California Society of Municipal Finance Officers GASB Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB are determined only after extensive due process and deliberation.

California Society of Municipal Finance Officers GASB Update The views expressed in this presentation are those of Mr. Bean. Official positions of the.

Dec 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

California Society of Municipal Finance Officers

GASB Update

The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB are determined only after extensive due process and deliberation.

2

Current Events

3

Where Are We Now?

4

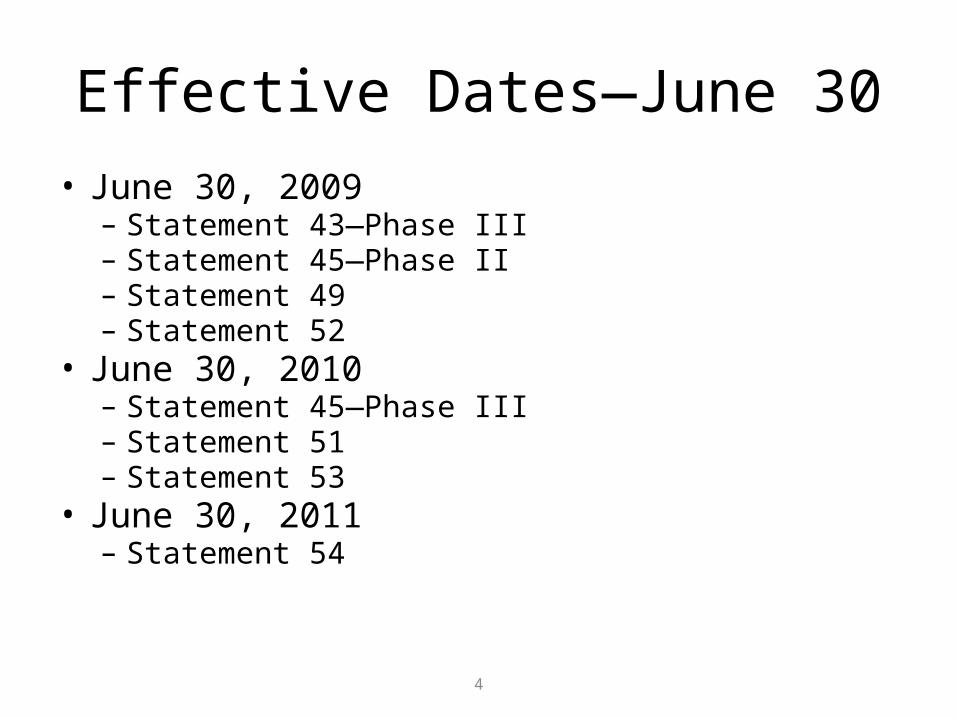

Effective Dates—June 30• June 30, 2009

– Statement 43—Phase III– Statement 45—Phase II– Statement 49– Statement 52

• June 30, 2010– Statement 45—Phase III– Statement 51– Statement 53

• June 30, 2011– Statement 54

5

Other Postemployment Benefits

Implementation Is Here

6

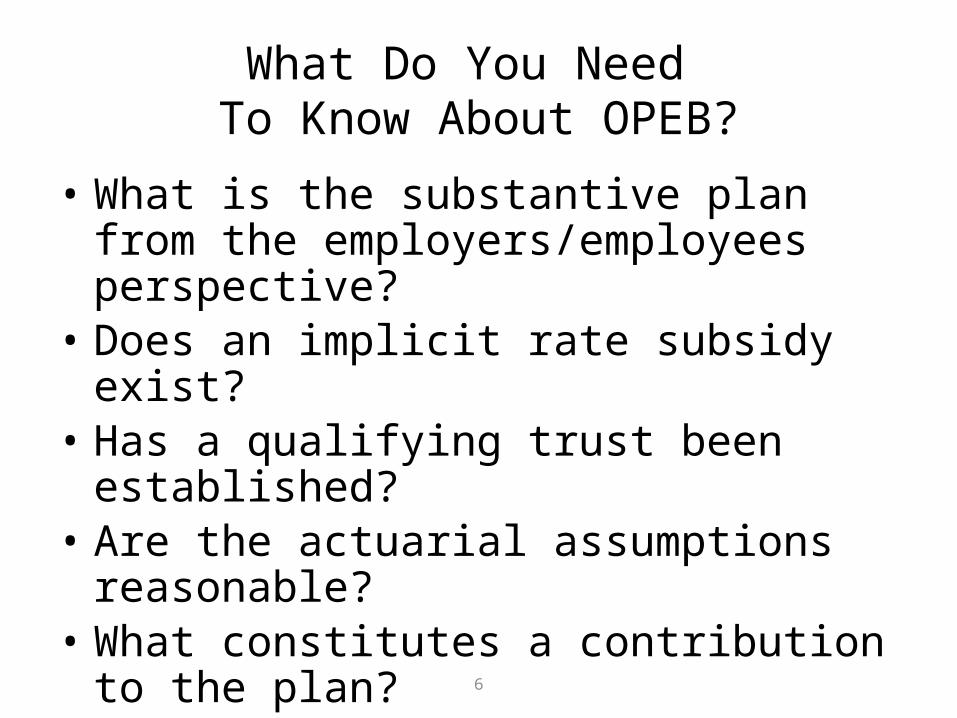

What Do You Need To Know About OPEB?

• What is the substantive plan from the employers/employees perspective?

• Does an implicit rate subsidy exist?• Has a qualifying trust been established?• Are the actuarial assumptions reasonable?• What constitutes a contribution to the plan?• What is required to be presented in the

financial statements?

7

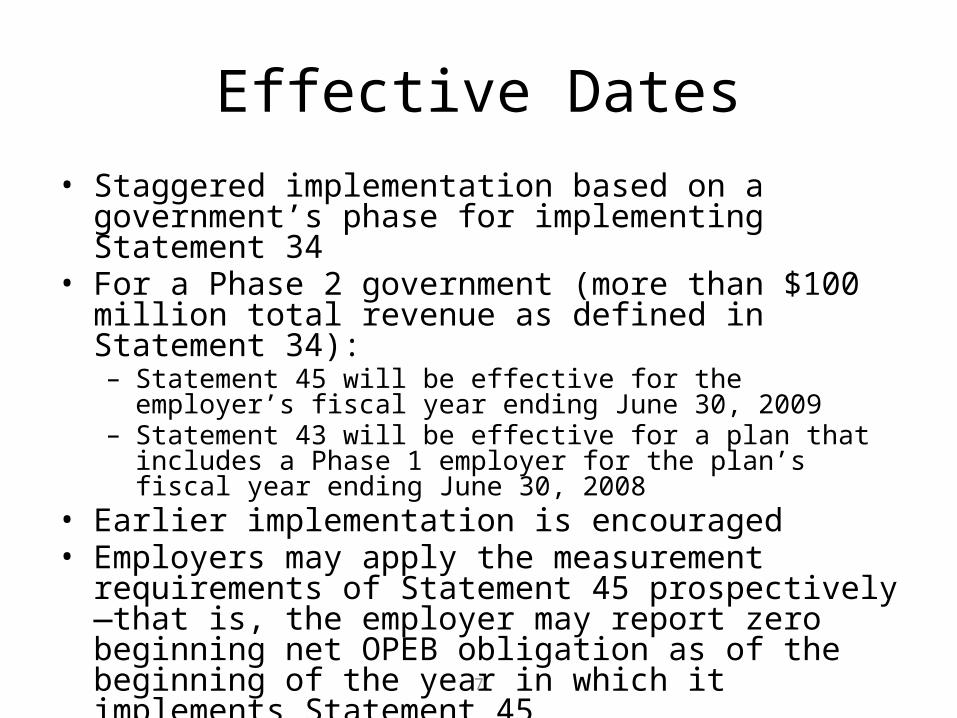

Effective Dates• Staggered implementation based on a government’s phase for

implementing Statement 34• For a Phase 2 government (more than $100 million total

revenue as defined in Statement 34):– Statement 45 will be effective for the employer’s fiscal year ending

