icfi.com/aviation | BUSINESS AVIATION OUTLOOK 18 March 2014 Prepared for: Revised: 11 March am

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

0 icfi.com/aviation |

BUSINESS AVIATION OUTLOOK

18 March 2014

Prepared for:

Revised: 11 March am

1 icfi.com/aviation |

Agenda

North American Business & General Aviation

Market Trends

Outlook for Recovery

Market Structure

Cyclical vs. Structural Factors

Independent Forecast

2 icfi.com/aviation |

Highlights

Revenue focus on North America 1 Trends were skewed by the fractional bubble 2

Performance is a tale of two markets 3 Fundamentals remain fundamental 4

Business investment is a key driver 5 The forecast is for recovery 6

3 icfi.com/aviation | 3

MARKET OVERVIEW

4 icfi.com/aviation |

North America drives worldwide FBO revenue

Source: ACAS, FAA, AirNav, ICF SH&E Analysis, EIA – November 2012

$7.26 $6.90 $6.05

$2.93

1 FBO 2 FBOs 3+ FBOs Spot Price

Jet A Retail Prices

63% of global fleet

Prices at Airports With…

1 FBO 2 FBOs 3+ FBOs

FBO Premium

Fuel model generates FBO revenue

4 million movements per year

North America Business Aviation

+Costs

5 icfi.com/aviation |

Large aircraft drive the fuel revenue

Movements vs. Fuel

18%

41%

28%

39%

54%

20%

0%

100%

Operations Fuel

Source: ACAS, Conklin Aircraft Cost Evaluator, ICF SH&E Analysis

Notes: Large Cabin shown as G550 (2.52FH/FC); Midsize shown as Challenger 300 (1.61FH/FC); Small jet shown as Citation II (1.27FH/FC)

Share of N. America

Large Cabin 200,000 gallons/year

Midsize 125,000 gallons/year

Small Jet 83,000 gallons/year

6 icfi.com/aviation |

$0

$5

$10

$15

$20

$25

0

250

500

750

1,000

1990 1995 2000 2005 2010

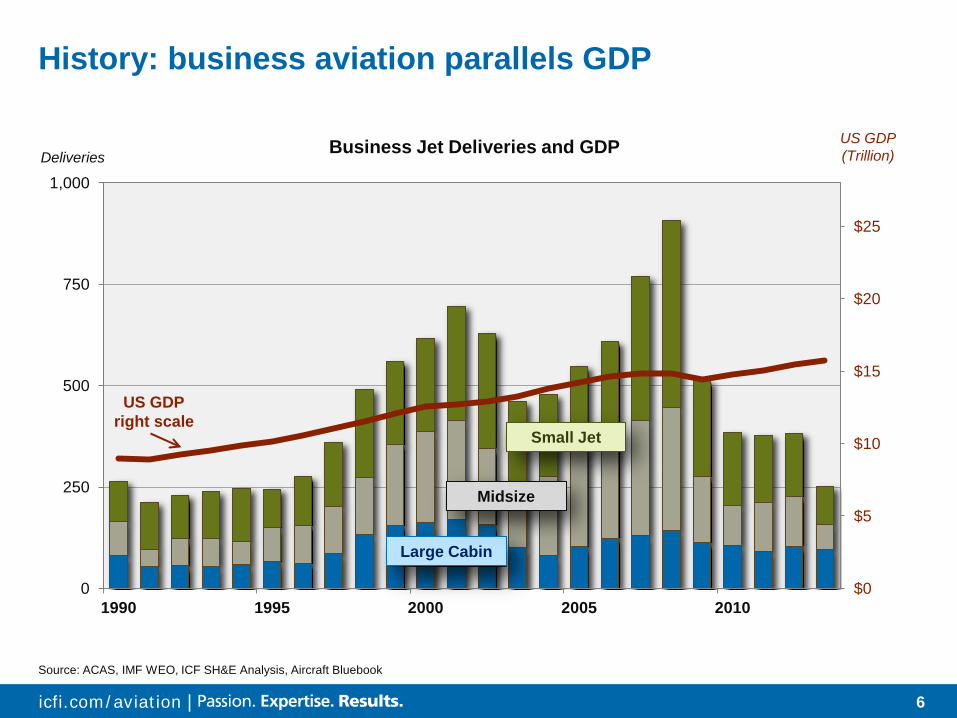

History: business aviation parallels GDP

US GDP (Trillion)

US GDP right scale

Large Cabin

Midsize

Small Jet

Source: ACAS, IMF WEO, ICF SH&E Analysis, Aircraft Bluebook

Business Jet Deliveries and GDP Deliveries

7 icfi.com/aviation |

…with 2 recent bubbles

$0

$5

$10

$15

$20

$25

0

250

500

750

1,000

1990 1995 2000 2005 2010

US GDP (Trillion)

