AIM RD.020 CURRENT BUSINESS BASELINE & BUSINESS PROCESS Author: Creation Date: March 19, 2009 Last Updated: May 27, 2010 Document Ref: <Document Reference Number> Version: 1.1 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AIMRD.020 CURRENT BUSINESS BASELINE & BUSINESS PROCESS

Author:

Creation Date: March 19, 2009

Last Updated: May 27, 2010

Document Ref: <Document Reference Number>

Version: 1.1

1

Document Control

Distribution

Copy No. Name Location

1 Library Master Project Library2 Project Manager Nairobi3 Satyam Library Hyderabad

Note to Holders:

If you receive an electronic copy of this document and print it out, please write your name on the equivalent of the cover page, for document control purposes.

If you receive a hard copy of this document, please write your name on the front cover, for document control purposes.

2

Table of Contents

Document Control........................................................................................................................................................... 2Change Control......................................................................................................................................................................2Reviewers..............................................................................................................................................................................2Distribution........................................................................................................................................................................... 2

Document Scope.............................................................................................................................................................. 5

Introduction.................................................................................................................................................................... 6

Business Function and Process Descriptions................................................................................................................... 7

1. The journal Vouchers.................................................................................................................................................. 81.1. Posting General Ledger Vouchers Procedures................................................................................................................81.2. The Journal Balancing...................................................................................................................................................101.3. Accounts Journal Summary..........................................................................................................................................111.4. Batch Slip......................................................................................................................................................................111.5. Foreign Currency Amount............................................................................................................................................12

2. Branch Contra Reconciliation................................................................................................................................... 132.1. Debit Voucher:.............................................................................................................................................................132.2. Credit Voucher:............................................................................................................................................................13

3. Foreign Accounts:..................................................................................................................................................... 143.1. Project Accounts:..........................................................................................................................................................143.2. Current Accounts:.........................................................................................................................................................143.3. DFCC (Domestic Foreign cheques clearing)..................................................................................................................143.4 Deposit accounts...........................................................................................................................................................153.5 Ramp.............................................................................................................................................................................153.6 Accrued Interest............................................................................................................................................................153.7 Gold...............................................................................................................................................................................15

4. Foreign Assets:.......................................................................................................................................................... 164.1. Analysis of Accrued Interest on Foreign Deposits.........................................................................................................174.2. Analysis of Revaluation Accounts.................................................................................................................................174.3. Forex Cash Reconciliations...........................................................................................................................................18

5. Local Assets............................................................................................................................................................... 195.1. Staff loans Reconciliations............................................................................................................................................195.2. Fixed Assets Analysis....................................................................................................................................................215.3. Annual Budget..............................................................................................................................................................215.4. Expenses, Income Liabilities and Other assets..............................................................................................................23

6. Analysis and Other Reconciliations........................................................................................................................... 256.1. Reconciliation of sundry Creditors/Debtors accounts..................................................................................................256.2. Miscellaneous & KSMS Accounts..................................................................................................................................256.3. Movement Summary of Banks under Liquidation........................................................................................................256.4. Analysis of the main general Ledger Asset Accounts, All local investment Earnings and Monetary Policy Interest expenses a/c........................................................................................................................................................................256.5. Banking Office Balances –End of month Adjustments..................................................................................................266.6. Payments in advance....................................................................................................................................................276.7 Amortization..................................................................................................................................................................276.8 Online posting...............................................................................................................................................................27

3

7. Claims and Reconciliation......................................................................................................................................... 287.1. Claims from Other Institutions.....................................................................................................................................28

8. Reconciliation and Analysis....................................................................................................................................... 298.1. Imprest account............................................................................................................................................................298.2. Other Debtors...............................................................................................................................................................298.3. Other accounts.............................................................................................................................................................298.4. Monthly Reconciliation.................................................................................................................................................30

Financial Statements..................................................................................................................................................... 31

Management Accounts.................................................................................................................................................. 32

Procedures for Closing the Month/year.......................................................................................................................... 33Procedures for the closure of Month..................................................................................................................................33Procedures for Closing/Opening the Financial Year............................................................................................................33

Process Flows................................................................................................................................................................ 34

GL critical requirements............................................................................................................................................... 39

9. Open and Closed Issues for this Deliverable.............................................................................................................. 53Open Issues.........................................................................................................................................................................53Closed Issues.......................................................................................................................................................................53

4

Document Scope

This document details the existing CBK General Ledger systems that are currently in practice. It aims to

provide the Project Team with an understanding of the functioning of the General Ledger System. The

General Ledger System of CBK is developed to cover the various processes of the GL viz. Foreign

Assets, Reconciliation and Analysis section, Local Assets. The way financial statements are prepared

from the data obtained from the books of the organization head office and branches which are

summarized for the period and expressed in monetary terms. This document will be used as the basis for

all Business Requirements. It provides the “As-Is” Scenario of the General Ledger functions in CBK.

5

Introduction

The General Ledger System of CBK is developed to cover the various processes of the General Ledger.

Financial Accounts division is divided into three sections, 1.Foreign Assets 2. Reconciliation and

Analysis section, 3.Local Assets. Foreign assets mainly deal with the deposits made by the bank in

foreign currencies and a separate subsidiary ledger is maintained in foreign department where

transactions are raised and posted, and at the end of the day they close the ledger and copy the same

transactions into Finance department where the functional currency ledger is maintained. Reconciliation

and Analysis section mainly handles reconciliation of Imprest accounts, other debtors, other accounts,

Branch contra Transactions, and monthly reconciliation accounts. Local assets are those, which mostly

deal with the employee staff loans to whom the bank has lend the money in the form of House loan, Car

loan, salary advance & related insurances, Development loans.

Financial statements of the Bank are prepared in the Finance Accounts division for Management

purposes and for external users e.g. Government, Auditors, etc. The main objective of preparing the final

accounts is to ascertain the performance and financial position of the Bank. Financial statements are

prepared from the data obtained from the books of the organization and it is summarized over a certain

period and expressed in monetary terms.

6

Business Function and Process Descriptions

This component describes each of the high-level business functions and the processes being followed at

Central Bank of Kenya. The business function contains the following sections:

Descriptive overview

Process descriptions

Process relationship

Descriptive Overview of General Ledger

Central Bank of Kenya (CBK) maintains the General ledger System which is developed to cover the

various processes of the GL viz. Foreign Assets, Reconciliation and Analysis section, Local Assets. The

way financial statements are prepared from the data obtained from the books of the organization head

office and branches which are summarized for the period and expressed in monetary terms. This

document will be used as the basis for all Business Requirements.

The activities carried out in the General Ledger can be broadly grouped under

Process Description CBK-GL-010 Posting GL voucher procedures

CBK-GL-020 Journal Balancing

CBK-GL-030 Foreign Assets

CBK-GL-040 Staff Reconciliations

CBK-GL-050 Analysis of Staff Deposits

CBK-GL-060 Fixed Assets Analysis

CBK-GL-070 Annual Budget

7

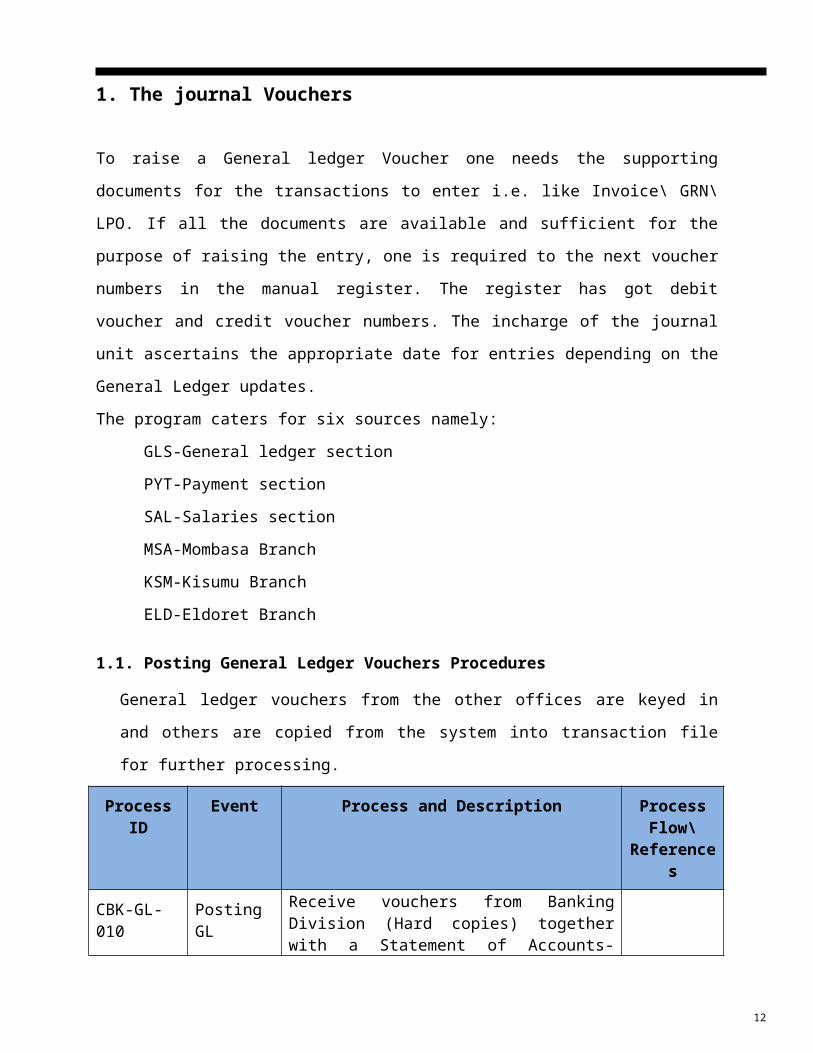

1. The journal Vouchers

To raise a General ledger Voucher one needs the supporting documents for the transactions to

enter i.e. like Invoice\ GRN\LPO. If all the documents are available and sufficient for the

purpose of raising the entry, one is required to the next voucher numbers in the manual register.