June 30, 2009– Statement 43 will be effective for a plan that includes a Phase 1

employer for the plan’s fiscal year ending June 30, 2008• Earlier implementation is encouraged• Employers may apply the measurement requirements of

Statement 45 prospectively—that is, the employer may report zero beginning net OPEB obligation as of the beginning of the year in which it implements Statement 45

OPEB Implementation Issues

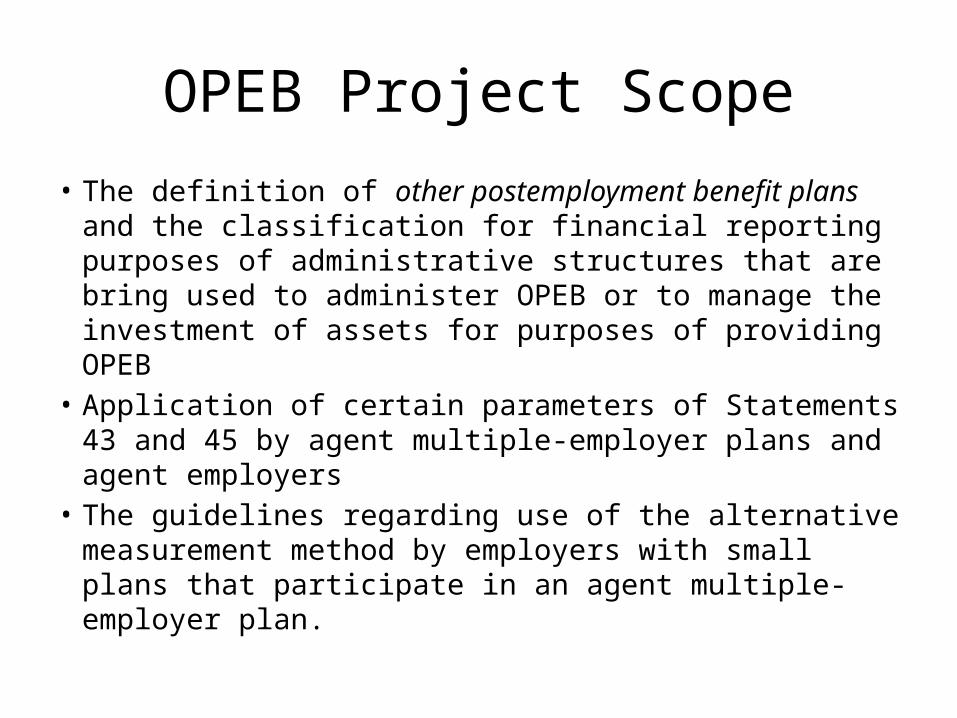

OPEB Project Scope

• The definition of other postemployment benefit plans and the classification for financial reporting purposes of administrative structures that are bring used to administer OPEB or to manage the investment of assets for purposes of providing OPEB

• Application of certain parameters of Statements 43 and 45 by agent multiple-employer plans and agent employers

• The guidelines regarding use of the alternative measurement method by employers with small plans that participate in an agent multiple-employer plan.

10

Statement 49

Accounting and Financial Reporting for Pollution Remediation Obligations

11

What Do You Need To Know About Statement 49?

• Thresholds are required to be met before the clock starts on recognition

• Measurement is based on expected cash flows• Amounts should be reasonably estimable• Some obligations will result in the recognition

of an asset• Recoveries—depend on the source

12

Recognition Threshold

• Determine whether one of more components of a pollution remediation obligation are recognizable as a liability when . . . – Government knows or reasonably believes that a

site is polluted, and– Obligating event occurs (the criteria effectively

serve as a safe harbor)

13

Obligating Events

a. Compelled to take remediation action because of pollution-caused imminent endangerment

b. Violate pollution-prevention permit—for example, RCRA permit

c. Named, or evidence indicates government will be named, as responsible party potential responsible party for remediation (or cost sharing)

14

Obligating Events

d. Named, or evidence indicates government will be named, in lawsuit to participate in remediation Excludes lawsuits having no merit—within

judicial jurisdiction

e. Government commences, or legally obligates self to commence Limited to portion legally required to complete

Implementation Ideas

• Internal controls to ensure obligating events identified

• For example—Year-end inquiry to departments– Similar to contingent liability inquiries, but for

obligating events

16

Recognition Overview

• Component recognition approach• Cost accumulation, not fair value• Current value, not present value• Expected cash flow technique

Capitalization

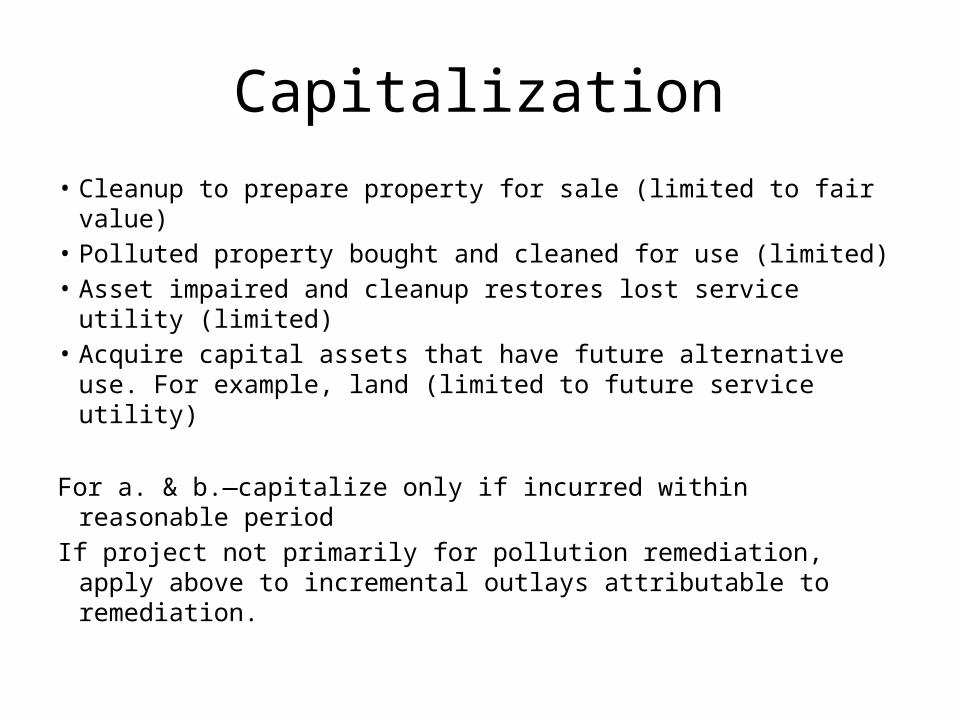

• Cleanup to prepare property for sale (limited to fair value)• Polluted property bought and cleaned for use (limited)• Asset impaired and cleanup restores lost service utility

(limited)• Acquire capital assets that have future alternative use. For

example, land (limited to future service utility)

For a. & b.—capitalize only if incurred within reasonable period

If project not primarily for pollution remediation, apply above to incremental outlays attributable to remediation.

