ACCOUNTING AND FINANCIAL STATEMENTS MK UNIT 19 RB, p. 32-36

ACCOUNTING AND FINANCIAL STATEMENTS MK UNIT 19 RB, p. 32-36.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ACCOUNTING AND FINANCIAL

STATEMENTS

MK UNIT 19

RB, p. 32-36

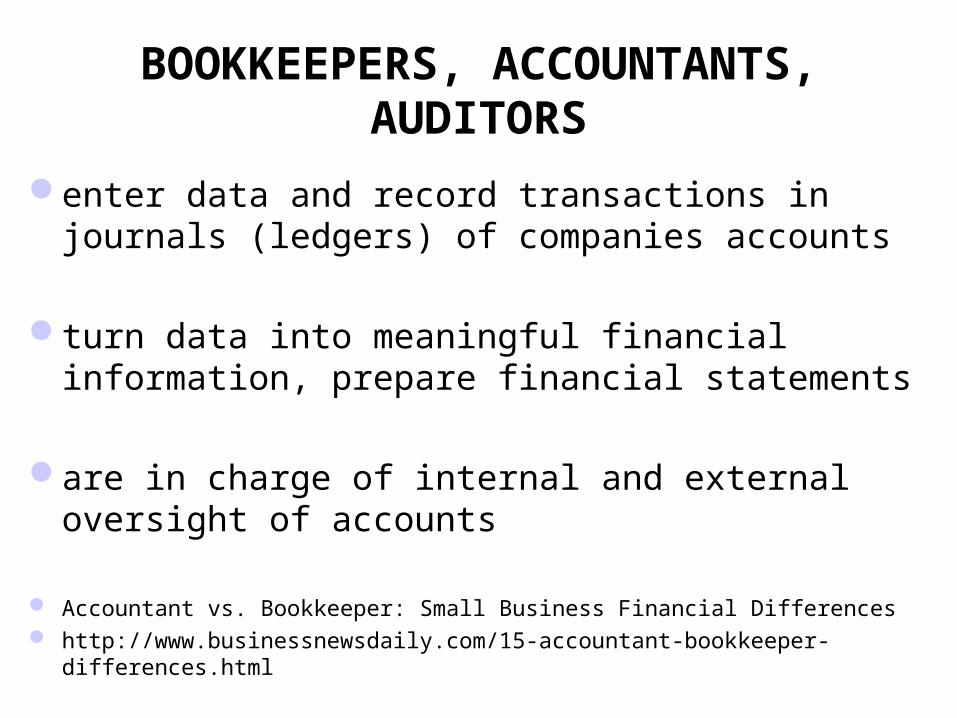

BOOKKEEPERS, ACCOUNTANTS, AUDITORS

enter data and record transactions in journals (ledgers) of companies accounts

turn data into meaningful financial information, prepare financial statements

are in charge of internal and external oversight of accounts

Accountant vs. Bookkeeper: Small Business Financial Differences http://www.businessnewsdaily.com/15-accountant-bookkeeper-differences.html

FINANCIAL TRANSACTIONS

EXPENDITURE

(MAKING PAYMENTS)

…to creditors

…to the government

…to shareholders

…to suppliers

INCOME

(RECEIVING MONEY)

