Forensic and Investigative Forensic and Investigative Accounting Accounting Chapter 1 Introduction to Forensic and Investigative Accounting © 2011 CCH. All Rights © 2011 CCH. All Rights Reserved. Reserved. 4025 W. Peterson Ave. 4025 W. Peterson Ave. Chicago, IL 60646-6085 Chicago, IL 60646-6085 1 800 248 3248 1 800 248 3248 www.CCHGroup.com www.CCHGroup.com

5Ed CCH Forensic Investigative Accounting Ch01

Oct 20, 2015

5Ed CCH Forensic Investigative Accounting Ch01

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Forensic and Investigative AccountingForensic and Investigative Accounting

Chapter 1

Introduction to Forensic and Investigative Accounting

© 2011 CCH. All Rights © 2011 CCH. All Rights Reserved.Reserved.

4025 W. Peterson Ave.4025 W. Peterson Ave.

Chicago, IL 60646-6085Chicago, IL 60646-6085

1 800 248 32481 800 248 3248

www.CCHGroup.comwww.CCHGroup.com

Chapter 1 Forensic and Investigative Accounting 2

Forensic Accounting vs. Fraud AuditingForensic Accounting vs. Fraud Auditing

Fraud Auditor:Fraud Auditor: An accountant especially An accountant especially skilled in auditing who is generally engaged skilled in auditing who is generally engaged in auditing with a view toward fraud in auditing with a view toward fraud discovery, documentation, and prevention.discovery, documentation, and prevention.

Chapter 1 Forensic and Investigative Accounting 3

Forensic Accounting vs. Fraud AuditingForensic Accounting vs. Fraud Auditing

Forensic Accountant:Forensic Accountant: A forensic accountant A forensic accountant may take on fraud auditing engagements and may take on fraud auditing engagements and may be a fraud auditor, but he or she will also may be a fraud auditor, but he or she will also use other accounting, consulting, and legal use other accounting, consulting, and legal skills in broader engagements. In addition to skills in broader engagements. In addition to accounting skills, he or she will need a accounting skills, he or she will need a working knowledge of the legal system and working knowledge of the legal system and excellent communication skills to carry out excellent communication skills to carry out expert testimony in the courtroom and to aid expert testimony in the courtroom and to aid in other litigation support engagements.in other litigation support engagements.

Chapter 1 Forensic and Investigative Accounting 4

Forensic Accounting DefinedForensic Accounting Defined

Time:Time: Forensic accounting focuses on the past, Forensic accounting focuses on the past, although it may do so in order to look forward.although it may do so in order to look forward.

Purpose:Purpose: Forensic accounting is performed for a Forensic accounting is performed for a specific legal forum or in anticipation of specific legal forum or in anticipation of presentation before a legal forum.presentation before a legal forum.

Peremptory: Peremptory: Forensic accountants may be Forensic accountants may be employed in a wide variety of risk management employed in a wide variety of risk management engagements within business enterprise as a engagements within business enterprise as a matter of right, without the necessity of allegations matter of right, without the necessity of allegations (e.g., proactive).(e.g., proactive).

Chapter 1 Forensic and Investigative Accounting 5

Forensic Accounting DefinedForensic Accounting Defined

Forensic accounting is the action of Forensic accounting is the action of identifying, recording, settling, extracting, identifying, recording, settling, extracting, sorting, reporting, and verifying past financial sorting, reporting, and verifying past financial data or other accounting activities for settling data or other accounting activities for settling current or prospective legal disputes or using current or prospective legal disputes or using such past financial data for projecting future such past financial data for projecting future financial data to settle legal disputes.financial data to settle legal disputes.

Chapter 1 Forensic and Investigative Accounting 6

Historical Roots of AccountingHistorical Roots of Accounting

10,000 years ago10,000 years ago—Temple priests took inventory of —Temple priests took inventory of village livestock.village livestock.

3,000 B.C.—Scribes recorded ruler’s wealth.3,000 B.C.—Scribes recorded ruler’s wealth.

1887—American Association of Public Accountants 1887—American Association of Public Accountants (later becoming the AICPA) was formed.(later becoming the AICPA) was formed.