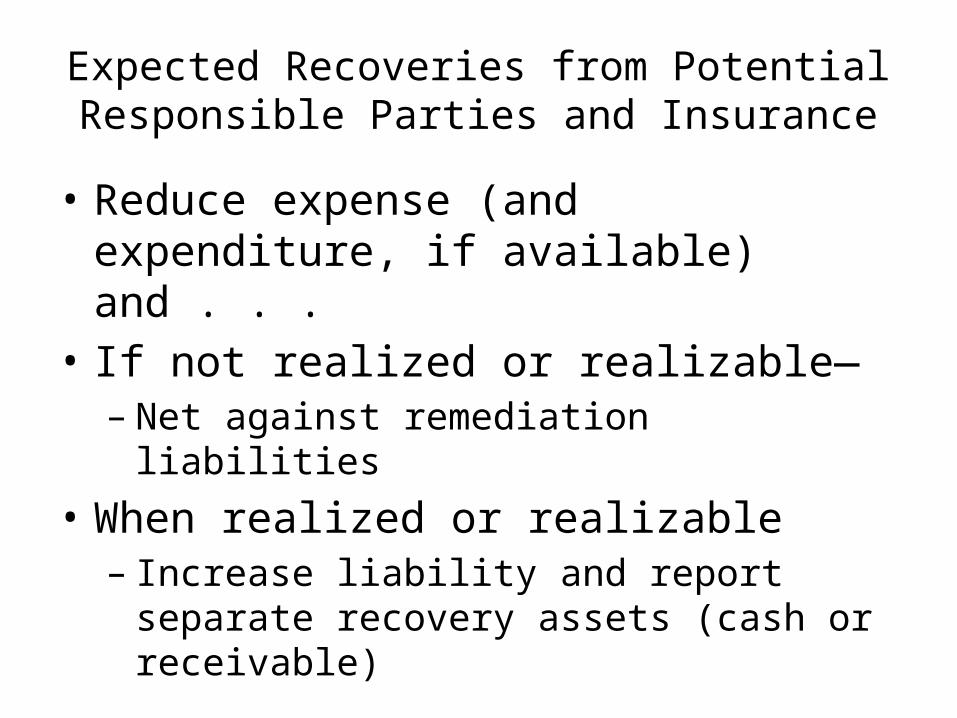

Expected Recoveries from Potential Responsible Parties and Insurance

• Reduce expense (and expenditure, if available) and . . .

• If not realized or realizable—– Net against remediation liabilities

• When realized or realizable– Increase liability and report separate recovery

assets (cash or receivable)

19

Effective Date

• Fiscal periods beginning after June 15, 2008

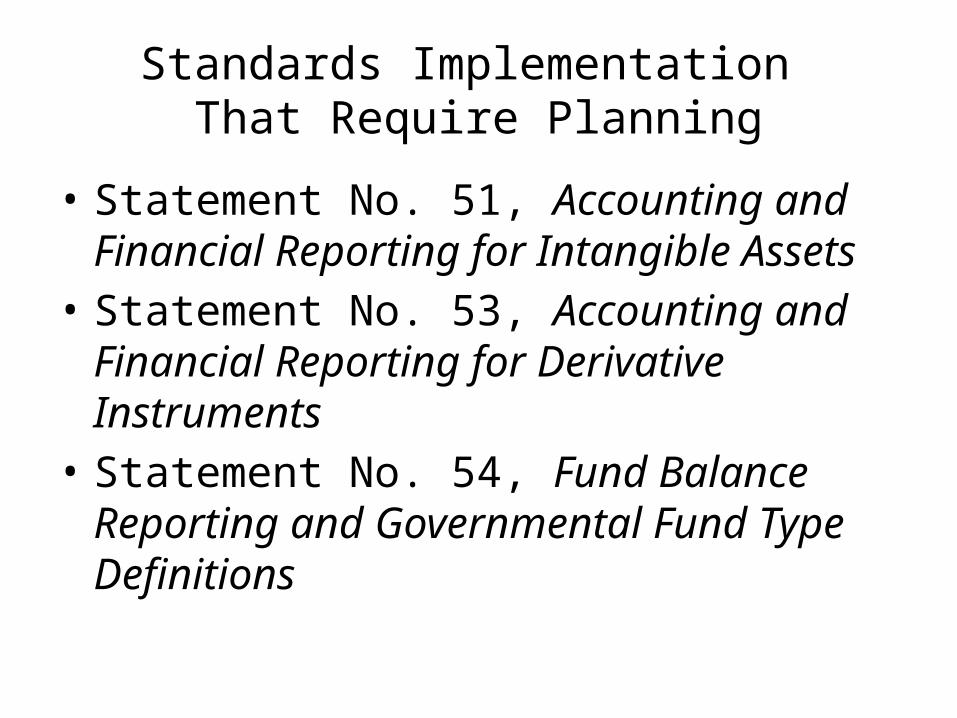

Standards Implementation That Require Planning

• Statement No. 51, Accounting and Financial Reporting for Intangible Assets

• Statement No. 53, Accounting and Financial Reporting for Derivative Instruments

• Statement No. 54, Fund Balance Reporting and Governmental Fund Type Definitions

