Managerial Economics ADL -04 ADL -04 Managerial Economics is the integration of economic theory with business practices for the purpose of facilitating Decision Making and Forward Planning by the management. ACeL

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Managerial Economics

ADL -04

ADL -04 Managerial Economics is the integration of economic theory with business practices for the purpose of facilitating Decision Making and Forward Planning by the management. ACeL

Table of Contents Chapter 1: MANAGERIAL ECONOMICS ........................................................................................................ 3

Chapter 2: DEMAND ANALYSIS ................................................................................................................... 15

Chapter 3: DEMAND FORECASTING .......................................................................................................... 31

Chapter 4: COST AND OUTPUT ANALYSIS ............................................................................................... 39

Chapter 5: OBJECTIVE OF A BUSINESS FIRM ......................................................................................... 60

Chapter 6: PRICING METHODS ................................................................................................................... 73

Chapter 7: PRODUCTION ANALYSIS .......................................................................................................... 84

Chapter 8: PRICING AND OUTPUT DECISIONS UNDER DIFFERENT MARKET STRUCTURES ................................ 106

Chapter 1: MANAGERIAL ECONOMICS

Managerial Economics is the integration of economic theory with business practices for the purpose of facilitating Decision Making and Forward Planning by the management.

As economics provides as a set of concepts, these concepts furnish us the tools and techniques of analysis. It s in this context economic analysis is an aid to understand business practices in a given environment.

As decision making is a basic function of manager, economics is a valuable guide to the manager.

In the following we shall be discussing the decision making process of the management and how managerial economics and its various tools and techniques help a manager in this process.

DECISION MAKING PROCESS

Decision making is commonly defined a choosing from among alternatives. Decision is a choice made from alternative courses of action in order to deal with a problem. A problem is the difference between a desired situation and the actual situation. Therefore, decision making is the process of choosing among alternative courses of action to solve a problem.

The Decision making process is construed as searching the environment for conditions calling for a decision; inventing, developing and analyzing the available courses of action; and choosing one of the particular courses of action.

A second and more detailed method is the following:

1. Identify the problem. 2. Diagnose the situation. 3. Collect and analyze data relevant to the issue. 4. Ascertain solution that may be used in solving the problem 5. Analyze these alternative solutions. 6. Select the approach that appears most likely to solve the problem 7. Implement it.

A practical example can be found in the following:

Corporate Decision Making : Ford Introduces the Taurus

In late 1985 Ford Introduced the Taurus -a newly designed, aerodynamically styled, front-wheel drive automobile. The car was a huge success at the time and helped Ford almost to double its profits by 1987. The design and efficient production of this car involved not only some impressive engineering advances, but a lot of economics as well.

Ford, had to think carefully about how the public would react to the Taurus design. Would consumers be swayed by the styling and performance of the car? How strong would demand depend on the price Ford changed? Understanding consumer preferences and trade-offs and predicting demand and its responsiveness to price were essential parts of the Taurus program.

Ford had to be concerned with cost of the Car. How high would production costs be, how would this depend on the number of cars for produced each year? How would union wage negotiations or the prices of steel and other raw materials effect costs? How much and how fast would costs decline as managers and workers gained experience with the production process? To maximize profits, how many cars should Ford plan to produce each year?

Ford also had to design a pricing strategy for the car and consider how its competitors would react to this strategy. For example, should Ford charge a low price for the basic stripped-down version of the car but high prices for individual options, such as air conditioning and power steering? Or would it be more comfortable to make these options "Standard" items and charge a high price for the whole package? Whatever prices ford choose, how were its competitors likely to react? Would GM and Chrystler try to under cut Ford by lowering prices? Might Ford be

able to deter GM and Chrysler from lowering prices by threatening to respond with its own price cuts? The Taurus program required a large investment in new capital equipment and Ford had to consider the risks involved and the possible outcomes. Some of this risk was due to uncertainty over the future price of gasoline (Higher gasoline prices would shift demand to smaller cars). What would happen if world oil prices doubled or tripled, or, if the government imposed a new tax on gasoline? How should Ford take these uncertainties into account when making its investment decisions?

Ford also had to worry about organizational problems, Ford is an integrated firm -separate divisions produce engines and parts, then assemble finished cars. How should the managers of the different divisions be rewarded? What price should the assembly division be charged for engines it receives from another division? Should all the parts be obtained from the upstream divisions, or other firms.

All these decision come under managerial decision taking process. We are going to discuss all these in our report.

TYPES OF DECISIONS

Managers make many decisions, in order to answer the following questions:

1. What goods shall firm produce? 2. How should firm raise the necessary capital and what shall be its legal form. 3. What technique shall be adopted, and what shall be the scale of operations? 4. Where production is located? 5. How shall its product be distributed? 6. How shall resources be combined? 7. What shall be the size of output? 8. How shall it deal with its employees?

Managers make these decisions, and in order to obtain a clear understanding of the decision making process, a classification system is useful. Three such systems are available; each based on different types of decisions. They are:

1. Organizational and personal decisions, 2. Basic and routine decisions 3. Programme and non-programme decisions.

Organizational decisions are those executives make in their official role as managers. The adoption of strategies, the setting of objectives and the approval of plans constitute only a few of these. Such decisions are often delegated to others, requiring the support of many people throughout the organizational if they are to be properly implemented.

Personal decisions are related to the managers as an individual, not as a member of the organizations. Such decisions are not delegated to others because their implementation does not require the support of organizational personnel. Deciding to retire, taking a job offer from a competitive firm, or slipping out and spending the afternoon on the golf course are all personal decisions.

A second approach is to classify decisions into basic and routine categories. Basic decisions can be viewed a much more important than routine ones. They involve long-range commitments, large expenditures of funds, and such a degree of importance that a serious mistake might well jeopardize the well being of the company. Selection of a product line, the choice of a new plant site, or a decision to integrate vertically by purchasing sources of raw materials to complement the current production facilities are all basic decisions.

Routine decisions are often repetitive in nature, having only a minor impact on the firm. For this reason, most organizations have formulated a host of procedures to guide the manager in handing these matters. Since some individuals in the organization spend most of their time making routine decisions, these guidelines are very useful to them.

Taking a cue from computer technology, decision could be classified as computer technology programmed and non-programmed. These two types can be viewed on a continuum, programmed being at one end and non-programmed at the other. Programmed decisions correspond roughly to the routine decisions, with procedures playing a key role. Non programmed decisions are similar to the category of basic decisions, being highly novel, important, and unstructured in nature. The value of viewing decision making in this manner is that it permits a clearer understanding of the methods that accompany each type.

CONDITIONS AFFECTING DECISION MAKING

In an ideal business situation, managers would have al of the information they need to make decisions with certainty. Most business situations, however are characterized by incomplete or ambiguous information, which affects the level of certainty with which a manager makes a decision. There are three conditions that affect decision making;

a. Certainty b. Risk c. Uncertainty

Certainty is the condition that exists when decision makes are fully informed about a problem its alternative solutions, and their respective outcomes. Under this condition, individuals can anticipate, and even exercise some control over, events and their outcomes.

In the context of decision making, risk is the condition .that exists when decision-makers must rely on incomplete, yet reliable information. Under a state of risk, the decision-maker does not know with certainty the future outcomes associated with alternative courses of action; the results are subjects to chance. However, the manager has enough information to determine the probabilities associated with each alternative. He or she can then choose. The alternative that has the highest probability of success.

Uncertainty is the condition that exists when little or no factual information is available about a problem, its alternative solution, and their respective outcomes. In a state of uncertainty, the decision-maker does not have enough information to determine the probabilities associated with each alternative. In actually, the decision-maker may have so little information that he or she may be unable even to define the problem, let alone identify alternative solutions and possible outcomes. THE STEPS OF A DECISION MAKING

1. Identifying the problem 2. Generating the alternative course of action 3. Evaluating the alternative 4. Selecting the best alternative 5. Implementing the decision; and 6. Evaluating the decision

The first step in the decision-making process is identifying the problem. Problem identification is probably the most critical art of the decision making process, for it is what determines the direction that the decision making process takes, and , ultimately, the decision that is made.

The second step in decision-making process is generating alternative solutions to the problem. This step involves identifying items or activities that could reduce or eliminate the difference between the actual situation and the desired situation. For this step to be effective, the decision makers must allot enough time to generate creative alternatives as well as ensure that all individuals involved in the process exercise patience and tolerance of others and their ideas.

In the Pursuit of a "quick fix" managers too often shortchange this step by failing to consider more than one or two alternatives, which reduces the opportunity to identify effective solutions.

After generating a list of alternatives, the arduous task of evaluating each of them begins. Numerous methods exist for evaluating the alternatives, including determining the pros and cons of each; performing a cost-benefit analysis for each alternative; and weighting factors important in the decision, ranking each alternative relative to its ability to meet each factor, and then multiplying cumulatively to provide a final value for each alternative.

SELECTING THE BEST ALTERNA TIVE

After the decision-makers have evaluated all the alternatives, it is time for the fourth step in the decision-making process; choosing the best alternative. Depending on the evaluation method used, the selection process can be fairly straightforward. The best alternative could be the one with the most "pros" and the fewest "cons"; the one with the greatest benefits and the lowest costs; or the one with the highest cumulative value, if using weighting.

IMPLEMENTING THE DECISION

This is the step in the decision making process that transforms the selected alternative from an abstract situation into reality. Implementing the decision involves planning and executing the actions that must take place so that the selected alternative can actually solve the problem.

EVALUATING THE DECISION

In evaluating the decision, the sixth and final step in the decision-making process, managers gather information to determine the effectiveness of their decision. Has original problem identified in the first step been resolved? If not, is the company closer to the situation it desired than it was at the beginning of the decision-making process?

DECISION MAKING MODELS

There are basically two major models of decision-making -the classical model and the administrative model. The Classical Model

The classical model of decision making is a prescriptive approach that outlines how managers should make decisions. Also called the rational model, the classical model is based on economic assumptions and asserts that managers are logical, rational individuals who make decision that are in the best interest of the organization. The classical model is characterized by the following assumptions:

1. The manager has completed information about the decision situation and operations under a condition of certainty. 2. The problem is clearly defined, and the decision-maker has knowledge of all possible alternatives and their outcomes. 3. Through the use of quantitative techniques, rationality, and logic, the decision-maker evaluates the alternatives and selects the

optimum alternative -the one that will maximize the decision situation by offering the best solution to the problem.

The Administrative Model

The Administrative model of decision making is a descriptive approach that outlines how managers actually do make decisions. Also called the organizational, neoclassical, or behavioral model, the administrative model is based on the work of economist Herbert A. Simon recognized that people do not always make decisions with logic and rationality, and he introduced two concepts that have become hallmarks of the administrative model- bounded rationality and satisfying.

Bounded Rationality

Bounded rationality means that people have limits, or boundaries, to their rationality. These limits exist because people are bound by their own values and skills, incomplete information, and their own inability-due to time, resource, and rational decisions. Because managers often lack the time of ability to process complete information about complex decisions, they usually wind up having to make decisions with only partial knowledge about alternative solutions and their outcomes. this leads managers often forgo the six steps of decision making in favour of a quicker, yet satisfying, process- satisficing.

The Administrative model of decision making also have some basic assumptions:

1. The manager has incomplete information about the decision situation and operates under a condition of risk or uncertainty. 2. The problem is not clearly defined, and the decision-maker has limited knowledge of possible alternatives and their outcomes. 3. The decision-maker satisfies by choosing the first satisfactory alternative- one that will resolve the problem situation by offering a good solution to the problem.

Decision Making Techniques:

It is useful to examine some of the specific technique that have proved valuable in the decision making process, two of which are marginal analysis and financial analysis.

Marginal Analysis:

The "margin product" of a productive factor is the extra product or output added by one extra unit of that factor, while other factors are being held constant. Labour's marginal product is the extra output you get when you add one unit of Labour holding all other inputs constant. Similarly, land's marginal -product is the change in total product resulting from one additional unit of land with all other inputs held constant.

The manager can use the concept to answer questions such as how much more output will result if one more worker is hired? The answer

often called marginal physical product, provides a basis for determining whether or not one new man will bring about profitable additional output.

Marginal Physical Product

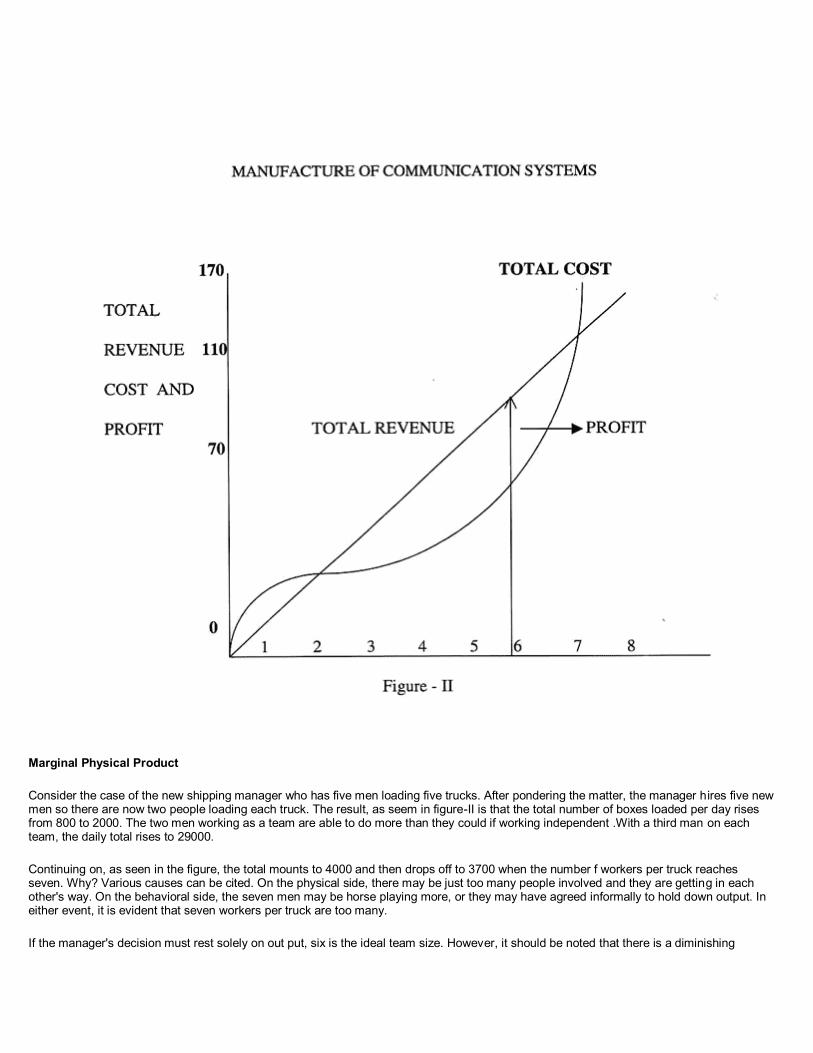

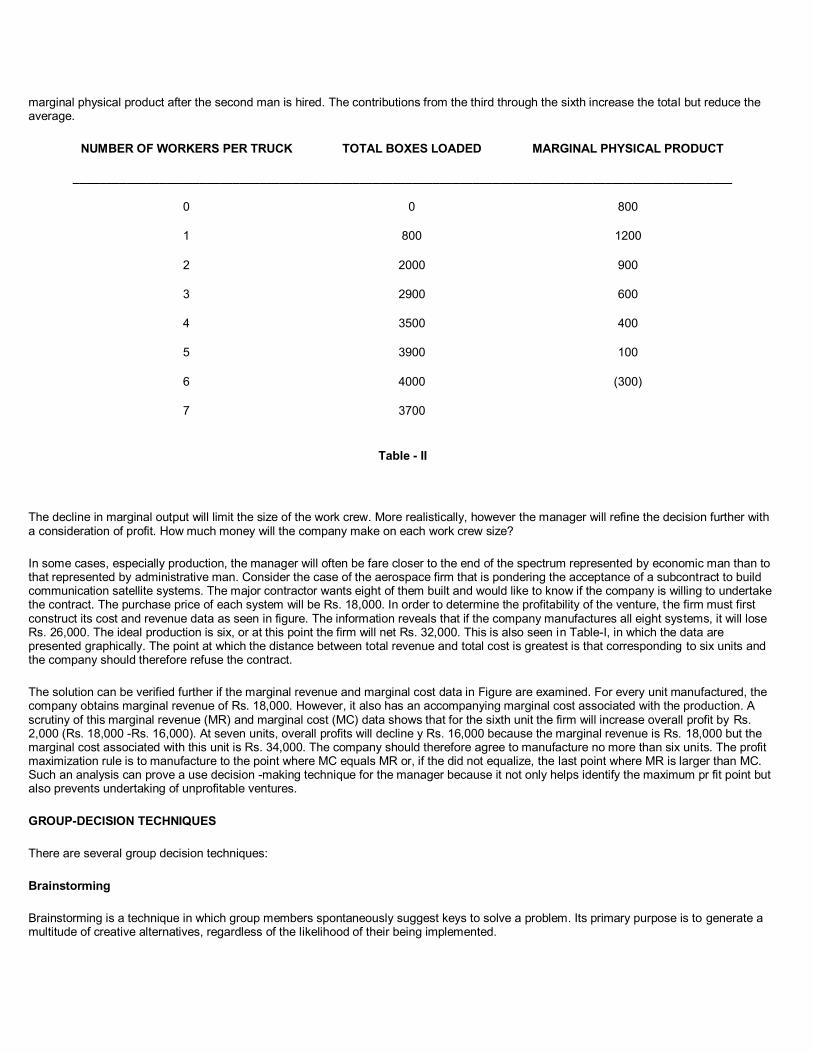

Consider the case of the new shipping manager who has five men loading five trucks. After pondering the matter, the manager hires five new men so there are now two people loading each truck. The result, as seem in figure-II is that the total number of boxes loaded per day rises from 800 to 2000. The two men working as a team are able to do more than they could if working independent .With a third man on each team, the daily total rises to 29000.