US GDP right scale

Large Cabin

Midsize

Small Jet

Source: ACAS, IMF WEO, ICF SH&E Analysis, Aircraft Bluebook

Business Jet Deliveries and GDP Deliveries

Fractional Bubble

FinancingBubble

8 icfi.com/aviation |

0

2,000

4,000

6,000

8,000

10,000

12,000

0

250

500

750

1,000

1990 1995 2000 2005 2010

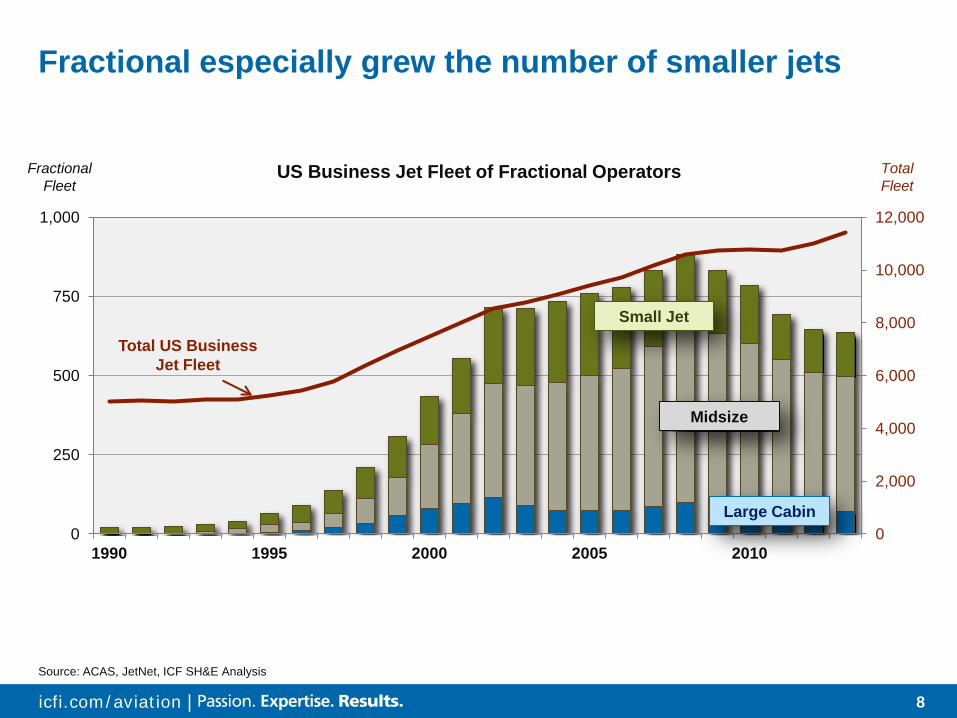

Fractional especially grew the number of smaller jets

Source: ACAS, JetNet, ICF SH&E Analysis

Fractional Fleet

US Business Jet Fleet of Fractional Operators

Large Cabin

Midsize

Small Jet

Total Fleet

Total US Business Jet Fleet

9 icfi.com/aviation |

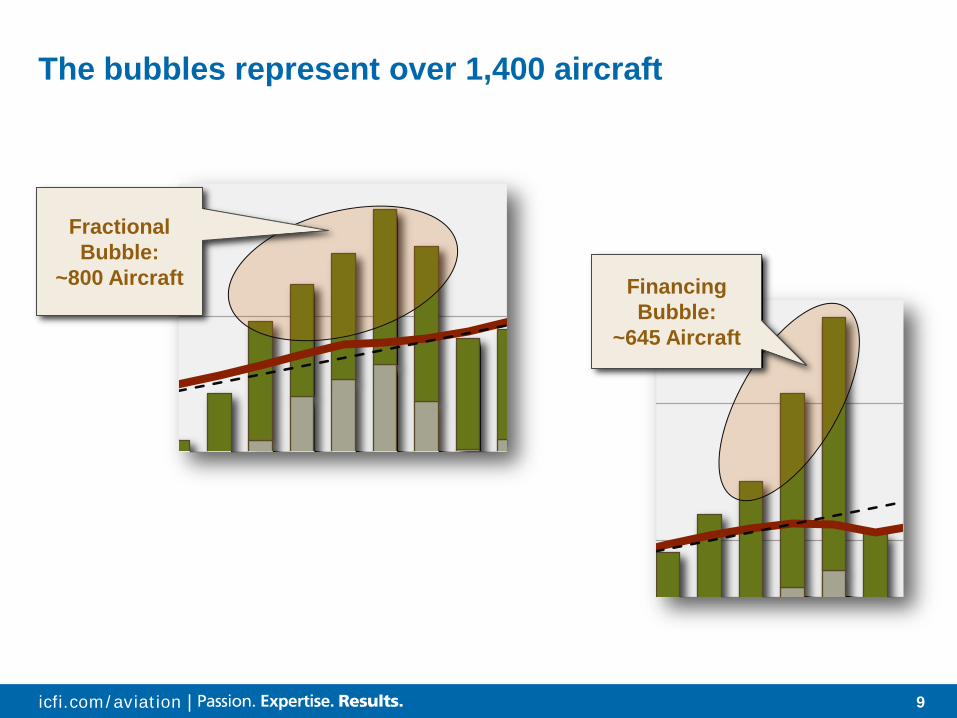

Fractional Bubble:

~800 Aircraft Financing Bubble:

~645 Aircraft

The bubbles represent over 1,400 aircraft

10 icfi.com/aviation |

The fractional model is evolving

Fractional disruption as OEMs question value and independents struggle

• Bombardier Flexjet sold to owner of Flight Options • Cessna (CitationShares) exits • Avantair exits

Underlying demand moves into other branded charter • Operated by the traditional fractionals • Or new ventures, such as VistaJet, XOJet

Weaker fractionals reduces operator concentration and reduces their pricing power

