BRASOV Real-Estate Overview CBRE RESEARCH Photo source: georgestoica93.blogspot.ro

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BRASOVReal-Estate Overview

CBRE RESEARCH

Photo source: georgestoica93.blogspot.ro

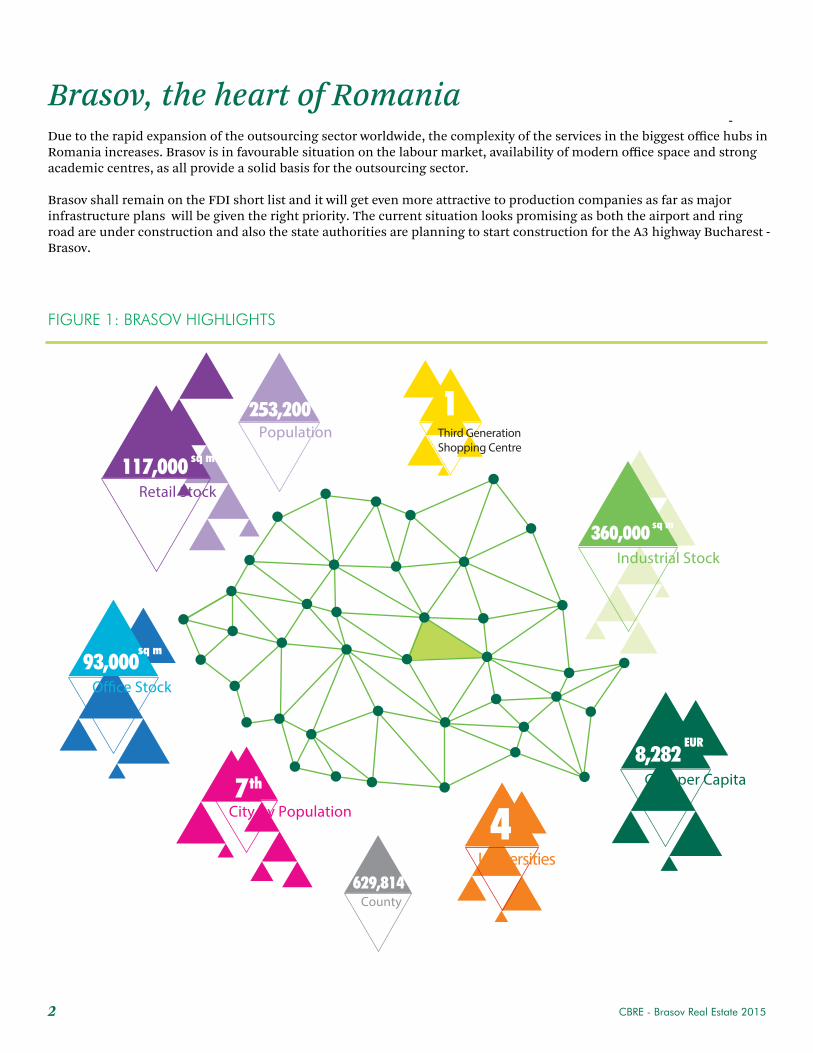

Due to the rapid expansion of the outsourcing sector worldwide, the complexity of the services in the biggest office hubs in Romania increases. Brasov is in favourable situation on the labour market, availability of modern office space and strong academic centres, as all provide a solid basis for the outsourcing sector.

Brasov shall remain on the FDI short list and it will get even more attractive to production companies as far as major infrastructure plans will be given the right priority. The current situation looks promising as both the airport and ring road are under construction and also the state authorities are planning to start construction for the A3 highway Bucharest - Brasov.

CBRE - Brasov Real Estate 2015

-

FIGURE 1: BRASOV HIGHLIGHTS

2

Brasov, the heart of Romania

253,200

Universities4

Third GenerationShopping Centre

1

7th

O�ce Stock

City by Population

93,000sq m

GDP per Capita8,282

EUR

Retail Stock

Population

629,814County

117,000 sq m

Industrial Stock360,000 sq m

OFFICE STOCK

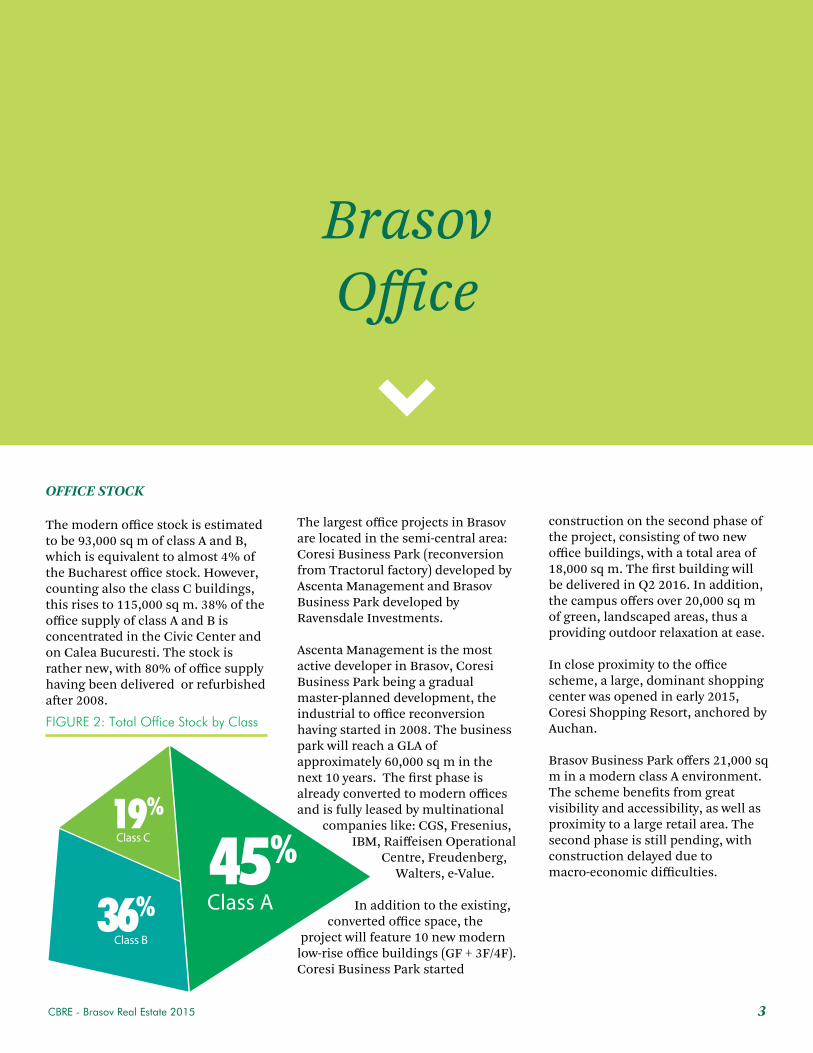

The modern office stock is estimated to be 93,000 sq m of class A and B, which is equivalent to almost 4% of the Bucharest office stock. However, counting also the class C buildings, this rises to 115,000 sq m. 38% of the office supply of class A and B is concentrated in the Civic Center and on Calea Bucuresti. The stock is rather new, with 80% of office supply having been delivered or refurbished a�er 2008.

BrasovOffice

3

The largest office projects in Brasov are located in the semi-central area: Coresi Business Park (reconversion from Tractorul factory) developed by Ascenta Management and Brasov Business Park developed by Ravensdale Investments.

