RESEARCH HOW BANKS ARE DEALING WITH THE ROAD TO RECOVERY JULY 2009

Bnp Paribas Real Estate Recovery Survey Of Banks Final

Jul 31, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

RESEARCH

HOW BANKS ARE DEALING WITH THE ROAD TO RECOVERY

JULY 2009

Recovery Report – July 2009

How ARE bAnkS Coping witH tHAt dEgREE of ExpoSuRE to CollApSEd vAluES? Some comfort for banks is provided by the margin between the loan made and the value of the building. Banks typically restrict the loan-to-value (LTV) when lending, to control the exposure to the borrower and the market.

In 2003 the average maximum LTV was 78% on a prime office or retail property, though it was possible to obtain a 90% LTV. The average maximum rose slowly to 80% in 2006. After the bubble burst the LTV available dropped to 77% in 2007 and to 75% in 2008. But the damage was done.

We can illustrate the degree of the difficulties for banks with some simple figures. Over £25 billion of net additional lending was made in 2006. If all those were new loans, made at 80% LTV, then the properties supporting those loans were worth £31 billion. Between the end of 2006 and 2007 property values fell 7.7%, reducing the value of the property to £29 billion and raising the implied LTV to 87%: uncomfortable but manageable. During 2008 values fell a further 26%. The value of the properties was now only £21 billion and the implied LTV rose to 118%. The value of the properties was now less than the loans outstanding. These numbers, based purely on averages and estimates, nevertheless give the flavour of the problems facing lenders in 2009. Loans made near the top of the market at maximum LTV are now ‘under water’, being worth less than the debt used to buy them.

Almost 90% of lenders replying to a survey by de Montfort University, had loans in breach of covenant. Three-quarters of the respondents accounted for 3,770 loans in default, amounting to over £10 billion pounds. Yet the surprising feature of this cycle is the low number of borrowers placed in administration and the small number of forced sales. REITs, property companies and funds have sold property to raise capital, but not on the scale expected from the size of the problem.

What have lenders been doing with their problem loans, particularly those which are in breach of their LTV conditions?

We talked directly to those who are involved to develop a better understanding of what is triggering their decision making. That led us to wonder how lenders view the future and how far that is consistent with history and with current forecasts of both the economy and property market.