…from debtors

…from customers

…from investors

…from banks

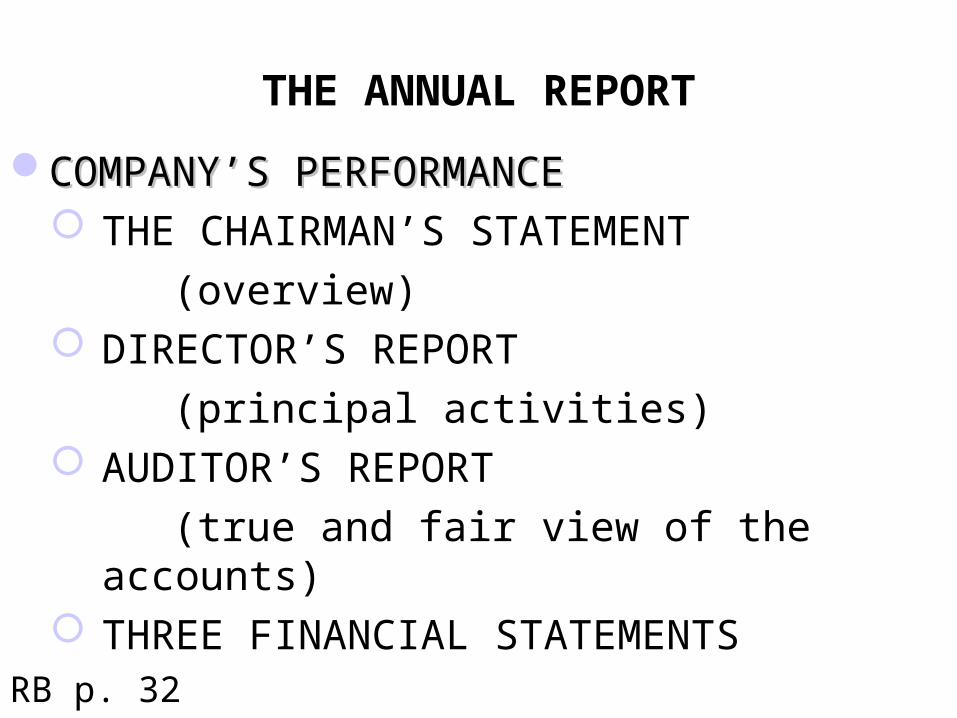

THE ANNUAL REPORT

COMPANY’S PERFORMANCECOMPANY’S PERFORMANCE THE CHAIRMAN’S STATEMENT

(overview) DIRECTOR’S REPORT

(principal activities) AUDITOR’S REPORT

(true and fair view of the accounts) THREE FINANCIAL STATEMENTS

RB p. 32

THREE FINANCIAL STATEMENTS

PROFIT & LOSS ACCOUNT

profitabilityBALANCE SHEET

financial position of a firm at a particular time

CASH FLOW STATEMENT

liquidity

THREE FINANCIAL STATEMENTS

PROFIT & LOSS ACCOUNT

revenue/turnover - costs /overheadsBALANCE SHEET

assets=liabilities+owners’ equityCASH FLOW STATEMENT

sources of funds v. applications of funds

(cash inflow v. cash outflow)

?

This document provides aggregate data regarding all cash inflows a company receives from both its ongoing operations and external investment sources, as well as all cash outflows that pay for business activities and investments during a given quarter.

Source: Investopedia

?

A financial statement that summarizes a company's assets, liabilities and shareholders' equity at a specific point in time.

These three segments give investors an idea as to what the company owns and owes, as well as the amount invested by the shareholders.

It must follow the following formula:Assets = Liabilities + Shareholders' Equityhttp://www.investopedia.com/video/play/introduction-balance-sheet/

?

A financial statement that summarizes the revenues, costs and expenses incurred during a specific period of time - usually a fiscal quarter or year.

These records provide information that shows the ability of a company to generate profit by increasing revenue and reducing costs.

It is also known as an "income statement".

