Benefits of Banks: Opening and Managing Savings and Checking Accounts Glow Foundation 2010

Benefits of Banks: Opening and Managing Savings and Checking Accounts Glow Foundation 2010.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Benefits of Banks: Opening and Managing Savings and Checking

Accounts

Glow Foundation2010

Page 2

Icebreaker!

Page 3

Group Agreements

Page 4

Pre-Assessment

(30 minutes)

Page 5

What We Will Discuss Today

Benefits of Banking

Savings Accounts (Opening an Account, Interest,

Tips)

Checking Accounts (Parts of a Check, Filling out a

Check and Deposit Slip)

Using a Debit / ATM Card

Tracking Your Spending

Protect Yourself from Fraud!

Page 6

Benefits of a Bank

DISCUSSION:

1. Why would someone decide to open a bank account?

2. What are some benefits of a bank?

Page 7

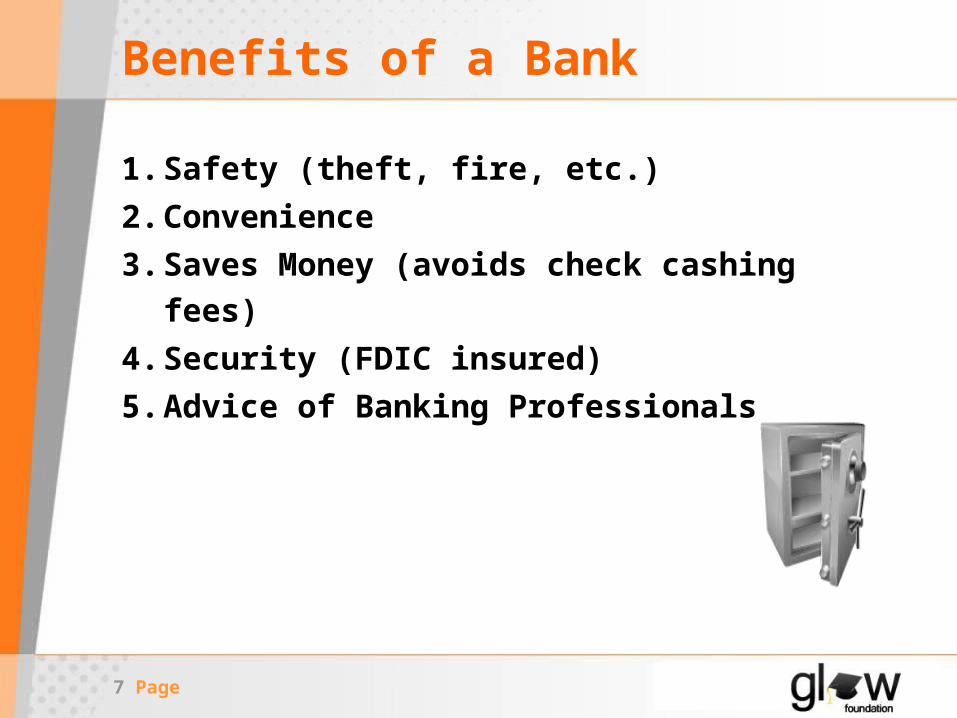

Benefits of a Bank

1. Safety (theft, fire, etc.)

2. Convenience

3. Saves Money (avoids check cashing fees)

4. Security (FDIC insured)

5. Advice of Banking Professionals

Page 8

Savings Account Basics

What is a Savings Account?

