Tuesday April 19, 2016 www.bloombergbriefs.com Bloomberg AAA Benchmark Yields DESCRIPTION CURRENT PREVIOUS NET CHANGE BVAL Muni Benchmark 1T 0.56 0.58 -0.01 BVAL Muni Benchmark 2T 0.70 0.70 0 BVAL Muni Benchmark 3T 0.80 0.82 -0.01 BVAL Muni Benchmark 4T 0.94 0.95 -0.01 BVAL Muni Benchmark 5T 1.04 1.06 -0.02 BVAL Muni Benchmark 6T 1.17 1.18 -0.01 BVAL Muni Benchmark 7T 1.28 1.28 0 BVAL Muni Benchmark 8T 1.40 1.40 0 BVAL Muni Benchmark 9T 1.52 1.52 0 BVAL Muni Benchmark 10T 1.65 1.66 -0.01 BVAL Muni Benchmark 20T 2.22 2.23 0 BVAL Muni Benchmark 30T 2.52 2.54 -0.01 Source: GBY<GO>, GC I493 <GO> Chicago Schools Need Line of Credit to Stay Solvent BY ELIZABETH CAMPBELL, BLOOMBERG NEWS The cash-strapped Chicago public schools need to borrow more money to stay solvent, according to , chief executive officer of the nation’s third- Forrest Claypool largest district. “We have to secure a new line of credit to stay solvent,” Claypool said yesterday in response to a reporter’s question on whether the district would need a line of credit in the coming fiscal year to pay for a new teachers’ contract. “We can’t pay for anything absent a line of credit.” The district, which has a revolving line of credit of $870 million with the banks, has reached the end of its borrowing and is in a “precarious situation,” Claypool said during a press conference to address the threat of a teachers’ strike. After cutting costs, including classroom spending and planning furlough days, the district is just “barely” going to make the $679 million pension payment due by June 30, Claypool said. The district is facing a $1 billion deficit and rising retirement fund costs. The school system is looking to renew existing credit lines and considering options for a new one, and the amount of that loan will be determined by next year’s budget, according to the district. It will help tide over its cash flow needs. Rising pension bills are at the core of the school system’s financial crisis, Claypool said. Chicago is the only school district in Illinois that has to pay the vast majority of its teachers’ retirement costs. Mayor , Claypool, and the teachers union Rahm Emanuel have called on state lawmakers to fix what they call inequitable educational funding. Illinois covers the pension costs of the rest of the state’s school districts. On Saturday, a third-party fact-finder recommended that the teachers’ union and district agree to a four-year contract that includes an 8.75 percent wage increase and the phaseout of the district’s coverage of teachers’ employee pension contributions. Claypool called the contract "fair” and urged the union to accept the independent arbitrators’ report. The union rejected the contract and threatened to strike as early as mid-May, which is the end of the required 30-day cooling off period. Teachers staged a one-day strike on April 1, and the union walked out in 2012 for seven days, the first strike in 25 years. STATE YIELD SPREAD TO AAA CHANGE CA 1.89 23 0 FL 1.81 15 0 IL 3.46 180 -0.02 NY 1.80 14 0 PA 2.31 65 -0.01 TX 1.90 24 0 MUNICIPALITY AMOUNT Maine Bond Bank $95 million Rev New Brunswick Parking NJ $118 million Rev West Fargo SD # 6 ND $45 million GO Regional Transportation Auth IL $150 million Rev Virginia Public Schools $98 million Rev Source: Bloomberg CDRA <GO> AMOUNT OUTSTANDING ($MLNS) MATURING NEXT 30 DAYS ($MLNS) ANNOUNCED CALLS NEXT 30 DAYS ($MLNS) 3,550,022 10,755 8,678 Source: MBM<GO> BENCHMARK STATES 10-YEAR PRIMARY FIXED RATE 30-Day Supply Fixed: $13.3 Bln (LT) 30-Day Supply Fixed: $482 Mln (ST) Sold YTD Fixed: $86.5 Bln (Neg LT) Sold YTD Fixed: $26.4 Bln (Comp LT) Sold YTD Fixed: $5.7 Bln (ST) SECONDARY MARKET MSRB: $10.3 Bln PICK: $15.8 Bln VARIABLE RATE SIFMA Muni Swap Rate: 0.4% Bloomberg Weekly AAA Rate: 0.4% Bloomberg Weekly AA Rate: 0.421% Daily Reset Inventory: $150 Mln Weekly Reset Inventory: $1.2 Bln IN THE PIPELINE SIZE OF MARKET CREDIT CLOSE-UP