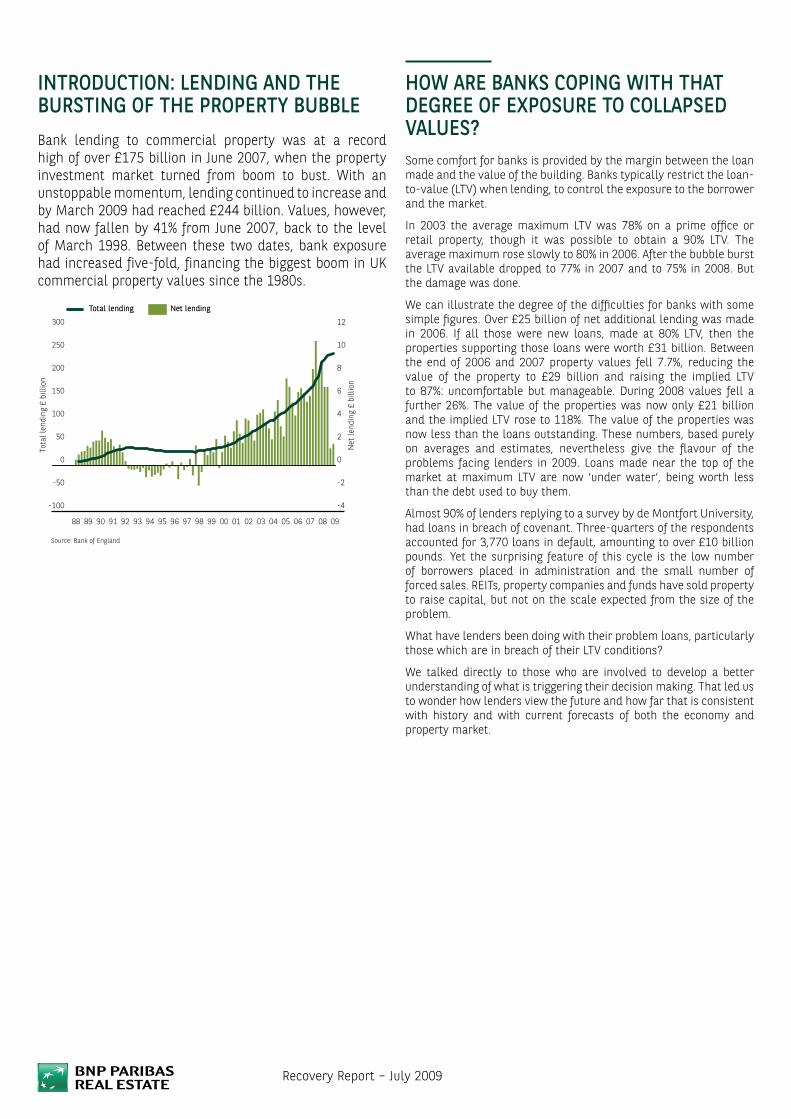

intRoduCtion: lEnding And tHE buRSting of tHE pRopERty bubblEBank lending to commercial property was at a record high of over £175 billion in June 2007, when the property investment market turned from boom to bust. With an unstoppable momentum, lending continued to increase and by March 2009 had reached £244 billion. Values, however, had now fallen by 41% from June 2007, back to the level of March 1998. Between these two dates, bank exposure had increased five-fold, financing the biggest boom in UK commercial property values since the 1980s.

12

10

8

6

4

2

0

-2

-4

Net

lend

ing

£ bi

llion

Total lending Net lending

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

300

250

200

150

100

50

0

-50

-100

Tota

l len

ding

£ b

illio

n

Total lending

Source: Bank of England

Net lending

I3I

tHE SuRvEyWe had three guidelines in setting up the survey. It had to be confidential, which meant using an experienced and respected agency to carry out the survey. We needed to have responses from senior lenders and from those involved in recovery, including accountancy. Since there are complex issues to be explored, we needed to do this by telephone interviews.

We had 30 responses from a range of interviewees. Since we explored issues we have an analysis of responses rather than people. An interviewee may have mentioned more than one issue in response to a question. The percentages given in the analysis are of matters raised by interviewees rather than interviewees themselves.

ExECutivE SummARy• Over 50% of respondents did not think that economic conditions would change much over the next year

• Most respondents see property as having a significant impact on the overall economy due to its size and the increase in recent property market related issues

• Banks tend to look at loan holders on a case-by-case basis to establish whether the loan is worth its continued investment or whether a restructure or termination is in the bank’s best interests

• The most common cause of a loan being called in was the failure of tenants, quickly followed by the lack of additional funds and increased financial pressure on the company or missed payments. Falls in LTV accounted for less than 15% of loans being called in

• Almost 50% said that an LTV breach was not reason enough to call in a loan and that additional capital or equity injection would be a plausible action for breached LTV covenant

• A further 17% said that they would waive the breach or take no action, with 15% negotiating or restructuring the loan

• Over a third of those interviewed said that there had been no change in their risk assessment procedures as these were already well established.

• Most of those interviewed pointed to the lower interest rates and the faster more global decline as the main differences between previous recessions and the current crisis

• Over 80% of those interviewed said that the recapitalisation of the banking system had no affect on their approach to breached loans

• A third of respondents felt that the government intervention was a positive action, with a further 20% saying it was a necessity to avoid total collapse

• The majority of respondents believe that recovery in the property sector will come within the next two years, some are less optimistic and looking to 2013

• Over 50% of respondents thought that the return of confidence was the key to the beginning of recovery, with just under a third pointing to an improvement in lending as the key factor

• A fifth of bankers thought that there would be no long-term problems or issues that will outlive the recovery, while only a sixth thought that the outcome would be that banks will be more conservative or prudent.

SECtion 1: How did pEoplE viEw tHE EConomiC CRiSiS?The property bubble burst in June 2007, 12 months before the economy slipped firmly into recession, in the second quarter of 2008. What kind of impact was this combination of financial and economic crisis having?

The economic downturn has affected lending and recovery decisions for almost all of our respondents.

Whilst some bankers commented that lending had simply ceased, a greater number commented that decisions were more focused on quality and as such tended to be more difficult and slower.

Some 6% continued to actively lend. At the opposite extreme almost a quarter of respondents had stopped lending and a further 6% were focusing purely on existing loans. Over 30% reported some constraints on lending, such as the need to pay close attention to the quality of the borrower and the fact that the process of approving loans was taking longer and was more difficult. Those comments match the sentiment of our investment agents who had reported loans approved at the initial level being turned down by credit committees.

The more general impact on lending policy was picked up on by 22% of the respondents. The growing pressure on banks for improved performance and profitability was cited. Respondents also mentioned the internal requirement to set aside more capital.

Most respondents seem to expect either no change or even a worsening of the economy and property market before lending improves.

Over 50% of respondents believe economic conditions would not change much. A fifth are worried conditions would change for the worse. There are a few optimists, who thought new lending will be limited to existing customers. This importance of concentrating on existing customers was already apparent from anecdotal evidence and is re-emphasised in later questions.

How significant is property for the banks, given the broad range of troubles they currently face?

