ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016 REAL ESTATE SERVICES

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ABU DHABI REAL ESTATE MARKET OVERVIEW

Q2 2016

REAL ESTATE SERVICES

REPORT HIGHLIGHTS Residential

�� A decline in tenant demand (enquiries down by over 25%) has started to translate into downward pressure on rents across the market with average rents showing a decline of around 3% this quarter, with anticipation that this trend will continue in the second half of the year, particularly as the scheduled new supply enters the market

�� Low transaction volumes and cautious investor sentiment prevail. Average sale prices in the secondary market have fallen by 2% and properties are now generally trading 5% below where they were 12 months ago. Off-plan sale prices are being held firm by developers

Office�� Continuing weak demand from the government

sector has resulted in another quarter of low leasing activity. Prevailing low demand over the last year has to date been balanced by equally low levels of new supply, however in the last quarter an increase in downsizing to reduce premises costs has become more prevalent in both the private and government sectors with vacancy levels rising. This has led to more noticeable rental declines over the last 3 months

�� Average Grade A rents for fitted space decreased by 6% now standing at AED 1,850 per sqm. Average Grade B rents decreased by 10% to reach AED 1,150 per sqm.

Retail Sector

�� The impact of government austerity measures are affecting the retail market which is currently experiencing a decline in retail spending putting pressure on retailer’s trading performance

�� Mall rents remained stable across A class locations, however pressure on rental rates is evident at lease renewals which could see rental growth slowing in the coming years. Mall operators are offering additional incentives in the form of extended rent free periods both on new lettings and also at lease renewal for key anchor tenants

Hospitality Sector�� Three new hotel properties opened this quarter

comprising the Four Seasons Hotel and Four Seasons Hotel Apartments at Al Maryah Island and the Gloria Downtown Hotel at Hamdan Street

�� H2 2016 is scheduled to witness the addition of 9 properties which together will add 2,410 keys, representing an 8.6% increase to the current stock level. Key additions include the Hilton Al Forsan, Grand Hyatt Emirates Pearl, and the Millennium Bab Al Qasr Hotel

�� Trading performance in the hospitality sector has been impacted by the prevailing economic conditions which have weighed on consumer and corporate spending, with the Average Daily Room Rates and RevPAR both down in Q2 by approximately 15% in comparison with 2015 levels

One of the aims of this report is to improve market transparency by basing our analysis wherever possible on primary transactional evidence derived from our own managed portfolio and from the analysis of our sales and home financing activities. We believe that this adds credibility to the analysis and we hope provides confidence in its reliability.

FOREWORD ADIB Real Estate Services comprises a comprehensive real estate banking and advisory platform providing the full range of professional services from a single provider. Our services include:-

�� Real estate financing�� Strategic development advisory�� Investment advisory�� Asset management�� Project management

�� Valuation�� Agency�� Market research�� Property management�� Facilities management

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016

2

MPM PROPERTIES FACTS AND FIGURES

136bn 9,500+

CONTENTSProject in Focus 14

Office Sector 16

Retail Sector 20

Hospitality Sector 22

Definitions & Methodology 24

Contact Information 25

Supply - Photo Gallery 26

Development Location Map 28

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016

3

DEMAND DRIVERS – Q2 2016

GOVERNMENT INITIATIVES �� Moody’s Investors Service has confirmed

Abu Dhabi’s long-term issuer ratings at Aa2. Moody’s expects Abu Dhabi government’s sizeable fiscal buffers, in the form of diversified offshore investments, to help manage challenges from any economic slowdown and allow it time to adjust its fiscal policy to lower oil prices

�� Investors subscribed over $17 billion (AED 62.4 billion) for Abu Dhabi’s $5 billion bond issue exhibiting investor confidence in the Emirate. This is the first bond issue by the Emirate in seven years and is partly expected to help with a projected budget deficit of AED 36.9 billion in 2016

�� The UPC wishes to encourage property developers to restart construction work on unfinished towers that were stalled due to the global financial crisis. The recommendation is being finalized and will be presented to the government during the next step

KEY EVENTS�� Isra’a Wal Mi’raj holiday, 5th May 2016

�� Abu Dhabi Classics, 7th May – 10th May 2016

�� Portrait of a Nation, 11th April – 10th May 2016

�� Abu Dhabi International Book Fair, 27th April – 3rd May 2016

�� International Market & Consumer Fair, 20th April – 6th May 2016

�� Airline Engineering & Maintenance: Middle East conference, 26th April – 27th April, 2016

�� Andrea Bocelli Live, 22nd April 2016

�� Abu Dhabi International Jewelry and Watch Show, 3rd May – 7th May 2016

�� Start of Ramadan, 6th June 2016

FREEZONES �� Abu Dhabi Financial Group (ADFG) and Bahrain’s GFH

Financial Group have received preliminary approval to jointly set up an Islamic bank with an initial capital of US$100 million at Abu Dhabi Global Market (ADGM)

4

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016 | DEMAND DRIVERS

TOURISM INITIATIVES�� Sheikh Zayed Grand Mosque has been ranked the world’s second

favourite landmark by TripAdvisor. The Abu Dhabi landmark beat iconic wonders such as the Taj Mahal and the Eiffel Tower being outranked only by the ancient Incan site of Machu Picchu in Peru

�� Ferrari World Abu Dhabi is soon looking to launch its third phase. After the recently completed second phased added seven new rides and 20% more capacity, this planned third phase is envisaged to add an additional capacity of 40% and eight new rides

�� A UAE-Thai joint committee meeting was held to improve investment opportunities between the two countries and encourage growth of tourism. Approximately 30,000 Thai tourists visited the UAE last year as the number of flights between the two countries has increased to 98 flights per week

�� Saudi-based national airline, Flynas, will add a second daily service between Riyadh and Abu Dhabi from June, increasing its combined offer with Etihad Airways to four daily services. Also, Flynas will enter the Jeddah - Abu Dhabi market, with a daily flight which will complement Etihad Airways ‘ existing thrice daily services

�� The TCA Abu Dhabi has formally notified hotels and tourist facilities that the proposed municipal fees on hotels in Abu Dhabi will be collected from 1st June 2016 onwards.

�� The Louvre Abu Dhabi is currently more than 95 per cent complete and progressing on schedule for handover to TCA by July or August 2016. The opening is expected in December 2016 or January 2017

REAL ESTATE AND CONSTRUCTION�� Aldar Properties has sold out the first phase of Yas Acres, which was

unveiled during the lead up to Cityscape Abu Dhabi, and generated over AED 1 billion from the sales. A proposed second phase will comprise 125 homes with a starting price of AED 2.9 million

�� Following the success of its Meera Shams scheme launched in June 2015, Aldar Properties plans to add mid-income housing to its developments at Shams Abu Dhabi and Al Raha Beach

�� Aldar Properties has sold 384 out of the 512 off-plan flats in the first phase of its Mayan development on Yas Island in the first six months of launch. This includes bulk deals for two of the five buildings which make up the first phase

�� Bloom Properties unveiled ‘Faya’, the fourth phase of its Bloom Gardens project at Cityscape Abu Dhabi. The project contains 132 town houses made up of 28 four-unit and four five-unit clusters. The company has targeted UAE nationals looking to bulk buy and has reportedly sold over 90% of the units offered

�� Bloom Holding plans to launch an affordable housing project comprising 5,000 homes close to Abu Dhabi International Airport.

The 2.2 million square feet plot will be developed into flats, villas and town houses. The project is under master planning and subject to statutory approvals, is scheduled to be launched next year with delivery of units anticipated from 2019 onwards

�� The UPC has approved detailed master plans for a 637,000 square metres phase 2 of Masdar City, which will include a research and development cluster, 2,000 apartments and a Gems school as well as another 341,000 sq metres phase, which will include 1,000 homes

�� Al Forsan, the Abu Dhabi-based sports resort and housing complex, had announced a “rent-to-buy” offer for Emiratis at Cityscape Abu Dhabi on 50 of the 385 villas and town houses it has completed in Khalifa City A

�� The first phase of Saadiyat Lagoons, the largest district on Abu Dhabi’s Saadiyat Island, has been launched by TDIC at Cityscape Abu Dhabi. The premium development with 4,000 residential units is expected to house 29,000 residents upon completion

