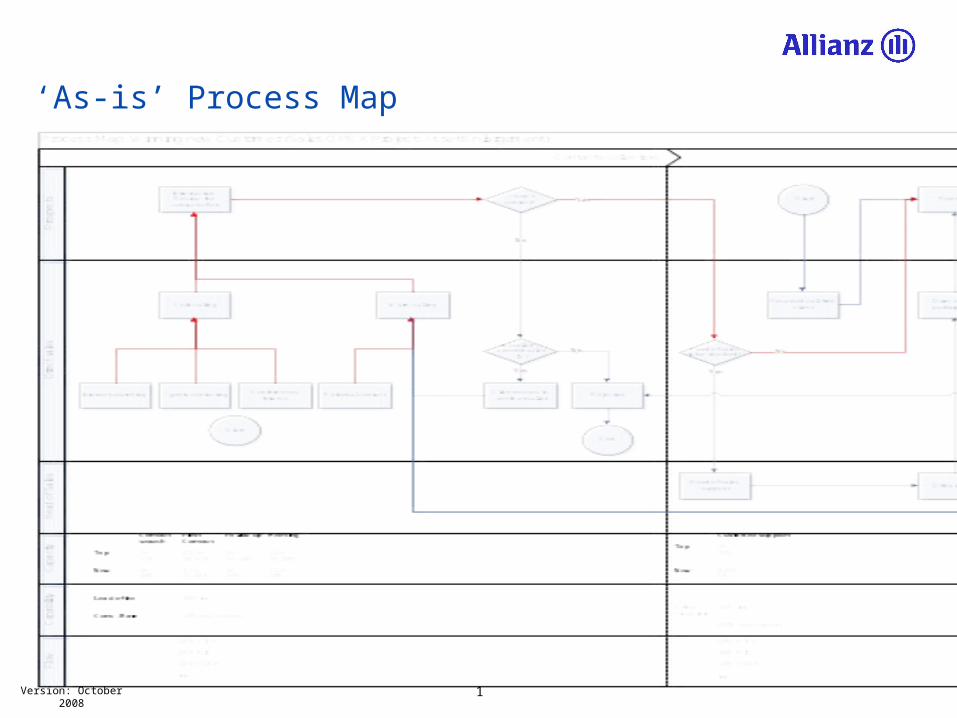

1 Version: October 2008 ‘As-is’ Process Map

Asset enlargement certification part 2

Jul 30, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1Version: October 2008

‘As-is’ Process Map

2Version: October 2008

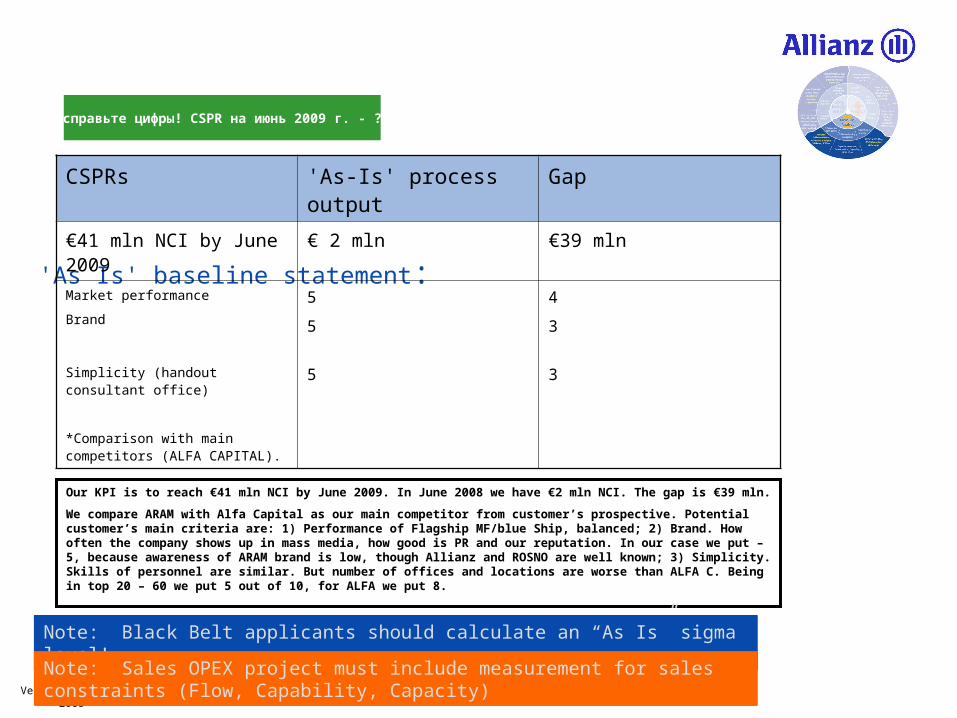

13. 'As Is' baseline statement

Note: Black Belt applicants should calculate an “As Is” sigma level!Note: Black Belt applicants should calculate an “As Is” sigma level!

'As Is' baseline statement:

Note: Sales OPEX project must include measurement for sales constraints (Flow, Capability, Capacity)Note: Sales OPEX project must include measurement for sales constraints (Flow, Capability, Capacity)

CSPRs 'As-Is' process output Gap

€41 mln NCI by June 2009 € 2 mln €39 mln

Market performance

Brand

Simplicity (handout consultant office)

*Comparison with main competitors (ALFA CAPITAL).

5

5

5

4

3

3

Our KPI is to reach €41 mln NCI by June 2009. In June 2008 we have €2 mln NCI. The gap is €39 mln.

We compare ARAM with Alfa Capital as our main competitor from customer’s prospective. Potential customer’s main criteria are: 1) Performance of Flagship MF/blue Ship, balanced; 2) Brand. How often the company shows up in mass media, how good is PR and our reputation. In our case we put – 5, because awareness of ARAM brand is low, though Allianz and ROSNO are well known; 3) Simplicity. Skills of personnel are similar. But number of offices and locations are worse than ALFA C. Being in top 20 – 60 we put 5 out of 10, for ALFA we put 8.

Исправьте цифры! CSPR на июнь 2009 г. - ??

