26-1 Monoline Dwelling Forms Dwelling Property 1 Basic Form DP 00 01 Dwelling Property 2 Broad Form DP 00 02 Dwelling Property 3 Special Form DP 00 03

26-1 Monoline Dwelling Forms Dwelling Property 1 Basic FormDP 00 01 Dwelling Property 2 Broad FormDP 00 02 Dwelling Property 3 Special FormDP 00 03.

Dec 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

26-1

Monoline Dwelling Forms

Dwelling Property 1 Basic Form DP 00 01

Dwelling Property 2 Broad Form DP 00 02

Dwelling Property 3 Special Form DP 00 03

26-2

Coverage Under Dwelling Program

A - Dwelling

B - Other structures

C - Personal property

D - Rental value

E - Additional living expense

26-3

Differences: Homeowners and Dwelling Forms

Monoline dwelling forms1. do not include coverage for theft. 2. do not include coverage for personal liability. 3. limit coverage on property away from premises to

10% of on-premises limit.4. exclude boats (other than rowboats and canoes).5. do not cover money or valuable papers.6. do not impose dollar limits on money, watercraft,

trailers, jewelry, firearms or silverware.

Theft and personal liability coverage by endorsement

26-4

The Mobilehome Policy Program

1. ISO program introduced in 1984

• mobilehome Endorsement MH 04 01

• used with H0 00 02 or H0 00 03

26-5

The Mobilehome Policy Program

2. Coverage on Mobile Home

• coverage A includes utility tanks attached to mobilehome

• all built-ins

• loss settlement provision provides for appearance damage

26-6

The Mobilehome Policy Program

3. Coverage on Personal Property

• standard amount of contents coverage is 40% of Coverage A

• rationale is that many normal contents items are “built-in” to mobilehomes

26-7

Mobilehome Policy Program

Other Coverage Features

1. Personal Property Removal coverage pays for expense of moving the mobile home to protect it from insured perils. $500 limit which may be increased to $2,500.

2. Transportation/Moving endorsement (30 days collision coverage while trailer is in transit).

3. Lienholders single interest (collision, conversion, embezzlement).

26-8

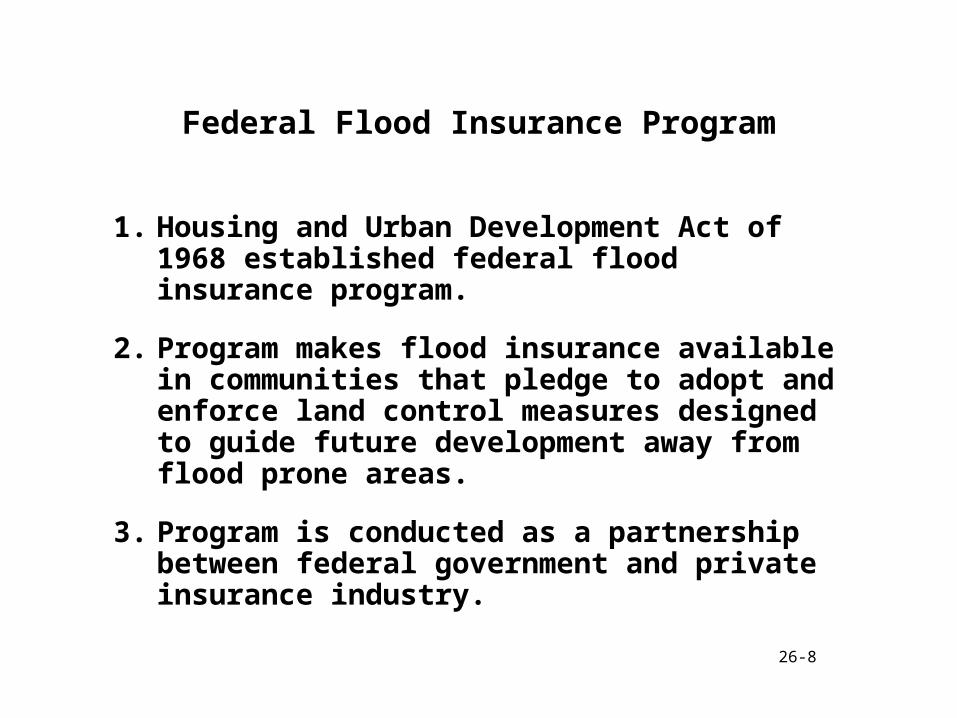

Federal Flood Insurance Program

1. Housing and Urban Development Act of 1968 established federal flood insurance program.

2. Program makes flood insurance available in communities that pledge to adopt and enforce land control measures designed to guide future development away from flood prone areas.