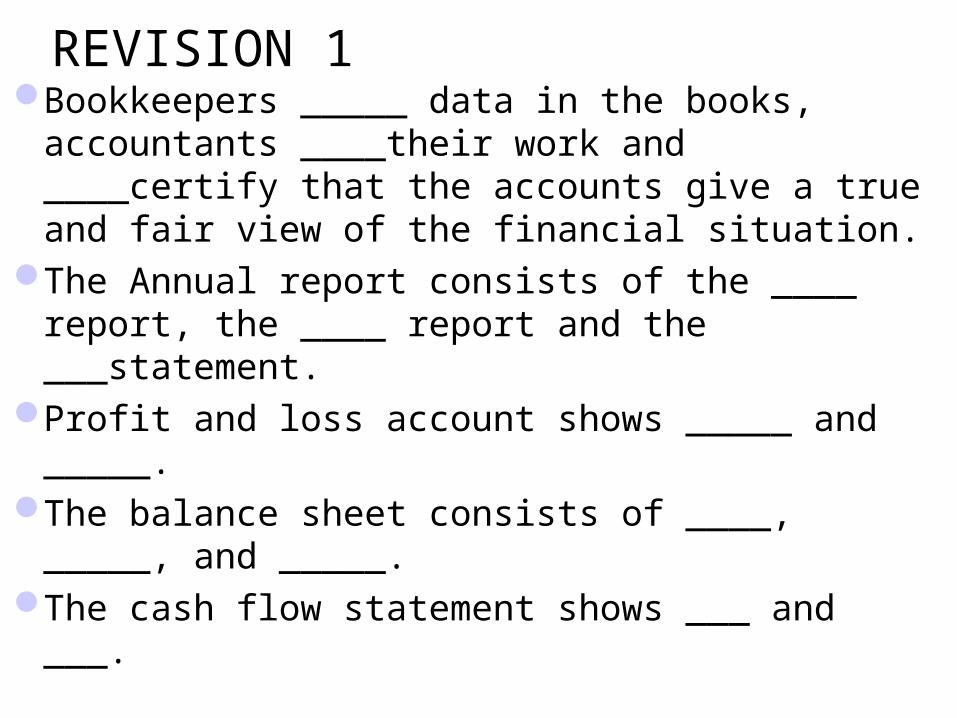

REVISION 1Bookkeepers _____ data in the books,

accountants ____their work and ____certify that the accounts give a true and fair view of the financial situation.

The Annual report consists of the ____ report, the ____ report and the ___statement.

Profit and loss account shows _____ and _____.

The balance sheet consists of ____, _____, and _____.

The cash flow statement shows ___ and ___.

P&L: From top line to bottom line

Revenues TOP LINE- Cost of sales= GROSS PROFIT - Operating expenses= EBITDA– Depreciation and amortization

= EBIT

-Interest- Taxes = NET PROFIT BOTTOM LINE P. 33

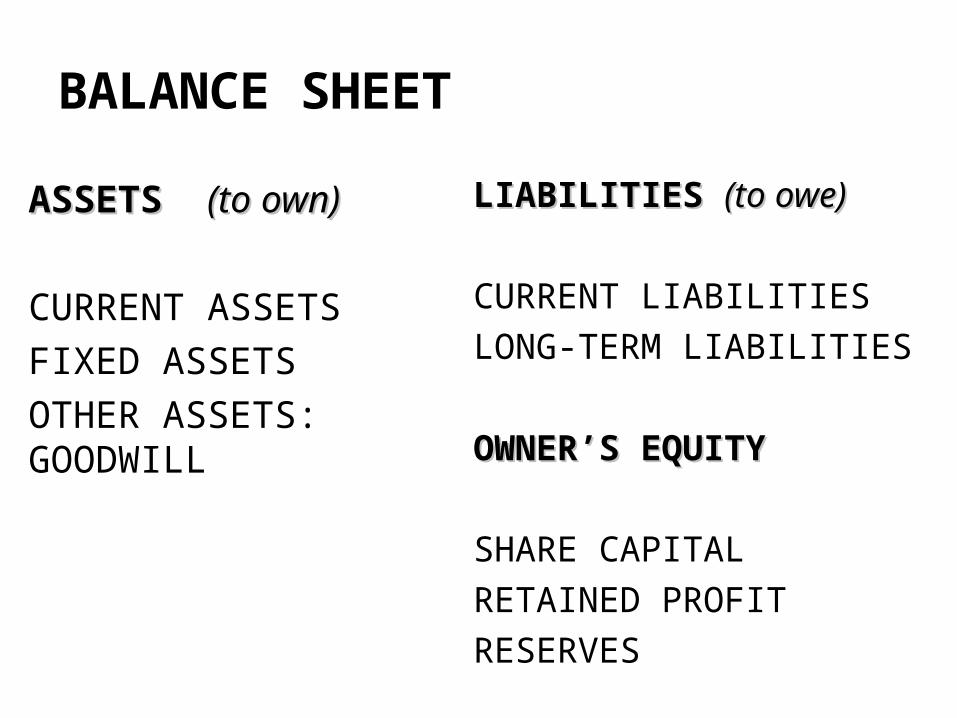

BALANCE SHEET

ASSETS ASSETS (to own)(to own)

CURRENT ASSETS

FIXED ASSETS

OTHER ASSETS: GOODWILL

LIABILITIES LIABILITIES (to owe)(to owe)

