Job Order Costing

1611 Job Order Costing

Dec 20, 2015

kjh

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Job Order Costing

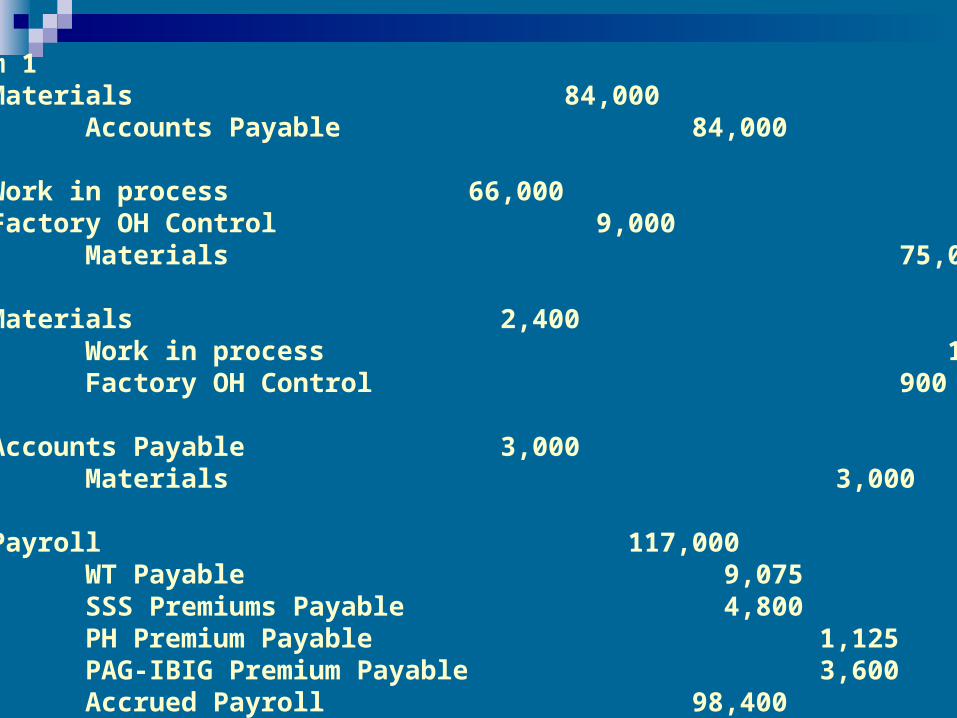

Problem 11. Materials 84,000

Accounts Payable 84,000

2. Work in process 66,000Factory OH Control 9,000

Materials 75,000

3. Materials 2,400Work in process 1,500Factory OH Control 900

4. Accounts Payable 3,000Materials 3,000

5. Payroll 117,000WT Payable 9,075SSS Premiums Payable 4,800PH Premium Payable 1,125PAG-IBIG Premium Payable 3,600Accrued Payroll 98,400