11 icfi.com/aviation |

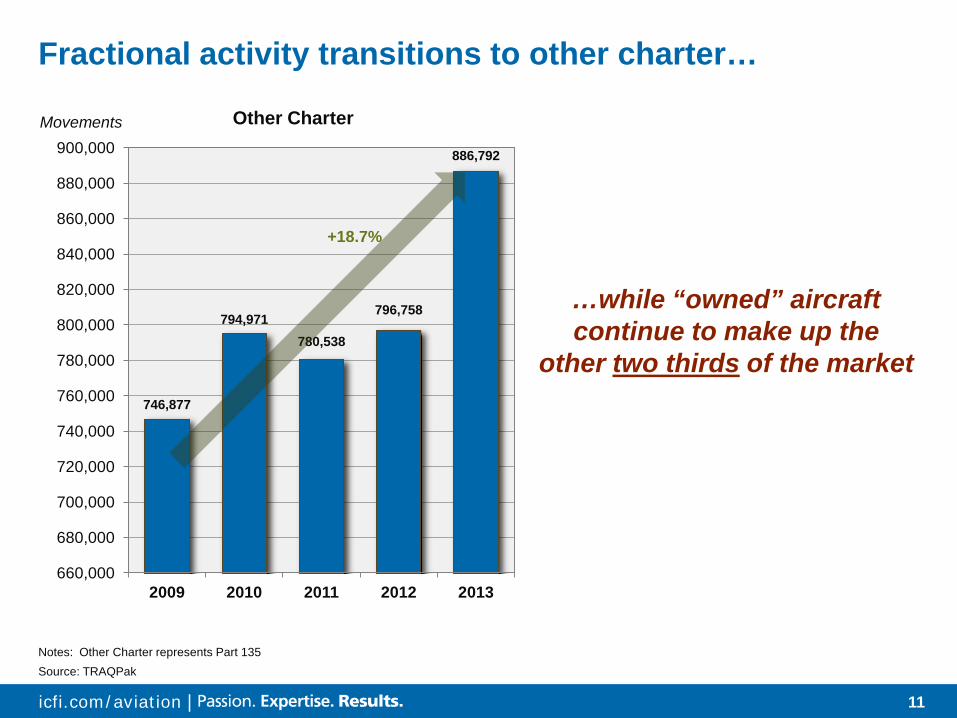

Fractional activity transitions to other charter…

746,877

794,971 780,538

796,758

886,792

660,000

680,000

700,000

720,000

740,000

760,000

780,000

800,000

820,000

840,000

860,000

880,000

900,000

2009 2010 2011 2012 2013

+18.7%

Other Charter

Source: TRAQPak Notes: Other Charter represents Part 135

…while “owned” aircraft continue to make up the

other two thirds of the market

Movements

12 icfi.com/aviation | 12

TRENDS

13 icfi.com/aviation |

Flight movements have recently started to turn up

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Monthly Business Jet Movements

Source: FAA

Percent Change y/y

14 icfi.com/aviation |

Large cabin movements dipped less and recovered faster

70

80

90

100

110

2008 2009 2010 2011 2012 2013

Large Cabin

Midsize

Source: FAA

Small Jet

Index: 2008 = 100 Annual Business Jet Movements

15 icfi.com/aviation |

New deliveries down while value goes up = bigger planes

$0

$5

$10

$15

$20

$25

$30

$35

0

200

400

600

800

1,000

1,200

1,400

1994 1998 2002 2006 2010

Units Delivered

Average Aircraft Value ($US Million)

5-Year CAGR

Delivery value increasing 13.3% per

year

Delivery volume down

12.2% per year

Global Business Jets Deliveries

Source: GAMA, ICF SH&E Analysis

16 icfi.com/aviation | 16

OUTLOOK

17 icfi.com/aviation |

Flight

Business Aviation has a meaningful value to the user

Even when the flight times are the same…

Hour Check-In

Security Theatre

Boarding Zoo Flight

Home to Plane-side

Meeting

Meeting Wait for Flight Home

…the experience isn’t

18 icfi.com/aviation |

Airline consolidation cuts service to smaller airports

Source: MIT Small Community Air Service White Paper

0

20

40

60

80

100

120

Large Airport Medium Airport Small Airport

Declining Airport Connectivity

Notes: ACQI Score for Large , Medium and Small Airports (Indexed to 2007).

ACQI Index 2007 = 100

-4%

-16% -11%

19 icfi.com/aviation |

Private aviation, like other travel, correlates to GDP

$0

$5

$10

$15

$20

0

5,000

10,000

15,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Aircraft GDP

Trillion

Note: Does not include Russian-manufactured aircraft

Source: ACAS, IMF WEO, ICF SH&E Analysis

Business Jet Fleet and GDP North America

Aircraft

GDP

Correlation: 98.8%

Elasticity: 1.96 Elasticity: 1.34 Elasticity: 1.76

20 icfi.com/aviation |

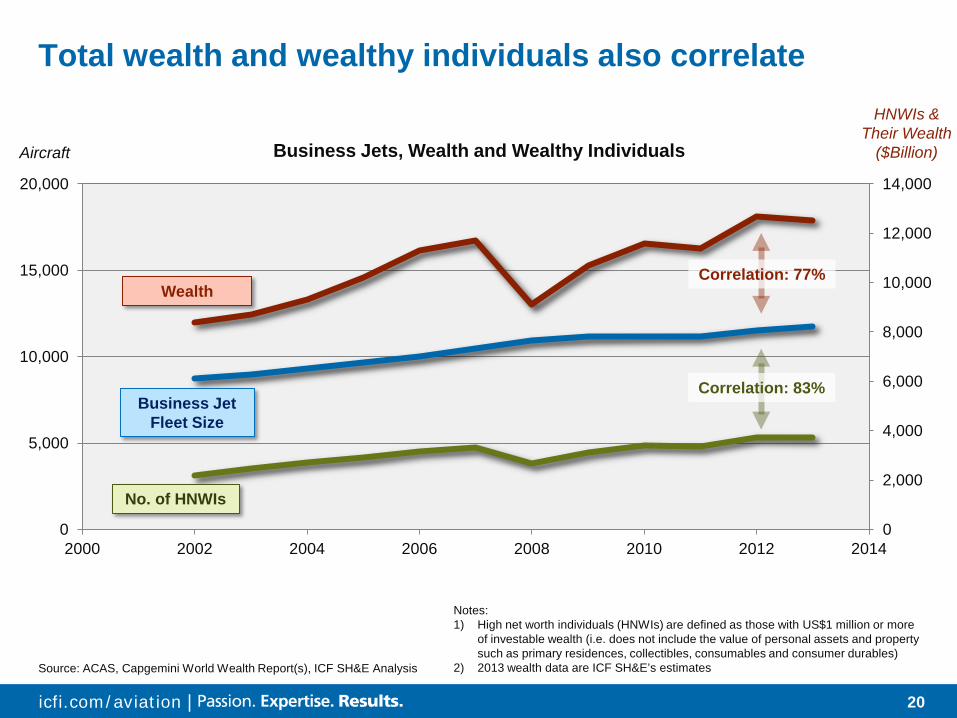

Total wealth and wealthy individuals also correlate

0

5,000

10,000

15,000

20,000

2000 2002 2004 2006 2008 2010 2012 2014 0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Aircraft

HNWIs & Their Wealth

($Billion)

Source: ACAS, Capgemini World Wealth Report(s), ICF SH&E Analysis

Wealth

Business Jet Fleet Size

No. of HNWIs

Notes: 1) High net worth individuals (HNWIs) are defined as those with US$1 million or more

of investable wealth (i.e. does not include the value of personal assets and property such as primary residences, collectibles, consumables and consumer durables)

