CHAPTER-1 1

Cash Flow Final Print

Oct 22, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER-1

1

INTRODUCTION OF THE STUDY

Introduction To Financial Management

Financial management is the Managerial activity which is concerned with

planning and controlling of the firm’s financial resources. Through it was a branch of

economics till 1890, as a separate activity or discipline it is of recent Origin. Still, it

has no unique body of knowledge of its own, and draws heavily on economics for its

Historical concepts today.

The subject of financial management is of immense interest to both

academicians and Practicing Managers. It is of great interest to academicians because

the Subject is still developing, and there are still certain areas where controversies

exist for which no unanimous solutions have been reached as yet. Practicing Managers

are interested in this subject because among the most crucial decisions of the firm are

those which related to the finance, and an understanding of the theory of financial

management provides them with conceptual and analytical insights to make those

decisions skillfully.

FINANCE FUNCTIONS:

Although, it may be difficult to separate the finance functions from production,

marketing and other functions, yet the functions themselves can be readily identified.

The functions of raising funds, investing them in assets and distributing returns earned

from assets to share holders are respectively known as financing, investment and

dividend decisions. While performing these functions, a firm attempts to balance cash

inflows and outflows. This is called liquidity and we may add it to the list of important

finance decisions or functions.

Finance functions or decisions include:

Investment or long-term assets-mix Decision.

Financing or capital mix decisions.

2

Dividend or profit allocation decision.

Liquidity or short-term asset-mix decision.

A firm performs finance functions simultaneously and continuously in the

normal course of the business. They do not necessarily occur in a sequence.

Finance functions call for skilful planning, control and execution of a firm’s

activities.

INVESTMENT DECISION:

Investment decision or capital budgeting involves the decision of allocation

of capital or commitment of funds to long-term assets that would yield benefits in

future. Two important assets of investment decision are:

a) The evaluation of prospective return on new investments and

b) The measurement of a cut-off rate against the prospective (profitability)

return of new investments should be compared.

These investment decisions involves risk. So the financial Managers evaluate

the investment proposals in terms of both return and risk.

FINANCING DECISION:

Financing decision is the second important function to be performed by the

financial manager. Broadly, he or she must decide when, where and how to acquire

funds to meet the firm’s investment needs. The central issue before him or her is to

determine the proportion of equity and debt. The mix of debt-equity is known as

firm’s capital structure. The financial manager must strive to obtain the best financing

mix or the optimum capital structure for his or her firm. Once the manager is able to

determine the best combination of debt and equity, he or she must raise the

appropriate amount through the best available sources.

3

DIVIDEND DECISION:

Dividend decision is the major financial decision. The financial manager must

decide whether the firm should distribute all profits, or retain them, or distribute a

portion, and retain the balance. The dividend policy should be determined in terms of

its impact on the shareholder’s value. The optimum dividend policy is one that

maximizes the market value of firm’s share. If the shareholders are not different to the

firm’s dividend policy, the financial manager must determine the optimum dividend-

pay-out ratio. The pay out ratio is equal to the percentage of dividends to earnings

available to share holders. The financial manager should also consider the questions of

dividend stability, bonus shares and cash dividend in practice.

LIQUIDITY DECISION:

Current assets management that affects a firm’s liquidity is yet another

important finance function, in addition to the management of long-term assets.

Current assets should be managed efficiently for safeguarding the firm against the

dangers of illiquidity and solvency. If the firm does not invest sufficient funds in

current assets, it may become illiquid. But it would lose profitability, as idle current

assets would not earn anything. In order to ensure that neither insufficient nor

unnecessary funds are invested in current assets, the financial manager should develop

sound techniques of managing current assets. He or she should estimate firm’s needs

for current assets and make sure that funds would be made available when needed. So

we may conclude that these finance functions may affect the size, growth, profitability

and risk of the firm, ultimately the value of the firm.

4

Need for the study

Cash flow statement analysis is the study of the cycle of business’ cash inflows and

outflows, with the purpose to know how a firm maintaining an adequate cash flow in

their business, and to provide the basis for cash flow management.

The cash flow statement was previously known as the statement of changes in

financial position or flow of funds statement. The cash flow statement reflects a

firm's liquidity or solvency.

The balance sheet is a snapshot of a firm's financial resources and obligations at a

single point in time, and the income statement summarizes a firm's financial

transactions over an interval of time. These two financial statements reflect the accrual

basis accounting used by firms to match revenues with the expenses associated with

generating those revenues. The cash flow statement includes only inflows and

outflows of cash and cash equivalents; it excludes transactions that do not directly

affect cash receipts and payments. These noncash transactions include depreciation or

write-offs on bad debts to name a few. The cash flow statement is a cash basis report

on three types of financial activities: operating activities, investing activities, and

financing activities. Noncash activities are usually reported in footnotes.

The cash flow statement is intended to

1. Provide information on a firm's liquidity and solvency and its ability to change

cash flows in future circumstances

2. Provide additional information for evaluating changes in assets, liabilities and

equity

3. Improve the comparability of different firms' operating performance by

eliminating the effects of different accounting methods

4. Indicate the amount, timing and probability of future cash flows

5

The cash flow statement has been adopted as a standard financial statement

because it eliminates allocations, which might be derived from different accounting

methods, such as various timeframes for depreciating fixed assets. Cash flow analysis

involves examining the components of the business that affect cash flow, such as

accounts receivable, inventory, accounts payable, and credit terms. By performing a

cash flow analysis on these separate components, you'll be able to more easily identify

cash flow problems and find ways to improve your cash flow.

OBJECTIVES OF THE STUDY

6

Objectives of the study:

The main objective of the study is to study the overall financial position of the

company from 2006-2011.

To study the financial performance of the company.

To study the sources and applications to the cash.

To offer suggestions for improvement in the relevant aspects.

To find out the financial stability of the firm.

To know how effectively the company is using its financial resources.

To measure the extent to which the company has been financing its needs

through borrowing.

To study about the profile of the oil industry and the FOODS,FATS AND

FERTILISERS Ltd. Company profile.

To make an overall view on theoretical approach of cash flow statements.

SCOPE OF THE STUDY

The study has been conducted to understand the position of the industry and

various functional areas of the company and their operations. The study mainly

focuses on Funds flow analysis of the company.

7

Methodology:

The data used for preparing this report is through 2 sources.

1. Primary data.

2.Secondary data.

Primary data:

Primary data was collected on the basis of personal observations discussions

and through interviews.

Secondary data:

Secondary data has been collected by referring to various annualreports and

records / documents of the company.

a)Annual Reports:

These are one of the important sources of information in collecting secondary

data. By referring the previous annual reports, the financial position of the company

and its requirement of funds for ratio analysis has been arrived.

b) Records & Documents:

These consists of

1.Balance sheet

2.Profit / Loss account.

8

Limitations of the study:

The time given to complete this project is very limited,

The study is based on accounting information.

The analysis is made from the information given by the organization.

The study was conducted with limited data available and analysis was done

accordingly.

The complexity and confidentiality of various operations is also a limitation to

this study.

9

CHAPTER-2

10

INDUSTRY PROFILE

INTRODUCTION TO EDIBLE OIL INDUSTRY

In the Indian context, the term ‘Vegetable Oils’ is almost synonymous with

‘Edible Oils’ and land is not used as cooking media. However it is important to keep

this distinction in mind not all Vegetable Oils are Edible - Some including castor oil

are mostly non-edible and some of the edible oils like Ground Nut and Coconut are

finding increasing industrial applications as in cosmetic, soap making etc.