1896—New York State legislated the first CPA law.1896—New York State legislated the first CPA law.

1900—School of Commerce, Accounts, and Finance 1900—School of Commerce, Accounts, and Finance at New York University opens.at New York University opens.

(continued on next slide)(continued on next slide)

Chapter 1 Forensic and Investigative Accounting 7

Historical Roots of AccountingHistorical Roots of Accounting

1902—Congress calls for audit reports for large 1902—Congress calls for audit reports for large corporations.corporations.

1913—Federal Reserve Board created.1913—Federal Reserve Board created.

1913—Federal income tax law was passed.1913—Federal income tax law was passed.

1914—Federal Trade Commission created.1914—Federal Trade Commission created.

By 1921—All states had passed laws requiring exam By 1921—All states had passed laws requiring exam for CPA certificate.for CPA certificate.

Chapter 1 Forensic and Investigative Accounting 8

History of Financial Reports and History of Financial Reports and Legal ChallengesLegal Challenges

Financial reports were created by accountants Financial reports were created by accountants long before independent audits were mandated.long before independent audits were mandated.

Current system of accounting checks and Current system of accounting checks and balances is relatively recent.balances is relatively recent.

(continued on next slide)(continued on next slide)

Chapter 1 Forensic and Investigative Accounting 9

History of Financial Reports and History of Financial Reports and Legal ChallengesLegal Challenges

Before financials were audited by outside Before financials were audited by outside experts, the courts often handled challenges experts, the courts often handled challenges and brought in experts to give testimony.and brought in experts to give testimony.

Practice of forensic accounting was common Practice of forensic accounting was common even before independent accountants were even before independent accountants were asked to certify financial statements in asked to certify financial statements in auditing engagements.auditing engagements.

Chapter 1 Forensic and Investigative Accounting 10

Threads of Forensic AccountingThreads of Forensic Accounting

18171817—Canadian court decision of —Canadian court decision of Meyer v. Meyer v. Sefton.Sefton.

1824—James McClelland started his business 1824—James McClelland started his business in Glasgow, Scotland.in Glasgow, Scotland.

1856—In England, the audit of corporations 1856—In England, the audit of corporations became required.became required.

Chapter 1 Forensic and Investigative Accounting 11

Forensic Accounting in PrintForensic Accounting in Print

Articles on arbitration, fraud, investigation, and Articles on arbitration, fraud, investigation, and expert witnesses began appearing in the late expert witnesses began appearing in the late 1800s.1800s.

After a comment in 1925 by the Chairman of After a comment in 1925 by the Chairman of the U.S. Board of Tax Appeal, the U.S. Board of Tax Appeal, The Journal of The Journal of AccountancyAccountancy proposed that educational proposed that educational institutions should start including in their institutions should start including in their curricula the study of the law of evidence.curricula the study of the law of evidence.

Chapter 1 Forensic and Investigative Accounting 12

Phrase “Forensic Accounting” Is BornPhrase “Forensic Accounting” Is Born Maurice E. Peloubet coined the phrase in print in 1946.Maurice E. Peloubet coined the phrase in print in 1946. Max Lourie wrote an article and also claimed to coin the Max Lourie wrote an article and also claimed to coin the

phrase, seven years after Peloubet. Lourie’s article voiced phrase, seven years after Peloubet. Lourie’s article voiced three important positions:three important positions:

– An accountant should not have to attend law school to An accountant should not have to attend law school to learn the art of expert testimony.learn the art of expert testimony.

– Colleges and universities should deliver forensic Colleges and universities should deliver forensic accounting training.accounting training.

– Forensic accounting reference books and textbooks Forensic accounting reference books and textbooks should be developed for students.should be developed for students.

The first forensic accounting book appeared in 1982.The first forensic accounting book appeared in 1982.

Chapter 1 Forensic and Investigative Accounting 13

FBI and ForensicsFBI and Forensics During WWII, the FBI employed During WWII, the FBI employed

approximately 500 agents who were approximately 500 agents who were accountants.accountants.

In 1960, about 700 FBI agents were Special In 1960, about 700 FBI agents were Special Agent Accountants.Agent Accountants.

