15-1 Accounting for a Capital Lease Chapter 15 Illustrated Solution: Problem 15-41

Accounting for a Capital Lease

Dec 30, 2015

Chapter 15. Illustrated Solution: Problem 15-41. Accounting for a Capital Lease. Problem Assumption. This is a capitalized lease that qualifies as a sales-type lease for both Dannell Tool Co., the lessee, and Crosby Equipment Co., the lessor. Present Value. Dannell Tool Company. - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

15-1

Accounting for aCapital Lease

Chapter 15Illustrated Solution: Problem 15-41Illustrated Solution: Problem 15-41

15-2

Problem AssumptionProblem Assumption

This is a capitalized lease that qualifies as a sales-type lease for both Dannell Tool Co., the lessee, and Crosby Equipment Co., the lessor.

15-3

Present ValuePresent Value

The first task is to compute the present value of the lease payments for Dannell. In this case, Dannell can use Crosby’s implicit interest rate of 10% because it is known and is lower than Dannell’s incremental borrowing rate.

Dannell Tool Company

15-4

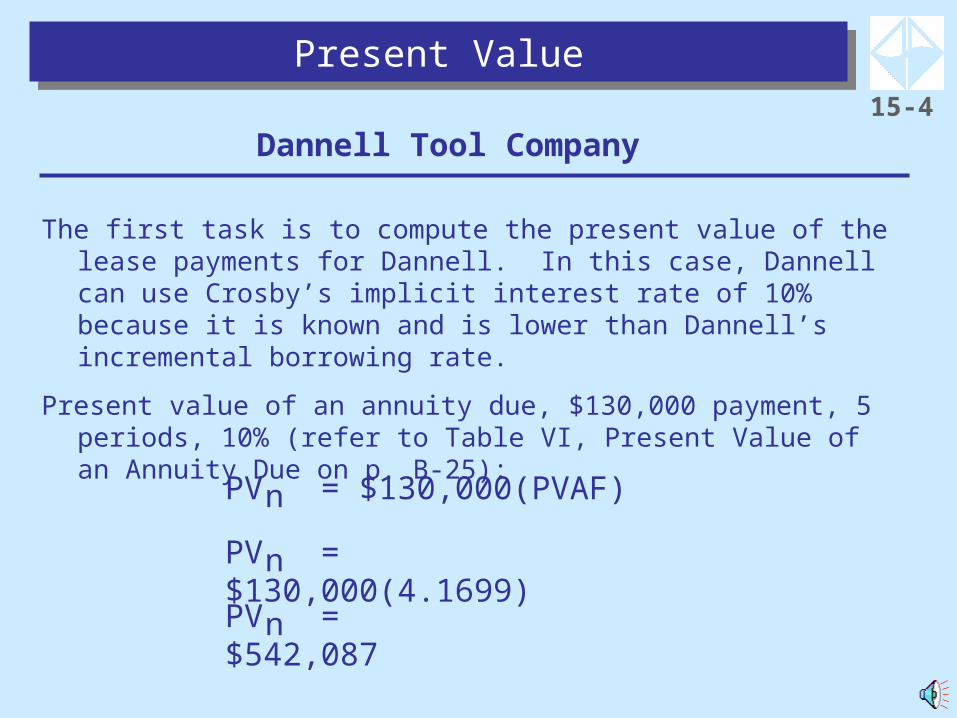

Present ValuePresent Value

The first task is to compute the present value of the lease payments for Dannell. In this case, Dannell can use Crosby’s implicit interest rate of 10% because it is known and is lower than Dannell’s incremental borrowing rate.

Present value of an annuity due, $130,000 payment, 5 periods, 10% (refer to Table VI, Present Value of an Annuity Due on p. B-25):

PV = $130,000(PVAF)n

PV = $130,000(4.1699)n

PV = $542,087n

Dannell Tool Company

15-5

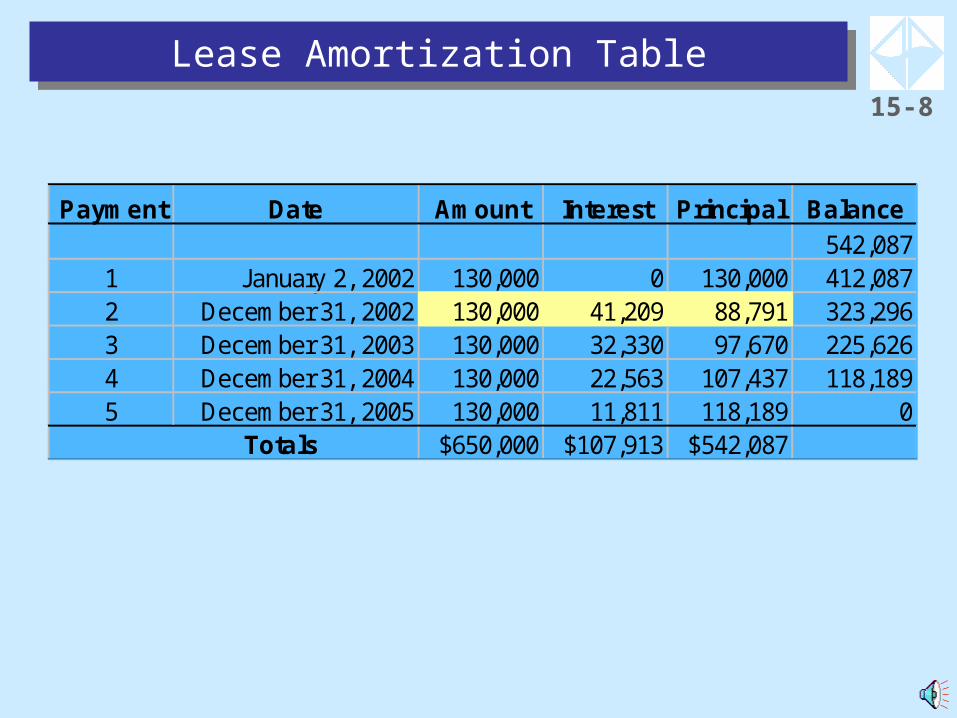

Lease Amortization TableLease Amortization Table

Payment Date Amount Interest Principal Balance542,087

1 January 2, 2002 130,000 0 130,000 412,0872 December 31, 2002 130,000 41,209 88,791 323,2963 December 31, 2003 130,000 32,330 97,670 225,6264 December 31, 2004 130,000 22,563 107,437 118,1895 December 31, 2005 130,000 11,811 118,189 0

$650,000 $107,913 $542,087 Totals

15-6

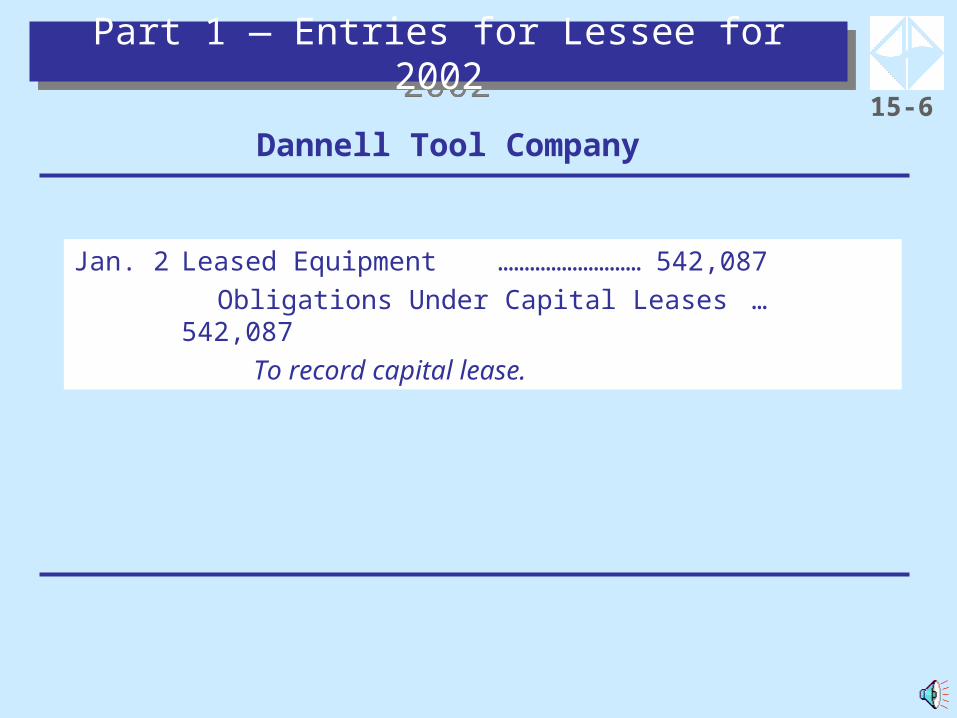

Jan. 2 Leased Equipment……………………… 542,087

Obligations Under Capital Leases… 542,087

To record capital lease.