By virtue if they’re high nutritive content, Edible oils from a major source of

nutrition. The fatty acids in Edible Oils are required by the body as a vehicle for

carrying vitamins, provide oil cakes, which are by-product of the oil extraction

process, are important source of animal nutrition. These can be processed in to Edible

flavors, which are rich in proteins.

Oil seeds occupy an important position as the agriculture map pf and rank

second after food grains as a farm commodity crop. India accounts for a tenth of the

world out put of Vegetable Oils and fats. It is the largest produces of Ground Nut,

rapeseed, mustard and sesame, second in respect of castor seeds, third in coconut,

fourth in cotton seed and fifth in line seed.

Our country has a highly developed oil based industry. Providing gainful

employment to nearly 15 million persons besides another half a million engaged in

milling and processing units. It is essential a food-oil industry accounting for four

fifths of the total supply of Vegetable Oils. Soap paints and varnish industries from

the bulk of non-food applications.

In spite of their national importance, production of food grains has been

suffering a negative growth rate all these years. Only during the first plan period, the

Targets set for production were realized after this no impressive achievement was

recorded. The main contributory factors are two fold, first only marginal land, in rain

fed areas is being used for their cultivation resulting inevitable in low productivity,

second agriculture in India is still subject to the vagaries of monsoon which makes for 11

erratic production. It is little wonder therefore that the annual rate; of growth of oil-

seed production for the decade 1965-1976 was a mere 1.2 percent while that of oil

seed productivity, an equally dismal one percent.

Viewed in the global context, India has the dubious distinction of having the

highest acreage under oil seeds and recording the highest output, and yet showing the

lowest yield, at 736 kg. India’s yield per hectare is lower than that of Nigeria (1615.38

Kg) U.S.A. (91474.58 Kg), Argentina (1153.49 Kg.) and China (1148.55 kg.) The

following table would give picture of Indian’s placing in the world settings.

For the year 1980-81, target for oil-seed production had been fixed at 11

million tones, actual production however lagged behind, with; provisional estimates

Placed at 10.2 million tones. Production of live major oil seeds viz./ groundnut,

rare seed mustard, sesame, line seed and castor seed and is estimated to be around 90

lakes tones, which is about 13 percent higher than the previous year’s production.

Production estimates of groundnut at 57 lake tones however show decline of 70,000

tones. At 2 lack tones castor seed production has also registered a decrease of 30,000

tones. Rapeseed, sesame and line seed have however, registered increase over the

previous year’s production levels.

The central Government therefore took various measures to increase

production of oil seeds. A centrally sponsored scheme for an intensive oil seed

development programmed was operated in 14 states with a coverage target 40.6 lakes

hectors under a liberalized pattern of central, assistance. However actual coverage was

only 36 lake hectares and the short fall was attributed to serve

Brought conditions in several states during the kharrif season.

Short falls in production persisted in the oil year 1981-82 as well. As a result,

domestic industry could not meet the consumption needs respect of edible oils. The

total edible and supplies from indigenous sources were estimated at about 30 lake

tones in 1981-82 (which however higher than the previous year’s levels of 25 lakes

tones). The gap of 10 lake tones had to be filled only through imports. Consequently, 12

the state-trading corporation was asked to import a million tones of Edible Oils during

the oil year 1981-82. The allotment of imported Edible Oils was also pruned in a bid

to ensure more supplies through fair price shops.

The trend of imports in expected to continue in the year to come despite the

best efforts of the union agriculture ministry to raise oil seed output. The genera-based

international trade center has projected import f 13 million tones of Vegetable Oils in

1985. As for exports, it is anticipated that India would export 15 Lake Tones of oil

equivalent of hand picked-selected groundnut, other nuts and castor oil by 1985.

PROFILE OF THE OIL INDUSTRY:

The power and strength of the company depends on how strong and secure it is

on the food front. In trying to achieve this goal, the oil seed scenario in the country

has undergone a substantial charge during the post few years. The country is moving

away from a situation of scarcity and huge import bills to one of self-sufficiency and

possibly even export of vegetable oils.

India ranks high among the oil seeds producing countries in the world with

perhaps the larges number of commercial varieties of oil seeds such as ground not,

rape and mustard, sesame, kardi seed, nigerseed, soya beans, sunflower seeds, linseed,

castor seed, copra, cotton seed and a number of minor seeds of tree origin oil seeds

takes their place, as the second largest agricultural crop, next only to food grains. The

cultivation of oil seeds in India is spread over various states with a distinct regional

pattern covering about 19 to 20 million hectares, which accounts for about 11 percent

of the total land under cultivation in the country.

In India where fats of animal origin such as fish oil are seldom used as cooking

media. The term “vegetable oils” is used as a synonym for “edible oils”. However it

needs to be recommended that there are, on the one hand vegetables oils such as

castor, groundnut and coconut oils, which are finding increasing. Industrial

applications such as in cosmetics, soap making etc… edible oils are a major source of

13

nutrition for the people in the country. Oil cakes that are by-products of the oil

extraction process are an important source of animal nutrition. They can also be

processed in to protein rich edible.

India has a highly developed oil based industry employing more than 15millon

persons. However it remains essentially food oil. Industry accounting for a much as

83% of the total supply of vegetable oil in the country. The major non-food users of

oil are soap, paint and vanish industries. Faced with major demand for their

conventional products, FMCG majors have been planning their hopes on branded

staple foods to deliver rapid top line extension. Negative growth in the oils and fats

business has been instruments in restraining top line growth for the FMCG.

PRODUCTS:

Broadly edible oil or fat products can be categorized as fallows.

a. Vegetable refined oil

b. Hydrogenated oil

c. Bakery fats

Expelled ground oil of good quality can be directly consumed. It can also be refined to

have higher purity other oils such as soya has to be refined to make them edible.

Vanaspathi is obtained by hydrogenation of edible oil. It is used as a suitable

for ghee by some segments of sources and also for making sweets, snacks including

biscuits, cakes etc…

CONSUMER AWARENESS AND PENETRATION:

Among FMCG products, edible oils has one of the highest penetration of 98%

in urban as well as in rural areas penetration of all these 3 cooking medium is very

high at 99.8% in urban areas as well as rural areas.

14

Vanaspathi penetration averages 17.4% at all India level, significantly higher at 28.8%

in urban areas and 13% in rural areas. It is highest in medium size towns of 0.5-1mm

population of 34.3% in metros and towns.

In metros refined edible oil is a relatively popular cooking medium. The per

capita vegetables oil consumption in the country was 7.6kg p.a in 1997-98,

significantly lower than 8.5 kg p.a during 1996-97.

CONSUMER HABITS AND PRACTICES:

Edible oil is one form or other is consumed is almost every household, and

Indian food habits show a strong preference for fried vegetables and several other

fixed snacks.

Traditionally the north and west have been milk surplus regions in the country.

This has led to surplus ghee production in these areas and higher ghee consumption.

The lower ends of the society which can not afford ghee consume vanaspathi.

Sweet meat makers in the unorganized sector, particularly in the north

represent one of the largest user segments for vanaspathi.

In the south there has been abundant availability of edible oils, namely coconut

oil, ground nut oil, sunflower oil etc. This had led to different consumer habits

southern consumer prefer refined oil cooking medium as compared to ghee or

vanaspathi. Similarly the eastern region, which is milk deficient, has preference for

vegetable oil as cooking medium.

There are also regional and cultural differences in the type of edible oil used for

cooking. For instance kerala uses more of coconut oil for cooking. Sesame oil is

widely used in the north, mustard oil in the north and east while there is an over

whelming preference for groundnut oil is in the west.

Most consumers, especially in the rural areas buy edible oil in loose form.