Today, there are more than 600 FBI agents Today, there are more than 600 FBI agents with accounting backgrounds. The FBI has a with accounting backgrounds. The FBI has a Financial Crimes Section that investigates Financial Crimes Section that investigates money laundering, Internet crimes, financial money laundering, Internet crimes, financial institutions fraud, and any other economic institutions fraud, and any other economic crime.crime.

Chapter 1 Forensic and Investigative Accounting 14

AICPA Practice AidAICPA Practice AidIn 1986, the AICPA broke forensic accounting into In 1986, the AICPA broke forensic accounting into two broad areas: investigative accounting and two broad areas: investigative accounting and litigation support.litigation support.The types of litigation services were further broken The types of litigation services were further broken down in Practice Aid 7, listing:down in Practice Aid 7, listing:

– damagesdamages– antitrust analysesantitrust analyses– accountingaccounting– valuationvaluation– general consultinggeneral consulting– analysesanalyses

Chapter 1 Forensic and Investigative Accounting 15

Panel on Audit EffectivenessPanel on Audit Effectiveness

In 1998, the Public Oversight Board In 1998, the Public Oversight Board appointed the Panel on Audit Effectiveness to appointed the Panel on Audit Effectiveness to review and evaluate how independent audits review and evaluate how independent audits of the financial statements of public of the financial statements of public companies are performed and to assess companies are performed and to assess whether recent trends in audit practices serve whether recent trends in audit practices serve the public interest.the public interest.

Chapter 1 Forensic and Investigative Accounting 16

Panel on Audit EffectivenessPanel on Audit Effectiveness

In 2000, the Panel issues a 200-page report, In 2000, the Panel issues a 200-page report, Report and RecommendationsReport and Recommendations, which includes , which includes a recommendation that auditors should a recommendation that auditors should perform forensic-type procedures during perform forensic-type procedures during every audit to enhance the prospects of every audit to enhance the prospects of detecting material financial statement fraud.detecting material financial statement fraud.

Chapter 1 Forensic and Investigative Accounting 17

AICPA Fraud Task Force ReportAICPA Fraud Task Force Report

In 2003, the AICPA’s Litigation and Dispute In 2003, the AICPA’s Litigation and Dispute Resolution Services Subcommittee issued a Resolution Services Subcommittee issued a report of its Fraud Task Force entitled, report of its Fraud Task Force entitled, “Incorporating Forensic Procedures in an Audit “Incorporating Forensic Procedures in an Audit Environment.” Environment.” The report covers the professional standards that The report covers the professional standards that apply when forensic procedures are employed in apply when forensic procedures are employed in an audit and explains the various means of an audit and explains the various means of gathering evidence through the use of forensic gathering evidence through the use of forensic procedures and investigative techniques.procedures and investigative techniques.

Chapter 1 Forensic and Investigative Accounting 18

Accountant’s Role in Fraud DetectionAccountant’s Role in Fraud Detection

In the early 1980s, companies began to use In the early 1980s, companies began to use computers to perform their record keeping.computers to perform their record keeping.

Intense competition caused auditing fees to fall as Intense competition caused auditing fees to fall as much as 50% from the mid-1980s to the mid-much as 50% from the mid-1980s to the mid-1990s. 1990s.

Auditors cut costs by reducing the process of Auditors cut costs by reducing the process of reviewing hundreds of corporate accounts. They reviewing hundreds of corporate accounts. They grew more reliant on internal controls.grew more reliant on internal controls.

The The Journal of Forensic AccountingJournal of Forensic Accounting was created. was created.(continued on next slide)(continued on next slide)

Chapter 1 Forensic and Investigative Accounting 19

Accountant’s Role in Fraud DetectionAccountant’s Role in Fraud Detection Top executives were able to circumvent internal Top executives were able to circumvent internal

controls and manipulate the records.controls and manipulate the records. This lead to situations such as Enron, WorldCom, This lead to situations such as Enron, WorldCom,

Xerox, Adelphia Communication, and the fall of Xerox, Adelphia Communication, and the fall of Arthur Andersen in the early 2000s.Arthur Andersen in the early 2000s.