Continuing on, as seen in the figure, the total mounts to 4000 and then drops off to 3700 when the number f workers per truck reaches seven. Why? Various causes can be cited. On the physical side, there may be just too many people involved and they are getting in each other's way. On the behavioral side, the seven men may be horse playing more, or they may have agreed informally to hold down output. In either event, it is evident that seven workers per truck are too many.

If the manager's decision must rest solely on out put, six is the ideal team size. However, it should be noted that there is a diminishing

marginal physical product after the second man is hired. The contributions from the third through the sixth increase the total but reduce the average.

NUMBER OF WORKERS PER TRUCK TOTAL BOXES LOADED MARGINAL PHYSICAL PRODUCT

___________________________________________________________________________________________________

0 0 800

1 800 1200

2 2000 900

3 2900 600

4 3500 400

5 3900 100

6 4000 (300)

7 3700

Table - II

The decline in marginal output will limit the size of the work crew. More realistically, however the manager will refine the decision further with a consideration of profit. How much money will the company make on each work crew size?

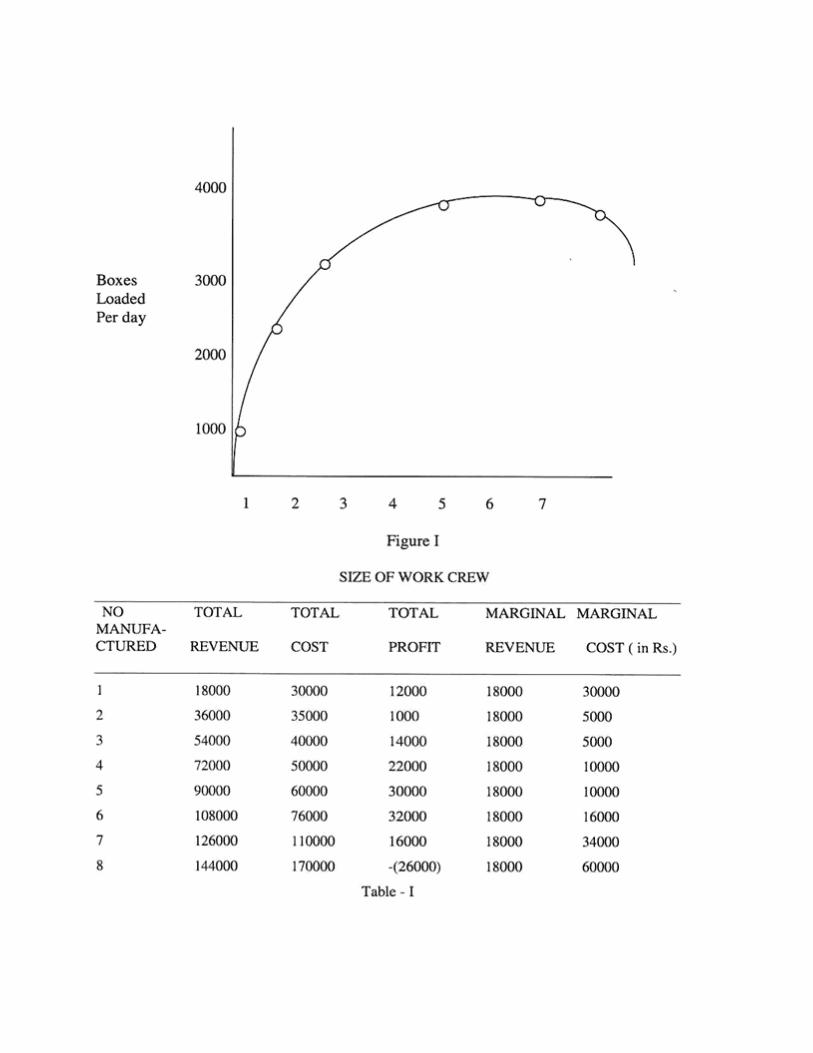

In some cases, especially production, the manager will often be fare closer to the end of the spectrum represented by economic man than to that represented by administrative man. Consider the case of the aerospace firm that is pondering the acceptance of a subcontract to build communication satellite systems. The major contractor wants eight of them built and would like to know if the company is willing to undertake the contract. The purchase price of each system will be Rs. 18,000. In order to determine the profitability of the venture, the firm must first construct its cost and revenue data as seen in figure. The information reveals that if the company manufactures all eight systems, it will lose Rs. 26,000. The ideal production is six, or at this point the firm will net Rs. 32,000. This is also seen in Table-I, in which the data are presented graphically. The point at which the distance between total revenue and total cost is greatest is that corresponding to six units and the company should therefore refuse the contract.

The solution can be verified further if the marginal revenue and marginal cost data in Figure are examined. For every unit manufactured, the company obtains marginal revenue of Rs. 18,000. However, it also has an accompanying marginal cost associated with the production. A scrutiny of this marginal revenue (MR) and marginal cost (MC) data shows that for the sixth unit the firm will increase overall profit by Rs. 2,000 (Rs. 18,000 -Rs. 16,000). At seven units, overall profits will decline y Rs. 16,000 because the marginal revenue is Rs. 18,000 but the marginal cost associated with this unit is Rs. 34,000. The company should therefore agree to manufacture no more than six units. The profit maximization rule is to manufacture to the point where MC equals MR or, if the did not equalize, the last point where MR is larger than MC. Such an analysis can prove a use decision -making technique for the manager because it not only helps identify the maximum pr fit point but also prevents undertaking of unprofitable ventures.

GROUP-DECISION TECHNIQUES

There are several group decision techniques:

Brainstorming

Brainstorming is a technique in which group members spontaneously suggest keys to solve a problem. Its primary purpose is to generate a multitude of creative alternatives, regardless of the likelihood of their being implemented.

Nominal Group Technique

The Norninal Group Technique involves, the use of highly structured meeting agenda and restricts discussion or interpersonal communication during the decision making process. While the group members are all physically present, they are required to operate independently.

Delphi Group Technique

The Delphi group Technique employs a written survey to gather expert opinions from a number of people without holding a group meeting. Unlike in brainstorming and nominal groups, Delphi group participants never meet fact to face; in fact, they may be located in different cities and never see each other.

DECISION-MAKING TOOLS

The major decision- making tools are as under:

1) Linear Programming: One of the most widely used techniques is that of linear programming. It has been described as a technique for specifying how to use limited resources or capacities of a business to obtain a particular objective, such as least cost, highest margin, or least time, when those resources have alternative uses. It is a technique that systematizes for certain conditions the process of selecting the most des able course of action from a number of available courses of action, thereby giving management information for making a more effective decision about the resources under its control. All linear programming problems must have two basic characteristics. First, two or more activities must be competing for limited resources. Second, all relationships in the problem must be linear. Linear programming can be used in the solution of many kinds of allocation decision problems, but its application is certainly limited. For example, to be employed effectively the decision problem must be formulated in quantitative terms. Nevertheless, the approach has many advantages and its application in the area of business decision making is increasing. 2) Inventory Control:

A problem faced by managers is that of maintaining adequate inventories. On the one hand, no one wants to have too many units available because there are costs associated with carrying these customer's future business.

There are two types of costs that merit the manager's consideration.

a. Clerical and Administrative costs: which are expenses associated with ordering inventory. b. Carrying costs: Carrying costs refer to the amount of money invested in the inventory, as well as other sundry expenses covering

storage space, taxes, and obsolescence.

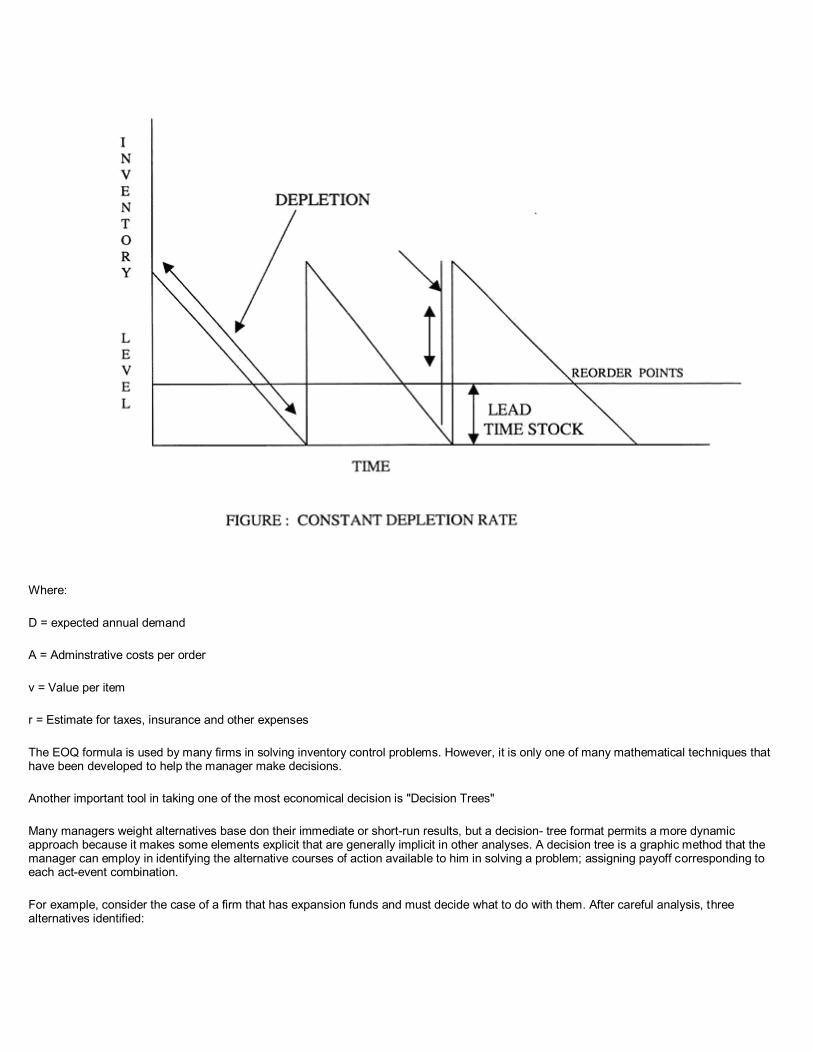

One way for the manager to solve the inventory problem is to make certain assumptions regarding future demand and then attempt a solution. Three of the most common assumptions made in determining optimal inventory size are : demand is known with certainty; the lead time necessary for recording goods is also known with certainty; and the inventory will be depleted at a constant rate. The assumptions can be diagrammed as in figure :-

Now, the manager has to decide if he or she wishes to use what can be labeled a trial-and -error approach, or if he wants to employ an OR (Operations Research) tool known as the economic order quantity (EOQ) formula which can be given by:

OQ =

{2DA}1/2 ______________

vr

Where:

D = expected annual demand

A = Adminstrative costs per order

v = Value per item

r = Estimate for taxes, insurance and other expenses

The EOQ formula is used by many firms in solving inventory control problems. However, it is only one of many mathematical techniques that have been developed to help the manager make decisions.

Another important tool in taking one of the most economical decision is "Decision Trees"

Many managers weight alternatives base don their immediate or short-run results, but a decision- tree format permits a more dynamic approach because it makes some elements explicit that are generally implicit in other analyses. A decision tree is a graphic method that the manager can employ in identifying the alternative courses of action available to him in solving a problem; assigning payoff corresponding to each act-event combination.

For example, consider the case of a firm that has expansion funds and must decide what to do with them. After careful analysis, three alternatives identified:

a. Use the money to buy a new company b. expand the facilities of the current firm; c. put the money in a saving account

And wait for better opportunities. In deciding which alternative is best, the company has gathered all the available information and constructed the decision tree.

In the figure there are four important components. One is the decision point, represented by a square, which indicates where the decision maker must choose a course of action. second is a chance point, represented by a circle, which indicates where a chance event is expected, such as solid economic growth, stagnation, or high inflation. A third is the branch, represented by a line flowing from the chance points, which indicates an event and its likelihood such as 0.5 per solid growth, 0.3 for stagnation or 0.2 for high inflation. Finally, at the far right is a payoff associated with the each branch. It is called a conditional payoff since its occurrence depends on certain conditions. For example, in figure the conditional ROI (Return on Investment) associated with buying a new firm and having solid economic growth is 15 per cent, but this return is conditional on the two preceding factors (buying the firm and having solid growth).

In building a decision tree, the company will start by identifying the three alternatives, the probabilities and events associated with each alternative, and the amount of return that can be expected from each. Having then constructed the tree, the firm will roll back it from right to left, analyzing as it goes.

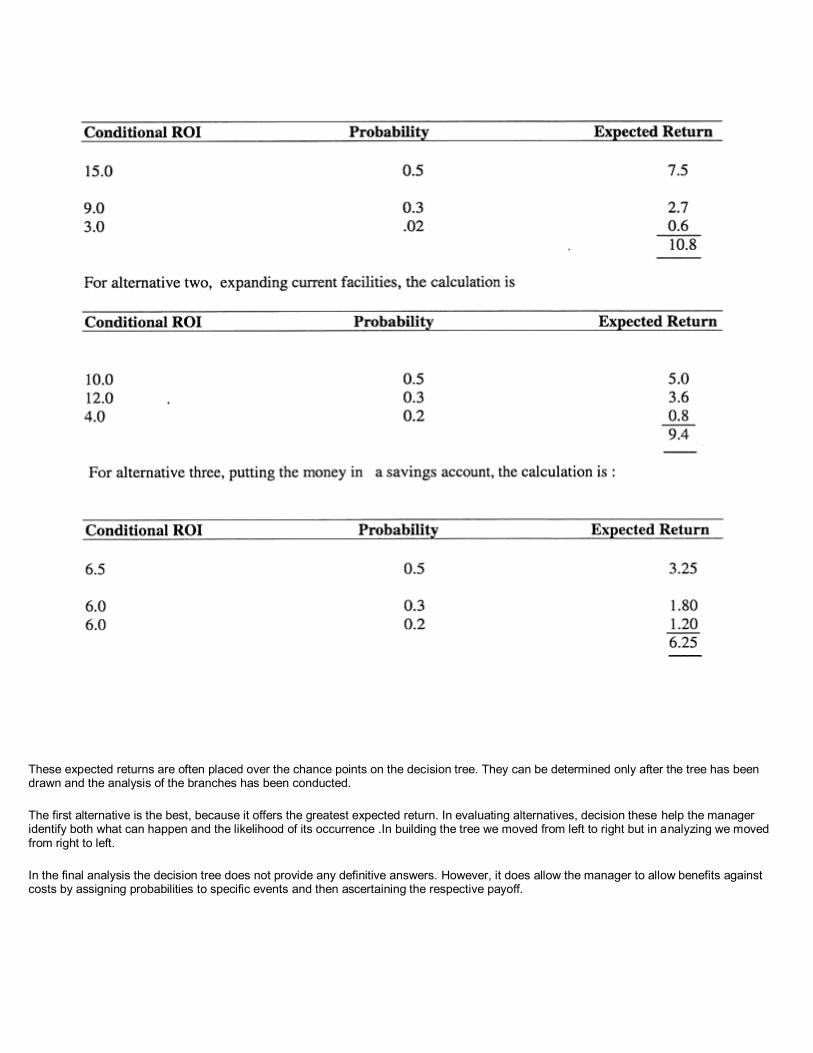

This analysis is conducted, first by taking the conditional ROIs at the far right of the tree and multiplying them by the probability of their occurrence. For example, if the company buys a new firm and there is solid growth in the economy, as seen in figure, it will obtain a 15 per cent ROI. However, the probability of such an occurrence is 0.5 Likewise, the probabilities associated with stagnant growth, where the return will be 9 percent, and high inflation, where the return will be 3 percent, are .3 and .2 respectively. In order to determine the expected return associated with buying a new firm, each of the conditional ROIs is multiplied by its respective probability and the products are then totaled. For alternative one, buying the firm, the calculation is as follows:

These expected returns are often placed over the chance points on the decision tree. They can be determined only after the tree has been drawn and the analysis of the branches has been conducted.

The first alternative is the best, because it offers the greatest expected return. In evaluating alternatives, decision these help the manager identify both what can happen and the likelihood of its occurrence .In building the tree we moved from left to right but in analyzing we moved from right to left.

In the final analysis the decision tree does not provide any definitive answers. However, it does allow the manager to allow benefits against costs by assigning probabilities to specific events and then ascertaining the respective payoff.