CURRENT LIABILITIES

LONG-TERM LIABILITIES

OWNER’S EQUITYOWNER’S EQUITY

SHARE CAPITAL

RETAINED PROFIT

RESERVES

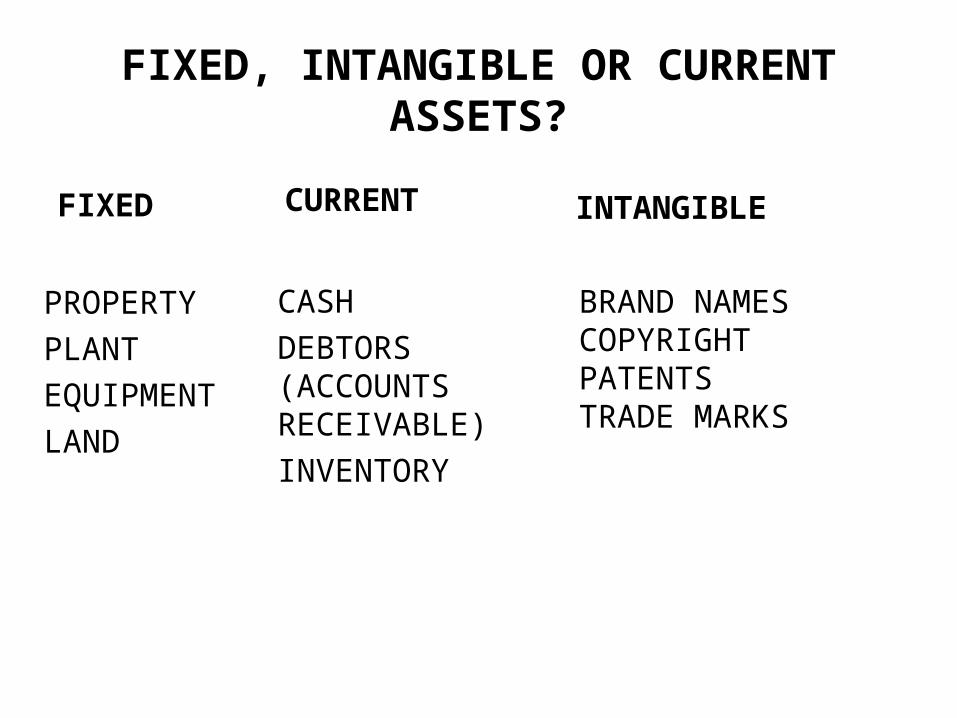

FIXED, INTANGIBLE OR CURRENT ASSETS?

FIXED

PROPERTY

PLANT

EQUIPMENT

LAND

CURRENT

CASH

DEBTORS (ACCOUNTS RECEIVABLE)

INVENTORY

INTANGIBLE

BRAND NAMESCOPYRIGHTPATENTSTRADE MARKS

LIABILITIES

CURRENT

ACCOUNTS PAYABLEACCRUED EXPENSES

ACCRUED:

recognized in the books before it is paid for

LONG TERM

DEFERRED INCOME TAX

LONG-TERM DEBT (MORTGAGE, BONDS)