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Tuesday

April 19, 2016

www.bloombergbriefs.com

Bloomberg AAA Benchmark Yields

DESCRIPTION CURRENT PREVIOUS NET CHANGE

BVAL Muni Benchmark 1T 0.56 0.58 -0.01

BVAL Muni Benchmark 2T 0.70 0.70 0

BVAL Muni Benchmark 3T 0.80 0.82 -0.01

BVAL Muni Benchmark 4T 0.94 0.95 -0.01

BVAL Muni Benchmark 5T 1.04 1.06 -0.02

BVAL Muni Benchmark 6T 1.17 1.18 -0.01

BVAL Muni Benchmark 7T 1.28 1.28 0

BVAL Muni Benchmark 8T 1.40 1.40 0

BVAL Muni Benchmark 9T 1.52 1.52 0

BVAL Muni Benchmark 10T 1.65 1.66 -0.01

BVAL Muni Benchmark 20T 2.22 2.23 0

BVAL Muni Benchmark 30T 2.52 2.54 -0.01Source: GBY<GO>, GC I493 <GO>

Chicago Schools Need Line of Credit to Stay SolventBY ELIZABETH CAMPBELL, BLOOMBERG NEWS

The cash-strapped Chicago public schools need to borrow more money to stay solvent, according to , chief executive officer of the nation’s third-Forrest Claypoollargest district.

“We have to secure a new line of credit to stay solvent,” Claypool said yesterday in response to a reporter’s question on whether the district would need a line of credit in the coming fiscal year to pay for a new teachers’ contract. “We can’t pay for anything absent a line of credit.”

The district, which has a revolving line of credit of $870 million with the banks, has reached the end of its borrowing and is in a “precarious situation,” Claypool said during a press conference to address the threat of a teachers’ strike.

After cutting costs, including classroom spending and planning furlough days, the district is just “barely” going to make the $679 million pension payment due by June 30, Claypool said. The district is facing a $1 billion deficit and rising retirement fund costs.

The school system is looking to renew existing credit lines and considering options for a new one, and the amount of that loan will be determined by next year’s budget, according to the district. It will help tide over its cash flow needs.

Rising pension bills are at the core of the school system’s financial crisis, Claypool said. Chicago is the only school district in Illinois that has to pay the vast majority of its teachers’ retirement costs. Mayor , Claypool, and the teachers union Rahm Emanuelhave called on state lawmakers to fix what they call inequitable educational funding. Illinois covers the pension costs of the rest of the state’s school districts.

On Saturday, a third-party fact-finder recommended that the teachers’ union and district agree to a four-year contract that includes an 8.75 percent wage increase and the phaseout of the district’s coverage of teachers’ employee pension contributions.

Claypool called the contract "fair” and urged the union to accept the independent arbitrators’ report. The union rejected the contract and threatened to strike as early as mid-May, which is the end of the required 30-day cooling off period. Teachers staged a one-day strike on April 1, and the union walked out in 2012 for seven days, the first strike in 25 years.

STATE YIELD SPREAD TO AAA CHANGE

CA 1.89 23 0

FL 1.81 15 0

IL 3.46 180 -0.02

NY 1.80 14 0

PA 2.31 65 -0.01

TX 1.90 24 0

MUNICIPALITY AMOUNT

Maine Bond Bank $95 million Rev

New Brunswick Parking NJ $118 million Rev

West Fargo SD # 6 ND $45 million GO

Regional Transportation Auth IL $150 million Rev

Virginia Public Schools $98 million RevSource: Bloomberg CDRA <GO>

AMOUNT OUTSTANDING

($MLNS)

MATURING NEXT 30

DAYS ($MLNS)

ANNOUNCED CALLS NEXT 30 DAYS ($MLNS)

3,550,022 10,755 8,678Source: MBM<GO>

BENCHMARK STATES 10-YEAR

PRIMARY FIXED RATE

30-Day Supply Fixed: $13.3 Bln (LT)30-Day Supply Fixed: $482 Mln (ST)Sold YTD Fixed: $86.5 Bln (Neg LT)Sold YTD Fixed: $26.4 Bln (Comp LT)Sold YTD Fixed: $5.7 Bln (ST)