Page 9

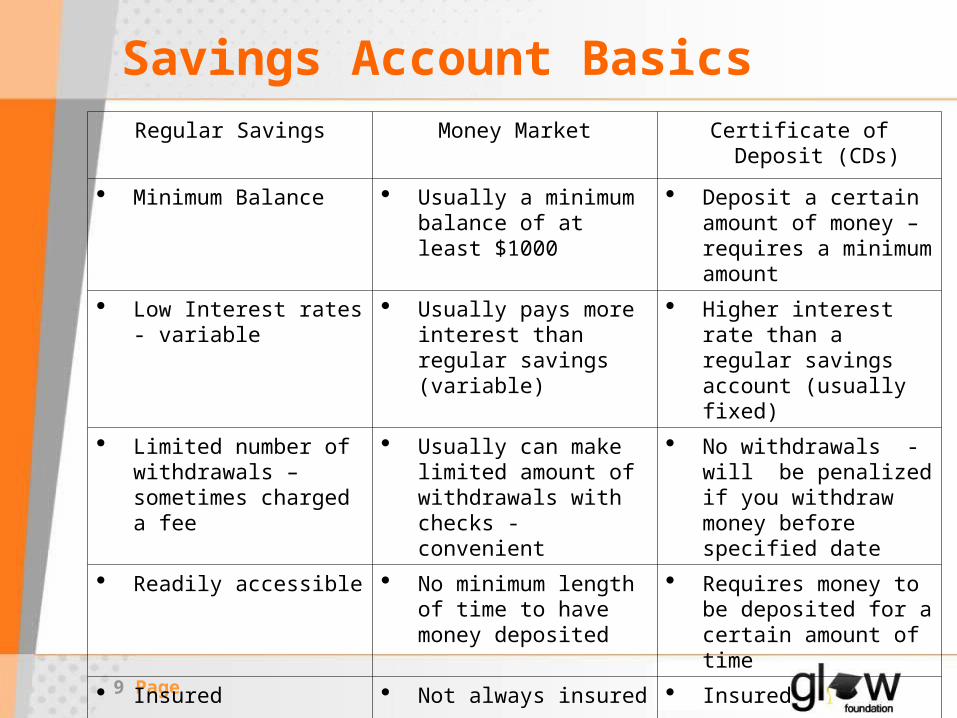

Savings Account BasicsRegular Savings Money Market Certificate of Deposit

(CDs)

Minimum Balance Usually a minimum balance of at least $1000

Deposit a certain amount of money – requires a minimum amount

Low Interest rates - variable

Usually pays more interest than regular savings (variable)

Higher interest rate than a regular savings account (usually fixed)

Limited number of withdrawals – sometimes charged a fee

Usually can make limited amount of withdrawals with checks - convenient

No withdrawals - will be penalized if you withdraw money before specified date

Readily accessible No minimum length of time to have money deposited

Requires money to be deposited for a certain amount of time

Insured Not always insured Insured

Page 10

Savings Account Basics

Financial Feud

Page 11

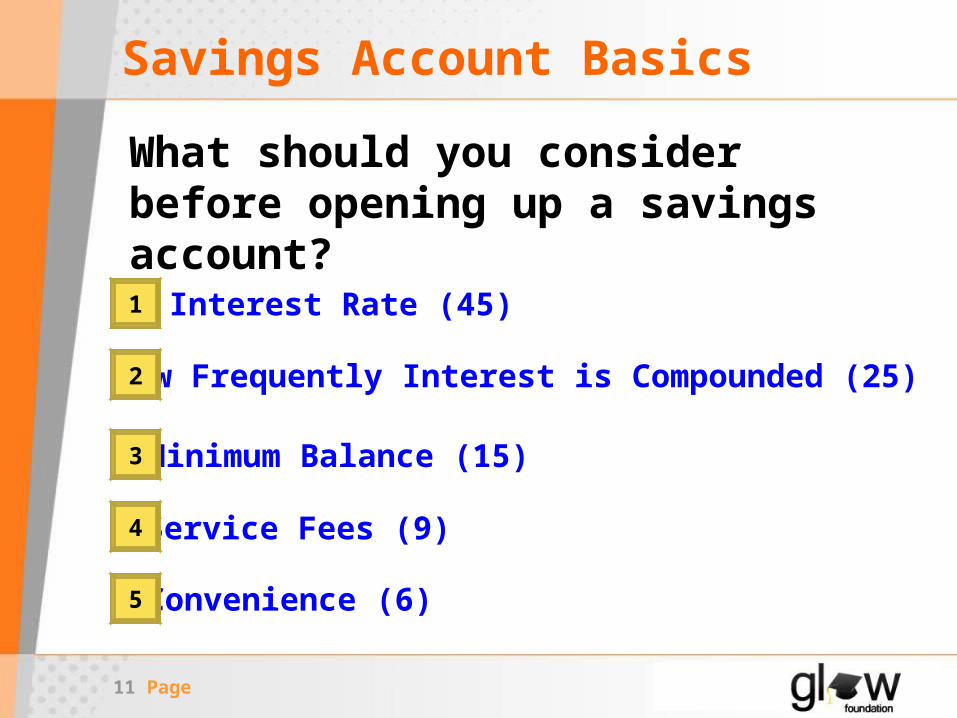

Savings Account Basics

What should you consider before opening up a savings account?