Where as in large metros loose oil is scarcely available as retailers find it difficult to

handle the same. In medium sized towns, loose as well as branded oil is available.15

In the last few years popularity of branded oil has been increasing particularly

with the introduction of low cost poly packs with the government ordering

compulsory packaging of edible oil in the wake of dropsy deaths in the country due to

use of adulterated mustard oil, the wage of branded oils is expected to witness

phenomenal growth.

India accounts for 9.3% of world oil seed production. It has the world’s fourth

largest edible oil economy. In 1999, India ranked as the world’s largest importer of

edible oils, displacing china. The bulk of edible oil, India imports under the open

general license is RBD palmolein of Malaysian and Indonesian origin.

India is one of the worlds leading producer of oil seeds and oil, contributing to

9.3% world oil seed production. It produces the largest number of commercial

varieties of oil seeds over nearly 28.4 million hectares of land. The major edible oils

produced in India are ground nut, rapeseed, soya, cottonseed, sesame seed, castor

seed, sunflower seed, etc. Groundnut was the most widely consumed and traded edible

oil determining edible oil economics, but is now being displaced by others. India is the

world’s second largest production of groundnut, next only to china. The govt. has set

up a technology mission on oil seeds, to increase production of other oil seeds and oil

and to reduce dependence on imports. The strategy followed was to

Increase productivity with better inputs and practices

Increase area under oil seed crop

This led to a sharp increase in oil seed production driven mainly by rapeseed,

sunflower, castor seed and soya. India is today the world’s third largest producer of

rapeseed and cottonseed and the largest producer of caster seed. India has

approximately 300 edible oil refining units, 60-70% of which are in the small scale

unlike the bigger refiners, the smaller one are unable to important huge quantities of

crude either low capacity or lack of financial resources, and may be forced to close

down or sell out to the bigger ones in the fore cable future.

16

Another major problem is the low capacity utilization. The installed capacity of

oil mills is around 36 million tones annually, but capacity utilization is only 40%

solvent extraction plants shows only 33% capacity utilization of vegetable oil

refineries 40% utilization.

The import of refined palm oil was put under OGC (Open general license) in

March 1994. Other edible oils were put under OGC in April 1995 when an item is

brought under OGC, it means that the item can be imported without seeking any

approval.Originally there was no discrimination between refined and non-refined

edible oil as far as import duty was concerned. The duty on both was 65% duty was

then slashed to 30% for both then to 20% in 1996 and 15 % in the 1999-2000 budgets.

In most parts of the world, import duty on the oil seeds is lower than that on

oils. But in India, it is higher 40%. That is why no import of oil seeds (or) oil-bearing

material has taken place in India. The industry wants the duty to be lowered from the

present 40% to 50%.

Edible oil prices in the Indian market have crashed owe to large imports by

multinational trading houses. The edible oil industry is one sector in India that will see

considerable reform in the foreseeable future.

Major players in refined edible oils in the organizational sector are the ITC

Agrotech, Marico Industries, Ahmed mills, Godrej foods. HLL and NDDB. The

market is highly fragmented among various brands. Sundrop refined Sunflower oil

brand with around 13l market share/ ITC Agrotechs other edible oil brands include

Real Gold mustard oil, Crystal refined oil and Sudan unrefined mustard oil. Sweekar

sunflower oil marketed by marica has an 8.2% share and saffola has 7.5% market

share other leading edible oil brands include NDDB’s Dhara rape seed oil. Godrej

foods (Godrej cooklite sunflower) with 11% market share, HLL’s flora with 2.5%

market share (6% in sunflower oil segment) and Postman with around 8% market

share.

17

The vanaspathi HLL’s Dalda is the oldest and largest brand with close to 36%

market share. Its brand extension Dalda manpasand was launched in 1996. In Feb 98,

HLL launched another brand variant dalda feel light. Other major vanaspathi

manufacturers are Wipro, Amrit Vanaspathi, IVP, Madhusudan industries Rasui and

Pioneer Agro.

IMPORT OF EDIBLE OILS:

It has not been done away completely, but whenever import is now made is

largely a measure of precaution than out of any composition from 1988-89. The edible

oils import has been drastically cut down/ In 1996-97, import totaled 3 lakh tones

valued at Rs 250 crores during the next 2 years it is expected around the same level.

The present import is significant compared to the napping to 19.45 lakh tones

imported value at Rs 969 crore in 1997-98.

India has signed a memorandum of understanding with Malaysia for an annual

import of two lakh tones of palm oil for two years. Besides the country is to receive

50,000 tones of soya been oil from the U.S. as a gift for meeting social objectives.

Although in the context of exceptionally large oil seeds production during the current

year, there is hardly and need for import, the country may avail the option to import

for building a buffer stock to meet the needs of public distribution system during the

lean period.

EXPORT

Export of oil mill, oil seed and minor oils and are expected to gather

momentum following the enouncement regarding the full float of rupee on the trade

account, according to the sources in the trade. The present export scenario shows that

the trade is in a beyond mood of achieving a formidable target, with increased export

earning in the current year. This basically enacts from bumper oil seeds output of 215

lakh tones in the offing. This expectation of a bumper crop, moreover has compelled

the union ministry of commerce to raise the current years export target for the oil

seeds from Rs 1250 crore over Rs 1300 crore.

18

According to the estimates made by the central coordination committee, the

exports of oil mills, oil seeds and minor oils during the current year would be more

than 3.3 lakh tones with a value of Rs 1362 crore as against 30 lakhs tones with the

value of Rs 1043 crore achieved during the year 1996-97 the export of oil meals, oil

seeds and minor oil during the period April 1996 to Jan 1998 stood at over 24 lakhs

tones valued at more than Rs 1000 crores.

CUSTOMER SATISFACTION:

Satisfaction is a persons feeling of pleasure (or) disappointment resulting from

comparing a products perceived performance in relation to his (or) her expectation.

As this definition makes clear satisfaction is a junction of perceived

performance and expectations. If the performance falls short of expectation, the

customer is dissatisfied. If the performance matches the expectations, the customer is

satisfied or delighted.

Many companies are aiming for high satisfaction because customers who are just

satisfied still find it easy to.

When a better offer comes along those who are highly satisfied are much less

ready to switch. High satisfaction (or) delight creates an emotional affinity with the

brand, not just a rational preference. The request is high customer loyalty.

19

PROFILE OF THE ORGANIZATION

Foods Fats and Fertilizers Limited

Foods Fats and Fertilizers limited Tadepalligudem is a family owned

organization. It is well known as Foods&Fats but the West Godavari farmers call it as

a tawdu factory. This organization is professionally carrying the business activity by

“Goenka”family. The company was established in the year 1962. It is having branches

in Chennai, Mumbai, Kakinada, Hyderabad, kolkata and Baroda.

Historical background of Foods Fats and Fertilizers Limited were

conceived in 1959 born in 1960 and were on its beet by 1962. Today Foods Fats and

Fertilizers LTD has matured into a conglomerate of its industrial units spread over 40

acres contently buzzing with activity and providing employment to over 800 persons.

The wheel of fortune has turned a full circle for Mr.B.K.Goeanka the

architect of FFF LTD, born and bred in Burma. The Goenka family established and

respected in Industry and Trade. The rice bran from Mr.Goenka’s mill was avidly

sought as a mal feed and wrapping papers used for sampling could this oil extracted.

These questions have to wait because in 1942, the Japanese invaded Burma and Mr.

Goenka has to abandon his business and return to India.

Being an optimist is transformed the adversity into opportunity by his grit and after a

brief spell in his native land in Rajasthan, his restless enterprising zeal brought

Mr.Goenka to Chennai in 1943. Where he is with his brother export of handloom

fabrics in due course, he established a textile business. In 1959, Mr. Goenka read on

article by Dr.Raghunath Prasad of central food technological institution of Mysore

that oil could be extracted from bran using alcohol as a catalyst.