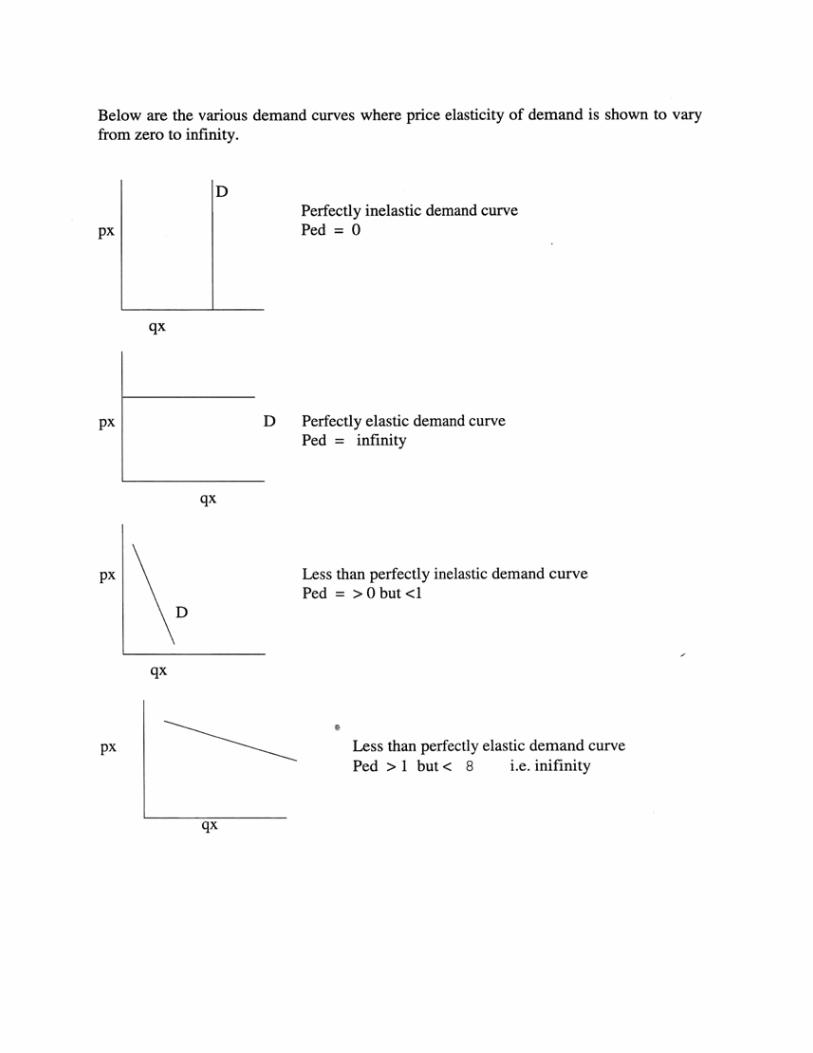

Chapter 2: DEMAND ANALYSIS

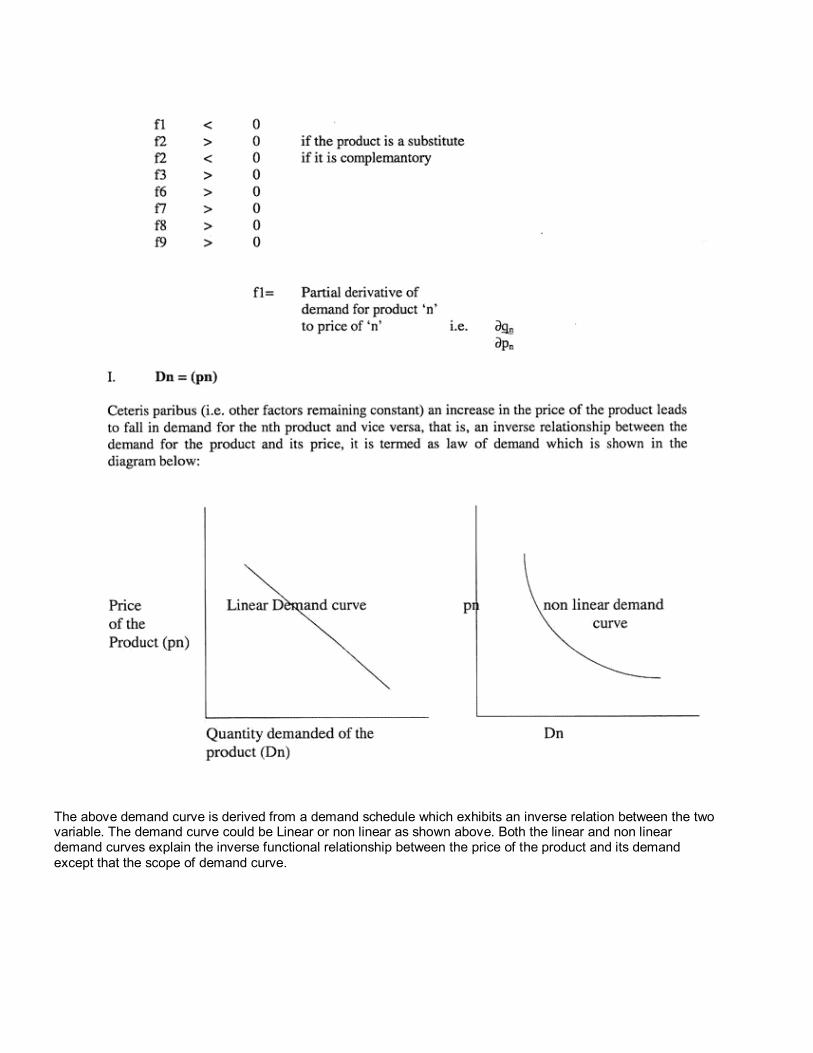

Demand can be said to be the requirement of a product by consumer (s). It is a multivariate relationship, that is , it is determined by many factors simultaneously, Some of the most important determinants of the market demand for a particular product are its own price, consumer's income, price of other commodities, consumer's tastes, income distribution, total population, consumer's wealth, credit availability, government policies, past level of demand and past level of income. The traditional theory of demand depends on four of the above determinants that are the price of the commodity, other prices, income and tastes, Demand for a commodity implies:

1. Desire to acquire it, 2. Willingness to pay for it 3. Ability to pay for it

This can be illustrated as follows. A miser's desire to acquire a product and his ability to pay for a product does not constitute a demand, as he is not willing to pay for the product. Similarly a poor man desire for a product and his willingness to pay for it is not complemented by his ability to pay for it. Hence the desire is not translated into a demand. Similarly a rich man willingness and ability to pay for a product cannot constitute a demand if he does not wish to by the product.

Thus the demand for any commodity is the desire for that commodity backed by the willingness as well as the ability to pay for it and is always defined with reference to a particular time and given values of variables on which it depends.

Types of demands

Demands for a commodity can be grouped into various categories for better understanding of its characteristics. The main categories may be:

A. Demand for consumer goods and producers goods B. Demand for perishable and durable goods C. Derived and autonomous demand D. Firm and Industry demand E. Demand by total market and industry segments

Consumer's goods and producer's goods demands

Consumer goods are those, which are, meant for the final consumption by the consumers or the end users. Producer's goods on the other hand are used for the production of consumer goods or they are intermediate goods, which are further processed upon to convert them into a form to be used by the end user. Another distinction is that the demand for producer's goods are derived demand and it indirectly depends on the demand for the consumer goods which the producer goods is used to produce. It may also be possible that this demand may be accelerated or accentuated that is I won't vary in the same proportion as the change in the demand for the final consumer goods. A small change in the demand for consumer goods may either completely wipe out the demand for the producer goods or may accelerate it.

Perishable and durable goods

Perishable (non-durable) goods are defined as those which can be used only once whereas durable goods are those which can be used over and over again. In specific cases perishable goods may also have a fixed life

span. This distinction is useful because of demand analysis. Sale of non durable goods are generally for meeting current demand whereas sale of durable goods add to the stock of existing goods whose services are used over a long period of time. Their demand is thus of two types. Replacement of old products and expansion of existing stock.

Derived and autonomous demand

When the demand for a product is tied to the demand for some parent product, then the demand is termed as derived demand. On the other hand if the demand for a commodity is completely independent of the demand of other commodities, which may be substitute or complementary or on the raw material side or on the product side, the demand for the product is termed as independent. It is very difficult to find a product whose demand is totally autonomous but some commodities like tea and vegetables do come absolute terms.

Company and Industry demand

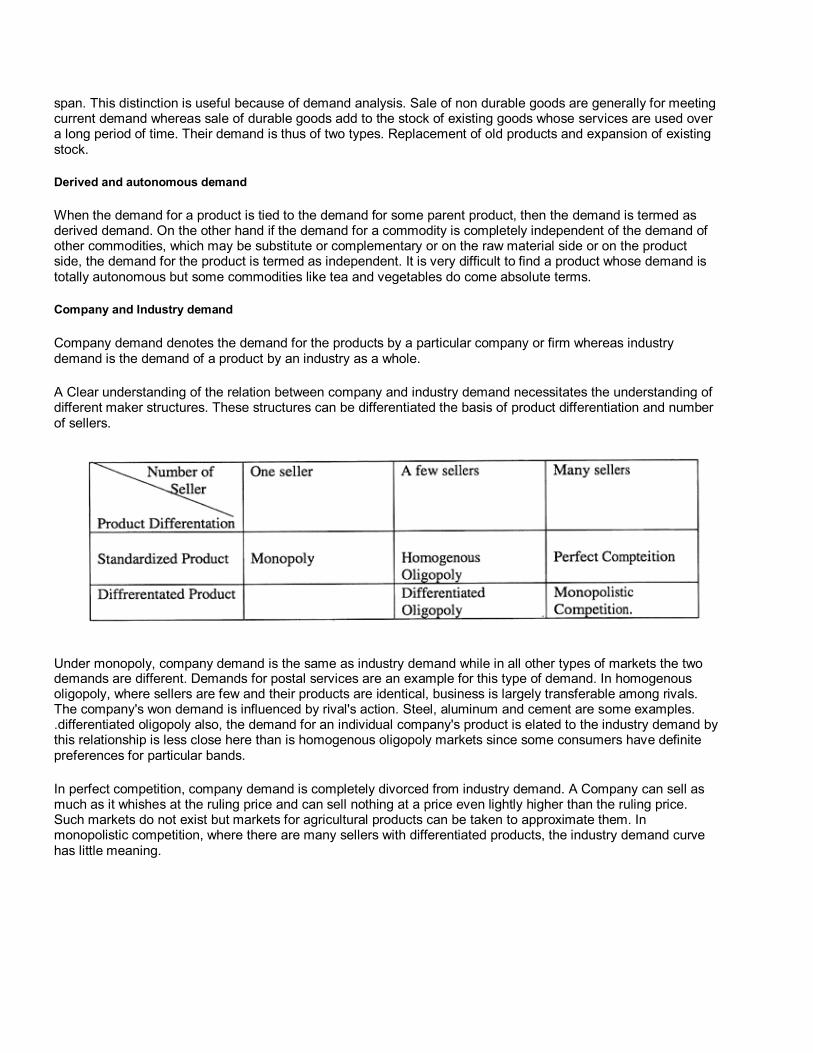

Company demand denotes the demand for the products by a particular company or firm whereas industry demand is the demand of a product by an industry as a whole.

A Clear understanding of the relation between company and industry demand necessitates the understanding of different maker structures. These structures can be differentiated the basis of product differentiation and number of sellers.

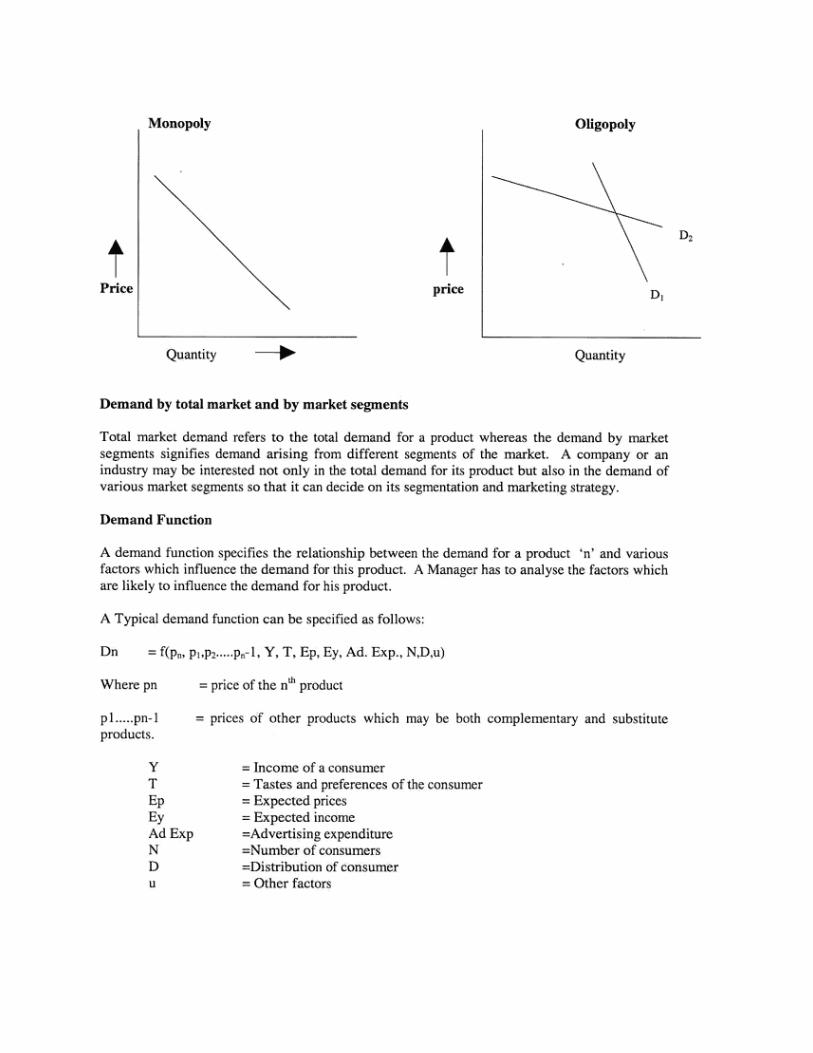

Under monopoly, company demand is the same as industry demand while in all other types of markets the two demands are different. Demands for postal services are an example for this type of demand. In homogenous oligopoly, where sellers are few and their products are identical, business is largely transferable among rivals. The company's won demand is influenced by rival's action. Steel, aluminum and cement are some examples. .differentiated oligopoly also, the demand for an individual company's product is elated to the industry demand by this relationship is less close here than is homogenous oligopoly markets since some consumers have definite preferences for particular bands.

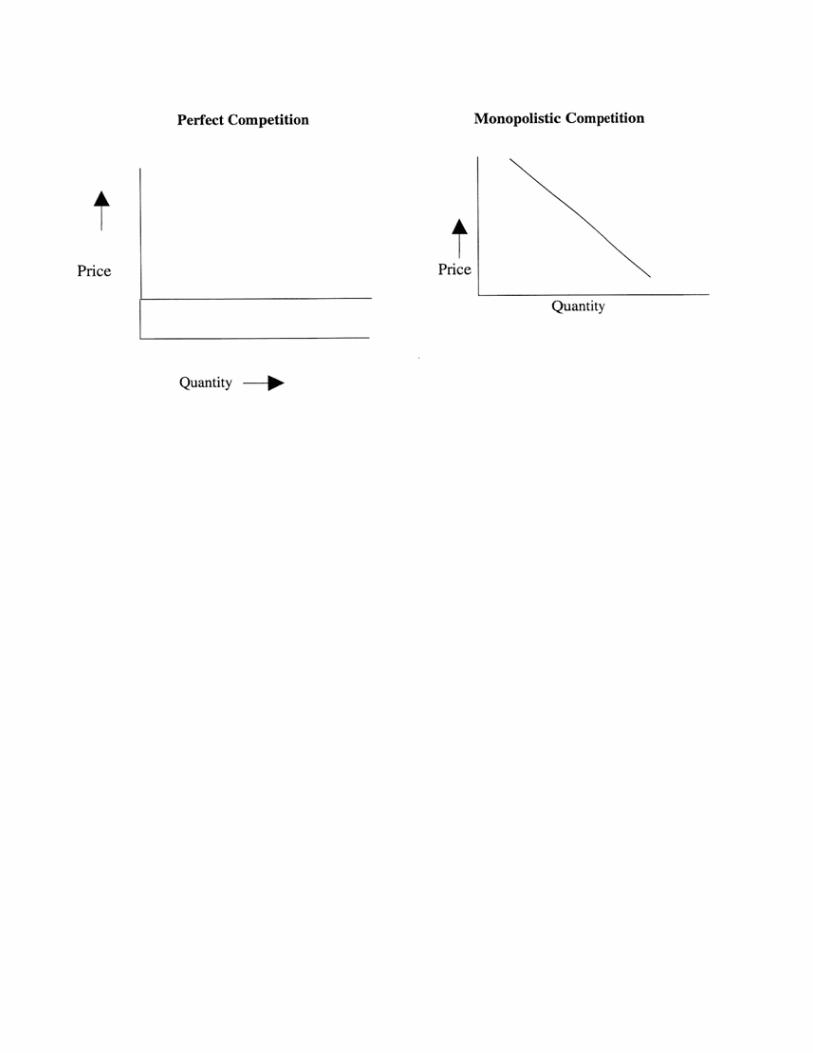

In perfect competition, company demand is completely divorced from industry demand. A Company can sell as much as it whishes at the ruling price and can sell nothing at a price even lightly higher than the ruling price. Such markets do not exist but markets for agricultural products can be taken to approximate them. In monopolistic competition, where there are many sellers with differentiated products, the industry demand curve has little meaning.

The above demand curve is derived from a demand schedule which exhibits an inverse relation between the two variable. The demand curve could be Linear or non linear as shown above. Both the linear and non linear demand curves explain the inverse functional relationship between the price of the product and its demand except that the scope of demand curve.