The register has got debit voucher and credit voucher numbers. The incharge of the journal unit

ascertains the appropriate date for entries depending on the General Ledger updates.

The program caters for six sources namely:

GLS-General ledger section

PYT-Payment section

SAL-Salaries section

MSA-Mombasa Branch

KSM-Kisumu Branch

ELD-Eldoret Branch

1.1. Posting General Ledger Vouchers Procedures

General ledger vouchers from the other offices are keyed in and others are copied from the

system into transaction file for further processing.

Process ID Event Process and Description Process Flow\

References

CBK-GL-010

Posting GL vouchers procedures

Receive vouchers from Banking Division (Hard copies) together with a Statement of Accounts-General Ledger for the same date.

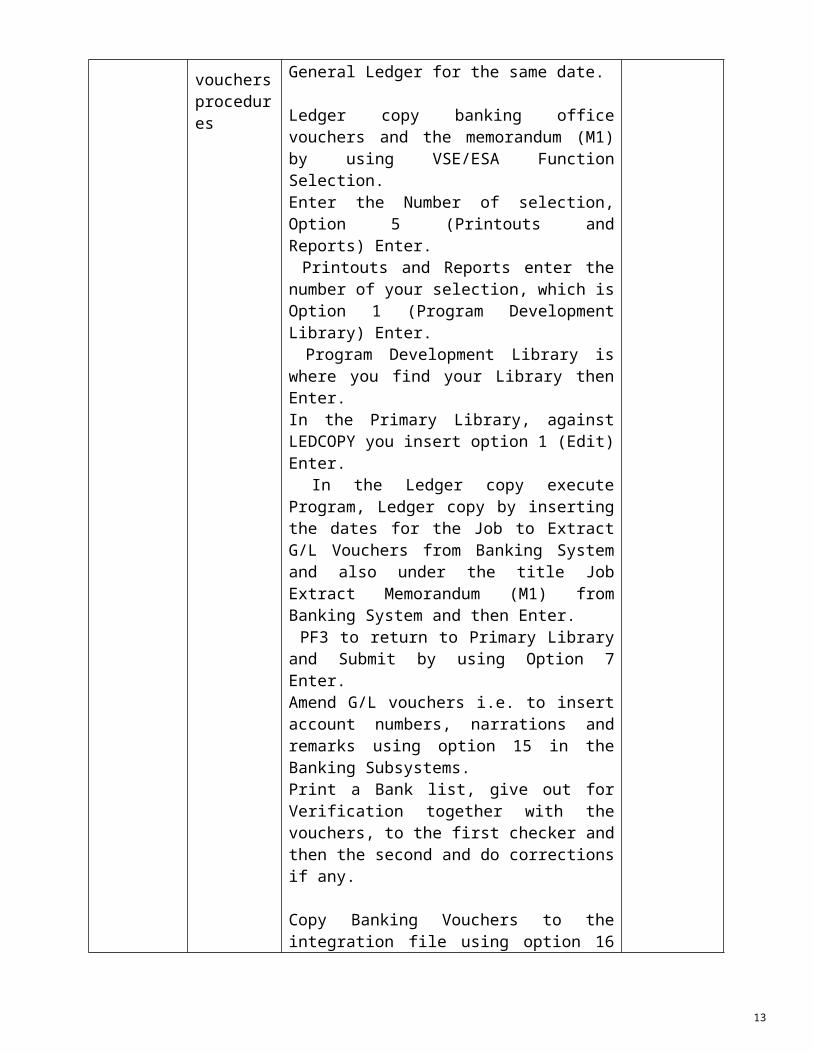

Ledger copy banking office vouchers and the memorandum (M1) by using VSE/ESA Function Selection.Enter the Number of selection, Option 5 (Printouts and Reports) Enter. Printouts and Reports enter the number of your selection, which is Option 1 (Program Development Library) Enter. Program Development Library is where you find your Library then Enter.In the Primary Library, against LEDCOPY you insert option 1 (Edit) Enter. In the Ledger copy execute Program, Ledger copy

8

by inserting the dates for the Job to Extract G/L Vouchers from Banking System and also under the title Job Extract Memorandum (M1) from Banking System and then Enter. PF3 to return to Primary Library and Submit by using Option 7 Enter.Amend G/L vouchers i.e. to insert account numbers, narrations and remarks using option 15 in the Banking Subsystems.Print a Bank list, give out for Verification together with the vouchers, to the first checker and then the second and do corrections if any. Copy Banking Vouchers to the integration file using option 16 in the Banking Subsystems.

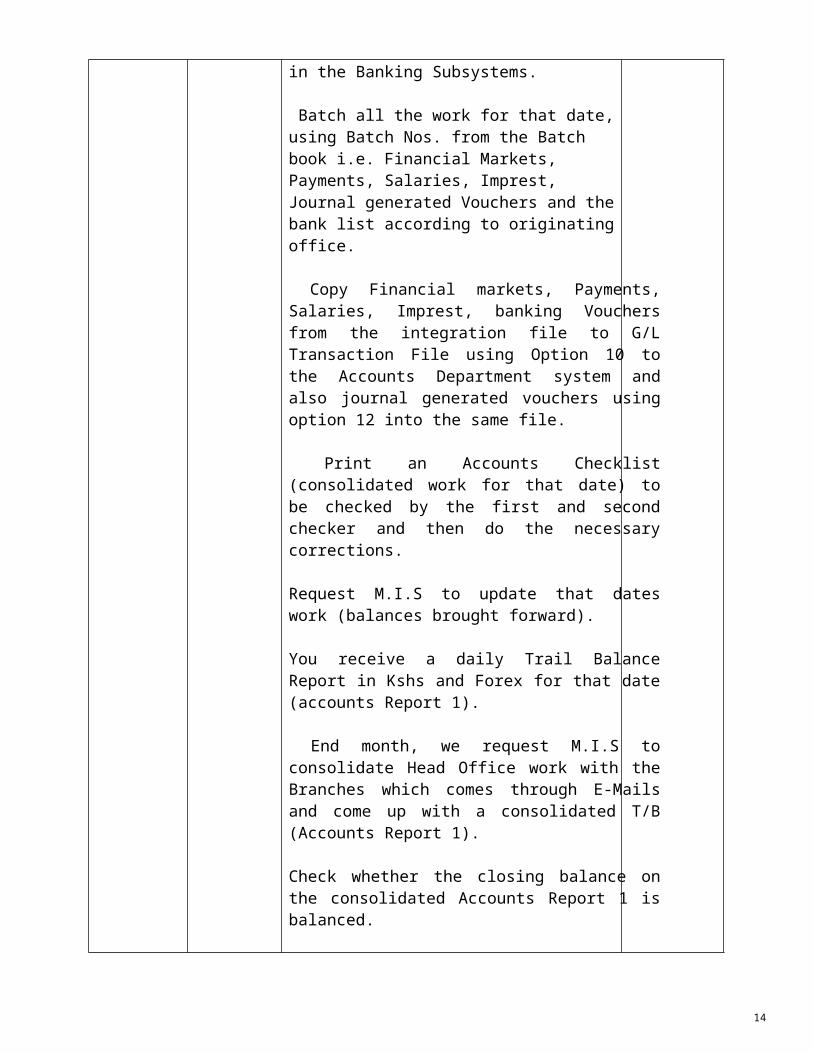

Batch all the work for that date, using Batch Nos. from the Batch book i.e. Financial Markets, Payments, Salaries, Imprest, Journal generated Vouchers and the bank list according to originating office.

Copy Financial markets, Payments, Salaries, Imprest, banking Vouchers from the integration file to G/L Transaction File using Option 10 to the Accounts Department system and also journal generated vouchers using option 12 into the same file.

Print an Accounts Checklist (consolidated work for that date) to be checked by the first and second checker and then do the necessary corrections.

Request M.I.S to update that dates work (balances brought forward).

You receive a daily Trail Balance Report in Kshs and Forex for that date (accounts Report 1).

End month, we request M.I.S to consolidate Head Office work with the Branches which comes through E-Mails and come up with a consolidated T/B (Accounts Report 1).

Check whether the closing balance on the consolidated Accounts Report 1 is balanced. Request M.I.S to print end month Reports 7,2,5,F and Accounts monthly/Special statements for the General

9

Ledger Accounts, running from the first working day of the month to the last day.