Ascenta Management is the most active developer in Brasov, Coresi Business Park being a gradual master-planned development, the industrial to office reconversion having started in 2008. The business park will reach a GLA of approximately 60,000 sq m in the next 10 years. The first phase is already converted to modern offices and is fully leased by multinational

companies like: CGS, Fresenius, IBM, Raiffeisen Operational

Centre, Freudenberg, Walters, e-Value.

In addition to the existing, converted office space, the

project will feature 10 new modern low-rise office buildings (GF + 3F/4F). Coresi Business Park started

construction on the second phase of the project, consisting of two new office buildings, with a total area of 18,000 sq m. The first building will be delivered in Q2 2016. In addition, the campus offers over 20,000 sq m of green, landscaped areas, thus a providing outdoor relaxation at ease.

In close proximity to the office scheme, a large, dominant shopping center was opened in early 2015, Coresi Shopping Resort, anchored by Auchan.

Brasov Business Park offers 21,000 sq m in a modern class A environment. The scheme benefits from great visibility and accessibility, as well as proximity to a large retail area. The second phase is still pending, with construction delayed due to macro-economic difficulties.

FIGURE 2: Total Office Stock by Class

45%

36% Class A

Class B

Class C19%

CBRE - Brasov Real Estate 2015

On the short and medium term, the proportion between demand and supply for office space is balanced. On the long-term however and with reaching a critical mass of highly skilled human resources and a quality business environment, we expect the demand for class A office space to substantially increase.