21

Statement 51

Intangible Assets

22

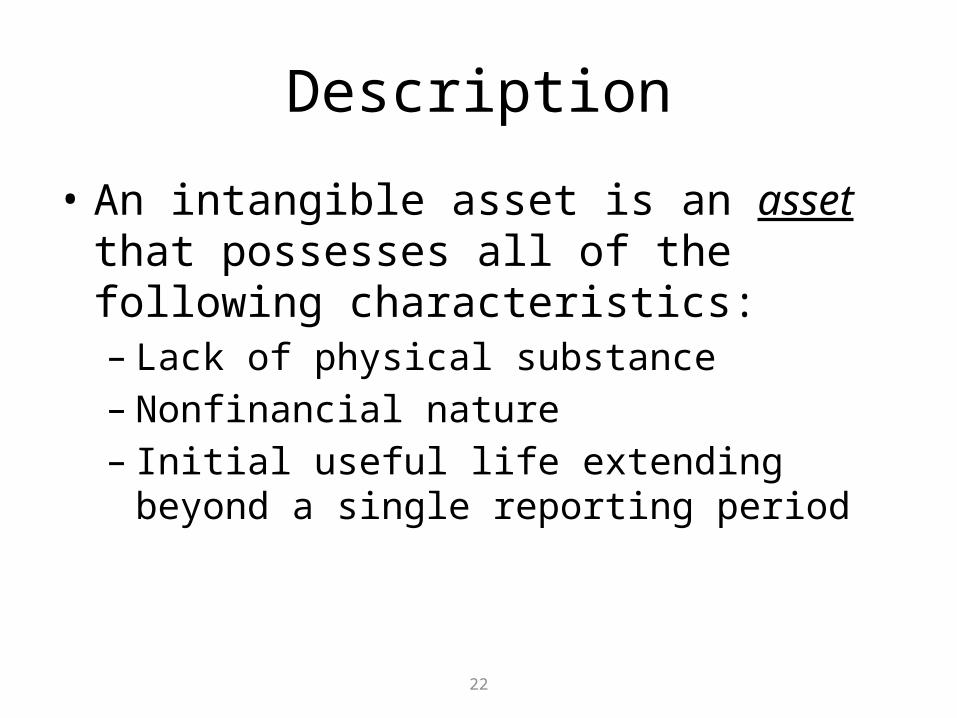

Description

• An intangible asset is an asset that possesses all of the following characteristics:– Lack of physical substance – Nonfinancial nature– Initial useful life extending beyond a single

reporting period

23

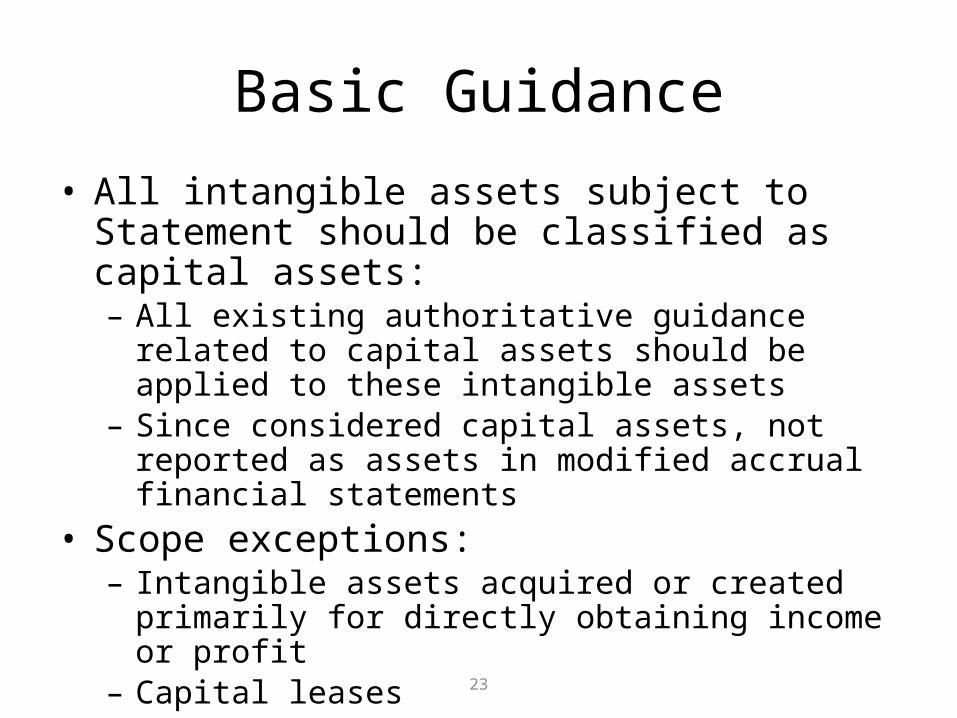

Basic Guidance

• All intangible assets subject to Statement should be classified as capital assets:– All existing authoritative guidance related to capital assets

should be applied to these intangible assets– Since considered capital assets, not reported as assets in

modified accrual financial statements• Scope exceptions: – Intangible assets acquired or created primarily for directly

obtaining income or profit– Capital leases– Goodwill from a combination transaction

24

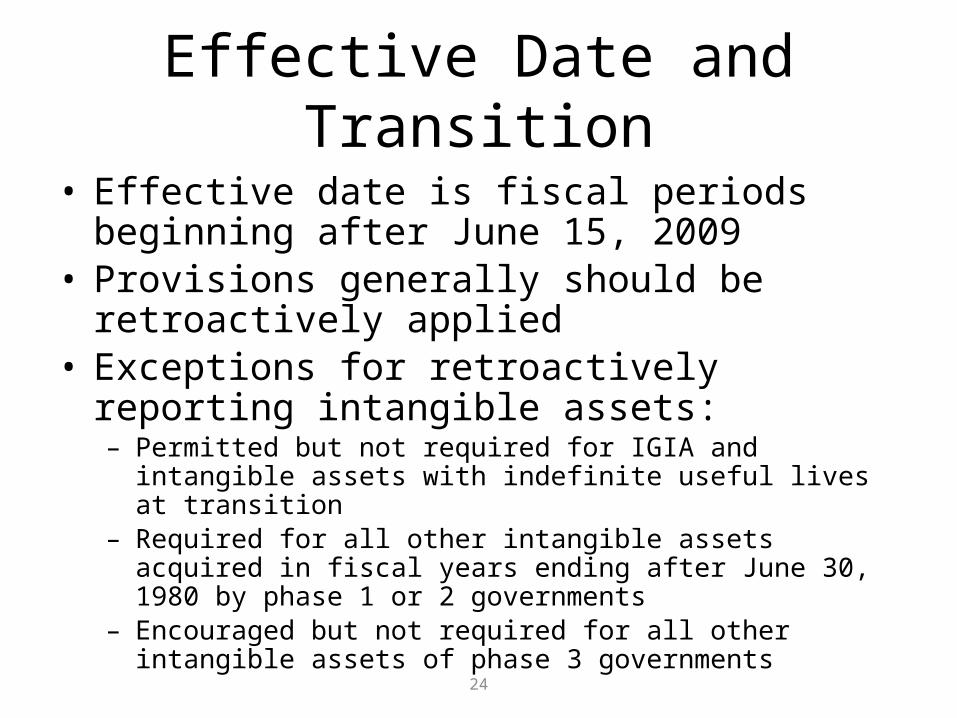

Effective Date and Transition

• Effective date is fiscal periods beginning after June 15, 2009

• Provisions generally should be retroactively applied• Exceptions for retroactively reporting intangible

assets:– Permitted but not required for IGIA and intangible assets with

indefinite useful lives at transition– Required for all other intangible assets acquired in fiscal years ending

after June 30, 1980 by phase 1 or 2 governments– Encouraged but not required for all other intangible assets of phase 3