1.2. The Journal Balancing

Journal balancing provides a quick check of the entries posted as regards the double entry system i.e. all

transactions posted is equal in amounts and balanced. The journal balancing is the place where the user

cross verifies the entries of all ledger transactions which are flown from Banking, Forex, Payments

Vouchers and salaries Gl vouchers. The user will cross verify the general ledger transactions data with

the sub ledger transaction data to do the journal balancing. If any mismatch found means then they write

to the respective department to do the needful inspection.

If the once the journal balancing is done then they run a report, where in the report one can find the Checked by and approved by

Process ID Event Process and Description Process Flow\

References

CBK-GL-020

Journal Balancing

For one to do the journal balancing the following documents are required:

Memorandum from banking departmentFinancial markets from journal summaryJournal Vouchers from various officesPayroll vouchers from salaries sectionImprest vouchers from payments sectionPayments vouchers from payments section

Once the user get all the need documents then they will cross verify the same with the ledger in order to perform the journal balancing.

After sorting out documents according to originating offices, ensure all the documents have:

Ensure the documents have two signatures.Ascertain the following documents from financial markets have been submitted to you.

Certificate - voucherFinancial markets – journal summary at the

10

close of the day. Checking list for vouchers posted on that particular day.

Thereafter take the banking memorandum debit grand totals subtract the corresponding credit vouchers amount from financial markets certificates; enter the amount you have arrived at in the batch slip.

The same treatment applies to credits on the banking memorandum and the debit voucher from financial markets.

Add the totals on other offices vouchers according to the originating offices.For the Journal Vouchers – Print Journal RPT 2 the Amount on RPT 2 must agree with the Total Amount on the Vouchers.

Enter the total amount in the batch slip.

These are all self - balancingFinally enter the total amounts on the daily summary for that particular day.

1.3. Accounts Journal Summary

The main objective of preparing this is to ensure Total debits agree with Total credits.

There are Columns for all the affected Offices, enter the amount on the corresponding Debit and

Credit.

The Total Debits must agree with Total Credits.

Finally attach a detailed cast for easier counter checking of the Work.

1.4. Batch Slip

The following details must be entered in the Batch Slip: -

Originating Office

Ledger Date

Batch Code

Amount in Local Currency (Kshs)

Foreign Currency Amount

11

This is the final stage of journal balancing and it must balance before the next stage of transactions

consolidation commences.

1.5. Foreign Currency Amount

Add DEBITS (FOREX) and CREDITS (FOREX) Amount from all the Batches in the Checking List of

Financial Markets for Vouchers posted on that particular Day.

Subtract Forex amount from all Local Accounts in the Journal Summary in (kshs).

Finally enter the Forex Amount on the Batch S.

12

2. Branch Contra ReconciliationThe head office will do some payments n behalf of the branches at times, so whenever such transactions

arise they or call it as contra transactions. And here there will not be any cash movement when they

settle the contra transactions. Central Bank has three branches namely: Mombasa, Kisumu and Eldoret.

Branch contra reconciliation aims at clearing claims and reimbursements both from H/O and branches.

The branches raise two types of general ledger Vouchers: Credit and Debit.

2.1. Debit Voucher:

When a branch incurs expenses on behalf of the Head office e.g. in training or medical, they pass entries

debiting the Head office. When the voucher is received, entries are raised crediting the particular branch

and debiting the various accounts e.g. local courses.

As regards utilities for the police attached to the branch, the branch debits the head office. The generated

list from the branch is sent to Salaries section for action, where recoveries are made from the police

through the payroll.

2.2. Credit Voucher:

When the Head office incurs expenditure on behalf of the branch, documents evidencing the expenditure

i.e. L.P.O., G.R.N., and invoices, which are obtained from the payments section of head office, are sent to

the particular branch making the claim. When satisfied, the branch credits the H/office.

As regards repayments of loans, branches raises’ entries by crediting H/office contra. When received at

the h/office, entries are raised by; debiting the branch concerned and crediting the particular account e.g.

house loan, salary advance, development loan etc. Salaries section also updates by passing the entries

through the payroll.

13

3. Foreign Accounts:

Foreign accounts are of three types namely:1. Project accounts2. Current accounts3. DFCC Accounts (Domestic foreign currency checks & clearing)4. Deposits account5. Special project accounts6. Gold7 Ramp accounts8. Accrued interest

3.1. Project Accounts:

Central Bank of Kenya provides the funds to government to fund for the activities like Dams, Poverty

fund, Drought and etc. So the bank defines some accounts in order to fund for such, which are named as

Project funds.

3.2. Current Accounts:

Central Bank of Kenya utilises current accounts for payments both on behalf of government’s payments

and itself. Does the main purpose as outlined above is usually met by opening various accounts in

different currencies. At the month end all foreign accounts are revalue using closing rates provided by

Treasury/Dealing room Section and posted into profit & loss accounts by foreign investments. To capture

such foreign currency transactions they bank defined some accounts which are named as foreign accounts

(Assets), Interest income and revaluations accounts.

3.3. DFCC (Domestic Foreign cheques clearing)

These are the accounts that are used by Central Bank of Kenya for the clearing the locally denominated

Forex cheques.

.

14

3.4 Deposit accounts

The bulk of the Bank’s foreign assets are held in major correspondent banks which situated in several countries in the world i.e. England, America and Germany.

3.5 Ramp

This is a new program for investing the bank’s deposits with the World Bank. It is World Bank program where the bank’s invest in several securities (bonds, bills, shares etc) and are managed by the investment manager and global custodian.

3.6 Accrued Interest

This is interest earned from deposits held in various correspondent banks. This interest is accrued over the investment period on monthly basis.

3.7 Gold

Gold are part of foreign assets but held locally in bank. We usually revalue the asset on monthly basis and no entries are passed on sale or purchases.

15

4. Foreign Assets:Foreign assets mainly deal with the deposits made by the bank in foreign currencies and a separate

subsidiary ledger is maintained in foreign department where transactions are raised and posted, and at

the end of the day they close the ledger and copy the same transactions into Finance department where

the functional currency ledger is maintained. The main reconciliation and analysis of foreign accounts is

done in Financial Markets Department. Financial Accounts division reconcile financial markets ledger

to General Ledger and advice the appropriate department to raise correcting entries in case of

differences.

Process ID Event Process and Description Process Flow\

References

CBK-GL-030

Foreign Assets reconcile

To do the reconcile of foreign accounts

An accrptf; which shows the balances of foreign

accounts and compares the G/ledger and F/ledger

and gives the differences (deviations) at the close of

a certain period.

A Special statement of the Foreign ledger account

for a certain period (Done in Foreign department)

An Accounts statement of the General ledger

account for the same period

Previous reconciliation if there was any.

One needs to examine the deviations in the Accrptf

among all the accounts to identify those with a

difference, as this is the basis of reconciliation.

Then one ticks the figures in the special and

accounts statements and leaves out the outstanding

or unmatched figures for the reconciliation report is

drawn on them.

16

Using Excel or spreadsheet one can key in the

outstanding figures starting with the balance from

one ledger.

Key in the figures to be added with the necessary

remarks and the office to rectify.

Key in the figures to be deducted if any with the

necessary remarks and the office to rectify.

The differences between the GL and the FL must

be zeroed by necessary adjustments to the various

accounts. Notification of the office to respond to

any query is to be raised

4.1. Analysis of Accrued Interest on Foreign Deposits

This report is prepared monthly in order to determine the accrued interest on the three major foreign

currency deposits held in foreign financial institutions. One is required to have:

The interest deposits profiles, from foreign department, which have deposits with maturity dates

succeeding the period/ month of reconciliation i.e. the current profile and preceding ones.

Accounts statements are printed from the GL for the various accrued interest on the deposit

accounts.

An excel spread sheet is then prepared, summing up the accrued interest at the end of a specific month.

This has to tally with the figures in the GL. The minimal difference due to rounding up of figures is

cleared off through the passing of necessary entries in the GL after a period of time.

4.2. Analysis of Revaluation Accounts

The revaluation of accounts is done through the run of statements in GL accounts.Revaluation is

computed when encashing the investment on Maturity or at the End of the month. Revaluation amount

could be either realised or unrealised or both. To determine the realised from the unrealised one is

required to understand that end of the month or end of the year revaluation is unrealized and the rest is

realized. With the exception of current accounts and cash in hand, this realized in every revaluation

done.

17

4.3. Forex Cash Reconciliations

The Forex cash reconciliation talks about the foreign currency note purchases and selling during the day

or period. GL accounts statement is printed for the various cash accounts in order to reconcile the

accounts of foreign currency notes purchased with the cash registers. One is required to have two

registers from the Forex Cashier and the Custodian.

An Excel sheet again is used to produce the final output; by taking the GL balance and

reconciling it to the Custodian balance in banking for all the Forex accounts.

An Excel sheet again is used to produce the final output; by taking the GL balance and

reconciling it to the Custodian balance in banking for all the Forex accounts.