Part 1 — Entries for Lessee for 2002Part 1 — Entries for Lessee for 2002

Dannell Tool Company

15-7

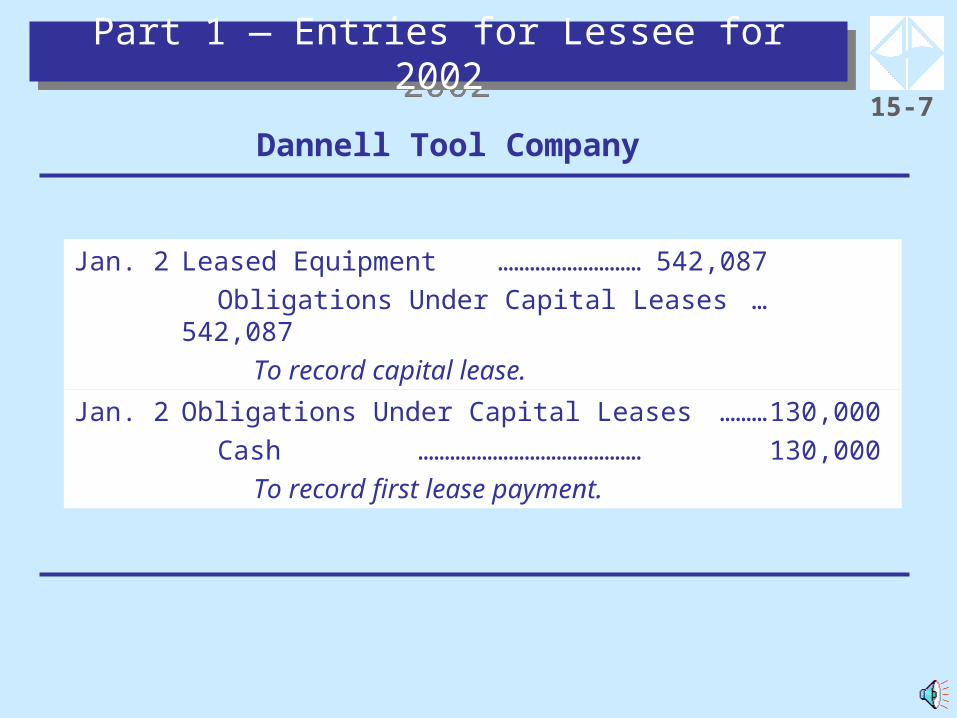

Jan. 2 Leased Equipment……………………… 542,087

Obligations Under Capital Leases… 542,087

To record capital lease.

Part 1 — Entries for Lessee for 2002Part 1 — Entries for Lessee for 2002

Jan. 2 Obligations Under Capital Leases……… 130,000

Cash…………………………………… 130,000

To record first lease payment.

Dannell Tool Company

15-8

Lease Amortization TableLease Amortization Table

Payment Date Amount Interest Principal Balance542,087

1 January 2, 2002 130,000 0 130,000 412,0872 December 31, 2002 130,000 41,209 88,791 323,2963 December 31, 2003 130,000 32,330 97,670 225,6264 December 31, 2004 130,000 22,563 107,437 118,1895 December 31, 2005 130,000 11,811 118,189 0

$650,000 $107,913 $542,087 Totals

15-9

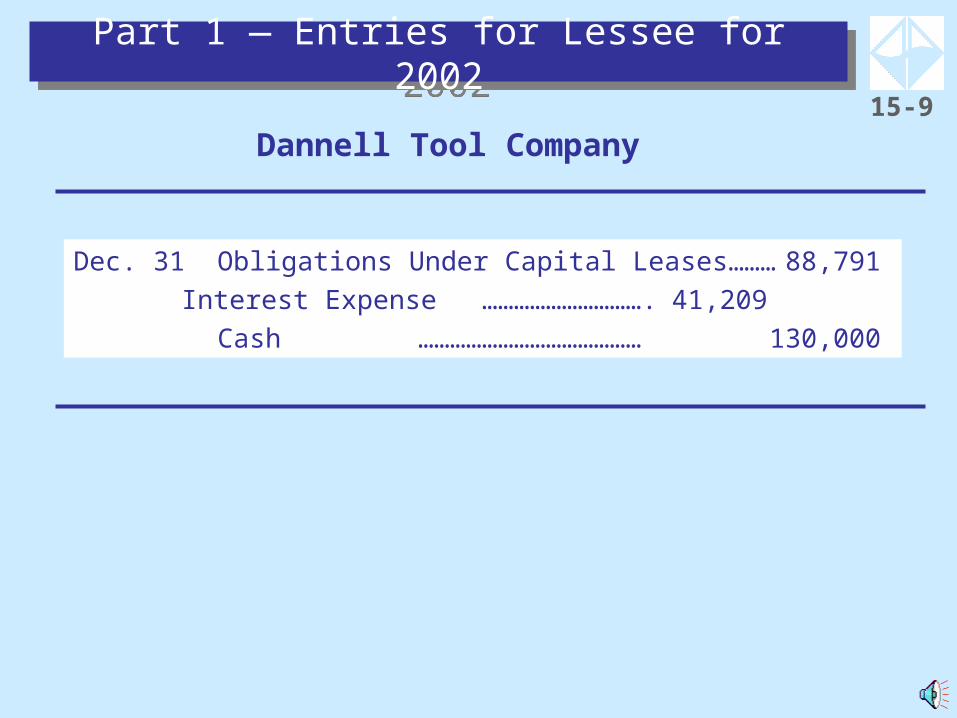

Dec. 31 Obligations Under Capital Leases……… 88,791

Interest Expense…………………………. 41,209

Cash…………………………………… 130,000

Part 1 — Entries for Lessee for 2002Part 1 — Entries for Lessee for 2002

Dannell Tool Company

15-10

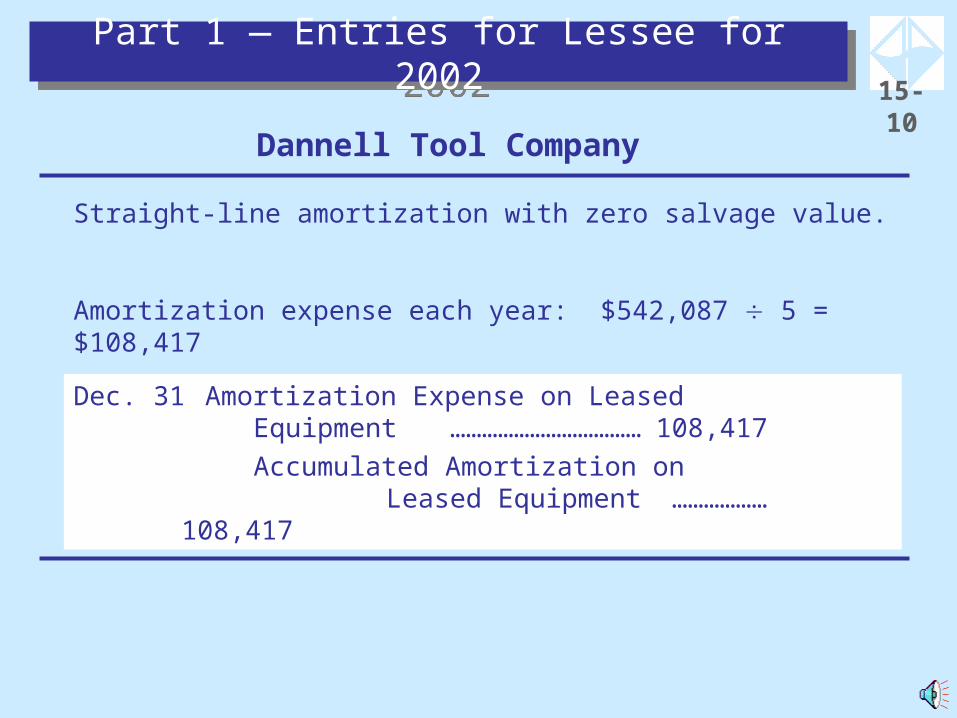

Straight-line amortization with zero salvage value.