SECONDARY MARKET

MSRB: $10.3 BlnPICK: $15.8 Bln

VARIABLE RATE

SIFMA Muni Swap Rate: 0.4%Bloomberg Weekly AAA Rate: 0.4% Bloomberg Weekly AA Rate: 0.421% Daily Reset Inventory: $150 Mln Weekly Reset Inventory: $1.2 Bln

IN THE PIPELINE

SIZE OF MARKET

CREDIT CLOSE-UP

April 19, 2016 Bloomberg Brief Municipal Market 2

CREDIT CLOSE-UPPuerto Rico's Bondholders Divided in Fight Over Federal RescueBY MICHELLE KASKE, BLOOMBERG NEWS

Puerto Rico bondholders are lining up on different sides of the battle in Congress over legislation to rescue the island from financial collapse as lawmakers rewrite the bill in an effort to overcome opposition from Democrats and Republicans.

Hedge funds that own about $5 billion of Puerto Rico’s general-obligation bonds, which are guaranteed under the island’s constitution, are fighting the House measure that would give the U.S. territory ability to write off some of its $70 billion in debt. Firms that own securities backed by sales taxes are working to ensure its passage, seeing it as a way to protect their investment from a cascading series of defaults.

The fracture is adding to the political discord over the broadest effort yet in Washington to address the Puerto Rican debt crisis, which has been building over the past 10 months as the island’s government runs out of cash and can no longer borrow money to remain afloat. After members from both parties bristled at aspects of the bill, the House Natural Resources Committee last week abruptly canceled a planned vote on the measure so legislators could revise it.

Puerto Rico is veering toward major bond defaults in May and July after Governor Alejandro Garcia Padillasigned a law allowing him to suspend debt payments through January. He has pushed Congress to give his government legal powers to restructure debt in court, which it currently cannot do, to avert painful spending cuts on an island where nearly half the residents live in poverty and the economy has been contracting for a decade.

If not addressed, the crisis threatens to leave owners of Puerto Rico’s varying securities — with differing legal protections or promised rights to certain revenue — fighting in court over whatever money Puerto Rico brings in.

Garcia Padilla has proposed preventing that by allowing investors to voluntarily exchange their bonds for new securities, though no formal offer has been extended as his administration waits on action from

Washington. In its most recent proposal, Puerto Rico said it would pay 74 cents on the dollar for general-obligation and government-guaranteed debt and 57 cents for sales-tax securities.

The creditor schism on Capitol Hill between investors with competing interests underscores the obstacles that Puerto Rico faces in reaching a timely agreement to reduce its debt, which was issued by 17 different arms of the government, including $13 billion ofgeneral obligations and $15 billion of sales-tax bonds. It took more than a year for its electric company to reach such a deal in December — and it still hasn’t been completed.

"The House Super Chapter 9 bankruptcy

legislation would violate the priority given to general-obligation bonds

under Puerto Rico’s constitution, which

Congress has already twice affirmed.”

— ANDREW ROSENBERG, PAUL WEISS RIFKIND WHARTON & GARRISON

A group of general-obligation bondholders that includes Monarch Alternative Capital, Davidson Kempner Capital Management and Stone Lion Capital Partners are among those opposed to the House legislation, which would give a federally-appointed board power to oversee Puerto Rico’s budget and a restructuring with creditors. The bondholders, who have hired former U.S. Representative to lobby on Connie Macktheir behalf, say the legislation threatens

their rights to be paid back first.“The House Super Chapter 9

bankruptcy legislation would violate the priority given to general-obligation bonds under Puerto Rico’s constitution, which Congress has already twice affirmed,”

, a lawyer at Paul Andrew RosenbergWeiss Rifkind Wharton & Garrison, which is representing the GO bondholder group, said in a statement. “As a result, the holders of $18 billion of GO and commonwealth-guaranteed bonds could assert takings claims against the U.S. government.”

That position has put them at odds with a rival group that holds $1.6 billion of securities known as Cofinas that are backed by a share of Puerto Rico’s sales taxes. The group includes GoldenTree Asset Management, Merced Capital, Tilden Park Capital Management and Whitebox Advisors. , a Judd Greggformer U.S. Senator from New Hampshire, is advising the group.