18

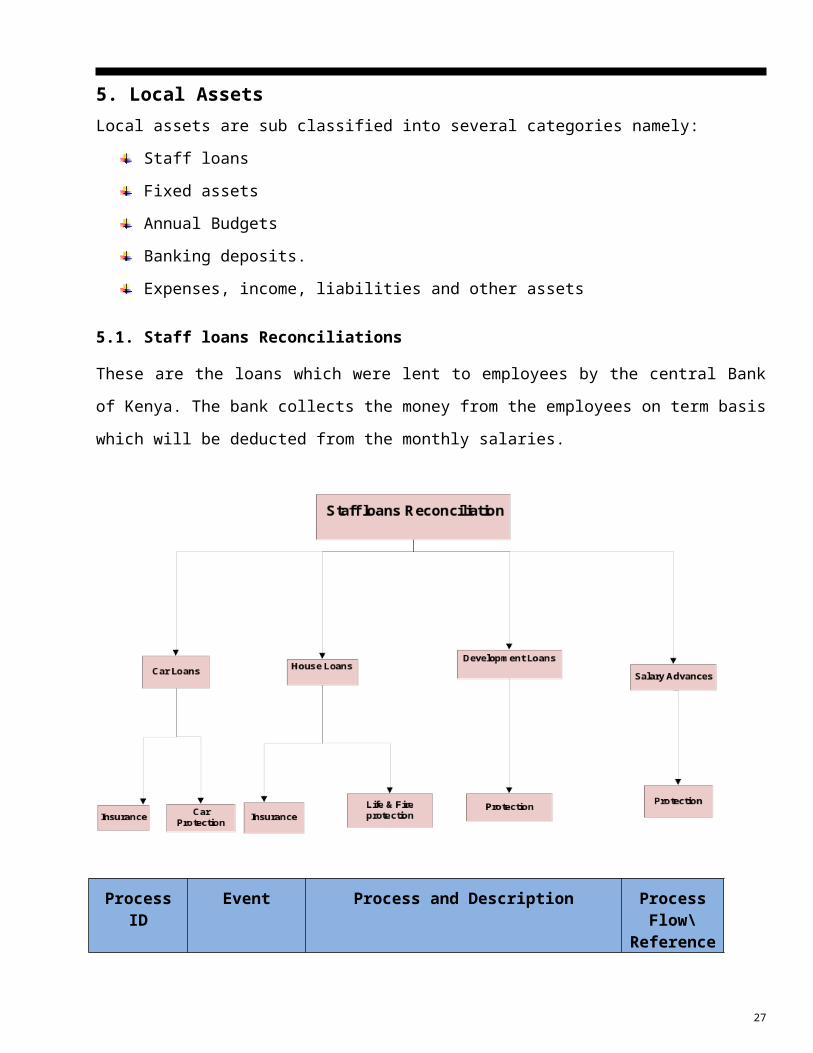

5. Local AssetsLocal assets are sub classified into several categories namely:

Staff loans

Fixed assets

Annual Budgets

Banking deposits.

Expenses, income, liabilities and other assets

5.1. Staff loans Reconciliations

These are the loans which were lent to employees by the central Bank of Kenya. The bank collects the

money from the employees on term basis which will be deducted from the monthly salaries.

Process ID Event Process and DescriptionProcess Flow\

References

CBK-GL-040

Staff Loans Reconciliation

The Gl accountant will print the monthly gl

statements and compare the physical vouchers

with the entries raised in GL for accurate

19

information. To find the variances and

complete reconciliation process they compare

payroll closing balances with the GL closing

balances to do the

If they find any variances then they take the

below action

Reversal of payroll entries.

Amend payroll where necessary

(salaries section).

5.1.1 Analysis of Staff loan deposits

Process ID Event Process and DescriptionProcess Flow\

References

CBK-GL-050

Analysis of Staff loan deposits

Staff loan deposit is an amount paid by staffs

to purchase houses, whose value is more than

the loan entitlement as per the rules.

The amount of loan given is combined with

amount deposited and the total amount paid

to the seller.

The Gl entries would be as follows :

Housing Loan A/c DR.

Staff house loan A/c CR.

5.2. Fixed Assets Analysis

Process ID Event Process and DescriptionProcess Flow\

References

20

CBK-GL-060

Fixed Assets analysis

The user prints the statement for the current

month to do the analysis.

They get the actual items purchased during the

month from the sundry payments voucher

from payment section and compares the with

GL vouchers.

Then enters the data into the system showing

the opening balances of the current year, date,

voucher no, batch no, SPV no, Memo no ( if it

is a foreign payment) and amount balances.

Give the analysis to Budgetary Section to

enable them prepare Depreciation

Incase of any mis-posting correct the journals

by reversing and raise a new journal entry.

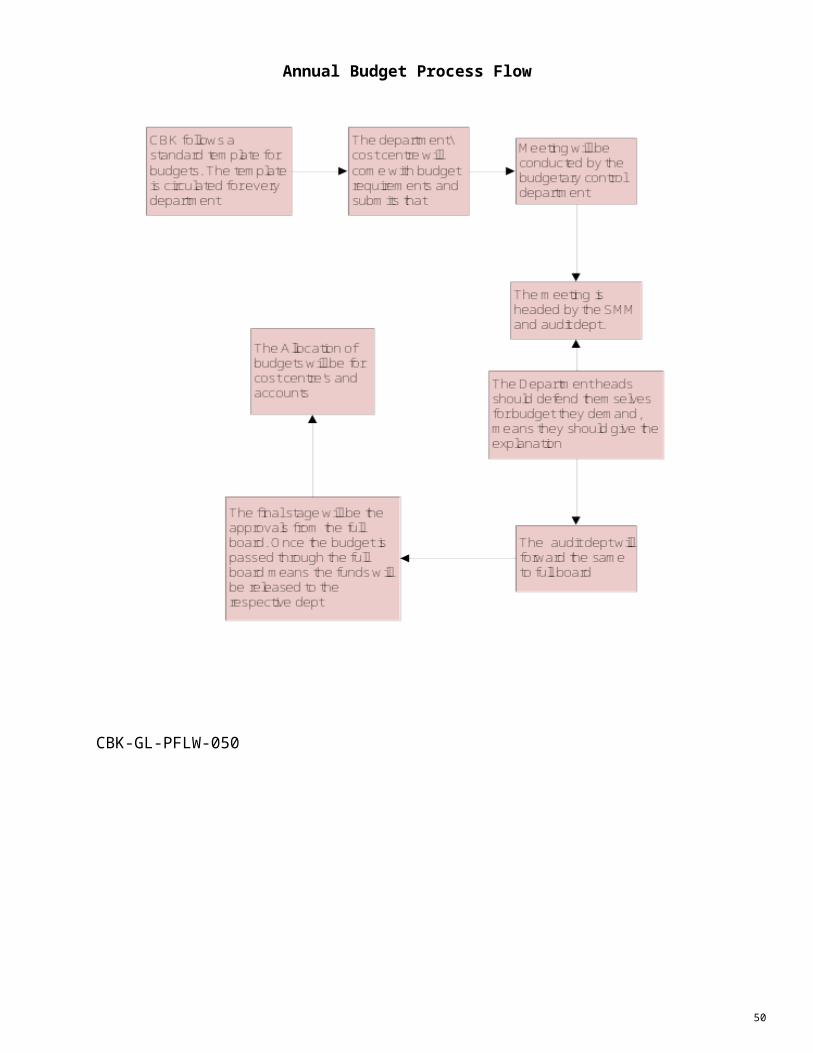

5.3. Annual Budget

The Central Bank of Kenya does the future projections based on their budgets. The budget template will

be circulated for all respective departments in the month of January, so the departments\ cost centre heads

should come up with their requirements to meet the needs of future. This involves preparing recurrent

and capital estimates to be incurred by the department during the financial year. These estimates are zero

based and an agreed inflation rate is assumed. Then budgetary control conducts a board meet headed by

the SMM, department heads and Audit department.

The Department \cost centre heads should defend themselves against their requirement of funds.

It will be reviewed by the audit dept and will forward the same to the full board to seek the final

approvals to release the funds to the respective departments\cost centres. The naming convention of the

budget will be represented with the year, it is a consolidated budget.

21

Process ID Event Process and DescriptionProcess Flow\

References

CBK-GL-070

Annual Budget A list is made of the requirements of every

section in the department with cost estimates.

Check list to avoid duplication of items and to

make sure what is in the list is really required

for cost control.

The estimates are compiled and displayed on a

spreadsheet showing monthly budget estimates

and totals.

Forward the compiled list with explanatory

notes to the finance director for approval.

5.3.1. Supplementary Budget

This involves submitting a request for additional allocation for votes overdrawn and for expenses that

were not foreseen by the time of the annual budget.

An analysis of the budget status is done by Budget department and prepares a table with the following

details:

Revenue/Expenditure heads

Approved Provision

Expenditure/Receipts to date

Revised provision

Required increase(+) or decrease(-)

For every vote a supplementary budget is required or is reduced or removed altogether explanatory notes

a required.

The list is later forwarded to the finance director for approval.

5.3.2. Monthly Budget Variance Report

22

This involves explanations for positive or negative monthly variances.

Budgrpt10 from budgetary section shows the Actual expenditure/Income Vice-versa the

budgeted expenditure/income and the variance.