3. Program is conducted as a partnership between federal government and private insurance industry.

26-9

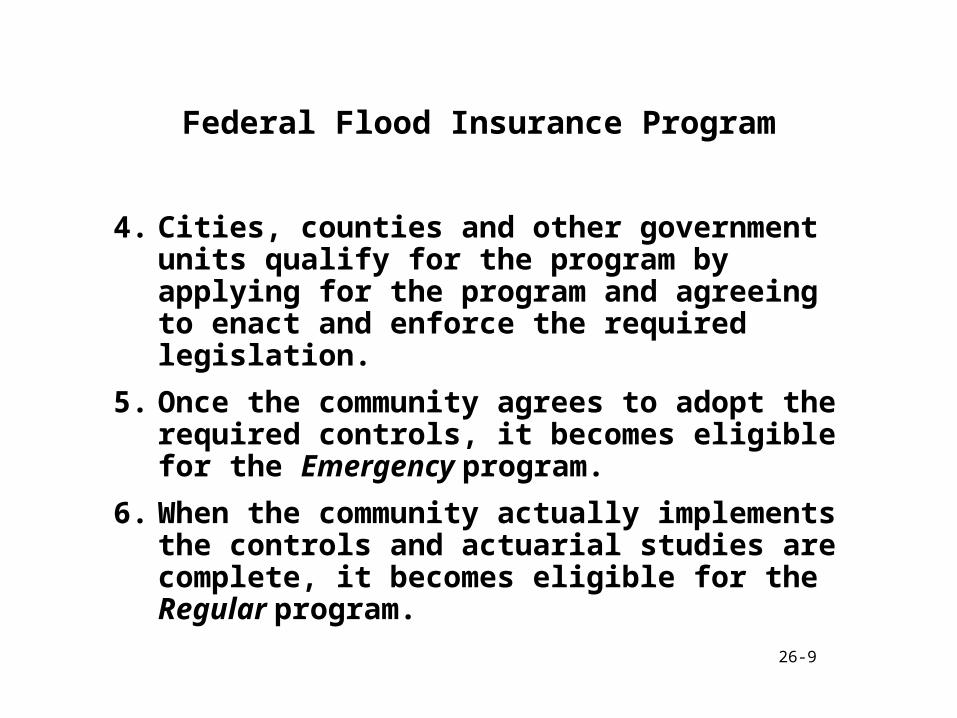

Federal Flood Insurance Program

4. Cities, counties and other government units qualify for the program by applying for the program and agreeing to enact and enforce the required legislation.

5. Once the community agrees to adopt the required controls, it becomes eligible for the Emergency program.

6. When the community actually implements the controls and actuarial studies are complete, it becomes eligible for the Regular program.