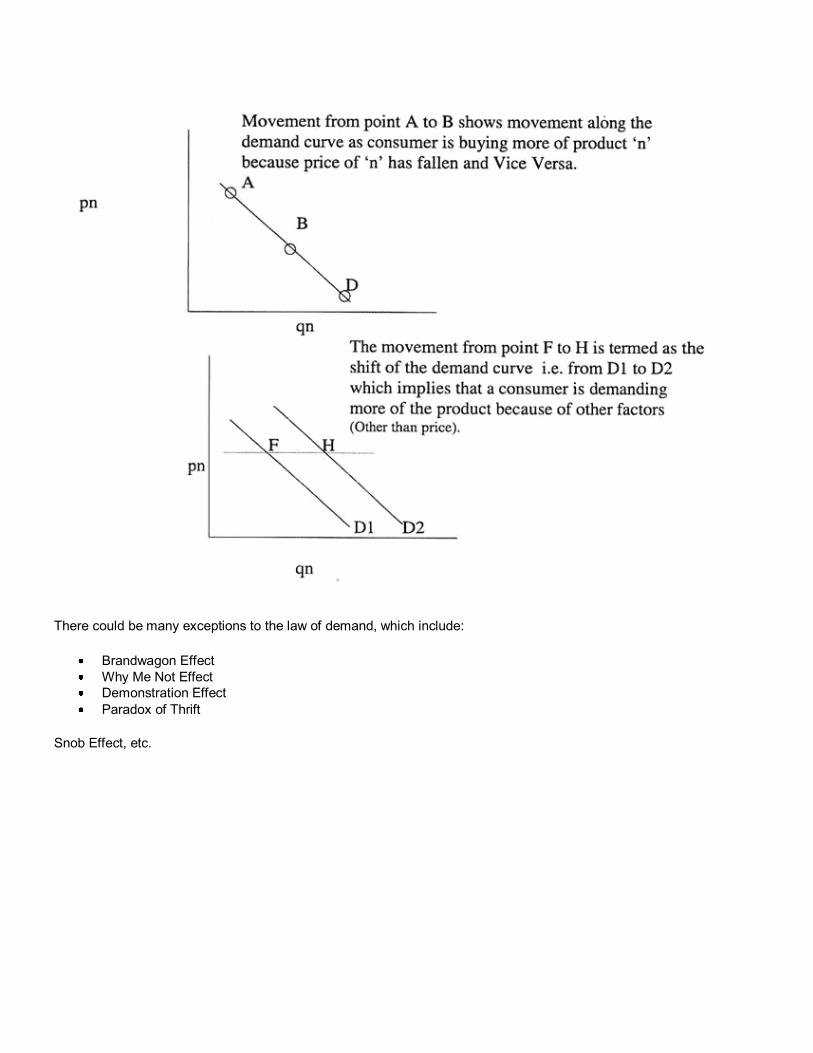

There could be many exceptions to the law of demand, which include:

Brandwagon Effect

Why Me Not Effect

Demonstration Effect

Paradox of Thrift

Snob Effect, etc.

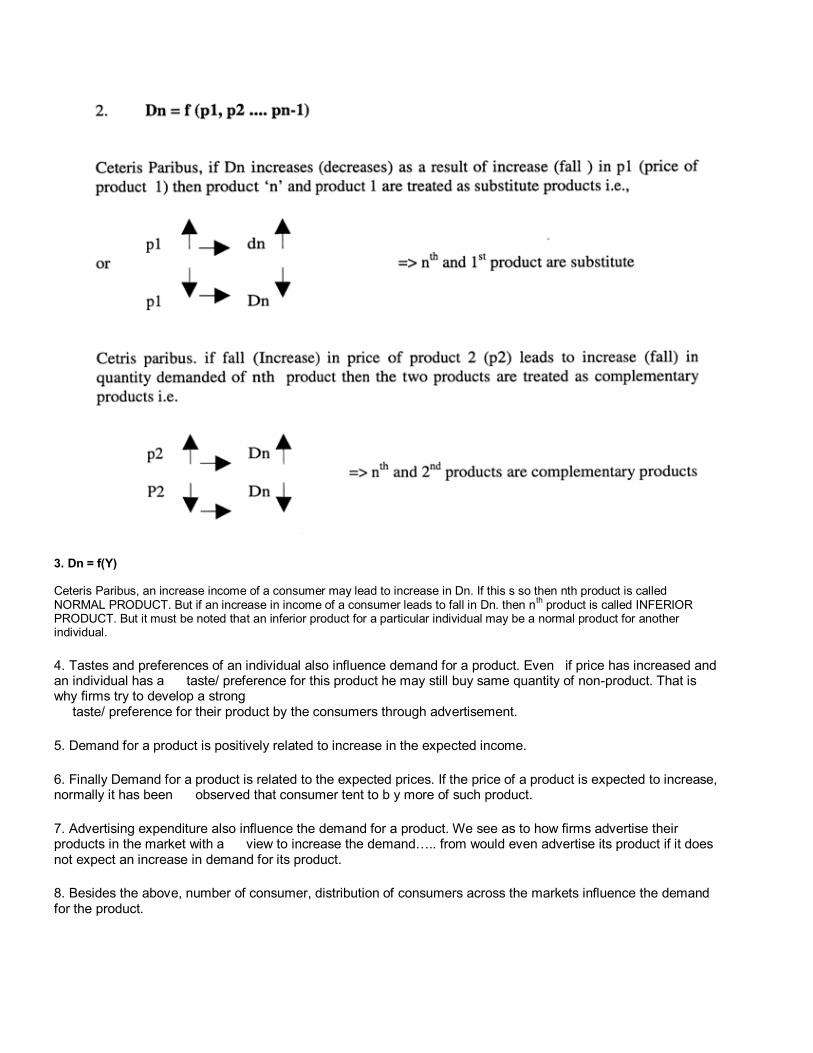

3. Dn = f(Y) Ceteris Paribus, an increase income of a consumer may lead to increase in Dn. If this s so then nth product is called NORMAL PRODUCT. But if an increase in income of a consumer leads to fall in Dn. then n

th product is called INFERIOR

PRODUCT. But it must be noted that an inferior product for a particular individual may be a normal product for another individual.

4. Tastes and preferences of an individual also influence demand for a product. Even if price has increased and an individual has a taste/ preference for this product he may still buy same quantity of non-product. That is why firms try to develop a strong taste/ preference for their product by the consumers through advertisement.

5. Demand for a product is positively related to increase in the expected income.

6. Finally Demand for a product is related to the expected prices. If the price of a product is expected to increase, normally it has been observed that consumer tent to b y more of such product.

7. Advertising expenditure also influence the demand for a product. We see as to how firms advertise their products in the market with a view to increase the demand….. from would even advertise its product if it does not expect an increase in demand for its product.

8. Besides the above, number of consumer, distribution of consumers across the markets influence the demand for the product.

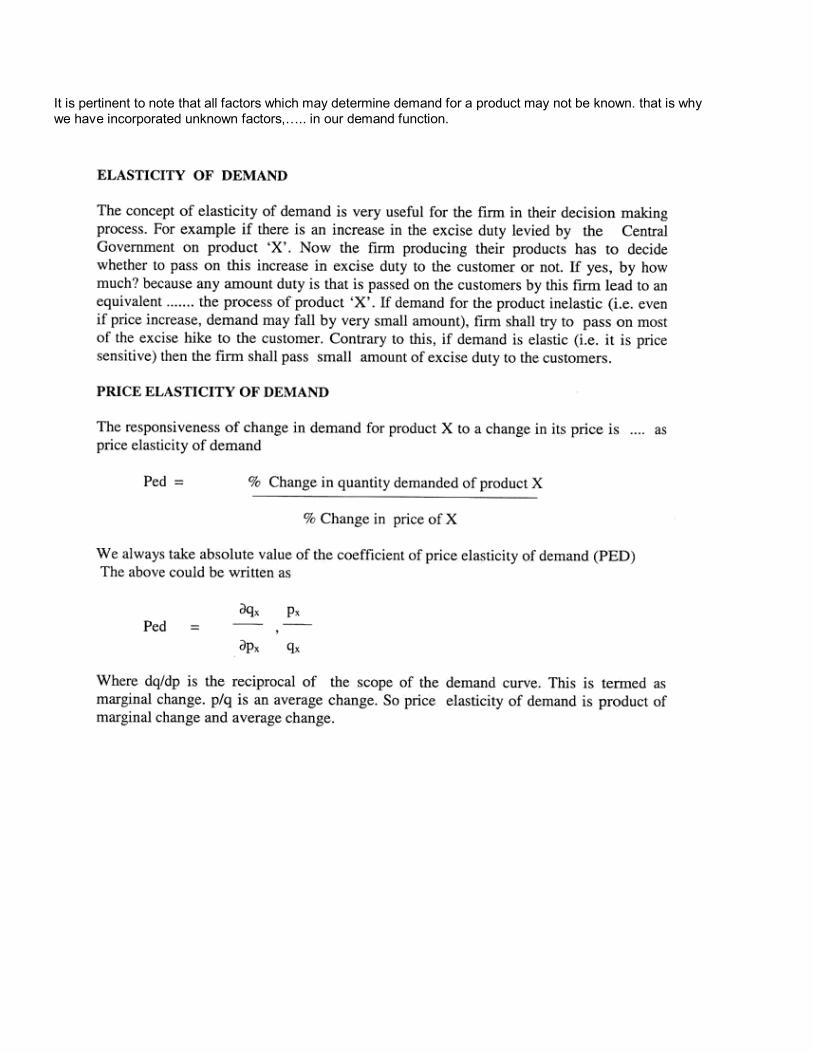

It is pertinent to note that all factors which may determine demand for a product may not be known. that is why we have incorporated unknown factors,….. in our demand function.

Chapter 3: DEMAND FORECASTING

Estimation of demand for a product in a forecast year/ period is termed as Demand forecast.

Demand forecast is a must for a firm operating its business as today's market is competitive, dynamic and volatile.

Purpose and need of forecasting

Forecasting is done both for long term as well as short term.

The purpose of the two however differs.

In a short run forecast seasonal patters are of prime importance. Such a forecast helps in preparing suitable sales policy and proper scheduling of output in order to avoid over-stocking or costly delay in meeting the orders. It helps in arriving at suitable price for the product and necessary modifications in advertising and sales techniques.

Long run forecasts are helpful in proper capital planning. It helps in saving the wastages in material, m -hours, machine time and capacity. Long run forecasting is used for new unit planning, expansion of the existing units, planning long run financial requirements and manpower requirements. Different set of variables is used in than in short term forecasts.

Specific purposes of demand forecasting

1. Better planning and allocation of resources 2. Appropriate production scheduling 3. Inventory control 4. Determining appropriate pricing policies 5. Setting s les targets and establishing controls and incentives. 6. Planning a new unit or expanding existing one 7. Planning long term financial requirements 8. Planning Human Resource Development strategies.

Steps Involved in Forecasting

1. Identification of objective 2. Determining the nature of goods under consideration. 3. Selecting a proper method of forecasting. 4. Interpretation of results.

Scope of Forecasting

1. Period of forecasting

a. Short run forecasting: In short run forecasting, we look for factors which bring fluctuation in demand pattern in the market for example weather conditions like monsoon affecting the demand.

b. Medium run forecasting: In medium run forecasting is done basically for timing of an activity like advertising expenditure.

c. Long run forecasting: It is done to ascertain the validity of trend. It is done for decision like diversification.

2. Levels of Forecasting

a. Macroeconomic forecasting is concerned with business conditions of the whole economy. It is measured with the help of indices like wholesale price index, consumer price index.

b. Industry demand forecasting gives indication to firm regarding direction in which the whole industry will be moving. It is used to decide the way the firm should plan for future in relation to the industry.

c. Firm demand forecasting is done for planning companies overall operations like sales forecasting etc.

d. Product line forecasting helps the firm to decide which of the product or products should have priority in the allocation of firm's limited resources.

3. General purpose or specific purpose forecast helps the firm in taking general factors into consideration while forecasting for demand.

4. Forecast of established product or a new product

5. Types of commodity for which forecast is to be done. Goods can be broadly classified into capital goods, consumer durable and non-durable consumer goods. For each of these categories of goods there is a distinctive pattern of demand.

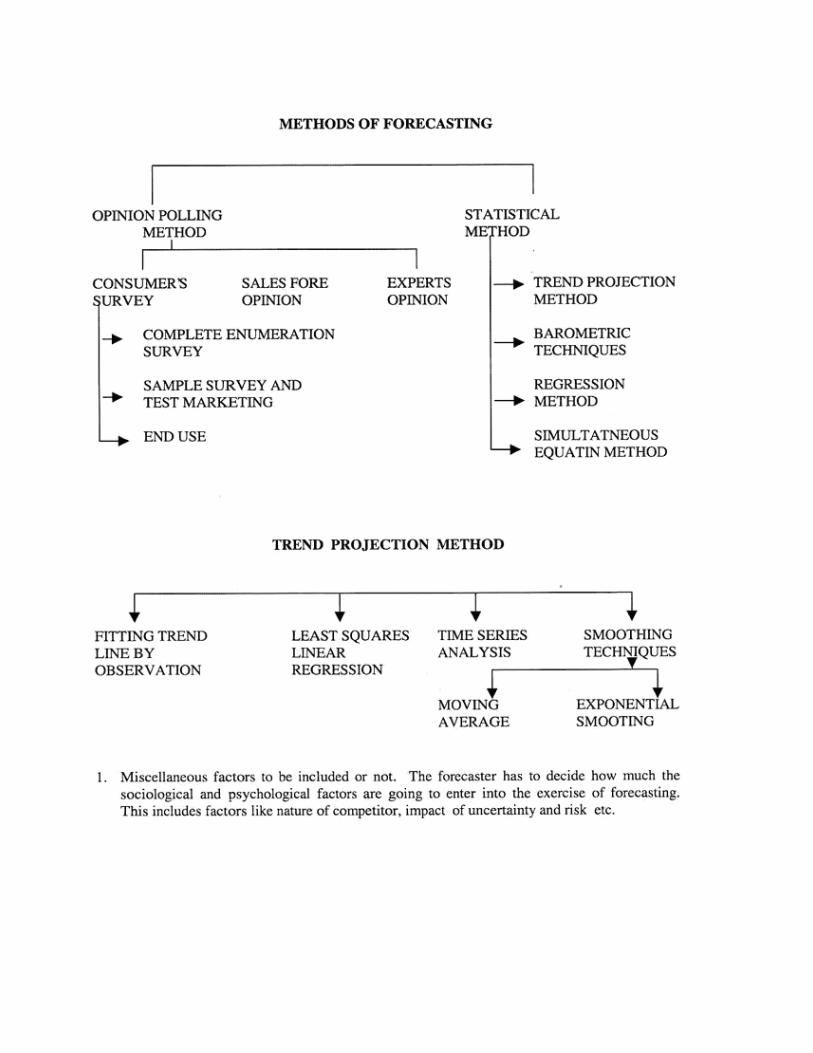

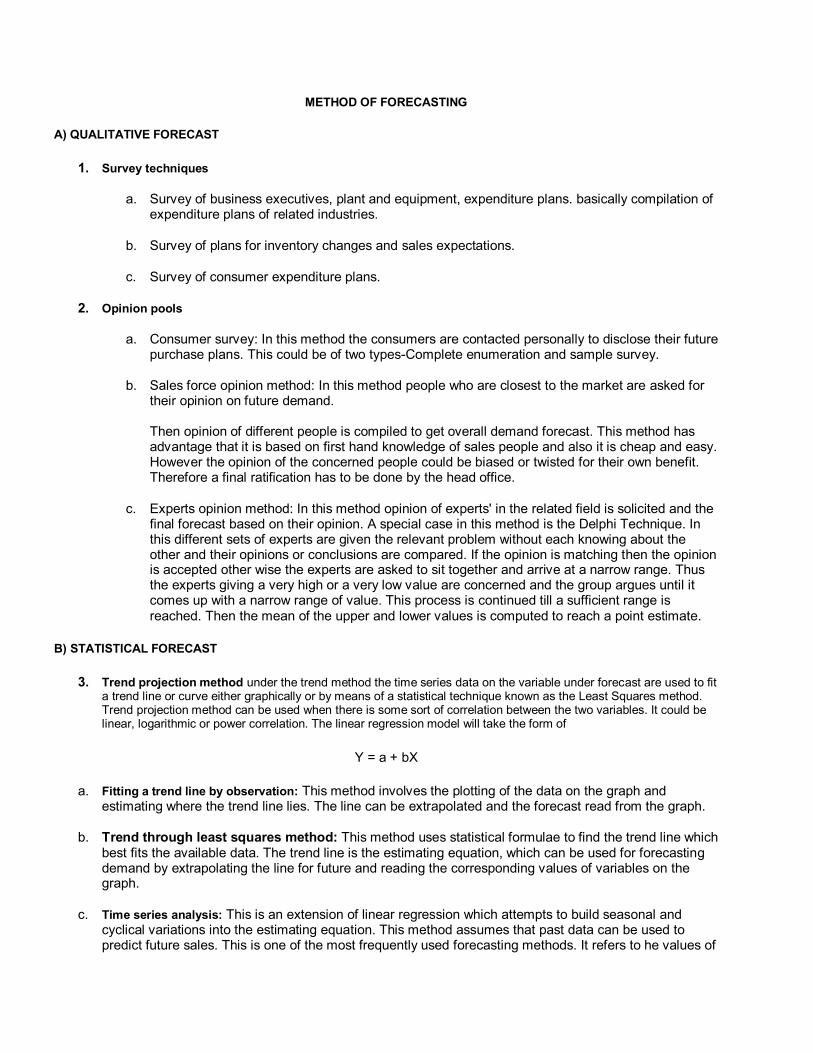

METHOD OF FORECASTING

A) QUALITATIVE FORECAST

1. Survey techniques

a. Survey of business executives, plant and equipment, expenditure plans. basically compilation of expenditure plans of related industries.

b. Survey of plans for inventory changes and sales expectations.

c. Survey of consumer expenditure plans.

2. Opinion pools

a. Consumer survey: In this method the consumers are contacted personally to disclose their future purchase plans. This could be of two types-Complete enumeration and sample survey.

b. Sales force opinion method: In this method people who are closest to the market are asked for their opinion on future demand. Then opinion of different people is compiled to get overall demand forecast. This method has advantage that it is based on first hand knowledge of sales people and also it is cheap and easy. However the opinion of the concerned people could be biased or twisted for their own benefit. Therefore a final ratification has to be done by the head office.

c. Experts opinion method: In this method opinion of experts' in the related field is solicited and the final forecast based on their opinion. A special case in this method is the Delphi Technique. In this different sets of experts are given the relevant problem without each knowing about the other and their opinions or conclusions are compared. If the opinion is matching then the opinion is accepted other wise the experts are asked to sit together and arrive at a narrow range. Thus the experts giving a very high or a very low value are concerned and the group argues until it comes up with a narrow range of value. This process is continued till a sufficient range is reached. Then the mean of the upper and lower values is computed to reach a point estimate.