3Version: October 2008

Conclusion:

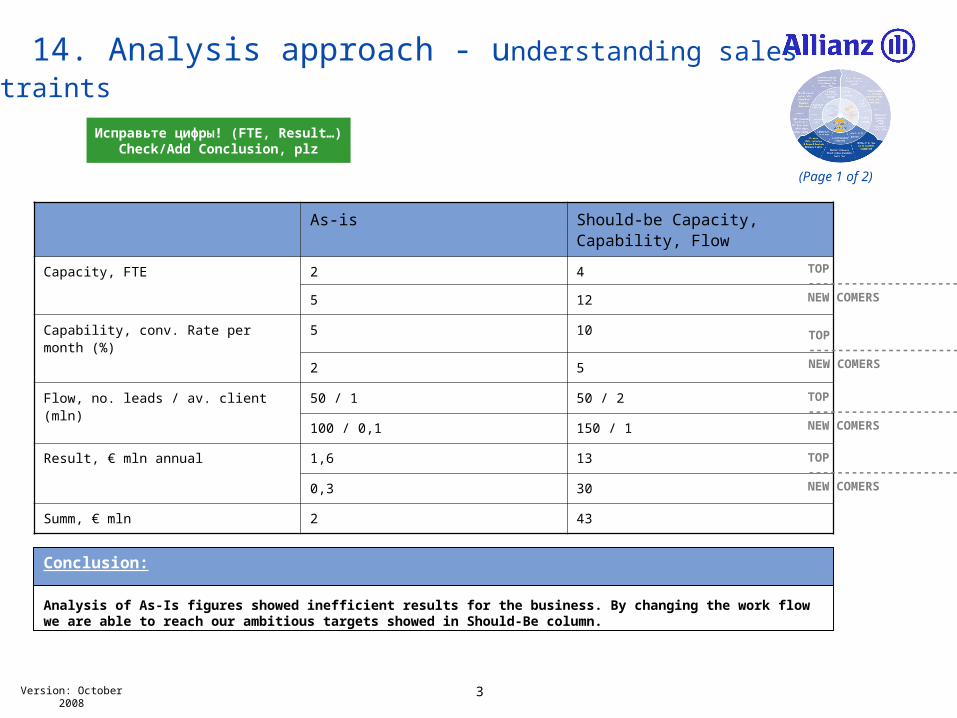

14. Analysis approach - understanding sales constraints

(Page 1 of 2)

As-is Should-be Capacity, Capability, Flow

Capacity, FTE 2 4

5 12

Capability, conv. Rate per month (%) 5 10

2 5

Flow, no. leads / av. client (mln) 50 / 1 50 / 2

100 / 0,1 150 / 1

Result, € mln annual 1,6 13

0,3 30

Summ, € mln 2 43

TOP----------------------NEW COMERS

TOP----------------------NEW COMERS

TOP----------------------NEW COMERS

TOP----------------------NEW COMERS

Исправьте цифры! (FTE, Result…)Check/Add Conclusion, plz

Analysis of As-Is figures showed inefficient results for the business. By changing the work flow we are able to reach our ambitious targets showed in Should-Be column.

4Version: October 2008

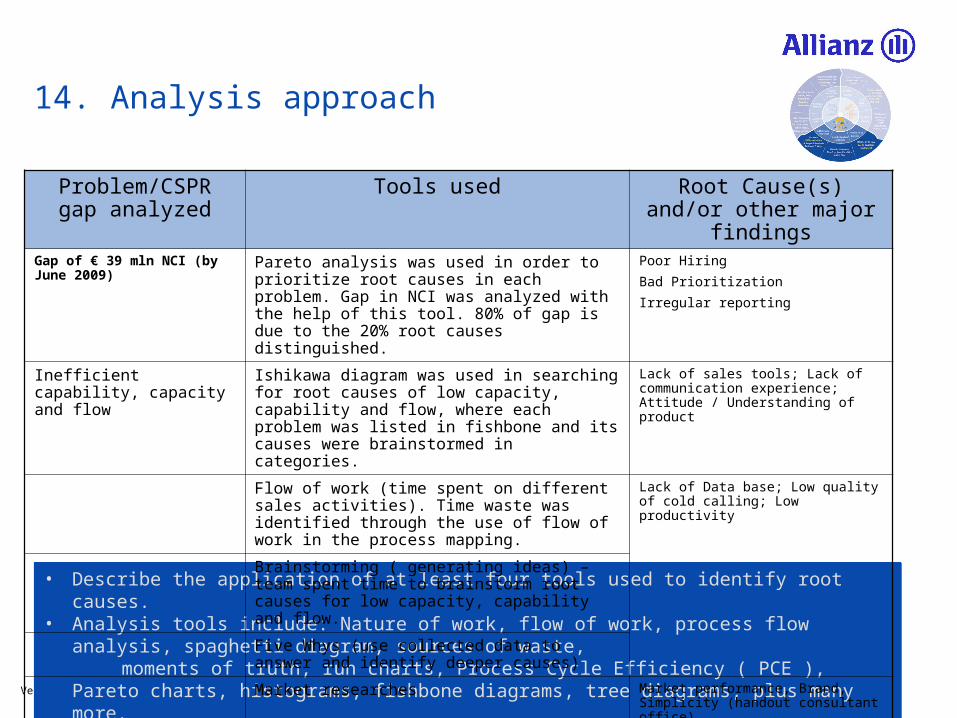

14. Analysis approach

• Describe the application of at least four tools used to identify root causes.• Analysis tools include: Nature of work, flow of work, process flow analysis, spaghetti diagram, sources of waste, moments of truth, run charts, Process Cycle Efficiency ( PCE ), Pareto charts, histograms, fishbone diagrams, tree

diagrams, plus many more.• Supporting documentation can be attached to this page ( if required ).

• Describe the application of at least four tools used to identify root causes.• Analysis tools include: Nature of work, flow of work, process flow analysis, spaghetti diagram, sources of waste, moments of truth, run charts, Process Cycle Efficiency ( PCE ), Pareto charts, histograms, fishbone diagrams, tree

diagrams, plus many more.• Supporting documentation can be attached to this page ( if required ).