5

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016 | DEMAND DRIVERS

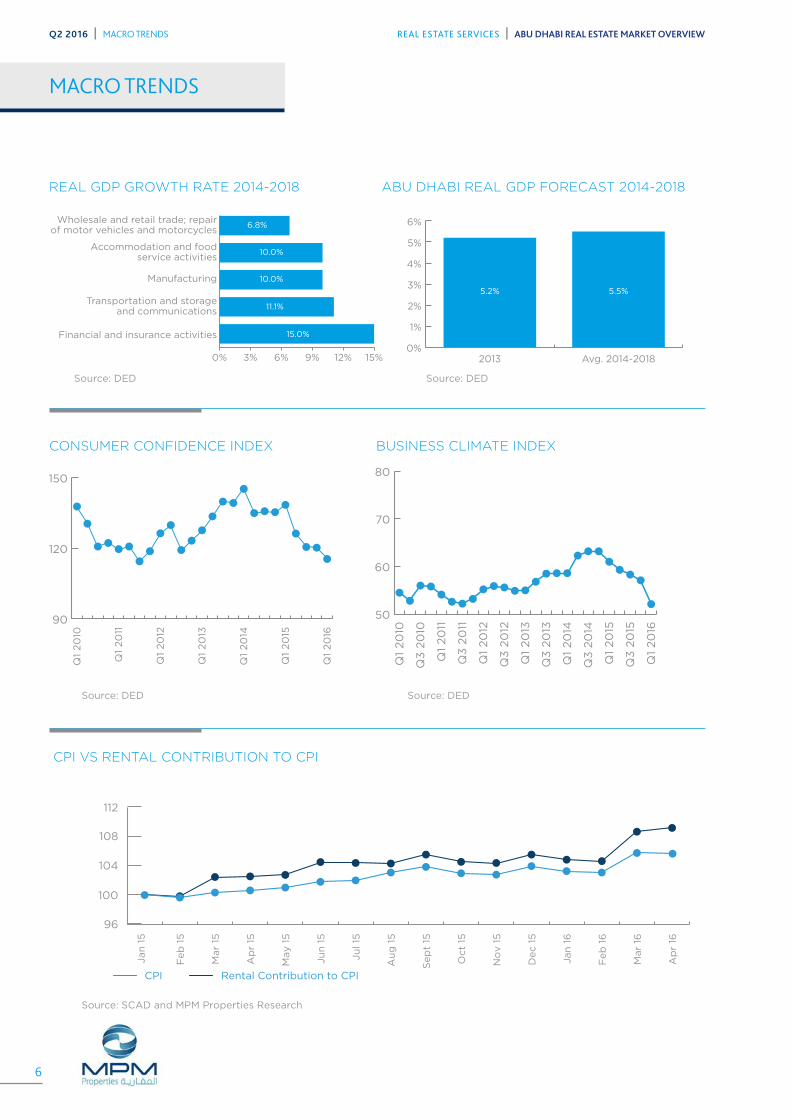

ABU DHABI REAL GDP FORECAST 2014-2018

Source: DED

0%

1%

2%

3%

4%

5%

6%

2013 Avg. 2014-2018

5.2% 5.5%

MACRO TRENDS

REAL GDP GROWTH RATE 2014-2018

Source: DED

0% 3% 6% 9% 12% 15%

Wholesale and retail trade; repairof motor vehicles and motorcycles

Accommodation and foodservice activities

Manufacturing

Transportation and storageand communications

Financial and insurance activities

6.8%

10.0%

10.0%

11.1%

15.0%

Source: DEDSource: DED

REAL GDP GROWTH RATE 2014-2018 ABU DHABI REAL GDP FORECAST 2014-2018

50

60

70

80

Q1

20

16

Q3

20

15

Q1

20

15

Q3

20

14

Q1

20

14

Q3

20

13

Q1

20

13

Q3

20

12

Q1

20

12

Q3

20

11

Q1

20

11

Q3

20

10

Q1

20

10

90

120

150

Q1

20

16

Q1

20

15

Q1

20

14

Q1

20

13

Q1

20

12

Q1

20

11

Q1

20

10

CONSUMER CONFIDENCE INDEX

Source: DED

Source: SCAD and MPM Properties Research

Source: DED

BUSINESS CLIMATE INDEX

CPI VS RENTAL CONTRIBUTION TO CPI

Feb

16

Mar

16

Ap

r 16

CPI Rental Contribution to CPI

Jan

15

Feb

15

Mar

15

Ap

r 15

Oct

15

No

v 1

5

Dec 1

5

May 1

5

Ju

n 1

5

Ju

l 15

Au

g 1

5

Sep

t 15

Jan

16

96

100

104

108

112

6

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016 | MACRO TRENDS

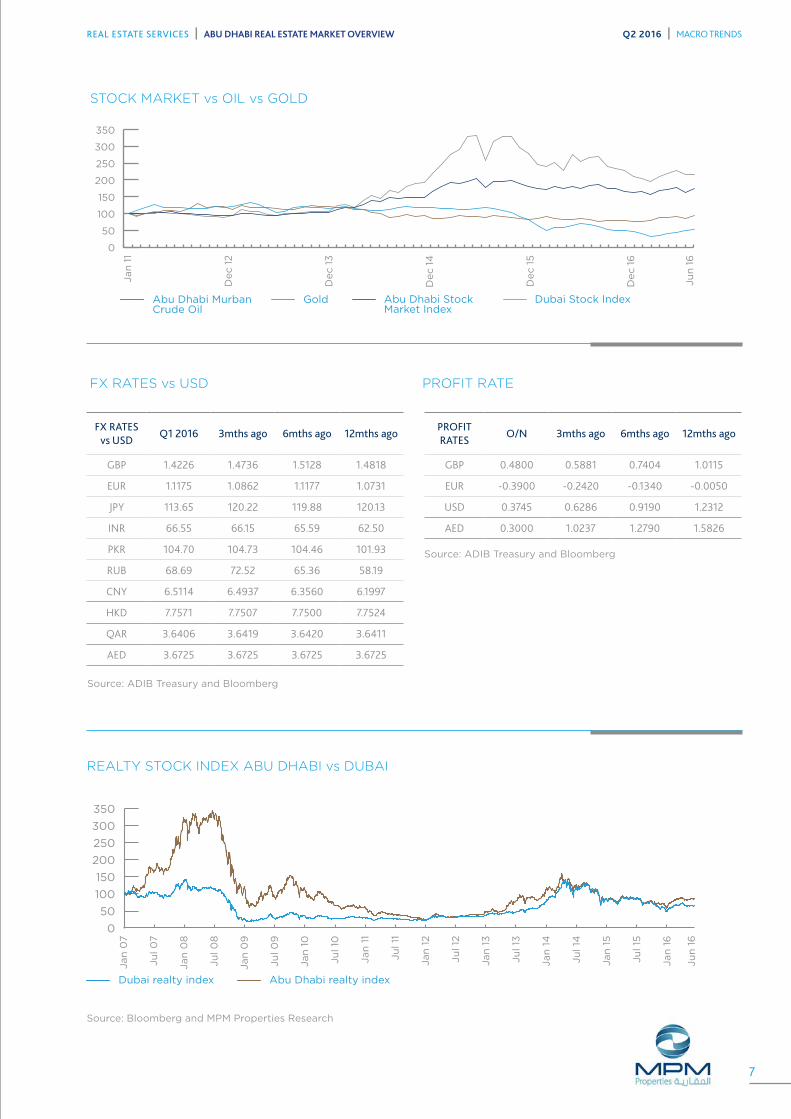

Dubai realty index Abu Dhabi realty index

Ju

l 0

7

Jan

07

Ju

l 0

8

Jan

08

Ju

l 0

9

Jan

09

Ju

l 10

Jan

10

Ju

l 11

Jan

11

Ju

l 12

Jan

12

Ju

l 13

Jan

13

Ju

l 14

Jan

14

Ju

l 15

Jan

15

Ju

n 1

6

Jan

16

0

50

100

150

200

250

300

350

Abu Dhabi MurbanCrude Oil

Gold Abu Dhabi Stock Market Index

Dubai Stock Index

Ju

n 1

6

Dec 1

6

Dec 1

5

Dec 1

4

Dec 1

3

Dec 1

2

Jan

11

0

50

100

150

200

250

300

350

Source: Bloomberg and MPM Properties Research

Source: ADIB Treasury and Bloomberg

Source: ADIB Treasury and Bloomberg

FX RATES vs USD

REALTY STOCK INDEX ABU DHABI vs DUBAI

PROFIT RATE

STOCK MARKET vs OIL vs GOLD

FX RATES vs USD

Q1 2016 3mths ago 6mths ago 12mths ago

GBP 1.4226 1.4736 1.5128 1.4818

EUR 1.1175 1.0862 1.1177 1.0731

JPY 113.65 120.22 119.88 120.13

INR 66.55 66.15 65.59 62.50

PKR 104.70 104.73 104.46 101.93

RUB 68.69 72.52 65.36 58.19

CNY 6.5114 6.4937 6.3560 6.1997

HKD 7.7571 7.7507 7.7500 7.7524

QAR 3.6406 3.6419 3.6420 3.6411

AED 3.6725 3.6725 3.6725 3.6725

PROFIT RATES

O/N 3mths ago 6mths ago 12mths ago

GBP 0.4800 0.5881 0.7404 1.0115

EUR -0.3900 -0.2420 -0.1340 -0.0050

USD 0.3745 0.6286 0.9190 1.2312

AED 0.3000 1.0237 1.2790 1.5826

7

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016 | MACRO TRENDS

MARKET OVERVIEW Q2 2016

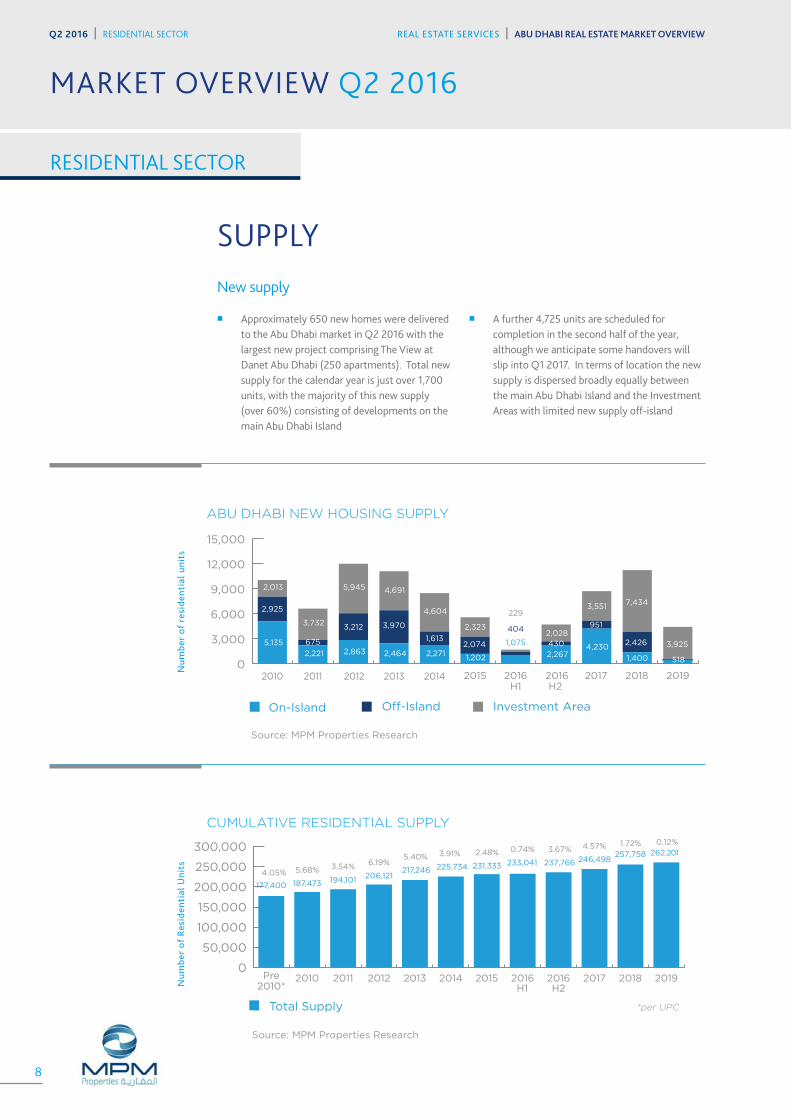

SUPPLY New supply

�� Approximately 650 new homes were delivered to the Abu Dhabi market in Q2 2016 with the largest new project comprising The View at Danet Abu Dhabi (250 apartments). Total new supply for the calendar year is just over 1,700 units, with the majority of this new supply (over 60%) consisting of developments on the main Abu Dhabi Island

�� A further 4,725 units are scheduled for completion in the second half of the year, although we anticipate some handovers will slip into Q1 2017. In terms of location the new supply is dispersed broadly equally between the main Abu Dhabi Island and the Investment Areas with limited new supply off-island