Due to the financial disaster of companies such as Due to the financial disaster of companies such as Enron and WorldCom, there has been an increased Enron and WorldCom, there has been an increased use of forensic techniques in audits and an increase use of forensic techniques in audits and an increase in fees.in fees.

(continued on next slide)(continued on next slide)

Chapter 1 Forensic and Investigative Accounting 20

Accountant’s Role in Fraud DetectionAccountant’s Role in Fraud Detection

Some accounting experts believe that every audit Some accounting experts believe that every audit engagement should include much more skepticism engagement should include much more skepticism and detailed review of transactions.and detailed review of transactions.

Other accounting experts suggest that only special Other accounting experts suggest that only special engagements specifically targeting fraud can engagements specifically targeting fraud can adequately and effectively root out the problem.adequately and effectively root out the problem.

The Big Four and the next two accounting firms The Big Four and the next two accounting firms believe that every public corporation should have believe that every public corporation should have a forensic audit every three years.a forensic audit every three years.

Chapter 1 Forensic and Investigative Accounting 21

Recent EventsRecent EventsEconomic recessions often increase fraud, since executives may engage in more “cooking the books” techniques to improve financial results, and financially strapped employees will steal business funds or commit other types of fraud and abuse. In April 2009, Audit Analytics predicted that 3,589 companies (nearly 25%) will report that their auditors doubt they will continue as going concerns. In 2001, the percentage was only 19.2 percent.1

The Federal Government’s $787 billion economic stimulus and bailout programs will be breeding grounds for fraud, waste, and abuse. Dan Weil estimates that up to $50 billion of the total (or 5 to 10 percent) will be susceptible to fraud. FBI Director Robert Mueller warns of fraud stemming from the stimulus packages.2 There should be much work for forensic accountants.

11 Sarah Johnson, “Auditors: Nearly 25% of Companies May Not Be Going Concerns,” Sarah Johnson, “Auditors: Nearly 25% of Companies May Not Be Going Concerns,” CFOCFO, April 22, , April 22, 2009, 2009, www.cfo.com/article.cfm/13525910/c_2984368/?f=archiveswww.cfo.com/article.cfm/13525910/c_2984368/?f=archives22 Dan Weil, “Expert: Stimulus Fraud May Hit $50 Billion,” Newsmax.com, June 16, 2009, Dan Weil, “Expert: Stimulus Fraud May Hit $50 Billion,” Newsmax.com, June 16, 2009, http://http://mmoneynews.newsmax.com/printTemplate.htmlmmoneynews.newsmax.com/printTemplate.html

Chapter 1 Forensic and Investigative Accounting 22

Big-Six's PositionBig-Six's Position

A forensic audit is akin to a A forensic audit is akin to a police investigationpolice investigation.. All public companies should have a forensic audit on a regular All public companies should have a forensic audit on a regular

basis. Companies would be required to have such an audit basis. Companies would be required to have such an audit every every three or five yearsthree or five years or face these audits on a random or face these audits on a random basis.basis.

Forensic auditors scrutinize Forensic auditors scrutinize anyany records of companies, records of companies, including emails, and would be able, if not required, to including emails, and would be able, if not required, to question all company employees, and to require statements question all company employees, and to require statements under oath.under oath.

Might be necessary for an Might be necessary for an audit networkaudit network or a specialized or a specialized forensic auditors to complete a forensic audit with the forensic auditors to complete a forensic audit with the aid of aid of independent attorneysindependent attorneys (not those who have represented the (not those who have represented the audit client in the other engagements).audit client in the other engagements).

Source: “Serving Global Markets and the Global Economy: A View from the CEOs of the Source: “Serving Global Markets and the Global Economy: A View from the CEOs of the International Audit Networks, November 2006, p. 13.International Audit Networks, November 2006, p. 13.

Chapter 1 Forensic and Investigative Accounting 23

More DifferencesMore DifferencesTwo practitioners have suggested these additional procedures may Two practitioners have suggested these additional procedures may be used in a forensic audit:be used in a forensic audit:

Extensive use of Extensive use of interviews interviews and leveraging techniques and leveraging techniques designed to elicit sufficient information to prove or designed to elicit sufficient information to prove or disprove a hypothesis.disprove a hypothesis.