2) 2013 wealth data are ICF SH&E’s estimates

Business Jets, Wealth and Wealthy Individuals

Correlation: 77%

Correlation: 83%

21 icfi.com/aviation |

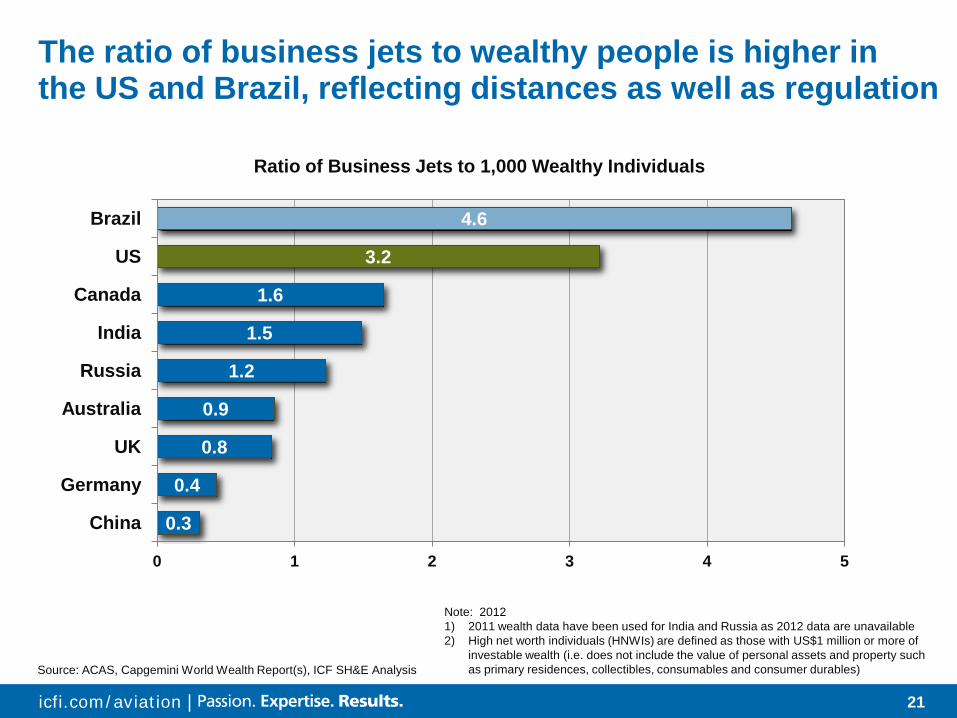

The ratio of business jets to wealthy people is higher in the US and Brazil, reflecting distances as well as regulation

0.3

0.4

0.8

0.9

1.2

1.5

1.6

3.2

4.6

0 1 2 3 4 5

China

Germany

UK

Australia

Russia

India

Canada

US

Brazil

Note: 2012 1) 2011 wealth data have been used for India and Russia as 2012 data are unavailable 2) High net worth individuals (HNWIs) are defined as those with US$1 million or more of

investable wealth (i.e. does not include the value of personal assets and property such as primary residences, collectibles, consumables and consumer durables) Source: ACAS, Capgemini World Wealth Report(s), ICF SH&E Analysis

Ratio of Business Jets to 1,000 Wealthy Individuals

22 icfi.com/aviation |

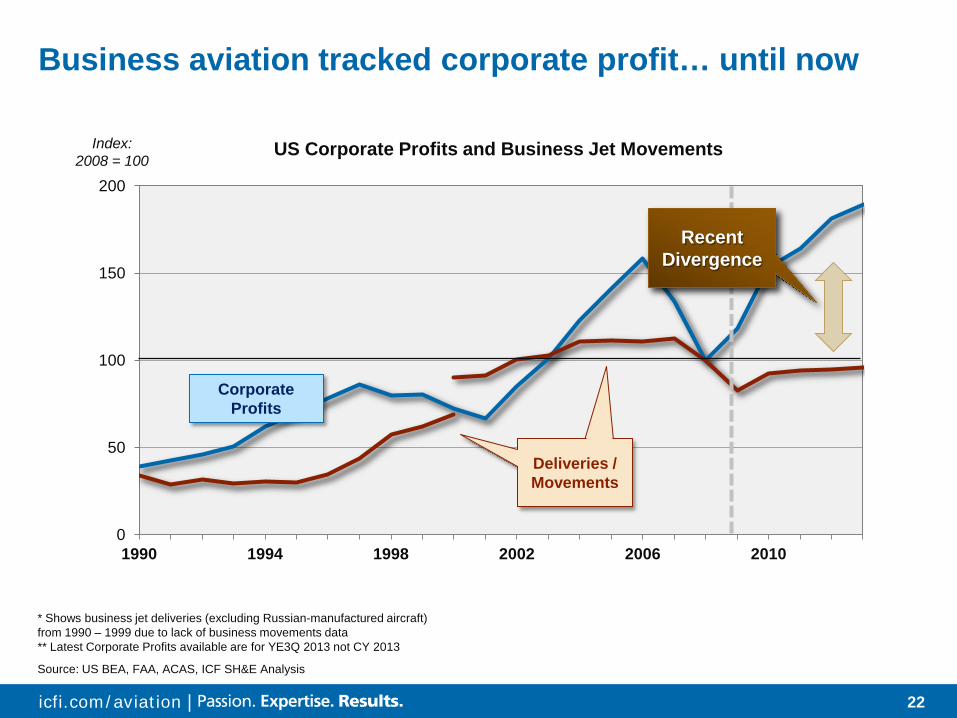

Business aviation tracked corporate profit… until now

Source: US BEA, FAA, ACAS, ICF SH&E Analysis

0

50

100

150

200

1990 1994 1998 2002 2006 2010

Index: 2008 = 100

Corporate Profits

US Corporate Profits and Business Jet Movements

Recent Divergence

* Shows business jet deliveries (excluding Russian-manufactured aircraft) from 1990 – 1999 due to lack of business movements data ** Latest Corporate Profits available are for YE3Q 2013 not CY 2013

Deliveries / Movements

23 icfi.com/aviation |

The more important measure is corporate investment

* Shows business jet deliveries (excluding Russian-manufactured aircraft) from 1990 – 1999 due to lack of business movements data