Amortization expense each year: $542,087 5 = $108,417

Dannell Tool Company

Part 1 — Entries for Lessee for 2002Part 1 — Entries for Lessee for 2002

Dec. 31 Amortization Expense on LeasedEquipment……………………………… 108,417

Accumulated Amortization onLeased Equipment……………… 108,417

15-11

Initial direct costs are deferred until the time of sale. They will be included in Cost of Goods Sold.

Crosby Equipment Company

Part 2 — Entries for Lessor for 2002Part 2 — Entries for Lessor for 2002

15-12

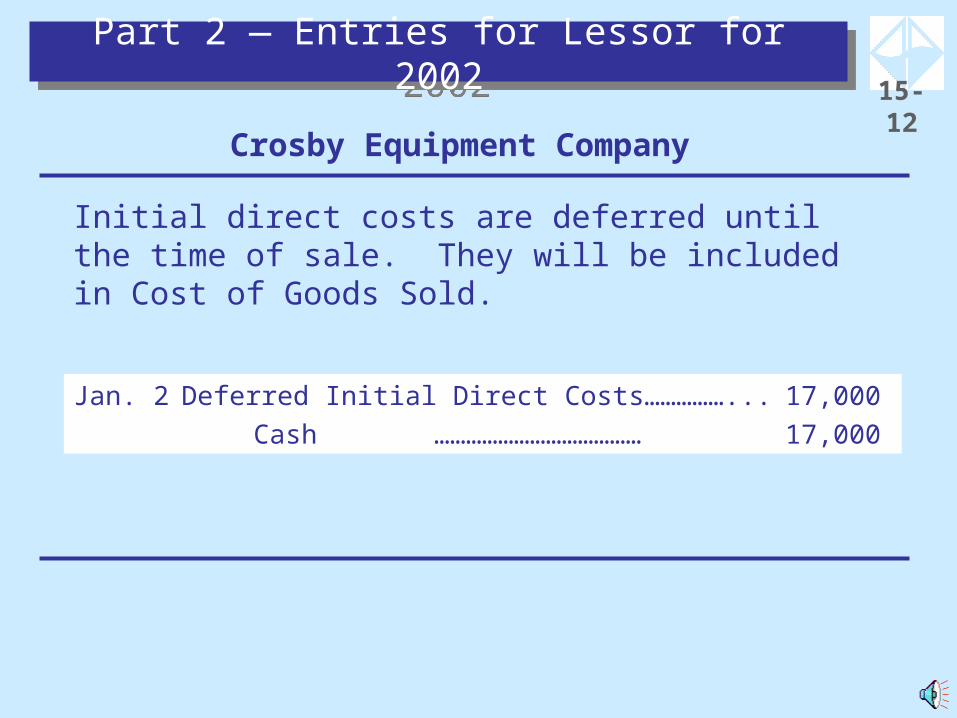

Initial direct costs are deferred until the time of sale. They will be included in Cost of Goods Sold.

Crosby Equipment Company

Jan. 2 Deferred Initial Direct Costs……………... 17,000

Cash………………………………… 17,000

Part 2 — Entries for Lessor for 2002Part 2 — Entries for Lessor for 2002

15-13

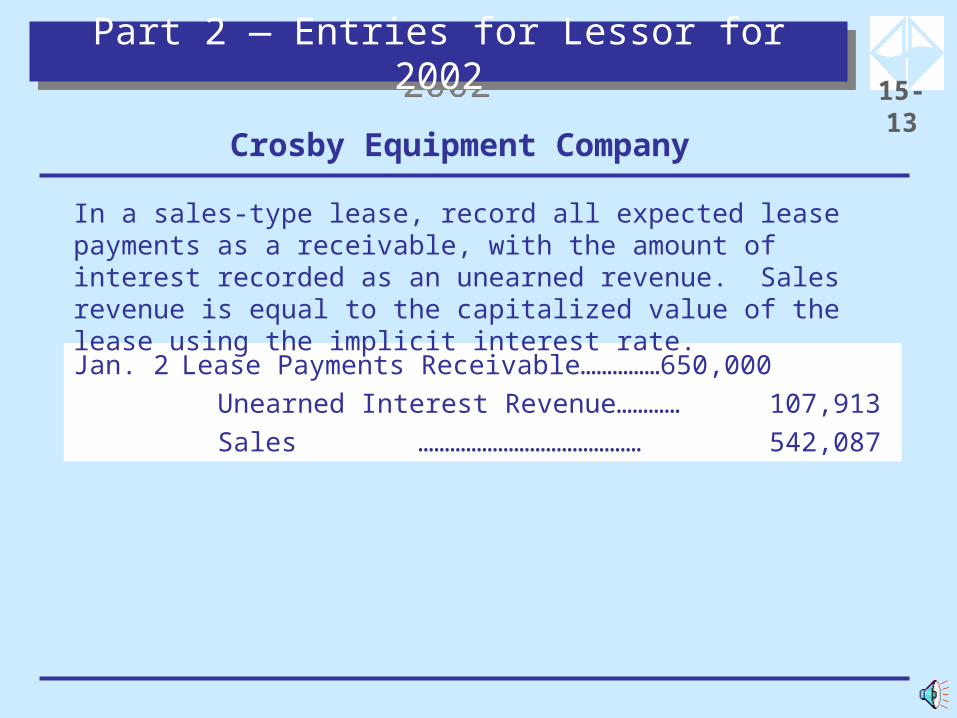

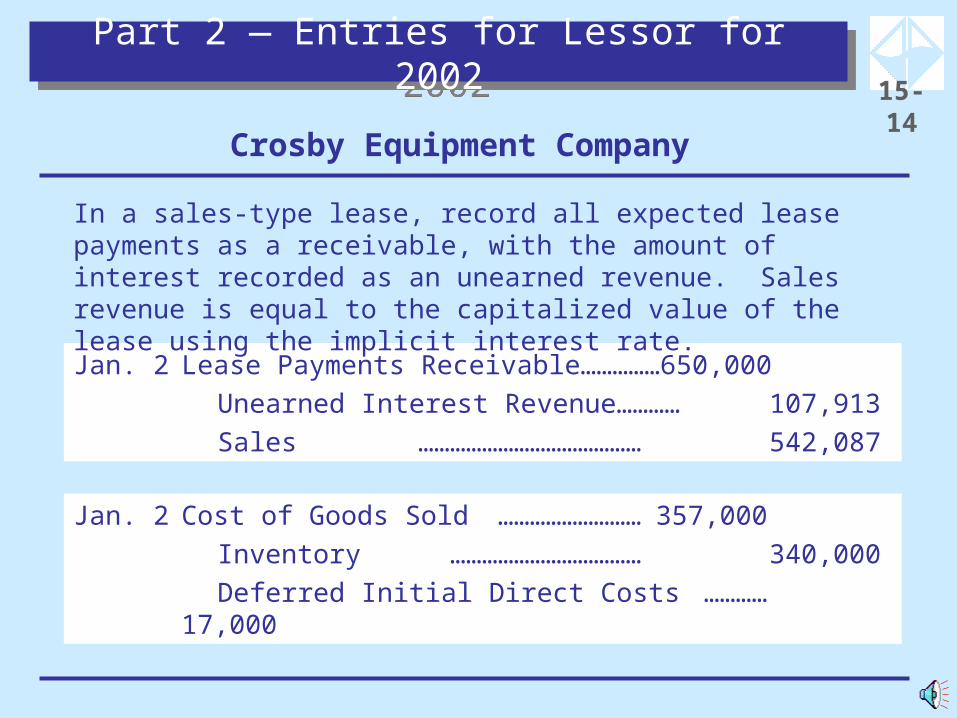

Jan. 2 Lease Payments Receivable…………… 650,000

Unearned Interest Revenue………… 107,913

Sales…………………………………… 542,087

In a sales-type lease, record all expected lease payments as a receivable, with the amount of interest recorded as an unearned revenue. Sales revenue is equal to the capitalized value of the lease using the implicit interest rate.

Part 2 — Entries for Lessor for 2002Part 2 — Entries for Lessor for 2002

Crosby Equipment Company

15-14

Jan. 2 Lease Payments Receivable…………… 650,000

Unearned Interest Revenue………… 107,913

Sales…………………………………… 542,087

Jan. 2 Cost of Goods Sold……………………… 357,000

Inventory……………………………… 340,000

Deferred Initial Direct Costs………… 17,000

In a sales-type lease, record all expected lease payments as a receivable, with the amount of interest recorded as an unearned revenue. Sales revenue is equal to the capitalized value of the lease using the implicit interest rate.