Accrued Payroll 98,400Cash 98,400

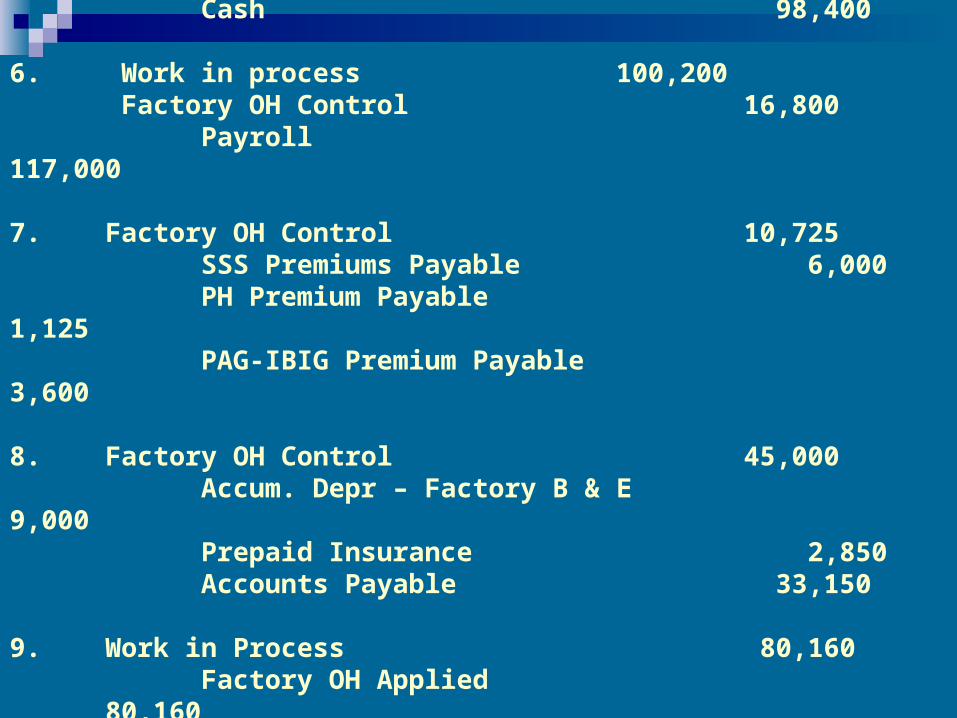

6. Work in process 100,200 Factory OH Control 16,800

Payroll 117,000

7. Factory OH Control 10,725SSS Premiums Payable 6,000PH Premium Payable

1,125PAG-IBIG Premium Payable

3,600

8. Factory OH Control 45,000Accum. Depr – Factory B & E

9,000Prepaid Insurance 2,850Accounts Payable 33,150

9. Work in Process 80,160Factory OH Applied

80,160100,200 x 80%

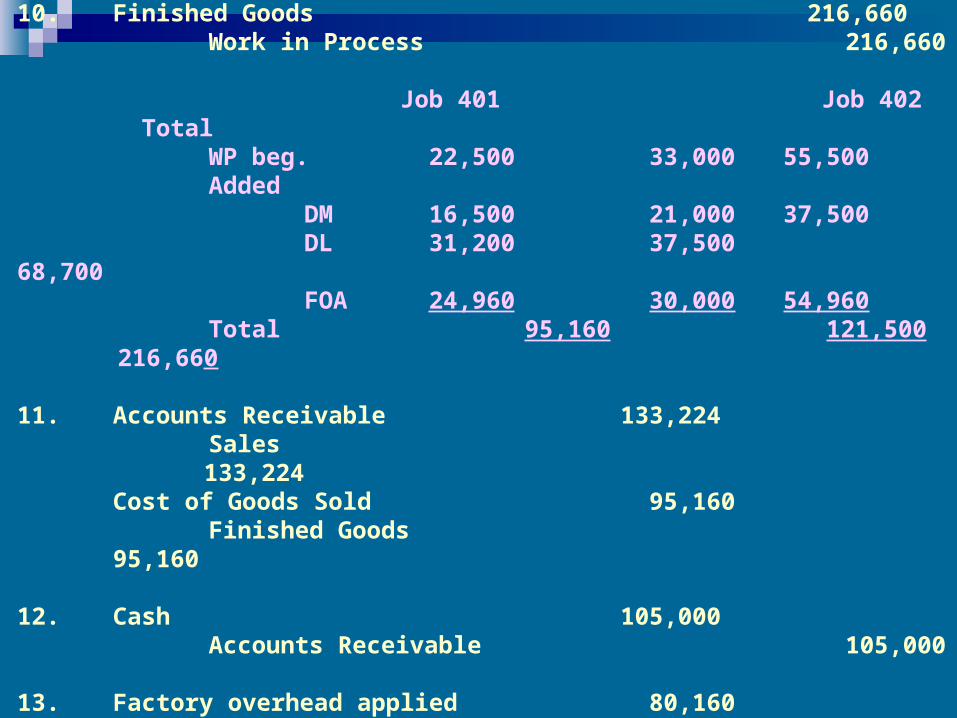

10. Finished Goods 216,660Work in Process 216,660

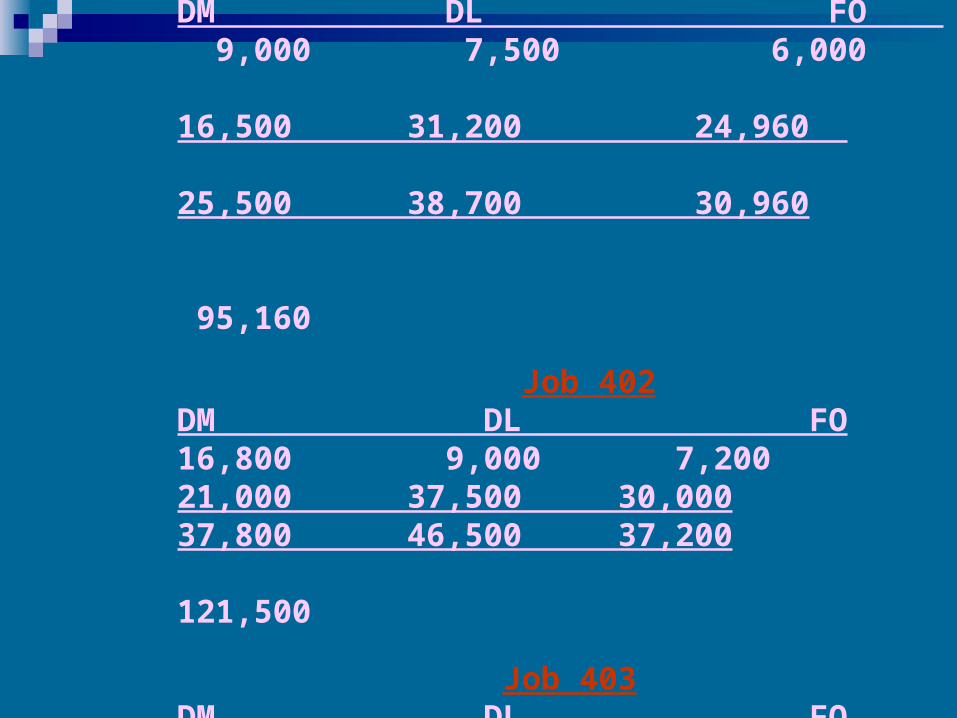

Job 401 Job 402 Total

WP beg. 22,500 33,000 55,500Added

DM 16,500 21,000 37,500DL 31,200 37,500 68,700FOA 24,960 30,000 54,960

Total 95,160 121,500 216,660

11. Accounts Receivable 133,224Sales 133,224

Cost of Goods Sold 95,160Finished Goods

95,160

12. Cash 105,000Accounts Receivable 105,000

13. Factory overhead applied 80,160Cost of Good sold 465

Factory overhead control 80,625

Job 401 DM DL FO 9,000 7,500 6,000 16,500 31,200 24,960 25,500 38,700 30,960 95,160

Job 402DM DL FO16,800 9,000 7,20021,000 37,500 30,00037,800 46,500 37,200 121,500

Job 403DM DL FO28,500 31,500 25,200 83,700( 1,500)