Simultaneously his brother in Rangoon informed him of plans being

setup with Japanese and German technologists for extracting oil from rice bran Mr.

Goenka held deliberation with Dr Raghunathprasad and visited Burma with him to

study the relevant technology better, he was not fully satisfied and asked his brother

20

Mr. G.G.Goenka who was in Japan to study in Europe to study the process of Hurgi of

Germany and Dr smith of Belgium.

LOCATON:

The Company is a conglomerate of various industrial units spread over 40 acres of

land, with a built up area of aprx. 4 lack sft . located in the vicinity of Tadepalligudem

Mandal & Muncipality in West Godavari District of Andhra Pradesh.

DEPARTMENTS IN FFF; -

Personnel department

Production department

Marketing department

Accounts department.

Research & Development

MANAGEMENT:

The manufacturing activities of the company are managed by Sri O.P.Goenka and Sri

sushil Goenka at the helm of affairs as whole time Directors at factory, supported by

team of highly educated and committed professional having wide range of experience

in the field of oils, derivatives and allied fields.

1.Names of present Directors : Sri B.K.Goenka -Managing Director

Sri G.S.Goenka -Whole Time Director

Sri S.B.Goenka - Whole Time Director

Sri O.P.Goenka - Whole Time Director

Sri Bharat Goenka - Whole Time Director

Sri Sitarama Goenka - Whole Time Director

Sri Sushil Goenka - Whole Time Director

Sri Vinod kumar saraogi - Director

Sri Shiv Kumar jatia - Director

Sri Anand choradi - Director

2.Particulars of present collaboration if any, No Collaboration

21

(name and address,nature of collaboration, period of collabaration etc.,)

3.Name of chief Executive Sri B. K. Goenka

CAPITAL STRUCTURE: - Finance is very much needed to any business so finance

is as heart to the business the company was incorporated kin the year 1960, the

original share capital subscribed is RS 5 lakhs.

The company is a closely held industrial houses with no public investment in the form

of equity share capital. Following is the capital structure as on 31.03.06.

Share Capital : (Including Reserves) 41.64 Crs.

Loaned funds: (Secured Loans) 71.49 Crs

(Unsecured Loans) 17.51 Crs

TOTAL 130.64 Crs

BANKERS: -

STATE BANK OF INDIA [CHENNAI]

STATE BANK OF HYDERABAD [CHENNAI]

ANDHRA BANK [TADEPALLIGUDEM]

CENTREL BANK OF INDIA [CHENNAI]

INDUSTRIAL DEVELOPMENT BANK OF INDIA LTD [CHENNAI]

KARUR VYSYA BANK LTD [TADEPALLIGUDEM]

BRANCHES: -

MUMBAI

22

HYDERABAD

KAKINADA

NEW DELHI

MULTIFARIOUS PROGRESS: -

Starting with a solvent extraction plant in 1962 units was

continuously added year after year to form a wide spectrum of products. Current

manufacturing activities comprise of -

Solvent Extraction Plant 1 [lurgi, Germany]

Solvent Extraction Plant 2 [desmet, Belgium/India]

Solvent Extraction plant 3 [fabricated and installed by engineering division of 3f

group.

Solvent Extraction plant 4 [fabricated and installed by oilex India and engineering

division of 3f group]

The above four extraction plants provide versatility of operation in

processing different oil seeds/oil cakes at the same time and hence are highly advantageous

in marketing. The plants have facilities to process a wide variety of oil seeds/oil cakes like

rice bran, soybean, sunflower, groundnut, rapeseed, sesame, mango, sal, Niger, etc.

continuous upgradation of manufacturing process through in house and world wide research

is our hallmark.

Refinery; - [sharpels USA and engineering division 3f group]

High quality refining of a variety of vegetable oils.

23

Fat Splitting Plant; - [wurster&Sanger USA and engineering division of 3f group]

High pressure splitting of oil into fatty acids and sweet water.

Fatty Acid Distillation Plant; - [luwa, Switzerland]

High quality distillation of crude fatty acids obtained from the splitting plant.

High quality distillation of crude fatty acids obtained from the splitting plant.

Glycerin plant; - [wurster & Sanger USA]Processing of sweet water obtained from fat

splitting plant into various grades of refined glycerin.

Stearic acid plant: -[engineering of 3f group]

Hydrogenation of fatty acids into stearic acid flakes.

Hydrogenation plant: - [Bernardino Italy and engineering division of 3f group]

Hydrogenation of fats and fatty acids for industrial use.

Physical refinery: - [yoshinoi technology and engineering division of 3f group]

Refining of high free fatty acid oils by steam distillation.

Canning division: -[fabrication and installation by engineering division of 3f group]

Processing of fruits into pulp. Juice, and bars.

Vanaspati-shortening- margarine division: -[fabrication and installed by engineering

division of 3f group]

Production of vanaspati shortening high quality bakery fats and margarine from

refined oils.

Fractionation plant: - This division produces high quality oleins and stearines from

various edible fats for use in manufacture of chocolate confectionery and cosmetics.

Leading manufacturers in this field of activity all over the world are our customers.

Turnkey engineering division: - In collaboration with yoshino Seisakusho co LTD

Japan who have done pioneering work in developing process and technical know-how

for refining high FFA rice bran oil, our engineering division has installed and

commissioned five plants of a total project cost of RS. 170 million in south India. 24

India is the second largest producer of rice with a large potential of crude rice bran oil

to be processed and turned into a fine cooking medium to satisfy the requirements of

an immense Indian market. 3f group engineering division is equipped to set up any

vegetable oil and derivative processing project.

Oil palm project: - plantation of oil palm to progressively cover 25000 hectares in

Andhra Pradesh and Karnataka the southern states of India is sponsored by us.

High yielding variety of sprouted seeds from India and abroad is grown in our

nursery and seedlings are regularly supplied for planting to the farmers to cover the

targeted area. Under comprehensive extension services provided by us the maturing of

plantation is expected to be ideal mean while the group has set up plant and machinery

along with suitable infrastructure to crush the palm fruits and kernels into oil and

process the same into refined oils olien stearine and a host of other products. Total

project outlay is estimated to be df1 billion Indian rupees.

International trading: - Besides the export of the manufactured products with

large warehouse for dry cargo bulk storage installation for liquid cargo at the ports,

required infrastructure at our command and international trading experience of over

40 years the 3f group has set up high standards and achieved substantial growth in

international trading of commodities like rice, edible oils, industrial fats, maize,

tapioca, hps groundnut kernels dyes and chemicals. The group has been a pioneer in

introducing various Indian products manufactured by us to new international markets

and has won awards for our performance. However, a research and development new

product is being done on a continuous basis for enriching the international trading in

both quality and volumes.

SEARCH AND RESEARCH: - Research and development is the pivot of our

activities and has made us to stand in good steady continuous upgradation of production

process with the help of a well-equipped R&D laboratory at Hyderabad and

diversification in new research based projects in our corporation. Culture leading us to a

steady upward movement.

25

SERVICE TO SOCIETY: - The 3f group is involved in a large way in social service

activities the goenka family trust runs Arts and Science college for women in Andhra

Pradesh and a Higher Secondary School in Rajasthan. It has a established a boys college

in Andhra Pradesh, a Higher Secondary School in Myanmar and a multistory building

in Tamilnadu, providing accommodation to Tourist’s and Social functions with a library

and reading room. In addition to the above projects the group has also being regularly

contributing to several educational, medical and social service institutions.

ETHICS : -

The 3f group is proud of its inherent values, which are, persuade relentlessly to drive

it towards sustainable growth. These values are common language that binds all its

people.