B) STATISTICAL FORECAST

3. Trend projection method under the trend method the time series data on the variable under forecast are used to fit a trend line or curve either graphically or by means of a statistical technique known as the Least Squares method. Trend projection method can be used when there is some sort of correlation between the two variables. It could be linear, logarithmic or power correlation. The linear regression model will take the form of

Y = a + bX

a. Fitting a trend line by observation: This method involves the plotting of the data on the graph and estimating where the trend line lies. The line can be extrapolated and the forecast read from the graph.

b. Trend through least squares method: This method uses statistical formulae to find the trend line which best fits the available data. The trend line is the estimating equation, which can be used for forecasting demand by extrapolating the line for future and reading the corresponding values of variables on the graph.

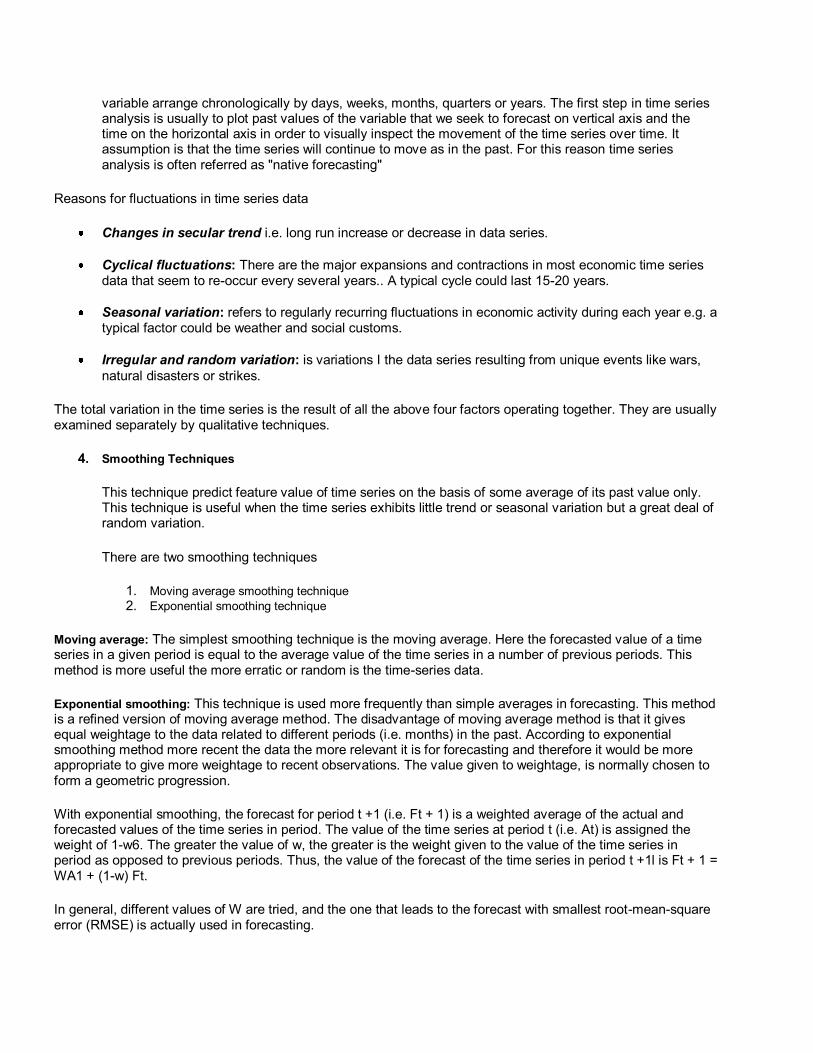

c. Time series analysis: This is an extension of linear regression which attempts to build seasonal and cyclical variations into the estimating equation. This method assumes that past data can be used to predict future sales. This is one of the most frequently used forecasting methods. It refers to he values of

variable arrange chronologically by days, weeks, months, quarters or years. The first step in time series analysis is usually to plot past values of the variable that we seek to forecast on vertical axis and the time on the horizontal axis in order to visually inspect the movement of the time series over time. It assumption is that the time series will continue to move as in the past. For this reason time series analysis is often referred as "native forecasting"

Reasons for fluctuations in time series data

Changes in secular trend i.e. long run increase or decrease in data series.

Cyclical fluctuations: There are the major expansions and contractions in most economic time series data that seem to re-occur every several years.. A typical cycle could last 15-20 years.

Seasonal variation: refers to regularly recurring fluctuations in economic activity during each year e.g. a typical factor could be weather and social customs.

Irregular and random variation: is variations I the data series resulting from unique events like wars,

natural disasters or strikes.

The total variation in the time series is the result of all the above four factors operating together. They are usually examined separately by qualitative techniques.

4. Smoothing Techniques

This technique predict feature value of time series on the basis of some average of its past value only. This technique is useful when the time series exhibits little trend or seasonal variation but a great deal of random variation.

There are two smoothing techniques

1. Moving average smoothing technique 2. Exponential smoothing technique

Moving average: The simplest smoothing technique is the moving average. Here the forecasted value of a time series in a given period is equal to the average value of the time series in a number of previous periods. This method is more useful the more erratic or random is the time-series data.

Exponential smoothing: This technique is used more frequently than simple averages in forecasting. This method is a refined version of moving average method. The disadvantage of moving average method is that it gives equal weightage to the data related to different periods (i.e. months) in the past. According to exponential smoothing method more recent the data the more relevant it is for forecasting and therefore it would be more appropriate to give more weightage to recent observations. The value given to weightage, is normally chosen to form a geometric progression.

With exponential smoothing, the forecast for period t +1 (i.e. Ft + 1) is a weighted average of the actual and forecasted values of the time series in period. The value of the time series at period t (i.e. At) is assigned the weight of 1-w6. The greater the value of w, the greater is the weight given to the value of the time series in period as opposed to previous periods. Thus, the value of the forecast of the time series in period t +1l is Ft + 1 = WA1 + (1-w) Ft.

In general, different values of W are tried, and the one that leads to the forecast with smallest root-mean-square error (RMSE) is actually used in forecasting.

5. Barometric methods: Barometric methods are used to forecast or anticipate short term changes in economic activity by using leading economic indicators. These indicators are time series that tend to precede changes in the level of economic activity. There are only three types of indicators:

I. Leading economic indicator: These indicators tend normally to anticipate turning points in a business cycle. There are certain problems associated with this method. The major problem is not choosing the technique but choosing the relevant indicator for the product in question. Secondly even if the relevant indicator is found out the changes in factors may render the indicator redundant over time. Thirdly the time lag between the indicator and forecast could be so small that it could become useless.

II. Coincident indicators: These are indicators which move in step or coincide with movements in general economic activity or business cycle.

III. Lagging indicator: These are indicators which lag the movements in economic activity or business cycle.

6. Regression method: It is one of the statistical tools to fore cast demand. In this estimating equations are established and tests can be carried out to observe any statistically significant. It involves following steps -:

a. Identification of variables which influence the demand for the good whose function is under estimation. b. Collection of historical data on all relevant variables.

c. Choosing an appropriate form of the function.

d. Estimation of the function

Regression method is popular because it is prescriptive as well as descriptive. Also it is not as subjective or objective as other methods. However if the variables chosen are wrong then the forecast will also be wrong. A typical demand equation could be :

Log d = -12.4 + 1.78 log y -1.22 log 0 + 2.20 log v + 0.8 log g + 1.62 log e

Y = National income

O = groundnut oil price

V = Vanaspati price

G = ghee price

E = egg, fish and meat price

The above equation is a demand forecast equation for groundnut oil

7. Simultaneous equation method (Econometric Models): Econometric forecasting incorporates or utilizes the best features of other forecasting techniques such as trend and seasonal variation, smoothing techniques and leading indicators. Econometric forecasting models range from single equation models of the demand that the firm faces for tits product to large multiple equation models describing hundreds of sectors and industries of the economy.

a. Single equation models: The simplest form of econometric forecasting is with the single equation model. The first step here is to identify the determinants of the variable to be forecasted.

Q = a0 + a1P + a2Y +a3N + a4P5 + a5Pc + a6a + e Q = demand

P = Price

Y = disposable income

N = size of population

Ps = price of a substitute

Pc = price of complement A = level of advertising by the firm

b. Multiple equation model: Sometimes economic relationships may be so complex that a multiple equation model may be required. This is particularly used in forecasting micro variables or the demand and sales of major sectors or industries. Multiple equation model for GNP-:

Ct = a1+b1GNPt+u1t It =a2+b2IIt-1+U2t GNPt= Ct+ It+Gt

C = consumption expenditures

GNP = Gross national product in year t

I = investment

II = Profit

G = Government expenditures

U = stochastic disturbance (random error term)

T = current year

t-1 = previous year

Variables to the left of the equal sign are called endogenous variable. These are the variables that the model seeks to explain or predict from the solution of the model. Exogenous variables are those determinants outside the model or right of the equal sign of the equation.

8. Input Output Forecasting

Input output analysis was introduced by Prof. Leontief. With this technique the firm can also forecast using Input output tables. It shows the use of the output of each industry as input by other industries and for final consumption. Input and output analysis allow us to trace through all these inter industry input and outputs flow though out the economy and to determine the total increase of all the inputs required to meet the increased demand. In this technique we have two input output matrixes

1. Direct requirement matrix 2. Total requirement matrix

Uses and Shortcomings of input-output forecasting

Input-output analysis and forecasting has many uses and applications. It is used by the firm to forecast the raw material, labour, and capital requirement needed to meet the forecasted change in the demand for their product.

Shortcomings:

1. The direct and total requirement coefficient are assumed to be fixed and thus do not allow input substitution.

2. Input output tales are usually available with a time lag of many years and while the input output coefficient do not change very rapidly over the course of many years they can become very biased.

RISKS IN DEMAND FORECASTING

Demand forecasting faces two major risks.

1. Overestimating demand 2. Underestimating demand

One risk arises from entirely unforeseen events such as war, political upheavals and natural disasters.

The second risk arises from inadequate analysis of the market.

All these costly forecasting errors could possibly have been avoided.

a. Carefully defining the market for the product to include all potential users of the market and considering the possibility of product substitution

b. Dividing total industry demand into its components and analyzing each component separately. c. Forecasting the main driver or user of the product in each segment of the market and projecting how

they are likely to change in the future.

Conducting sensitivity analysis of how the forecast would be affected by change in any of the assumption on

which the forecast is based.

The physical conditions of production, the price of resources and the economically efficient conduct of an entrepreneur jointly determine the cost of production of a business.

Apart from being determined by other exogenous variables, the output level of a firm is also determined by the cost of producing the desired level of output. A firm aims at operating in a situation where revenues are maximum and costs are minimum. It would also like to produce a that optimal out put where it gets a maximum profit as determined by the difference between cost and revenue. Hence it is important to analyze the cost output relationship.

COST CONCEPTS

The most widely accepted concept is the money cost of production. It means the aggregate money expenditure by a firm on various items required in the production of a commodity. For example expenditure on raw materials purchased salary & wages paid to the employees etc.

There are several useful cost concepts and clear understanding of them is necessary for cost analysis:

ECONOMICS COST: It refers to the cost incurred by the firm in the production of a good and the payments made to the factors of production in the production of that good. For example a firm produces 10 tones of wheat by employing the following resources:-

Factors hired from outside (Cost in Rs)

Raw Materials 800

Labour 2000

Tractor 2000

Fertilizer 1100

Tubewell for irrigation 1250

_________________

7150

_________________

Self owned factors employed Opportunity cost

Family labour 3500

Land 4000

Chapter 4: COST AND OUTPUT ANALYSIS

_________________

7500

_________________

Thus the total economic cost comes out to be Rs.14650.

Direct cost / Explicit cost / Expenditure cost

Explicit costs include those payments which are made by the employer to those factors of production which do not belong to the employer himself. For e.g.: payments made for raw materials, power, fuel, rent paid on land etc.

These are the costs that the accountants list as the firm's expenditure.

They may also be called accounting costs.

Imputed costs / Implicit costs / Non-expenditure Costs

The implicit costs or imputed costs (or non-expenditure costs) arise in the cases of those factors which are owned and supplied by the employer himself. For e.g.: An employer may contribute his own land, his own capital and may even work as the manager of the firm

Normal profits

It is not a profit but an item of economic cost. It stands for the opportunity cost of an entrepreneur's time. The cost of owner's time is the implicit cost of entrepreneurship or normal profit.

Historical and replacements cost

The historical cost of an asset refers to the actual cost incurred at the time the asset was acquired. On the other hand the replacement cost is the cost which must be incurred if the asset is to be purchased today. For e.g. Supposing the original cost of shirt is Rs.250 where as the replacement cost would be Rs.290.

Incremental and sunk costs

Incremental costs are those which vary with the decision. On the other hand sunk costs refers to that fixed costs which has already been incurred in the productive process and which cannot be retrieved even though it was found to be a blunder on second thought. Eg: the costs of the time of faculty clerk-cum-peon and the amount spent on electricity bills etc. Will be incremental costs where as the costs of using a classroom and blackboard are sunk costs. The costs relevant for decision making are incremental costs and not sunk costs.

Fixed and variable costs

Certain costs vary if the output varies and they remain fixed if the output remains the same. Thus the costs associated with fixed factors of production are fixed cost where as the costs associated with variable factors of production are called variable costs. For e.g.: if the capital is the fixed factor, capital rent is a fixed cost and if labour is a variable factor, wage bill is the variable cost.

Opportunity cost

It refers to the cost of producing a particular product which is the value of the other products that the resources used in its production could have produced instead. For e.g.: The cost of producing locomotives is the value of the goods and services that could have been obtained from the manpower, equipment, and the materials used currently in locomotive production.

Separable and common costs

Costs are classified on their basis of their traceability. The costs, which can be attributed to a product, a department or a process, are the separable costs and the rests are non- -separable or common costs. Eg: IN a multi-product firm raw materials cost is a separable product wise but the management cost is not separable that way.

Social and private costs

Private costs refer to the costs incurred by an individual firm while social costs stand for the costs incurred by the society as a whole. The former is the sum total of explicit and implicit costs that a firm incurs in the production. But since managerial economics deals primarily with decision making by a firm only economic costs are relevant.

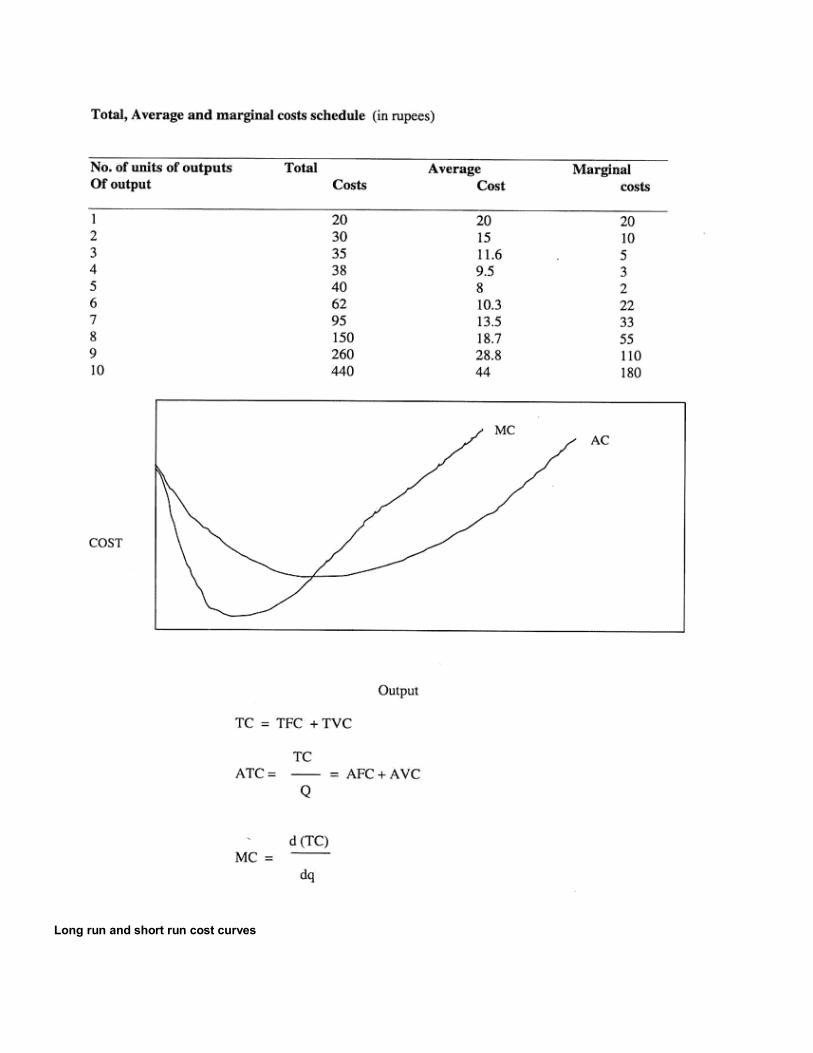

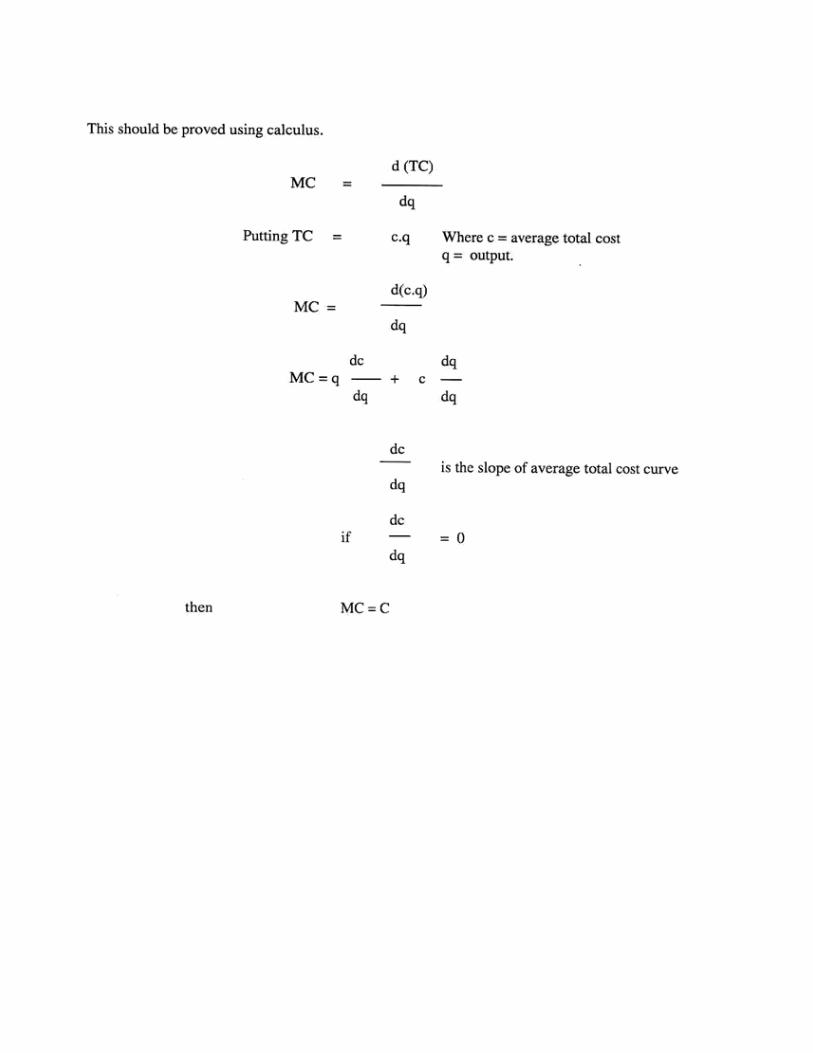

Total. Average and marginal costs

The three concepts of total, average and marginal costs on the supply side are the counterparts of the total, average and marginal revenue on the demand side. Total cost is the total money cost of production of a commodity. The average cost is obtained by dividing total cost of production by the number of units of the commodity reduced so that

Average Cost =

Total Cost _________

Output

Marginal cost is the cost of producing the final or the marginal unit of the commodity. Alternately it may be expressed as the total cost of n units of the output minus the total cost of n-1units. Both average as well as the marginal cost curves are normally U- shaped curves. As long as average cost curve (AC) is falling the marginal cost (MC) curve is below it. Likewise, when the average cost curve starts rising, the marginal cost curve is above it.