The overall feeling is that they are very significant, given the scale of property lending and the severity of the crisis the market is facing.

A fifth, on the other hand, were somewhat dismissive, suggesting that property is not that important. Others, similarly unimpressed, pointed out that property is simply one of a variety of challenges faced by the financial industry.

Recovery Report – July 2009

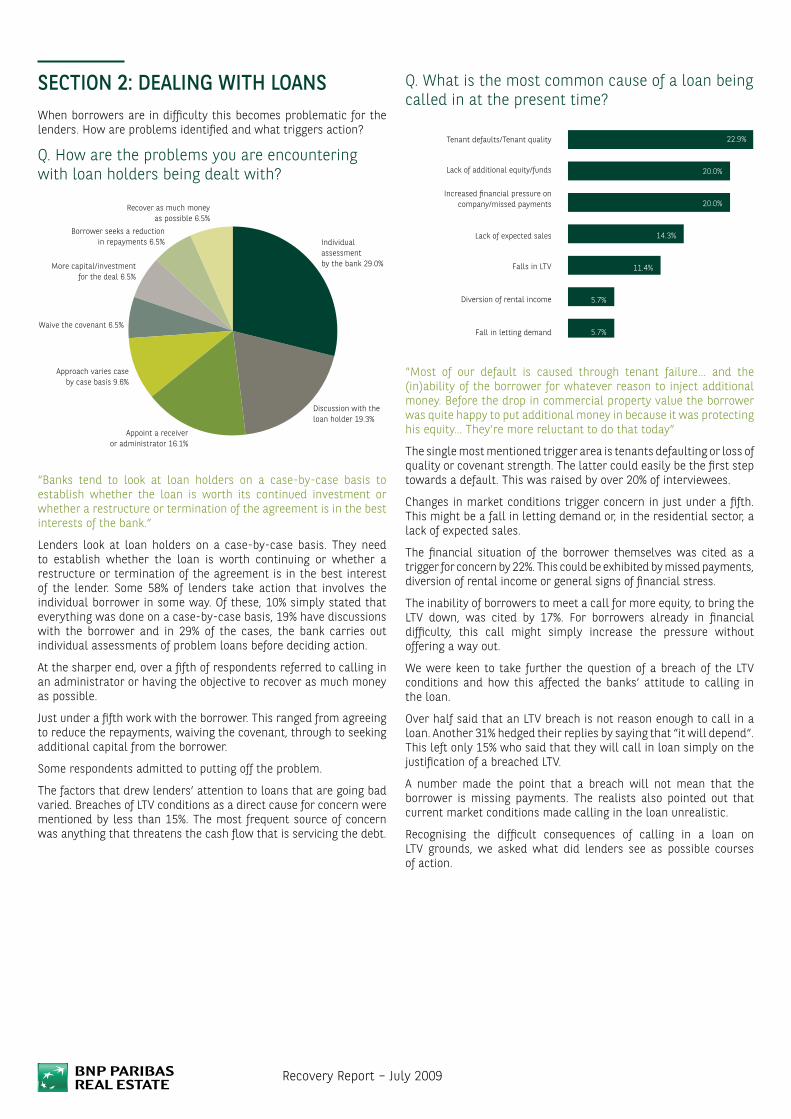

Q. What is the most common cause of a loan being called in at the present time?

22.9%

20.0%

20.0%

14.3%

11.4%

5.7%

5.7%

Tenant defaults/Tenant quality

Lack of additional equity/funds

Increased �nancial pressure on company/missed payments

Lack of expected sales

Falls in LTV

Diversion of rental income

Fall in letting demand

“Most of our default is caused through tenant failure… and the (in)ability of the borrower for whatever reason to inject additional money. Before the drop in commercial property value the borrower was quite happy to put additional money in because it was protecting his equity… They’re more reluctant to do that today”

The single most mentioned trigger area is tenants defaulting or loss of quality or covenant strength. The latter could easily be the first step towards a default. This was raised by over 20% of interviewees.

Changes in market conditions trigger concern in just under a fifth. This might be a fall in letting demand or, in the residential sector, a lack of expected sales.

The financial situation of the borrower themselves was cited as a trigger for concern by 22%. This could be exhibited by missed payments, diversion of rental income or general signs of financial stress.

The inability of borrowers to meet a call for more equity, to bring the LTV down, was cited by 17%. For borrowers already in financial difficulty, this call might simply increase the pressure without offering a way out.

We were keen to take further the question of a breach of the LTV conditions and how this affected the banks’ attitude to calling in the loan.

Over half said that an LTV breach is not reason enough to call in a loan. Another 31% hedged their replies by saying that “it will depend“. This left only 15% who said that they will call in loan simply on the justification of a breached LTV.