Problem/CSPR gap analyzed

Tools used Root Cause(s) and/or other major findings

Gap of € 39 mln NCI (by June 2009)

Pareto analysis was used in order to prioritize root causes in each problem. Gap in NCI was analyzed with the help of this tool. 80% of gap is due to the 20% root causes distinguished.

Poor Hiring

Bad Prioritization

Irregular reporting

Inefficient capability, capacity and flow

Ishikawa diagram was used in searching for root causes of low capacity, capability and flow, where each problem was listed in fishbone and its causes were brainstormed in categories.

Lack of sales tools; Lack of communication experience; Attitude / Understanding of product

Flow of work (time spent on different sales activities). Time waste was identified through the use of flow of work in the process mapping.

Lack of Data base; Low quality of cold calling; Low productivity

Brainstorming ( generating ideas) – team spent time to brainstorm root causes for low capacity, capability and flow.

Five Whys (use collected data to answer and identify deeper causes)

Market researches Market performance, Brand, Simplicity (handout consultant office)

5Version: October 2008

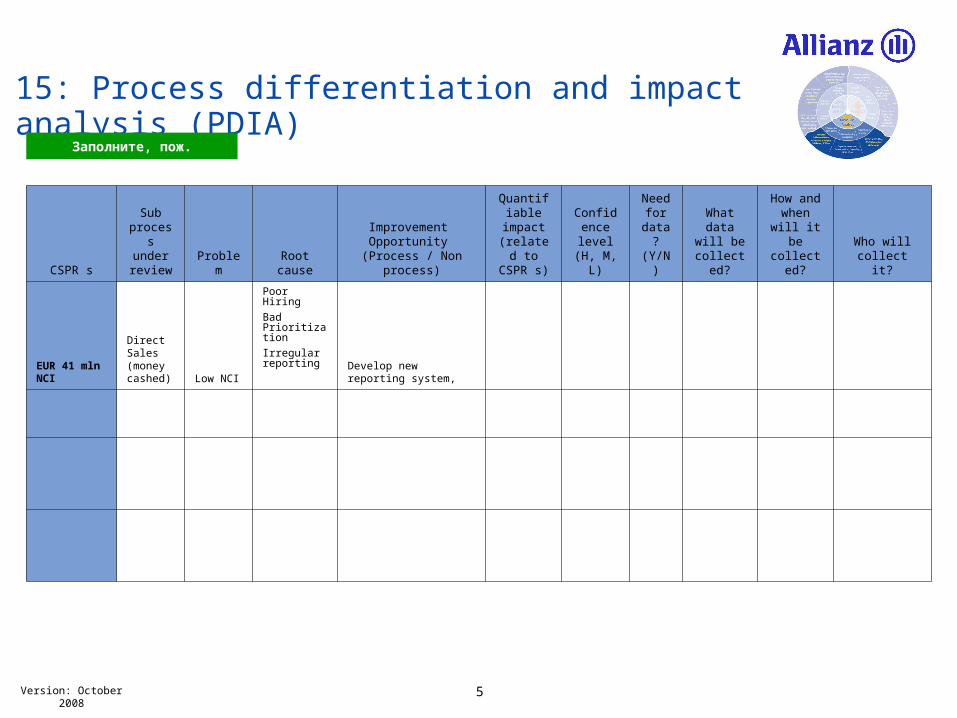

15: Process differentiation and impact analysis (PDIA)

CSPR s

Sub process under review Problem Root cause

Improvement Opportunity

(Process / Non process)

Quantifiable impact (related to CSPR s)

Confidence level (H, M, L)

Need for

data? (Y/N)

What data will be

collected?

How and when will

it be collected?

Who will collect it?

EUR 41 mln NCI

Direct Sales (money cashed) Low NCI

Poor Hiring

Bad Prioritization

Irregular reporting Develop new reporting

system,

Заполните, пож.

6Version: October 2008

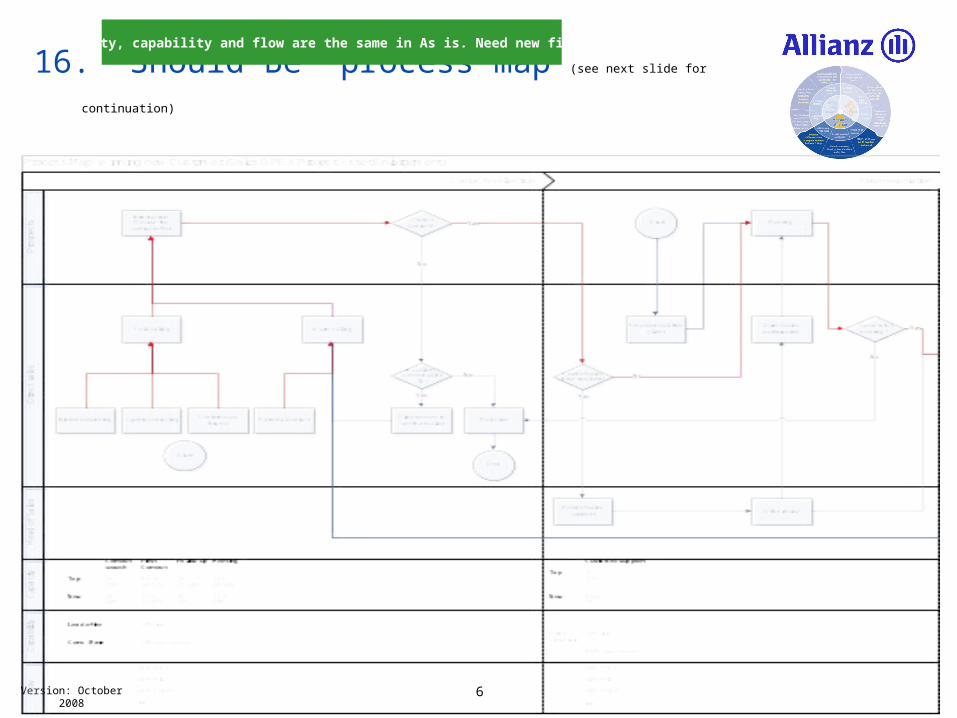

16. 'Should Be' process map (see next slide for continuation)

Capacity, capability and flow are the same in As is. Need new figures!