Long run and short run cost curves

Long run costs and short run costs are related to long and short run production functions. In the long run all costs are variable costs while in the short run, some costs are fixed and some are variable. Combining this classification with the earlier one between the total, marginal and average costs, there are three long run cost concepts and seven short run ones. The former consists of the long run total costs (LTC)., long run average costs (LAC) and long run marginal cost (LMC), and the latter comprises of short run average fixed cost (AFC), short run total variable cost (TVC) and short run average cost (AVC). Hence,

STC = TFC + TVD

SAC = AFC + AVC

Both long run and short run costs are useful for decision making. In the long run, a fIrm is concerned with optimum output within a given plant size.

COST FUNCTION:

Cost functions are derived functions. They are derived from the production function which describes the available efficient methods of production at any point of time.

Both in the short run and in the long run, total cost is a multivariate function. That is total cost is determined by many factors. Symbolically we may write the long run cost function as

C = f (X, T, Pf)

And the short run cost function as

C = f(X, T, Pf, K)

Where C = Total Cost

X = Output

T = Technology

Pf = Price of Factors

K = Fixed Factors

Graphically these are shown on two dimensional diagrams. Such curves imply that cost is a function of output, C = f (X) ceteris paribus of the three, sets of cost determinants, output assumes a special role. This is for two reasons. One, output is the only variable which is under the direct control of the firm .Two, the relationship between total cost and output is unique.

SHORT RUN COST CURVES

AVERAGE FIXED COST CURVE

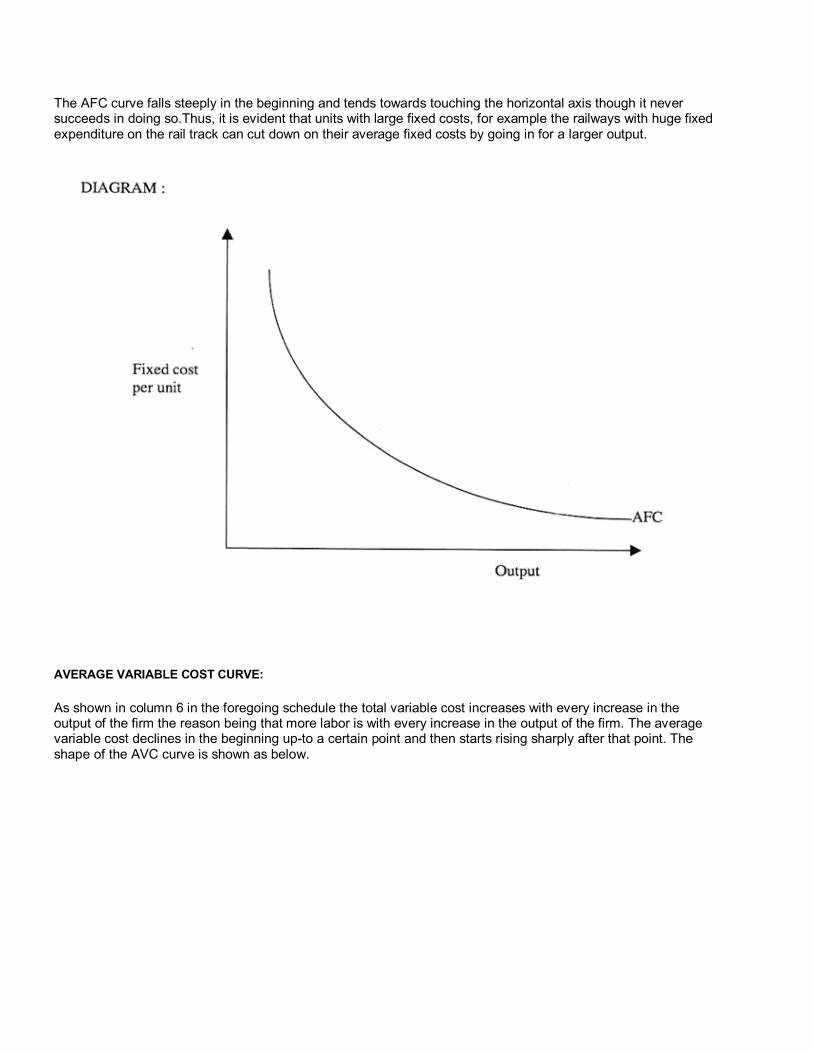

The total fixed cost remains constant through out what ever be the level of output but the average fixed cost diminishes with every increase in output. The reason is that fixed overhead cost is spread over an increasingly larger number of units of the output. If we represent AFC graphically the curve will take the shape of a rectangular hyperbola. To call the AFC a rectangular hyperbola is only to say that the fixed cost is spread over a large units of output and as you divide a constant with a variable, the quotient will fall. .

The AFC curve falls steeply in the beginning and tends towards touching the horizontal axis though it never succeeds in doing so.Thus, it is evident that units with large fixed costs, for example the railways with huge fixed expenditure on the rail track can cut down on their average fixed costs by going in for a larger output.

AVERAGE VARIABLE COST CURVE:

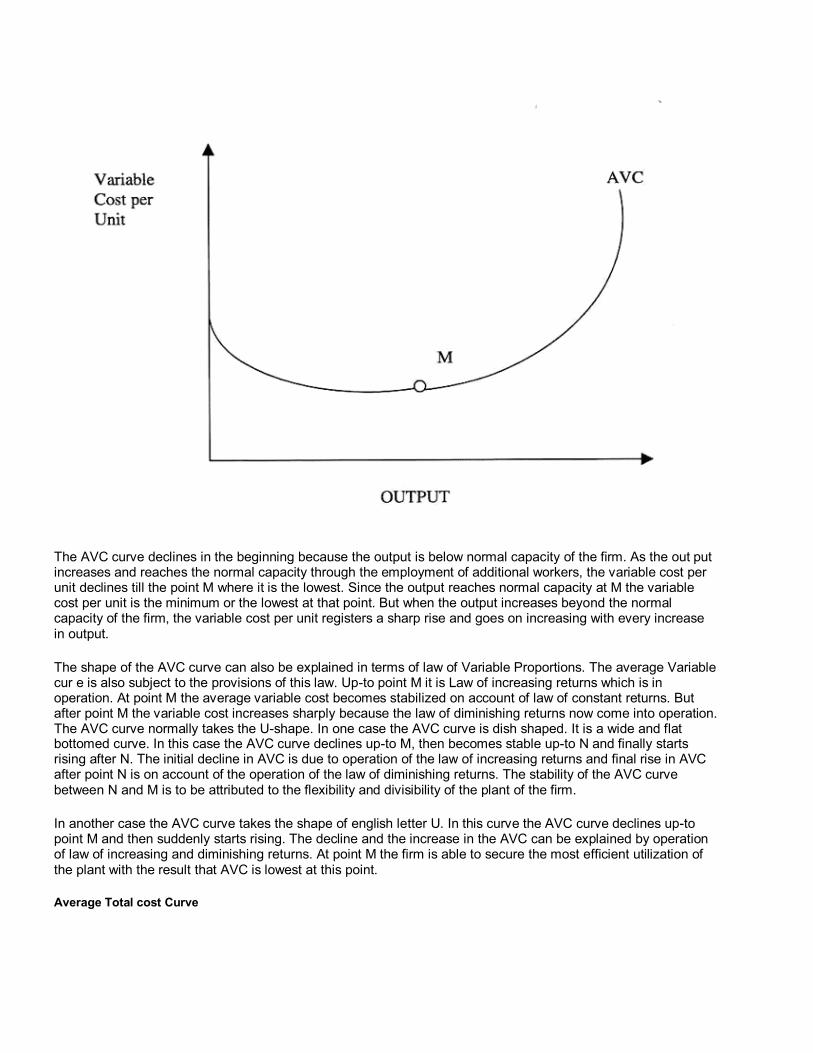

As shown in column 6 in the foregoing schedule the total variable cost increases with every increase in the output of the firm the reason being that more labor is with every increase in the output of the firm. The average variable cost declines in the beginning up-to a certain point and then starts rising sharply after that point. The shape of the AVC curve is shown as below.

The AVC curve declines in the beginning because the output is below normal capacity of the firm. As the out put increases and reaches the normal capacity through the employment of additional workers, the variable cost per unit declines till the point M where it is the lowest. Since the output reaches normal capacity at M the variable cost per unit is the minimum or the lowest at that point. But when the output increases beyond the normal capacity of the firm, the variable cost per unit registers a sharp rise and goes on increasing with every increase in output.

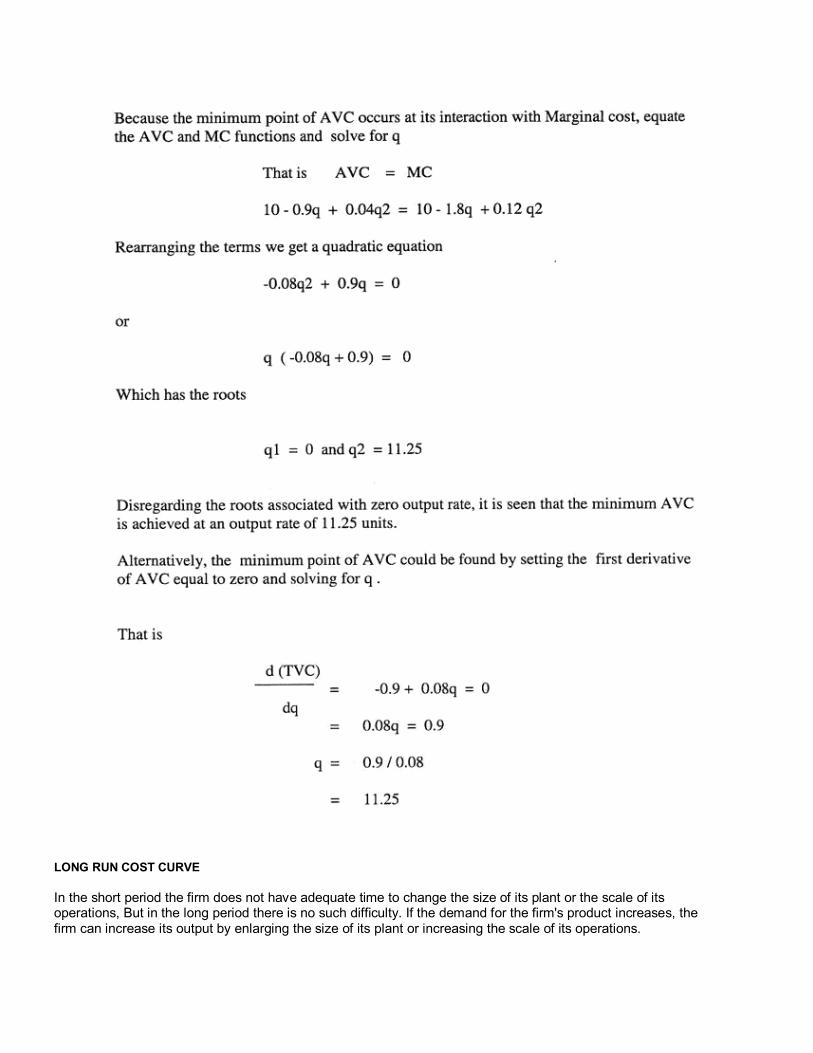

The shape of the AVC curve can also be explained in terms of law of Variable Proportions. The average Variable cur e is also subject to the provisions of this law. Up-to point M it is Law of increasing returns which is in operation. At point M the average variable cost becomes stabilized on account of law of constant returns. But after point M the variable cost increases sharply because the law of diminishing returns now come into operation. The AVC curve normally takes the U-shape. In one case the AVC curve is dish shaped. It is a wide and flat bottomed curve. In this case the AVC curve declines up-to M, then becomes stable up-to N and finally starts rising after N. The initial decline in AVC is due to operation of the law of increasing returns and final rise in AVC after point N is on account of the operation of the law of diminishing returns. The stability of the AVC curve between N and M is to be attributed to the flexibility and divisibility of the plant of the firm.

In another case the AVC curve takes the shape of english letter U. In this curve the AVC curve declines up-to point M and then suddenly starts rising. The decline and the increase in the AVC can be explained by operation of law of increasing and diminishing returns. At point M the firm is able to secure the most efficient utilization of the plant with the result that AVC is lowest at this point.