governments

25

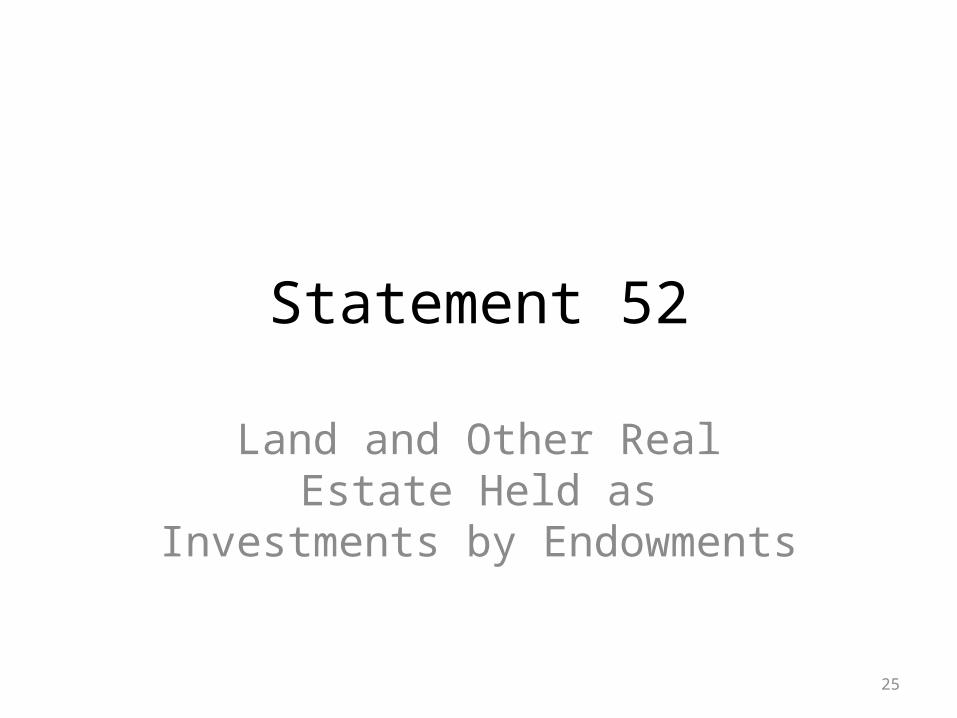

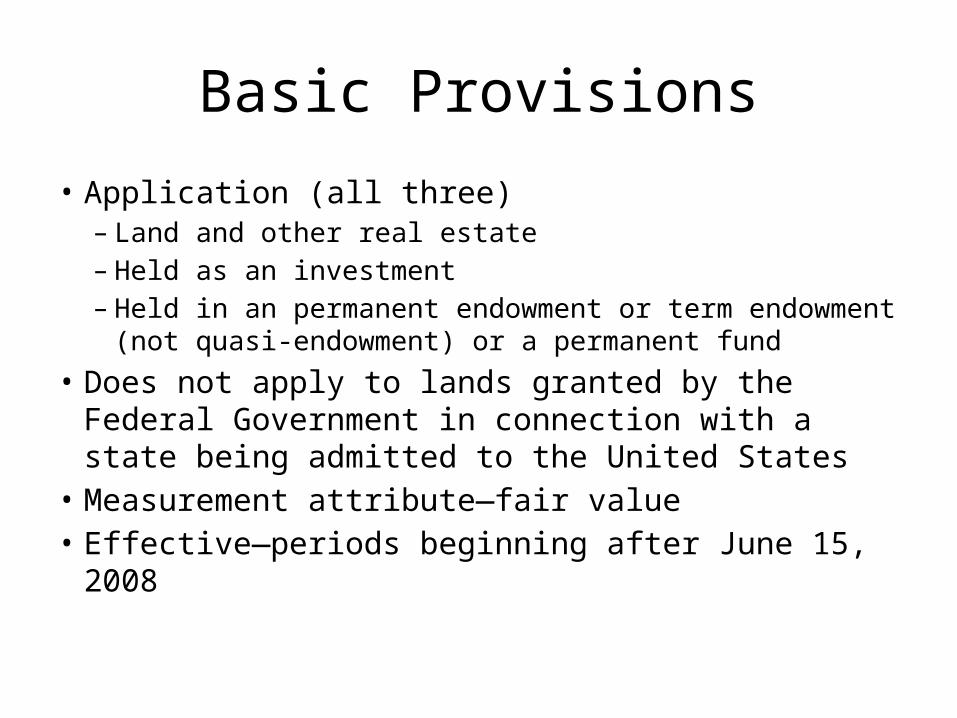

Statement 52

Land and Other Real Estate Held as Investments by Endowments

Basic Provisions

• Application (all three)– Land and other real estate– Held as an investment– Held in an permanent endowment or term endowment

(not quasi-endowment) or a permanent fund• Does not apply to lands granted by the Federal

Government in connection with a state being admitted to the United States

• Measurement attribute—fair value• Effective—periods beginning after June 15, 2008

27

Statement 53

Accounting and Financial Reporting for Derivative Instruments

28

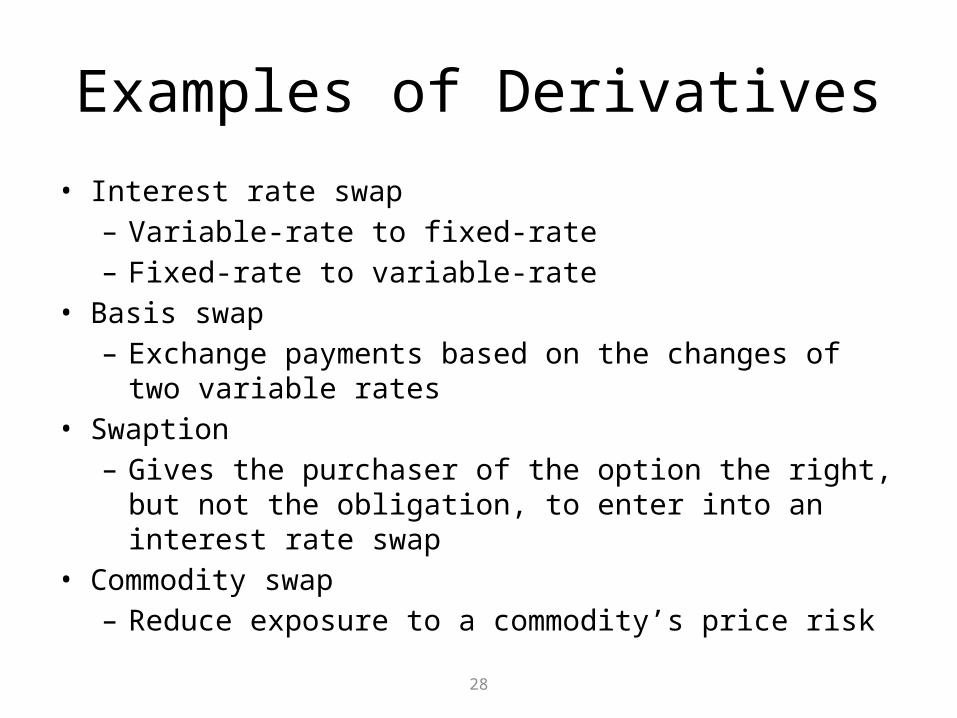

Examples of Derivatives

• Interest rate swap– Variable-rate to fixed-rate– Fixed-rate to variable-rate

• Basis swap– Exchange payments based on the changes of two variable

rates• Swaption– Gives the purchaser of the option the right, but not the

obligation, to enter into an interest rate swap• Commodity swap– Reduce exposure to a commodity’s price risk