A number made the point that a breach will not mean that the borrower is missing payments. The realists also pointed out that current market conditions made calling in the loan unrealistic.

Recognising the difficult consequences of calling in a loan on LTV grounds, we asked what did lenders see as possible courses of action.

SECtion 2: dEAling witH loAnSWhen borrowers are in difficulty this becomes problematic for the lenders. How are problems identified and what triggers action?

Q. How are the problems you are encountering with loan holders being dealt with?

Individualassessment by the bank 29.0%

Discussion with the loan holder 19.3%

Appoint a receiveror administrator 16.1%

Approach varies caseby case basis 9.6%

Waive the covenant 6.5%

More capital/investmentfor the deal 6.5%

Borrower seeks a reductionin repayments 6.5%

Recover as much moneyas possible 6.5%

“Banks tend to look at loan holders on a case-by-case basis to establish whether the loan is worth its continued investment or whether a restructure or termination of the agreement is in the best interests of the bank.”

Lenders look at loan holders on a case-by-case basis. They need to establish whether the loan is worth continuing or whether a restructure or termination of the agreement is in the best interest of the lender. Some 58% of lenders take action that involves the individual borrower in some way. Of these, 10% simply stated that everything was done on a case-by-case basis, 19% have discussions with the borrower and in 29% of the cases, the bank carries out individual assessments of problem loans before deciding action.

At the sharper end, over a fifth of respondents referred to calling in an administrator or having the objective to recover as much money as possible.

Just under a fifth work with the borrower. This ranged from agreeing to reduce the repayments, waiving the covenant, through to seeking additional capital from the borrower.

Some respondents admitted to putting off the problem.

The factors that drew lenders’ attention to loans that are going bad varied. Breaches of LTV conditions as a direct cause for concern were mentioned by less than 15%. The most frequent source of concern was anything that threatens the cash flow that is servicing the debt.

I5I

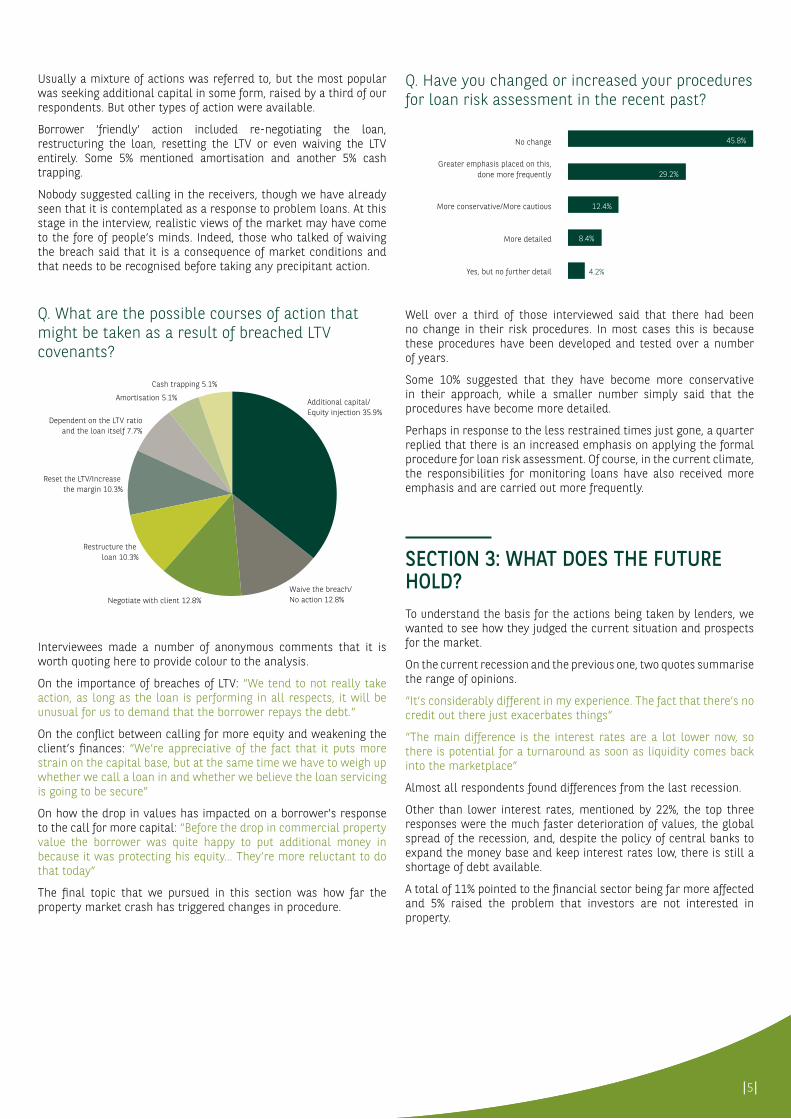

Q. Have you changed or increased your procedures for loan risk assessment in the recent past?

45.8%

29.2%

12.4%

8.4%

4.2%

No change

Greater emphasis placed on this,done more frequently

More conservative/More cautious

More detailed

Yes, but no further detail

Well over a third of those interviewed said that there had been no change in their risk procedures. In most cases this is because these procedures have been developed and tested over a number of years.