Silviu Savin - PartnerAscenta Management

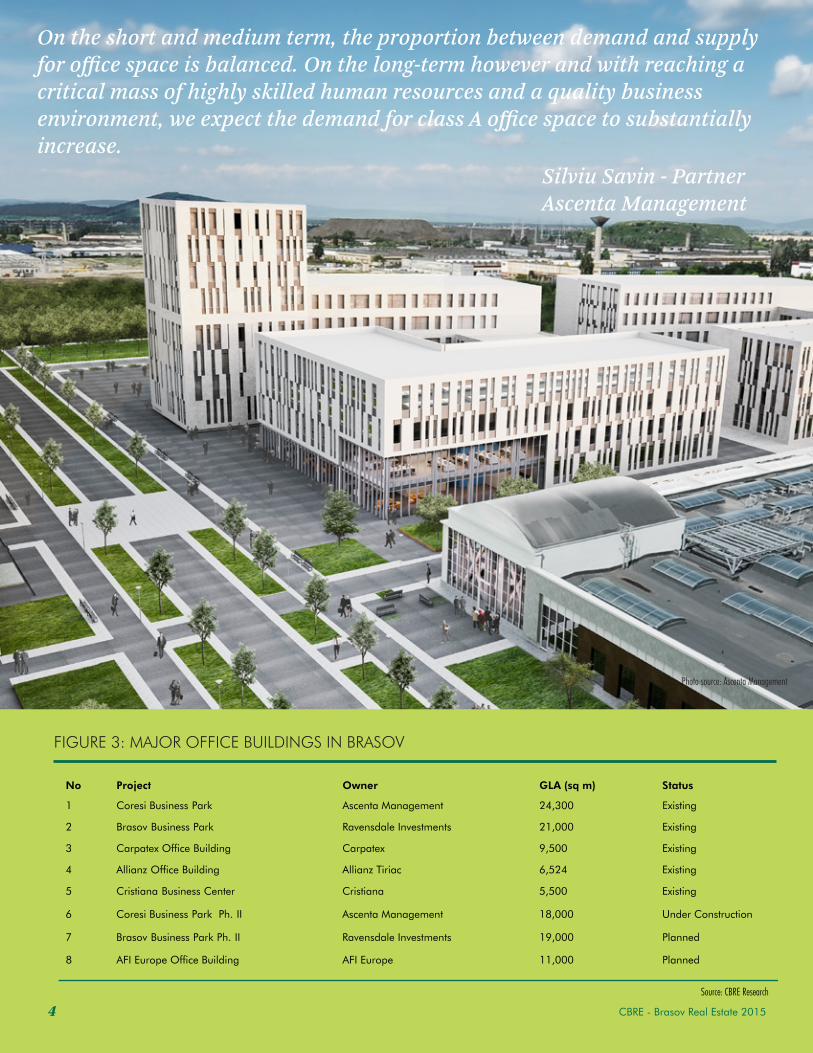

No Project Owner GLA (sq m) Status

1 Coresi Business Park Ascenta Management 24,300 Existing

2 Brasov Business Park Ravensdale Investments 21,000 Existing

3 Carpatex Office Building Carpatex 9,500 Existing

4 Allianz Office Building Allianz Tiriac 6,524 Existing

5 Cristiana Business Center Cristiana 5,500 Existing

6 Coresi Business Park Ph. II Ascenta Management 18,000 Under Construction

7 Brasov Business Park Ph. II Ravensdale Investments 19,000 Planned

8 AFI Europe Office Building AFI Europe 11,000 Planned

FIGURE 3: MAJOR OFFICE BUILDINGS IN BRASOV

Source: CBRE Research

CBRE - Brasov Real Estate 20154

Photo source: Ascenta Management

5

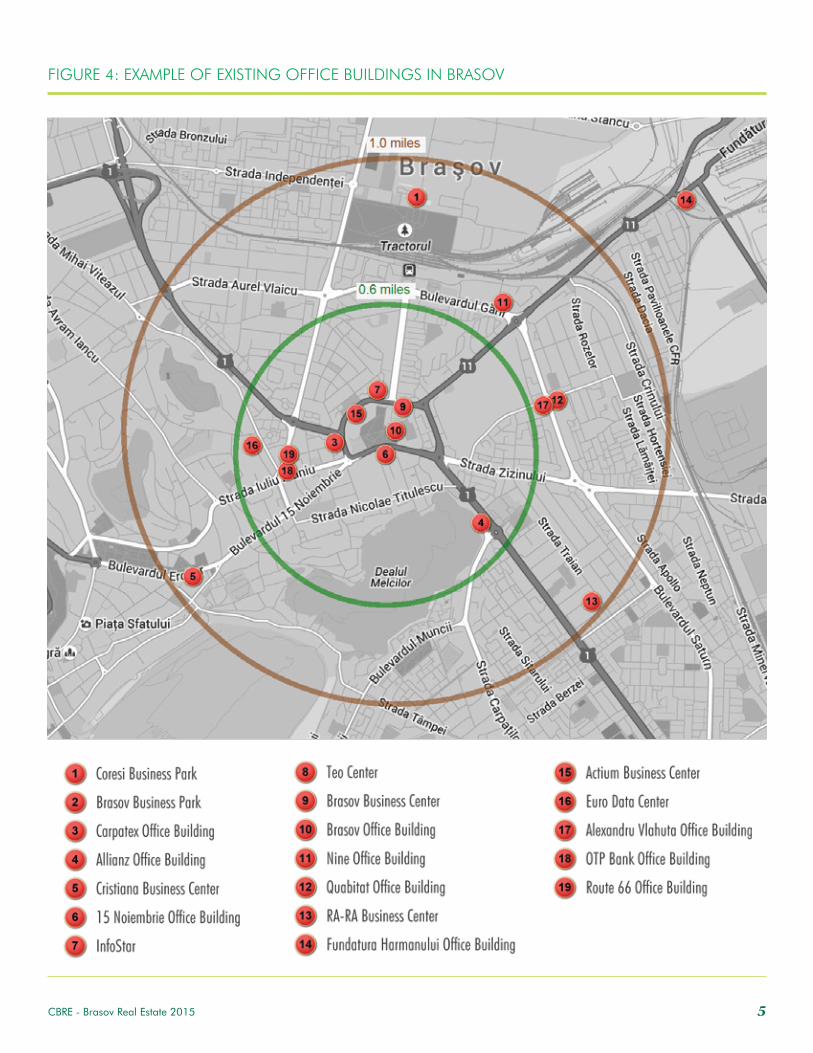

FIGURE 4: EXAMPLE OF EXISTING OFFICE BUILDINGS IN BRASOV

CBRE - Brasov Real Estate 2015

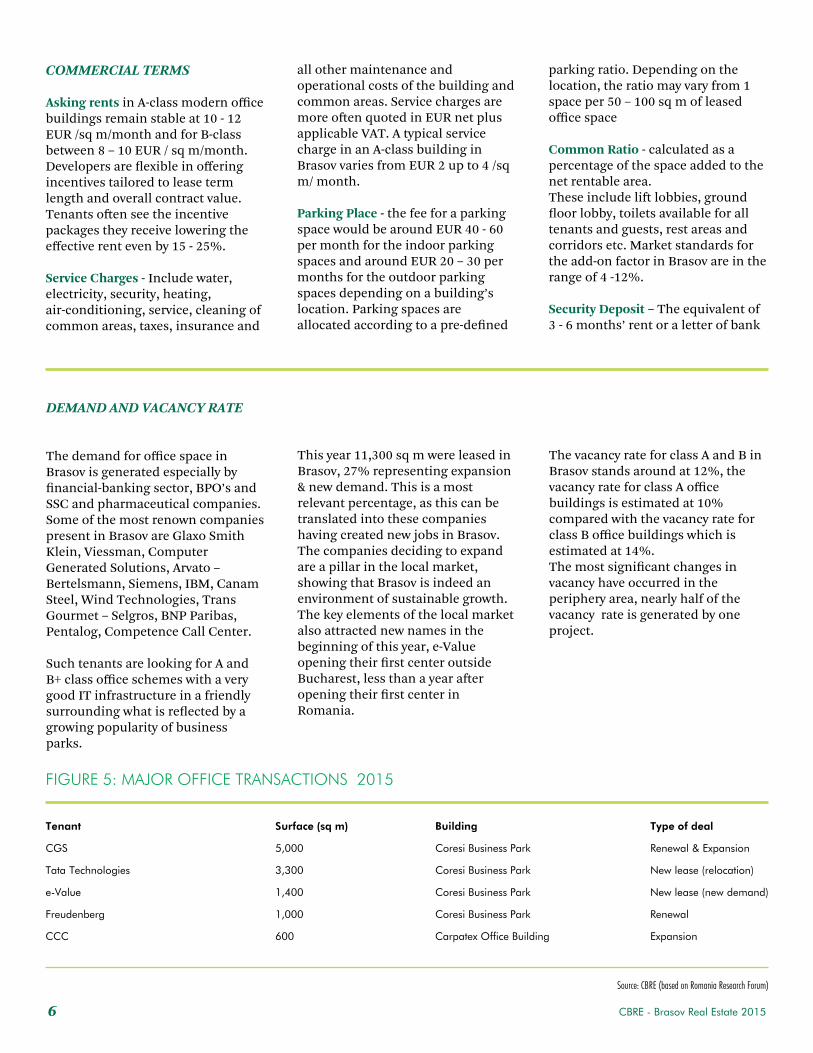

COMMERCIAL TERMS

Asking rents in A-class modern office buildings remain stable at 10 - 12 EUR /sq m/month and for B-class between 8 – 10 EUR / sq m/month. Developers are flexible in offering incentives tailored to lease term length and overall contract value. Tenants o�en see the incentive packages they receive lowering the effective rent even by 15 - 25%.

Service Charges - Include water, electricity, security, heating, air-conditioning, service, cleaning of common areas, taxes, insurance and

all other maintenance and operational costs of the building and common areas. Service charges are more o�en quoted in EUR net plus applicable VAT. A typical service charge in an A-class building in Brasov varies from EUR 2 up to 4 /sq m/ month.

Parking Place - the fee for a parking space would be around EUR 40 - 60 per month for the indoor parking spaces and around EUR 20 – 30 per months for the outdoor parking spaces depending on a building’s location. Parking spaces are allocated according to a pre-defined

parking ratio. Depending on the location, the ratio may vary from 1 space per 50 – 100 sq m of leased office space

Common Ratio - calculated as a percentage of the space added to the net rentable area.These include li� lobbies, ground floor lobby, toilets available for all tenants and guests, rest areas and corridors etc. Market standards for the add-on factor in Brasov are in the range of 4 -12%.

Security Deposit – The equivalent of 3 - 6 months’ rent or a letter of bank

DEMAND AND VACANCY RATE

The demand for office space in Brasov is generated especially by financial-banking sector, BPO’s and SSC and pharmaceutical companies. Some of the most renown companies present in Brasov are Glaxo Smith Klein, Viessman, Computer Generated Solutions, Arvato – Bertelsmann, Siemens, IBM, Canam Steel, Wind Technologies, Trans Gourmet – Selgros, BNP Paribas, Pentalog, Competence Call Center.

Such tenants are looking for A and B+ class office schemes with a very good IT infrastructure in a friendly surrounding what is reflected by a growing popularity of business parks.

This year 11,300 sq m were leased in Brasov, 27% representing expansion & new demand. This is a most relevant percentage, as this can be translated into these companies having created new jobs in Brasov. The companies deciding to expand are a pillar in the local market, showing that Brasov is indeed an environment of sustainable growth. The key elements of the local market also attracted new names in the beginning of this year, e-Value opening their first center outside Bucharest, less than a year a�er opening their first center in Romania.

The vacancy rate for class A and B in Brasov stands around at 12%, the vacancy rate for class A office buildings is estimated at 10% compared with the vacancy rate for class B office buildings which is estimated at 14%. The most significant changes in vacancy have occurred in the periphery area, nearly half of the vacancy rate is generated by one project.

CBRE - Brasov Real Estate 20156

Coresi Business Park

Coresi Business Park

Coresi Business Park

Coresi Business Park

Tenant Surface (sq m) Building Type of deal

CGS 5,000 Renewal & Expansion

Tata Technologies 3,300 New lease (relocation)

e-Value 1,400 New lease (new demand)

Freudenberg 1,000 Renewal

CCC 600 Carpatex Office Building Expansion

FIGURE 5: MAJOR OFFICE TRANSACTIONS 2015

Source: CBRE (based on Romania Research Forum)

7CBRE - Brasov Real Estate 2015

METHODOLOGY & DEFINITIONS

Prime Rent - represents the top open-market tier of rent that could be expected for a unit of standard size (commensurate with demand in each location), of the highest quality and specification and in the best location in a market at the survey date. The Prime Rent should reflect the level at which relevant transac-tions are being completed in the market at the time, but need not be exactly identical to any of them, particularly if deal flow is very limited or made up of unusual one-off deals. If there are no relevant transactions during the survey period, the quoted figure will be more hypothetical, based on an expert opinion of market conditions.

Vacancy Rate - represents the percentage ratio of total vacant space to stock.

Total Stock – represents the total completed space (occupied and vacant) in the private and public sector at the survey date. Includes owner occupied space.

Business Process Outsourcing (BPO) – a specialized organization that provides specific business functions (or processes), usually non-produc-tion ones to third parties.