Part 2 — Entries for Lessor for 2002Part 2 — Entries for Lessor for 2002

Crosby Equipment Company

15-15

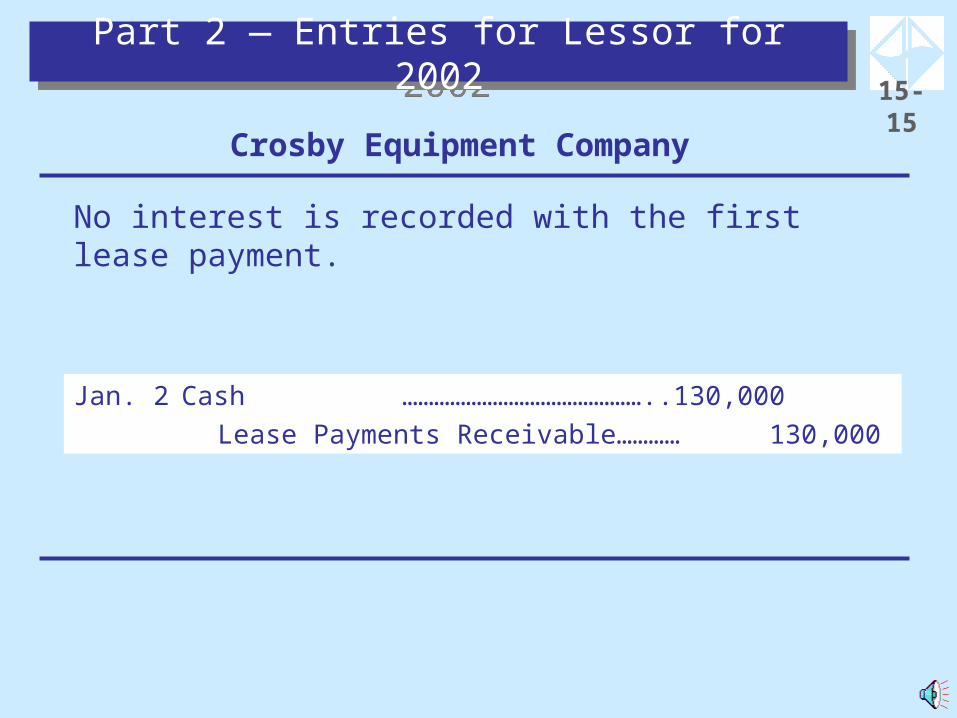

No interest is recorded with the first lease payment.

Crosby Equipment Company

Jan. 2 Cash……………………………………….. 130,000

Lease Payments Receivable………… 130,000

Part 2 — Entries for Lessor for 2002Part 2 — Entries for Lessor for 2002

15-16

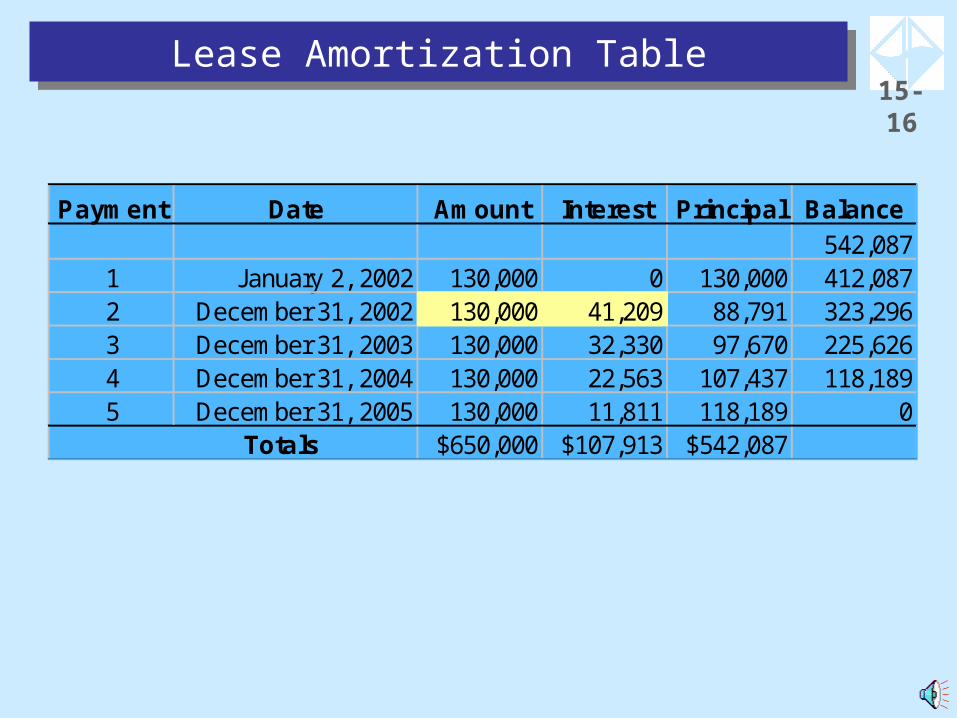

Lease Amortization TableLease Amortization Table

Payment Date Amount Interest Principal Balance542,087

1 January 2, 2002 130,000 0 130,000 412,0872 December 31, 2002 130,000 41,209 88,791 323,2963 December 31, 2003 130,000 32,330 97,670 225,6264 December 31, 2004 130,000 22,563 107,437 118,1895 December 31, 2005 130,000 11,811 118,189 0