Those bondholders anticipate that the federal oversight panel would honor their claims more than Puerto Rico, which has already siphoned off gas- and rum-tax revenue pledged to some debt to avoid defaulting on general obligations. The group is concerned that Puerto Rico may begin redirecting sales-tax revenue as soon as July to help pay other expenses, something the House bill may prevent.

“We feel that the chances of our property rights being properly respected are greater in the hands of disinterested, dispassionate control board members than they would be in the hands of the administration in Puerto Rico, which seems to treat all property as house money,” said , a Susheel Kirpalanipartner at Quinn Emanuel Urquhart & Sullivan, which is representing the holders of the sales-tax debt.

House lawmakers were shooting to have a legislative fix for Puerto Rico done by the end of March, only to see the process take longer than anticipated. The bill won’t be voted on by the House Natural Resources Committee until next week at the earliest because it’s still being revised, according to Democratic and Republican aides to the committee.

April 19, 2016 Bloomberg Brief Municipal Market 3

Q&A

April 19, 2016 Bloomberg Brief Municipal Market 4

Q&A

About 96 Percent of Rating Outlooks on Public Power Sector Are Stable: Moody's

A big challenge facing the public power sector is

the potential capital requirements needed,

according to a report by Moody's Investors

Service. To the extent substantial capital

investments are made, how public power utilities

finance those investments will have an impact on

ratings. , associate managing AJ Sabatelle

director of project finance at Moody’s, spoke with

Bloomberg Radio’s Taylor Riggs. His comments

have been edited and condensed.

Q: Despite all of the problems we’ve heard about the oil and the energy sector, overall at Moody’s the rating and outlook changes have been trending positive. Why is that?A: It’s a reflection of the sector which historically has a very stable sector outlook. Something like 96 percent of the rating outlooks on that sector are stable. That’s primarily because you have a monopoly system and generally speaking the municipal sector tends to have lower rates than their investor-owned brethren, so what makes them an attractive business model is they can offer competitive rates, and have been able to do that for an extended period of time.

Q: You also write there’s been a willingness or ability to increase rates to help cover costs. What are some of the electric power municipal districts that have been doing an especially good job?A: The sector is very highly rated and has a stable outlook but the report highlights some examples of the last two years. Of the 24 rating changes, 17 were upgrades and seven were downgrades, so certainly a sizable amount of upgrades relative to downgrades. Some of the issuers that are on the list are Sacramento Municipal Utility District. We upgraded them to Aa3 from A1 and that was the case of them putting in place some incremental rate increases as well as having some strength in their over all service territory. Another example of an entity we

upgraded was the city of Anaheim. And that was a case where they made some changes to their rate design and by doing so it kept rates flat but it improved the overall credit metrics.

Q: How has the drop in oil prices affected these over the years, if at all? Does that even play a role?A: It does indirectly. Probably more so with the drop in natural gas prices and primarily because any drop in commodity prices, to the extent that they use that fuel source to generate electricity, results in a lower rate for the end-use customer. So it does enable them, if they were thinking of putting through a rate increase for infrastructure expansion, it makes it easier to do so because your cost of electricity from the commodity side has gone down. And so low commodity prices for a regulated utility tends to be a good thing.

Q: I know you also highlight regulatory relationships, and being in New York and New Jersey the Long Island Power Authority was under a lot of scrutiny after Hurricane Sandy. How have regulatory relationships changed over the years?A: LIPA now has to go before the New York Public Service Commission to implement rates. And I think while there was some concern about that — that’s an additional layer of scrutiny that typically isn’t there for most of these issuers — the performance so far has been quite good.

And the biggest thing that change did was improve transparency. The commission and interested parties understood what LIPA was asking for. The other thing with LIPA was bringing in Public Service Electric & Gas Company to operate the system. Their ability to respond to storms and the like has improved dramatically.

Q: One of the major challenges facing the sector are the capital requirements and getting the money to make some capital investments. If they take on more debt, how does that play into the ratings? Are you still going in pretty bullish on the sector?A: To the extent there is substantial capital investment, how they finance that really does have implications for how it affects the ratings. As a good example that we talk about, Santee Cooper is building a nuclear power plant in South Carolina and while that’s had its own sets of problems with delays and cost overruns, what’s really strengthened the over all credit quality is the utility implemented sizable rate increases in 2016 and 2017 to basically pass through this incremental debt service that is associated with the construction of the plant. It definitely has the potential to weaken credit quality, but it really comes down to how managements respond, how they finance it and if they implement rate increases.