Shared Service Centre (SSC) – a separated part of an enterprise that provides a service to an organization or group where that service had previously been found in more than

one part of the organization or group. The funding and resourcing of the service is shared and the providing department effectively becomes an internal service provider.

Knowledge Process Outsourcing (KPO) – a form of outsourcing, in which knowledge-related and information-related work is carried out by workers in a different compa-ny or by a subsidiary of the same organization, which may be in the same country or in an offshore location to save cost. This typically involves high-value work carried out by highly skilled staff.

Cities like Brasov have long been a magnet for diverse, skilled, valuable talent, and recent economic evolutions have made the city retain and attract both entry, and mid-level and top-level professionals. With a solid education, varied opportunities and international exposure, these talents have grown into a workforce pool that can drive business growth for companies investing in the region.

Emil Minciu, Operations & Sales DirectorManpower Romania

When compared with other cities, Brasov has the substantial advantage of the high number of foreign language speakers, available for employment, especially those fluent in German. More educational centres for learning foreign languages would increase the attractiveness of the city.

Source: Manpower

LABOUR MARKET

Brasov has emerged as a favourable office location for Shared Service Centers, BPO & KPO, business services and IT&C support centers. Brasov is a destination as an alterna-tive location to Bucharest or as an additional location for companies that already have set up operations in the capital.

The increase in the number of people employed in the service centres also means expanding the pool of candidates who understand the nature of work in the sector and have experience in servicing custom-ers from abroad. The average length of service in the sector is about three years and is still growing.

At present, we can clearly distinguish a group of employees who see their future career in the business services sector. Many of these individuals continue to develop their skills, including learning additional foreign languages.’

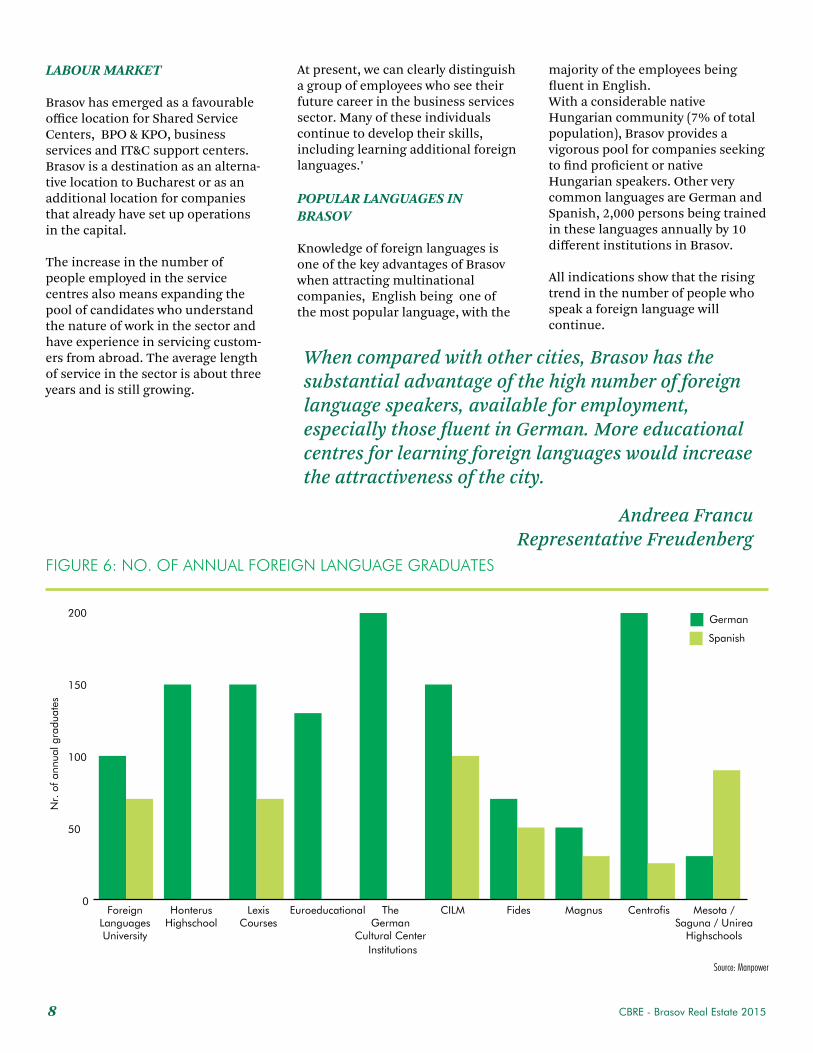

POPULAR LANGUAGES IN BRASOV

Knowledge of foreign languages is one of the key advantages of Brasov when attracting multinational companies, English being one of the most popular language, with the

majority of the employees being fluent in English.With a considerable native Hungarian community (7% of total population), Brasov provides a vigorous pool for companies seeking to find proficient or native Hungarian speakers. Other very common languages are German and Spanish, 2,000 persons being trained in these languages annually by 10 different institutions in Brasov.

All indications show that the rising trend in the number of people who speak a foreign language will continue.

0

50

100

150

200

ForeignLanguagesUniversity

HonterusHighschool

LexisCourses

Euroeducational TheGerman

Cultural Center

CILM Fides Magnus Centrofis Mesota /Saguna / Unirea

Highschools

Nr.