$650,000 $107,913 $542,087 Totals

15-17

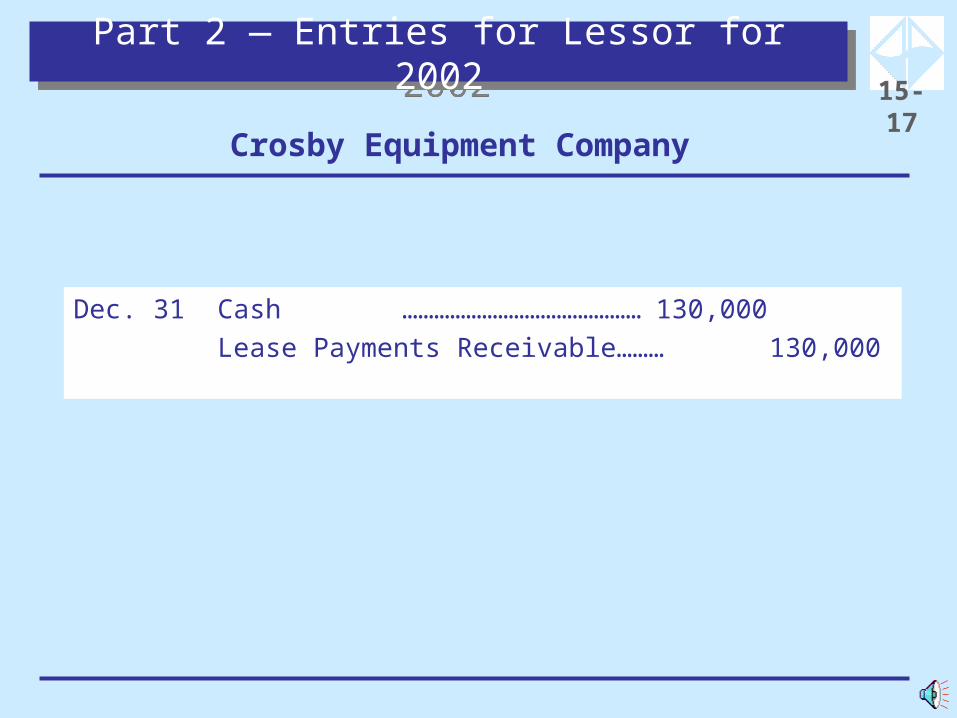

Dec. 31 Cash……………………………………… 130,000

Lease Payments Receivable ……… 130,000

Part 2 — Entries for Lessor for 2002Part 2 — Entries for Lessor for 2002

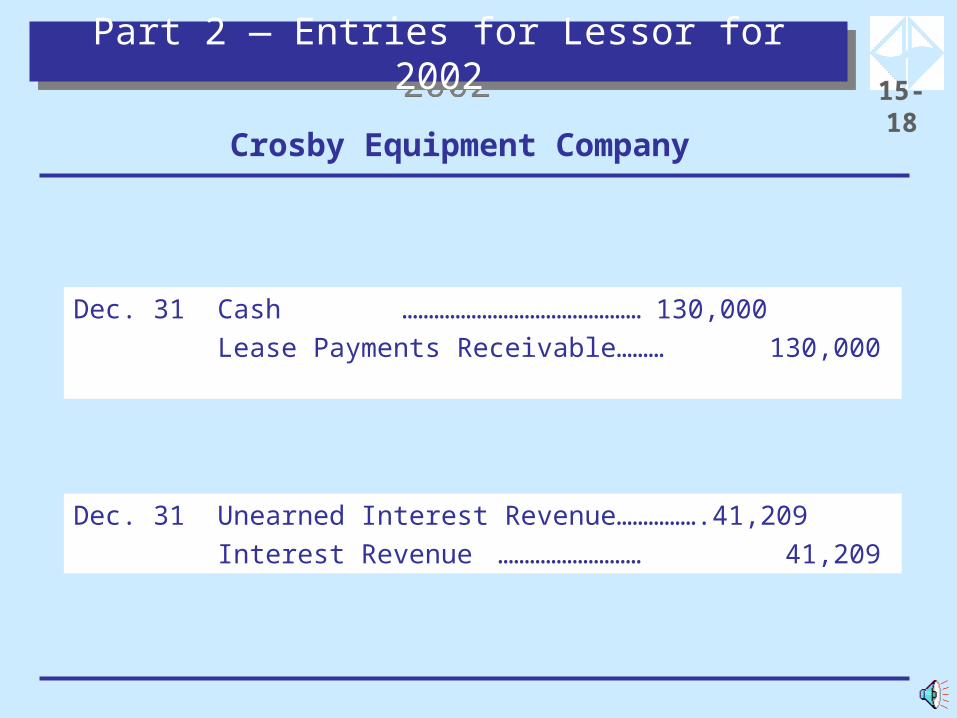

Crosby Equipment Company

15-18

Dec. 31 Cash……………………………………… 130,000

Lease Payments Receivable ……… 130,000

Dec. 31 Unearned Interest Revenue……………. 41,209

Interest Revenue……………………… 41,209

Part 2 — Entries for Lessor for 2002Part 2 — Entries for Lessor for 2002

Crosby Equipment Company

15-19

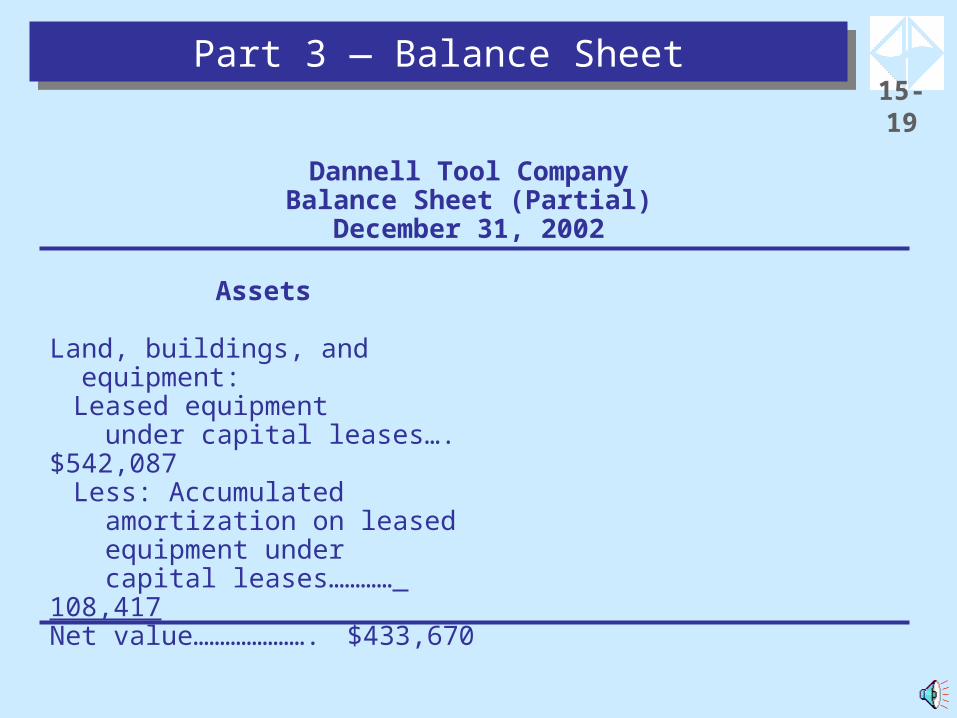

Dannell Tool CompanyBalance Sheet (Partial)

December 31, 2002

Part 3 — Balance SheetPart 3 — Balance Sheet

Assets

Land, buildings, and equipment:

Leased equipment under capital leases…. $542,087Less: Accumulated amortization on leased equipment under capital leases………… 108,417

Net value…………………. $433,670

15-20

Dannell Tool CompanyBalance Sheet (Partial)

December 31, 2002

Part 3 — Balance SheetPart 3 — Balance Sheet

Assets

Land, buildings, and equipment:

Leased equipment under capital leases…. $542,087Less: Accumulated amortization on leased equipment under capital leases………… 108,417

Net value…………………. $433,670

Liabilities

Current liabilities:Obligations under capital leases—current portion..

Long-term liabilities:Obligations under capital leases, exclusive of $??,??? included in current liabilities………..

15-21

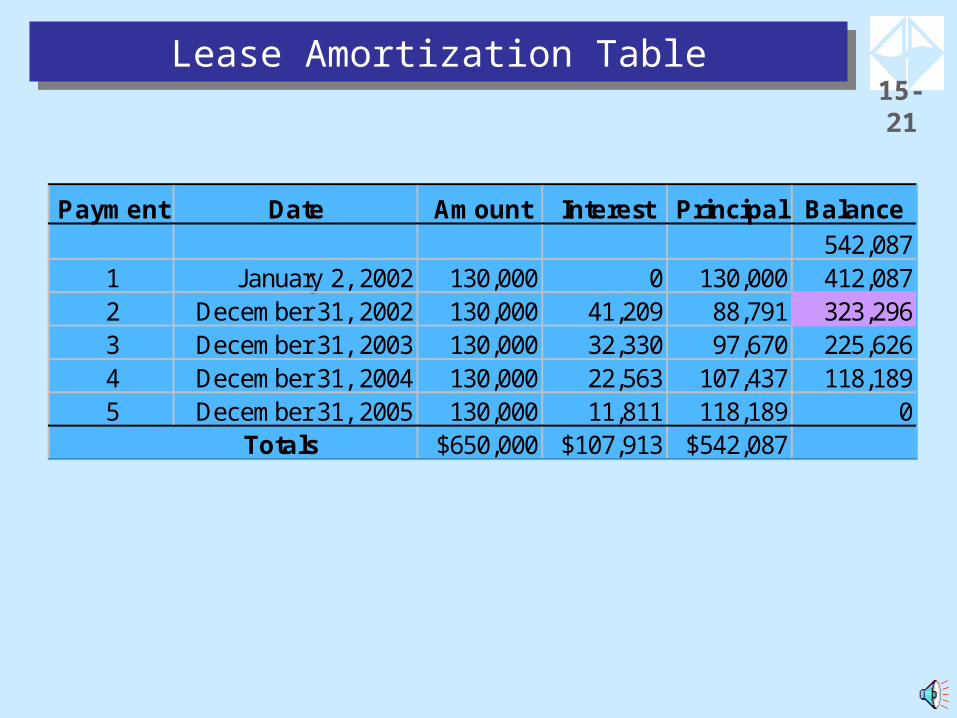

Lease Amortization TableLease Amortization Table

Payment Date Amount Interest Principal Balance542,087

1 January 2, 2002 130,000 0 130,000 412,0872 December 31, 2002 130,000 41,209 88,791 323,2963 December 31, 2003 130,000 32,330 97,670 225,6264 December 31, 2004 130,000 22,563 107,437 118,1895 December 31, 2005 130,000 11,811 118,189 0