The 3f group stands for: -

An intrinsic commitment to its people A culture of trust, mutual respect, open communication and transparency of action. Commitment to welfare-driven initiatives that make a qualitative difference to the

lives of marginalized people. An environment-conscious group through its eco-friendly units.

Indian values with a global mind set.

3f groups manufacture a variety of products including vanaspati granite

readymade garments computer software etc. we have listed a few of our products here.

TANDUL; - Refined rice bran oil

A multi purpose-cooking medium judged as the safest cooking oil in the world.

Contains tocopherol and oryzanol that reduce cholesterol. It is extensively used in

Japan an evidence for the Japanese larger living.

Packing 15kg/1litre flex pouch.

SUN DELITE: - Refined sunflower oil.

26

Imported from Argentina and refined in the most modern refinery contains high puff.

It lowers cholesterol. A general purpose cooking oil.

Packing, 15kgtin/15litre tin/5litre jar/1litre flex pouch.

SURABHI: - Vanaspati

An economical vegetable fat for small-scale bakeries. Multi utility fat widely used all

over the country.

Packing, 15kg bag-in-box/15kg tin/15kg jar.

BAKER’S PET: - Bakery shortening.

Multipurpose bakery shortening creamy white and bland in taste. A blend of specially

formulated and textured hydrogenated fats to provide excellent plasticity. The largest

selling brand in south India for manufacturing cakes breads biscuits filling cream

cookies also used for shallow and deep-frying.

Packing; 15kgbag-in-box/15kg tin/15kg jar.

3F: - Vanaspati

100% granulated vegetable fat. A favourite of south Indian housewives for cooking

and deep-frying. A must for all festival cooking and sweet preparations.

Packing, 15kg tin/15 liter tin/1litre flex pouch/500,200 and 100 ml flex pouch.

MELLO; - Margarine.

Margarine made from the choicest of refined oils for bakery industries recommended

by the best bakers in the country for cake cream pastry biscuits icing and cookies.

Ideal because it is not colored and not flavored.

Packing; 15kg bags-in-box.

27

BISCREME: - Aerated bakery shortening.

Uniform dispersion of nitrogen gas in the fat produces a superior bakery shortening

[contains 10% v/wt nitrogen] specially used for filling cream and icing. Best for

premium biscuits and cookies.

Packing; 15kg bag-in-box.

PALM DELITE; - Imported R&D palmolein.

A refined bleached and deodorized palm olein imported from Malaysia. Economical

oil supplied all over the country directly from our ports on the east and west.

Packing, 15kg tin/1litre flex pouch/ 500 ml flex pouch.

BAKERS DELITE; - Puff pastry fat, An in house development to produce a smooth

fat designed for use in puff pastry products. A specialty fat, which gives a flaky, puff

with a good life.Packing; 15kg bag-in-box.

GOLDEN SPREAD: - Margarine for puffs

Specially formulated product for puffs. There is already a great demand for these

margarine for its superior quality.

Packing; 15kg bag-in-box.

BAHAAR: - Mango bar

A papad made from mango pulp favorite mouth tingler for the young and the old.

Packing; 20gms sachet.

3F GLYCERINE: - Refined glycerin made from sweet water obtained in fat splitting.

Grades available--- Industrial white –IW

Chemically pure-CP

28

Indian pharmacopeia-IP

Packing; 250kg plastic drums.

TRIFFA: - Fatty acids/stearic acids.

Standard and hardened quality distilled fatty acids made from rice bran palm coconut

sunflower rapeseed Soya and linseed oil. Custom made formulations available on

order. Raw material for cosmetic premium soap lubricants chemical industries rubber

and PVC formulations.

Packing, 110kg in plastic carboys for liquids 50 kg woven hdpe lined bags for

hardened quality in flake form.

OTHERS; - Crude palm, oil-bulk.

Refined palms oil-bulk; contract farming by farmers. We provide imported seedlings

after acclimatizing know how for growing is provided to the farmers.

Specialty fats;

Refined kokum fat [garcenia]

Sal stearine [shorea robusta]

Produced from forest sources. An important nontimber forest produce.

Mango stearine [mangifera India]

Shea stearine.

Cosmetic ingredients ---- mango olien Shea olien.

Refined rice bran oil wax: - Used in various industries like paper coating candles

water proofing floor shoe and furniture polish cosmetics carbon paper printing inks

fruit and vegetable coatings and pharmaceuticals. Rice bran oil wax may substitute

wax like carnauba.

29

Packing, 25kg in lined paper bags.

Exporters of: - Indian rice [non-basmati]

De oiled rice bran

De oiled salseed meal -pellets non- –dusty.

Importers of; -

Palm oil and its fractions.

Crude sunflower oil

Crude soybean oil; -

Have sea-worthy barges for unloading from ships when anchored

near shallow water ports. Presence in all minor ports in India. West coast Kochi and

Mangalore east coast gopalpur Kakinada and nagapattinam.

Turnkey project - Supplier for double solvent refining of high FFA oils up to 20%

such as Rica bran oil solvent extracted high FFA oils. The refined oil obtained is of

excellent quality as per food standards.

GARMENT EXPORTERS; - We export woven garments to United States of

America, United kingdom Canada Germany Japan Chile France and Australia.

Our customer span ranges from chain stores mail order boutiques and wholesalers

order sizes vary from 1000 to 1,00,000 units.

GRANITE EXPORTERS - We initially started exporting rough blocks and have

expanded by exporting cut-to-size slabs and random slabs. Later we shifted towards

manufacturing of finished products like monument artifact items and fireplaces.

30

SOFTWARE DEVELOPMENT: - Goenka InfoTech limited provides the full range

of IT solutions and services in the following segments.

1. Conformance services.

2. Web gardening

3. Software maintenance and web enabling of legacy applications.

4. IT applications in power sector

5. Smart card based solutions.

The 500 square meters of software development center at Hyderabad has been

designed to provide the state of art infrastructure for software professionals.

31

CHAPTER-3

32

CONCEPTUAL FRAME WORK OF

CASH FLOW STATEMENT

Introduction:

Cash plays a very important role in the entire economic life of a business. A firm

needs cash to make payments to its suppliers, to incur day-to-day expenses and to pay

salaries, wages, interest and dividend, etc. In fact, what blood is to a human body,

cash is to a business enterprise. It is very essential for a business to maintain an

adequate balance of cash. But many times, a concern operates profitably and yet it

becomes very difficult to pay taxes and dividend. This may because

(i) Although huge profits have been earned yet cash may not have been

received or

(ii) Even if cash has been received, it may have drained out for some other

purposes.

This movement of cash is of vital importance to the management. The two basic

financial statements, i.e., the balance sheet and profit & loss account, provided the

essential basic information on the financial activities of a business, but their

usefulness is limited for analysis and planning purpose. The balance sheet does not

disclose the causes for changing in the assets and liabilities between two different

points of time. The profit and loss account also fails to disclose the reasons for

shortage of cash in spite of positive net income. Thus, another statement, called Funds

Flows Statements, was prepared to show the changes in the assets and liabilities from

the end of one period of time to the end of another period of time. To underline the

importance of funds statements was prepared to show the changes in the assets and

liabilities from the end of one period of time to the end of another period of time.

There was a need for cash flow statement prepared in standard format The

Financial Accounting Standard Board, U.S.A., has emphasis the need for cash flow

statement as,

33

“Financial reporting should provide information to help present and potential

investors and creditors and to her users in assessing the amounts, timing and

uncertainty of prospective cash receipts from dividends or interest and proceeds from

the sales, redemption or maturity of securities or loans. The prospects for those cash

receipts are affected by an enterprise’s ability to generate enough cash to meet the

obligations when due and its other

operating needs, to reinvest in operations and to pay cash dividends.”