Document Document inspection inspection that may extend to authentication that may extend to authentication procedures and handwriting analysis.procedures and handwriting analysis.

Significant Significant public recordspublic records search to uncover, for search to uncover, for example, unexpected title or ownership, other known example, unexpected title or ownership, other known addresses, and prior records of individuals.addresses, and prior records of individuals.

Legal knowledge regarding Legal knowledge regarding rules of evidencerules of evidence including including chain of custody and preservation of evidence integrity.chain of custody and preservation of evidence integrity.

Source: Annett Stalker and M.G. Ueltzen, “An Audit Versus A Fraud Examination,” CPA Expert, Winter 2009, p. 4.

Chapter 1 Forensic and Investigative Accounting 24

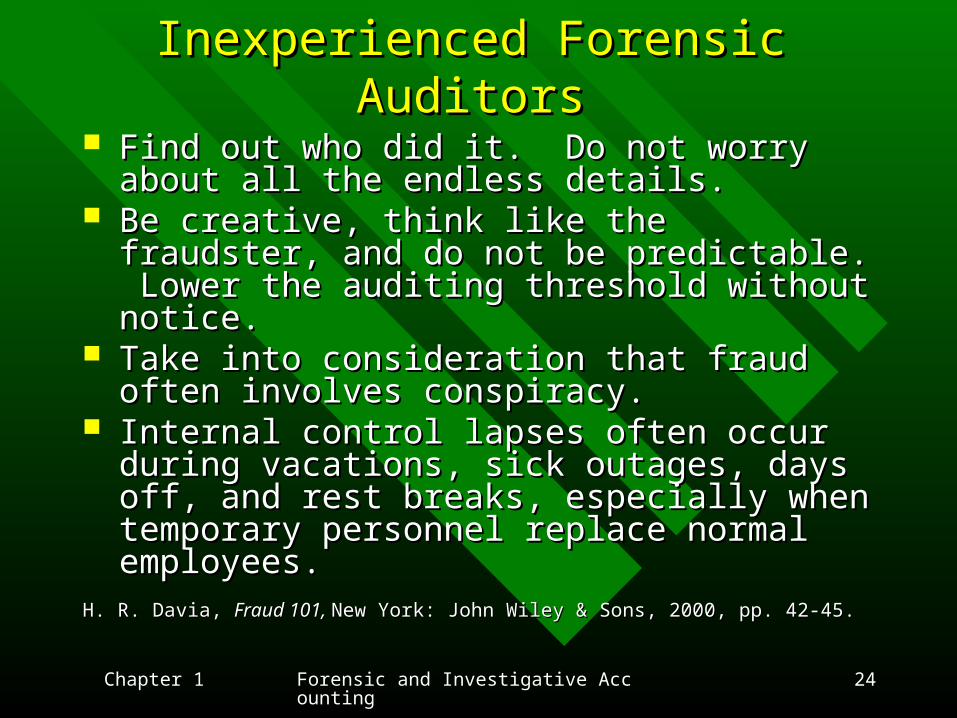

Inexperienced Forensic AuditorsInexperienced Forensic Auditors

Find out who did it. Do not worry about all the Find out who did it. Do not worry about all the endless details.endless details.

Be creative, think like the fraudster, and do not be Be creative, think like the fraudster, and do not be predictable. Lower the auditing threshold without predictable. Lower the auditing threshold without notice.notice.

Take into consideration that fraud often involves Take into consideration that fraud often involves conspiracy.conspiracy.

Internal control lapses often occur during Internal control lapses often occur during vacations, sick outages, days off, and rest breaks, vacations, sick outages, days off, and rest breaks, especially when temporary personnel replace especially when temporary personnel replace normal employees.normal employees.

H. R. Davia, H. R. Davia, Fraud 101, Fraud 101, New York: John Wiley & Sons, 2000, pp. 42-45.New York: John Wiley & Sons, 2000, pp. 42-45.