Some 10% suggested that they have become more conservative in their approach, while a smaller number simply said that the procedures have become more detailed.

Perhaps in response to the less restrained times just gone, a quarter replied that there is an increased emphasis on applying the formal procedure for loan risk assessment. Of course, in the current climate, the responsibilities for monitoring loans have also received more emphasis and are carried out more frequently.

SECtion 3: wHAt doES tHE futuRE Hold?To understand the basis for the actions being taken by lenders, we wanted to see how they judged the current situation and prospects for the market.

On the current recession and the previous one, two quotes summarise the range of opinions.

“It’s considerably different in my experience. The fact that there’s no credit out there just exacerbates things”

“The main difference is the interest rates are a lot lower now, so there is potential for a turnaround as soon as liquidity comes back into the marketplace”

Almost all respondents found differences from the last recession.

Other than lower interest rates, mentioned by 22%, the top three responses were the much faster deterioration of values, the global spread of the recession, and, despite the policy of central banks to expand the money base and keep interest rates low, there is still a shortage of debt available.

A total of 11% pointed to the financial sector being far more affected and 5% raised the problem that investors are not interested in property.

Usually a mixture of actions was referred to, but the most popular was seeking additional capital in some form, raised by a third of our respondents. But other types of action were available.

Borrower ‘friendly’ action included re-negotiating the loan, restructuring the loan, resetting the LTV or even waiving the LTV entirely. Some 5% mentioned amortisation and another 5% cash trapping.

Nobody suggested calling in the receivers, though we have already seen that it is contemplated as a response to problem loans. At this stage in the interview, realistic views of the market may have come to the fore of people’s minds. Indeed, those who talked of waiving the breach said that it is a consequence of market conditions and that needs to be recognised before taking any precipitant action.

Q. What are the possible courses of action that might be taken as a result of breached LTV covenants?

Additional capital/Equity injection 35.9%

Waive the breach/No action 12.8%Negotiate with client 12.8%

Restructure the loan 10.3%

Reset the LTV/Increase the margin 10.3%

Dependent on the LTV ratioand the loan itself 7.7%

Amortisation 5.1%

Cash trapping 5.1%

Interviewees made a number of anonymous comments that it is worth quoting here to provide colour to the analysis.

On the importance of breaches of LTV: “We tend to not really take action, as long as the loan is performing in all respects, it will be unusual for us to demand that the borrower repays the debt.”

On the conflict between calling for more equity and weakening the client’s finances: “We’re appreciative of the fact that it puts more strain on the capital base, but at the same time we have to weigh up whether we call a loan in and whether we believe the loan servicing is going to be secure”

On how the drop in values has impacted on a borrower’s response to the call for more capital: “Before the drop in commercial property value the borrower was quite happy to put additional money in because it was protecting his equity… They’re more reluctant to do that today”

The final topic that we pursued in this section was how far the property market crash has triggered changes in procedure.