Career History: Moody’s Investors Service 1997-2016; Bank of New York Mellon 1985-1997 (analyst/banker covering the broad infrastructure related sectors, both public-owned and investor-owned)Education: Columbia University, AB, Economics; New York University, Stern School of Business, MBA - Finance

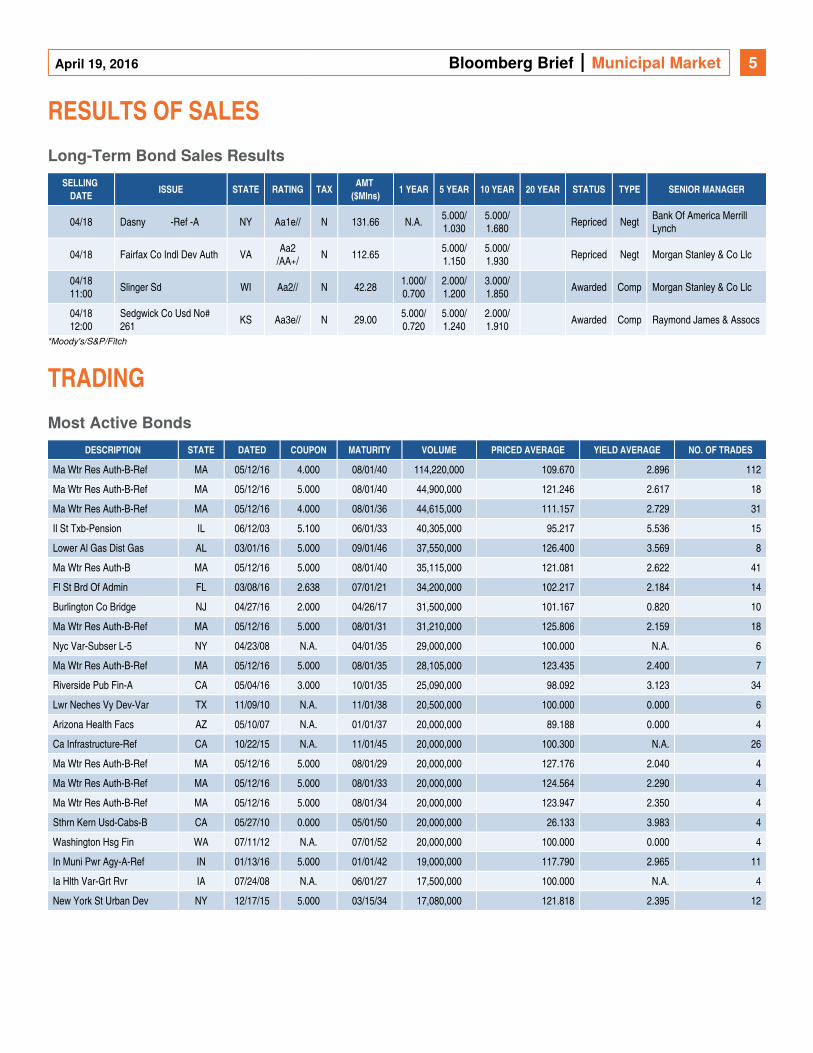

RESULTS OF SALES

April 19, 2016 Bloomberg Brief Municipal Market 5

Long-Term Bond Sales Results

SELLING DATE

ISSUE STATE RATING TAXAMT

($Mlns)1 YEAR 5 YEAR 10 YEAR 20 YEAR STATUS TYPE SENIOR MANAGER

04/18 Dasny -Ref -A NY Aa1e// N 131.66 N.A.5.000/1.030

5.000/1.680

Repriced NegtBank Of America Merrill Lynch

04/18 Fairfax Co Indl Dev Auth VAAa2

/AA+/N 112.65

5.000/1.150

5.000/1.930

Repriced Negt Morgan Stanley & Co Llc

04/1811:00

Slinger Sd WI Aa2// N 42.281.000/0.700

2.000/1.200

3.000/1.850

Awarded Comp Morgan Stanley & Co Llc

04/1812:00

Sedgwick Co Usd No# 261

KS Aa3e// N 29.005.000/0.720

5.000/1.240

2.000/1.910

Awarded Comp Raymond James & Assocs

*Moody's/S&P/Fitch

Most Active Bonds

DESCRIPTION STATE DATED COUPON MATURITY VOLUME PRICED AVERAGE YIELD AVERAGE NO. OF TRADES

Ma Wtr Res Auth-B-Ref MA 05/12/16 4.000 08/01/40 114,220,000 109.670 2.896 112

Ma Wtr Res Auth-B-Ref MA 05/12/16 5.000 08/01/40 44,900,000 121.246 2.617 18

Ma Wtr Res Auth-B-Ref MA 05/12/16 4.000 08/01/36 44,615,000 111.157 2.729 31

Il St Txb-Pension IL 06/12/03 5.100 06/01/33 40,305,000 95.217 5.536 15

Lower Al Gas Dist Gas AL 03/01/16 5.000 09/01/46 37,550,000 126.400 3.569 8

Ma Wtr Res Auth-B MA 05/12/16 5.000 08/01/40 35,115,000 121.081 2.622 41

Fl St Brd Of Admin FL 03/08/16 2.638 07/01/21 34,200,000 102.217 2.184 14

Burlington Co Bridge NJ 04/27/16 2.000 04/26/17 31,500,000 101.167 0.820 10

Ma Wtr Res Auth-B-Ref MA 05/12/16 5.000 08/01/31 31,210,000 125.806 2.159 18

Nyc Var-Subser L-5 NY 04/23/08 N.A. 04/01/35 29,000,000 100.000 N.A. 6