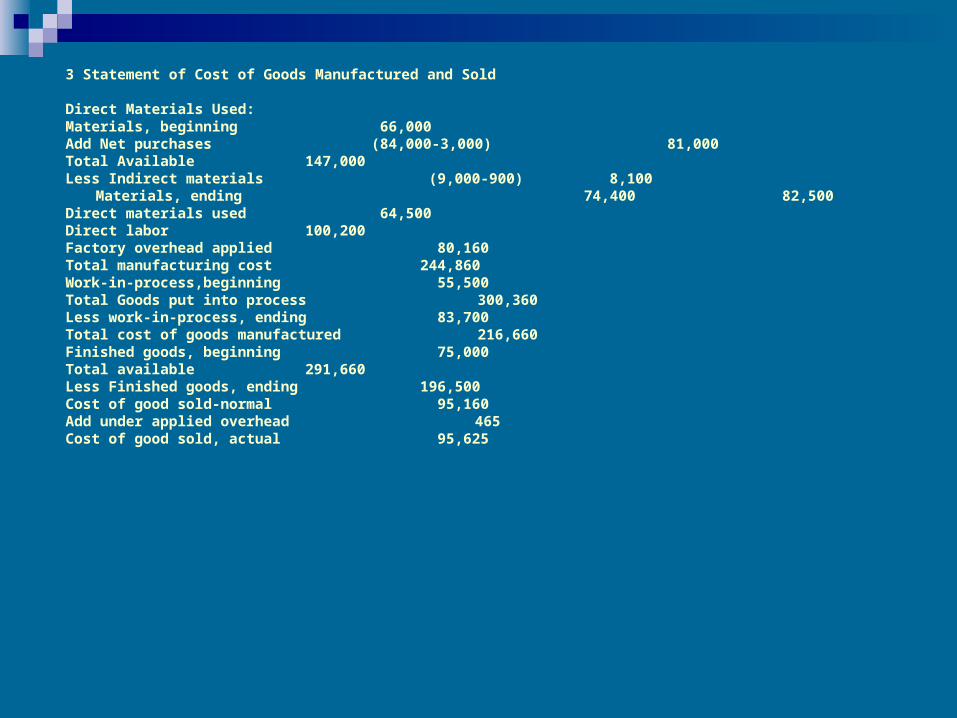

3 Statement of Cost of Goods Manufactured and Sold

Direct Materials Used: Materials, beginning 66,000Add Net purchases (84,000-3,000) 81,000Total Available 147,000Less Indirect materials (9,000-900) 8,100

Materials, ending 74,400 82,500Direct materials used 64,500Direct labor 100,200Factory overhead applied 80,160Total manufacturing cost 244,860Work-in-process,beginning 55,500Total Goods put into process 300,360Less work-in-process, ending 83,700Total cost of goods manufactured 216,660Finished goods, beginning 75,000Total available 291,660Less Finished goods, ending 196,500Cost of good sold-normal 95,160Add under applied overhead 465Cost of good sold, actual 95,625

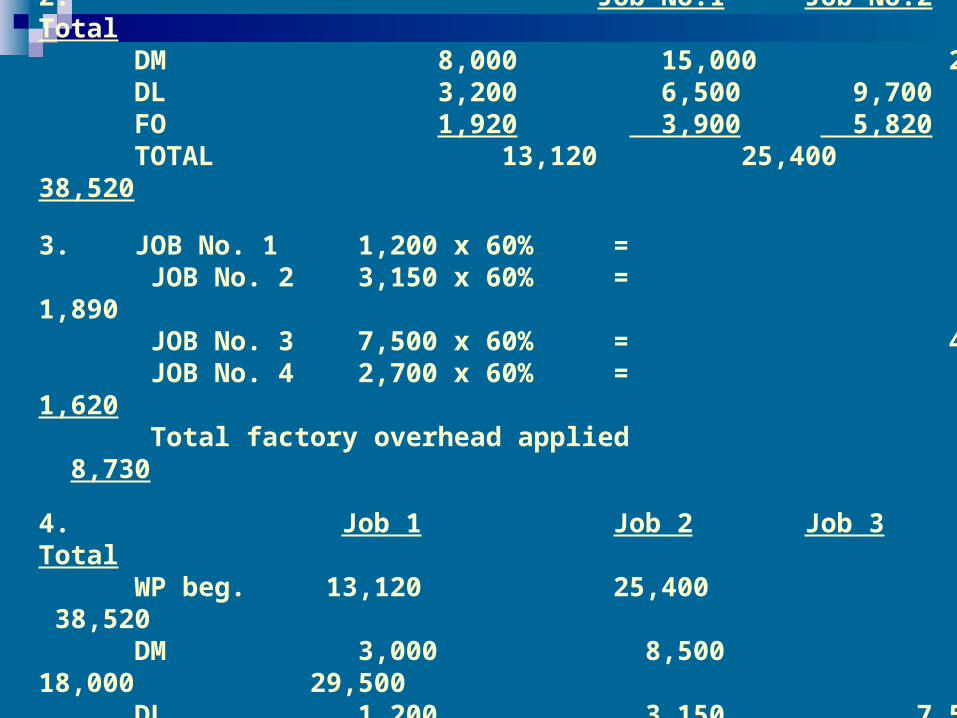

Problem 21. FOH rate = FO 1,920 3,900

DL 3,200 6,500 = 60% of DLC = 60% of DLC

2. Job No.1 Job No.2 TotalDM 8,000 15,000 23,000DL 3,200 6,500 9,700FO 1,920 3,900 5,820TOTAL 13,120 25,400 38,520

3. JOB No. 1 1,200 x 60% = 720 JOB No. 2 3,150 x 60% = 1,890 JOB No. 3 7,500 x 60% = 4,500 JOB No. 4 2,700 x 60% = 1,620 Total factory overhead applied 8,730