$650,000 $107,913 $542,087 Totals

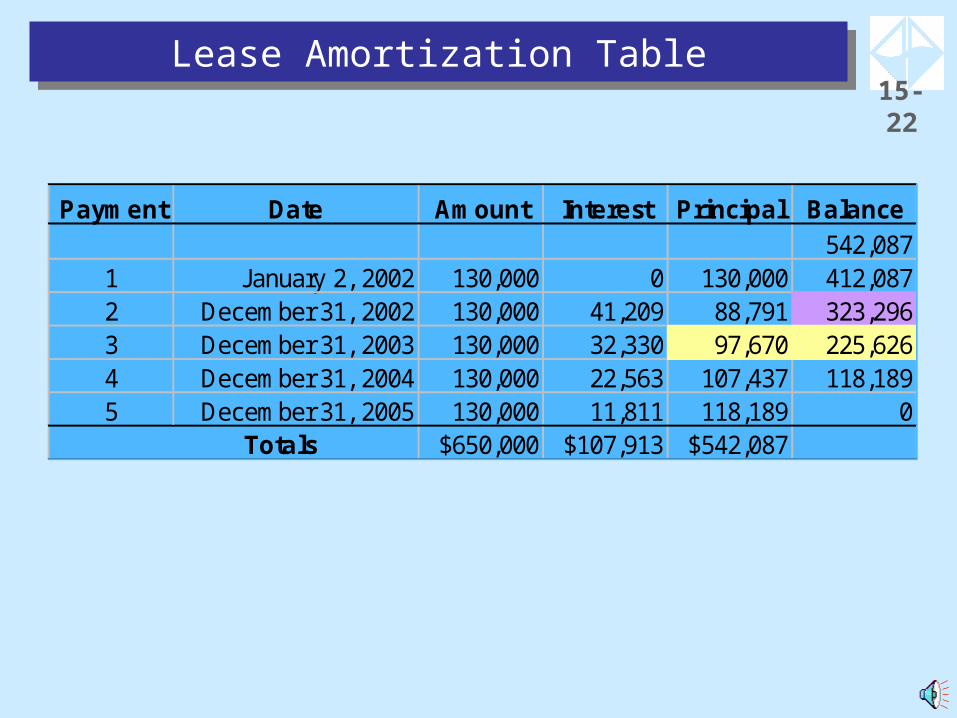

15-22

Lease Amortization TableLease Amortization Table

Payment Date Amount Interest Principal Balance542,087

1 January 2, 2002 130,000 0 130,000 412,0872 December 31, 2002 130,000 41,209 88,791 323,2963 December 31, 2003 130,000 32,330 97,670 225,6264 December 31, 2004 130,000 22,563 107,437 118,1895 December 31, 2005 130,000 11,811 118,189 0

$650,000 $107,913 $542,087 Totals

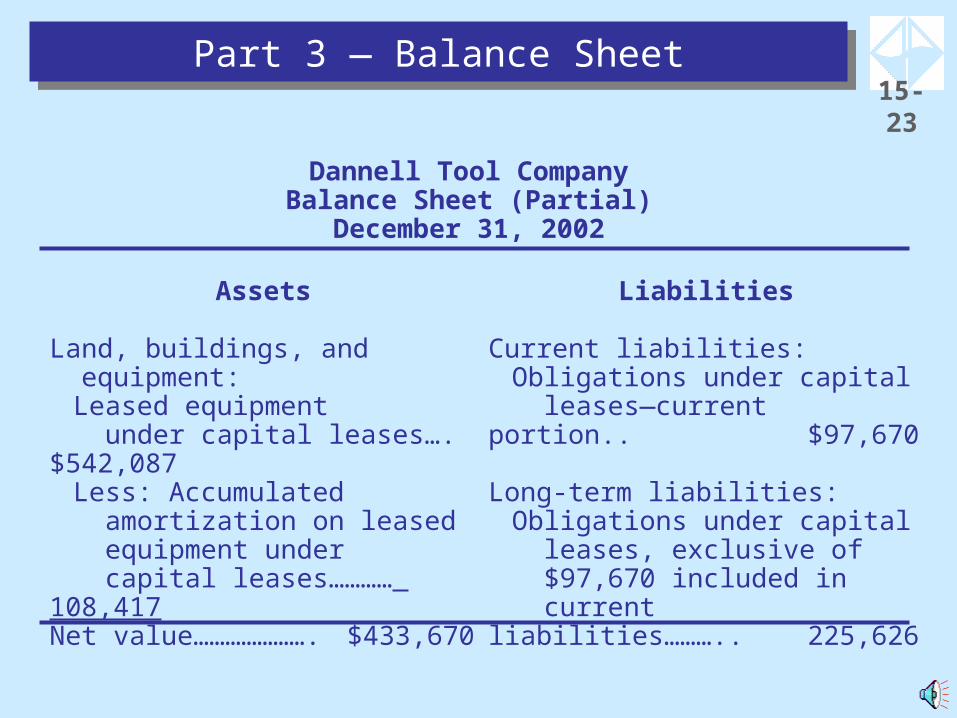

15-23

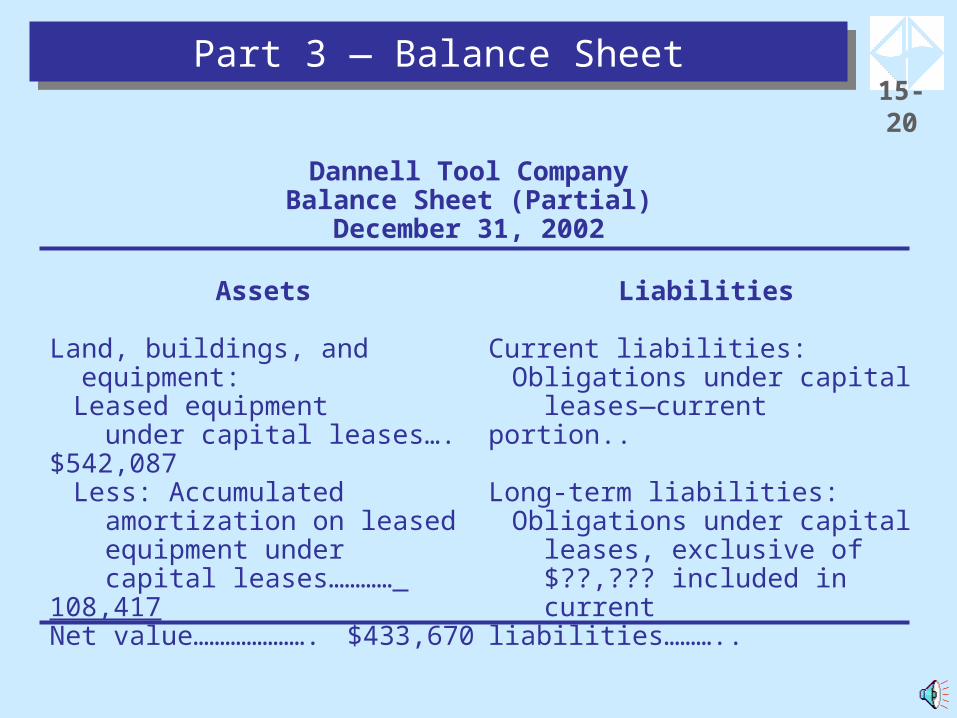

Dannell Tool CompanyBalance Sheet (Partial)

December 31, 2002

Part 3 — Balance SheetPart 3 — Balance Sheet

Assets

Land, buildings, and equipment:

Leased equipment under capital leases…. $542,087Less: Accumulated amortization on leased equipment under capital leases………… 108,417

Net value…………………. $433,670

Liabilities

Current liabilities:Obligations under capital leases—current portion.. $97,670

Long-term liabilities:Obligations under capital leases, exclusive of $97,670 included in current liabilities……….. 225,626

15-24

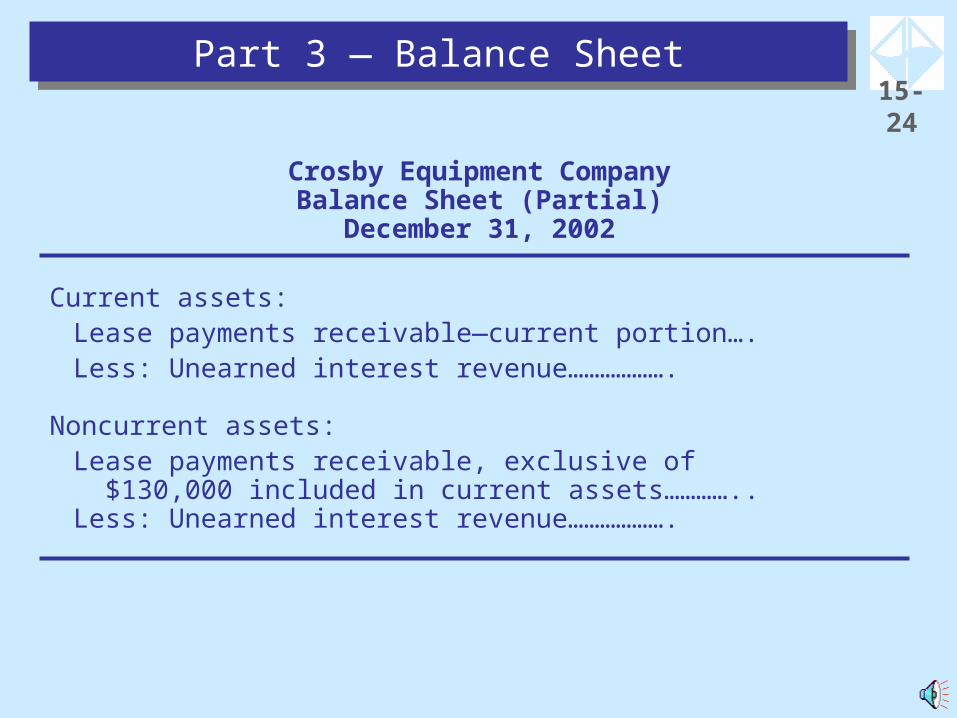

Crosby Equipment CompanyBalance Sheet (Partial)

December 31, 2002

Part 3 — Balance SheetPart 3 — Balance Sheet

Current assets:Lease payments receivable—current portion….Less: Unearned interest revenue……………….