0

3,000

6,000

9,000

12,000

15,000

Investment AreaOn-Island Off-Island

20112010 2012 2013 2014 2015 2016H1

2016H2

2017 2018 2019

5,135

2,925

2,013

2,221

675

3,732

2,863

3,212

5,945

2,464

3,970

4,691

2,271

1,613

4,604

1,202

2,074

2,323

1,075

404

229

2,267

4302,028

1,400

2,426

7,434

4,230

951

3,551

518

3,925

Num

ber

of r

esid

enti

al u

nits

Pre2010*

2010 2011 2012 2013 2014 2015 2016H1

2017 2018 20192016H2

Total Supply *per UPC

0

50,000

100,000

150,000

200,000

250,000

300,000

177,400

5.68%4.05%187,473

3.54%

194,101

6.19%

206,121

5.40%

217,246

3.91%

225,734

2.48%

231,333

0.74%

233,041

3.67%

237,766

4.57% 1.72% 0.12%

246,498257,758 262,201

Num

ber

of R

esid

enti

al U

nits

RESIDENTIAL SECTOR

Source: MPM Properties Research

Source: MPM Properties Research

ABU DHABI NEW HOUSING SUPPLY

CUMULATIVE RESIDENTIAL SUPPLY

8

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016 | RESIDENTIAL SECTOR

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016 | RESIDENTIAL SECTOR

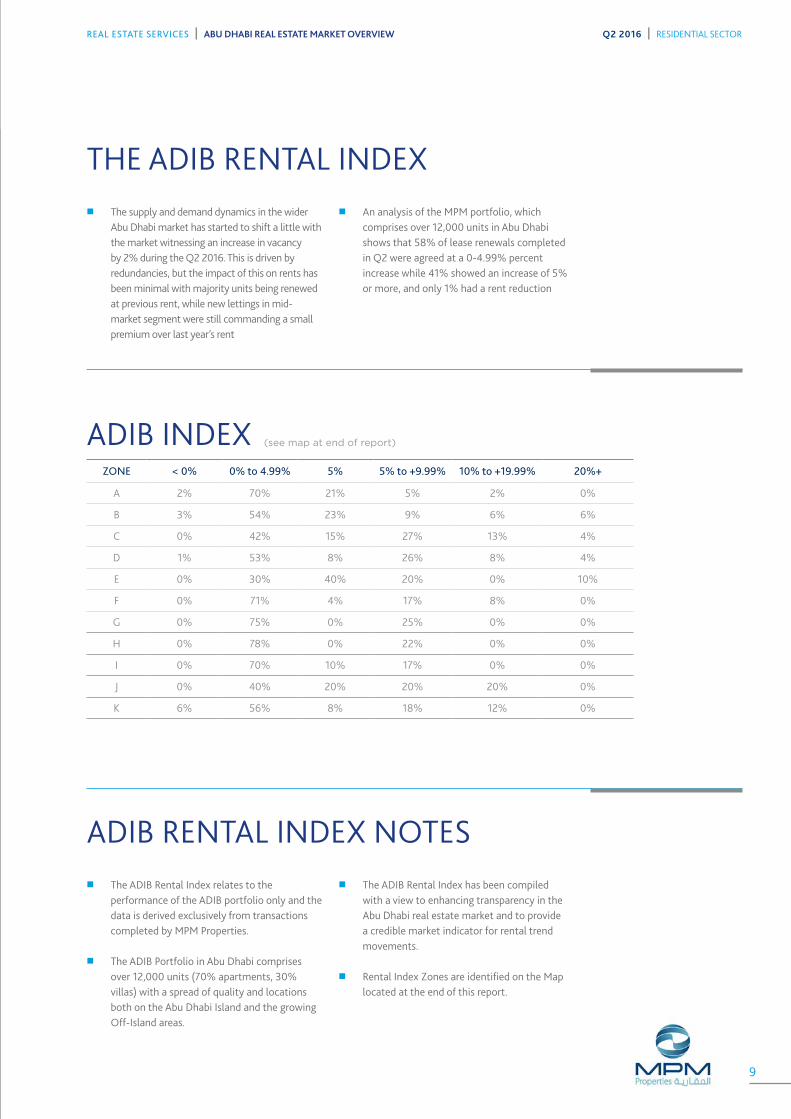

THE ADIB RENTAL INDEX �� The supply and demand dynamics in the wider

Abu Dhabi market has started to shift a little with the market witnessing an increase in vacancy by 2% during the Q2 2016. This is driven by redundancies, but the impact of this on rents has been minimal with majority units being renewed at previous rent, while new lettings in mid-market segment were still commanding a small premium over last year’s rent

�� An analysis of the MPM portfolio, which comprises over 12,000 units in Abu Dhabi shows that 58% of lease renewals completed in Q2 were agreed at a 0-4.99% percent increase while 41% showed an increase of 5% or more, and only 1% had a rent reduction

ADIB RENTAL INDEX NOTES �� The ADIB Rental Index relates to the

performance of the ADIB portfolio only and the data is derived exclusively from transactions completed by MPM Properties.

�� The ADIB Portfolio in Abu Dhabi comprises over 12,000 units (70% apartments, 30% villas) with a spread of quality and locations both on the Abu Dhabi Island and the growing Off-Island areas.

�� The ADIB Rental Index has been compiled with a view to enhancing transparency in the Abu Dhabi real estate market and to provide a credible market indicator for rental trend movements.

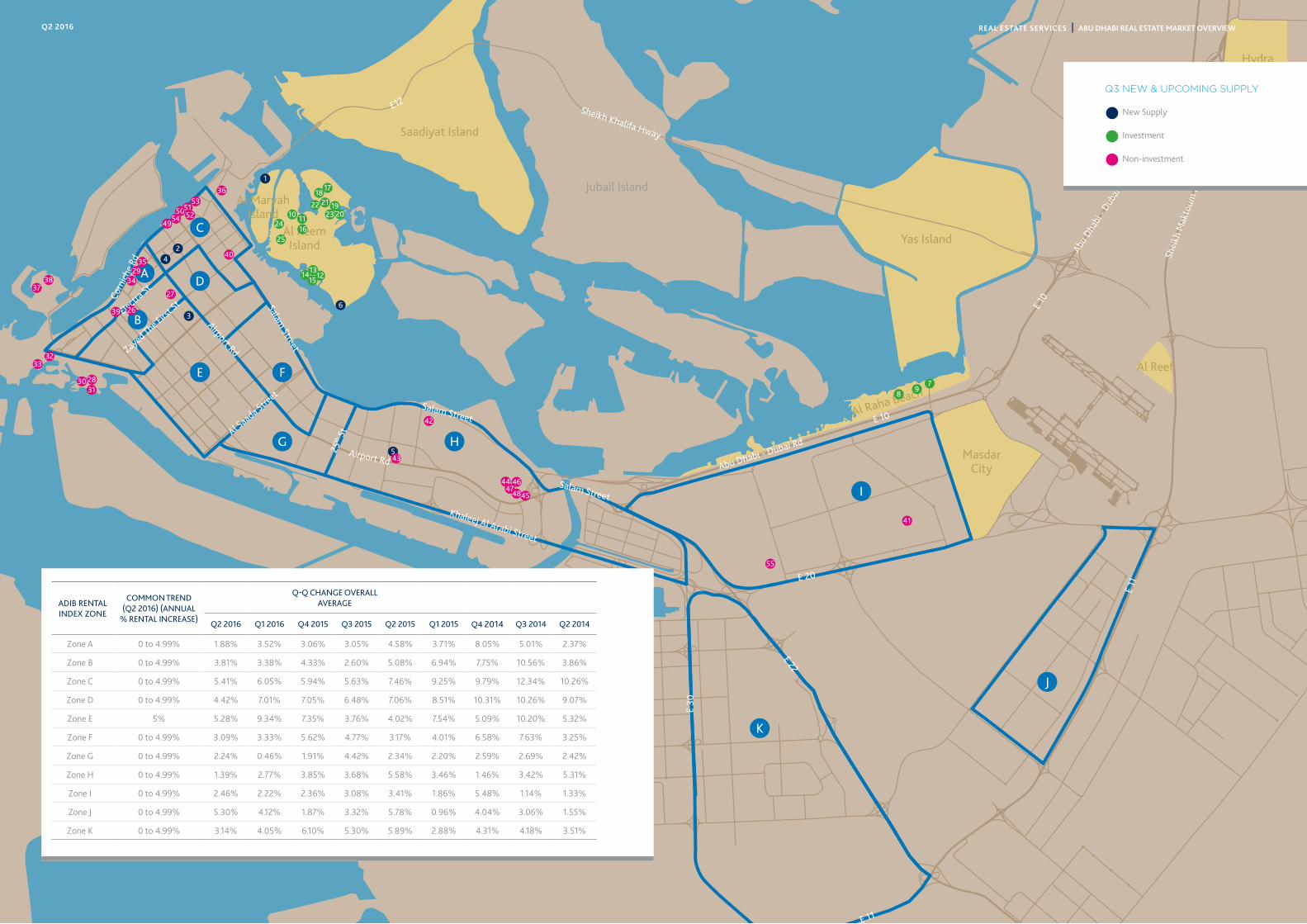

�� Rental Index Zones are identified on the Map located at the end of this report.

ZONE < 0% 0% to 4.99% 5% 5% to +9.99% 10% to +19.99% 20%+

A 2% 70% 21% 5% 2% 0%

B 3% 54% 23% 9% 6% 6%

C 0% 42% 15% 27% 13% 4%

D 1% 53% 8% 26% 8% 4%

E 0% 30% 40% 20% 0% 10%

F 0% 71% 4% 17% 8% 0%

G 0% 75% 0% 25% 0% 0%

H 0% 78% 0% 22% 0% 0%

I 0% 70% 10% 17% 0% 0%

J 0% 40% 20% 20% 20% 0%

K 6% 56% 8% 18% 12% 0%

ADIB INDEX (see map at end of report)

9

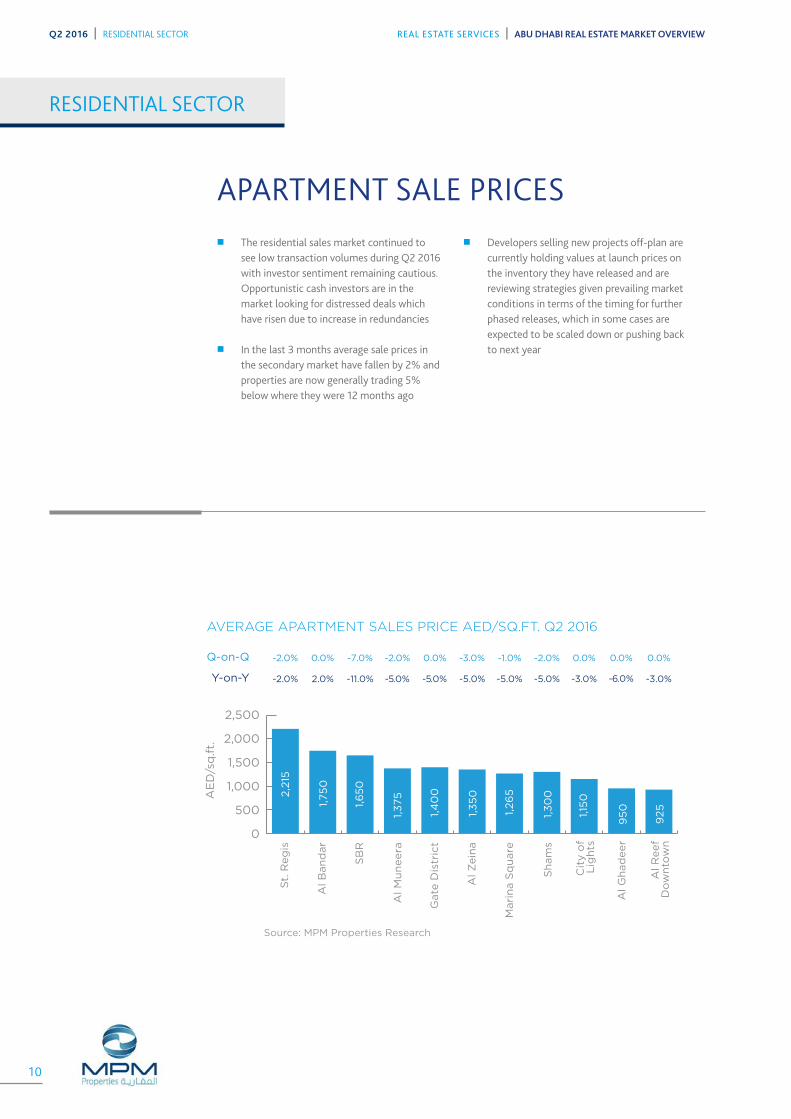

APARTMENT SALE PRICES �� The residential sales market continued to

see low transaction volumes during Q2 2016 with investor sentiment remaining cautious. Opportunistic cash investors are in the market looking for distressed deals which have risen due to increase in redundancies

�� In the last 3 months average sale prices in the secondary market have fallen by 2% and properties are now generally trading 5% below where they were 12 months ago

�� Developers selling new projects off-plan are currently holding values at launch prices on the inventory they have released and are reviewing strategies given prevailing market conditions in terms of the timing for further phased releases, which in some cases are expected to be scaled down or pushing back to next year

RESIDENTIAL SECTOR

0

500

1,000

1,500

2,000

2,500

Al R

eef

Do

wn

tow

n

Al G

had

eer

Cit

y o

fL

igh

ts

Mari

na S

qu

are

Sh

am

s

Al Z

ein

a

Gate

Dis

tric

t

Al M

un

ee

ra

SB

R

Al B

an

dar

St.