29

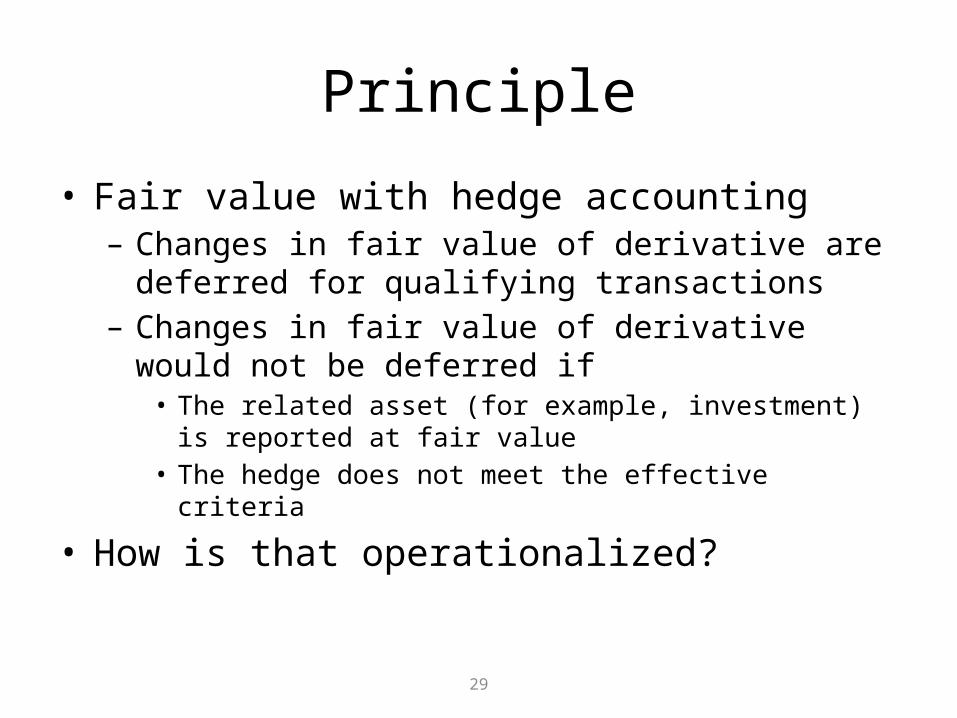

Principle

• Fair value with hedge accounting– Changes in fair value of derivative are deferred for

qualifying transactions– Changes in fair value of derivative would not be deferred if

• The related asset (for example, investment) is reported at fair value

• The hedge does not meet the effective criteria

• How is that operationalized?

30

Hedge Effectiveness

• Consistent critical terms• Quantitative techniques– Synthetic instrument– Dollar offset– Regression– Other qualifying quantitative methods

31

Effective Date and Transition

• Effective for financial periods beginning after June 15, 2009

• Implementation guide approved by the Board at the January 2009 meeting

32

Fund Balance Reporting and Governmental Fund Type Definitions

Statement 54

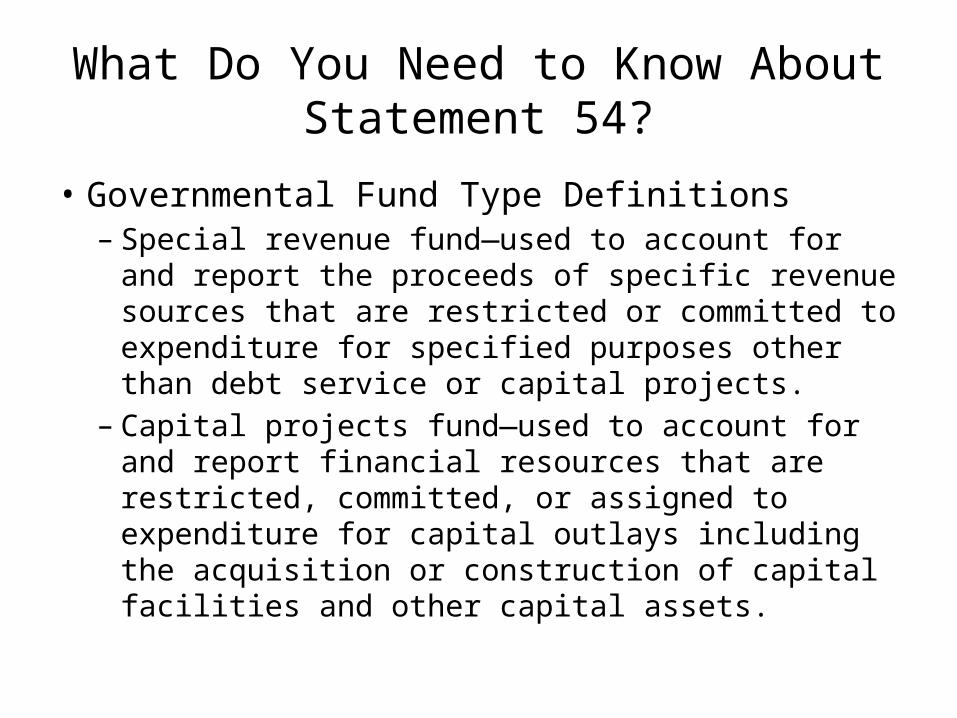

What Do You Need to Know About Statement 54?

• Fund Balance Reporting– Nonspendable– Restricted– Committed– Assigned– Unassigned

What Do You Need to Know About Statement 54?

• Governmental Fund Type Definitions– Special revenue fund—used to account for and report

the proceeds of specific revenue sources that are restricted or committed to expenditure for specified purposes other than debt service or capital projects.

– Capital projects fund—used to account for and report financial resources that are restricted, committed, or assigned to expenditure for capital outlays including the acquisition or construction of capital facilities and other capital assets.

35

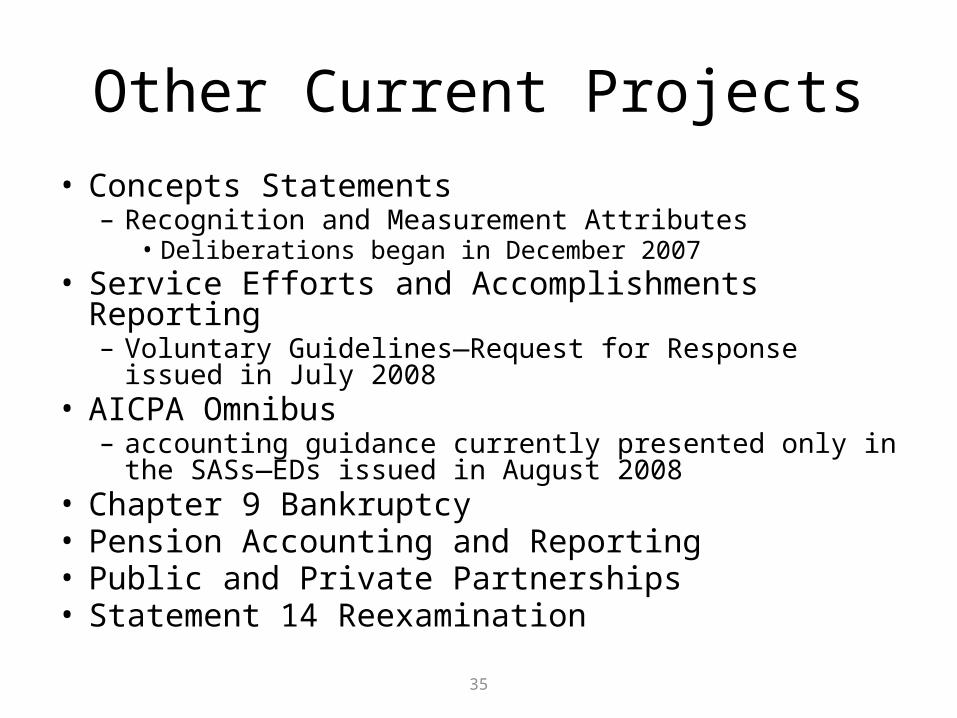

Other Current Projects• Concepts Statements

– Recognition and Measurement Attributes• Deliberations began in December 2007

• Service Efforts and Accomplishments Reporting– Voluntary Guidelines—Request for Response issued in July