Chapter 1 Forensic and Investigative Accounting 25

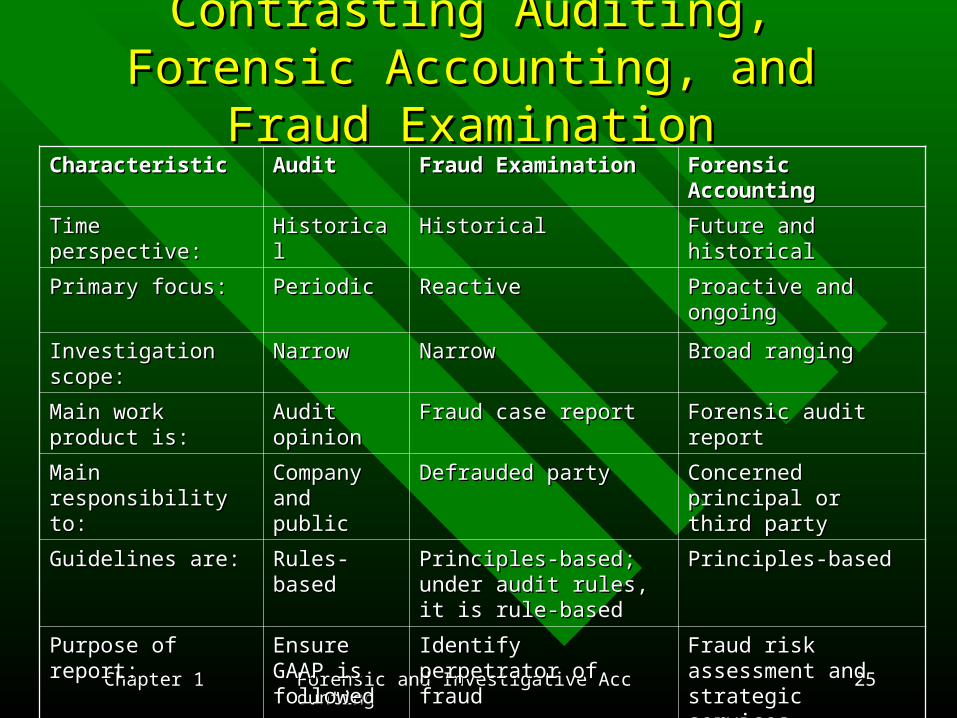

Contrasting Auditing, Forensic Contrasting Auditing, Forensic Accounting, and Fraud ExaminationAccounting, and Fraud Examination

CharacteristicCharacteristic AuditAudit Fraud ExaminationFraud Examination Forensic AccountingForensic Accounting

Time perspective:Time perspective: HistoricalHistorical HistoricalHistorical Future and historicalFuture and historical

Primary focus:Primary focus: PeriodicPeriodic ReactiveReactive Proactive and ongoingProactive and ongoing

Investigation scope:Investigation scope: NarrowNarrow NarrowNarrow Broad rangingBroad ranging

Main work product is:Main work product is: Audit opinionAudit opinion Fraud case reportFraud case report Forensic audit reportForensic audit report

Main responsibility to:Main responsibility to: Company and Company and publicpublic

Defrauded partyDefrauded party Concerned principal or Concerned principal or third partythird party

Guidelines are:Guidelines are: Rules-basedRules-based Principles-based; under audit Principles-based; under audit rules, it is rule-basedrules, it is rule-based

Principles-basedPrinciples-based

Purpose of report:Purpose of report: Ensure GAAP Ensure GAAP is followedis followed

Identify perpetrator of fraudIdentify perpetrator of fraud Fraud risk assessment and Fraud risk assessment and strategic servicesstrategic services

Professional stance:Professional stance: Non-Non-adversarialadversarial

AdversarialAdversarial Adversarial and non-Adversarial and non-adversarialadversarial