How Frequently Interest is Compounded (25)

Minimum Balance (15)

Service Fees (9)

Convenience (6)

Interest Rate (45)1

2

3

4

5

Page 12

Savings Account Basics

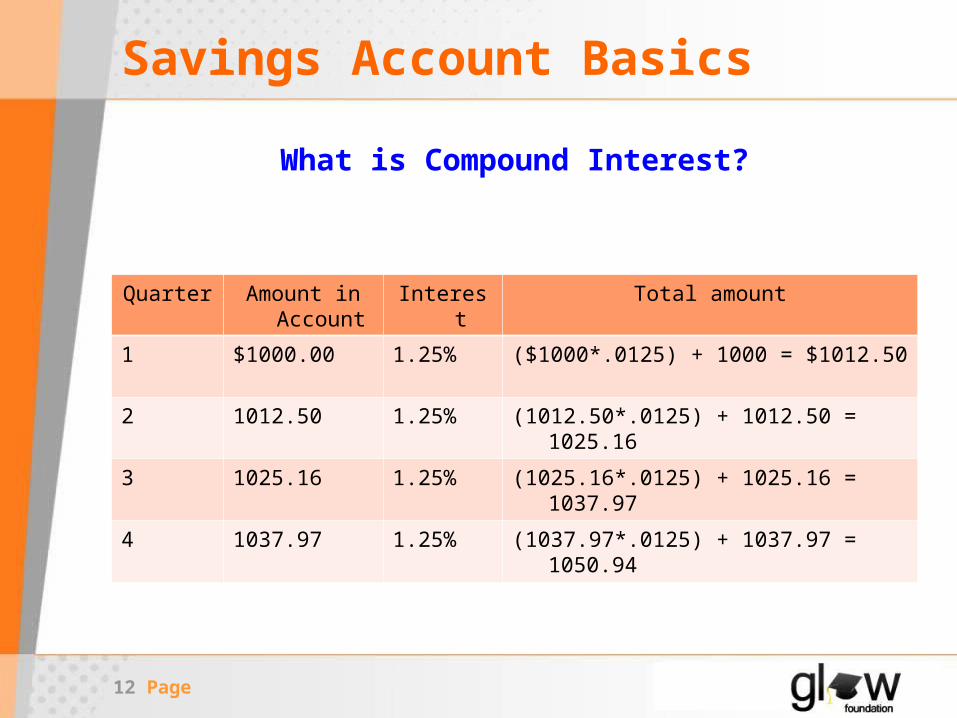

What is Compound Interest?