4. Job 1 Job 2 Job 3 TotalWP beg. 13,120 25,400

38,520DM 3,000 8,500 18,000 29,500DL 1,200 3,150 7,500

11,850FO 720 1,890 4,500 7,110CofGM 18,040 38,940 30,000 86,980

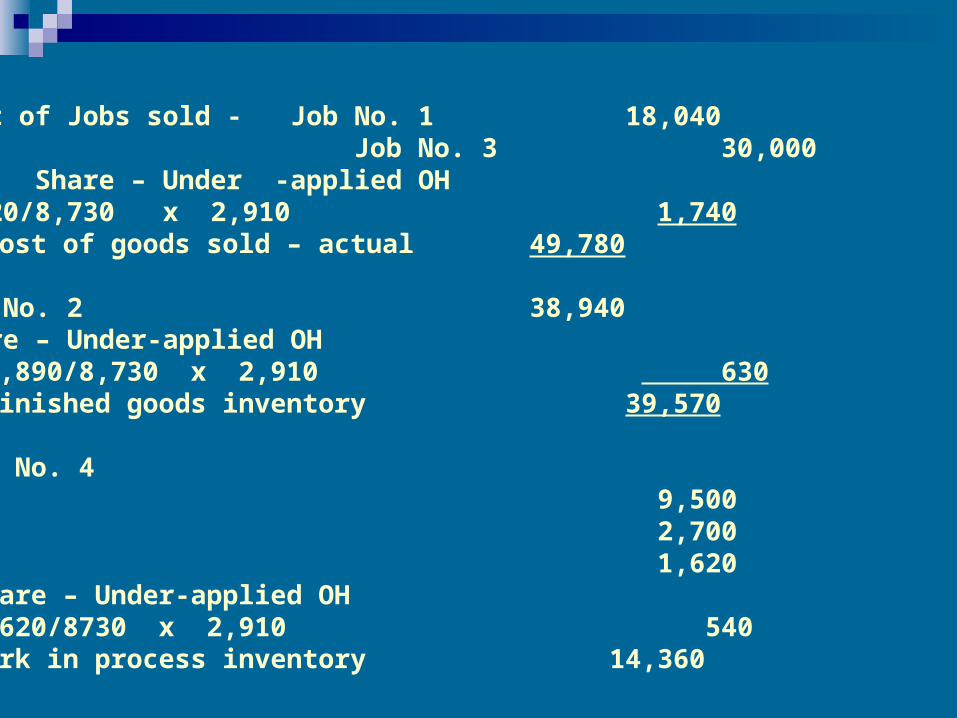

5. Cost of Jobs sold - Job No. 1 18,040 Job No. 3 30,000 Share – Under -applied OH

5,220/8,730 x 2,910 1,740 Cost of goods sold – actual 49,780 6. Job No. 2 38,940

Share – Under-applied OH 1,890/8,730 x 2,910 630 Finished goods inventory 39,570

7. Job No. 4DM 9,500DL 2,700FO 1,620

Share – Under-applied OH 1,620/8730 x 2,910 540 Work in process inventory 14,360

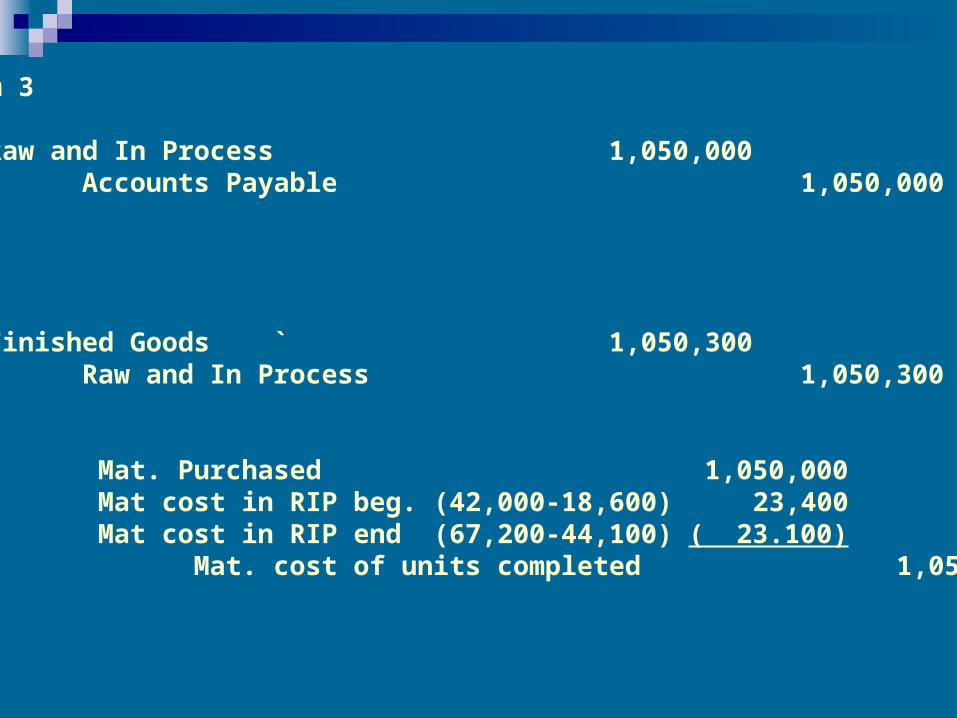

Problem 3

1. Raw and In Process 1,050,000Accounts Payable 1,050,000

2.` Finished Goods ` 1,050,300Raw and In Process 1,050,300

Mat. Purchased 1,050,000 Mat cost in RIP beg. (42,000-18,600) 23,400 Mat cost in RIP end (67,200-44,100) ( 23.100)

Mat. cost of units completed 1,050,300

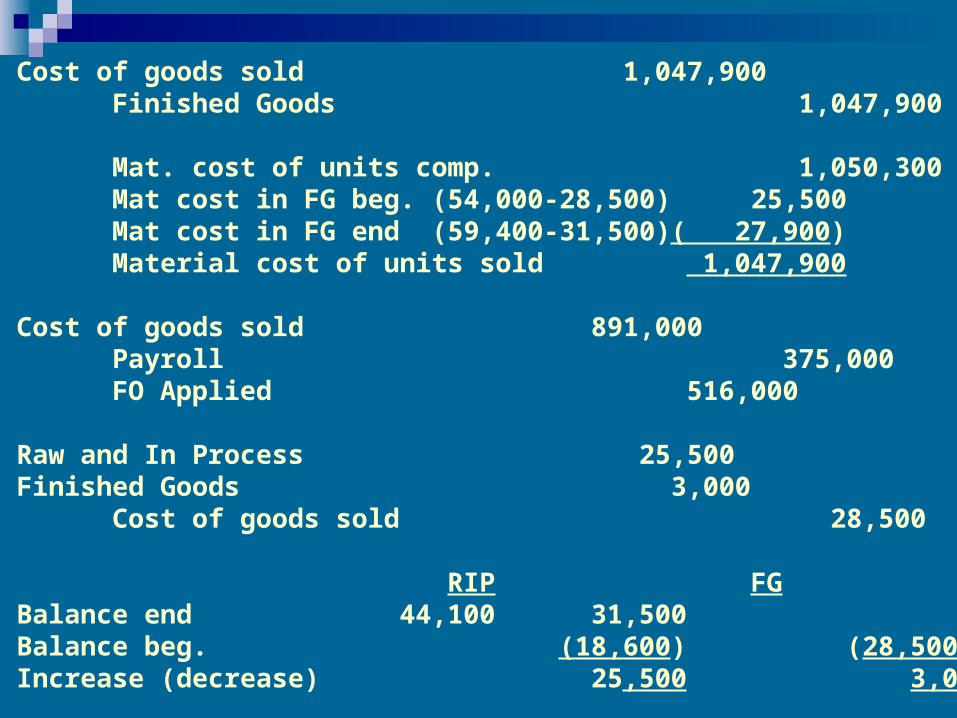

3. Cost of goods sold 1,047,900Finished Goods 1,047,900

Mat. cost of units comp. 1,050,300Mat cost in FG beg. (54,000-28,500) 25,500Mat cost in FG end (59,400-31,500)( 27,900)Material cost of units sold 1,047,900