7Version: October 2008

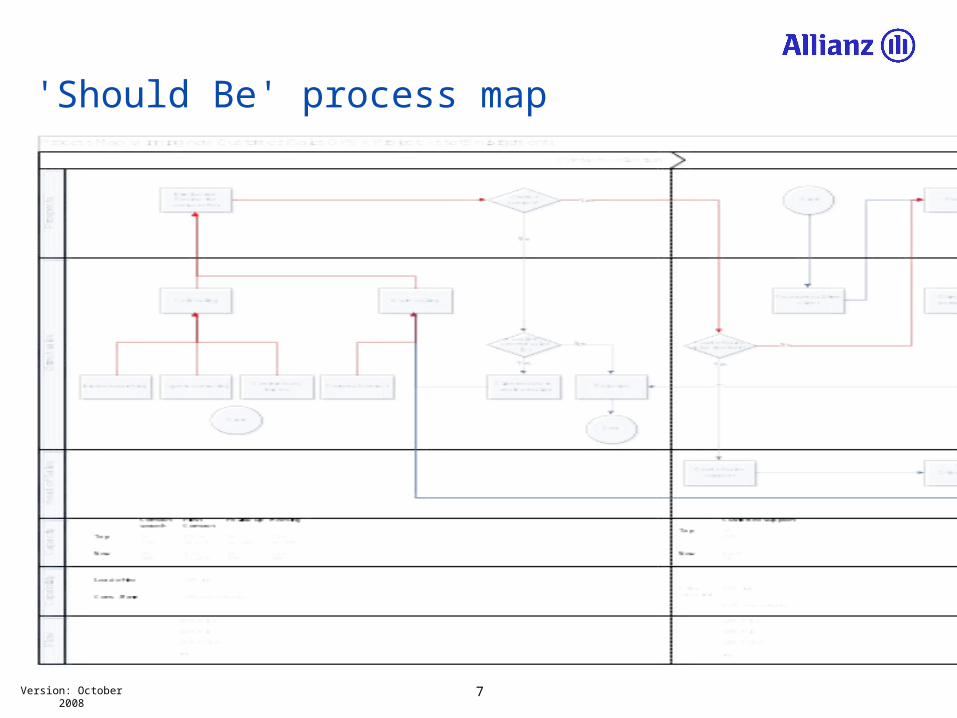

'Should Be' process map

8Version: Oct. 2008

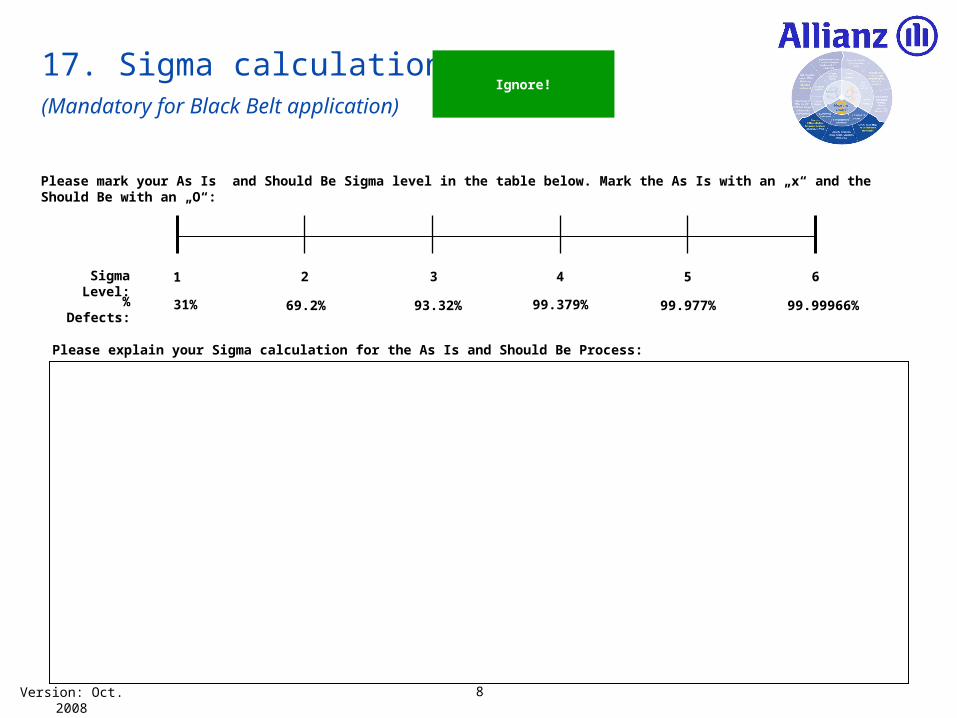

17. Sigma calculation (Mandatory for Black Belt application)

Sigma Level: 1 2 3 4 5 6

% Defects: 31% 69.2% 93.32% 99.379% 99.977% 99.99966%

Please explain your Sigma calculation for the As Is and Should Be Process:

Please mark your As Is and Should Be Sigma level in the table below. Mark the As Is with an „x“ and the Should Be with an „O“:

Ignore!