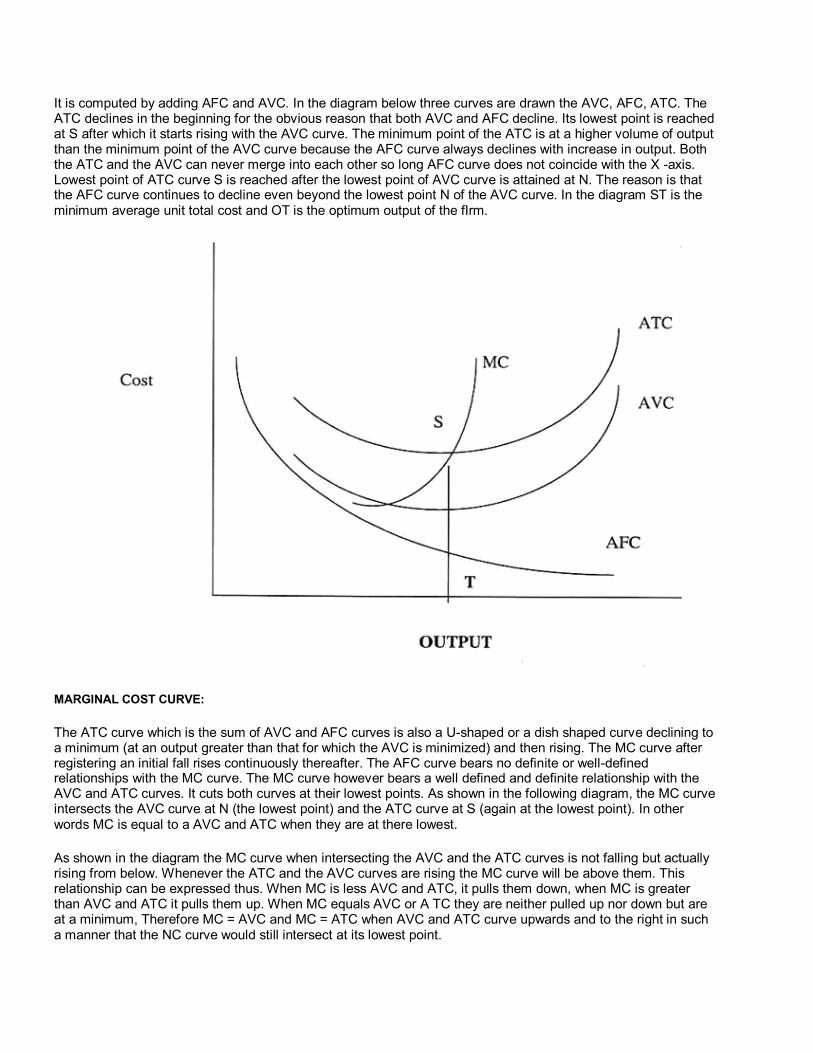

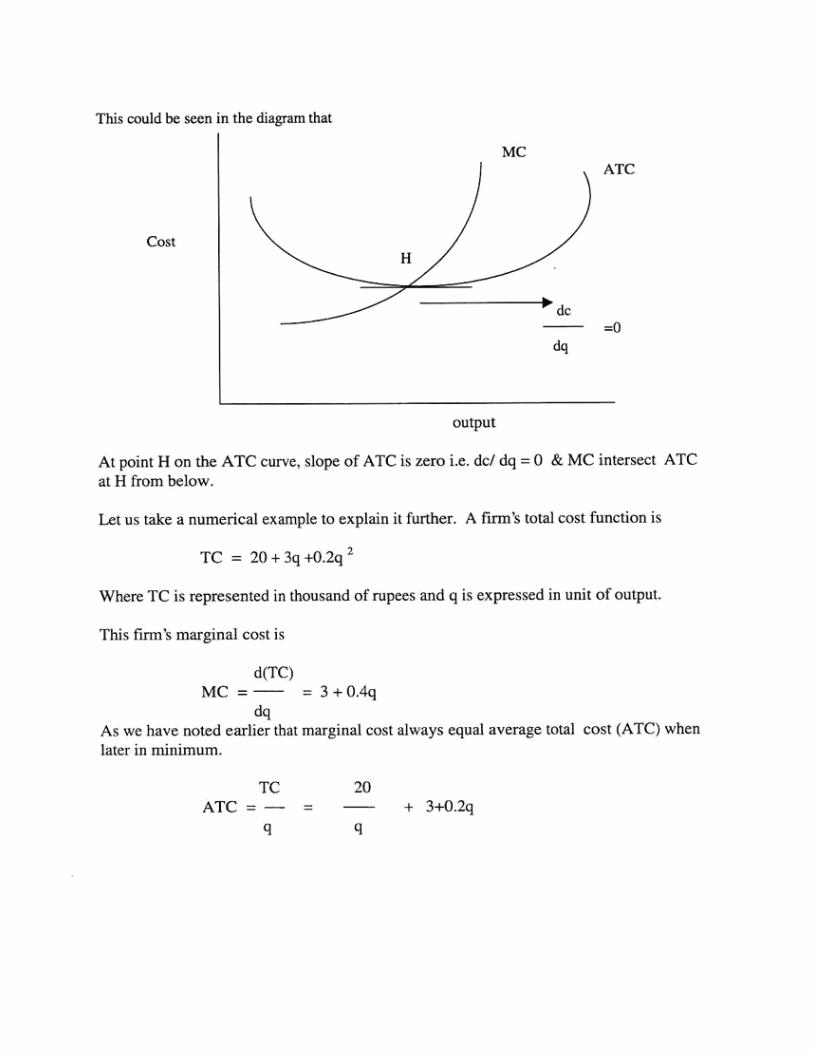

Average Total cost Curve

It is computed by adding AFC and AVC. In the diagram below three curves are drawn the AVC, AFC, ATC. The ATC declines in the beginning for the obvious reason that both AVC and AFC decline. Its lowest point is reached at S after which it starts rising with the AVC curve. The minimum point of the ATC is at a higher volume of output than the minimum point of the AVC curve because the AFC curve always declines with increase in output. Both the ATC and the AVC can never merge into each other so long AFC curve does not coincide with the X -axis. Lowest point of ATC curve S is reached after the lowest point of AVC curve is attained at N. The reason is that the AFC curve continues to decline even beyond the lowest point N of the AVC curve. In the diagram ST is the minimum average unit total cost and OT is the optimum output of the fIrm.

MARGINAL COST CURVE:

The ATC curve which is the sum of AVC and AFC curves is also a U-shaped or a dish shaped curve declining to a minimum (at an output greater than that for which the AVC is minimized) and then rising. The MC curve after registering an initial fall rises continuously thereafter. The AFC curve bears no definite or well-defined relationships with the MC curve. The MC curve however bears a well defined and definite relationship with the AVC and ATC curves. It cuts both curves at their lowest points. As shown in the following diagram, the MC curve intersects the AVC curve at N (the lowest point) and the ATC curve at S (again at the lowest point). In other words MC is equal to a AVC and ATC when they are at there lowest.

As shown in the diagram the MC curve when intersecting the AVC and the ATC curves is not falling but actually rising from below. Whenever the ATC and the AVC curves are rising the MC curve will be above them. This relationship can be expressed thus. When MC is less AVC and ATC, it pulls them down, when MC is greater than AVC and ATC it pulls them up. When MC equals AVC or A TC they are neither pulled up nor down but are at a minimum, Therefore MC = AVC and MC = ATC when AVC and ATC curve upwards and to the right in such a manner that the NC curve would still intersect at its lowest point.

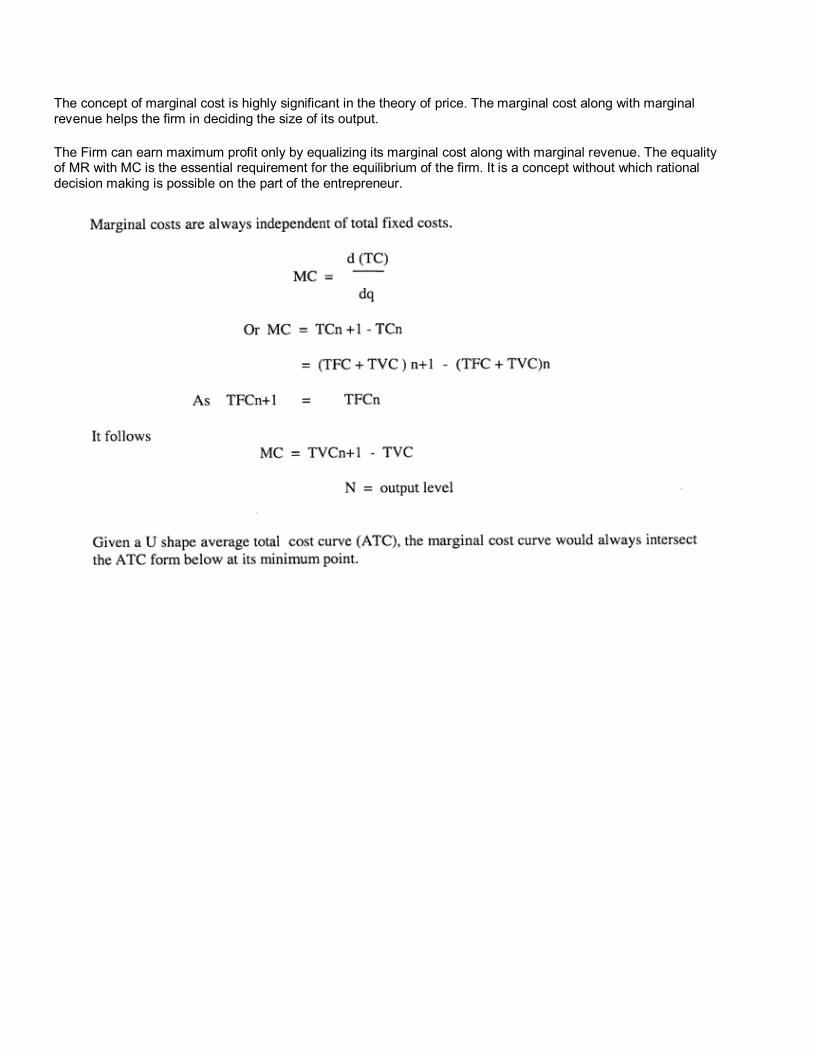

The concept of marginal cost is highly significant in the theory of price. The marginal cost along with marginal revenue helps the firm in deciding the size of its output.

The Firm can earn maximum profit only by equalizing its marginal cost along with marginal revenue. The equality of MR with MC is the essential requirement for the equilibrium of the firm. It is a concept without which rational decision making is possible on the part of the entrepreneur.

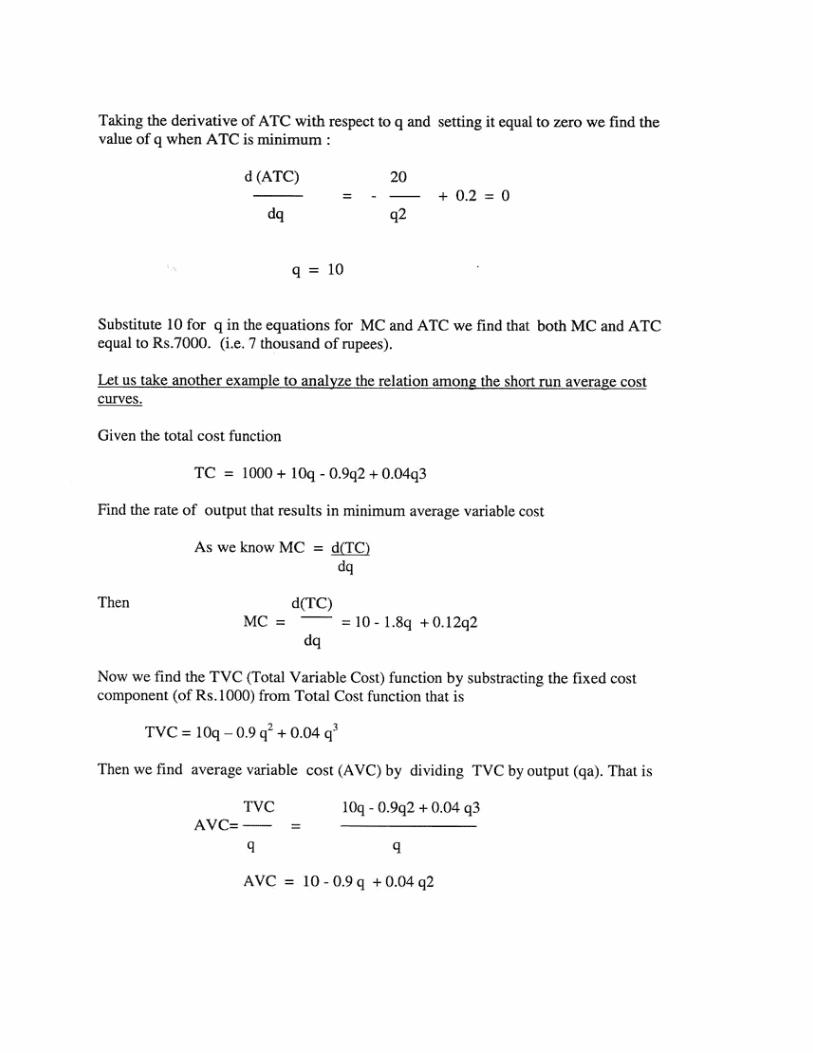

LONG RUN COST CURVE In the short period the firm does not have adequate time to change the size of its plant or the scale of its operations, But in the long period there is no such difficulty. If the demand for the firm's product increases, the firm can increase its output by enlarging the size of its plant or increasing the scale of its operations.

All the factors are variable, none is fixed. Hence, there is no need; of an average fixed cost curves in the long period. The long run cost curves are also, like the short run cost curves, U shaped. The only difference is that the long run cost curves are flatter than the short run cost curves, or the U shape of the long run cost curves is less pronounced than that of short run cost curves.

Let us now take up the more advanced explanation why the U-shape of the long run cost curves is less pronounced compared with the U shape of the short run cost curves. In the short period, as we have already seen as machinery and management are indivisible.

On account of the availability of adequate time, the size of these factors (say machinery and management) can be altered in the long run so that they can be used in differing proportions for the purpose of production. These factors do not therefore remain completely indivisible in the long run.

Since all factors of production (including machinery and management) can be used in variable proportions in the long run, it is possible for the firm to alter its scale of operations in accordance with the requirements of output.

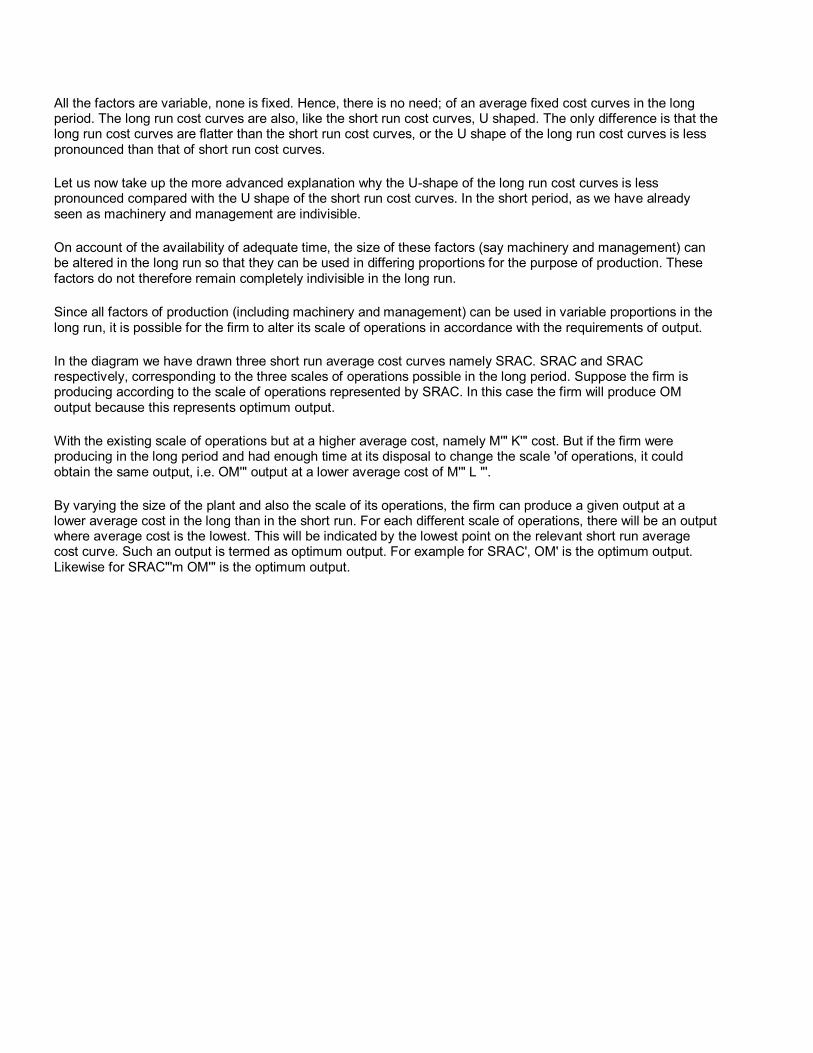

In the diagram we have drawn three short run average cost curves namely SRAC. SRAC and SRAC respectively, corresponding to the three scales of operations possible in the long period. Suppose the firm is producing according to the scale of operations represented by SRAC. In this case the firm will produce OM output because this represents optimum output.

With the existing scale of operations but at a higher average cost, namely M'" K'" cost. But if the firm were producing in the long period and had enough time at its disposal to change the scale 'of operations, it could obtain the same output, i.e. OM'" output at a lower average cost of M'" L "'.

By varying the size of the plant and also the scale of its operations, the firm can produce a given output at a lower average cost in the long than in the short run. For each different scale of operations, there will be an output where average cost is the lowest. This will be indicated by the lowest point on the relevant short run average cost curve. Such an output is termed as optimum output. For example for SRAC', OM' is the optimum output. Likewise for SRAC"'m OM'" is the optimum output.

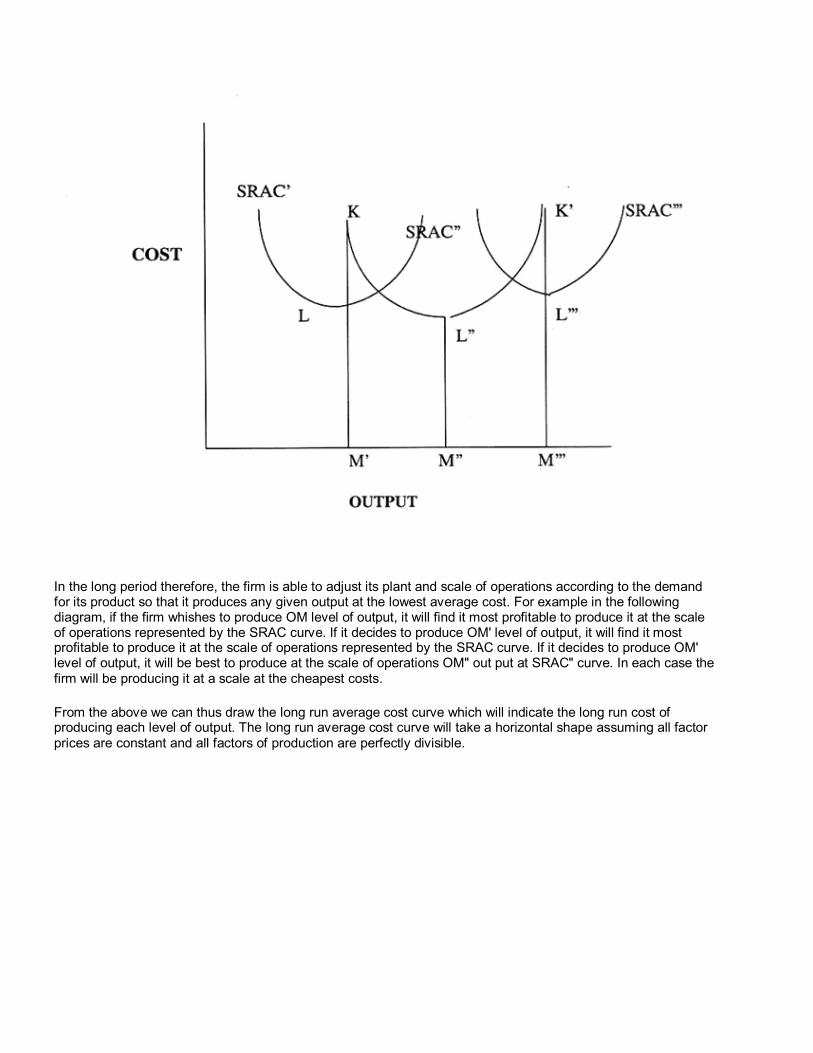

In the long period therefore, the firm is able to adjust its plant and scale of operations according to the demand for its product so that it produces any given output at the lowest average cost. For example in the following diagram, if the firm whishes to produce OM level of output, it will find it most profitable to produce it at the scale of operations represented by the SRAC curve. If it decides to produce OM' level of output, it will find it most profitable to produce it at the scale of operations represented by the SRAC curve. If it decides to produce OM' level of output, it will be best to produce at the scale of operations OM" out put at SRAC" curve. In each case the firm will be producing it at a scale at the cheapest costs.