Recovery Report – July 2009

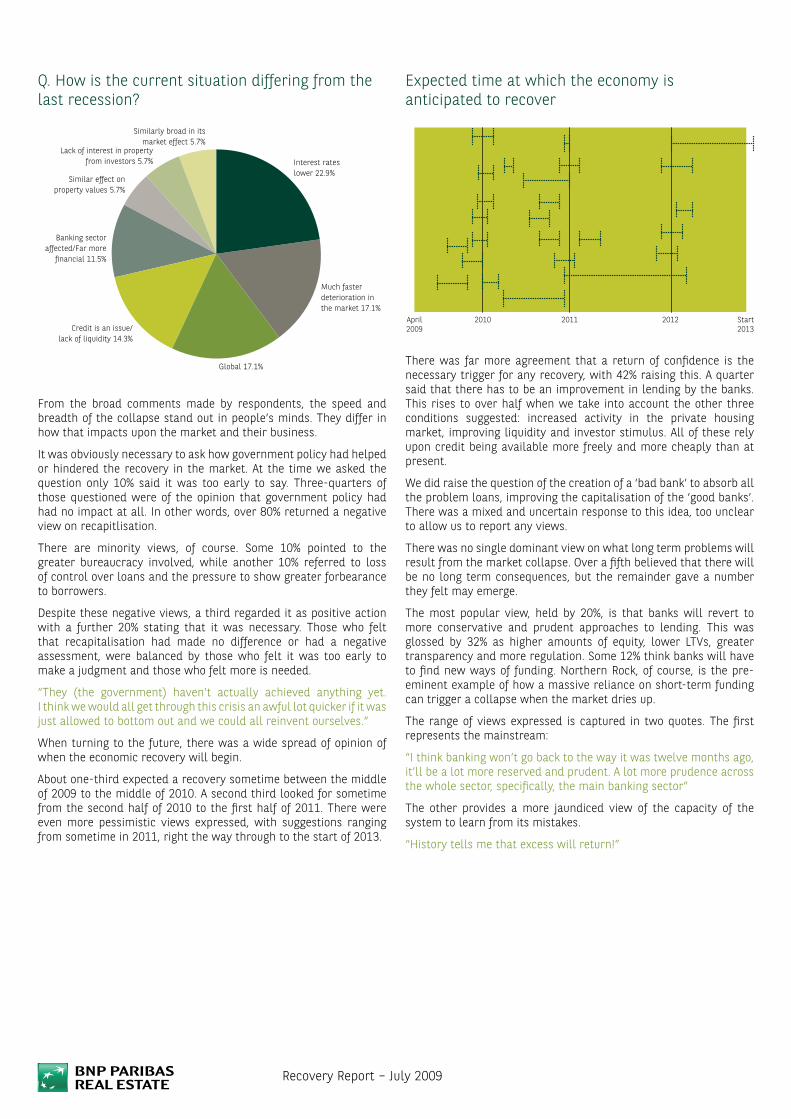

Expected time at which the economy is anticipated to recover

April2009

2010 2011 2012 Start2013

There was far more agreement that a return of confidence is the necessary trigger for any recovery, with 42% raising this. A quarter said that there has to be an improvement in lending by the banks. This rises to over half when we take into account the other three conditions suggested: increased activity in the private housing market, improving liquidity and investor stimulus. All of these rely upon credit being available more freely and more cheaply than at present.

We did raise the question of the creation of a ‘bad bank’ to absorb all the problem loans, improving the capitalisation of the ‘good banks’. There was a mixed and uncertain response to this idea, too unclear to allow us to report any views.

There was no single dominant view on what long term problems will result from the market collapse. Over a fifth believed that there will be no long term consequences, but the remainder gave a number they felt may emerge.

The most popular view, held by 20%, is that banks will revert to more conservative and prudent approaches to lending. This was glossed by 32% as higher amounts of equity, lower LTVs, greater transparency and more regulation. Some 12% think banks will have to find new ways of funding. Northern Rock, of course, is the pre-eminent example of how a massive reliance on short-term funding can trigger a collapse when the market dries up.

The range of views expressed is captured in two quotes. The first represents the mainstream:

“I think banking won’t go back to the way it was twelve months ago, it’ll be a lot more reserved and prudent. A lot more prudence across the whole sector, specifically, the main banking sector”

The other provides a more jaundiced view of the capacity of the system to learn from its mistakes.

“History tells me that excess will return!”

Q. How is the current situation differing from the last recession?

Interest rateslower 22.9%

Much faster deterioration inthe market 17.1%

Global 17.1%

Credit is an issue/lack of liquidity 14.3%

Banking sectoraffected/Far more

financial 11.5%

Similar effect onproperty values 5.7%

Lack of interest in propertyfrom investors 5.7%

Similarly broad in itsmarket effect 5.7%

From the broad comments made by respondents, the speed and breadth of the collapse stand out in people’s minds. They differ in how that impacts upon the market and their business.

It was obviously necessary to ask how government policy had helped or hindered the recovery in the market. At the time we asked the question only 10% said it was too early to say. Three-quarters of those questioned were of the opinion that government policy had had no impact at all. In other words, over 80% returned a negative view on recapitlisation.

There are minority views, of course. Some 10% pointed to the greater bureaucracy involved, while another 10% referred to loss of control over loans and the pressure to show greater forbearance to borrowers.

Despite these negative views, a third regarded it as positive action with a further 20% stating that it was necessary. Those who felt that recapitalisation had made no difference or had a negative assessment, were balanced by those who felt it was too early to make a judgment and those who felt more is needed.

“They (the government) haven’t actually achieved anything yet. I think we would all get through this crisis an awful lot quicker if it was just allowed to bottom out and we could all reinvent ourselves.”

When turning to the future, there was a wide spread of opinion of when the economic recovery will begin.

About one-third expected a recovery sometime between the middle of 2009 to the middle of 2010. A second third looked for sometime from the second half of 2010 to the first half of 2011. There were even more pessimistic views expressed, with suggestions ranging from sometime in 2011, right the way through to the start of 2013.