9Version: October 2008

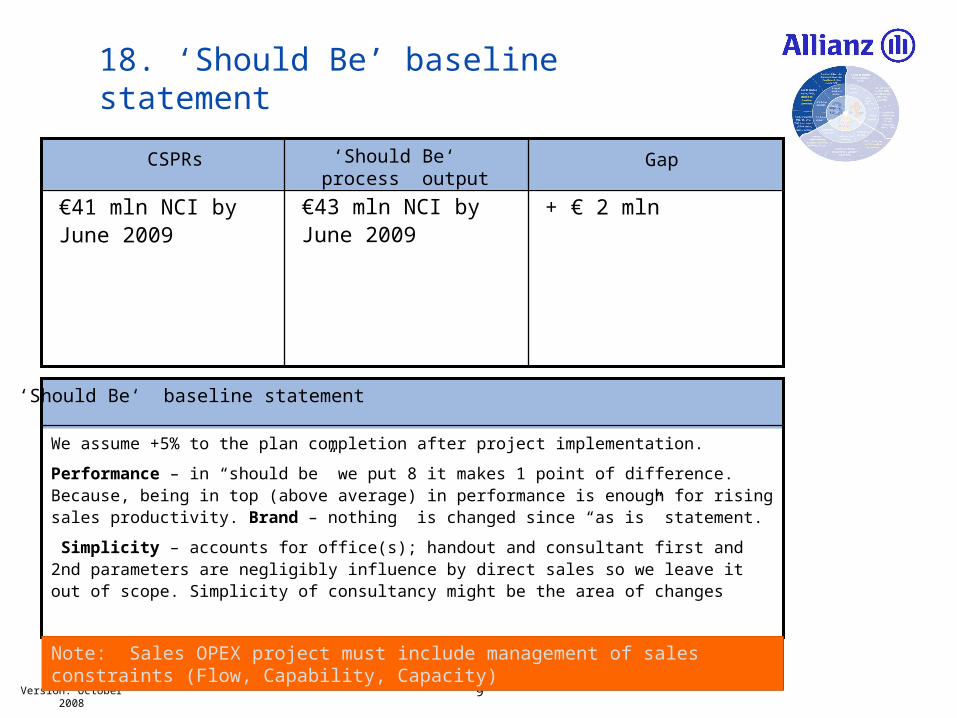

18. ‘Should Be’ baseline statement

We assume +5% to the plan completion after project implementation.

Performance – in “should be” we put 8 it makes 1 point of difference. Because, being in top (above average) in performance is enough for rising sales productivity. Brand – nothing is changed since “as is” statement.

Simplicity – accounts for office(s); handout and consultant first and 2nd parameters are negligibly influence by direct sales so we leave it out of scope. Simplicity of consultancy might be the area of changes

‘Should Be‘ baseline statement

CSPRs ‘Should Be‘ process output

Gap

Note: Sales OPEX project must include management of sales constraints (Flow, Capability, Capacity)Note: Sales OPEX project must include management of sales constraints (Flow, Capability, Capacity)

€41 mln NCI by June 2009

€43 mln NCI by June 2009

+ € 2 mln

10Version: October 2008

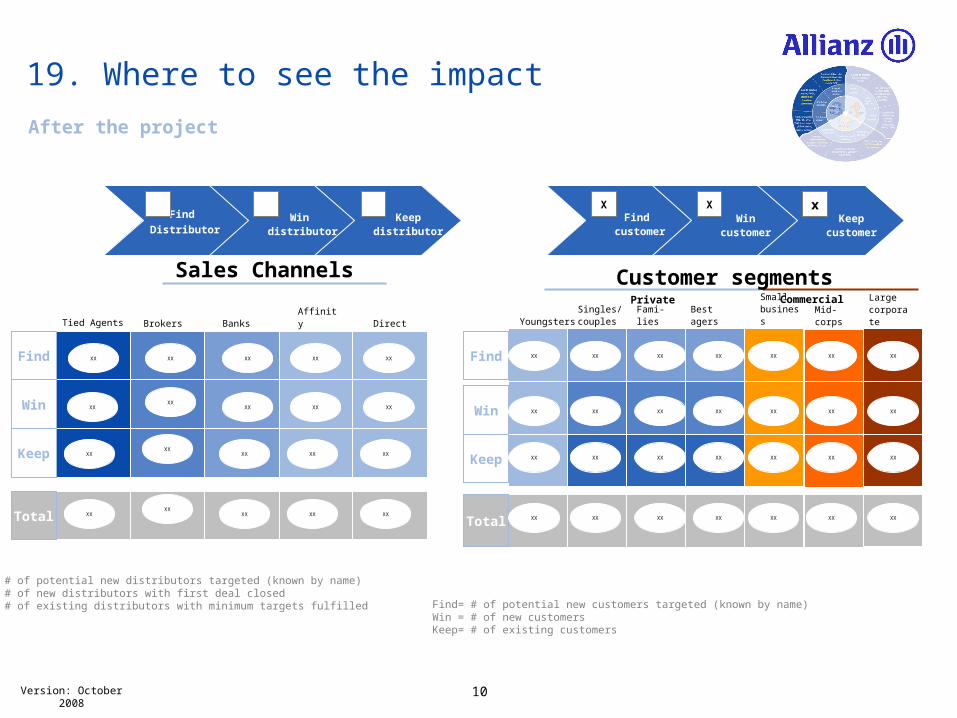

19. Where to see the impact

Find

DistributorWin

distributorKeep

distributorFind

customerWin

customerKeep

customer

X X x

After the project

YoungstersSingles/ couples

Fami-lies

Best agers

PrivateSmall business

Mid-corps

Large corporate

Commercial

Tied Agents Brokers Banks Affinity

Sales Channels

Direct

Customer segments

XXFind

Win

Keep

Total

Find= # of potential new distributors targeted (known by name)Win = # of new distributors with first deal closed Keep= # of existing distributors with minimum targets fulfilled Find= # of potential new customers targeted (known by name)