26-10

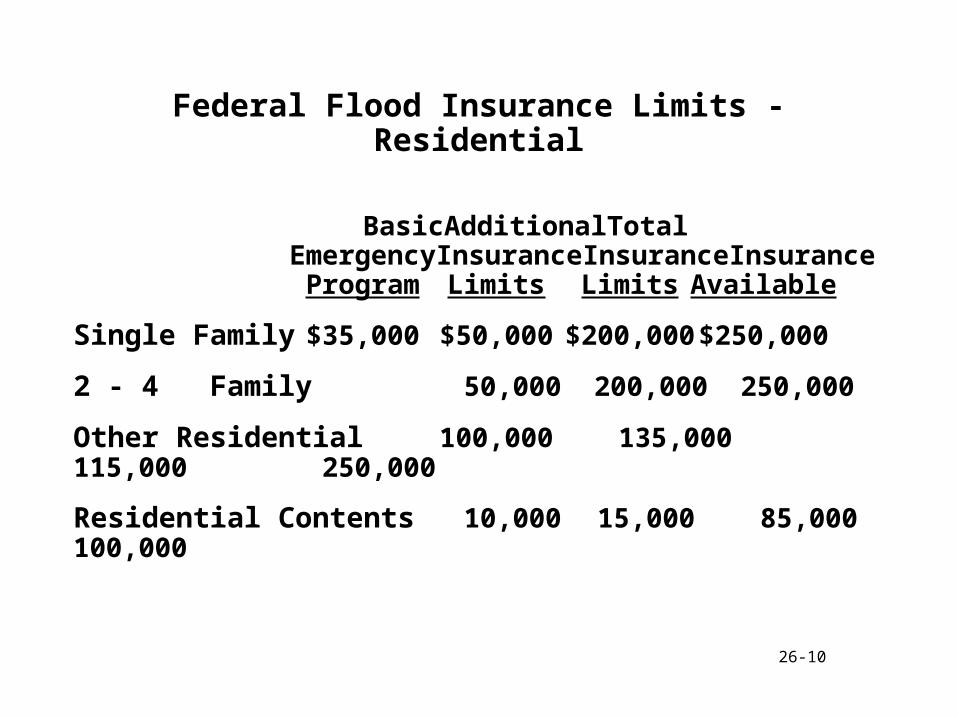

Federal Flood Insurance Limits - Residential

Basic Additional TotalEmergency Insurance Insurance Insurance

Program Limits Limits Available

Single Family $35,000 $50,000 $200,000 $250,000

2 - 4 Family 50,000 200,000 250,000

Other Residential 100,000 135,000 115,000 250,000

Residential Contents 10,000 15,000 85,000 100,000

26-11

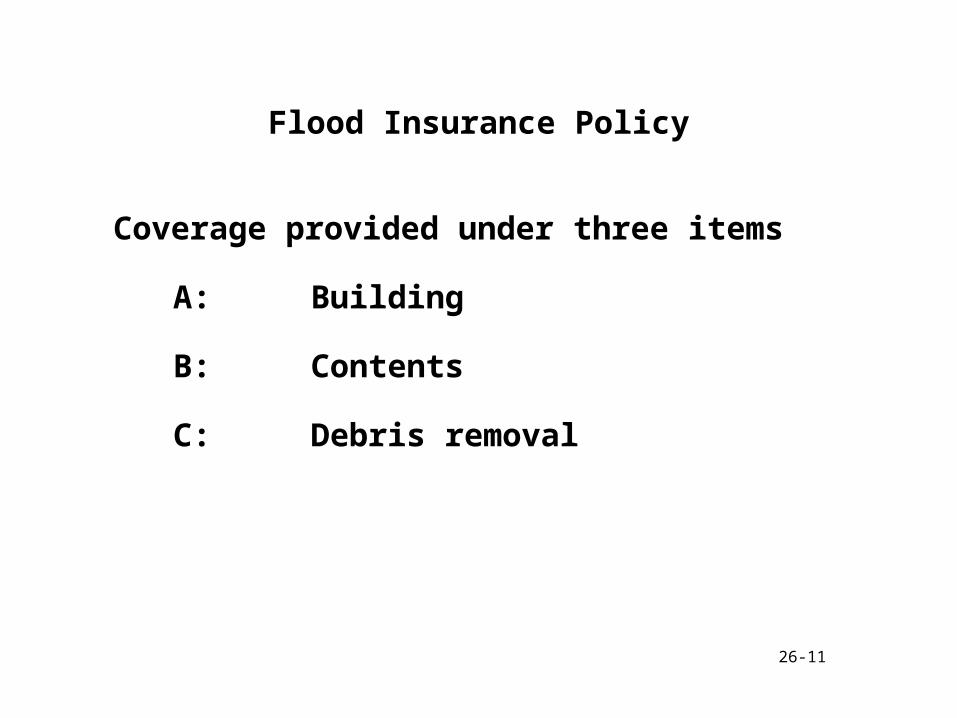

Flood Insurance Policy

Coverage provided under three items

A: Building

B: Contents