In June 1995, the Securities and Exchange Board of India (SEBI) amended

clause 32 of the Listing Agreement requiring every listed company to give along with

the balance sheet and profit and loss account, a cash flow statement prepared in the

prescribed format, showing separately cash flows from operating activities, investing

activities and financing activities.

Recognizing the importance of cash flow statements, the Institute of Chartered

Accountants of India (ICAI) issued.

A.S -3 Revised: Cash flows statements in March, 1997. The revised accounting

standard supersedes A.S -3 changes in Financial Statements Position, issued in June

1981.

MEANING

Cash flow statement is a statement which describes the inflows (sources) and

outflows (uses) of cash and cash equivalents in an enterprise during a specified period

of time. Such a statements enumerated net effects of the various business transactions

on cash and its equivalents and takes onto account receipts and disbursements of cash.

A cash flow statement summarises the causes of changes in cash flow Statement and

should present it for each period for which financial statement are prepared. The terms

cash, cash equivalents and cash flow are used in this statement with the following

meanings:

34

1. Cash comprises cash on hand and demand deposits with banks.

2. Cash equivalents are short term, highly liquid investments that are readily

convertible into known amounts of cash and which are subject to an

insignificant risk of changes in value. Cash are held for the purpose of meeting

short-term cash commitment rather than for investment or other purposes. For

an investment to qualify as a cash equivalent, it must be readily convertible to a

known amount of cash and be subject to an insignificant risk of change in

value. Therefore, an investment normally qualifies as a cash equivalent only

when it has a short-maturity, of say, three months or less from the date of

acquisition. Investments in shares are excluded unless they are, in substance,

cash equivalents: for example, preference shares of a company acquired shortly

before their specified redemption date (provided there is only an insignificant

risk of failure of the company to repay the amount at maturity).

3. Cash flow are inflows and outflows of cash and cash equivalents. Flow of cash

is said to have taken place when any transaction makes changes in the amount

of cash and cash equivalents available before happening of the transaction. If

the effect of transaction results ion the increase of cash and its equivalents, it is

called an inflow (source) and if it results in the decrease of total cash, it is

known as outflow (use) of cash.

CLASSIFICATION OF CASH FLOWS :

According to AS-3 (Revised), the cash flow statement should report cash flows

during the period classified by operating, investing and financing activities. Thus,

cash flows are classified into three main categories:

1. Cash flows from operating activities.

2. Cash flows from investing activities.

3. Cash flows from financing activities.

35

1. Cash flows from operating activities: operating activities are the principal

revenue-producing activities of the enterprise and other activities that are not

investing or financing activities.

The amount of cash flows arising from activities is a key indicator of the extent to

which the operations of the enterprise have generated sufficient cash flows to

maintain the operating capability of the enterprise, pay dividend, repay loans, and,

make new investments without recourse to external sources of financing.

Information about the specific components of historical operating cash flows is

useful, in conjunction with other information, in forecasting future operating cash

flows.

Cash flows from operating activities are primarily derived from the principal

revenue-producing activities of the enterprise. Therefore, they generally result

from the transactions and other events that enter into the determination of net

profit or loss.

2. Cash flows from investing activities: Investing activities are the acquisition

and disposal of long-term assets and other investments not included in cash

equivalents. The separate disclosure of cash flows arising from investing

activities is important to generate future income and cash flows.

3. Cash flows from financing activities: Financing activities are activities that

result in changes in the size and composition of the owner’ capital (including

preference share capital in the case of a company and borrowing of the

enterprise).

The separate disclosure of cash flows arising from financing activities is

important because it is useful in predicting claims on future cash flows

provided of funds (both capital and borrowings) to the enterprise.

36

Optimum Cash Level:

If the firm maintains lower cash balance, its liquidity position is affected. For

urgent payments it has to sell some marketable securities incurring penal interest and

transaction costs. But the profitability will be higher by utilizing the released funds If

the firm maintains the higher cash balance its liquidity will improve but profitability

will decline by lasting the interest on it, which involves an opportunity cost. Thus the

optimum cash balance is to be arrived by matching the transaction costs and

opportunity costs Similar to EOQ formula, optimum cash balance is the amount of

cash balance at which the sum of both the transaction costs and opportunity costs will

be minimum.

Uses and significance of cash flow statement.

Cash flow statement is of vital importance to the financial management. It is an

essential tool of financial analysis for short-term planning. The chief advantages of

cash flow statement are as follows:

1. Since a cash flow statement is based on the cash basis of accounting, it is

very useful in the evaluation of cash position of a firm.

2. A projected cash flow statement can be prepared in order to know the future

cash position of a concern so as to enable a firm to plan and coordinate its

financial operations properly. By preparing this statement a firm can come

to know as to how much cash will be needed into the firm and how much

cash will be needed to make various payments and hence the firm can well

plan to arrange for the future requirements of cash.

3. A comparison of the historical and projected cash flow statements can be

made so as to find the variations and the deficiency or otherwise in the

performance so as to enable the firm to take immediate and effective action.

4. A series of intra-firm and inter-firm cash flow statements reveal whether the

firm’s liquidity (short-term paying capacity) is improving or deteriorating

37

over a period of time and in comparison to other firms over a given period

of time.

5. Cash flow statement helps in planning the repayment of loans, replacement

of fixed assets and other similar long-term planning of cash. It is also

significant for capital budgeting decisions.

6. It better explains the causes for poor cash position in spite of substantial

profits in a firm by throwing light on various applications of cash made by

the firm. It further helps in answering some intricate questions like what

happened to the net profit? Where did the profits go? Why more dividends

could not be paid in spite of sufficient available profit?

7. Cash flows analysis is more useful and appropriate than funds flow analysis

for short –term financial analysis as in a very short period it is cash which is

more relevant then the working capital for forecasting the ability of the firm

its immediate obligations.

8. Cash flow statement prepared according to AS-3 (Revised) is more suitable

for making comparisons than the funds flow statements as there is no

standard format used for the same.

9. Cash flow statement provides information of all activites classified under

operating, investing and activities, The funds statements even when

prepares on cash basis, did not disclose cash flows from such activities

separately, Thus, cash flows statements is more useful than the funds

statements.

10. Limitation of Cash Flow Statement:

Despite a number of uses, cash flow statements suffer from the following

limitations:

38

a. It is difficult to precisely define the term “cash”. There are controversies

over a number of items like cheques, stamps, postal orders, etc. to be

included in cash.

b. A cash flow statement reveals the inflow and outflow of cash but the

exclusion of near cash items from cash obscures the true reporting of the

firm’s liquidity position.

c. Working capital being a wider concept of funds, a funds flow statement

presents a more complete picture than cash flow statement.

d. As cash flow statements are based on cash basis of accounting, it ignores

the basic accounting concept of accrual basis.

e. Some people feel that as working capital is a wider concept of funds, a fund

flow statement provides a more complete picture than cash flow statements.

f. Cash flow statements are not suitable for the judging the profitability of the

firm as non-cash charges are ignored while calculating cash flows from

operating activities.

Determinants of Cash flow:

The following factors will determine the cash flow :

a. Operating decisions-operating expenses, sales revenue and net profit.

b. Capital expenditure decisions-investment decisions, expansion etc.

c. Credit policy-credit period allowed to customers and followed by suppliers.

d. Inventory decisions-inventory control and management.

e. Tax on profits-tax planning, investment in IDBI etc.

f. Payment of Interest, dividends and issue of bonus shares.

g. Productive decisions.