Quarter Amount in Account

Interest Total amount

1 $1000.00 1.25% ($1000*.0125) + 1000 = $1012.50

2 1012.50 1.25% (1012.50*.0125) + 1012.50 = 1025.16

3 1025.16 1.25% (1025.16*.0125) + 1025.16 = 1037.97

4 1037.97 1.25% (1037.97*.0125) + 1037.97 = 1050.94

Page 13

Saving Account Basics

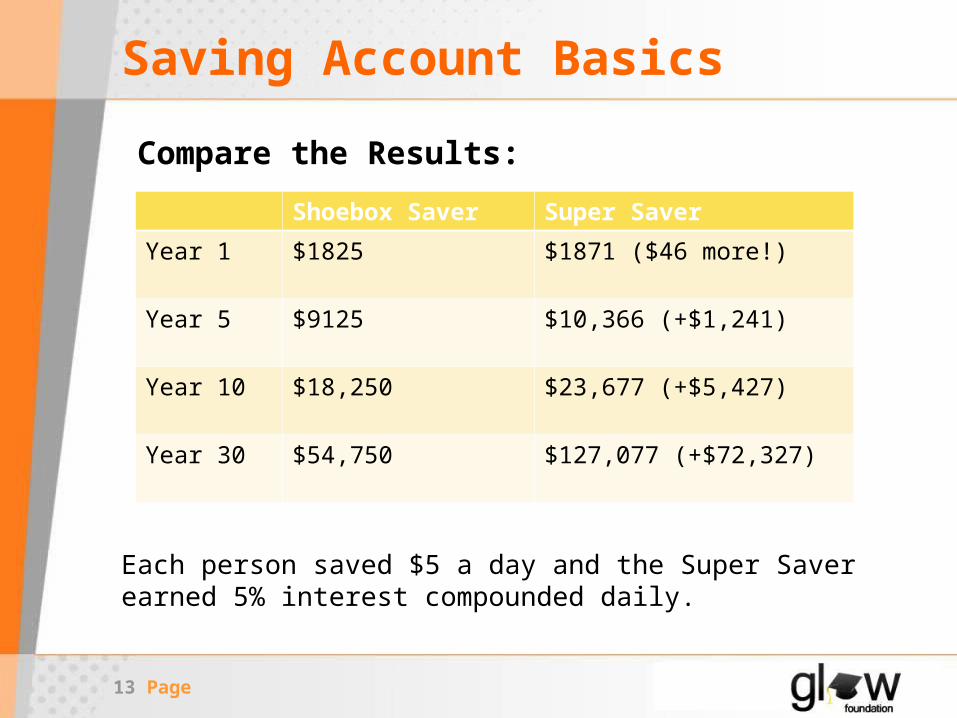

Compare the Results:

Shoebox Saver Super Saver

Year 1 $1825 $1871 ($46 more!)

Year 5 $9125 $10,366 (+$1,241)

Year 10 $18,250 $23,677 (+$5,427)

Year 30 $54,750 $127,077 (+$72,327)

Each person saved $5 a day and the Super Saver earned 5% interest compounded daily.

Page 14

Savings Account Basics

Some tips to SAVE MORE MONEY:

Ask yourself, “Do I NEED this?” Pay YOURSELF first before you spend any money If you get money as a gift or a bonus, save a portion

of it Save spare change and deposit it Pay bills on time Avoid check cashing stores Take lunch with you instead of eating out Carry small amounts of cash with you Use direct deposit Others?

Page 15

Individual Development Account Matched Savings Account for your College Education -

for every $1 you save, receive $2 in matched funds up to $6,000!!

Enroll after the completion of Glow’s Financial Education Program

To be eligible, you must meet income restrictions, have a SSN or ITIN, be able to save a minimum of $20 a month.

Page 16

Checking Account Basics

What is a Checking Account?

Page 17

Checking Account Basics

Checking Accounts:

Keep your money safe and accessible Help control your spending Don’t pay interest May require you to keep a minimum

balance or do direct deposit (to avoid fees)

Checks function like cash

Page 18

Checking Account Basics

Handout:

The Parts of a Check

Page 19

Checking Account Basics

Handout:

How to Write a Check

Page 20

Checking Account Basics

Check-Writing Tips:

Always write in blue or black ink Write neatly Save your receipts and record your spending in

your register Initial your (small) mistakes / VOID checks with

large mistakes Avoid writing “bad” checks - you will get fined

and it’s against the law in some cases

Page 21

Checking Account Basics

Handout:

How to Endorse a Check

Page 22

Checking Account Basics

Handout:

How to Fill In a Deposit Slip

Page 23

ATM / Debit Cards

What’s the difference between an ATM and debit

card?

Page 24

ATM / Debit Cards

ATM Cards are used to: Deposit, withdraw, or transfer money

Debit cards can do this in addition to: Purchasing items Online banking – pay your bills, check account

balances

Page 25

ATM / Debit Cards

What information is on your ATM / debit card?

(If you have a debit card, you can examine it as we look at the parts of a debit card)

Page 26

ATM / Debit Cards

Using an ATM Machine

Page 27

ATM / Debit Cards

ATM / Debit Card Tips:

You may be charged a fee if you use an ATM that is operated by another bank

Know your balance available Be aware of what you’re buying - it’s easier to

spend more with plastic! Be careful with your Personal Identification

Number (PIN) – Never write it on your card Avoid magnets – they can de-magnetize your card Contact your bank if your card is lost or stolen!

Page 28

Tracking Your Spending

What are some ways to track your spending and control the

money you have?

Page 29

Tracking Your Spending

1. Save your receipts

2. Record transactions

3. Avoid over-spending

4. Review statements

5. Compare with the bank

Page 30

Tracking Your Spending

Handout:

Parts of a Check Register

Page 31

Tracking Your Spending

What happens if you spend more money than you have in your

account?

Page 32

Protect Yourself From Fraud

Breakout:

Being Safe at Home and Online

Page 33

Recap

Benefits of Banking

Savings Accounts (Opening an Account, Interest,

Tips)

Checking Accounts (Parts of a Check, Filling out a

Check and Deposit Slip)

Using a Debit / ATM Card

Tracking Your Spending

Protect Yourself from Fraud!

Page 34

Homework:

Save your receipts for one week

and bring it to the next session

Related Documents