Note: US Net Non-Residential Fixed Investments (NNRFI) Source: US BEA, ACAS, FAA, ICF SH&E Analysis

0

50

100

150

1990 1994 1998 2002 2006 2010

Total Business Jet Deliveries / Movements*

US Net Non-Residential Fixed Investments

Index: 2008 = 100

Correlation: 74%

Business Investment and Business Jet Movements

Correlates during recovery with

1-year lag

24 icfi.com/aviation |

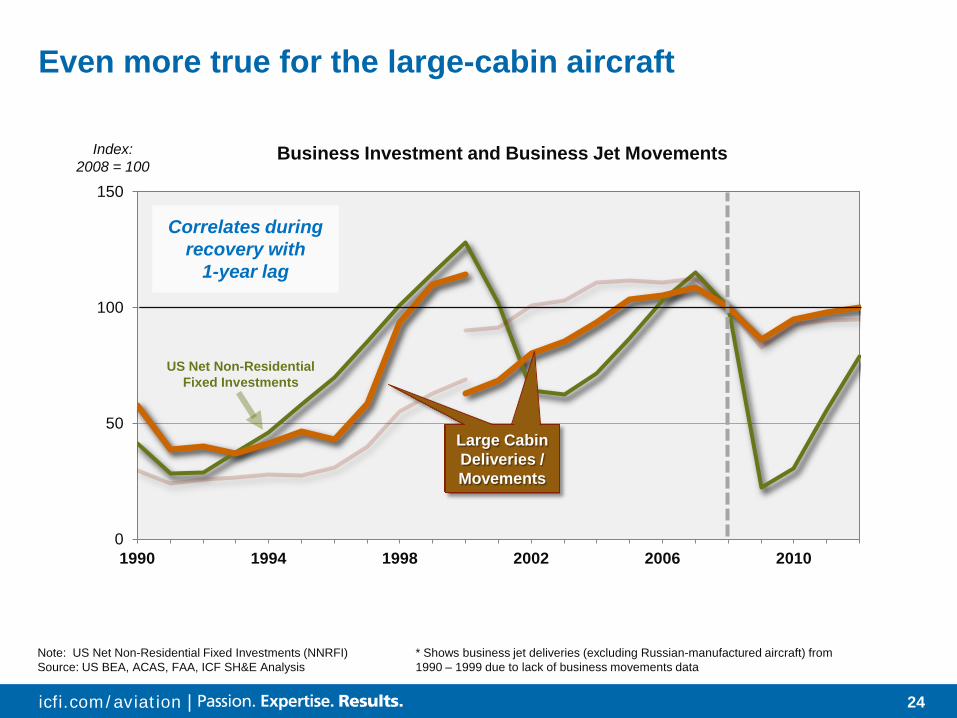

Even more true for the large-cabin aircraft

0

50

100

150

1990 1994 1998 2002 2006 2010

Index: 2008 = 100

Business Investment and Business Jet Movements

US Net Non-Residential Fixed Investments

Correlates during recovery with

1-year lag

* Shows business jet deliveries (excluding Russian-manufactured aircraft) from 1990 – 1999 due to lack of business movements data

Note: US Net Non-Residential Fixed Investments (NNRFI) Source: US BEA, ACAS, FAA, ICF SH&E Analysis

Large Cabin Deliveries / Movements

25 icfi.com/aviation |

Corporations have hoarded cash rather than investing

Source: Compustat and Goldman Sachs Global ECS Research

26 icfi.com/aviation |

US industry is becoming less capital-intensive

Services require less capital than manufacturing

But offshore manufacturing will slow as transport and foreign labor costs rise while US energy prices fall

Trend continues

but slowing

Capital Intensity of US Corporate Profits

Source: Haver/OEF/UBS estimates, Zerohedge

27 icfi.com/aviation |

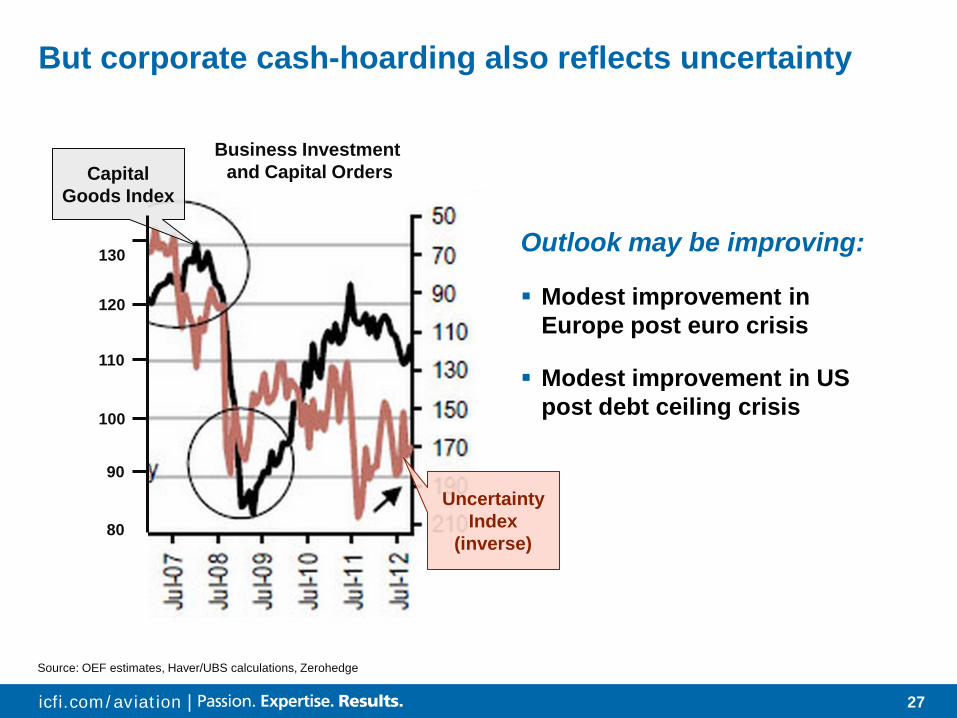

But corporate cash-hoarding also reflects uncertainty

Business Investment and Capital Orders Capital

Goods Index

Uncertainty Index

(inverse) 80

90

100

110

120

130 Outlook may be improving:

Modest improvement in Europe post euro crisis

Modest improvement in US post debt ceiling crisis

Source: OEF estimates, Haver/UBS calculations, Zerohedge

28 icfi.com/aviation | 28

FORECAST

29 icfi.com/aviation |

GDP Growth • Near term (2012 – 2018) 2.8% - Oxford (EIU same; IMF 2.9%) • Longer term (2018 – 2023) 2.7% - Oxford