of a

nnua

l gra

duat

es

Institutions

German

Spanish

FIGURE 6: NO. OF ANNUAL FOREIGN LANGUAGE GRADUATES

Andreea Francu Representative Freudenberg

CBRE - Brasov Real Estate 20158

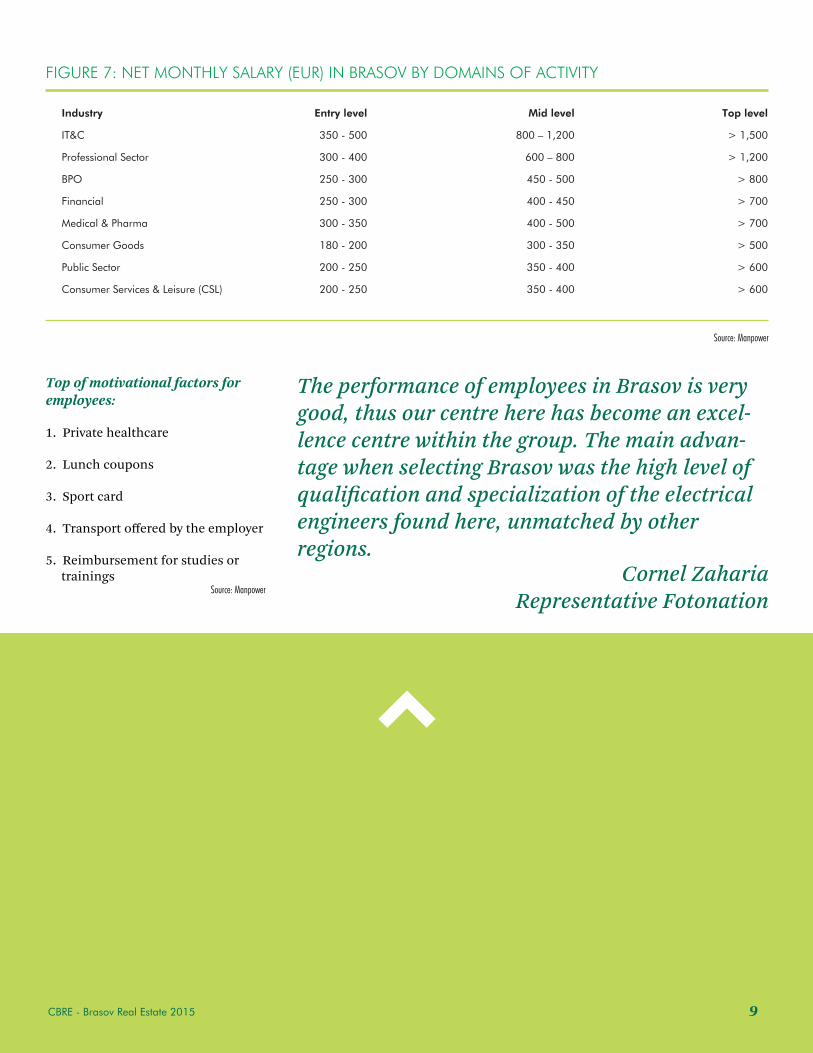

FIGURE 7: NET MONTHLY SALARY (EUR) IN BRASOV BY DOMAINS OF ACTIVITY

Industry

IT&C

Professional Sector

BPO

Financial

Medical & Pharma

Consumer Goods

Public Sector

Consumer Services & Leisure (CSL)

Entry level

350 - 500

300 - 400

250 - 300

250 - 300

300 - 350

180 - 200

200 - 250

200 - 250

Mid level

800 – 1,200

600 – 800

450 - 500

400 - 450

400 - 500

300 - 350

350 - 400

350 - 400

Top level

> 1,500

> 1,200

> 800

> 700

> 700

> 500

> 600

> 600

Source: Manpower

Top of motivational factors for employees:

1. Private healthcare

2. Lunch coupons

3. Sport card

4. Transport offered by the employer

5. Reimbursement for studies or trainings

Source: Manpower

The performance of employees in Brasov is very good, thus our centre here has become an excel-lence centre within the group. The main advan-tage when selecting Brasov was the high level of qualification and specialization of the electrical engineers found here, unmatched by other regions.

9CBRE - Brasov Real Estate 2015

Cornel ZahariaRepresentative Fotonation

INDUSTRIAL STOCK

The modern industrial stock is estimated to be around 360,000 sq m of class A and B, which is equivalent to almost 35% of the Bucharest industrial stock. Brownfield schemes, class C&D buildings adds to the overall stock another 450,000 sq m.

BrasovIndustrial

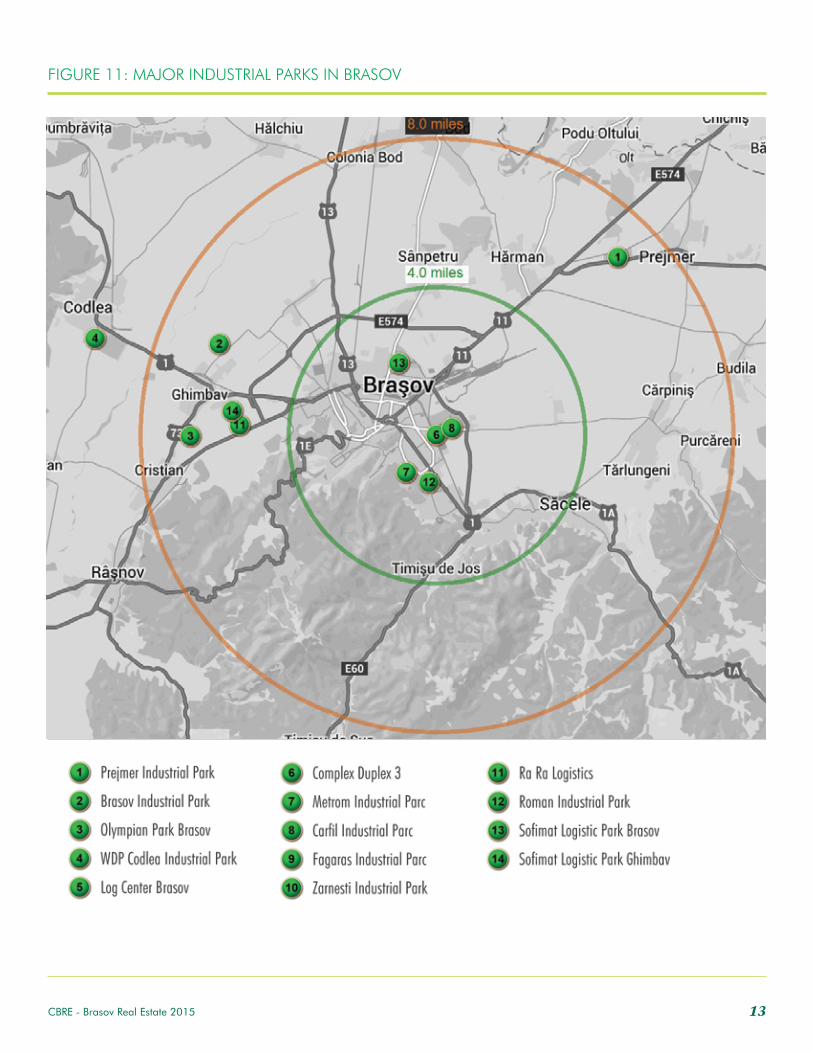

The new supply of industrial space is concentrated now mainly in the West part of Brasov, greenfields developments like: Brasov Industrial Park, Olympian Park Brasov, WDP Codlea Industrial Park are located near Ghimbav and Codlea the other major industrial park: Prejmer Industrial Park is situated in the North East part.

The remaining former industrial platforms are located in the South, South East part of Brasov city, while other brownfield spaces are spread along the county. Part of the projects have been demolished creating new

urban spaces and those remaining have been

refurbished to accommodate different industrial activities.

A great deal of companies which previously been in

brownfieldd buildings or even tenants in greenfield developments had took in some point in time the decision to develop their own buildings due to favourable real

estate conditions.

The majority of new industrial developments has purely production purposes and only to a small degree distribution and logistics matters. 'Built to suit' facilities have been common in the past few years in terms of development trends only a few speculative projects were registered. The trend might continue for a period of time and contribute to maintaing a lower based vacancy rate which now actually stands at 3.8%, even lower for class A buildings 2.9%.

The construction of the Comarnic – Brasov highway, the airport and the ring road should boost the demand for industrial warehouse and logistics facilities and even for production plants.

Purchasers interested in buying plots of land for industrial purposes could find offers that already have all the permits included and utilities on site for a price that can range between 20 and 30 Eur/sq m.

FIGURE 8: Total Industrial Stock by Class

35%55%Class A

Class C&D

Class B10%

CBRE - Brasov Real Estate 201510

We chose to develop our industrial park in central Romania due to the continuous increasing demand for warehousing solutions of the global tenants present here. Major attraction deciding points are the soon to be developed airport and road infrastructure connecting the area to the most important European transportation routes.