Ma Wtr Res Auth-B-Ref MA 05/12/16 5.000 08/01/35 28,105,000 123.435 2.400 7

Riverside Pub Fin-A CA 05/04/16 3.000 10/01/35 25,090,000 98.092 3.123 34

Lwr Neches Vy Dev-Var TX 11/09/10 N.A. 11/01/38 20,500,000 100.000 0.000 6

Arizona Health Facs AZ 05/10/07 N.A. 01/01/37 20,000,000 89.188 0.000 4

Ca Infrastructure-Ref CA 10/22/15 N.A. 11/01/45 20,000,000 100.300 N.A. 26

Ma Wtr Res Auth-B-Ref MA 05/12/16 5.000 08/01/29 20,000,000 127.176 2.040 4

Ma Wtr Res Auth-B-Ref MA 05/12/16 5.000 08/01/33 20,000,000 124.564 2.290 4

Ma Wtr Res Auth-B-Ref MA 05/12/16 5.000 08/01/34 20,000,000 123.947 2.350 4

Sthrn Kern Usd-Cabs-B CA 05/27/10 0.000 05/01/50 20,000,000 26.133 3.983 4

Washington Hsg Fin WA 07/11/12 N.A. 07/01/52 20,000,000 100.000 0.000 4

In Muni Pwr Agy-A-Ref IN 01/13/16 5.000 01/01/42 19,000,000 117.790 2.965 11

Ia Hlth Var-Grt Rvr IA 07/24/08 N.A. 06/01/27 17,500,000 100.000 N.A. 4

New York St Urban Dev NY 12/17/15 5.000 03/15/34 17,080,000 121.818 2.395 12

RESULTS OF SALES

TRADING

ACCORDING TO

April 19, 2016 Bloomberg Brief Municipal Market 6

ACCORDING TO

The margin of safety for the U.S. Virgin Islands' public-power utility is shrinking, according to Fitch Ratings.

Citing the utility's liquidity constraints, Fitch cut its rating on the U.S. Virgin Islands Water and Power Authority's electric system and subordinated revenue bonds on Friday. Fitch lowered its rating on the authority's $127 million electric system revenue bonds to BB- from BB and its $100.1 million electric system subordinated revenue bonds to B+ from BB-. Fitch also placed the bonds on negative rating watch.

WAPA faces financial strain due to overdue receivables from the Virgin Islands government, Fitch analysts led by

wrote. Since Christopher Hessenthalerfiscal 2013, the authority's total government receivables have risen by about 84 percent to $46.9 million as of Dec. 31, 2015, according to Fitch.