High Net Worth Individuals: 4.5% growth is the trend based on relationships to GDP from 2001 to 2012

Corporate Profits: 9.1% growth is average of past 3 economic cycles

Business Investment: 2.1% of GDP is current level; 3% of GDP is past 3 recovery cycles

The forecast is based on key drivers of business aviation

30 icfi.com/aviation |

The base case assumes continuation of current trends

Scenario GDP HNWI Corp Profits Corp

Investment

2012-2018 2018-2023 2012-2023 2012-2023 2013-2023

Base 2.8% 2.7% 4.5% 9.1% 2.1% of GDP

31 icfi.com/aviation |

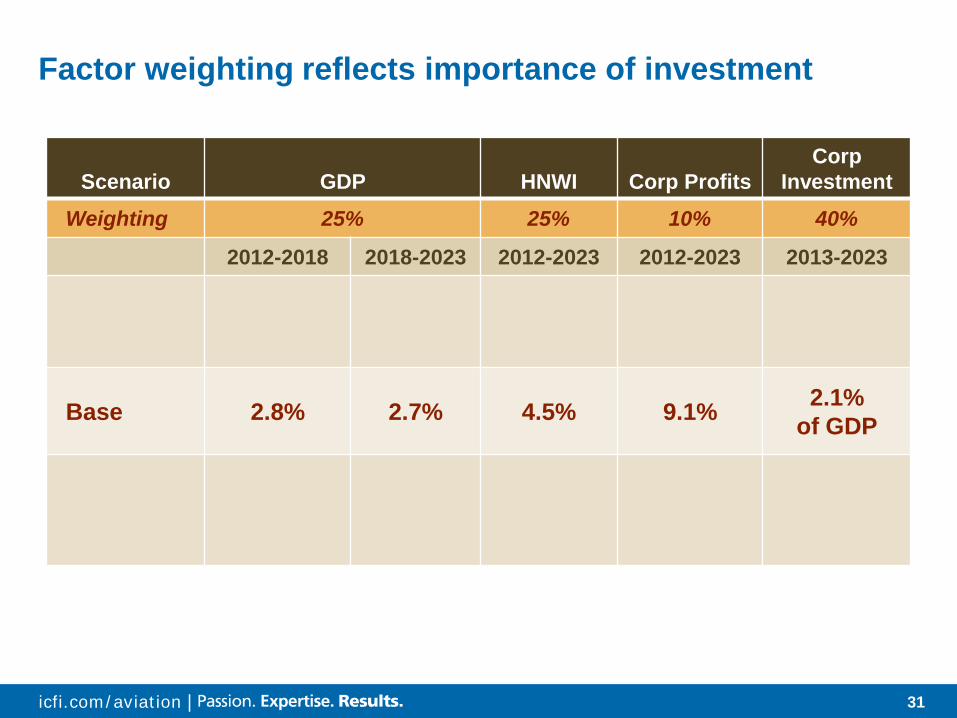

Factor weighting reflects importance of investment

Scenario GDP HNWI Corp Profits Corp

Investment

Weighting 25% 25% 10% 40%

2012-2018 2018-2023 2012-2023 2012-2023 2013-2023

Base 2.8% 2.7% 4.5% 9.1% 2.1% of GDP

32 icfi.com/aviation |

Base Case: 4.2% growth

Source: Oxford Economics, FAA, ACAS, Capgemini, BEA, ICF SH&E Analysis

3

4

5

6

7

2012 2013E 2014F 2015F 2016F 2017F 2018F 2019F 2020F 2021F 2022F 2023F

Million Movements

Forecast of Business Jet Movements

Forecast

Base 2012 – 2023 Growth: 4.2%

2018: 5.2 million movements

33 icfi.com/aviation |