C: Debris removal

26-12

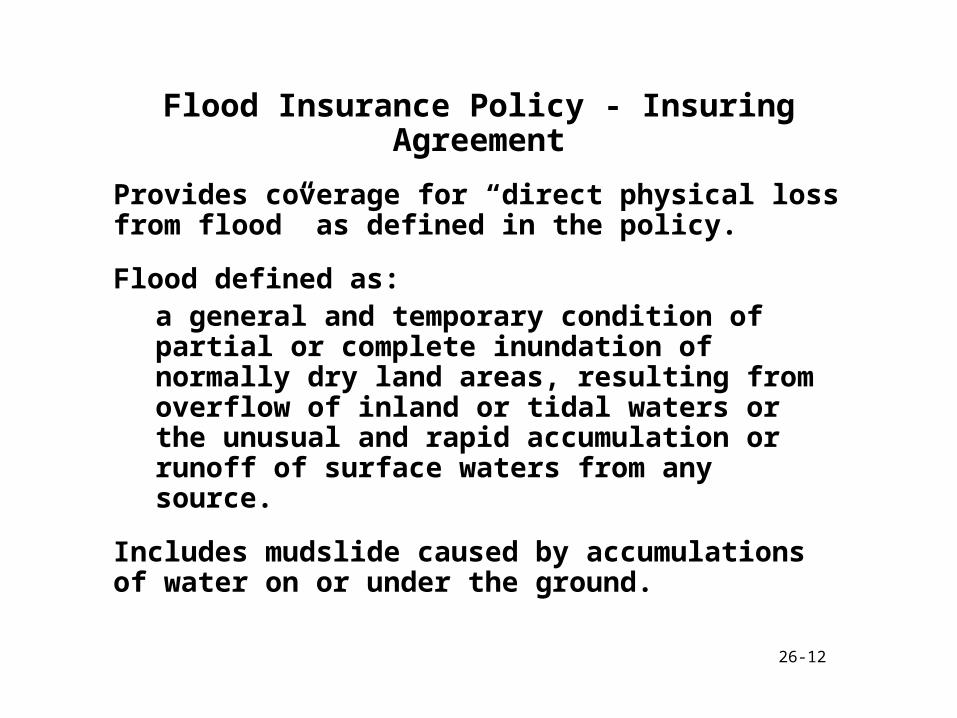

Flood Insurance Policy - Insuring Agreement

Provides coverage for “direct physical loss from flood” as defined in the policy.

Flood defined as:a general and temporary condition of partial or complete inundation of normally dry land areas, resulting from overflow of inland or tidal waters or the unusual and rapid accumulation or runoff of surface waters from any source.

Includes mudslide caused by accumulations of water on or under the ground.