Reg

is

AE

D/s

q.ft.

-2.0% 0.0% -7.0% -2.0% 0.0% -3.0% -1.0% -2.0% 0.0% 0.0% 0.0%Q-on-Q

-2.0% 2.0% -11.0% -5.0% -5.0% -5.0% -5.0% -5.0% -3.0% -6.0% -3.0%Y-on-Y

2,2

15

1,75

0

1,6

50

1,3

75

1,4

00

1,3

50

1,26

5

1,3

00

1,15

0

95

0

925

Source: MPM Properties Research

AVERAGE APARTMENT SALES PRICE AED/SQ.FT. Q2 2016

10

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016 | RESIDENTIAL SECTOR

APARTMENT RENTS �� The residential leasing market in Abu Dhabi

has witnessed a decline in tenant demand during Q2 2016 with new tenant enquiries down by over 25% in comparison with the same period in 2015 (based on an analysis of MPM data). Enquiries for 3 and 4 bedroom apartments with budgets over AED 180,000 per annum have fallen significantly, which could reflect the impact of job cuts in the government sector

�� This drop in tenant demand has started to translate into downward pressure on rents across the market with average rents showing a decline of around 3% this quarter, with anticipation that this trend will continue in the second half of the year, particularly as the scheduled new supply enters the market

1 BRStudio 2 BR 3 BR

0

50

100

150

200

250

300

No

n-I

nvest

men

tZ

on

e G

rad

e B

No

n Invest

men

tP

rim

e Z

on

e

Al R

eef

Do

wn

tow

n

Sh

am

s

Mari

na

Sq

uare

Gate

Dis

tric

t

Al M

un

eera

Al Z

ein

a

Al B

an

dar

Al G

had

eer

St.

Reg

is

SB

R

0.0% -1.4% -0.7% -3.1% -1.6% 0.0% -3.0% -3.1% -1.2% -3.3% 2.7%Q-on-Q

-2.0%

-2.9%

-5.0% 4.0% 1.0% -3.0% -1.0% -3.0% -4.0% -7.0% 7.0% -10.0% 6.0%Y-on-Y

105

45

105

75

70

70

70 7

5

55

120 15

5170

210

26

5

26

0

20

0

195

185

185

180

135

24

0

135

195

75

170

150

150

145

135

130

110

160

110

60

135

115

115

100

90

90

80

115

85

Source: MPM Properties Research

AVERAGE APARTMENT ANNUAL RENT Q2 2016

11

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016 | RESIDENTIAL MARKET PERFORMANCE

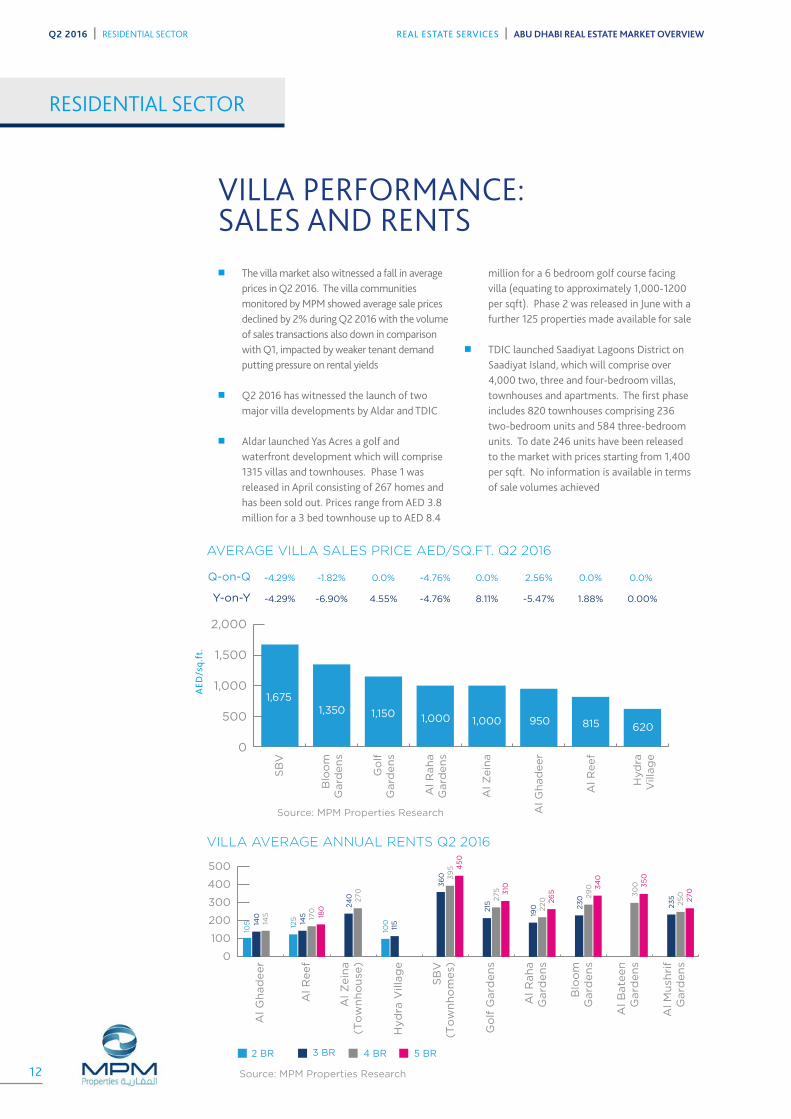

VILLA PERFORMANCE:SALES AND RENTS �� The villa market also witnessed a fall in average

prices in Q2 2016. The villa communities monitored by MPM showed average sale prices declined by 2% during Q2 2016 with the volume of sales transactions also down in comparison with Q1, impacted by weaker tenant demand putting pressure on rental yields

�� Q2 2016 has witnessed the launch of two major villa developments by Aldar and TDIC

�� Aldar launched Yas Acres a golf and waterfront development which will comprise 1315 villas and townhouses. Phase 1 was released in April consisting of 267 homes and has been sold out. Prices range from AED 3.8 million for a 3 bed townhouse up to AED 8.4

million for a 6 bedroom golf course facing villa (equating to approximately 1,000-1200 per sqft). Phase 2 was released in June with a further 125 properties made available for sale

�� TDIC launched Saadiyat Lagoons District on Saadiyat Island, which will comprise over 4,000 two, three and four-bedroom villas, townhouses and apartments. The first phase includes 820 townhouses comprising 236 two-bedroom units and 584 three-bedroom units. To date 246 units have been released to the market with prices starting from 1,400 per sqft. No information is available in terms of sale volumes achieved

RESIDENTIAL SECTOR

3 BR2 BR 4 BR 5 BR

100125

105

235

25

0270

230 2

90 3

40

190 220 26

5

215

275 3103

60

115

39

5 45

0

145

140 17

0

145 18

0 24

0 270 30

0 35

0

0

100

200

300

400

500

Al M

ush

rif

Gard

en

s

Al B

ate

en

Gard

en

s

Blo

om

Gard

en

s

Al R

ah

aG

ard

en

s

Go

lf G

ard

en

s

SB

V(T

ow

nh

om

es)

Hyd

ra V

illag

e

Al Z

ein

a(T

ow

nh

ou

se)

Al R

eef

Al G

had

eer

AED

/sq.

ft.

0

500

1,000

1,500

2,000H

yd

raV

illag

e

Al R

eef

Al R

ah

aG

ard

en

s

Go

lfG

ard

en

s

Blo

om

Gard

en

s

SB

V

-4.29%Q-on-Q

-4.29%

-1.82%

-6.90%

0.0%

4.55%

-4.76%

-4.76%

0.0%

8.11%

2.56%

-5.47%

0.0%

1.88%

0.0%

0.00%Y-on-Y

620815

Al Z

ein

a

1,0001,0001,1501,3501,675

Al G

had

eer

950

Source: MPM Properties Research

AVERAGE VILLA SALES PRICE AED/SQ.FT. Q2 2016

VILLA AVERAGE ANNUAL RENTS Q2 2016

Source: MPM Properties Research12

Q2 2016 | RESIDENTIAL SECTOR REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW

Main island KCA MBZ

Low AverageHigh

0

5

10

15

20

25

16.17

5.4

6

6.7

510.8

10.3

7

23

.0

7.15 15

.07

14.0

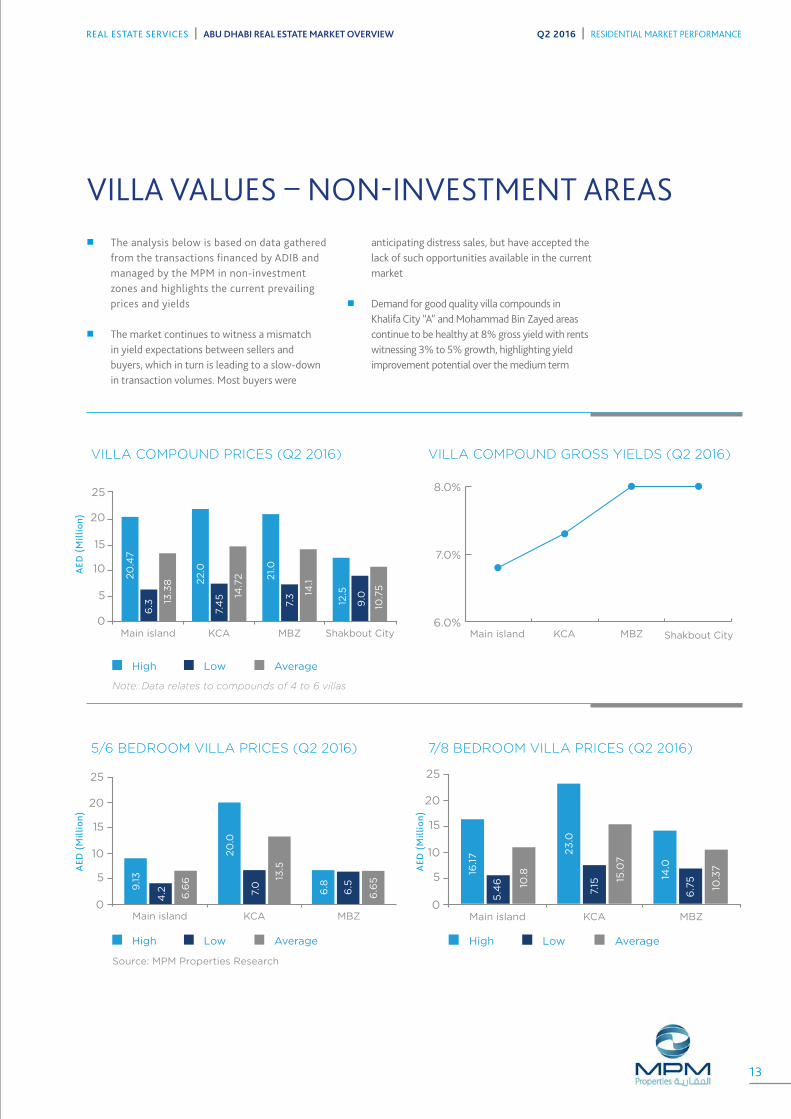

VILLA VALUES – NON-INVESTMENT AREAS�� The analysis below is based on data gathered

from the transactions financed by ADIB and managed by the MPM in non-investment zones and highlights the current prevailing prices and yields