4. Cost of goods sold 891,000Payroll 375,000FO Applied 516,000

Raw and In Process 25,500Finished Goods 3,000

Cost of goods sold 28,500

RIP FGBalance end 44,100 31,500Balance beg. (18,600) (28,500)Increase (decrease) 25,500 3,000

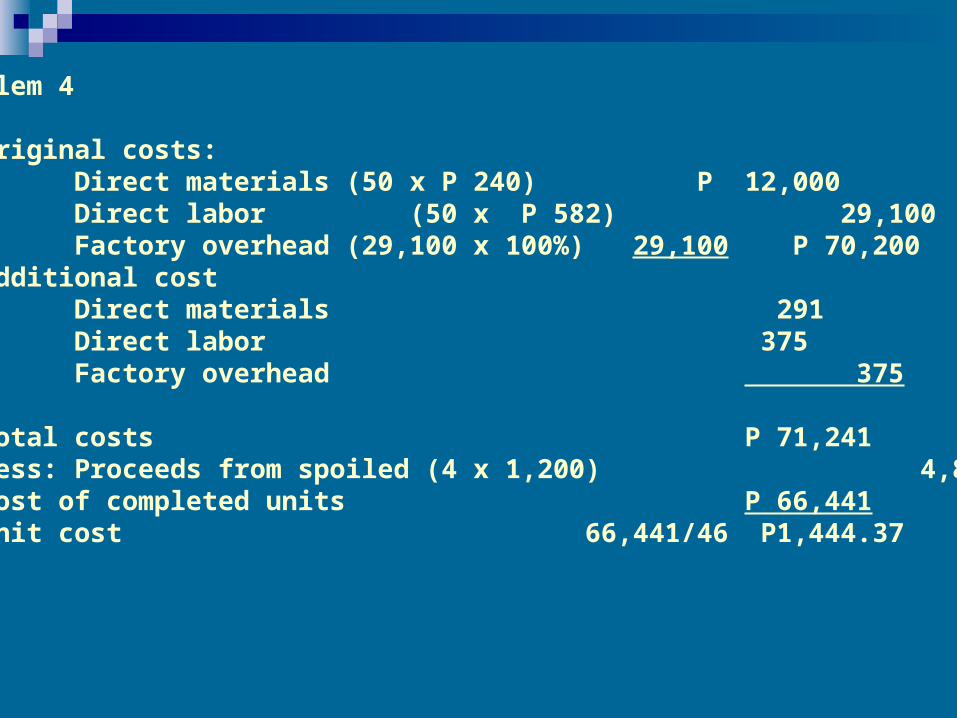

Problem 4

1) Original costs:Direct materials (50 x P 240) P 12,000Direct labor (50 x P 582) 29,100Factory overhead (29,100 x 100%) 29,100 P 70,200

Additional cost Direct materials 291Direct labor 375Factory overhead 375

1,041Total costs P 71,241Less: Proceeds from spoiled (4 x 1,200)