Noncurrent assets:Lease payments receivable, exclusive of $130,000 included in current assets…………..Less: Unearned interest revenue……………….

15-25

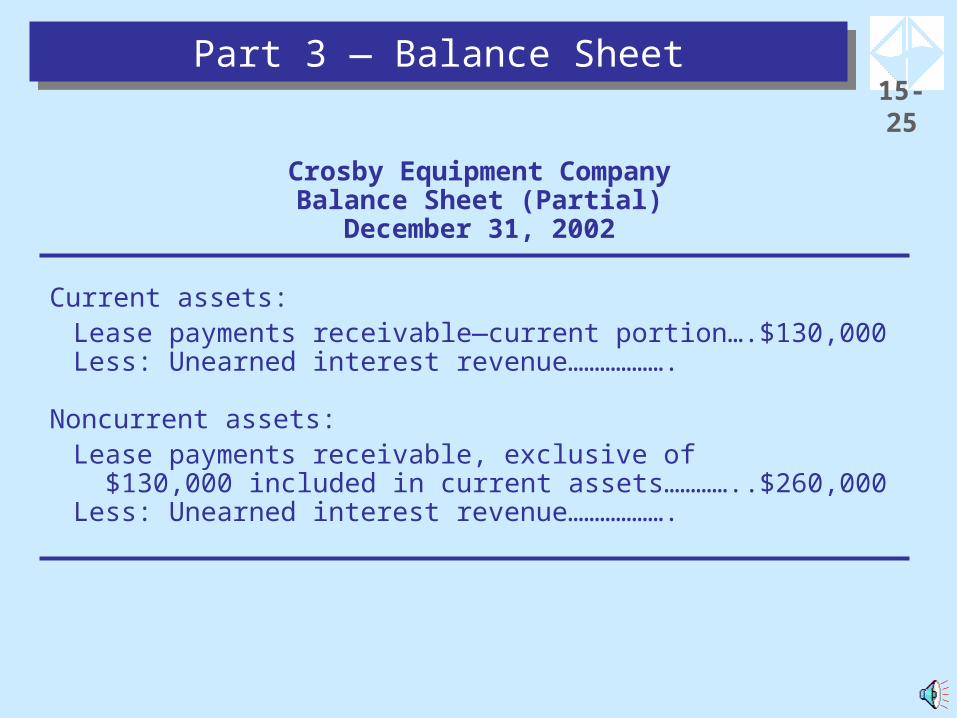

Crosby Equipment CompanyBalance Sheet (Partial)

December 31, 2002

Part 3 — Balance SheetPart 3 — Balance Sheet

Current assets:Lease payments receivable—current portion…. $130,000Less: Unearned interest revenue……………….

Noncurrent assets:Lease payments receivable, exclusive of $130,000 included in current assets………….. $260,000Less: Unearned interest revenue……………….

15-26

Lease Amortization TableLease Amortization Table

Payment Date Amount Interest Principal Balance542,087

1 January 2, 2002 130,000 0 130,000 412,0872 December 31, 2002 130,000 41,209 88,791 323,2963 December 31, 2003 130,000 32,330 97,670 225,6264 December 31, 2004 130,000 22,563 107,437 118,1895 December 31, 2005 130,000 11,811 118,189 0

$650,000 $107,913 $542,087 Totals

15-27

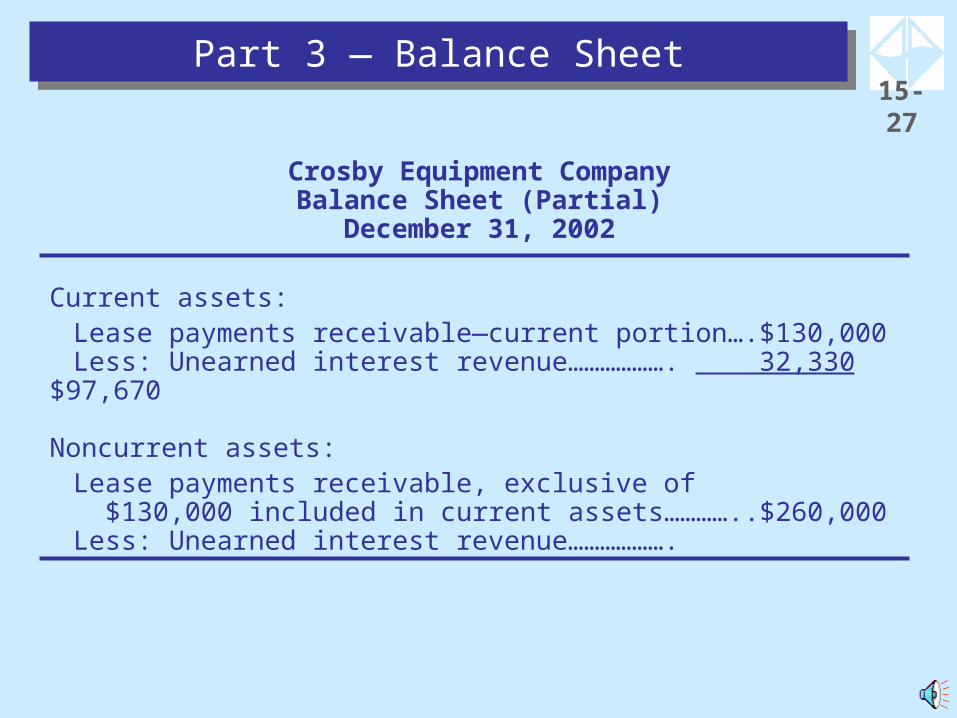

Crosby Equipment CompanyBalance Sheet (Partial)

December 31, 2002

Part 3 — Balance SheetPart 3 — Balance Sheet

Current assets:Lease payments receivable—current portion…. $130,000Less: Unearned interest revenue………………. 32,330 $97,670

Noncurrent assets:Lease payments receivable, exclusive of $130,000 included in current assets………….. $260,000Less: Unearned interest revenue……………….

15-28

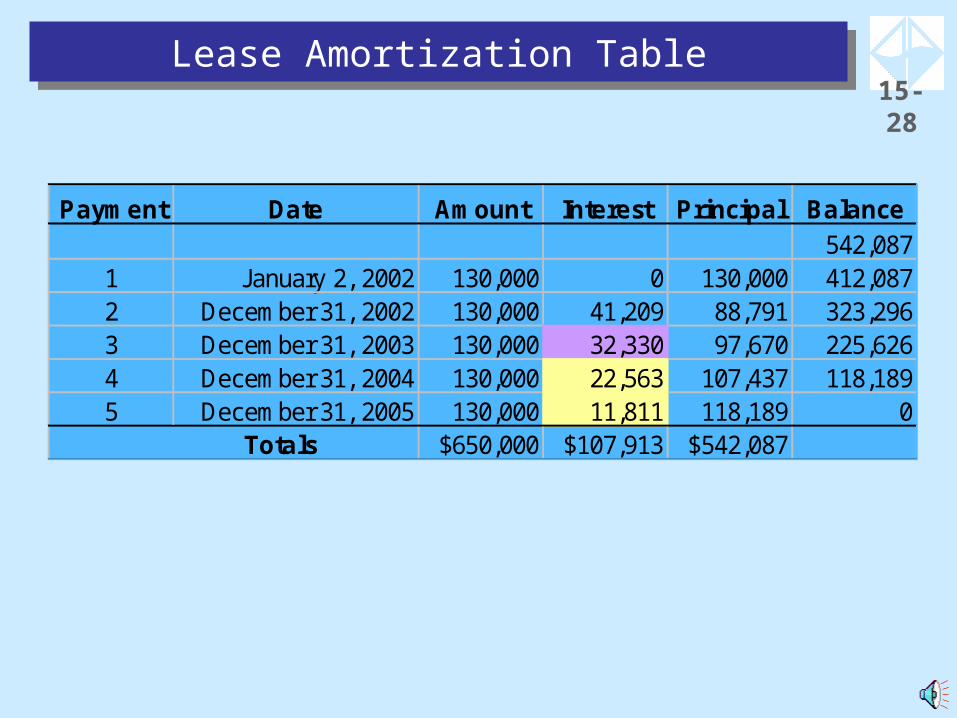

Lease Amortization TableLease Amortization Table

Payment Date Amount Interest Principal Balance542,087

1 January 2, 2002 130,000 0 130,000 412,0872 December 31, 2002 130,000 41,209 88,791 323,2963 December 31, 2003 130,000 32,330 97,670 225,6264 December 31, 2004 130,000 22,563 107,437 118,1895 December 31, 2005 130,000 11,811 118,189 0