Win = # of new customers Keep= # of existing customers

Find

Win

Keep

Total

XX XX XX

XXXX

XX

XX

XX XX

XXXX

XX XX XX

XXXX

XX XX XX

XX XX XX XX XX XX XX

XX XX XX XX XX XX XX

XX XX XX XX XX XX XX

XX XX XX XX XX XX XX

11Version: October 2008

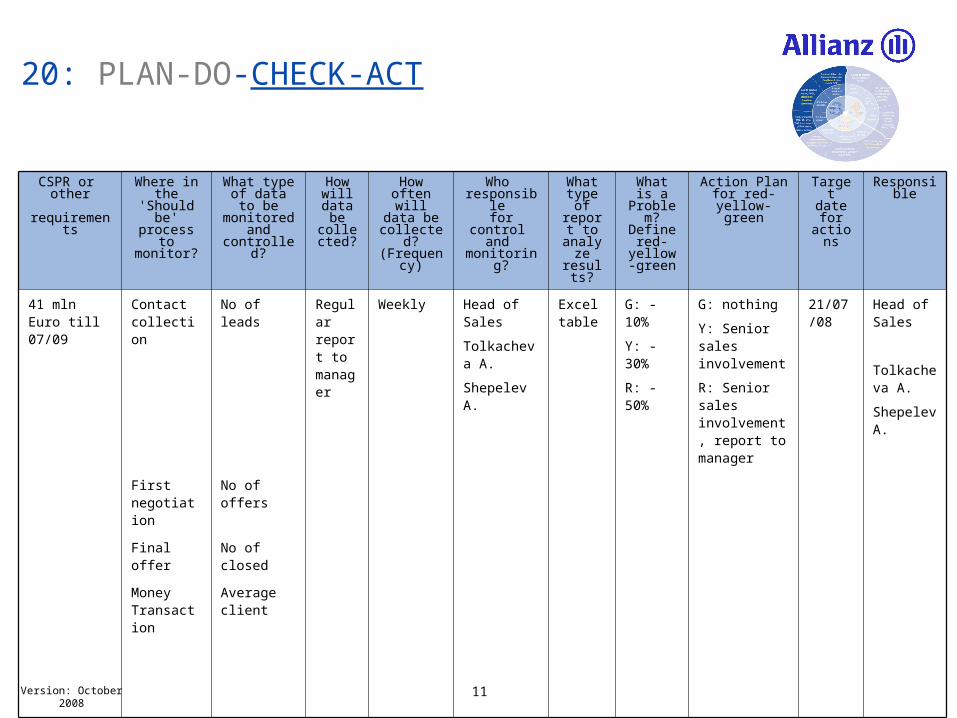

20: PLAN-DO-CHECK-ACT

CSPR or other

requirements

Where in the 'Should be' process to monitor?

What type of data to be

monitored and controlled?

How will data be

collected?

How often will data be collected?

(Frequency)

Who responsible for control

and monitoring?

What type of

report to analyze results?

What is a Problem?

Define red-yellow-green

Action Planfor red-yellow-

green

Target datefor

actions

Responsible

41 mln Euro till 07/09

Contact collection

No of leads Regular report to manager

Weekly Head of Sales

Tolkacheva A.

Shepelev A.

Excel table

G: -10%

Y: -30%

R: -50%

G: nothing

Y: Senior sales involvement

R: Senior sales involvement, report to manager

21/07/08 Head of Sales

Tolkacheva A.

Shepelev A.

First negotiation

No of offers

Final offer No of closed

Money Transaction

Average client

12Version: Oct. 2008

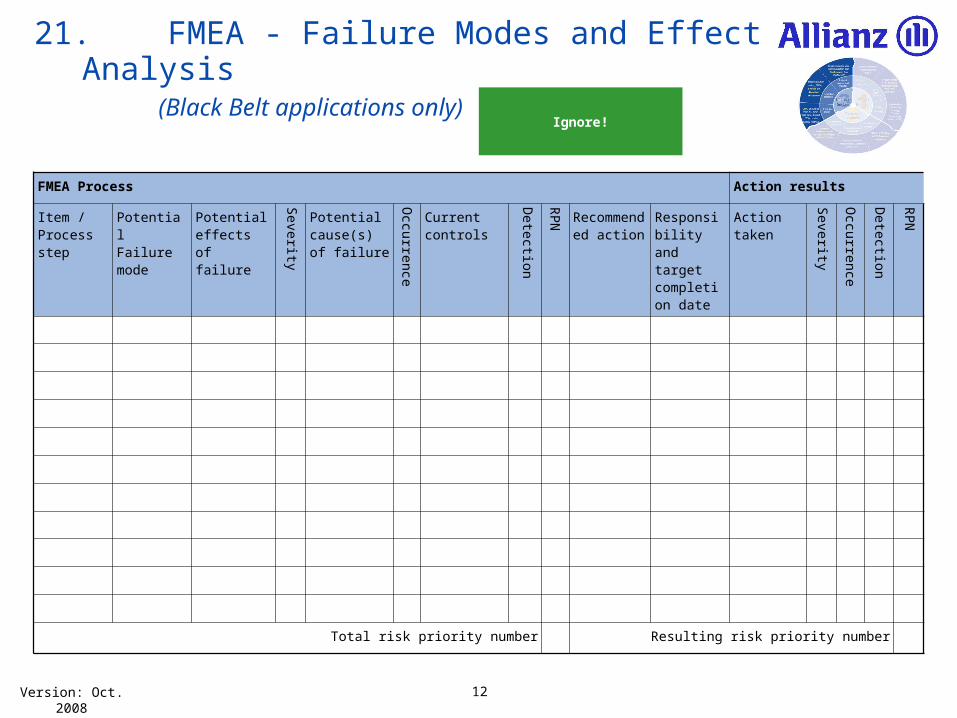

21.FMEA - Failure Modes and Effect Analysis (Black Belt applications only)

FMEA Process Action results

Item / Process step

Potential Failure mode

Potential effects of failure

Severity

Potential cause(s) of failure

Occurrence

Current controls

Detection

RPN Recommended action

Responsibility and target completion date

Action taken

Severity

Occurrence

Detection

RPN

Total risk priority number Resulting risk priority number

Ignore!