39

h. Liquidity gaps – arising out of delay in cash realisation, utilization of

working capital for capital expenditure, high fixed charges obligation and

finally low generation of internal resources which may be due to lower

production and sales etc…

i. Procedure for preparing a Cash Flow Statement.

Cash flow statement shows the impact of various transaction on cash position

of firms. It is prepared with the help of financial statements, i.e., balance sheet and

profit and loss account and some additional information. A cash flow statement starts

with the opening balance of cash and balance at bank, all the inflows of cash are

added to the opening balance and the out flows of cash are deducted from the total.

The balance i.e., opening balance of cash and bank balance plus inflows of cash

minus outflows of cash is reconciled with the closing balance of cash. The

preparation of cash flow statement involves the determining of:

a. Inflow of cash

b. Out flows of cash

[a] Sources of cash Inflows:

The main sources of Cash flows are:

1. Cash flow form operations

2. Increase in existing liabilities or creation of new liabilities.

3. Reduction in or Sale of Assets.

4. Non-trading Receipts.

40

[b] Application of cash or cash flows:

1. Cash lost in operations.

2. Decrease in or discharge of liabilities.

3. Increase in or purchase of assets.

4. Non-trading payments.

Generally cash flow statement is prepared in two forms.

a. Report form

b. T form or an account form or self-Balancing types.

41

Format Of Cash Flow Statement Approved By SEBI

Cash Flow Statement( for the year ended ------------)

XYZ Limited Rs.

A. Cash Flow From Operating Activities Net profit/loss before tax and extraordinary itemsAdjustments for: Depreciation Gain/loss on sale of fixed assets Foreign exchange Miscellaneous expenditure written off Investment income Interest Dividend Operating profit before working capital changes Adjustments for : Trade and other receivables Inventories Trade payables Cash generated from operations Interest paid Direct taxes paid Cash flow before items Net cash from operating activities

B. Cash Flow From Investing Activities Purchase of fixed assets Sales of fixed assets Purchase of investments Sale of investmentsInterest received Dividend received Net cash from /used in investing activities

C. Cash Flow From Financing Activities Proceeds from issue of share capital Proceeds from long-term borrowings/banks Payments of long-term borrowings Dividend paid Net cash from/ used in financing activities

Net increase / decrease in cash and cash equivalents Cash and cash equivalents as at ---------( opening balance )Cash and cash equivalents as at --------( closing balance )

42

T FORM OR AN ACCOUNT FORM OF CASH FLOW STATEMENT

Rs. Rs.

Cash balance in the beginning

ADD: Cash Inflows:

Cash flow from operations

Sales of assets

Issue of shares

Issue of debentures

Raising of loans

Collection from debtors

Dividends received

Refund of tax

Xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

Out flow of cash

Redemption of

Preference shares

Redemption of dentures

Payment of Loans

Payment of dividends

Payment of tax

Cash lost in operations

xxx

xxx

xxx

xxx

xxx

xxx

xxx

xxx

Cash balance at the end Xxx

43

CHAPTER-4

44

CASH FLOW STATEMENT FOR THE YEAR ENDED

31ST MARCH 2006-07

Cash Flow Statement

( for the year ended 2007-)

Foods Fats & Fertilizers Limited 2006-07

Rs. Rs.

A. Cash Flow From Operating Activities

Net profit before tax 56407087

Depreciation 31856107

Interest (net) 64304282

loss on sale of assets 3441539

profit on sale of assets (1515867)

assets written off

Dividend received (9559873)

provision for leave encashment 23758 88549946

Operating profit before working capital

changes

144957033

Adjustments for Working capital changes

Inventories 39311985

Trade and other receivables (49315411)

Trade payables 101866649 91863223

Cash generated from operations 236820256

Direct taxes paid (8096802)

Net cash from operating activities 228723454

B. Cash Flow From Investing Activities

Purchase of fixed assets (175857713)

increase in capital Works in progress (100442215)

45

Sales of fixed assets 12140640

Sale of investments 0

Interest received 2988510

Dividend received 9559873

Purchase of investments (16109754)

Net cash from /used in investing

activities

-267720659

C. Cash Flow From Financing Activities

interest paid -66628765

increase /(decrease) in long term

borrowings

83089936

increase /(decrease) in unsecured

loans

26754511

issue of equity shares 2884600

share premium received 13419600

Dividend paid -5000000

tax on dividend -701250

Net cash from/ used in financing activities 53818632

Net increase / decrease in cash and cash

equivalents

14821427

Cash and cash equivalents as at ---------( opening

balance )

37385785

Cash and cash equivalents as at --------( closing

balance )

52207212

46

CASH FLOW STATEMENT FOR THE YEAR ENDED 31ST

MARCH 2007-08

Cash Flow Statement

( for the year ended-2008)

Foods Fats & Fertilisers Limited 2007-08

Rs. Rs.

A. Cash Flow From Operating Activities

Net profit before tax 132256042

Depreciation 49259510

interest (net) 101170028

loss on sale of assets 336278

profit on sale of assets -47520

assets written off 55223

Dividend received -664838

provision for leave encashment 75054 150183735

Operating profit before working capital changes 282439777

less :adjustments for Working capital

changes

inventories -659939857

trade and other receivables 32125894

trade payables 375180792 -252633171

Cash generated from operations 29806606

Direct taxes paid -20410969

Net cash from operating activities 9395638

B. Cash Flow From Investing Activities

Purchase of fixed assets -283141340

increase in capital Works in progress 282907496

Sales of fixed assets 1981855

47

Sale of investments 100000

Interest received 4270113

Dividend received 664838

Purchase of investments -11512750

Net cash from /used in investing

activities

-4729788

C. Cash Flow From Financing Activities

interest paid -105155246

increase /(decrease) in long term

borrowings

100233880

increase /(decrease) in unsecured loans 31240013

Dividend paid -10382265

tax on dividend -1456113

Net cash from/ used in financing activities 14480269

Net increase / decrease in cash and cash

equivalents

19146119

Cash and cash equivalents as at ---------( opening

balance )

52207212

Cash and cash equivalents as at --------( closing

balance )

71253331

48

CASH FLOW STATEMENTS FOR THE YEAR ENDED 31ST

MARCH 2008-09

Cash Flow Statement

( for the year ended-2009)

Foods Fats &Fertilizers Limited 2008-09

Rs. Rs.

A. Cash Flow From Operating Activities

Net profit before tax 242919590

Depreciation 57333045

interest (net) 129168630

loss on sale of assets 929712

profit on sale of assets -59135

Assets written off 45848

Dividend received -8109

provision for leave encashment 0

187409991

Operating profit before working capital changes 430329581

less :adjustments for Working capital changes

inventories -629318282

trade and other receivables -209901035

trade payables 430615593 -408603724

Cash generated from operations 21725857

Direct taxes paid -48509383

Net cash from operating activities -26783526

B. Cash Flow From Investing Activities

Purchase of fixed assets -71040267

increase in capital Works in progress -49565238

Sales of fixed assets 3206869

49

Sale of investments 691450

Interest received 10606433

Dividend received 8109

Purchase of investments -28363150

Net cash from /used in investing

activities

-134455794

C. Cash Flow From Financing Activities

Interest paid -140411398

Increase /(decrease) in long term

borrowings

342058431

Increase /(decrease) in unsecured loans 27807685

Dividend paid -15925088

Tax on dividend -2706469

Net cash from/ used in financing activities 210823161

Net increase / decrease in cash and cash

equivalents

51850936

Cash and cash equivalents as at ---------( opening

balance )

71353331

Cash and cash equivalents as at --------( closing

balance)

123204267

50

CASH FLOW STATEMENTS FOR THE YEAR ENDED 31ST

MARCH 2009-10Cash Flow Statement

( for the year ended-2010)

Foods Fats &Fertilizers Limited 2009-10

Rs. Rs.