From the above we can thus draw the long run average cost curve which will indicate the long run cost of producing each level of output. The long run average cost curve will take a horizontal shape assuming all factor prices are constant and all factors of production are perfectly divisible.

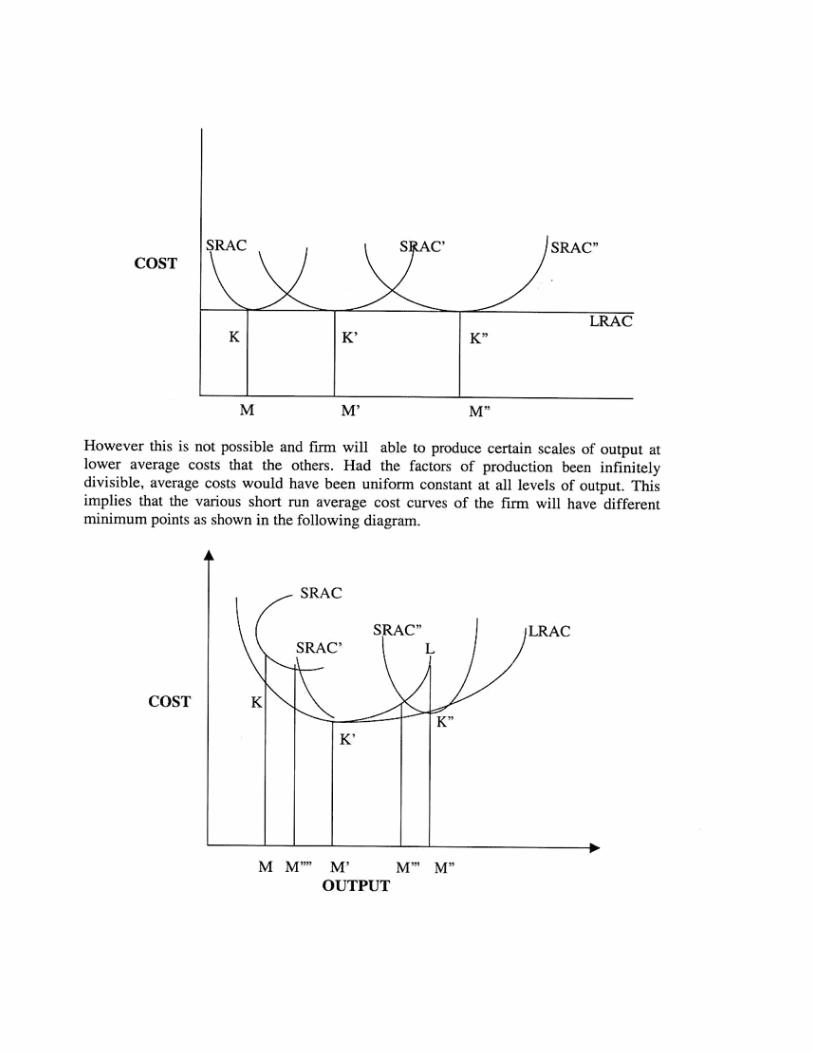

In the above diagram the curve SRAC' has a lower minimum point at K' at either the curve SRAC or the curve SRAC". OM' constitutes the optimum output of curve SRAC'. The LRAC is the long run average cost curves. It is tangent to all the SRAC curves at different points. It is tangent to SRAC at K. SRAC' at K' and SRAC" at K". The LRAC curve is U-shaped though it U shape is not as pronounced as the SRAC curves. It is flatter than the SRAC curve and is also known as the envelope curve as it envelopes all the SRAC. The LRAC is also called the planning curve as it represents the cost output data which are useful to the firm when it is formulating its policy with regard to its scale of operations over a long period of time.

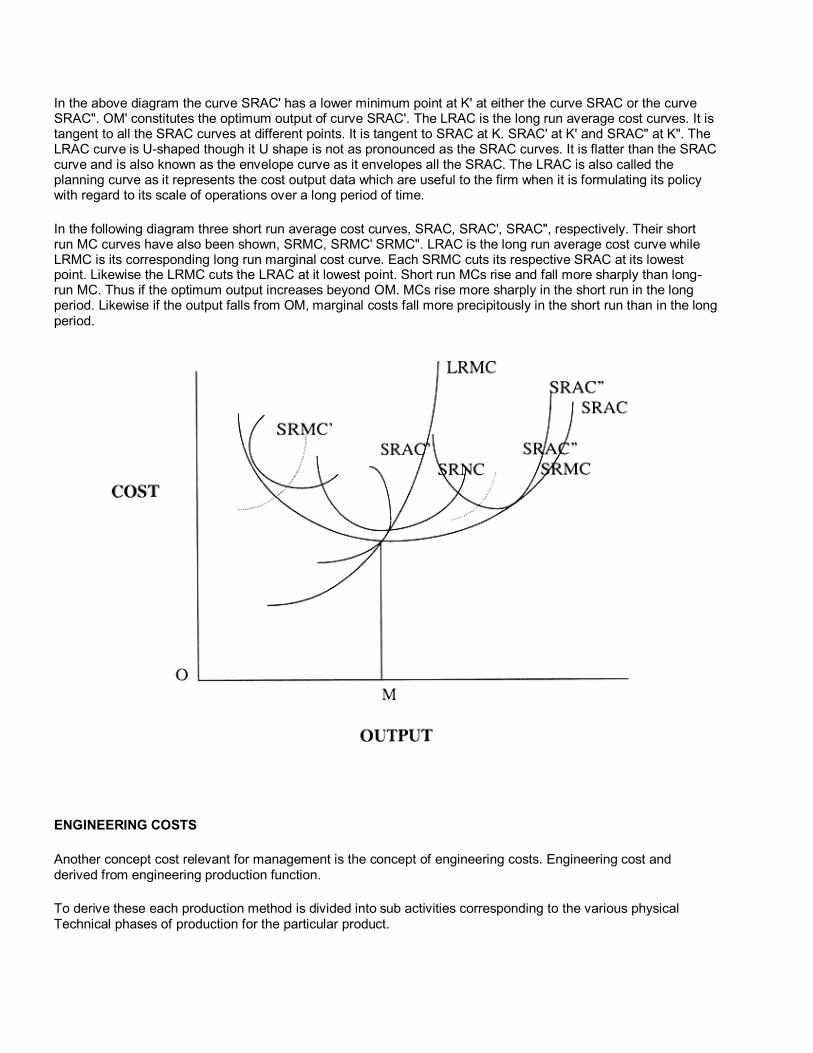

In the following diagram three short run average cost curves, SRAC, SRAC', SRAC", respectively. Their short run MC curves have also been shown, SRMC, SRMC' SRMC". LRAC is the long run average cost curve while LRMC is its corresponding long run marginal cost curve. Each SRMC cuts its respective SRAC at its lowest point. Likewise the LRMC cuts the LRAC at it lowest point. Short run MCs rise and fall more sharply than long-run MC. Thus if the optimum output increases beyond OM. MCs rise more sharply in the short run in the long period. Likewise if the output falls from OM, marginal costs fall more precipitously in the short run than in the long period.

ENGINEERING COSTS

Another concept cost relevant for management is the concept of engineering costs. Engineering cost and derived from engineering production function.

To derive these each production method is divided into sub activities corresponding to the various physical Technical phases of production for the particular product.

For each phase the quantities of factor of production are estimated and finally the cost of each phase is calculated on the basic of prevailing factor prices. The total cost of the particular method of production is the sum of cost of its different phases.

A firm has to do calculation for all available plant sizes. Production isoquants are subsequently estimated and from them, given the factor prices, the long run and short run function may be derived.

It is pertinent to note that the engineering production function and the cost functions derived from them refer usually to the production costs and do not, the administrative cost for the operation of any given plant.

ECONOMIES OF SCALE:

A firm is said to be reaping economies of scale when its LTC increases less than proportionately with increase in its scale of operations or when its LAC falls as its output expands. Alternatively it could be defined in terms of output elasticity of total cost (e TC, Q):

ETC, Q = [d (TC) / dQ]

If eTC, Q < 1 there are economies of scale. The reasons for firms to enjoy economies of scale are :

1. Due to large plant 2. Due to large firm

DUE TO LARGE FIRM: The various economies of scale which are enjoyed by the firm due to its large size are :

Specialization: This improves productivity by need for limited training for a specialized job only, learning by doing, saving of time which otherwise gets lost in moving from one activity to another. The bigger plants are able to introduce the desired level of specialization which the small firms are not able to afford.

Indivisibility: There are certain plants and equipment's which are indivisible in small size and units like tractor and tube-well for agriculture, large plants and machines for manufacturing, computers for computation work etc. Small firm's are not able to enjoy fruits of up-to date technology.

Productivity / Purchase prices: It is believed that why the productive capacity of capital equipment rises much faster than its purchase price.

Equipment Maintenance: Large plants need to carry relatively less spare parts and personnel for attending to random breakdown than small firms need to do. Thus larger firms need to produce less on repairs and maintenance, and thereby reap the economies of mass scale production.

DUE TO LARGE PLANT: There are several economies which rise to the firm due to size of the plant. It is believe that while manufacturing work is handled by individual plants, purchases of raw materials, selling of products, advertisements, fund raising and overall management are centralized at firm level.

Quantity Discounts: Firms that purchase large quantities of goods and services from suppliers are often able to negotiate large discounts which results in lower average costs in relation to small firms. Also per unit voucher cost is less for large firms vis-a-vis small firms.

Fund raising: The administrative cost of negotiating debt and floating cost of equity capital and debentures per unit of funds raised vary inversely with the size of the debt / capital ratio. In addition the securities of the large

firms are less risky than the securities of the small firm, and thereby the large firms get an edge over the small firms in fund raising.

Sales Promotion: Large firms are even able to secure quantity discounts even in securing space in various advertising media. Besides advertising outlay is like a fixed cost and so they create lesser burden per unit of unit of output rather than on smaller ones.

Innovation: Large firm's are in a better position to carry out research and development activities and thereby adopt the latest method of material procurements, production and sales, than their smaller counterparts.

Management: Large firm's enjoy the benefit of top caliber management personnel, specialization and so on.

Due to the above economies of production, the long run total cost curve is concave from the output axis, the output elasticity of total cost is less than unity, or the long run average cost curve is downward sloping until the output level where such economies dominate.

DISECONOMIES OF SCALE

There are certain cost disadvantages in mass production vis-a-vis small production. The reasons for this are summarized as below:

Transportation cost: Primary cause of diseconomies of scale due to large plant are transportation cost. If the raw material is spatially well spread, then the transportation cost of raw-material will be more in a large plant wherever located than in a number of small plants well dispersed geographically.

Imperfection in the Labour market: In a developing economy like India there is high degree of immobility in labor market due to attachment of relatives and land. There is also cost mobility in terms of transport and residential accommodation, contentedness etc.

DUE TO LARGE FIRM: The existence of diseconomies of scale for a fIrm arises due to problems of coordination and control experienced by the management. Labour unions and their size grow faster than the size of the firm. There are evidences of strikes, lockouts and absenteeism. There is also a dearth of capable and honest top-management.

Due to all these factors small firms are better managed than large firms and thereby have lower costs than the larger firm.

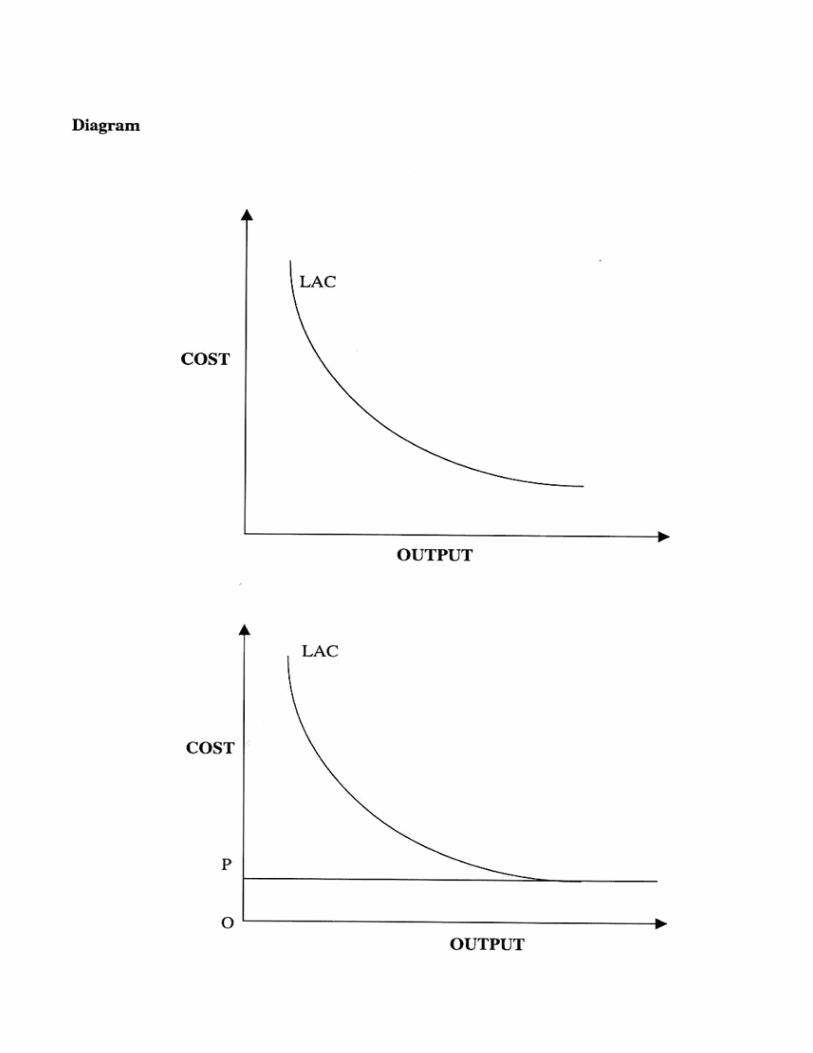

Diseconomies of scale explain the upward sloping long-run average cost curve or the less than unit elasticity of total cost with respect to output. These together with the economies of scale fully rationalize the V-shaped of the long run average cost curve.

In the above figure, LAC declines as output expands up-to Q1, beyond which it stays constant at OP. The output level where LAC is the least is called the optimum level of output from the supply side. In the case of the other figure, the optimum level thus comprises of output level Q1 or any level greater than that. To distinguish Q1 output from other optimum output levels under such a situation, MES terminology can be used. The MES is the Minimum Efficient Scale and is Q1 marks the MES while output > = Q1 gives the optimum level of output.

In the second diagram LAC falls monotonically as the output expands, that is economies of scale out weight the

diseconomies of scale at all levels of output.

A business firm charters its business operations with reference to specified objective function. Its business operations are conducted in such a manner that its objective function is maximized. If objective is to maximize profits, then business operation are carried out in such a way that profits is maximized. The objectives may be sales maximization.

We shall discuss from models of the objectives of a business firm :

1. Model of project maximization 2. Baumol's model of sales maximization 3. Marris model managerial enterprise 4. Williansom's model of managerial discussion

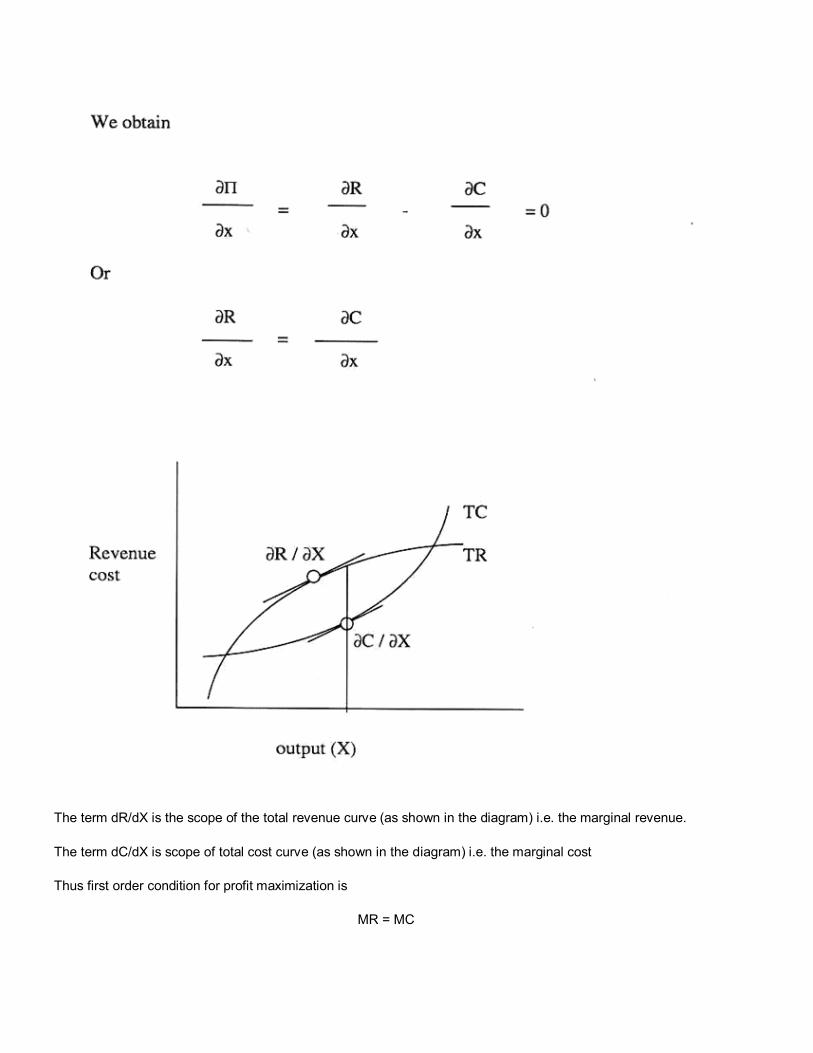

1. Model of Project Maximization

A firm shall choose that level of output at which profit is maximized Project is the difference between total revenue and total cost

Mathematically

Total project function of a firm is

II= R-C

II = Profit