13Version: October 2008

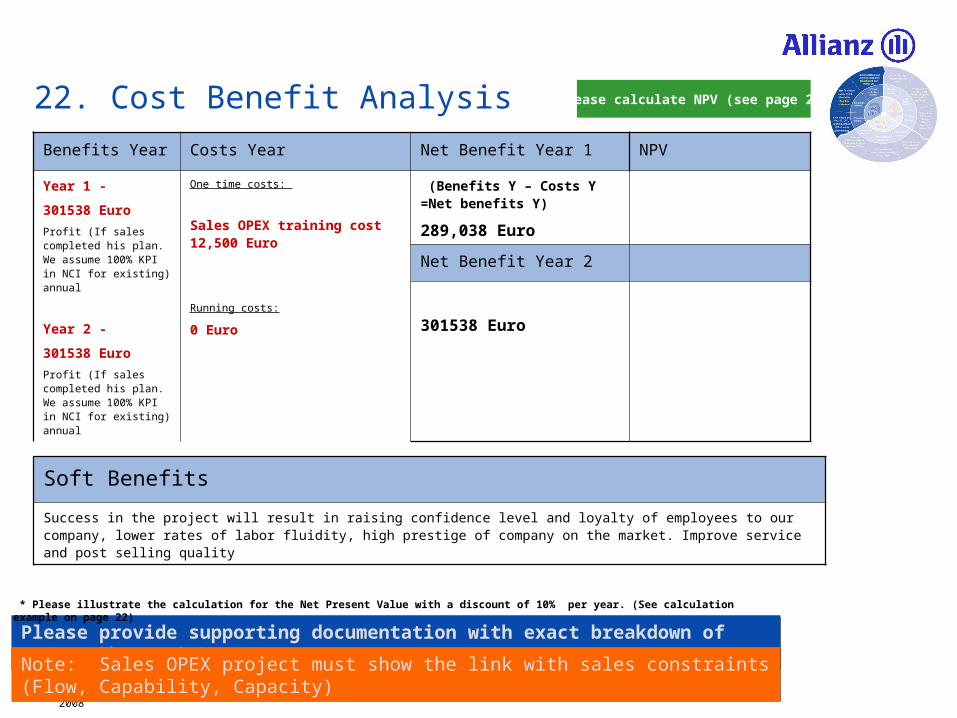

22. Cost Benefit Analysis

Benefits Year Costs Year Net Benefit Year 1 NPV

Year 1 -

301538 Euro

Profit (If sales completed his plan. We assume 100% KPI in NCI for existing) annual

Year 2 -

301538 Euro

Profit (If sales completed his plan. We assume 100% KPI in NCI for existing) annual

One time costs:

Sales OPEX training cost 12,500 Euro

Running costs:

0 Euro

(Benefits Y – Costs Y =Net benefits Y)

289,038 Euro

Net Benefit Year 2

301538 Euro

Please provide supporting documentation with exact breakdown of Benefits and Costs! (see page 23)Please provide supporting documentation with exact breakdown of Benefits and Costs! (see page 23)

* Please illustrate the calculation for the Net Present Value with a discount of 10% per year. (See calculation example on page 22)

Note: Sales OPEX project must show the link with sales constraints (Flow, Capability, Capacity)Note: Sales OPEX project must show the link with sales constraints (Flow, Capability, Capacity)

Soft Benefits

Success in the project will result in raising confidence level and loyalty of employees to our company, lower rates of labor fluidity, high prestige of company on the market. Improve service and post selling quality

Please calculate NPV (see page 22)

14Version: October 2008

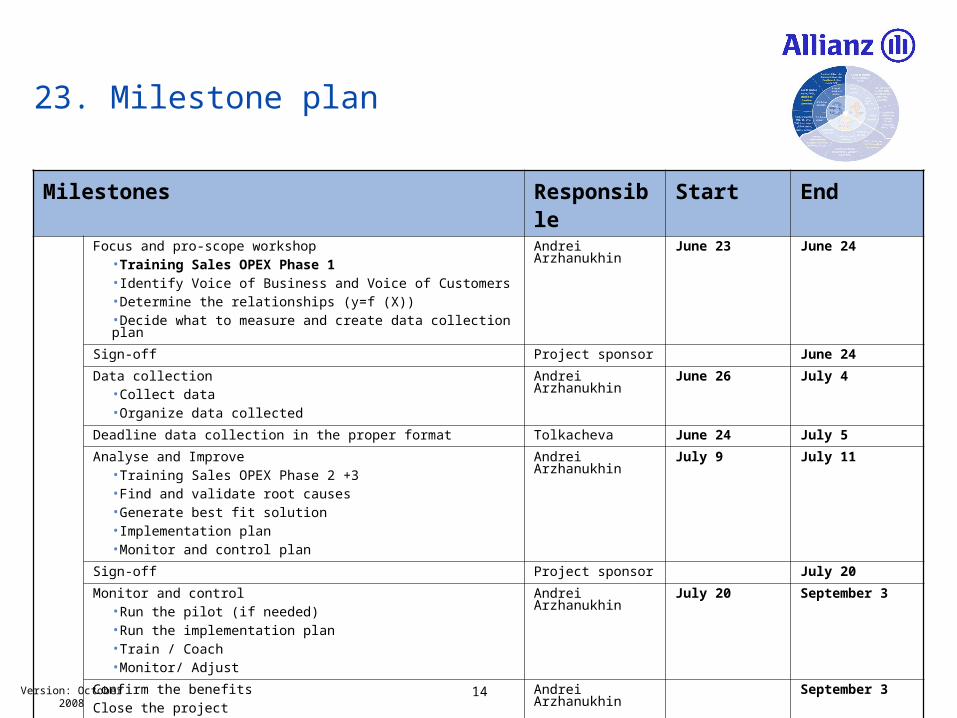

23. Milestone plan

Milestones Responsible Start EndFocus and pro-scope workshop

•Training Sales OPEX Phase 1•Identify Voice of Business and Voice of Customers•Determine the relationships (y=f (X)) •Decide what to measure and create data collection plan

Andrei Arzhanukhin June 23 June 24

Sign-off Project sponsor June 24

Data collection •Collect data•Organize data collected

Andrei Arzhanukhin June 26 July 4

Deadline data collection in the proper format Tolkacheva June 24 July 5

Analyse and Improve•Training Sales OPEX Phase 2 +3•Find and validate root causes •Generate best fit solution•Implementation plan •Monitor and control plan

Andrei Arzhanukhin July 9 July 11

Sign-off Project sponsor July 20

Monitor and control•Run the pilot (if needed)•Run the implementation plan •Train / Coach•Monitor/ Adjust