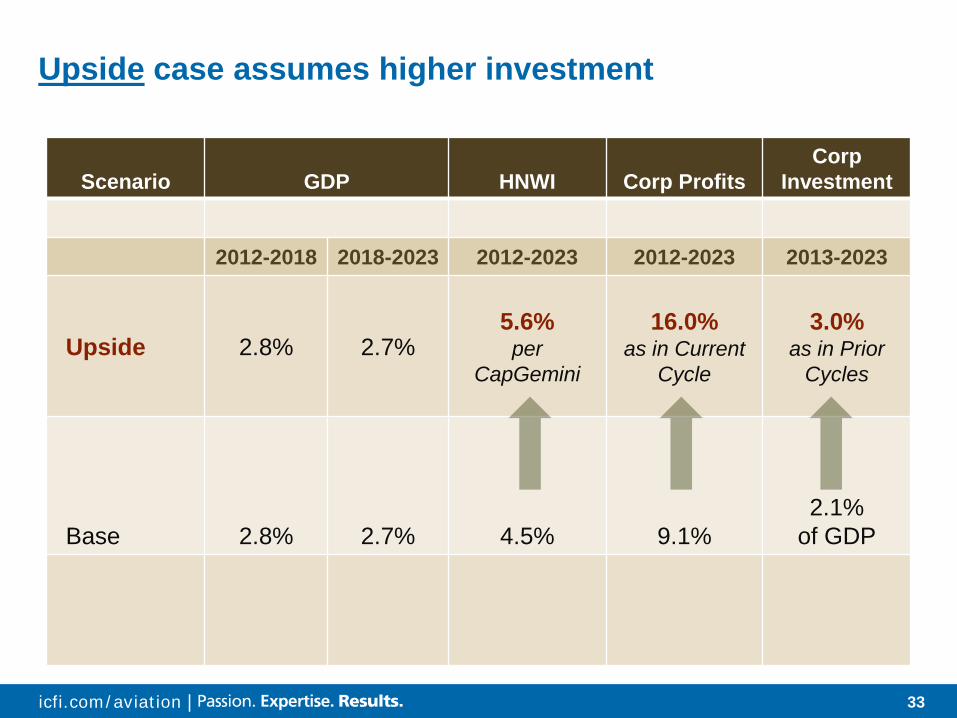

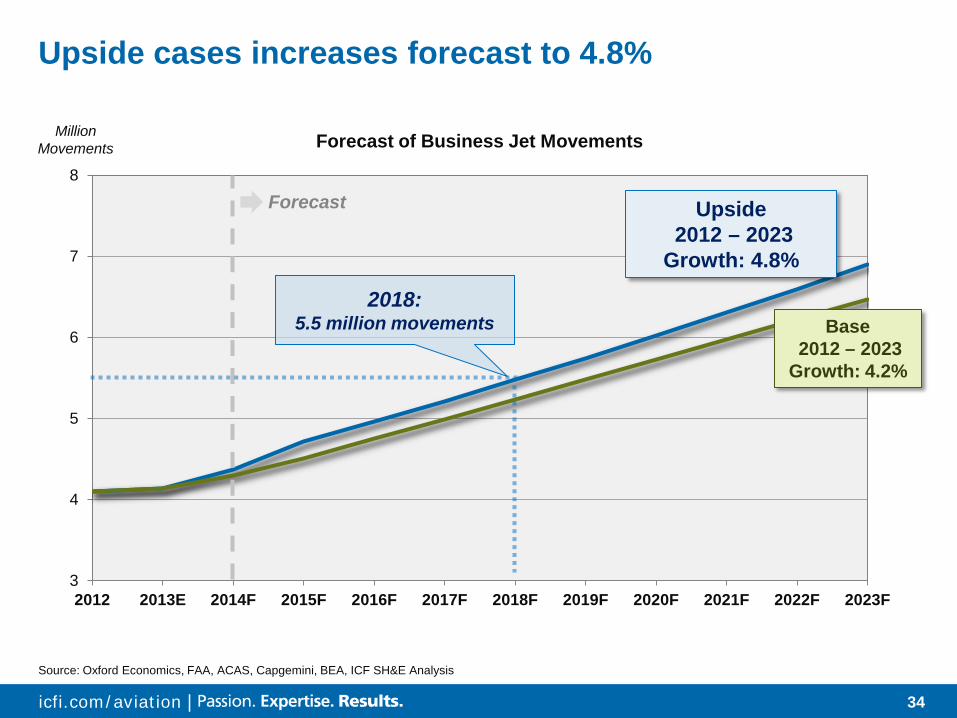

Upside case assumes higher investment

Scenario GDP HNWI Corp Profits Corp

Investment

2012-2018 2018-2023 2012-2023 2012-2023 2013-2023

Upside 2.8% 2.7% 5.6%

per CapGemini

16.0% as in Current

Cycle

3.0% as in Prior

Cycles

Base 2.8% 2.7% 4.5% 9.1% 2.1%

of GDP

34 icfi.com/aviation |

Upside cases increases forecast to 4.8%

Source: Oxford Economics, FAA, ACAS, Capgemini, BEA, ICF SH&E Analysis

3

4

5

6

7

8

2012 2013E 2014F 2015F 2016F 2017F 2018F 2019F 2020F 2021F 2022F 2023F

Million Movements Forecast of Business Jet Movements

Forecast Upside 2012 – 2023 Growth: 4.8%

Base 2012 – 2023 Growth: 4.2%

2018: 5.5 million movements

35 icfi.com/aviation |

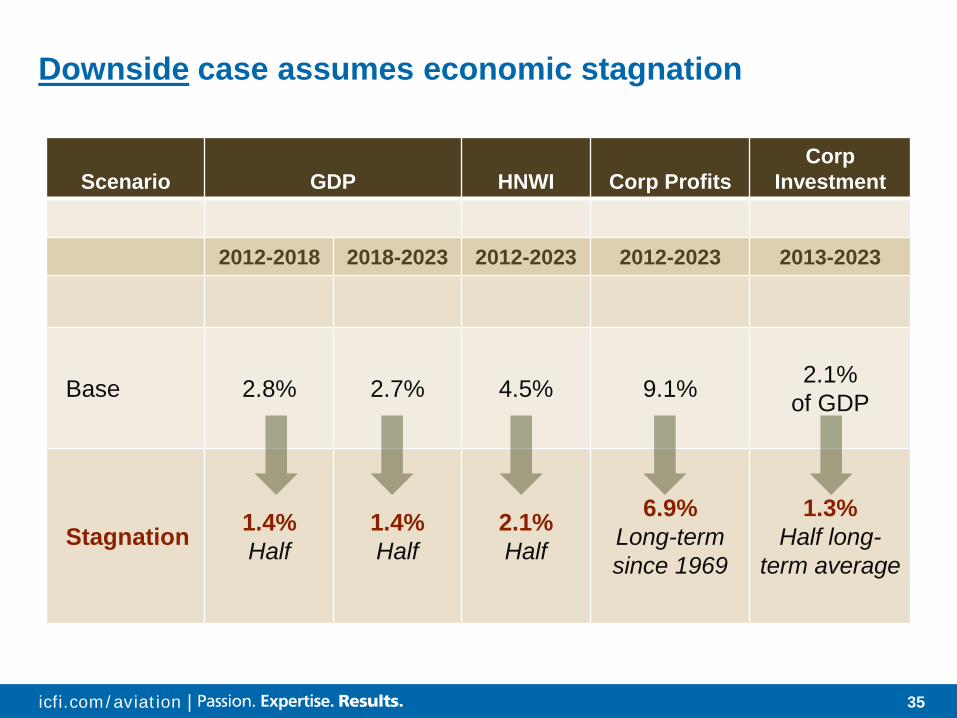

Downside case assumes economic stagnation

Scenario GDP HNWI Corp Profits Corp

Investment

2012-2018 2018-2023 2012-2023 2012-2023 2013-2023

Base 2.8% 2.7% 4.5% 9.1% 2.1% of GDP

Stagnation 1.4% Half

1.4% Half

2.1% Half

6.9% Long-term since 1969

1.3% Half long-

term average

36 icfi.com/aviation |

Stagnation Case: 2.1% growth

Source: Oxford Economics, FAA, ACAS, Capgemini, BEA, ICF SH&E Analysis