�� The market continues to witness a mismatch in yield expectations between sellers and buyers, which in turn is leading to a slow-down in transaction volumes. Most buyers were

anticipating distress sales, but have accepted the lack of such opportunities available in the current market

�� Demand for good quality villa compounds in Khalifa City “A” and Mohammad Bin Zayed areas continue to be healthy at 8% gross yield with rents witnessing 3% to 5% growth, highlighting yield improvement potential over the medium term

0

5

10

15

20

25

Main island KCA MBZ Shakbout City

Low AverageHigh

20

.47

6.3 13

.38 2

2.0

7.4

5 14.7

2 21.0

7.3 14

.1

12.5

9.0

10.7

5

Main island KCA MBZ

Low AverageHigh

9.13

4.2 6.6

6

20

.0

7.0

13.5

6.8

6.5

6.6

5

0

5

10

15

20

25

6.0%

7.0%

8.0%

Main island KCA MBZ Shakbout City

AED

(M

illio

n)A

ED (

Mill

ion)

AED

(M

illio

n)

VILLA COMPOUND PRICES (Q2 2016)

5/6 BEDROOM VILLA PRICES (Q2 2016)

VILLA COMPOUND GROSS YIELDS (Q2 2016)

7/8 BEDROOM VILLA PRICES (Q2 2016)

Source: MPM Properties Research

Note: Data relates to compounds of 4 to 6 villas

13

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016 | RESIDENTIAL MARKET PERFORMANCE

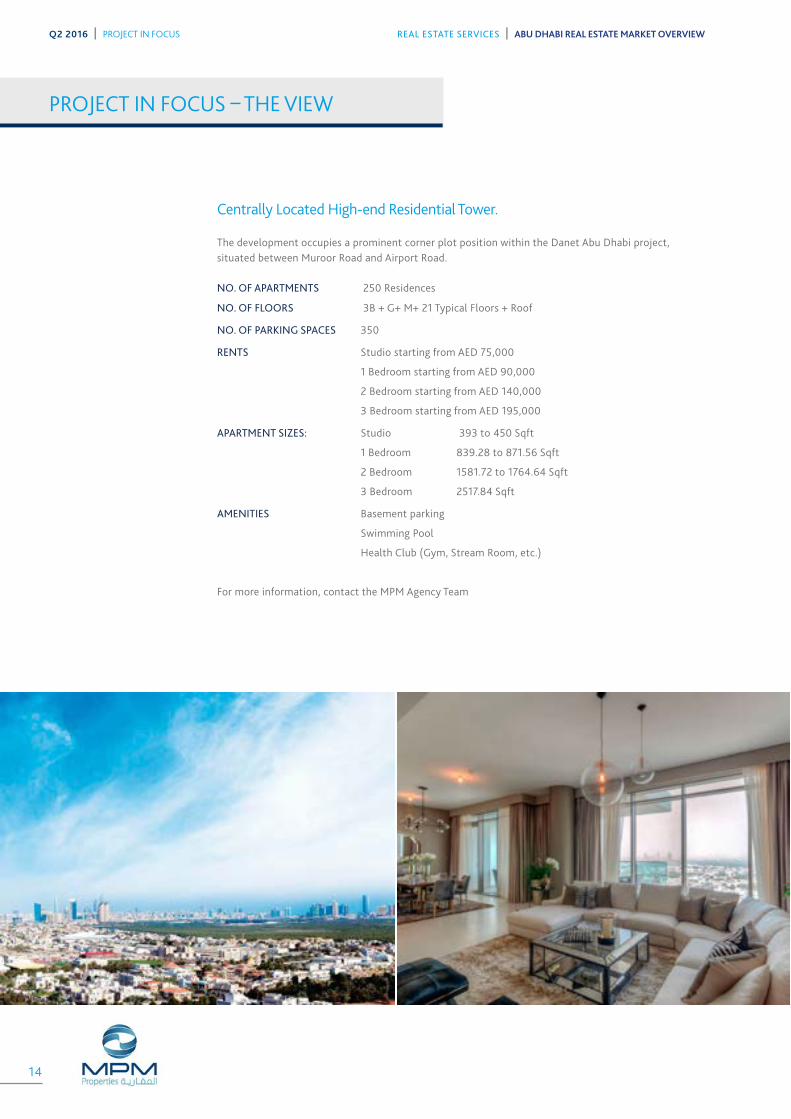

PROJECT IN FOCUS – THE VIEW

Centrally Located High-end Residential Tower.

The development occupies a prominent corner plot position within the Danet Abu Dhabi project, situated between Muroor Road and Airport Road.

NO. OF APARTMENTS 250 Residences

NO. OF FLOORS 3B + G+ M+ 21 Typical Floors + Roof

NO. OF PARKING SPACES 350

RENTS Studio starting from AED 75,000

1 Bedroom starting from AED 90,000

2 Bedroom starting from AED 140,000

3 Bedroom starting from AED 195,000

APARTMENT SIZES: Studio 393 to 450 Sqft

1 Bedroom 839.28 to 871.56 Sqft

2 Bedroom 1581.72 to 1764.64 Sqft

3 Bedroom 2517.84 Sqft

AMENITIES Basement parking

Swimming Pool

Health Club (Gym, Stream Room, etc.)

For more information, contact the MPM Agency Team

14

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016 | PROJECT IN FOCUS

15

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016 | PROJECT IN FOCUS

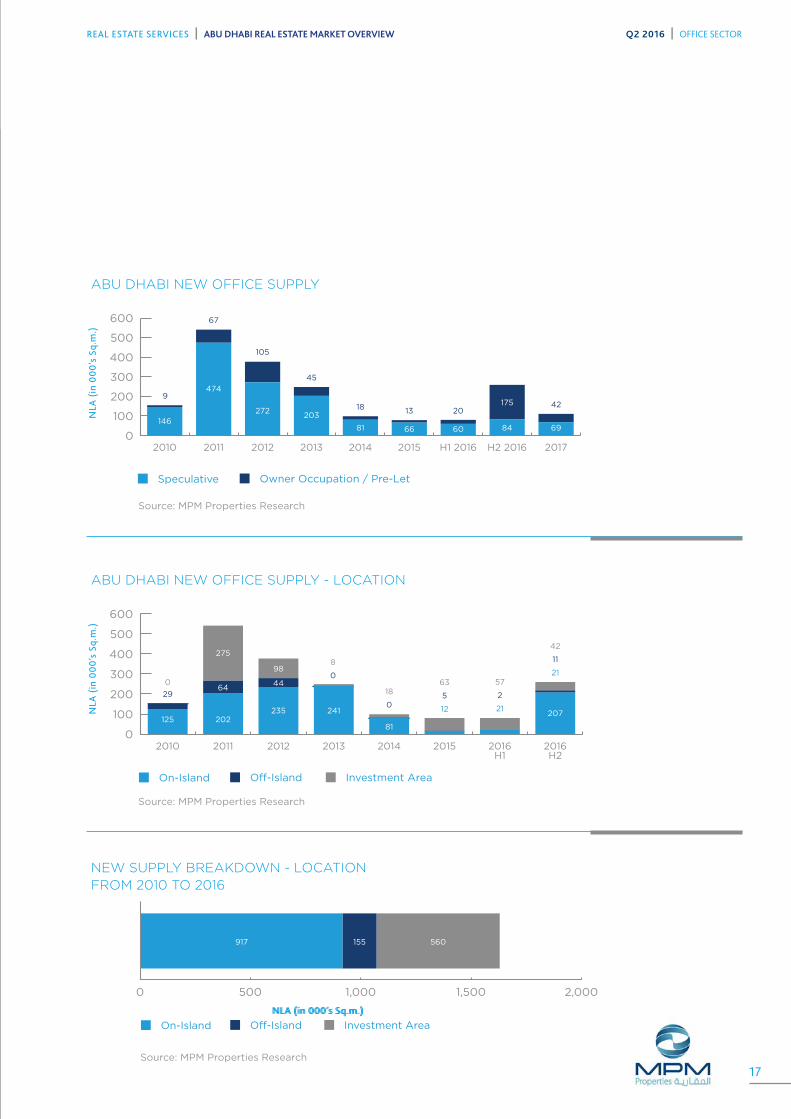

SUPPLY �� There have been no major additions to the Abu

Dhabi office market, with only 22,000Sq.m. of new space being added in Q2 2016. The total office stock now stands at around 3.38 million sq.m.

�� Announcement of recent mergers (i.e. Mubadala - IPIC and NBAD – FGB), is anticipated to increase the Grade “A” office supply as these firms will consolidate their offices and HQ, potentially vacating some of their offices and releasing it back in the market for tenant occupation or holding it for future expansion

�� On the other hand, fair few small to mid-sized companies have moved from larger offices to smaller offices or are in the process of relocating

their offices from Abu Dhabi Island to outside Abu Dhabi Island. This decision is driven by prevailing lower rents on Abu Dhabi mainland and availability of better parking facilities

�� Given the current market cycle investment opportunities are expanding in built-to-suit properties within the public / government sector with most investors only looking at such deals if the lease term was 10 years+

�� Business Park accommodation continues to be in demand from SME sector and this is an opportunity that needs to be tapped by developers and investors with a long term investment view in mind

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2017H2 2016H1 20162015201420132012201120102009

Running Total New Supply Completed Scheduled New Supply

0155

541

377249 99

2598079

1,800 1,800 1,9552,495

2,872 3,121 3,220 3,299 3,379

111

3,638

MARKET OVERVIEW Q2 2016

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016 | OFFICE SECTOR

NLA

(in

00

0’s

Sq.

m.)

ABU DHABI OFFICE SUPPLY (2009-2017)

Source: MPM Properties Research

16

On-Island Off-Island Investment Area

0 500 1,000 1,500 2,000

560155917

NLA (in 000’s Sq.m.)

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015 H1 2016 H2 2016 2017

Speculative Owner Occupation / Pre-Let

69

4220

9

1318

45

105

67

84

175

606681

203272

474

146

0

100

200

300

400

500

600

On-Island Off-Island Investment Area

125 202

64

275

235

44

98

241

81

12 21

21

207

29 5 2

11

63

0

18

0

8

57

42

0

2010 2011 2012 2013 2014 2015 2016H1

2016H2

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016 | OFFICE SECTOR

NLA

(in

00

0’s

Sq.

m.)

NLA

(in

00

0’s

Sq.

m.)

NLA (in 000’s Sq.m.)

ABU DHABI NEW OFFICE SUPPLY

ABU DHABI NEW OFFICE SUPPLY - LOCATION

NEW SUPPLY BREAKDOWN - LOCATIONFROM 2010 TO 2016

Source: MPM Properties Research

Source: MPM Properties Research

Source: MPM Properties Research

17

Q1 2016 Q2 2016

Grade BGrade A S&CGrade A Fitted0

500

1,000

1,500

2,000

1,975 1,850

1,650 1,550

1,260 1,150

-6.3% -8.7%-6.1%Q-on-Q

-1.3% -6.1%0.0%Y-on-Y

Rent

/ S

q.m

. (A

ED)

Sales Price / Sq.ft.

Prestige TowerMBZ

Tamouh TowerAddaxThe WaveSky Tower0

300

600

900

1,200

1,500

1,4001,250

1,165 1,150 1,125

-3.0% -2.0%-3.0% -2.0%0.0%Q-on-Q

-5.0% -4.0%-1.0% 2.0%0.0%Y-on-Y

Sale

s Pr

ice

/ Sq

.ft.