You are required to provide explanations on variances exceeding 20% both negative and

positive by referring to relevant documents in Payments Section.

Detailed explanatory notes are compiled and forwarded to finance director for approval.

At the end of the financial year a cumulative variance explanation is given to include the

whole year.

5.4. Expenses, Income Liabilities and Other assets

5.4.1. Sundry salaries Deduction Suspense

The following is required to reconcile this account;

Previous Month Reconciliation

General Ledger current Statements

Vouchers posted in Salaries Office

Analyse every Entry DEBITS / CREDITS on current Month special statement, using the relevant

Vouchers from Salaries Office.

Compare Debits and Credits

Using the previous Month Reconciliation pick the outstanding amount, Key in on a Spread

Sheet.

The Closing Balance for that particular Month Reconciliation should agree with the end

Month closing Balance with the Ledger.

Finally Print the Reconciliation

5.4.2. Analysis of Banking Deposits

5.4.2.1. Accounts Involved

Government Of Kenya

Banks – Local

Banks – External

Others

23

Impersonal

This involves comparison of the posted figures in the General Ledger with the figures in the Banking

Memorandum Report. Any difference arising is detected by scrutinising the General Ledger individual

entry. Reversal entries are posted in the General Ledger.

24

6. Analysis and Other Reconciliations

6.1. Reconciliation of sundry Creditors/Debtors accounts

Provisions are made every close of Financial Year to these accounts.

Memos are received from various Departments with list of accruals to be made.

Entries are passed where you credit/debit the above account and debit/credit the relevant expense

accounts then; you file all the memos in one file for future reference and reconciliation.

When a payment is made the amount appears on the General Ledger special statement, this is

where you reconcile with amount on the memos by reducing with the amount paid and indicating

the pay date on the memo.

After reconciling, the outstanding figures are keyed in an Excel spreadsheet showing outstanding

items, where the total Closing Balance amount has to agree with the General Ledger Closing

Balance amount on the special statement.

Reconciliation are done on monthly basis.

6.2. Miscellaneous & KSMS Accounts.

Check all the entries in the General Ledger special statement analyse one by one indicating the nature of

the entry. Check any mis-posting and pass the necessary entries.

6.3. Movement Summary of Banks under Liquidation

After the trial balance of every end of month has been produced use Accounts report 7 and 2 to update

the previous summary showing the balances for the current month and the previous two months.

For the analysis show the opening balance of the current year, additions, recoveries and the closing

balance for all the banks under liquidation. Send a copy to Research Dept and one to Head, Financial

Accounts.

6.4. Analysis of the main general Ledger Asset Accounts, All local investment Earnings and

Monetary Policy Interest expenses a/c

Print a special statement for the current month.

Confirm whether the postings in the statements are correctly posted.

Indicate remarks, which may not have been captured in the statement.

25

Enter the data in the computer showing the opening balance of the current year, date, voucher no,

batch no, and particulars of amount and balances.

Compare General Ledger balances with Financial Markets balances.

In case of any miss posting, correct the same by raising a Journal entry.

6.5. Banking Office Balances –End of month Adjustments

Request for Report M2 from Banking Office for the last day of the current month and raise Journal

entries for the following accounts as shown below:

National bank overdrawn account –02-010-1100

Dr: Overnight Advances-1-12-0501-001

Cr: Local Banks (Deposit)-1-22-0201-001

Government of Kenya Overdraft-01-010-E305

Dr: Government of Kenya Overdraft-1-12-0503-001

Cr: Government of Kenya-1-22-0199-001

Unclear effects\Accounts affected

05-010-0002-Clearing A/C

05-010-0083-Outward Clearing Suspense A/C

If balance is credit

Dr: Impersonal A/c-1-23-0101-001

Cr: Uncleared Effects-1-12-0403-001

If balance is debit

Cr: Impersonal A/C-1-23-0101-001

Dr: Uncleared effects-1-12-0403-001

Reverse the Journal entries on the first working day of the following month.

In order to capture the entry for Interest on Government Overdraft for the current month in the

General Ledger request Banking Office for a copy of the entry which they raise early in the

General Ledger the following month and raise a Journal entry.

26

The Journal entry is then reversed on the day B/O has raised theirs’ since Banking Office entry is

posted on the day it has been raised.

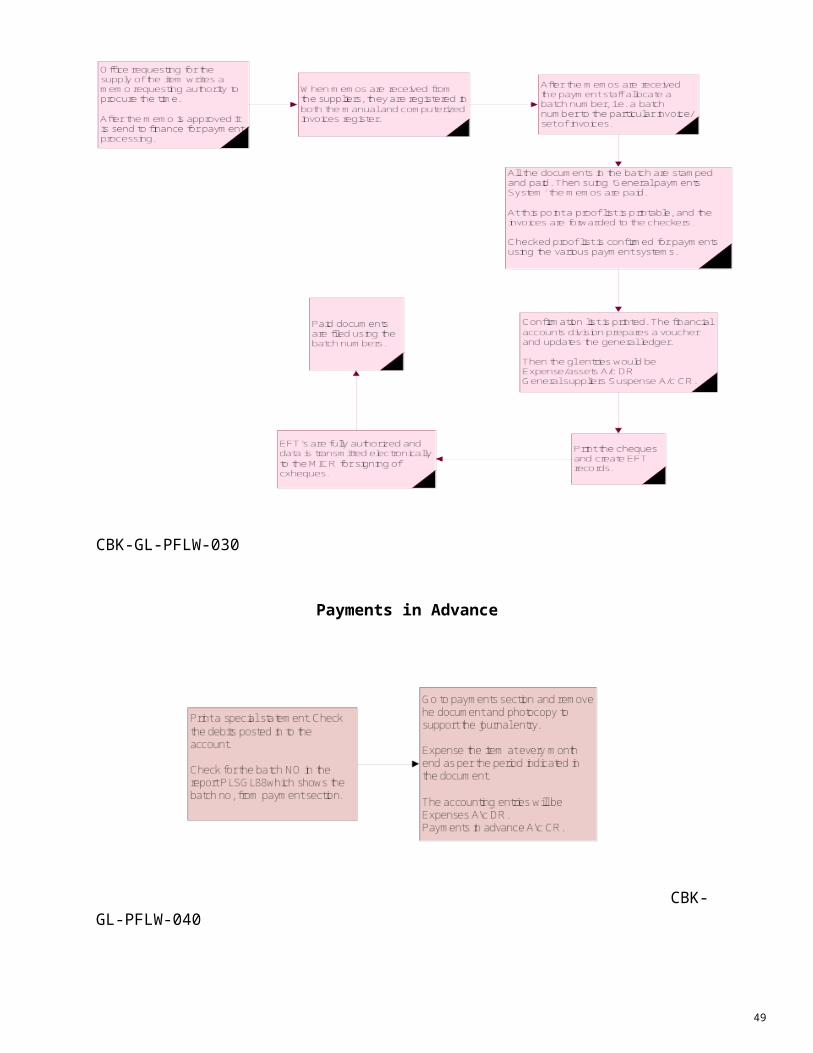

6.6. Payments in advance

Analyse the account at the end of each month.

Print a special statement for Payments in Advance a/c no.112-0703-004 before the current month

is closed.

Check the debits into the account.

From the batch, check for the entry in Report PLSGL88 which shows the batch no. of Payments

Section .The batch will show the item, which has been accrued, and the period.

Photocopy the batch to support the Journal entry.

If the payment is for that month then you expense the item by crediting Payments in Advance

A/C and debiting the expense A/C.

6.7 Amortization

The Bank pays an advance Payment to the Supplier for Currency printing. Printed Banknotes are received by Currency Department. The Banknotes are amortized after they are issued Kshs 50/= & 100/= 1year, 200/=, 500/= & 1000/=2years.

6.8 Online posting

Transferring balances from banking office to general ledger. Interest payment Interest is payable monthly @ 3% per annum on outstanding amount.

P*t*r 365*100Since by end month the government has not paid the interest we accrue by:Dr:1-12-0704-013 sundry debtorsCr:2-12-0102-001 interest on pre-1997 gok overdrawn a/c.

When payment is received from gok through kepss account no. 05-010-0126 is credited and we then:

Dr:05-010-0126 -finance dept,kepss inward payment.Cr:1-12-0704-013- sundry debtors

If the payment is by cheque:Cr: 1-12-0704-013-Sundry Debtors

27

7. Claims and Reconciliation

7.1. Claims from Other Institutions

Claim from other institutions for expenses incurred on seconded staff is made on monthly basis.

A list of seconded staff is obtained from salaries section.

General ledger Entries are passed to make provision for the expenses.

Letters of claims are prepared to various institutions.

Cheques received for payment are banked to the account of provision.

Letter of acknowledgement is then issued.

28

8. Reconciliation and Analysis

8.1. Imprest account

Step 1Impro 46 schedule containing imprest issued per day for the month to reconcile is put together.

Ledger entries on the imprest account are checked against imprest amounts on the impro 46

Imprest surrendered is struck off form the outstanding balance.

New outstanding imprest balance is obtained.

This new balance is compared with the imprest account balance in the ledger.

Reconciliation is obtained by explaining any outstanding credits in the ledger if any.