4,800Cost of completed units P 66,441 Unit cost 66,441/46 P1,444.37

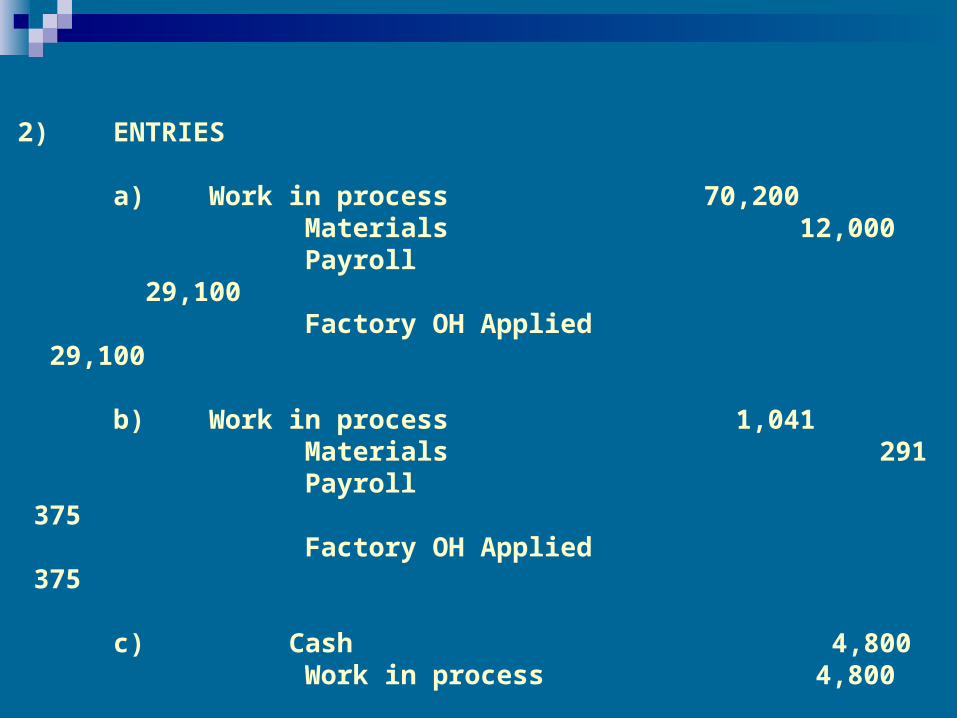

2) ENTRIES

a) Work in process 70,200Materials 12,000Payroll

29,100Factory OH Applied

29,100

b) Work in process 1,041Materials 291Payroll

375Factory OH Applied

375

c) Cash 4,800Work in process 4,800

d) Finished goods 66,441Work-in-process 66,441

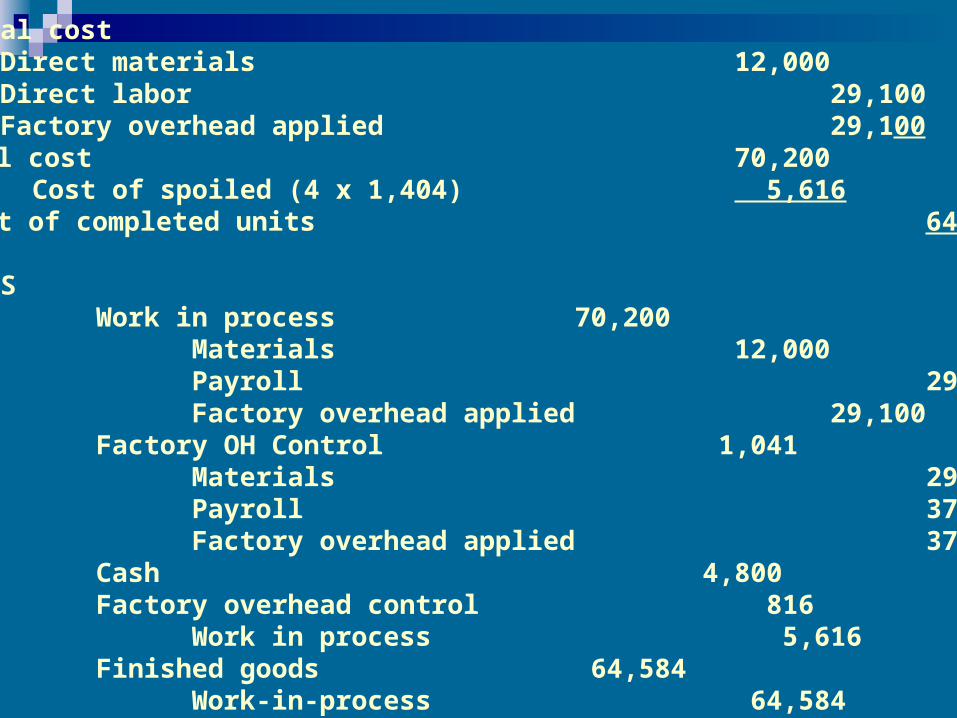

3) Original costDirect materials 12,000Direct labor 29,100Factory overhead applied 29,100

Total cost 70,200 Less: Cost of spoiled (4 x 1,404) 5,616

Cost of completed units 64,584

ENTRIESa) Work in process 70,200

Materials 12,000Payroll 29,100Factory overhead applied 29,100

b) Factory OH Control 1,041Materials 291Payroll 375Factory overhead applied 375

c) Cash 4,800Factory overhead control 816

Work in process 5,616d) Finished goods 64,584

Work-in-process 64,584

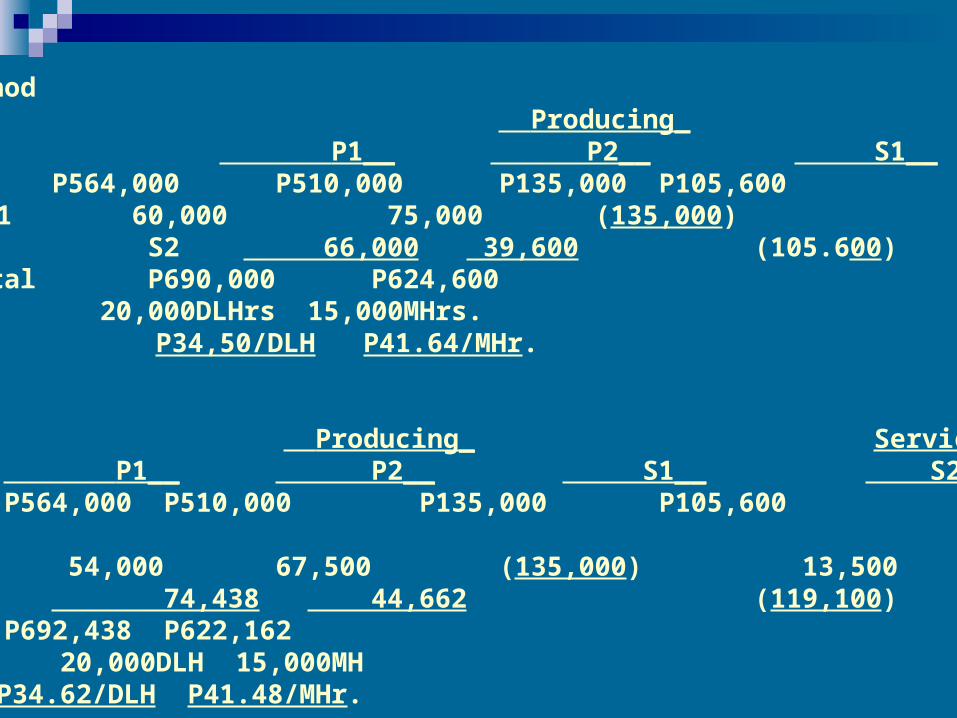

Problem 5 a) Direct method Producing_ Service

P1__ P2__ S1__ S2__Budgeted FO P564,000 P510,000 P135,000 P105,600Allocated S1 60,000 75,000 (135,000)

S2 66,000 39,600 (105.600) Total P690,000 P624,600

Base 20,000DLHrs 15,000MHrs.FO rate P34,50/DLH P41.64/MHr.

b) Step method Producing_ Service

P1__ P2__ S1__ S2__Budgeted FO P564,000 P510,000 P135,000 P105,600

AllocatedS1 54,000 67,500 (135,000) 13,500

S2 74,438 44,662 (119,100)Total P692,438 P622,162Base 20,000DLH 15,000MHFO rate P34.62/DLH P41.48/MHr.