I7I

Land

83 85 87 89 91 93 95 97 0799 01 0503

300

250

200

150

100

50

0

10.5 years

13.5 years

Jan

89 p

eak

= 10

0

Nominal

Source: VOA

Real

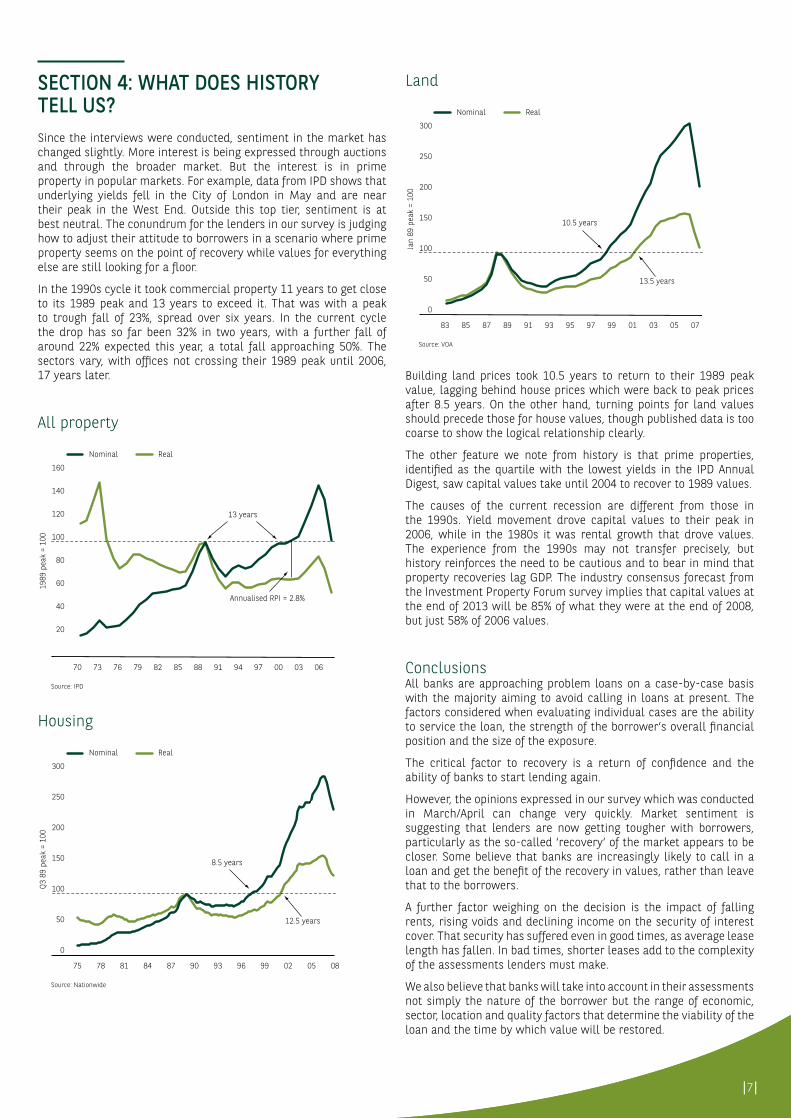

Building land prices took 10.5 years to return to their 1989 peak value, lagging behind house prices which were back to peak prices after 8.5 years. On the other hand, turning points for land values should precede those for house values, though published data is too coarse to show the logical relationship clearly.

The other feature we note from history is that prime properties, identified as the quartile with the lowest yields in the IPD Annual Digest, saw capital values take until 2004 to recover to 1989 values.

The causes of the current recession are different from those in the 1990s. Yield movement drove capital values to their peak in 2006, while in the 1980s it was rental growth that drove values. The experience from the 1990s may not transfer precisely, but history reinforces the need to be cautious and to bear in mind that property recoveries lag GDP. The industry consensus forecast from the Investment Property Forum survey implies that capital values at the end of 2013 will be 85% of what they were at the end of 2008, but just 58% of 2006 values.

ConclusionsAll banks are approaching problem loans on a case-by-case basis with the majority aiming to avoid calling in loans at present. The factors considered when evaluating individual cases are the ability to service the loan, the strength of the borrower’s overall financial position and the size of the exposure.

The critical factor to recovery is a return of confidence and the ability of banks to start lending again.

However, the opinions expressed in our survey which was conducted in March/April can change very quickly. Market sentiment is suggesting that lenders are now getting tougher with borrowers, particularly as the so-called ‘recovery’ of the market appears to be closer. Some believe that banks are increasingly likely to call in a loan and get the benefit of the recovery in values, rather than leave that to the borrowers.

A further factor weighing on the decision is the impact of falling rents, rising voids and declining income on the security of interest cover. That security has suffered even in good times, as average lease length has fallen. In bad times, shorter leases add to the complexity of the assessments lenders must make.