Chapter 1 Forensic and Investigative Accounting 26

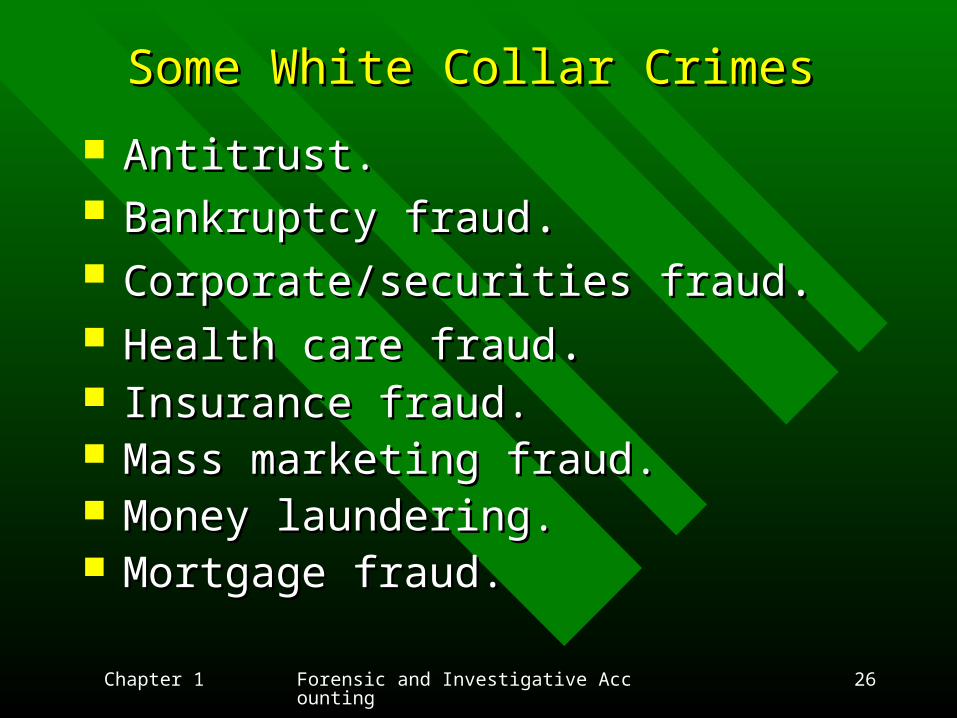

Some White Collar CrimesSome White Collar Crimes

Antitrust.Antitrust. Bankruptcy fraudBankruptcy fraud.. Corporate/securities fraudCorporate/securities fraud.. Health care fraudHealth care fraud.. Insurance fraud.Insurance fraud. Mass marketing fraud.Mass marketing fraud. Money laundering.Money laundering. Mortgage fraud.Mortgage fraud.

Chapter 1 Forensic and Investigative Accounting 27

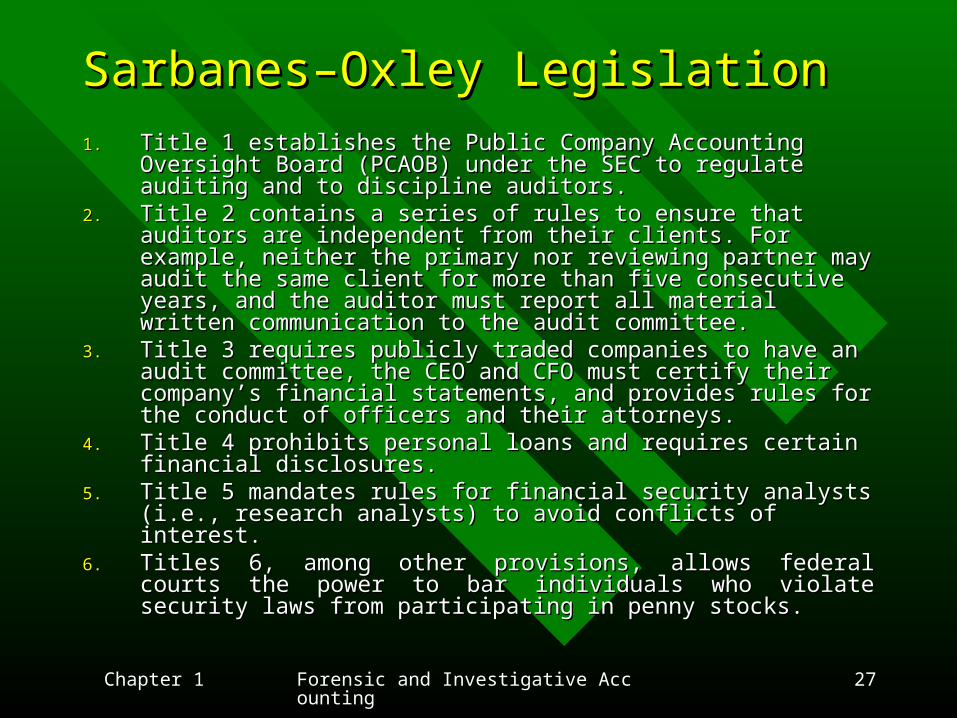

Sarbanes–Oxley LegislationSarbanes–Oxley Legislation 1.1. Title 1 establishes the Public Company Accounting Oversight Board Title 1 establishes the Public Company Accounting Oversight Board