A lawsuit filed by Trafigura Trading has also added pressure on the utility, Fitch

U.S. Virgin Islands' Utility Cut by Fitch

analysts said. Trafigura's lawsuit alleges that WAPA owes the fuel supplier about $25 million in fuel delivery charges.

WAPA, which provides electricity to about 55,000 customers, also serves a challenged territory, the Fitch analysts added. The Virgin Islands' economy relies on tourism and government jobs.

"Strains related to the USVI's narrow economy are compounded by the authority's exceptionally high electric rates, declining sales, and per capita personal income levels that approximate just half of the U.S. average," the analysts wrote.

— Amanda Albright, Bloomberg Brief

The brokerage arm of Wells Fargo & Co., the third-biggest U.S. bank by assets, was designated a U.S. primary dealer by the Federal Reserve Bank of New York yesterday. It’s the first addition to the list since February 2014, when the

Wells Fargo Joins Exclusive Bond Market Club

U.S.-based brokerage of Toronto-Dominion Bank was included. The roster of primary dealers has grown to 23 firms from as low as 17 in 2008, although it remains below its 1988 peak of 46.

“A long process of working with the Fed has come to a conclusion,” said Elise

, a spokeswoman for San WilkinsonFrancisco-based Wells Fargo. “The scope and scale of what we’ve been doing, it’s been at the level of a primary dealer for a long time.” The process took years, Wilkinson said, declining to elaborate.

The addition of Wells Fargo Securities LLC signals the arrival of a large competitor in a market where roughly $500 billion trades daily, according to the Securities Industry and Financial Markets Association. It’s the first U.S.-based bond dealer to join the list since MF Global Holdings Ltd. in 2011, which was dropped before the end of that year after the firm’s collapse.

— Alexandra Scaggs and Laura J. Keller,

Bloomberg News

TWEET OF THE DAY BY JOE MYSAK, BLOOMBERG BRIEF

April 19, 2016 Bloomberg Brief Municipal Market 7

Find Muni Data on the Bloomberg Terminal

DATA FREQUENCY ON THE TERMINAL

AAA Benchmark Valuation Daily GC I493 <GO>

Benchmark State Yields Daily MBM <GO>

VRDO Rates, Inventory Daily MBIX <GO>, ALLX BVRD <GO>

Upcoming Sales Daily CDRA <GO>

Volume, MSRB, PICK Daily SPLY <GO>, YTDM <GO>, MSRB <GO>, MBIX <GO>

Results of Sales Daily CDRA <GO>

Most Active Daily MSRB <GO>

Most Searched DES Every Wednesday SECF <GO>

Variable-Rate Calendar Every Thursday CDRV <GO>

Most Traded Borrowers Every Friday MFLO <GO>

Week-Ahead Calendar Every Monday CDRA <GO>

Supply and Demand Every Friday SPLY <GO>, BVMB <GO>

Muni Credit Risk Every Monday MRSK <GO>

TWEET OF THE DAY BY JOE MYSAK, BLOOMBERG BRIEF

Borrowing Regularly and Chapter 9 Don't Mix

MuniNetGuide@MuniNetGuide

Jim Spiotto's Insight into Ch. 9 Bankruptcy as Remedy for Distressed School Districts PART ONE muninetguide.com/chapter-9-

best… #muniland #schoolsDetails

MuniNetGuide tweets a link to an article by bankruptcy specialist (and MuniNetGuide co-publisher) James

, concerning school districts Spiottoand why they usually don't avail themselves of Chapter 9.

Bloomberg Brief:Municipal Market

Newsletter Managing Editor

Jennifer Rossa

Municipal Market Editor

Joe Mysak

Municipal Market Reporter

Amanda Albright

Brief Editor

Siobhan Wagner

Contributing Analyst

Sowjana Sivaloganathan

Municipal Data Team

Marketing & Partnership Director

Johnna Ayres

+1-212-617-1833

Advertising

Christopher Konowitz

+1-212-617-4694

Reprints & Permissions

Lori Husted

+1-717-505-9701 x2204

Interested in learning more about the Bloomberg

terminal? Request a free demo .here

This newsletter and its contents may not be

forwarded or redistributed without the prior

consent of Bloomberg. Please contact our

reprints and permissions group listed above for

more information. Bloomberg believes the

information herein came from reliable sources,

but does not guarantee its accuracy.

© 2016 Bloomberg LP. All rights reserved.

Related Documents