(A

ED)

Q2 2016 | OFFICE SECTOR REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW

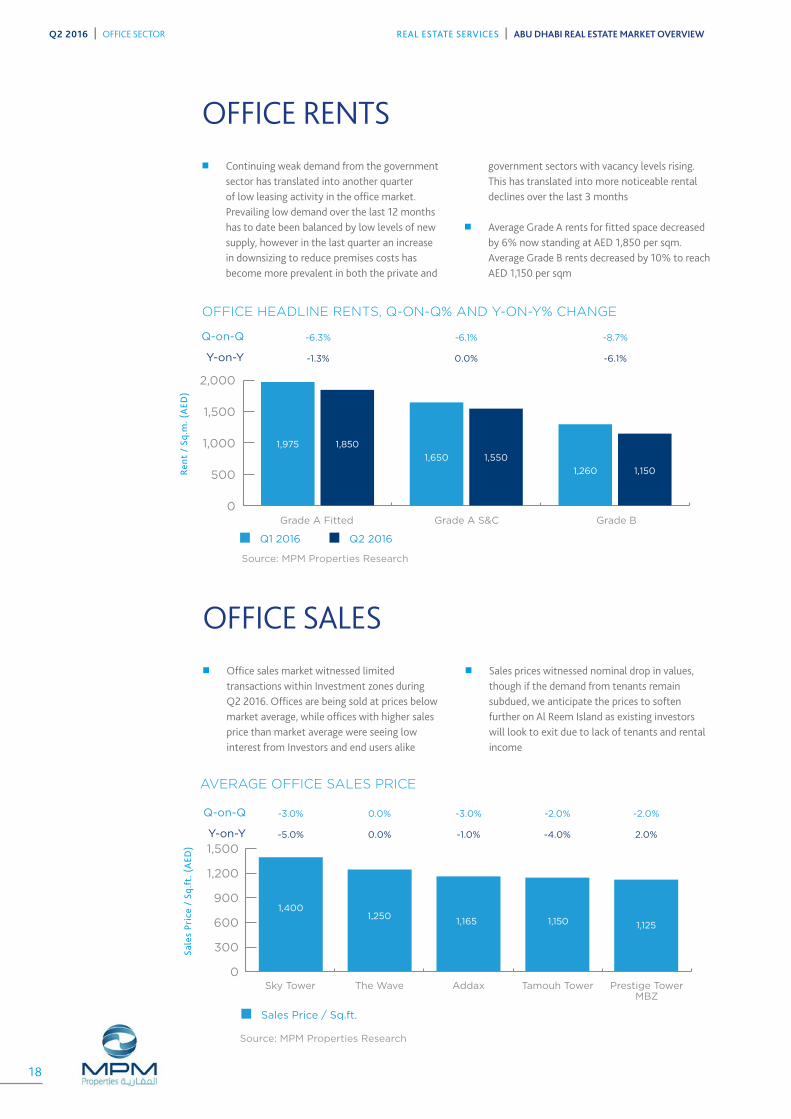

OFFICE RENTS �� Continuing weak demand from the government

sector has translated into another quarter of low leasing activity in the office market. Prevailing low demand over the last 12 months has to date been balanced by low levels of new supply, however in the last quarter an increase in downsizing to reduce premises costs has become more prevalent in both the private and

government sectors with vacancy levels rising. This has translated into more noticeable rental declines over the last 3 months

�� Average Grade A rents for fitted space decreased by 6% now standing at AED 1,850 per sqm. Average Grade B rents decreased by 10% to reach AED 1,150 per sqm

OFFICE SALES �� Office sales market witnessed limited

transactions within Investment zones during Q2 2016. Offices are being sold at prices below market average, while offices with higher sales price than market average were seeing low interest from Investors and end users alike

�� Sales prices witnessed nominal drop in values, though if the demand from tenants remain subdued, we anticipate the prices to soften further on Al Reem Island as existing investors will look to exit due to lack of tenants and rental income

OFFICE HEADLINE RENTS, Q-ON-Q% AND Y-ON-Y% CHANGE

Source: MPM Properties Research

AVERAGE OFFICE SALES PRICE

Source: MPM Properties Research

18

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016 | OFFICE SECTOR

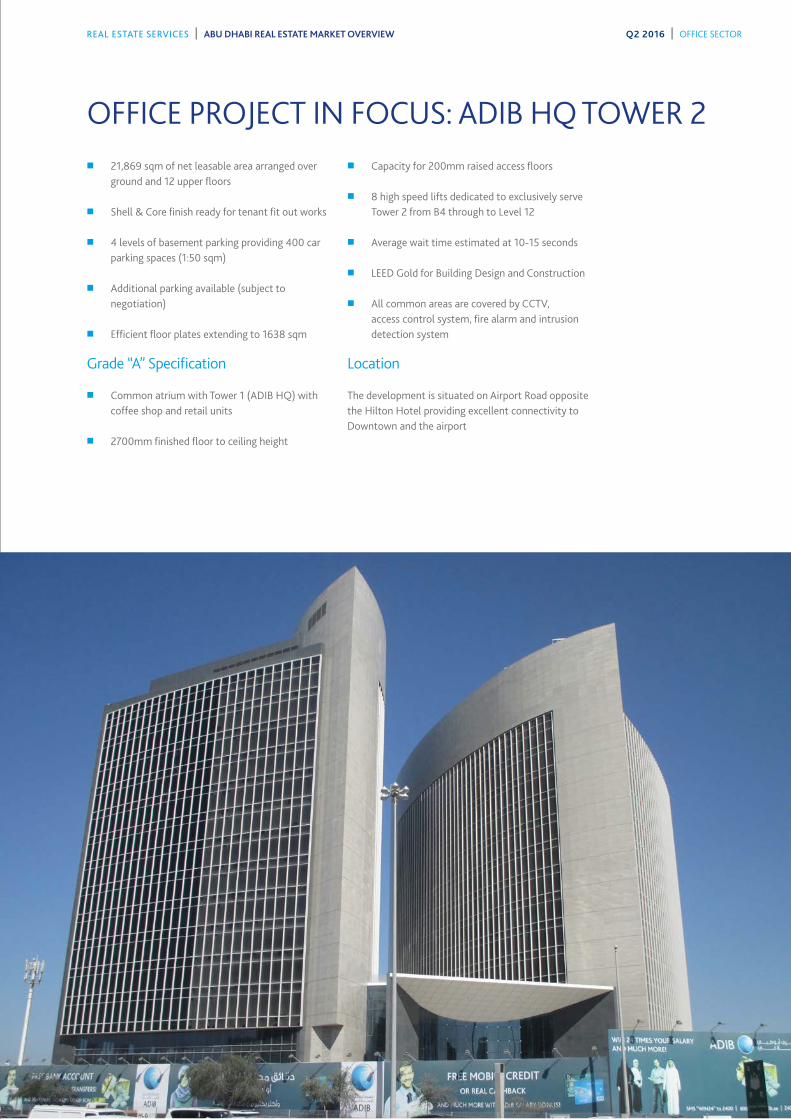

OFFICE PROJECT IN FOCUS: ADIB HQ TOWER 2�� 21,869 sqm of net leasable area arranged over

ground and 12 upper floors

�� Shell & Core finish ready for tenant fit out works

�� 4 levels of basement parking providing 400 car parking spaces (1:50 sqm)

�� Additional parking available (subject to negotiation)

�� Efficient floor plates extending to 1638 sqm

Grade “A” Specification

�� Common atrium with Tower 1 (ADIB HQ) with coffee shop and retail units

�� 2700mm finished floor to ceiling height

�� Capacity for 200mm raised access floors

�� 8 high speed lifts dedicated to exclusively serve Tower 2 from B4 through to Level 12

�� Average wait time estimated at 10-15 seconds

�� LEED Gold for Building Design and Construction

�� All common areas are covered by CCTV, access control system, fire alarm and intrusion detection system

Location

The development is situated on Airport Road opposite the Hilton Hotel providing excellent connectivity to Downtown and the airport

MARKET OVERVIEW Q2 2016

0

500

1000

1500

2000

2500

3000

3500

2009 2010 2011 2012 2013 2014 2015 2016H1

2016H2

20182017

Scheduled New Supply Running Total New Supply Completed

28

259113

185

342 43 1 19177

749

2,5662,3892,3702,3702,3271,9851,800

1,6871,4281,4001,400NLA

(in

00

0’s

) pe

r Sq

.m.

ABU DHABI RETAIL SUPPLY (2009 - 2018+)

Source: MPM Properties Research

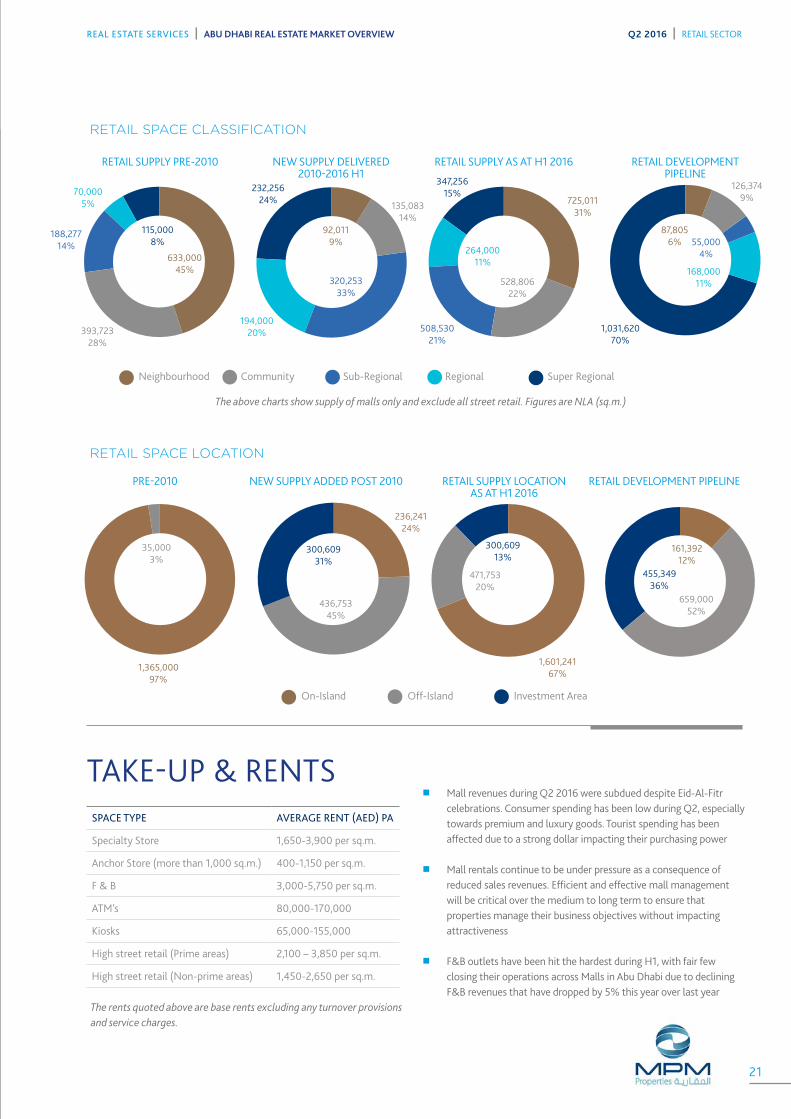

OVERVIEW �� There were no major retail developments delivered

during Q2 2016 with total retail space in the capital standing at approximately 2.4 million sq m NLA

�� In addition to the two super regional malls due to be completed in 2018/19 (Al Maryah Central Mall and Reem Mall), other sizeable retail schemes in the pipeline include the much delayed Paragon Bay at Marina Square and Paragon Point at the Meena Plaza mixed use development which together will add around 50,000 sqm of leasable retail space to the market

�� The impact of government austerity measures are affecting the retail market which is currently experiencing a decline in retail spending putting pressure on retailers trading performance. Overall, households are placing a greater impetus on saving and achieving greater value for money on both core and non-core spending. Therefore, there has been an increase in spending on necessities like food items while non-essential spending has tightened, often seeking promotions and sales

20

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016 | RETAIL SECTOR

TAKE-UP & RENTS

The rents quoted above are base rents excluding any turnover provisions and service charges.