No Industrial Park Developer/Owner GLA (sq m) Status

1 Prejmer Industrial Park

Brasov Industrial Park

Olympian Park Brasov

WDP Codlea Industrial Park

Log Center Brasov

Sofimat Logistic Park Brasov

Graells&Llonch and Local Authorities

ICCO

Helios Phoenix

WDP

Immofinanz Group

Sofimat

181,000

72,000

18,000

6,000

0

35,000

Existing

Existing

Existing

Existing

Planned

Existing

Main Tenants

Eldon, Indcar, DHL

Preh, Continental Powertrain

Terwa, Draxlmaier, HIB Solutions

Inter Cars

N/A

Coca Cola

2

3

4

5

6

FIGURE 9: MAJOR INDUSTRIAL PARKS IN BRASOV

Source: CBRE Research

Mr. Jeroen Biermans - Managing DirectorWDP Romania

11CBRE - Brasov Real Estate 2015

Photo source: WDP Romania

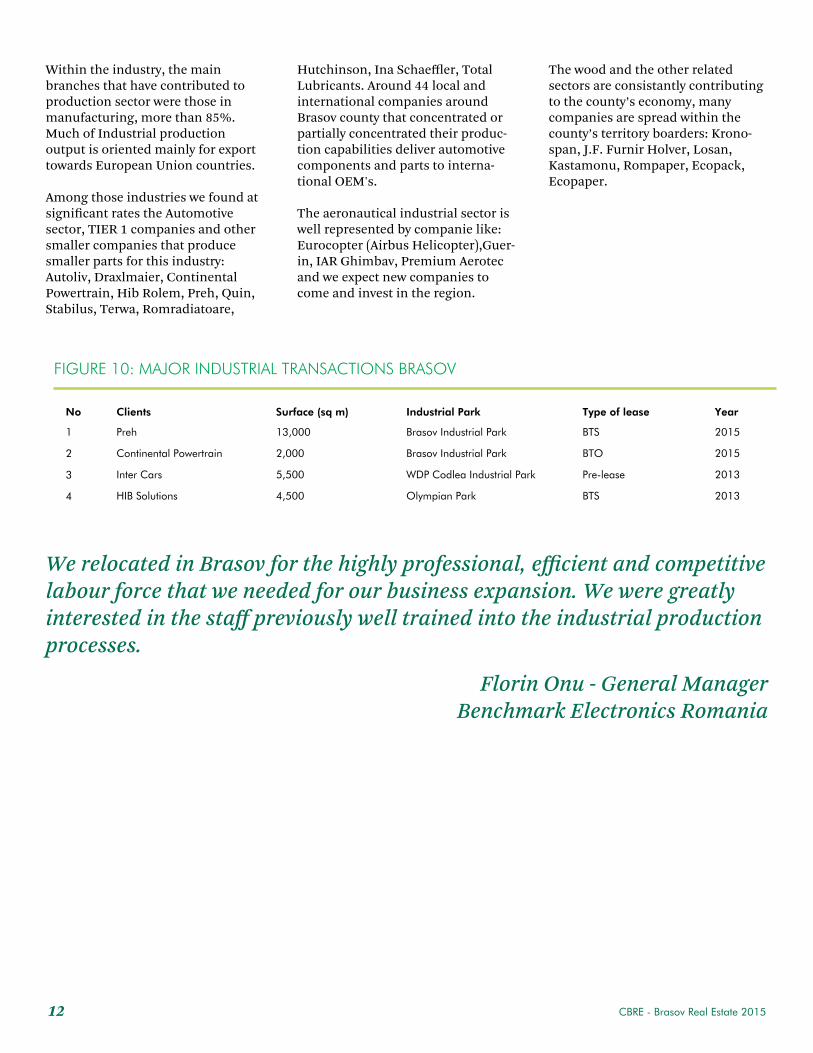

Within the industry, the main branches that have contributed to production sector were those in manufacturing, more than 85%. Much of Industrial production output is oriented mainly for export towards European Union countries.

Among those industries we found at significant rates the Automotive sector, TIER 1 companies and other smaller companies that produce smaller parts for this industry: Autoliv, Draxlmaier, Continental Powertrain, Hib Rolem, Preh, Quin, Stabilus, Terwa, Romradiatoare,

Hutchinson, Ina Schaeffler, Total Lubricants. Around 44 local and international companies around Brasov county that concentrated or partially concentrated their produc-tion capabilities deliver automotive components and parts to interna-tional OEM's.

The aeronautical industrial sector is well represented by companie like: Eurocopter (Airbus Helicopter),Guer-in, IAR Ghimbav, Premium Aerotec and we expect new companies to come and invest in the region.

The wood and the other related sectors are consistantly contributing to the county’s economy, many companies are spread within the county’s territory boarders: Krono-span, J.F. Furnir Holver, Losan, Kastamonu, Rompaper, Ecopack, Ecopaper.

We relocated in Brasov for the highly professional, efficient and competitive labour force that we needed for our business expansion. We were greatly interested in the staff previously well trained into the industrial production processes.

Florin Onu - General ManagerBenchmark Electronics Romania

No Clients Surface (sq m) Industrial Park Type of lease

1 Preh

Continental Powertrain

Inter Cars

HIB Solutions

13,000

2,000

5,500

4,500

Brasov Industrial Park

Brasov Industrial Park

WDP Codlea Industrial Park

Olympian Park

BTS

BTO

Pre-lease

BTS

Year

2015

2015

2013

2013

2

3

4

FIGURE 10: MAJOR INDUSTRIAL TRANSACTIONS BRASOV

CBRE - Brasov Real Estate 201512

FIGURE 11: MAJOR INDUSTRIAL PARKS IN BRASOV

13CBRE - Brasov Real Estate 2015

COMMERCIAL TERMS AND MARKET PRACTICE

ASKING RENTS• Class A 4.5-6 EUR/Sq m • Class B 2.5-3 EUR/Sq m• Class C&D 0.5-1.5 EUR/Sq m

LEASE TERM• 3 years in existing buildings• 7-10 years for built-to-suit (BTS) projects

HEADLINE RENT• Paid monthly in advance; quoted in EUR, paid in RON• Annual indexation linked to CPI indices (usually HICP Index)

EFFECTIVE RENT• Average rent accounted over entire lease period, including financial incentives provided to tenant by

landlord (e.g. rent free periods, fit-out contribution)

SERVICE CHARGES• Class A 0.8 EUR/Sq m• For class B buildings the service charge is usually covered by the rent• Paid monthly in advance; generally quoted in EUR, paid in RON• Based on ‘open book principle’, reconciled annually

SCOPE OF SERVICES INCLUDED IN SERVICE CHARGES• Security of park - common areas; Property taxes; Property insurance (excl. tenant internal area); Property management; Maintenance and repairs; Landscaping / site cleaning; Snow removal; On-site personnel

LEASE SECURITY• Bank guarantee (common) or deposit (rare), equal to 3 - 6 months’

rent + service charges + VAT• Parent company guarantee (espe-cially in the case of new companies)

INSURANCE• Liability insurance, insurance for own installations and owned equip-ment - covered by tenant• Building insurance and landlord liability insurance included in service charges - covered by tenant

REPAIRS• Internal - covered by tenant• Structural and common areas - covered by tenant (part of the service charge)

TENANT INCENTIVES• Rent-free periods• Partial fit-out according to tenant’s specification and the required adaptation works

METHODOLOGY & DEFINITIONS

Prime headline rent (in Euro per sq m) represents the top open-market tier of rent that could be expected for a unit of standard size commensu-rate with demand in each location, of highest quality and specification and in the best location in a market at the survey date. For the purposes of this report, a unit of standard size is assumed to be around 2,000 sq m GLA.

Vacancy Rate - (in sq m) represents the total net lettable (or rentable) floor space in existing properties, which is physically vacant and being actively marketed at the survey date. Prime headline rent (in Euro per sq m) represents the top open-market tier of rent that could be expected for a unit of standard size commensu-rate with demand in each location, of highest quality and specification and

in the best location in a market at the survey date. For the purposes of this report, a unit of standard size is assumed to be around 2,000 sq m GLA. Effective rent – an average rent over the whole lease period which includes tenant’s incentives.