Step 2A report Impro 41 that gives the imprest register balance is obtained from Payments section.

A comparison is done between the register balance and the new imprest account balance by

checking out the imprest surrendered but entries not yet posted to the ledger.

Any difference between imprest register balance and the imprest ledger account balance should

be analyzed and explained for farther investigation or action by the payments section.

The ledger and the register are then compared and should balance off.

8.2. Other Debtors

Deposit protection fund account:

Salaries section should reconcile the salaries and emoluments part of this account.

D.P.F ledger account is analysed.

Any items paid by C.B.K on behalf of D.P.F are investigated and a claim is raised to D.P.F. for

a reimbursement.

D.P.F should do a reconciliation, which should be compared with our analysis.

Any discrepancies should be investigated and explained.

8.3. Other accounts

These accounts should be checked through for any mis-postings and any anomalies.

Administrative expenses, which includes:

Directors Expenses

Personnel Emoluments

Medical Benefits Scheme

29

Staff training and development

Debtors: Petty cash accounts

Liabilities:Kenya notes

Kenya Coins

Miscellaneous Suspense

8.4. Monthly Reconciliation

The following is needed:Special statement from the branch for the whole month.

Head office special statement, for the particular month.

Reconciliation statement for the previous month.

Compare the two statements. Key in the outstanding figures into an excel spreadsheet.

The footer has:Prepared by…

Reviewed by…

Document is ready for signing.

A copy of the reconciliation is sent to the Branch Manager with a covering letter.

30

Financial StatementsPreparation of final accounts is the final task of the division. One is required to have the following

reports to perform the task above.

Report 7-Consolidated Trial Balance

Report 2-Balance sheet in summary

Report 5- Consolidated Profit and loss account

Report F-Forex Balances for GL, Financial Markets and Difference for comparison.

Previous month or year reports.

Final accounts consist ofProfit and loss account

Balance sheet

Statement of Changes in Equity

Cash flow Statement

Notes to the Accounts

The above reports are usually prepared once a year

31

Management Accounts For Management purposes the following reports are prepared on monthly basis

Profit and loss account

Balance sheet

Cash flow statement

For one to prepare the above he /she require the following outputs from general ledger system. They

are updated once a month in the system i.e. they are monthly reports.

Report 7-Consolidated Trial Balance

Report 2-Balance sheet in summary

Report 5- Consolidated Profit and loss account

Previous month or year report

The final report is keyed into Excel spread sheet for monthly accounts or Word for end of year accounts.