A. Cash Flow From Operating Activities

Net profit before tax 251213606

Depreciation 61410133

interest (net) 156397727

loss on sale of assets 508968

profit on sale of assets (1231297)

Assets written off 589

Dividend received (4717257)

provision for leave encashment

230152

207744722

Operating profit before working capital changes 458958328

less :adjustments for Working capital changes

inventories 653814967

trade and other receivables (123209646)

trade payables (532968038) (2362716)

Cash generated from operations 456595612

Direct taxes paid (79900730)

Net cash from operating activities 376694882

B. Cash Flow From Investing Activities

Purchase of fixed assets (142131138)

increase in capital Works in progress 29653864

Sales of fixed assets 4852979

Sale of investments 0

51

Interest received 25268526

Dividend received 4717257

Purchase of investments (98959042)

Net cash from /used in investing

activities

(176597555)

C. Cash Flow From Financing Activities

Interest paid (173719225)

Increase /(decrease) in long term

borrowings

(63725952)

Increase /(decrease) in unsecured loans 65178537

Dividend paid (21233450)

Tax on dividend (3608625)

Net cash from/ used in financing activities (197108714)

Net increase / decrease in cash and cash

equivalents

2988613

Cash and cash equivalents as at ---------( opening

balance )

123204267

Cash and cash equivalents as at --------( closing

balance)

126192880

52

CASH FLOW STATEMENTS FOR THE YEAR ENDED 31ST

MARCH 2010-11

Cash Flow Statement

( for the year ended-2011)

Foods Fats &Fertilizers Limited 2010-11

Rs. Rs.

A. Cash Flow From Operating Activities

Net profit before tax 281559223

Depreciation 68732377

interest (net) 129179291

loss on sale of assets 453814

profit on sale of assets (104041)

Assets written off

0

Dividend received 0

provision for leave encashment

395093

204411814

Operating profit before working capital changes 485971037

less :adjustments for Working capital changes

inventories (98070526)

trade and other receivables 11423538

trade payables 541971467 (455324479)

Cash generated from operations 941295516

Direct taxes paid (105060924)

Net cash from operating activities 836234592

B. Cash Flow From Investing Activities

Purchase of fixed assets (165063711)

53

increase in capital Works in progress 16510186

Sales of fixed assets 2053384

Sale of investments 0

Interest received 30968867

Dividend received 0

Purchase of investments (63321110)

Net cash from /used in investing

activities

(178852384)

C. Cash Flow From Financing Activities

Interest paid (153527898)

Increase /(decrease) in long term

borrowings

(553174226)

Increase /(decrease) in unsecured loans 90398069

Dividend paid 0

Tax on dividend 0

Net cash from/ used in financing activities (616304055)

Net increase / decrease in cash and cash

equivalents

41078153

Cash and cash equivalents as at ---------( opening

balance )

126192880

Cash and cash equivalents as at --------( closing

balance)

167271033

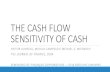

Cash flows over the five years period of the firm

54

Year

Business

income ( sales ) Net profit

business cash

flows

Investment

CFs

Financial

cash flows

2006-07

2107633808

56407087 228723454 267720659 53818632

2007-08 3053159161 132256042 9395638 -4729788 14480269

2008-09 4563870619 242919590 -26783526 -134455794 210823161

2009-10 4781788930 251213606 376694882 176597555 197108714

2010-11 5007498552 281559223 836234592 178852384 616304055

-1000000000

0

1000000000

2000000000

3000000000

4000000000

5000000000

6000000000

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

Business income (sales )

Net profit

business cash flows

Investment CFs

Financial cash flows

Fig :1 cash flows over the five years period of the firm

55

INTERPRETATION:

The graph fig no: 1 explains the cash flows for the past five years, sales are the major

source of the cash inflows for any firm shows the continuous increase of 259.6 crs to 456 cr

from the year 2006-07 to 2010-11, the reason behind this was the increase in the turnover of

the goods such as the refined oil, Vanaspati, fatty acids, from the year 2009 power had been

joined this portfolio. This surge in the sales shows the good positive signal for the firm’s

future growth.

Even though the firm shows the good potential in sales the net profit shows very little

margin to the firm the firm P&L account in the year 2006-07 shows the profit of 4.95 cr and

it was stand at 2.08cr in the next year, here is caused by the decrease in the sales. Profit was

increased from 20.08cr to 24.29 cr from the year 2006-07to 2009-10, on the left side of the

profit it was very small margin while comparing the sales of the firm, but on the right of the

profit is it shows continuous increase shows the potential of the firm.

Business cash flows or the cash from the operating activities are obtained by adding

non-cash/ non –operating expenditure to the net profit, and subtract the non-operating

incomes, and adjusted working capital changes, it shows the negative operating flows in the

years 2006-07 and 2010-11, accretion in the inventories, increase in trade and other

receivables, and increase In the non- operating incomes such as the dividend received.

Remaining year’s shows positive operating cash flows.

Investment activities are the acquisition and disposal of long-term assets and other

investments. Positive investment cash flows are shown in the year 2006-07 instance

remaining years were shown in negative cash flows it caused for the increase in the

investment outflows over the inflows.

Financing activities are activities that result in changes in the size and composition of

the owner’s capital the firm financial cash flows in the year 2006-07 was 10.7 cr it was

increased in the year 2006-07 to 12.8cr and preceding years 2008-09 and 2009-10 it marked

in the decreased cash flows while comparing the previous year it was amounted as 5.38cr and

1.49 cr correspondingly again in the year 2010-11 there is a surge in the financial flows of the

firm.

56

Chapter-5

57

FINDINGS

Firm has good growth in their sales, sales been continuous accelerated from

259.6 crs to 456 cr from the year 2006-07 to 2010-11, the reason behind this

was the increase in the turnover of the goods such as the refined oil,

Vanaspathi, fatty acids, from the year 2009 power had been joined this

portfolio.

Business cash flows or the cash from the operating activities are obtained by

adding non-cash/ non –operating expenditure to the net profit, and subtract the

non-operating incomes, and adjusted working capital changes, it shows the

negative operating flows in the years 2006-07 and 2010-11, accretion in the

inventories, increase in trade and other receivables, and increase In the non-

operating incomes such as the dividend received. Remaining year’s shows

positive operating cash flows

Even though the firm shows the good potential in sales the net profit shows

very little margin. Firm’s P&L account in the year 2006-07 shows the profit of

4.95 cr and it was stand at 2.08cr in the next year, here is caused by the

decrease in the sales.

The liquidity position i.e., short term solvency of the company is not

satisfactory.

In the year i.e., 2007-2008. The net profit before tax is 2,08,72,988. It is

decreased by 58% compared to 2006-2007. After adjustments cash from

operating activities is 6, 37, 86,390.

Cash from unsecured loans were increased 22.lakhs to 278 laths within the five years

from 2006-11, the company is using more sources from secured and unsecured

loans.

58

Finally the payment of the interest was the major component in the total

financial cash out flows. It occupies approximately 84% of the total financial

out flows.

59

SUGGESTIONS

1. Investments are very high. So it should be reduced.

2. Cash from operations is very high. So, decrease in the working capital when

obtaining loans from banks.

3. The firm has to maintain the adequate liquidity position.

4. Adequate promotional activities should be taken.

60

CHAPTER-6

BIBLIOGRAPHY

61

1. Financial Management – I.M. PANDEY

2. Financial Management, Text & Problems – M.Y KHAN

- P.K. JAIN

3. Financial Management - S.N.MAHESWARI

4. Annual reports of Foods Fats & Fertilizers LTD Tadepalligudem

62

Related Documents