Andrei Arzhanukhin July 20 September 3

Confirm the benefits

Close the project

Andrei Arzhanukhin September 3

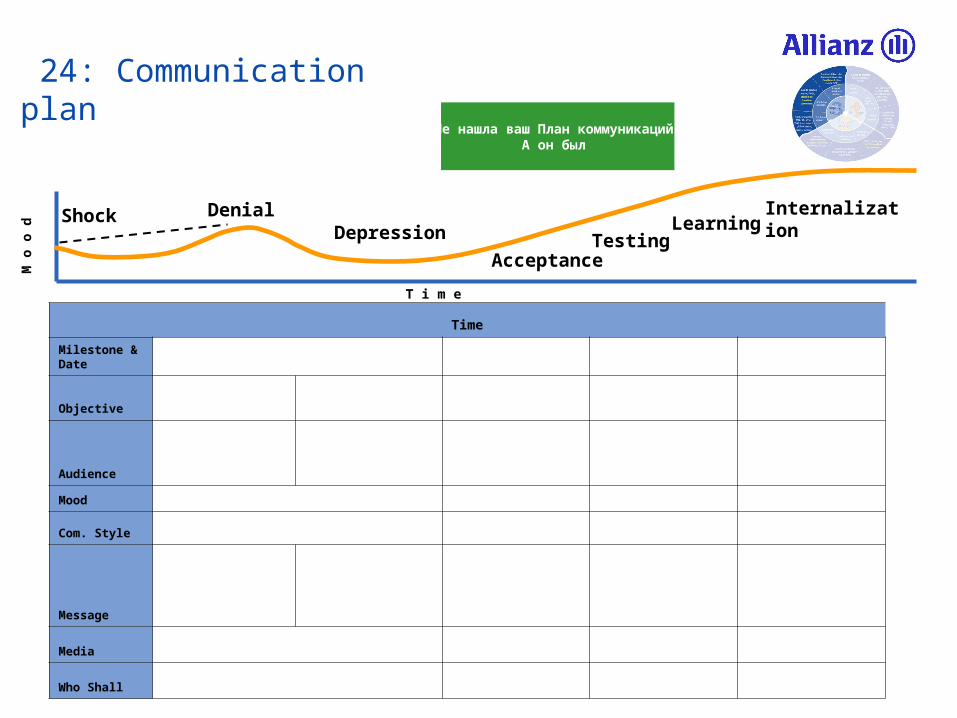

T i m e

M o

o d

Denial ShockDepression

Acceptance

LearningInternalization

Testing

24: Communication plan

Time

Milestone & Date

Objective

Audience

Mood

Com. Style

Message

Media

Who Shall

Не нашла ваш План коммуникаций,А он был

16Version: October 2008

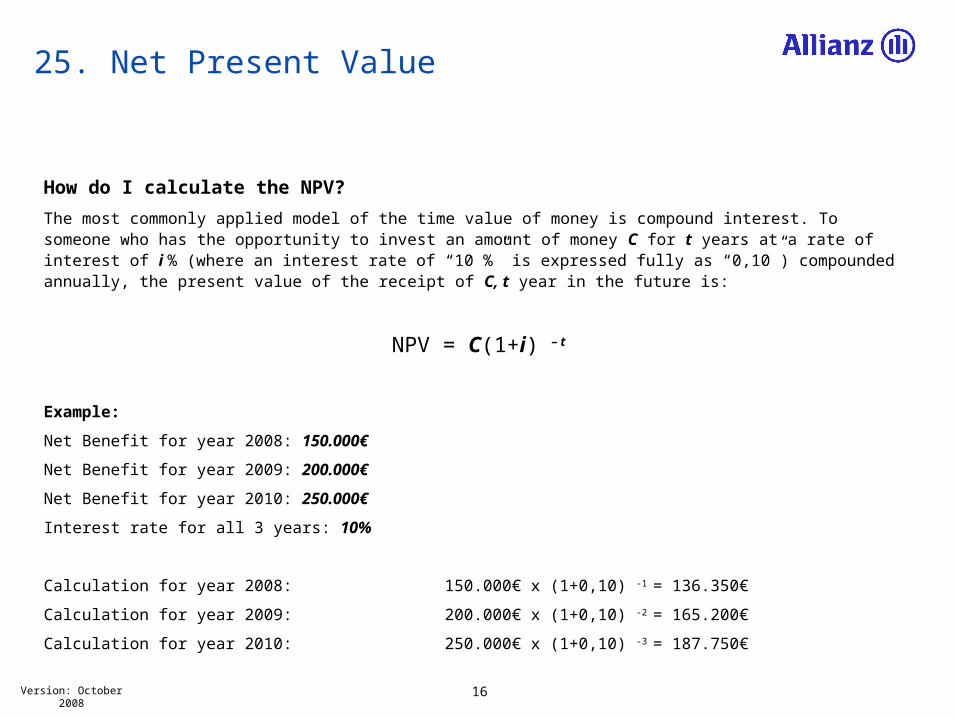

25. Net Present Value

How do I calculate the NPV?

The most commonly applied model of the time value of money is compound interest. To someone who has the opportunity to invest an amount of money C for t years at a rate of interest of i % (where an interest rate of “10 %” is expressed fully as “0,10”) compounded annually, the present value of the receipt of C, t year in the future is:

NPV = C(1+i) – t

Example:

Net Benefit for year 2008: 150.000€

Net Benefit for year 2009: 200.000€

Net Benefit for year 2010: 250.000€

Interest rate for all 3 years: 10%

Calculation for year 2008: 150.000€ x (1+0,10) -1 = 136.350€

Calculation for year 2009: 200.000€ x (1+0,10) -2 = 165.200€

Calculation for year 2010: 250.000€ x (1+0,10) -3 = 187.750€

17Version: October 2008

26. How to complete this form: Hints and tips

Slide Comment

2. Glossary Please complete this slide if you are using internal abbreviations or acronyms unique to your OE.

8. “As Is” process map If your “As Is” process does not fit onto one page, you may use additional pages. Please ensure the entire “As Is” process is included.

12. “Should Be” process map If your “Should Be” process does not fit onto one page, you may use additional page.

Please ensure the entire “Should Be” process is included.

17. Cost Benefit Analysis The breakdown must show how you calculated each item in the benefits and cost column.

You can also attach additional information to support your calculations.

Related Documents