Build-to-suit (BTS) – a non-standard warehouse or industrial scheme designed according to specific tenant’s requirements regarding size, location and building standards. The design is based on the client’s technology process. The projects are usually dedicated for one tenant, newly built or a�er general refurbishments. BTS projects are more and more popular, especially for production companies. Clients preferring BTS investments over constructing their own buildings, limit the risk by choosing an experi-enced developer, shorten the time necessary for the development

process and reduce the development cost by using the developer’s resourc-es. Lease agreements are more advantageous than the construction of a company’s own facilities, mainly because such projects do not require the involvement of their own capital and provide flexibility for future extension or relocation.

CBRE - Brasov Real Estate 201514

LABOUR MARKET

Between 1990 and 2004 industrial production in Brasov county decreased by 70%, companies like: Roman Trucks Factory, Tractorul Plant and Bearing Factory Brasov which previously employed about 80,000 people decreased their manufacturing activity or even closed it. As a consequence a large labour pool available for being employed appeared within a couple of years.

Among the first international companies to consider relocating their production processes in the central part of Romania was HIB Rolem in 1994 with around 1,200 employees and Autoliv in 1997 which now has around 5,800 employees.

Companies have been attracted back then by the high unemployment rate,

the skilled labour force which previously worked in different industrial sectors and of course by the educational facilities.

Lately we see an increasing demand, thus difficulty, to hire unskilled workers forcing companies to expand their search area to over 60 km and offer a salary bump. Almost the same situation we can observe when looking towards the more qualified labour force as more and more companies started to open local R&D departaments such as: Autoliv, Ina Schaeffler, Continental Powetrain.

German companies decided to help the local educational system in Brasov by creating Kronstadt German Professional School which at the end of the program hire the students.

FIGURE 12: NET MONTHLY SALARY (EUR) IN BRASOV BY DOMAINS OF ACTIVITY

Industrial Sector

Plant manager

Production manager

Logistics Manager

Production engineer

Quality engineer

Maintenance engineer

Shift leader

Skilled operator

Net Salary-Euro

2000-4000

1200-1800

800-1300

600-1000

500-800

500-800

400-600

250-400

Source: Manpower

Good road routes connections, central country location and the growing necessities for A class warehouses pushed us into considering further devel-opment projects in Brasov region in the comong few months.

Athos Myrianthous -Development DirectorHelios Phoenix

15CBRE - Brasov Real Estate 2015

Source: CBRE Research

RETAIL MARKET

Even if Brasov is the 7th largest city in Romania, until recently the retail market was rather undeveloped and scattered into multiple, small and medium size schemes. A�er the opening of Coresi Shopping Resort, in Q1 2015, the situation is different, Brasov having a retail density of 463 sq m of retail space per 1,000 inhabitants.

HIGH-STREET

Compared to many other regional cities, Brasov has a strong,

BrasovRetail

high-performing and attractive high-street environment. Republicii Blvd, Muresenilor Blvd, Piata Sfatului and the surrounding streets form a mix of retail, leisure and entertainment, set within the beautiful medieval architecture of the old city center.

Among the most important retailers present we can name: Stefanel, Ecco, Tamaris, Carturesti, Librariile Humanitas, Nissa, Gaastra, Musette, Depot 96, Tommy Hilfiger, DM Drogerie, Sensiblu. In terms of food & beverage international chains like McDonald’s, KFC, Come Back are

present, alongside local and national operators: Chocolat, Taverna Sarbului, Prato, Bistro dell’Arte, Betty Ice, Petru.

SHOPPING CENTERS

The market is polarised between two types of malls: first and second generation centers, opened before 2008 / 2009, in some cases obsolete and under-performing, and one third generation scheme (Coresi Shopping Resort). In total the modern retail stock in Brasov is of 117,000 sq m, with first and second generation schemes accounting for 60%.

0

100

200

300

400

500

600

700

800

Sq m

/ 1

,000

inha

bita

nts

Current Retail Density Under Construction Retail Density

Romania

Bucharest

ClujNapoca

Timisoara

Iasi Constanta

Craiova

Brasov

Galati

Oradea

BrailaArad

Pitesti

FIGURE 13: RETAIL DENSITY

CBRE - Brasov Real Estate 201516

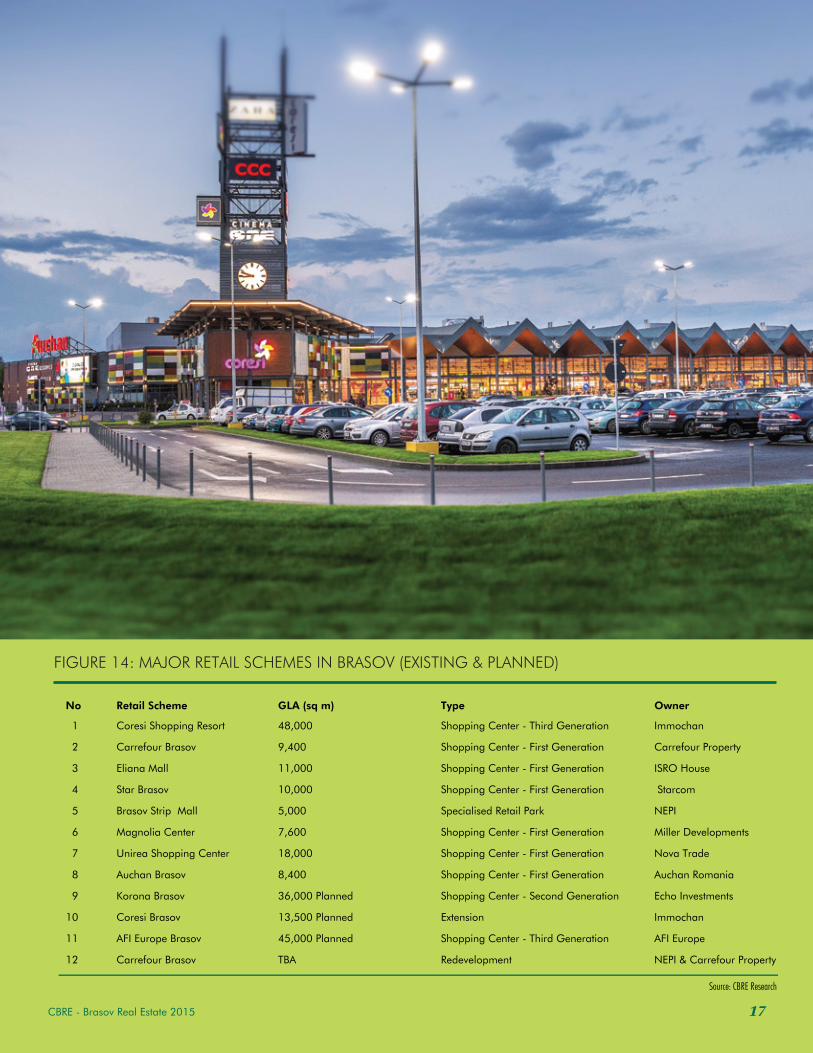

No Retail Scheme GLA (sq m) Type Owner

Coresi Shopping Resort

Carrefour Brasov

Eliana Mall

Star Brasov

Brasov Strip Mall

Magnolia Center

Unirea Shopping Center

Auchan Brasov

Korona Brasov

Coresi Brasov

AFI Europe Brasov

Carrefour Brasov

1

2

3

4

5

6

7

8

9

10

11

12

48,000

9,400

11,000

10,000

5,000

7,600

18,000

8,400

36,000 Planned

13,500 Planned

45,000 Planned

TBA

Shopping Center - Third Generation

Shopping Center - First Generation

Shopping Center - First Generation

Shopping Center - First Generation

Specialised Retail Park

Shopping Center - First Generation

Shopping Center - First Generation

Shopping Center - First Generation

Shopping Center - Second Generation

Extension

Shopping Center - Third Generation

Redevelopment

Immochan

Carrefour Property

ISRO House

Starcom

NEPI

Miller Developments

Nova Trade

Auchan Romania

Echo Investments

Immochan

AFI Europe

NEPI & Carrefour Property

FIGURE 14: MAJOR RETAIL SCHEMES IN BRASOV (EXISTING & PLANNED)