2008 • AICPA Omnibus

– accounting guidance currently presented only in the SASs—EDs issued in August 2008

• Chapter 9 Bankruptcy • Pension Accounting and Reporting• Public and Private Partnerships• Statement 14 Reexamination

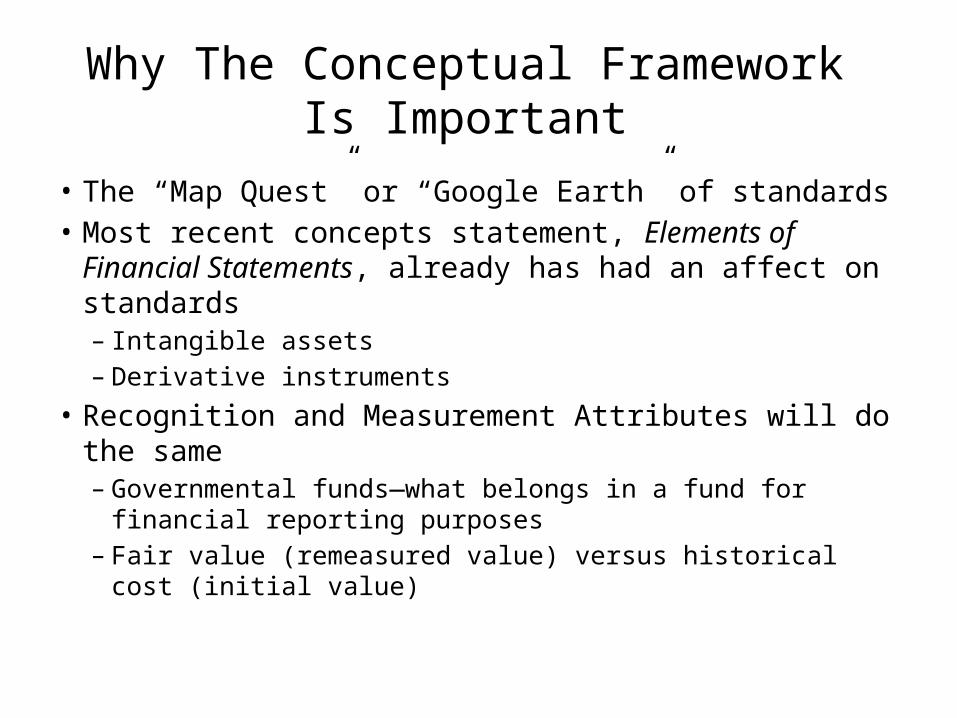

Why The Conceptual Framework Is Important

• The “Map Quest” or “Google Earth” of standards• Most recent concepts statement, Elements of Financial

Statements, already has had an affect on standards– Intangible assets– Derivative instruments

• Recognition and Measurement Attributes will do the same– Governmental funds—what belongs in a fund for financial

reporting purposes– Fair value (remeasured value) versus historical cost (initial

value)

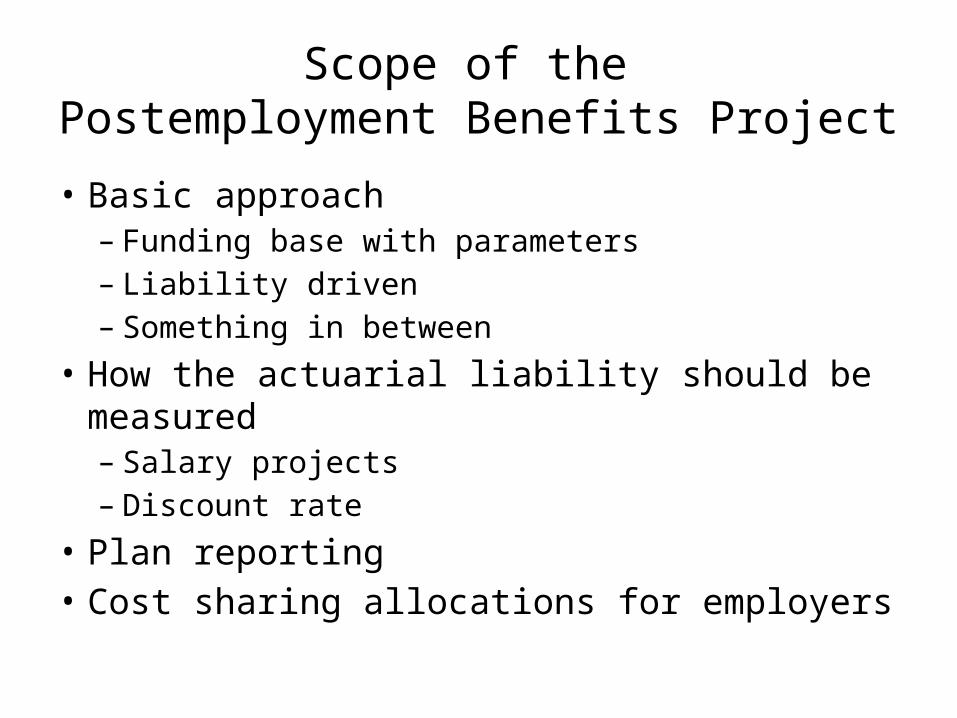

Scope of the Postemployment Benefits Project

• Basic approach– Funding base with parameters– Liability driven– Something in between