26-13

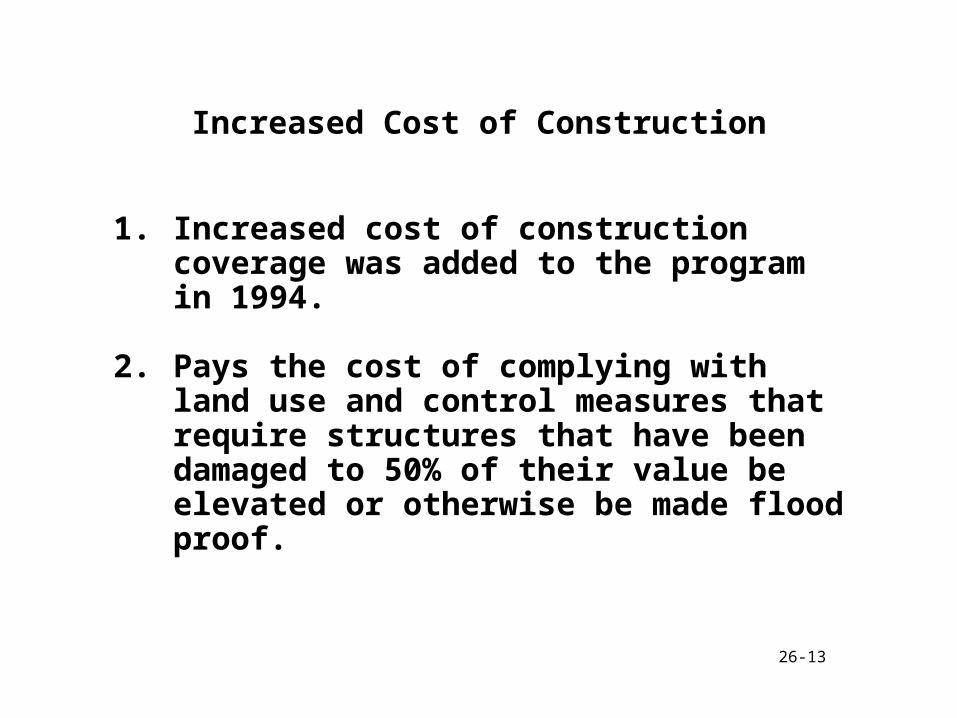

Increased Cost of Construction

1. Increased cost of construction coverage was added to the program in 1994.

2. Pays the cost of complying with land use and control measures that require structures that have been damaged to 50% of their value be elevated or otherwise be made flood proof.