$650,000 $107,913 $542,087 Totals

15-29

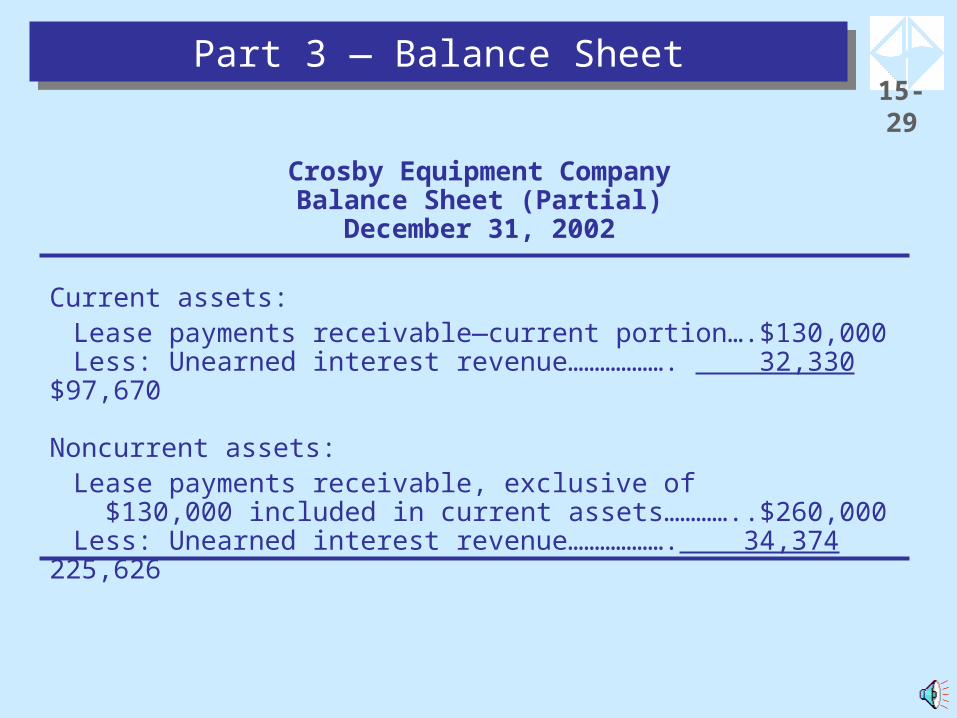

Crosby Equipment CompanyBalance Sheet (Partial)

December 31, 2002

Part 3 — Balance SheetPart 3 — Balance Sheet

Current assets:Lease payments receivable—current portion…. $130,000Less: Unearned interest revenue………………. 32,330 $97,670

Noncurrent assets:Lease payments receivable, exclusive of $130,000 included in current assets………….. $260,000Less: Unearned interest revenue………………. 34,374 225,626

15-30

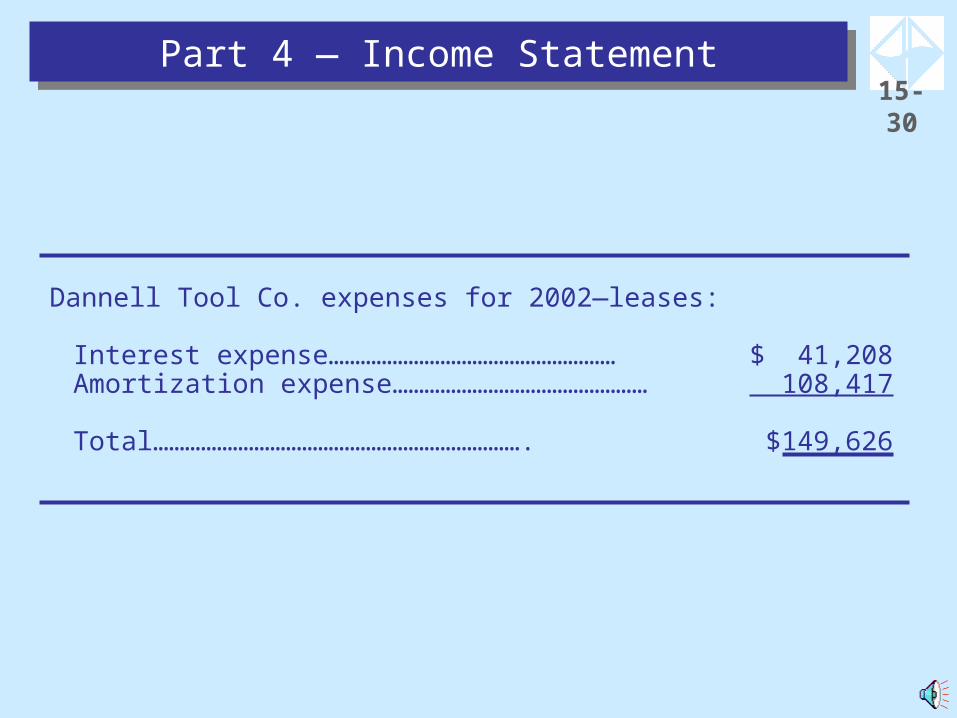

Part 4 — Income StatementPart 4 — Income Statement

Dannell Tool Co. expenses for 2002—leases:

Interest expense……………………………………………… $ 41,208Amortization expense………………………………………… 108,417

Total……………………………………………………………. $149,626

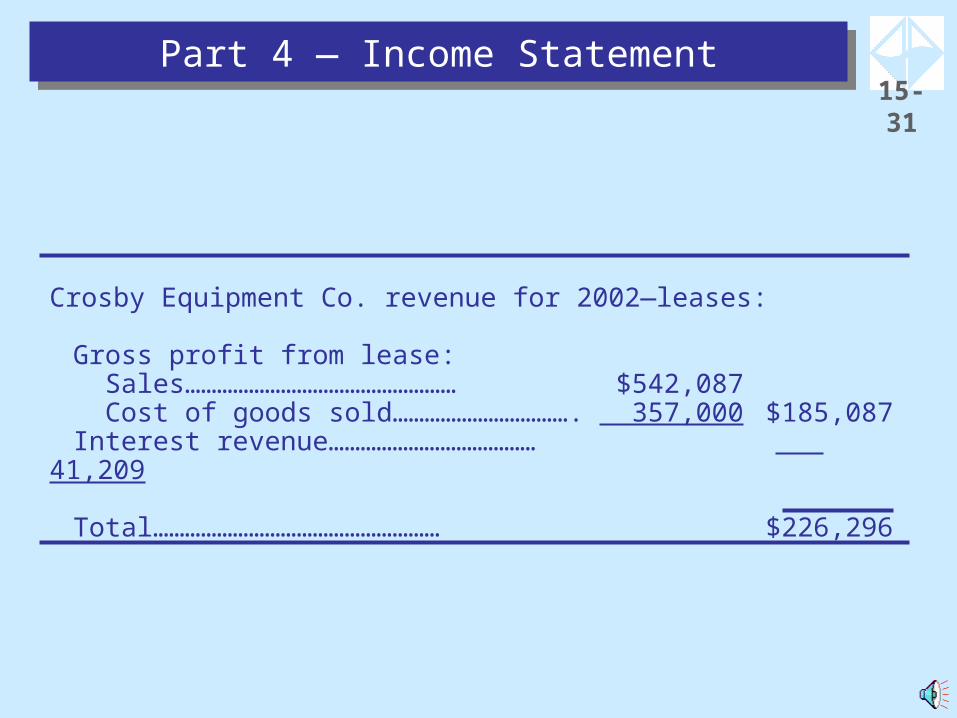

15-31

Crosby Equipment Co. revenue for 2002—leases:

Gross profit from lease: Sales…………………………………………… $542,087 Cost of goods sold……………………………. 357,000 $185,087Interest revenue………………………………… 41,209

Total……………………………………………… $226,296

Part 4 — Income StatementPart 4 — Income Statement

15-32

End of ProblemEnd of Problem

Related Documents