We also believe that banks will take into account in their assessments not simply the nature of the borrower but the range of economic, sector, location and quality factors that determine the viability of the loan and the time by which value will be restored.

SECtion 4: wHAt doES HiStoRy tEll uS?Since the interviews were conducted, sentiment in the market has changed slightly. More interest is being expressed through auctions and through the broader market. But the interest is in prime property in popular markets. For example, data from IPD shows that underlying yields fell in the City of London in May and are near their peak in the West End. Outside this top tier, sentiment is at best neutral. The conundrum for the lenders in our survey is judging how to adjust their attitude to borrowers in a scenario where prime property seems on the point of recovery while values for everything else are still looking for a floor.

In the 1990s cycle it took commercial property 11 years to get close to its 1989 peak and 13 years to exceed it. That was with a peak to trough fall of 23%, spread over six years. In the current cycle the drop has so far been 32% in two years, with a further fall of around 22% expected this year, a total fall approaching 50%. The sectors vary, with offices not crossing their 1989 peak until 2006, 17 years later.

All property

70 73 76 79 82 85 88 91 0694 97 00 03

160

140

120

100

80

60

40

20

13 years

Annualised RPI = 2.8%

1989

pea

k =

100

Nominal

Source: IPD

Real

Housing

75 78 81 84 87 90 93 96 0899 02 05

300

250

200

150

100

50

0

8.5 years

12.5 years

Q3 8

9 pe

ak =

100

Nominal

Source: Nationwide

Real

Recovery Report – July 2009

ONE REAL ESTATE COMPANYTHAT'S INTERNATIONALAND LOCAL.

Canary Islands

Canada and USA

Japan

India

Cyprus

Our locationsOur alliances

Abu dhabiAl Bateen AreaPlot No. 144, W-11New Al Bateen MunicipalityStreet 32P.O. Box 2742Abu Dhabi, UAETel: +971 505 573 055Fax: +971 44 257 817

bahrainBahrain Financial HarbourWest Tower16th FloorP.O. Box 5253ManamaTel: + 971 505 573 055Fax: +973 17 536 506

belgiumBlue Tower avenue Louise 326 B14 1050 Brussels Tel: +32 2 646 49 49 Fax: +32 2 646 46 50

dubaiEmaar SquareBuilding No. 17th FloorP.O. Box 7233Dubai, UAETel: + 971 505 573 055Fax: +971 44 257 817

france32 rue Jacques Ibert 92309 Levallois cedex Tel: +33 (0)1 47 59 20 00 Fax: +33 (0)1 47 59 22 69

germanyGoetheplatz 4 60311 Frankfurt am Main Tel: +49 69 2 98 99 0 Fax: +49 69 29 29 14

india403, The Estate 121, Dickenson Road Bangalore - 560042 Tel: +91 80 40 508 888Fax: +91 80 40 508 899

ireland40 Fitzwilliam Place Dublin 2 Tel: +353 1 66 11 233 Fax: +353 1 67 89 981

italyCorso Italia, 15/A 20122 Milan Tel: +39 02 58 33 141 Fax: +39 02 58 33 14 39

Jersey 4th Floor, Conway House Conway Street St Helier Jersey JE2 3NT Tel: +44 15 34 62 90 01 Fax: +44 15 34 62 90 11

luxembourg EBBC, Route de Trèves 6Bloc D 2633 Senningerberg Tel: +352 34 94 84 Fax: +352 34 94 73

RomaniaUnion International Center 11 Ion Campineanu Street Sector 1 Bucharest 010031 Tel: +40 21 312 7000 Fax: +40 21 312 7001

SpainMaría de Molina, 54 28006 Madrid Tel: +34 91 454 96 00 Fax: +34 91 454 97 65

united kingdom90 Chancery Lane London WC2A 1EU Tel: +44 20 7338 4000 Fax: +44 20 7430 2628

uSA787 Seventh Avenue 31st Floor New York City, NY 10019 Tel: +1 917 472 4970Fax: +1 212 471 8100

Non

con

trac

tual

doc

umen

t - B

NP

PARI

BAS

REAL

EST

ATE

- Re

cove

ry R

epor

t – Ju

ly 2

009

- 10

771

H

eadq

uart

ers

: 13,

bd

du F

ort d

e Va

ux 7

5017

Par

is -

Fra

nce

- SA

S w

ith

capi

tal o

f E 2

5,20

5,61

6 -

RCS

Pari

s 69

2 01

2 18

0

LOCATIONS

Joe pitt – Head of Recovery and RestructuringTel: 020 7338 [email protected]

keith Steventon – Head of ResearchTel: 020 7338 [email protected]

CONTACTS

Related Documents