Source: CBRE Research

17CBRE - Brasov Real Estate 2015

18

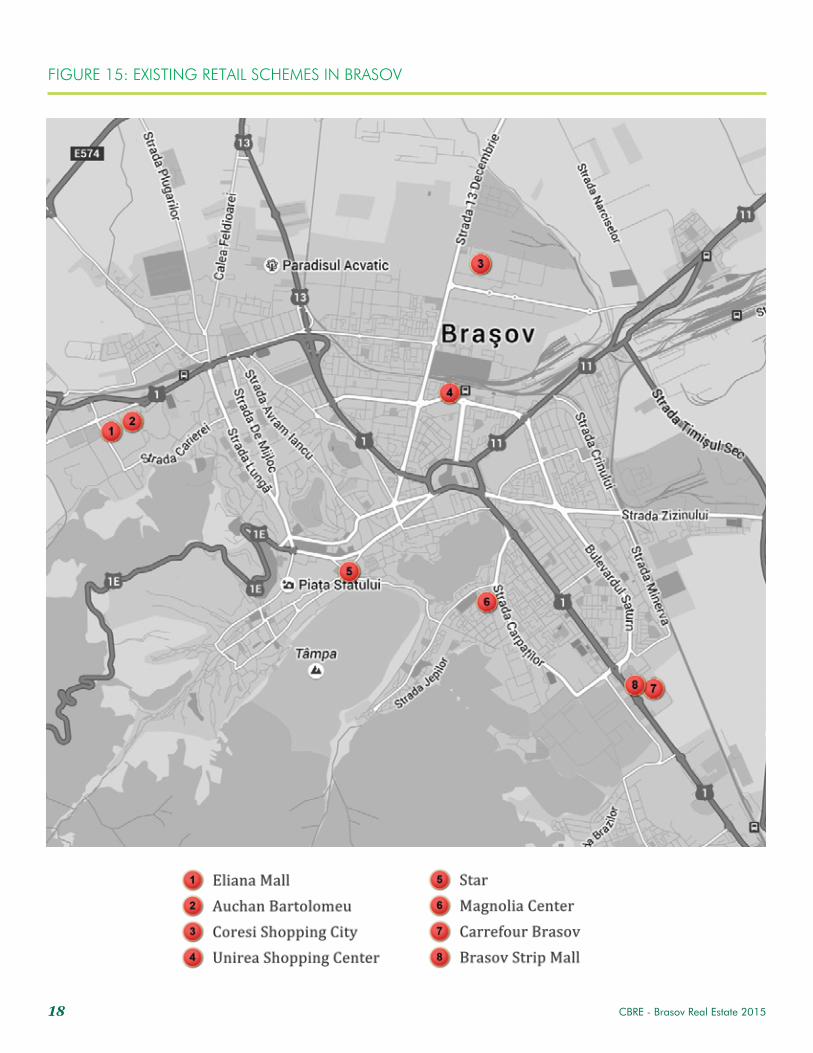

FIGURE 15: EXISTING RETAIL SCHEMES IN BRASOV

CBRE - Brasov Real Estate 2015

In addition to the above mentioned sites, there are multiple stand-alone units, operated by hypermarkets (Kaufland), discounters (Lidl, Penny Market), cash&carry (Metro, Selgros) and DIY units (Praktiker, Brico Depot, Horhbach, Dedeman, Baumax).

Brasov offers multiple options for shopping, within a variety of formats, targeting locals, customers from neighbouring counties and tourists.

PIPELINE

During 2007 – 2008 several retail schemes were proposed for develop-ment in Brasov, meaning IUS Center (Immofinanz), Civis Center (former Riofisa), Polus Center (Trigranit), Roua Shopping Park (Immofinanz). At the moment all of them are on hold, with limited chances for development in the format initially presented.

Most recently, three major develop-ers showed interest in Brasov: NEPI, through a partnership with Carrefour Property, to extend, redevelop the site where currently Carrefour operates, AFI Europe, through the acquisition of the Hidromecanica plot, owned by Cora, Echo Invest-ments, by pursuing the development of Korona Shopping Center (former factory Fartec).

AFI Europe plans to open up a third generation shopping center of around 45,000 sq m, alongside a class A office building of 12,000 sq m. The scheme is scheduled for opening in Q4 2017.

In addition, Coresi Shopping Resort is planned for an extension of around 13,500 sq m, in the form of exterior big box units, located near the existing shopping centre.

It is difficult to estimate which scheme will start first the construc-

tion, but it is unlikely that more than one developer will proceed with development.

DEMAND

All major food and DIY operators are present in the market, with one or multiple outlets. Also, homeware retailers like Altex, Flanco, Media Galaxy, Mobexpert, Jysk are present. Fashion stores include Inditex brands, H&M, German retailers like New Yorker, C&A, Takko, Deich-mann, niche retailers like Nissa, Steilmann, Ecco, Musette. Special-ised retailers like Noriel, Carturesti, Sergent Major, are also present. Comfort categories is represented by Douglas, Sephora, Yves Rocher, DM Dorgerie and others. In general the market is well balanced and offers plenty of attractions.

CBRE - Brasov Real Estate 2015 19

Recognising that Brasov is the main touristic destination in Romania, attracting approx. 1.5 million tourists a year and has a large number of inhabitants with above average spending power, convinced us to enter the Brasov retail market and develop this mixed use project of a 45,000 sqm GLA and a 12,000 sqm GLA class A office building.

David Hay - CEOAFI Europe Romania

CBRERazvan IorguManaging Director+40 21 313 10 [email protected]

ManpowerAlpar MajorKey Accounts Manager+40 268 424 [email protected]

Ascenta Management Florin RebicPartner+40 21 210 40 [email protected]

CBRE - Brasov Real Estate 201520

Contacts

Disclaimer: Information contained herein, including projections, has been obtained from sources believed to be reliable. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to confirm independently its accuracy and completeness. This information is presented exclusively for use by CBRE clients and professionals and all rights to the material are reserved and cannot be repro-duced without prior written permission of CBRE.

Daniela Gavril Research Analystt: +40 21 313 10 20e: [email protected]

Tudor MunteanResearch Analyst t: +40 21 313 10 20e: [email protected]

Laura Dumea-BenczeHead of Researcht: +40 21 313 10 20e: [email protected]

Walter WolflerSenior DirectorHead of Retail CEE CBRE GmbHt: +43 1 533 40 80 97e: [email protected]

Joerg KreindlSenior DirectorHead of Industrial CEEt: +48 22 544 8006e: [email protected]

Mike AtwellSenior DirectorHead of Capital Markets CEEt: +48 22 544 8070e: [email protected]

Related Documents