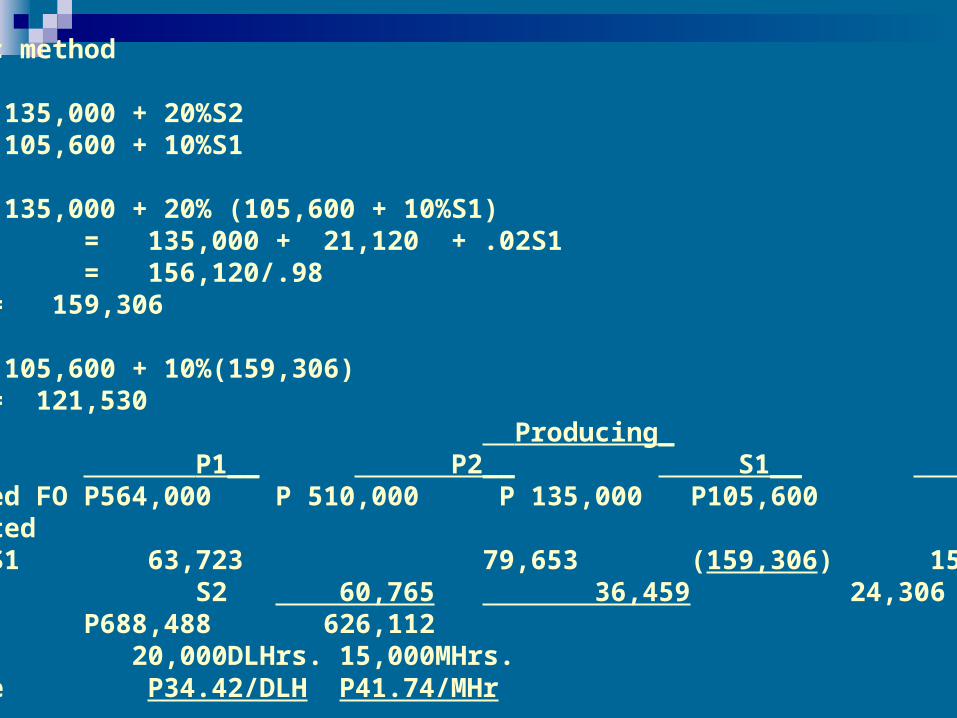

c) Algebraic method

S1 = 135,000 + 20%S2S2 = 105,600 + 10%S1

S1 = 135,000 + 20% (105,600 + 10%S1) = 135,000 + 21,120 + .02S1 = 156,120/.98

= 159,306

S2 = 105,600 + 10%(159,306) = 121,530

Producing_ Service P1__ P2__ S1__ S2__

Budgeted FO P564,000 P 510,000 P 135,000 P105,600Allocated

S1 63,723 79,653 (159,306) 15,930 S2 60,765 36,459 24,306 (121,530)

Total P688,488 626,112Base 20,000DLHrs. 15,000MHrs.FO rate P34.42/DLH P41.74/MHr

Problem 6

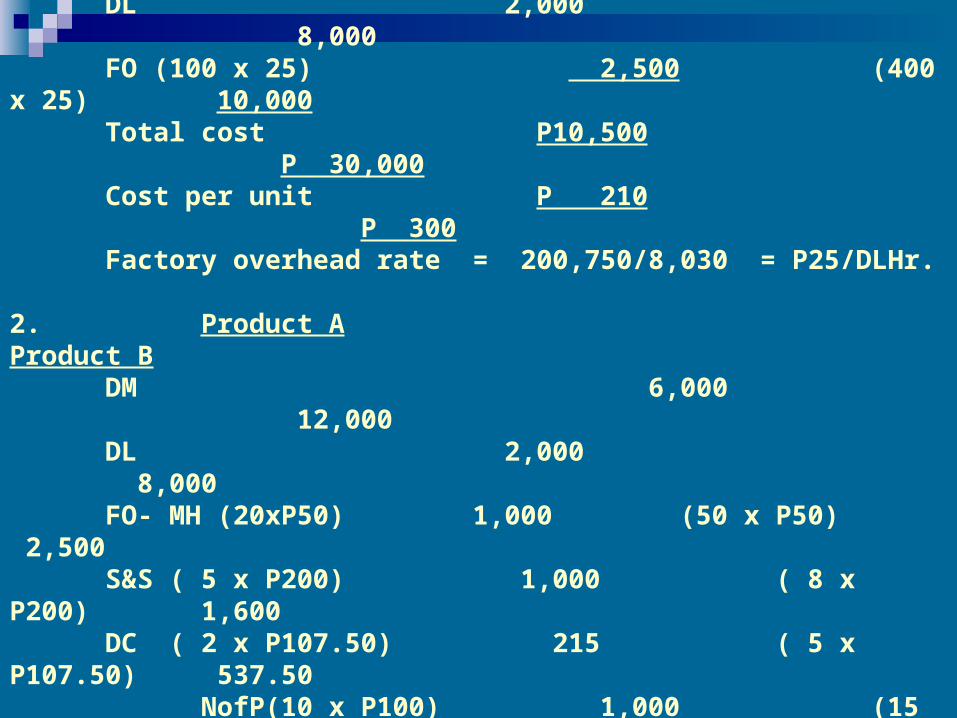

1. Product A Product BDM (50x 120) P 6,000 (100x120) P

12,000DL 2,000

8,000FO (100 x 25) 2,500 (400 x 25)

10,000Total cost P10,500 P

30,000Cost per unit P 210 P

300Factory overhead rate = 200,750/8,030 = P25/DLHr.