32

Procedures for Closing the Month/year Procedures for the closure of Month

The following procedures are used to close the month

The Value Date on the system should be the last day of the month

Close the Head Office transactions

Consolidate the Branches

Close the Month

Procedures for Closing/Opening the Financial Year

On the system when the value date=30th June

Users will give an OK for closure to proceed

Update the GL Master File, ACCMAST

Update the Ledger file, ACCLEDG

Take permanent backups for the files in 3. And 4. Above

The administrator will then

Extract the B/F balances to open the new FY

Delete the files from the system

The new FY is now ready for posting

33

Process Flows

General ledger Journal voucher entry process

CBK-GL-PFLW-010

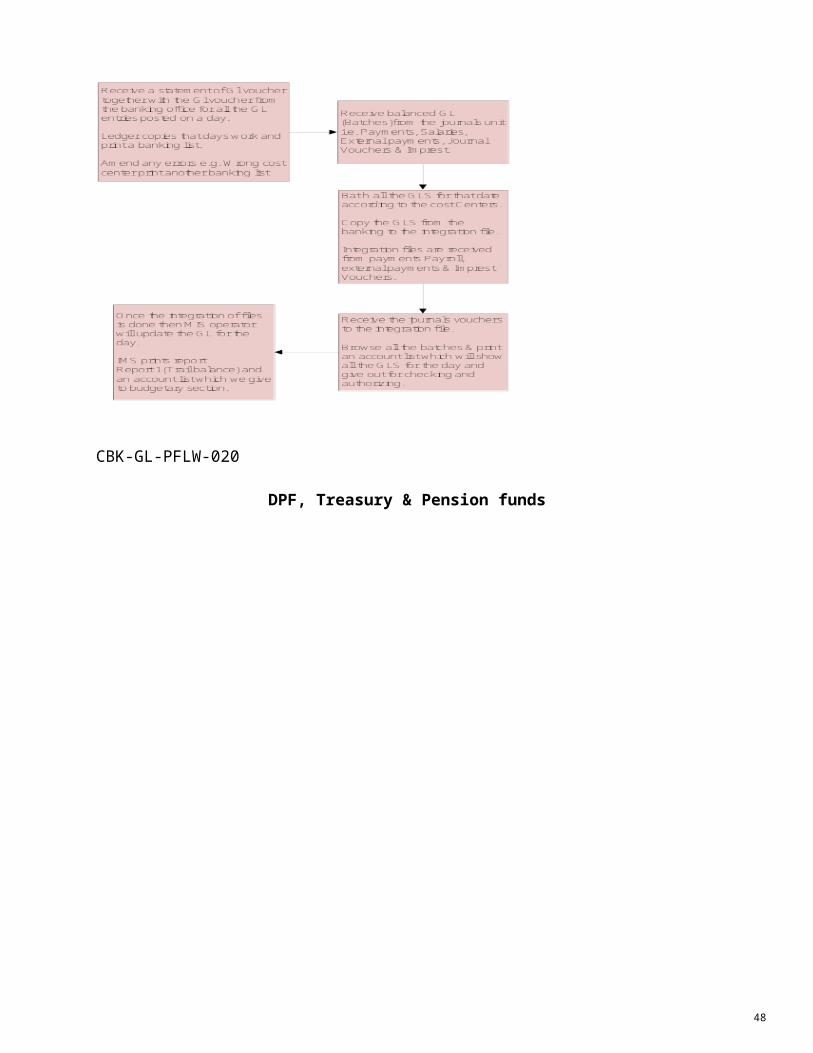

Integration of general Ledger Entries

CBK-GL-PFLW-020

34

DPF, Treasury & Pension funds

CBK-GL-PFLW-030

Payments in Advance

CBK-GL-PFLW-040

Annual Budget Process Flow

35

CBK-GL-PFLW-050

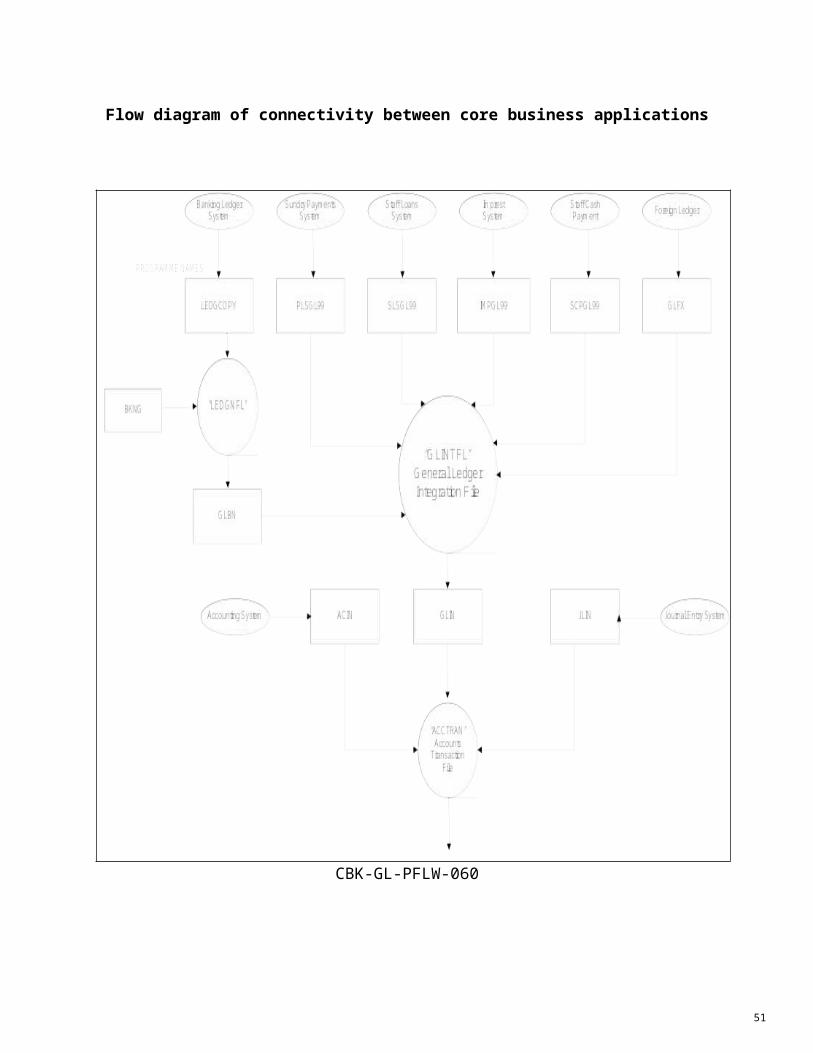

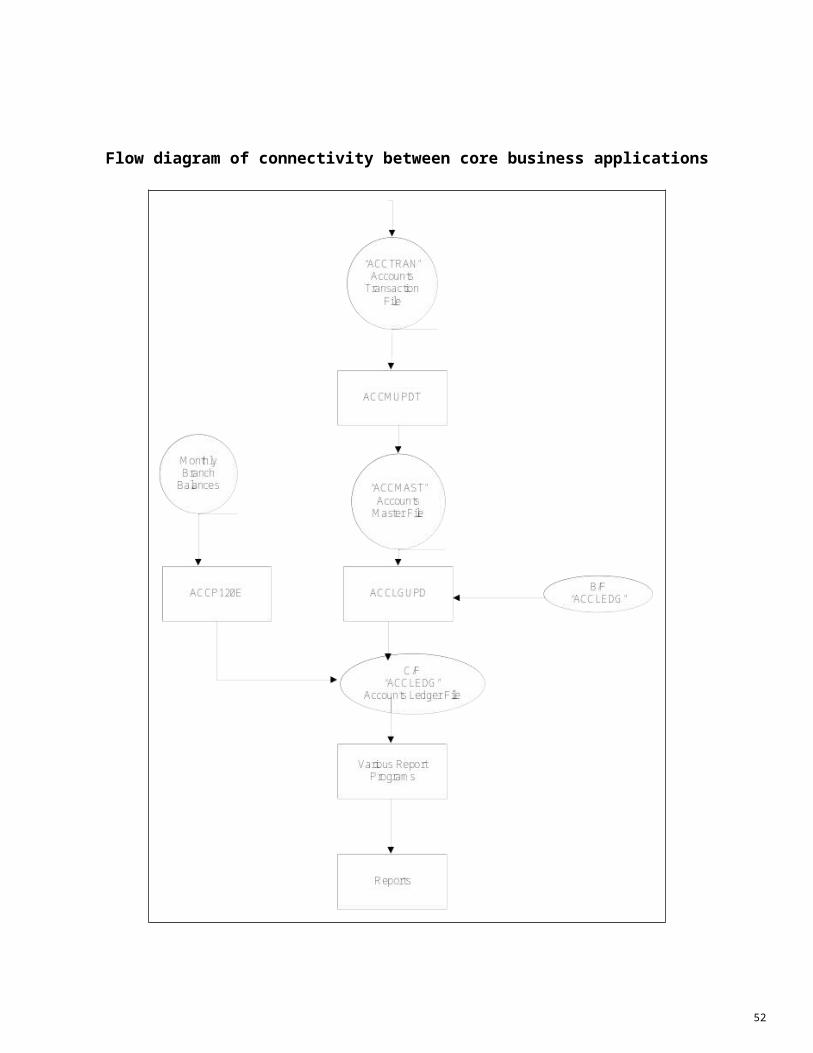

Flow diagram of connectivity between core business applications

36

CBK-GL-PFLW-060

Flow diagram of connectivity between core business applications

37

CBK-GL-PFLW-060

38

GL critical requirements

No Question Answer Revisit

1 General

1.1 About Your Business

1.1.1 What type of industry are you in? Banking Industry. Central Bank

1.1.2 What products and services do you provide?

Currency printing, commercial bank deposit, banker to govt, lend of loss resort, supervision of commercial banks, license forex, micro finance, processing commercial bank licence, make payment on be-half of govt.

1.1.3 Number of employees? 1300

1.1.4 What business areas and/or operations are targeted for improvement?

The current system should be a centralized one and should provide the facility to draw the Financial reports such as TB, P&l, Balance sheets reports

The system should facilitate the user to get the Trail balance report at branch and a consolidated statement.

1.1.5 Which of these business areas and/or operations is high, medium and low priority?

The current system should enable the users to generate financial reports at branch & Dept for decision making purposes.

1.1.6 Can you provide a systems flow diagram of connectivity between your core business applications?

Flow diagram was provided by IT.

PFLW-060

1.1.7 What is your organizational structure? Branch>>Cost centre>>Account

1.1.8 How many businesses are in Your Company?

Banking Industry (Central Bank of Kenya).s

39

No Question Answer Revisit

1.1.9 What is the structure or relationships of these businesses?

Central bank of Kenya is having 4 branches namely :

Nairobi

Kisumu

Eldoret

Mombasa

All branches fall under one roof and share’s the same ledger, same chart of accounts, same functional currency and same accounting method (Encumbrance Accrual accounting method as they follow budgets)

1.1.10 On how many sites are these companies located? What are these sites?

The branches are located at different locations:

Nairobi

Kisumu

Eldoret

Mombasa

1.1.11 Do all the locations have the same chart of accounts?

All branches are using the same chart of accounts and same account values.

1.1.12 Do all the locations have the same calendar?

All the CBK branches are following the same Accounting calendar which starts from July - June.

1.1.13 Do all the locations have the same functional currency?

Kenya Shillings is the functional currency for Central bank of Kenya. This includes branches Kisumu, Mombasa, Eldoret, and Nairobi.

1.1.14 Do you use more than one ledger? Central Bank of Kenya is maintaining single ledger and CBK will follow the same for oracle system.

1.1.15 Do all the businesses have assets? Fixed asset register is centralized. All the assets are booked & registered at Head-office Nairobi.

40

No Question Answer Revisit

1.1.16 Are assets assigned to cost centres? All assets are booked at cost centre level.

1.1.17 What is your accounting calendar? Central bank of Kenya is following Fiscal accounting calendar which starts from July - June.

1.2

1.2.1 Do you have any security policies around access to General Ledger? Is this documented?

Central bank of Kenya requires security controls. The requirements will be provided at the later stage.

2 Financial Management

2.1

2.1.1 What does your current chart of accounts look like?

Current Chart of Accounts of Central Bank of Kenya has categorized into three different segments called

Branch Code/Cost centre/Natural Account.

The three segments are made mandatory while capturing the transactions in books.

2.1.2 Do you plan to have a new chart of accounts?

Central Bank of Kenya wants to create a new chart of accounts to cater all the business reporting needs.

2.1.3 Are your account values in any order or range pattern?

The account values are followed by order with range pattern.

1. Assets

2. Liabilities

3.Equity/ownership accounts

4. Revenues

41

No Question Answer Revisit

5. Expenses

6. Inventory items.

2.1.4 What are the account parent or grandparent structures?

Central Bank of Kenya follows the Account value hierarchies.

Ex: Total Assets ( Great Grand Parent)

Local assets(Grand Assets)

Fixed assets (Parent)

Furniture account (Child)

Central Bank of Kenya captures the transaction at child level.

2.1.5 Do you use unique accounts to capture statistics?

Central Bank of Kenya wants to use Mass allocation option to distribute the expenses of Rent, electricity bills, water,

2.1.6 Who is going to maintain the segment values once entered?

It will be handled by Manager financial accounts, assistant director of finance, MIS.

2.1.7 Is there a need for a mapping from an old COA to a new COA?

One to one.

2.2 Consolidation

2.2.1 Do you require financial consolidations?

Central Bank of Kenya is going to maintain single ledger, so the question of consolidating books will not arise.

2.2.2 How often do you perform financial consolidations?

Not required

42

No Question Answer Revisit

2.2.3 What is the COA mapping during the consolidation?

Central Bank of Kenya is going to maintain single ledger, so the question of consolidating books and mapping will not arise.

2.2.4 Do you perform consolidation between various businesses that use different currencies?

Central Bank of Kenya is going to maintain single ledger, so the question of consolidating books will not arise.

2.3 Currency

2.3.1 Do you use multiple currencies in your business?

Central Bank of Kenya uses multiple foreign currencies to perform the day-to-day business transactions.

2.3.2 How many currencies do you use and what are they?

J.T. Bett has provided the data.

2.3.3 What is your policy on changing currency rates?

Follows the Exchange rates provided by Treasury Dept.

2.3.4 What is the primary currency you have?

Kenya Shillings is the primary and functional currency for Central Bank of Kenya.

2.4

2.4.1 Does Your Company prepare budgets? Yes.

2.4.2 What types of budgets do you prepare? (For example, revenue & expenses, balance sheets, capital, project, and so on). Do you do any budget allocations?

Central Bank of Kenya prepares revenue, expenditure and capital budgets once in a year.

The budget allocations are done at cost centre and votes (natural

43

No Question Answer Revisit

accounts level).

2.4.3 Do Your Company’s key performance indicators drive the budgets?

Budgets are one of the key performance indicators for dept and cost centre.

2.4.4 How many budgets do you prepare for an individual fiscal year?

Central Bank of Kenya Prepares only one budget for each financial year.

2.4.5 Do you prepare more than one budget per Ledger?

Central Bank of Kenya is going to maintain single ledger and budget will be only one for the entire financial year.

2.4.6 What is the range of accounting periods for each budget?

Though the Budget is projected for annual, vote’s amount are equally distributed for 12months.

In-case of non-utilization of funds, the funds will be carry forward to the next month.

2.4.7 At what organization level (for example, cost centre, division, or region) do you budget?

CBK>>Branches>>Cost centre>>Natural account (Vote)

2.4.8 Do budgets require approval? What levels of approvals are required?

The Budget for the financial year will be approved at three levels before it is captured into system

Senior management>>Audit committee>>Final board.