(PCAOB) under the SEC to regulate auditing and to discipline auditors.(PCAOB) under the SEC to regulate auditing and to discipline auditors.2.2. Title 2 contains a series of rules to ensure that auditors are independent Title 2 contains a series of rules to ensure that auditors are independent

from their clients. For example, neither the primary nor reviewing from their clients. For example, neither the primary nor reviewing partner may audit the same client for more than five consecutive years, partner may audit the same client for more than five consecutive years, and the auditor must report all material written communication to the and the auditor must report all material written communication to the audit committee. audit committee.

3.3. Title 3 requires publicly traded companies to have an audit committee, Title 3 requires publicly traded companies to have an audit committee, the CEO and CFO must certify their company’s financial statements, the CEO and CFO must certify their company’s financial statements, and provides rules for the conduct of officers and their attorneys.and provides rules for the conduct of officers and their attorneys.

4.4. Title 4 prohibits personal loans and requires certain financial Title 4 prohibits personal loans and requires certain financial disclosures.disclosures.

5.5. Title 5 mandates rules for financial security analysts (i.e., research Title 5 mandates rules for financial security analysts (i.e., research analysts) to avoid conflicts of interest. analysts) to avoid conflicts of interest.

6.6. Titles 6, among other provisions, allows federal courts the power to bar Titles 6, among other provisions, allows federal courts the power to bar individuals who violate security laws from participating in penny individuals who violate security laws from participating in penny stocks.stocks.

Chapter 1 Forensic and Investigative Accounting 28

Sarbanes–Oxley LegislationSarbanes–Oxley Legislation 7.7. Title 7 requires reports and studies on consolidation of accounting Title 7 requires reports and studies on consolidation of accounting

firms, credit rating agencies, enforcement actions, and investment firms, credit rating agencies, enforcement actions, and investment banks.banks.

8.8. Title 8 provides protection for whistleblowers and mandates penalties Title 8 provides protection for whistleblowers and mandates penalties and fines for certain acts not dischargeable by bankruptcy. For and fines for certain acts not dischargeable by bankruptcy. For example, failure of an auditor to keep working papers for 5 years is example, failure of an auditor to keep working papers for 5 years is subject to fines and 10 years in prison, and fine or imprisonment of up subject to fines and 10 years in prison, and fine or imprisonment of up to 25 years for anyone knowingly defrauding shareholders of publicly to 25 years for anyone knowingly defrauding shareholders of publicly traded companies. A person can receive 20 years in prison and fines for traded companies. A person can receive 20 years in prison and fines for altering, destroying, mutilating, concealing, covering up, falsifying or altering, destroying, mutilating, concealing, covering up, falsifying or making a false entry in any record, document, or tangible object.making a false entry in any record, document, or tangible object.

9.9. Title 9 increases maximum prison sentences for mail and wire fraud Title 9 increases maximum prison sentences for mail and wire fraud from 5 to 20 years. Willfully and knowingly certifying financial reports from 5 to 20 years. Willfully and knowingly certifying financial reports not in compliance with the Act is now a criminal offense.not in compliance with the Act is now a criminal offense.

10.10. Title 10 says that it is the “Sense of the Senate” to require the CEO to Title 10 says that it is the “Sense of the Senate” to require the CEO to sign the corporate tax return.sign the corporate tax return.

11.11. Title 11 provides a possible 20-year prison sentence for anyone Title 11 provides a possible 20-year prison sentence for anyone altering, destroying, mutilating, or concealing a record, document, or altering, destroying, mutilating, or concealing a record, document, or other object (or otherwise impeding) for an official proceeding.other object (or otherwise impeding) for an official proceeding.

Related Documents