�� Mall revenues during Q2 2016 were subdued despite Eid-Al-Fitr celebrations. Consumer spending has been low during Q2, especially towards premium and luxury goods. Tourist spending has been affected due to a strong dollar impacting their purchasing power

�� Mall rentals continue to be under pressure as a consequence of reduced sales revenues. Efficient and effective mall management will be critical over the medium to long term to ensure that properties manage their business objectives without impacting attractiveness

�� F&B outlets have been hit the hardest during H1, with fair few closing their operations across Malls in Abu Dhabi due to declining F&B revenues that have dropped by 5% this year over last year

SPACE TYPE AVERAGE RENT (AED) PA

Specialty Store 1,650-3,900 per sq.m.

Anchor Store (more than 1,000 sq.m.) 400-1,150 per sq.m.

F & B 3,000-5,750 per sq.m.

ATM’s 80,000-170,000

Kiosks 65,000-155,000

High street retail (Prime areas) 2,100 – 3,850 per sq.m.

High street retail (Non-prime areas) 1,450-2,650 per sq.m.

On-Island Off-Island Investment Area

RETAIL SUPPLY PRE-2010

PRE-2010

NEW SUPPLY DELIVERED 2010-2016 H1

NEW SUPPLY ADDED POST 2010

The above charts show supply of malls only and exclude all street retail. Figures are NLA (sq.m.)

RETAIL SUPPLY LOCATION AS AT H1 2016

RETAIL DEVELOPMENT PIPELINE

RETAIL SUPPLY AS AT H1 2016

RETAIL DEVELOPMENT PIPELINE

RETAIL SPACE CLASSIFICATION

RETAIL SPACE LOCATION

633,00045%

1,365,00097%

92,011 9%

725,011 31%

393,723 28%

135,083 14%

126,374 9%

70,0005%

194,000 20%

115,0008%

232,256 24%

347,256 15%

1,031,620 70%

188,27714%

320,253 33%

508,530 21%

Neighbourhood Community Sub-Regional Regional Super Regional

528,806 22%

264,000 11%

87,805 6% 55,000

4%

168,000 11%

35,000 3%

161,392 12%

659,000 52%

455,349 36%

21

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016 | RETAIL SECTOR

ARR RevPAR Occupancy

100%

90%

80%

70%

60%

50%

40%

30%

20%

Jan

13

Ju

l

Jan

14

Ju

l

Jan

15

Ju

l

Jan

16

Ap

r

0

100

200

300

400

500

600

700

800

MARKET OVERVIEW Q2 2016

HOTEL ESTABLISHMENT PERFORMANCE HISTORICAL TRADING PERFORMANCE 2013-2016

Source: TCA Abu Dhabi and MPM Properties Research

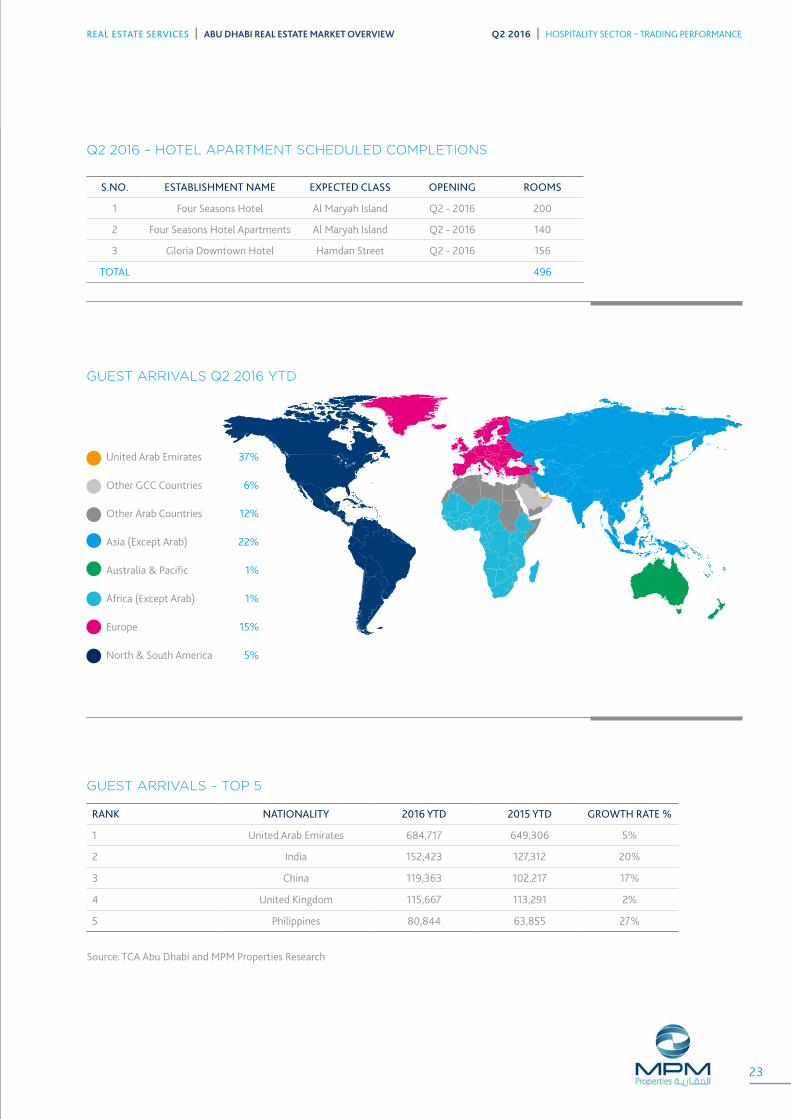

�� Q2 2016 saw the addition of three hotel properties in Abu Dhabi with the opening of the Four Seasons Hotel and Four Seasons Hotel Apartments at Al Maryah Island and the Gloria Downtown Hotel at Hamdan Street

�� These three properties have together added almost 500 keys to the hospitality stock which now stands at over 29,000 keys

�� H2 2016 is scheduled to witness the addition of 9 properties which will together add 2,410 keys,

which represents an 8.6% increase to the current stock level. Key additions include the Hilton Al Forsan, Grand Hyatt Emirates Pearl, and the Millennium Bab Al Qasr Hotel

�� Much like the retail sector the trading performance in the hospitality sector has been impacted by the prevailing economic conditions which have weighed on consumer and corporate spending, with the Average Daily Room Rates and RevPAR both down in Q2 by approximately 15% in comparison with 2015 levels

Num

ber

of r

oom

s

05,000

10,00015,000

20,00025,00030,00035,00040,000

Pre 2009

2009 2010 2011 20132012 2014 2015 2016H1

2016H2

2017+

Scheduled New Supply Running Total New Supply Completed

4,131

2,4104961,835

2,5232,312

2,6532,646

2,3975,374 30,924

28,51428,01826,18323,66021,34818,69516,04913,6528,2788,278

ABU DHABI HOTEL ROOM SUPPLY (2009 - 2017+)

Source: MPM Properties Research22

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016 | HOSPITALITY SECTOR – TRADING PERFORMANCE

Q2 2016 – HOTEL APARTMENT SCHEDULED COMPLETIONS

GUEST ARRIVALS – TOP 5

GUEST ARRIVALS Q2 2016 YTD

S.NO. ESTABLISHMENT NAME EXPECTED CLASS OPENING ROOMS

1 Four Seasons Hotel Al Maryah Island Q2 - 2016 200

2 Four Seasons Hotel Apartments Al Maryah Island Q2 - 2016 140

3 Gloria Downtown Hotel Hamdan Street Q2 - 2016 156

TOTAL 496

RANK NATIONALITY 2016 YTD 2015 YTD GROWTH RATE %

1 United Arab Emirates 684,717 649,306 5%

2 India 152,423 127,312 20%

3 China 119,363 102,217 17%

4 United Kingdom 115,667 113,291 2%

5 Philippines 80,844 63,855 27%

United Arab Emirates 37%

Other GCC Countries 6%

Other Arab Countries 12%

Asia (Except Arab) 22%

Australia & Pacific 1%

Africa (Except Arab) 1%

Europe 15%

North & South America 5%

Source: TCA Abu Dhabi and MPM Properties Research

23

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016 | HOSPITALITY SECTOR – TRADING PERFORMANCE

RESEARCH STUDY AREA

The geographical extent of the study area includes the Abu Dhabi Island, Investment Areas and the most populated Off-Island districts specifically Khalifa City A, Mohammed Bin Zayed City and Shakbout City.

RESIDENTIAL

New residential developments are classified as delivered and thus entered into the new supply category when they are made available for occupation. This is verified via a combination of site inspections and discussion with the developer and hence our supply numbers do take into consideration the phased release of large projects.

The ADIB Rental Index relates to the performance of the ADIB portfolio only and the data is derived exclusively from transactions completed by MPM Properties.

Other rental and sales trend analysis is based on transactional data derived from the MPM Properties Agency team and data sourced from developers and owners.

OFFICES

New office developments are classified as delivered and thus entered into the new supply category when they are available for tenant fit-outs.

Given the general lack of transparency in the local market rents quoted are headline rents, thus exclude any rent free period or other financial incentives that may have been negotiated between the parties. The rents quoted are also exclusive of service charges.

RETAIL

New retail developments are classified as delivered and thus entered into the new supply category when the first units are open and trading.

Our classification of malls is based on our own assessment having regard to size and the catchment area which the mall typically penetrates.

HOSPITALITY

New hotels are classified as delivered and thus entered into the new supply category when they are opened and trading. All trading performance data is provided by ADTCA.

FUTURE SUPPLY PROJECTIONS

Our future supply projections across all sectors are based on a combination of regular site inspections and discussions with developers.

DEFINITIONS & METHODOLOGY

DISCLAIMER:

The information contained in this report has been obtained

from and is based upon sources that ADIB Real Estate Services

believes to be reliable, however, no warranty or representation,

expressed or implied, is made to the accuracy or completeness

of the information contained herein, and same is submitted

subject to errors, omissions, change of price, rental or other

conditions, withdrawal without notice, and to any special listing

conditions imposed by our principals. ADIB Real Estate Services

will not be held responsible for any third-party contributions.

All opinions and estimates included in this report constitute

ADIB Real Estate Services, as of the date of this report and

are subject to change without notice. Figures contained in

this report are derived from a basket of locations highlighted

in this report and therefore represent a snapshot of the Abu

Dhabi market. Due care and attention has been used in the

preparation of forecast information. However, actual results

may vary from forecasts and any variation may be materially

positive or negative. Forecasts, by their very nature, involve

risk and uncertainty because they relate to future events and

circumstances which are beyond ADIB Real Estate Services’

control. For a full in-depth study of the market, please contact

ADIB Real Estate Services team.

BESPOKE CLIENT RESEARCH ADDING VALUE TO YOUR PROPERTY INTERESTSThe ADIB Real Estate Services team covers all sectors of the real estate market. We provide bespoke market research to our valued clients to meet their specific requirements.