3

4

5

6

7

8

2012 2013E 2014F 2015F 2016F 2017F 2018F 2019F 2020F 2021F 2022F 2023F

Million Movements Forecast of Business Jet Movements

Forecast

Stagnation 2012 – 2023

Growth: 2.1%

Base 2012 – 2023 Growth: 4.2%

2018: 4.6 million movements

37 icfi.com/aviation |

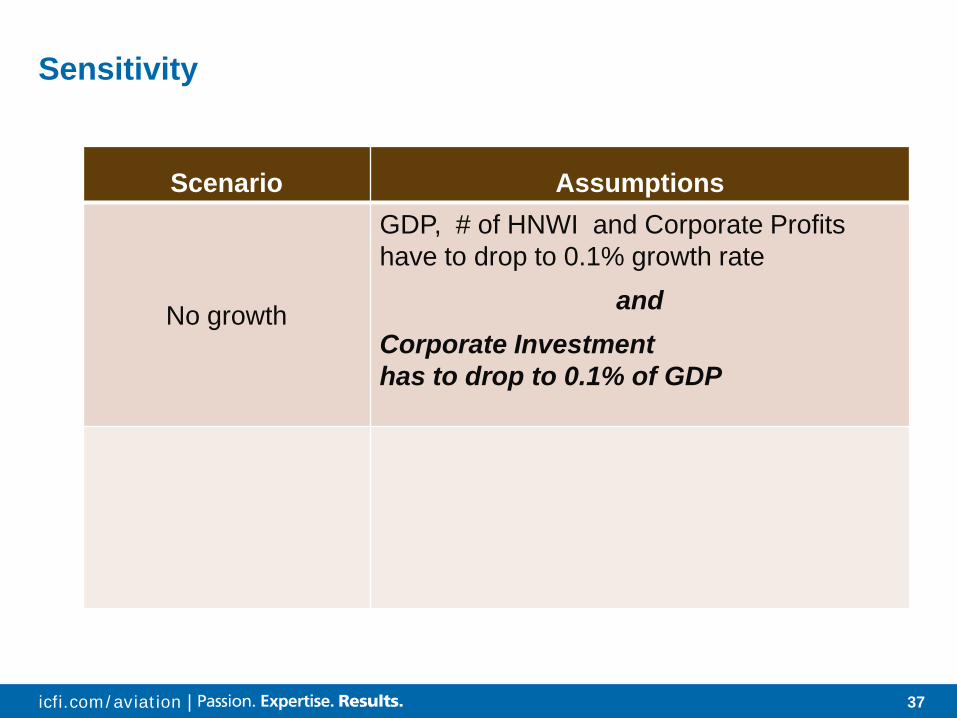

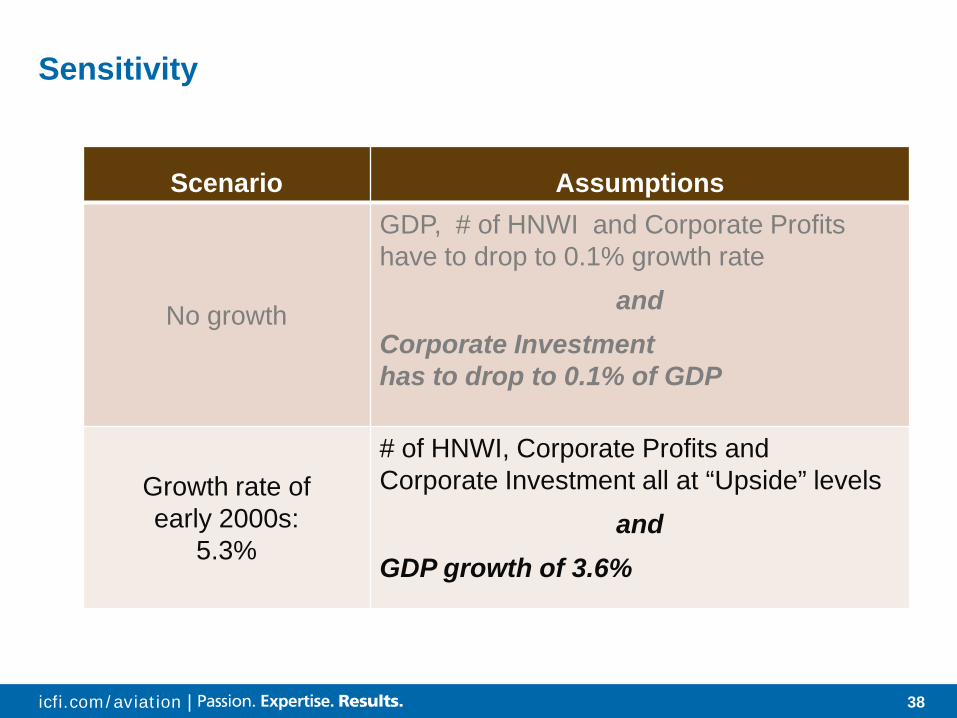

Sensitivity

Scenario Assumptions

No growth

GDP, # of HNWI and Corporate Profits have to drop to 0.1% growth rate

and Corporate Investment has to drop to 0.1% of GDP

38 icfi.com/aviation |

Sensitivity

Scenario Assumptions

No growth

GDP, # of HNWI and Corporate Profits have to drop to 0.1% growth rate

and Corporate Investment has to drop to 0.1% of GDP

Growth rate of early 2000s:

5.3%

# of HNWI, Corporate Profits and Corporate Investment all at “Upside” levels

and GDP growth of 3.6%

39 icfi.com/aviation |

Recap

Revenue focus on North America 1 Trends were skewed by the fractional bubble 2

Performance is a tale of two markets 3 Fundamentals remain fundamental 4

Business investment is a key driver 5 The forecast is for recovery 6

40 icfi.com/aviation |

Related Documents