The approval of budget process explained in fig.

GL-PFLW-050

2.4.9 How many budget "organizations" do you have (Budget Organization is an entity, which “owns” the budget in Oracle General Ledger)?

Central Bank of Kenya has only one budget organization, and it is owned by the bank.

2.4.10 What are the budget organizations and what is the convention or rule behind their names?

The Budget Organization Name will be Central Bank of Kenya

44

No Question Answer Revisit

Central Bank of Kenya follows year as the naming convention.

Example: Annual budget for the Financial year 2010/201.

2.4.11 Have you developed security procedures to prohibit access to certain budget organizations?

The security is already in place. There is a requirement of security for budgets. Only authorised persons like Head of budgets and deputy budget person should access the budgets.

In-case of any fund transfers from one vote to another vote within the same category it should be sent to finance director for an approval.

Upon the finance director approval, Head of budgets will transfer the funds from one vote to another vote within the same category.

2.4.12 Will budget organization security be required in the future?

Central bank of Kenya wants to deploy certain security options in oracle system so that other users should not modify or transfer the funds.

2.4.13 Do you create new budgets based on existing budgets (for example, new budget = 10% decrease from previous budget)?

Central Bank of Kenya follows Zero based budgets at the beginning of each financial year.

2.4.14 At what natural account level do you currently budget? Is this the same level of detail as actual are captured?

Yes. Central Bank of Kenya uses the same accounts for both budget projection and transactions.

2.4.15 Is your budgeting process centralized or decentralized?

The preparation of budgets is centralized; once the budget sheet is prepared it will be dispatched to each branch to

45

No Question Answer Revisit

come-up their budget requirements for submission.

2.4.16 Are reorganizations likely to affect how budgets should be prepared and/or reported?

If any new cost centre comes, they domicile with the existing cost centres.

2.4.17 Do you only budget in Kenya Shillings, or are statistics budgeted also (for example, headcount)?

Only in Kenya shillings.

2.4.18 Do you require consolidated budgets (budgeting across sets of books)?

Yes

2.4.19 Are all budgets prepared in the same currency?

Yes. All budgets are prepared in Kenya shillings.

2.4.20 Do you use Lotus, Excel, or another spreadsheet program to prepare budgets?

Visual Basic

2.4.21 Which spreadsheet products and which version do/will you use?

Visual basic 6.0 & 2003 excel

2.4.22 How do you close or "freeze" a budget once it is approved?

Once it is approved by final board it will be freeze.

2.5

2.5.1 Do you derive any type of forecast from budgets?

Yes. Require future forecast

2.5.2 Does Your Company prepare financial forecasts? What types of financial forecasts does Your Company prepare?

Central Bank of Kenya won’t do any financial forecasting in projection of budgets.

2.5.3 Is the financial forecasting process documented?

NO

2.6 Maintenance

46

No Question Answer Revisit

2.6.1 How do you maintain your General Ledger data?

Proper security measures need to deploy to control the reporting of general ledger data.

2.6.2 How do you audit your General Ledger data?

The general ledger data will be audited based on the source and unique journal batch numbering.

3

3.1

3.1.1 Do you track journal sources? What types?

Yes, central Bank of Kenya follows the journal source in current system; origin of journal was identified based on the journal source.

3.1.2 Do you track journal categories? What ones?

In current system though they don’t have the journal categories, they want to follow the journal category in oracle system.

3.1.3 Do you enter statistical accounts regularly? How often?

In current system they don’t follow allocation or distribution of costs. But going forward the want to distribute the expense On a monthly basis.

3.1.4 Do you use batches to enter journals? Yes.

3.1.5 Do you reverse journals on a regular basis? Explain.

Error journals, budget issues (if any funds are insufficient, they transfer funds from one cost centre to another & will finally reverse the budget journals.)

Accrual reversals

3.1.6 Do you have standard journals that recur with the same accounting information (but changing amounts)?

Water, electricity, Rent, telephone bills.

47

No Question Answer Revisit

Provide examples.

3.1.7 Do you use control totals when entering journals?

Yes. But will provide the figures at later stage.

3.1.8 How often do you post journals to your General Ledger balances?

As and when they are required.

3.1.9 What are the procedures you use to post these journals?

Central bank follow the below hierarchy position in posting the journals in system :Entry maker.CheckerApproval oneApprover two

3.1.10 Who posts the journal batches? Who approves the posting?

Requires journal approvals for manual Jv’s

Approval flow and limitations will be provided later.

3.1.11 Do you allow for posting out of balance journals into a suspense account?

No.

3.1.12 Do you import journals from spreadsheets

Yes.

3.1.13 Do you have any audit requirements that might be unique?

Source of Journal, date & time of creation, created by, updated by, approved by,

4 Period Processing

4.1 Periods

4.1.1 When is the beginning of your year? 1st working day of July

4.1.2 What is the period type? How many periods in your year?

13 periods per year, 13th period is for adjustment. CBK follows fiscal year.

48

No Question Answer Revisit

4.1.3 Do all the companies have the same calendar? Explain.

One Calendar as all the branches same COA, Calendar, Currency & ledger.

4.1.4 Do you have a naming convention for the periods?

The naming convention will be as follows:

The prefix will be the month name and suffix will be year Num.

Jan-10, Feb-10.

4.1.5 What accounting periods are in your quarters?

3 months.

4.2 Period Close

4.2.1 What is your period-end reconciliation process?

It is a monthly basis, if corrections are needed means will pass the manual journals entries to balance the figures. The recon will be done with the sub-ledgers to agree the totals.

4.2.2 When closing at year end do you use a 13th period?

Yes, to record the adjustments.

4.2.3 How do you close an accounting period?

Currently Each branch closes the month by posting all the transactions and reconciles them. Once the month end reconciliation is done branches send the Tb to head office.Central bank will consolidate the branches and head office TB to generate the overall bank TB.

4.2.4 Is the schedule to close an accounting period documented?

They have a process flow manual. But they will not do any documentation for closing the period.

49

No Question Answer Revisit

4.2.5 How long does it take to close an accounting period?

Closes by same day or the following day. Subject to the closure of sub-ledger modules periods.

4.2.6 How are adjustments to closed periods handled?

Central bank of Kenya wants to maintain the closed period status, upon completion of audit and adjustment entries CBK will perform the permanent close at year end.

4.2.7 Who performs the tasks associated with closing an accounting period?

The super user will own the responsibility of closing an accounting period.

4.2.8 Where in your accounting cycle do you run standard reports and statements?

TB on daily basis.Year end the consolidated TB.Each branch should be able to run their TB.

4.2.9 Do sub-ledgers have their own calendar?

No.

4.3 Period Open

4.3.1 How do you open an accounting period?

On 1st day of every month. In the current system the period open is done by IT.

4.3.2 Is the schedule to open an accounting period documented?

An operation manual was in place for closing a period. The information was capture in the page Number 32 of AS-IS document.

4.3.3 How long does it take to open an accounting period?

Opens on the 1st day of every month.

4.3.4 Who performs the tasks associated with opening an accounting period?

Currently the period opening and closing are done at IT dept, going forward it will be handled

50

No Question Answer Revisit

by GL super user.

5 Reporting

5.1 Financial Reporting

5.1.1 Describe your Financial Reporting. Management reporting and financial reporting,

Management reporting :

Management involves preparing budget and explaining the variance by month and by year.

Financial reporting :

Prepare the financial reporting such as TB, consolidated TB, P& L, balance sheet, cash flows.

5.1.2 Provide samples of your standard financial reports - Balance Sheet, Cash Flow Statement, Income/Operating Statement, Trial Balance, etc

Report templates are provided by finance Super user.

5.1.3 How long are reports kept on-line or are they re-run if needed again?

The data for the current year will be online. If the users can generate the financials reports. For all previous year the User need to raise a request to IT to place the previous tape data into system.

5.1.4 Do you have online account balance lookup? If needed, which accounts and how often?

Required. Will provide t he account details at later stage.

5.1.5 Please enclose a list of all reports used in the General Ledger area. Please annotate the report list with each report's name/number, description, the type of users, frequency on which these reports are generated.

GL voucher. Duly authorized Summary of source office ( it will give the details of entries that are captured during the day by each user)TB head office and branch wise.

51

No Question Answer Revisit

Will run on daily basis.Bank wise TB will be run on a month basisLedger statements.Require the TB on a daily basis on oracle

6 Miscellaneous

6.1 What else needs to be discussed?

6.1.1 How do you handle taxes? Answered in payables

52

9. Open and Closed Issues for this Deliverable

Open Issues

ID Issue Resolution Responsibility Target Date Impact Date

Closed Issues

ID Issue Resolution Responsibility Target Date Impact Date

53

Related Documents

![REPUBLIC OF GHANA THE COMPOSITE BUDGET OF THE …€¦ · DORMAA CENTRAL MUNICIPAL ASSEMBLY FOR THE 2015 FISCAL YEAR [DCMA BUDGET 2015] ... Composite budgets which integrated budgets](https://static.cupdf.com/doc/110x72/5f8a34cf6a73f4703d570074/republic-of-ghana-the-composite-budget-of-the-dormaa-central-municipal-assembly.jpg)