We provide reports, information and presentations derived from primary market data that directly assist our clients to save or make money from real estate and shape strategies to enhance value.

24

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016 | DEFINITIONS & METHODOLOGY

A collaborative team providing our integrated services

MOHAMED AL ZOUBI Head of Development Advisory BSc Civil Engineering T: +971 (0)2 610 0564 M: +971 (0)50 310 3570 [email protected]

PRADEEP FERNANDES MRICS Advisory & Valuation Manager BSc Civil Engineering T: +971 (0)2 510 0663 M: +971 (0)55 961 3626 [email protected]

JASON FIELDEN BSC (HONS) MRICS Valuation Manager - Abu Dhabi T: +971 (0)2 510 0653 M: +971 (0)56 244 7696 [email protected]

PAUL MAISFIELD BSC (HONS) MRICS CEO T: +971 (0)2 610 0545 M: +971 (0)50 660 9437 [email protected]

YOUSEF AL ZAROONI Regional Head – Al Ain T: +971 (0)3 708 8636 M: +971 (0)50 600 1002 [email protected]

ABDULLAH SAID AL KUWEITI Business Development Director T: +971 (0)2 610 1554 M: +971 (0)50 623 5854 [email protected]

WAHIDA KARAMA Head of Property Operations T: +971 (02) 610 0435 M: +971 (0)50 765 7679 [email protected]

FRANK O’DWYER MBA (Hons); BEng.COO T: +971 (0)2 610 0402 M: +971 (0)50 812 1070 [email protected]

DOMINIC BARLOW Head of Retail, Hospitality & Leisure T: +971 (0)2 510 0655 M: +971 (0)56 288 1458 [email protected]

JUBRAN AL HASHMI Head of Property Services T: +971 (0)2 610 0232 M: +971 (0)50 122 0041 [email protected]

ALI ABDULLAH ABDUL RAHMAN Acting Regional Head – Northern Emirates T: 971 (0)6 597 2514 M: +971 (0)50 656 2486 [email protected]

VAIBHAV SHARMA MCOM; MDBA Director of Strategic Advisory and Research T: +971 (0)2 412 8914 M: +971 (0)50 660 9295 [email protected]

KHALED AL SOLEH BSC MRICS Head of Valuation – Abu Dhabi T: +971 (0)2 610 0085 M: +971 (0)50 722 9718 [email protected]

VINEET KUMAR Director of Agency T: +971 (0)4 371 9462 M: +971 (0)50 651 6491 [email protected]

25

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q2 2016

SUPPLY - PHOTO GALLERY

SAMPLE OF NEW & UPCOMING SUPPLYNEW SUPPLY (Q2 2016)

INVESTMENT AREA - UPCOMING SUPPLY

2 GLORIA DOWNTOWN

6 NALAYA VILLAS, REEM ISLAND3 BLOOM CENTRAL AIRPORT ROAD

4 EMI STATE TOWER

NON INVESTMENT AREA - UPCOMING SUPPLY

20 SEA FACE TOWER, REEM ISLAND

23 M TOWER, REEM ISLAND

24 LEAF TOWER, REEM ISLAND

25 SKY GARDENS, REEM ISLAND

29 COMMERCIAL BUILDING C10 W1

32 REGENT EMIRATES PEARL HOTEL

40

46

52

ADTC PHASE 3

C104/C105 RESIDENTIAL BUILDINGS, RAWDHAT

AL JOWHARA TOWER, SARAYA

33 BAB AL QASR HOTEL

41

47

53

CENTRAL MALL

C83 COMMERCIAL BUILDING, RAWDHAT

HARD ROCK HOTEL, SARAYA

35 AL JAZEERA TOWER, CORNICHE (W1, C12)

34 LINK INTL. PROPERTIES

42 BURJ AL JEWN, DANET

36 FOUNDATION PROPERTIES, MEENA ROAD

37

43

49

54 55

MARINA SUNSET BAY

BLOOM GARDENS - PHASE 3 (147 VILLAS)

THE VIEWS 1 & 2 - SARAYA

C32 LINK PROPERTIES, SARAYA

HILTON HOTEL AL FORSAN

30 ABU DHABI MARINA

38

44

5048

FAIRMONT HOTEL

C74/C75/C76 RESIDENTIAL

C34 AL NAHDHA INVESTMENT

C70 EMIRATES LAND GROUP

31 THE BILTMORE HOTEL

39

45

51

MIXED-USE TOWER KHALIDIYA W10, C64

C60 COMMERCIAL BUILDING

C35 AL SARAYA RESIDENTIAL

10 HORIZON TOWERS, REEM ISLAND

7 AL HADEEL, RAHA BEACH

11 OMEGA TOWER - REEM ISLAND

8 LAMAR RESIDENCES, RAHA BEACH

14 UNB TOWERS, REEM ISLAND

15 WAFRA RESIDENTIAL BUILDING, REEM ISLAND

16 BOARDWALK RESIDENCE

17 ENI SHAMS TOWER, REEM ISLAND

18 YASMINA RESIDENCE, REEM ISLAND

21 THE KITE RESIDENCES

19 PARK VIEW TOWER, REEM ISLAND

22 AL QURM VIEW, REEM ISLAND

26 UNITED SQUARE 27 FOUNDATION PROPERTIES

28 MARSA AL BATEEN

1 FOUR SEASONS

5 THE VIEW, C38 DANET

12 SHEIKH OMAR TOWER

9 SHK FAISAL, RAHA BEACH

13 RDK TOWER, REEM ISLAND

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016 | SUPPLY - PHOTO GALLERY

Residential

Offices

Retail

Hotels

Residential

Offices

Retail

Hotels

Q2 2014 NEW SUPPLY UNDER CONSTRUCTION

Residential

Offices

Retail

Hotels

Residential

Offices

Retail

Hotels

Q2 2014 NEW SUPPLY UNDER CONSTRUCTION

Jubail Island

Al ReemIsland

Al MaryahIsland

Al Raha Beach

MasdarCity

Saadiyat Island

Yas Island

HydraVillage

Al Reef

B

D

E F

G H

K

I

J

A

C

Salam Street

Khaleej Al Arabi Street

Airport Rd

Airport Rd

E 20

E 22

E 30

Corn

iche

Rd

Electra St

Zayed The First S

t

E12

Al Saada Stre

et

25th S

t

Salam Street

Salam Street

Sheikh Khalifa Hway

Abu D

habi

- Dub

ai Rd

Abu Dhabi - Dubai Rd

E 10

Shei

kh M

akto

um B

in R

ashi

d Rd

E 11

E 11

E 10

6

5

4

1

89

7

1116

2322

10

1514 12

13

1920

21

1718

25

24

40

34

3130 28

3233

3837

3529

39 26

36

27

43

3

42

2

454847

44 46

49

5054

5153

52

55

41

New Supply

Investment

Non-investment

Q3 NEW & UPCOMING SUPPLY

ADIB RENTAL INDEX ZONE

COMMON TREND (Q2 2016) (ANNUAL

% RENTAL INCREASE)

Q-Q CHANGE OVERALL AVERAGE

Q2 2016 Q1 2016 Q4 2015 Q3 2015 Q2 2015 Q1 2015 Q4 2014 Q3 2014 Q2 2014

Zone A 0 to 4.99% 1.88% 3.52% 3.06% 3.05% 4.58% 3.71% 8.05% 5.01% 2.37%

Zone B 0 to 4.99% 3.81% 3.38% 4.33% 2.60% 5.08% 6.94% 7.75% 10.56% 3.86%

Zone C 0 to 4.99% 5.41% 6.05% 5.94% 5.63% 7.46% 9.25% 9.79% 12.34% 10.26%

Zone D 0 to 4.99% 4.42% 7.01% 7.05% 6.48% 7.06% 8.51% 10.31% 10.26% 9.07%

Zone E 5% 5.28% 9.34% 7.35% 3.76% 4.02% 7.54% 5.09% 10.20% 5.32%

Zone F 0 to 4.99% 3.09% 3.33% 5.62% 4.77% 3.17% 4.01% 6.58% 7.63% 3.25%

Zone G 0 to 4.99% 2.24% 0.46% 1.91% 4.42% 2.34% 2.20% 2.59% 2.69% 2.42%

Zone H 0 to 4.99% 1.39% 2.77% 3.85% 3.68% 5.58% 3.46% 1.46% 3.42% 5.31%

Zone I 0 to 4.99% 2.46% 2.22% 2.36% 3.08% 3.41% 1.86% 5.48% 1.14% 1.33%

Zone J 0 to 4.99% 5.30% 4.12% 1.87% 3.32% 5.78% 0.96% 4.04% 3.06% 1.55%

Zone K 0 to 4.99% 3.14% 4.05% 6.10% 5.30% 5.89% 2.88% 4.31% 4.18% 3.51%

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ2 2016

INTEGRATED SERVICES COVERING THE FULL PROPERTY LIFECYCLE

Property Management

Investment Advisory

Project Management and ESCROW

Research & Strategic AdvisoryAgency (Sales & Leasing)

Valuation

PAUL MAISFIELD BSC (HONS) MRICS CEO T: +971 (0)2 610 0545 M: +971 (0)50 660 9437 [email protected]

VAIBHAV SHARMA MCOM; MDBA Director of Strategic Advisory and Research T: +971 (0)2 412 8914 M: +971 (0)50 660 9295 [email protected]

ABU DHABI HEAD OFFICE 6th Floor, Al Wahda Tower P.O Box 114686 Abu Dhabi

Tel. +971 2 610 0252Fax. +971 2 610 0514 www.mpmproperties.ae

DUBAI OFFICE Office 2301,2303,2305 - Level 123 Arenco Tower, Dubai Internet City Dubai

Tel. +971 (0)4 371 9462

AL AIN OFFICE 201-204 ADIB Ladies Branch Building Oud Touba Street Al Ain

Tel. +971 (0)3 703 9521

SHARJAH OFFICE AL Ikhlas Tower AL Khan Shajrah

Tel. +971 (0)6 597 2555

Enhancing value for individual & institutional property owners:

�� Prompt leasing & debt collection

�� Effectively market & lease vacant units

�� Physical & technical maintenance of asset

�� Maintain tenant satisfaction

�� Timely lease renewals

�� Manage risk, insurance & litigation

�� Protect your interests and enhance value

Complete Project Management services at planning & construction stage:

�� Engineering Review & Scheduling

�� Cost Estimate & Procurement

�� Project Monitoring

�� Cost Control & Accounting

�� Assist with Permits & Licensing

�� Ensure appropriate fund movement for Escrow based on Project Assessment

Aiding developers and investors to maximize value:

�� Investment Advisory & Due Diligence

�� Investment Management

�� Disposal Strategy

�� Portfolio Review & Optimization

�� Deal Structuring & Capital Sourcing

�� Investment Sale

We work with developers, commercial tenants, retailers and individuals, offering:

�� Launch Strategy

�� Project Launch Handling

�� Project Marketing Events

�� Acquisitions

�� Leasing

�� Sales

We cover all sectors, including residential, commercial, industrial, retail, and land.

Bankable studies for your real estate and business needs:

�� Highest & Best Use

�� Market & Financial Feasibility

�� Development Strategy

�� Market Research

�� Corporate Real Estate Strategy

�� Master-plan and design review

Valuation reports for:

�� Mortgage & Loan Security

�� Securing Project Funding

�� Internal Accounting

�� Mergers & Acquisitions

�� Investment appraisal

�� Litigation

�� Inheritance

We cover all asset classes. Our reports are in compliance with the International Valuation Standards (IVS) and the RICS Professional Valuation Standards.

Related Documents