26-14

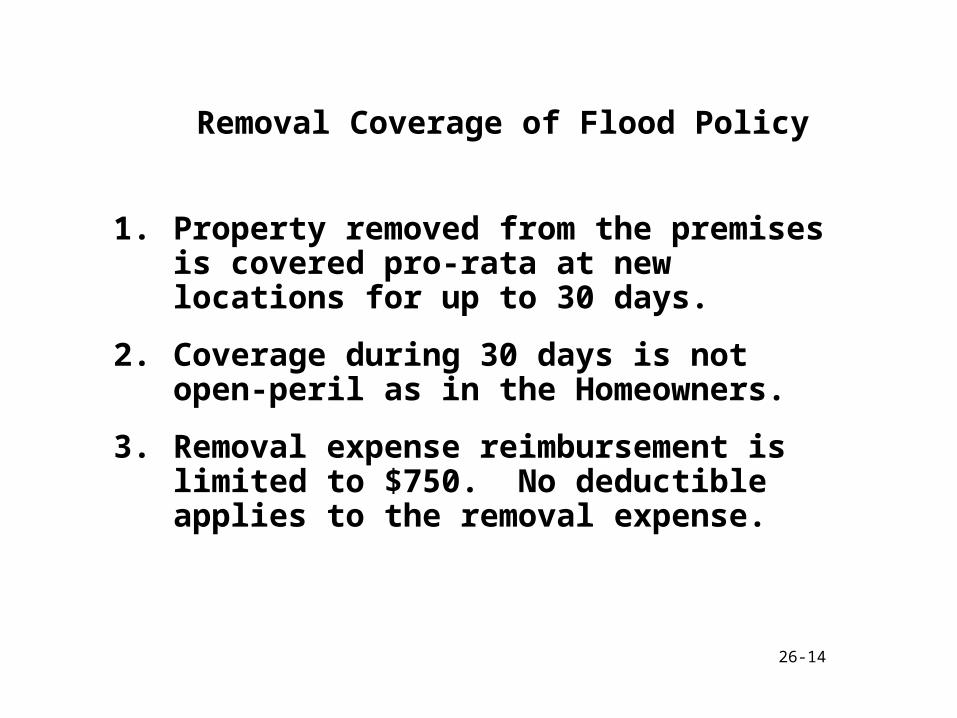

Removal Coverage of Flood Policy

1. Property removed from the premises is covered pro-rata at new locations for up to 30 days.

2. Coverage during 30 days is not open-peril as in the Homeowners.

3. Removal expense reimbursement is limited to $750. No deductible applies to the removal expense.

26-15

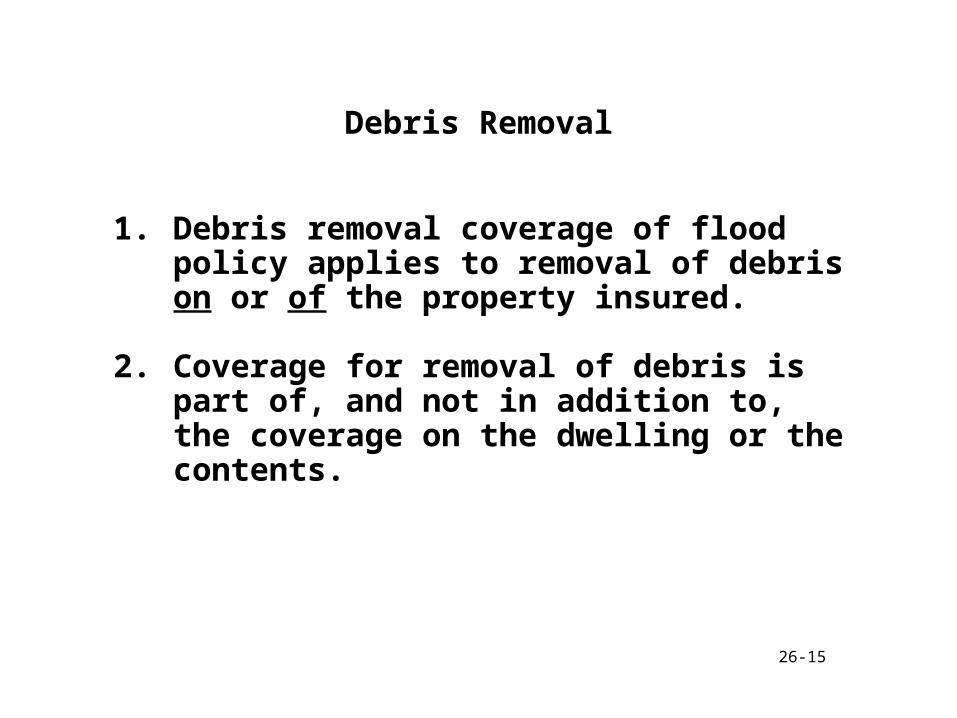

Debris Removal

1. Debris removal coverage of flood policy applies to removal of debris on or of the property insured.

2. Coverage for removal of debris is part of, and not in addition to, the coverage on the dwelling or the contents.

26-16

Flood Insurance Policy - Inception

1. 30 day waiting period after application and payment of premium, subject to two exceptions

2. Waiting period does not apply

• to the initial purchase of flood insurance in connection with making, increasing, extending or renewing a loan

• in first 13 months after revision or update of a Flood Insurance Rate Map

26-17

Flood Insurance Policy - Termination

1. Insurer may cancel only for nonpayment of premium, 20 days

2. Insured may cancel anytime, premium fully earned if insured retains title to the property

26-18

Scheduled Personal Property Endorsement

1. Personal fur floater

2. Personal jewelry floater

3. Silverware floater

4. Golfers equipment

5. Camera floater

6. Fine arts and antiques

7. Stamp and coin collections

8. Musical instruments

26-19

Boatowners Policy

Section I Physical Damage

Section II Liability Coverages

26-20

Boatowners Policy

Section I Physical Damage Coverages

1. The motor(s) described in the declarations, including remote controls and batteries

2. The boat described in the declarations, including its permanently attached equipment

3. The trailer described in the declarations if designed for the transportation of the boat

4. Equipment and accessories manufactured for marine use

26-21

Boatowners Policy

Section II: Liability Coverages

A: Watercraft Liability

B: Medical Payments

C: Uninsured Boaters

26-22

Buying Property Insurance for the Individual

1. Cost difference between HO-2 and HO-3 is so slight that HO-3 is obviously choice.

2. Dwelling should be insured for 100% of its replacement cost.

3. Coverage on contents should be increased from the standard 50% when there is a need.

4. Consider scheduling valuable jewelry, furs, guns, cameras and similar property.

5. Earthquake and flood insurance should be added to complete coverage.

26-23

Title Insurance

1. Legal principles involved in transfer of property complicated.

2. Possibility exists that a title may be defective.

3. Title insurance policy compensates insured for financial loss.

4. Policy relates to occurrences in the past rather than the future.

26-24

The Torrens System

1. Title is vested in the purchaser of the property.

2. Claimants are reimbursed out of the Torrens fund.

Related Documents