be willing to pay to get out of a 12 percent mortgage and into a

10 percent mortgage with 30 years remaining on the mortgage? Suggestion: Find the annual savings and then discount them back to the present at the current interest rate (10 percent).

9-44. Solution:

Appendix D

9-26

Chapter 09: Time Value of Money

Appendix Dc. New payments at 10%

9-44. (Continued)

Difference between old and new payments

P.V. of difference – Appendix D

9-27

Chapter 09: Time Value of Money

45. Annuity with changing interest rates (LO4) You are chairperson of the investment fund for the Continental Soccer League. You are asked to set up a fund of semiannual payments to be compounded semiannually to accumulate a sum of $200,000 after 10 years at an 8 percent annual rate (20 payments). The first payment into the fund is to take place six months from today, and the last payment is to take place at the end of the 10th year.a. Determine how much the semiannual payment should be. (Round to whole numbers.)

On the day after the sixth payment is made (the beginning of the fourth year) the interest rate goes up to a 10 percent annual rate, and you can earn a 10 percent annual rate on funds that have been accumulated as well as all future payments into the fund. Interest is to be compounded semiannually on all funds.b. Determine how much the revised semiannual payments should be after this rate

change (there are 14 payments and compounding dates). The next payment will be in the middle of the fourth year. (Round all values to whole numbers.)

9-45. Solution:

Appendix C

b. First determine how much the old payments are equal to after 6 periods at 4%. Appendix C.

Then determine how much this value will grow to after 14 periods at 5% (semi-annual rate).

Appendix A

9-28

Chapter 09: Time Value of Money

9-45. (Continued)

Subtract this value from $200,000 to determine how much you need to accumulate on the next 14 payments.

Determine the revised semi-annual payment necessary to accumulate this sum after 14 periods at 5%.

Appendix CA = FVA/FVIFA A = $111,797/19.599A = $5,704

46. Annuity consideration (LO4) Your younger sister, Brittany, will start college in five years. She has just informed your parents that she wants to go to Eastern State U., which will cost $30,000 per year for four years (cost assumed to come at the end of each year). Anticipating Brittany’s ambitions, your parents started investing $5,000 per year five years ago and will continue to do so for five more years.

How much more will your parents have to invest each year for the next five years to have the necessary funds for Brittany’s education? Use 10 percent as the appropriate interest rate throughout this problem (for discounting or compounding). Round all values to whole numbers.

9-46. Solution:

Present value of college costsAppendix D

9-29

Chapter 09: Time Value of Money

Accumulation based on investing $5,000 per year for 10 years.

Appendix C

Additional funds required 5 years from now when Brittany starts college.

$95,100 PV of college costs 79,685 Accumulation based on $5,000 per year $15,415 Additional funds required in five years

Additional annual contribution required between now and the time Brittany starts college in 5 years.

9-46. (Continued)

Appendix C

9-30

Chapter 09: Time Value of Money

47. Special consideration of annuities and time periods (LO4) Brittany (from problem 46) is now 18 years old (five years have passed), and she wants to get married instead of going to college. Your parents have accumulated the necessary funds for her education.

Instead of her schooling, your parents are paying $10,000 for her current wedding and plan to take year-end vacations costing $3,000 per year for the next three years.

How much money will your parents have at the end of three years to help you with graduate school, which you will start then? You plan to work on a master’s and perhaps a PhD. If graduate school costs $32,600 per year, approximately how long will you be able to stay in school based on these funds? Use 10 percent as the appropriate interest rate throughout this problem. (Round all values to whole numbers.

9-47. Solution:

Funds available after the wedding

$95,100 Funding available before the wedding– 10,000 Wedding85,100 Funds available after the wedding

Less present value of vacation

Appendix D

$85,100– 7,461 $77,639 Remaining funds for graduate school

Available funds after 3 years.

9-31

Chapter 09: Time Value of Money

9-47. (Continued)

Appendix A

Number of years of graduate education

Appendix D

with i = 10%, n = 4 for 3.170, the answer is 4 years.

COMPREHENSIVE PROBLEM

Modern Weapons, Inc. (Comprehensive time value of money) Mr. Rambo, President of Modern Weapons, Inc., was pleased to hear that he had three offers from major defense companies for his latest missile firing automatic ejector. He will use a discount rate of 12 percent to evaluate each offer.

9-32

Chapter 09: Time Value of Money

Offer I $500,000 now plus $120,000 from the end of years 6 through 15. Also if the product goes over $50 million in cumulative sales by the end of year 15, he will receive an additional $1,500,000. Rambo thought there was a 75 percent probability this would happen.

Offer II Twenty-five percent of the buyer’s gross margin for the next four years. The buyer in this case is Air Defense, Inc. (ADI). Its gross margin is 65 percent. Sales for year 1 are projected to be $1 million and then grow by 40 percent per year. This amount is paid today and is not discounted.

Offer III A trust fund would be set up for the next nine years. At the end of that period, Rambo would receive the proceeds (and discount them back to the present at 12 percent). The trust fund called for semiannual payments for the next nine years of $80,000 (a total of $160,000 per year). The payments would start immediately. Since the payments are coming at the beginning of each period instead of the end, this is an annuity due. To look up the future value of the annuity due in the tables, add 1 to n (18 + 1) and subtract 1 from the value in the table. Assume the annual interest rate on this annuity is 12 percent annually (6 percent semiannually). Determine the present value of the trust fund’s final value.Required: Find the present value of each of the three offers and then indicate which one has the highest present value.

CP 9-1. Solution:Modern Weapons, Inc.

Offer I$500,000 now plus:$120,000 from year six through fifteen (deferred annuity)$1,500,000 75% potential bonus if sales pass $50 million

Appendix D

Appendix B

9-33

Chapter 09: Time Value of Money

Probability of bonus = 75%.75 × $1,500,000 = $1,125,000

Appendix B

Total value of Offer I

$500,000 Payment today 384,426 Present value of deferred annuity 205,875 Present value of $1.5 million bonus$1,090,301

CP 9-1. (Continued)Offer II

Sales Gross Profit Payment 25% Year (40% Growth) (65% of Sales) of Gross Profit

1 $1,000,000 $ 650,000 $162,5002 1,400,000 910,000 227,5003 1,960,000 1,274,000 318,5004 2,744,000 1,783,600 445,900

$1,154,400

Offer IIIFuture value of an annuity due (Appendix C)9 years – semiannually

9-34

Chapter 09: Time Value of Money

N = 18 + 1 = 19I = 12%/2 = 6%FVIFA = 33.760 – 1 = 32.760 (using Appendix C)

Present value of trust fund (Appendix B)

CP 9-1. (Continued)Summary

Value of Offer I $1,090,301Value of Offer II $1,154,250Value of Offer III $ 946,109

Select Offer II.

9-35

Related Documents