P. 34

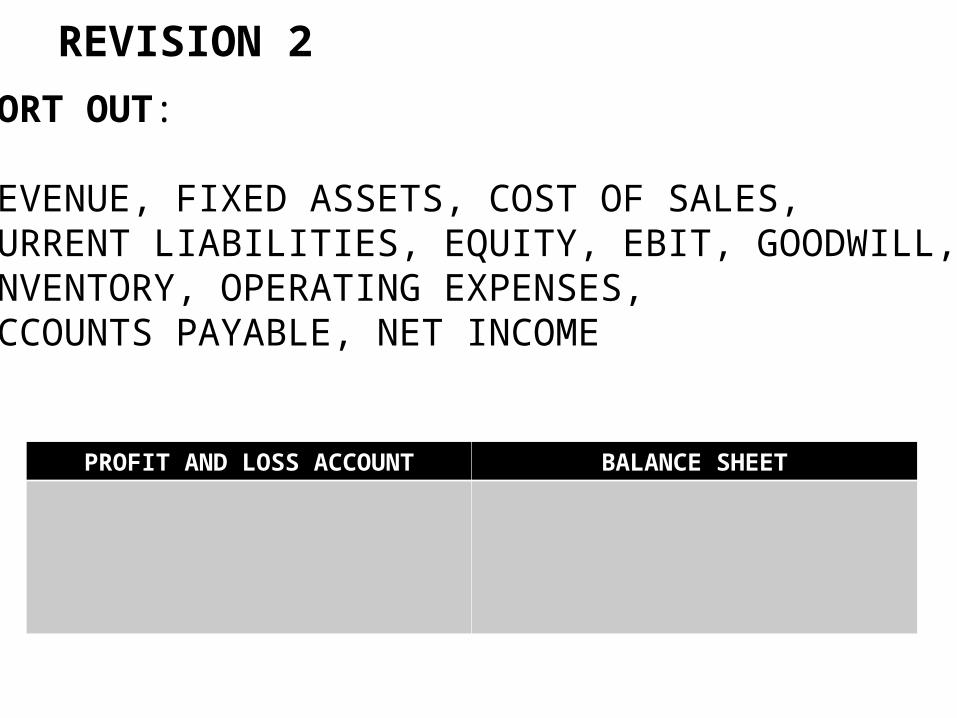

REVISION 2

PROFIT AND LOSS ACCOUNT BALANCE SHEET

SORT OUT:

REVENUE, FIXED ASSETS, COST OF SALES, CURRENT LIABILITIES, EQUITY, EBIT, GOODWILL,INVENTORY, OPERATING EXPENSES, ACCOUNTS PAYABLE, NET INCOME

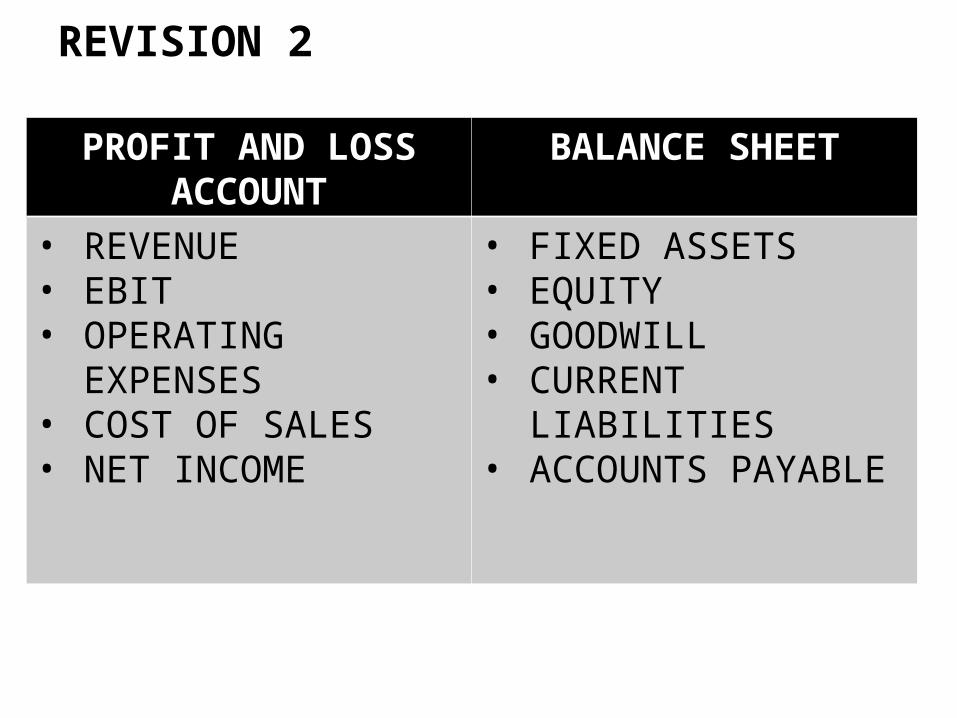

REVISION 2

PROFIT AND LOSS ACCOUNT

BALANCE SHEET

• REVENUE• EBIT• OPERATING

EXPENSES• COST OF SALES• NET INCOME

• FIXED ASSETS• EQUITY• GOODWILL• CURRENT

LIABILITIES• ACCOUNTS

PAYABLE

CASH FLOW STATEMENT

money coming into the business

(inflows)

money going out of the business

(outflows)

relating to

OPERATING/INVESTMENT/FINANCING ACTIVITIES

sale of goods, dividends, taxes, issuing shares etc.p. 35

REVISION 3

MK, p. 95

Vocabulary 1, 2, 3, 4MK, p. 97

definitions

http://www.investopedia.com/video/play/goodwill/

http://www.investopedia.com/video/play/operatingincome/

AktivaPasivaPrihod od prodajeTroškovi prodajeDugotrajna imovinaKratkoročne obvezeDospjeli, ali neplaćeni

troškoviZalihePotraživanjaAmortizacijaMaterijalna imovina

Related Documents