• How the actuarial liability should be measured– Salary projects– Discount rate

• Plan reporting• Cost sharing allocations for employers

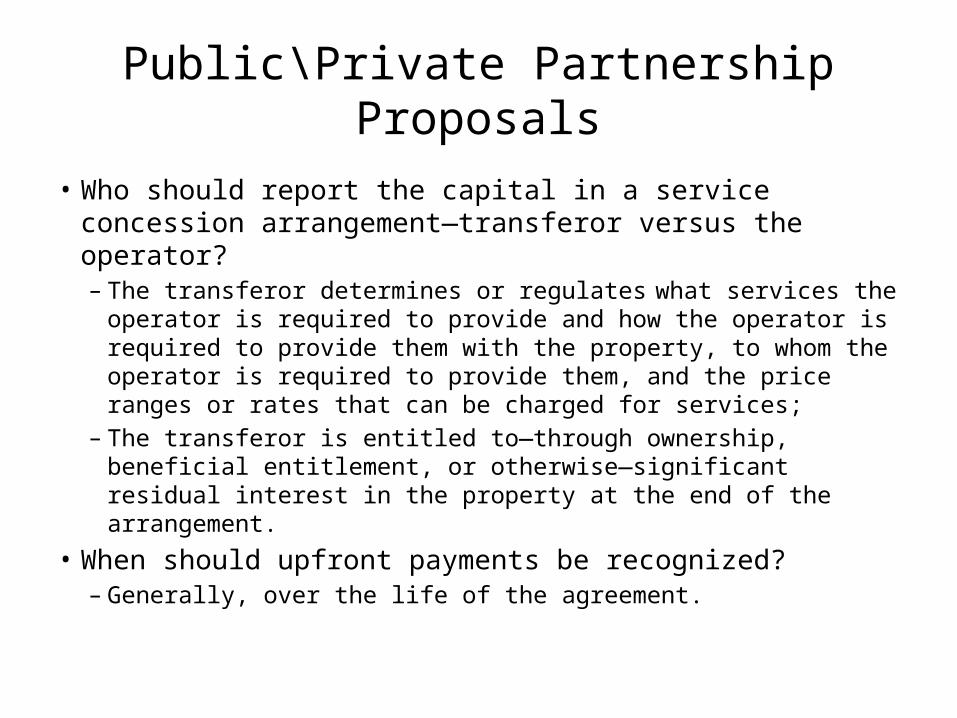

Public\Private Partnership Proposals

• Who should report the capital in a service concession arrangement—transferor versus the operator?– The transferor determines or regulates what services the

operator is required to provide and how the operator is required to provide them with the property, to whom the operator is required to provide them, and the price ranges or rates that can be charged for services;

– The transferor is entitled to—through ownership, beneficial entitlement, or otherwise—significant residual interest in the property at the end of the arrangement.

• When should upfront payments be recognized?– Generally, over the life of the agreement.

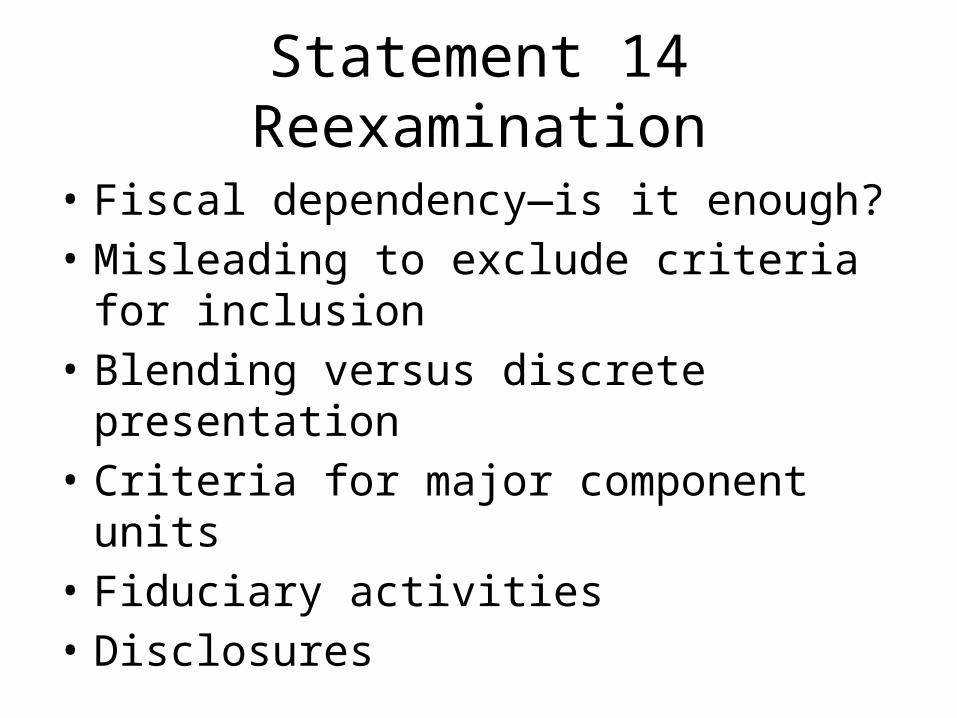

Statement 14 Reexamination

• Fiscal dependency—is it enough?• Misleading to exclude criteria for inclusion• Blending versus discrete presentation• Criteria for major component units• Fiduciary activities• Disclosures

40

Other Projects

41

Research Agenda

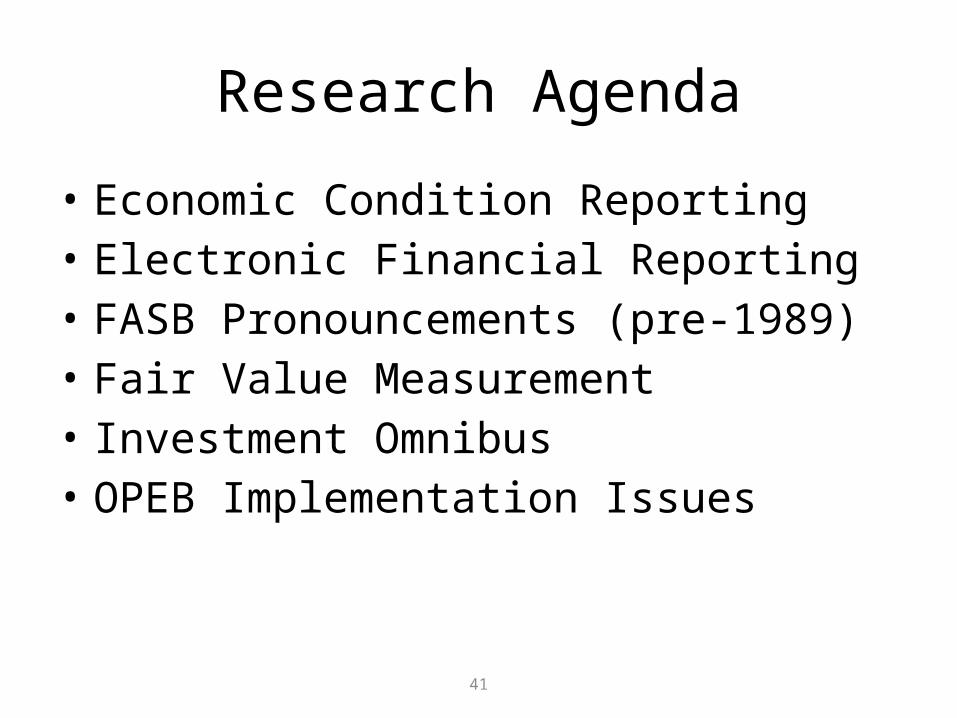

• Economic Condition Reporting• Electronic Financial Reporting• FASB Pronouncements (pre-1989)• Fair Value Measurement• Investment Omnibus• OPEB Implementation Issues

42

Calling All Issues

• Agenda is full; however, emerging issues still need to be addressed– GASB is not fishing for issues

• If you have identified an issue that you believe warrants the GASB’s attention, please submit that issue via email to [email protected]

• Agenda reviewed three times a year the GASB

43

Questions?

Telephone—(203) 847-0700Web site—www.gasb.org

Related Documents