2. Product A Product BDM 6,000

12,000DL 2,000

8,000FO- MH (20xP50) 1,000 (50 x P50) 2,500S&S ( 5 x P200) 1,000 ( 8 x P200)

1,600DC ( 2 x P107.50) 215 ( 5 x P107.50)

537.50 NofP(10 x P100) 1,000 (15 x P100) 1,500

Total costs 11,215 26,137.50

Cost per unit P224.30 P 261.38

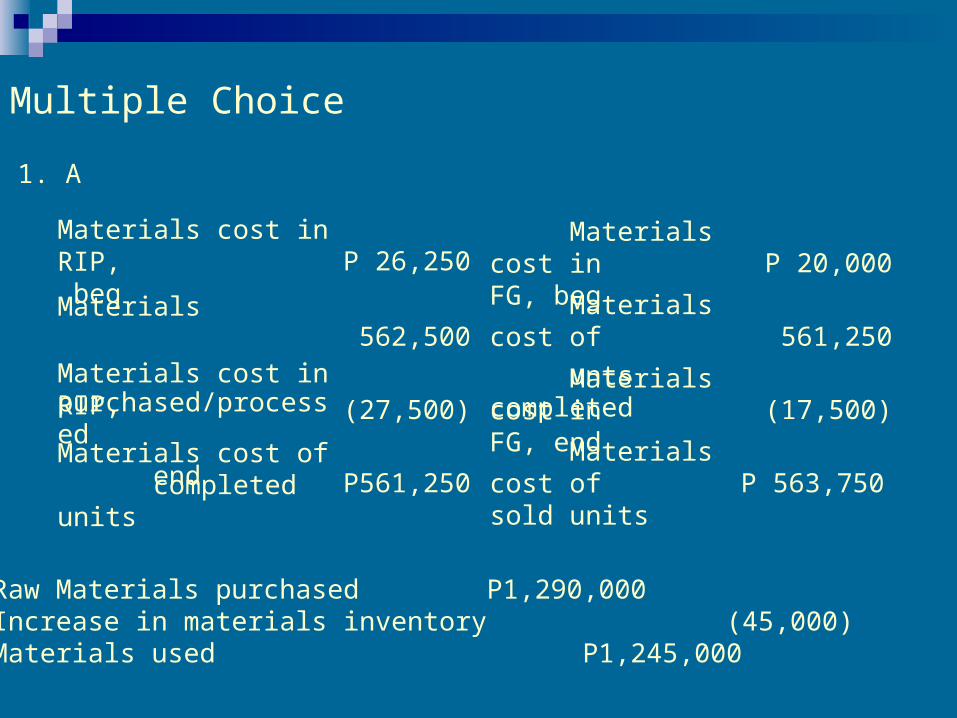

Multiple Choice

P 563,750 Materials cost of sold units P561,250

Materials cost of completed

units

(17,500) Materials cost in FG, end(27,500)

Materials cost in RIP, end

561,250 Materials cost of unts completed

562,500Materials purchased/processed

P 20,000 Materials cost in FG, begP 26,250

Materials cost in RIP, beg

1. A

2. A Raw Materials purchased P1,290,000

Increase in materials inventory (45,000)Materials used P1,245,000

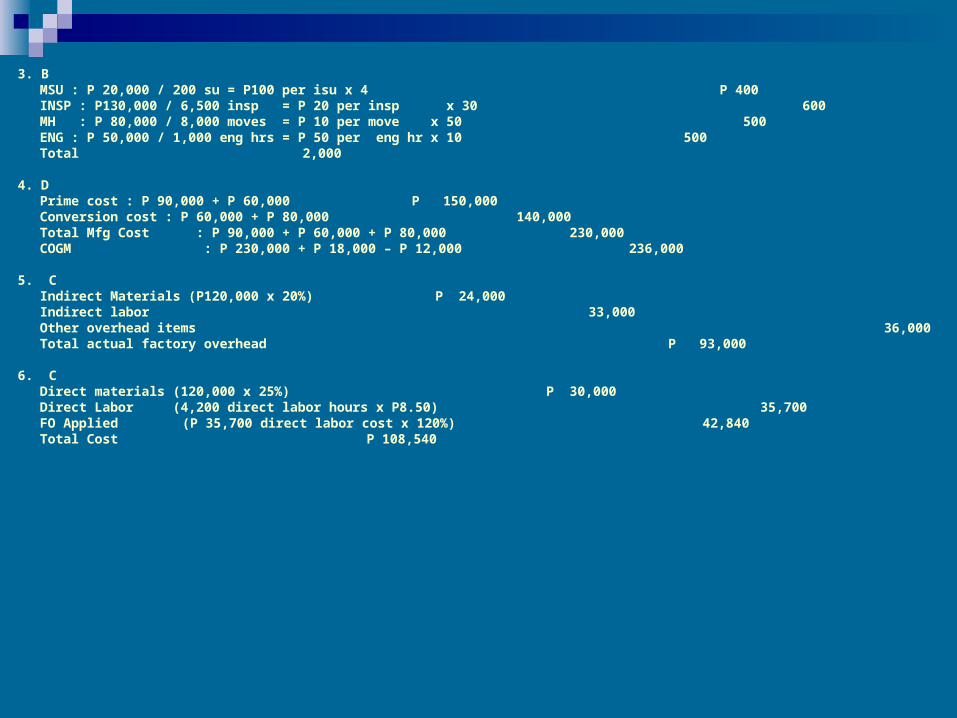

3. BMSU : P 20,000 / 200 su = P100 per isu x 4 P 400INSP : P130,000 / 6,500 insp = P 20 per insp x 30 600MH : P 80,000 / 8,000 moves = P 10 per move x 50 500ENG : P 50,000 / 1,000 eng hrs = P 50 per eng hr x 10 500Total 2,000

4. DPrime cost : P 90,000 + P 60,000 P 150,000Conversion cost : P 60,000 + P 80,000 140,000Total Mfg Cost : P 90,000 + P 60,000 + P 80,000 230,000

COGM : P 230,000 + P 18,000 – P 12,000 236,000

5. CIndirect Materials (P120,000 x 20%) P 24,000Indirect labor 33,000Other overhead items 36,000Total actual factory overhead P 93,000

6. CDirect materials (120,000 x 25%) P 30,000Direct Labor (4,200 direct labor hours x P8.50) 35,700FO Applied (P 35,700 direct labor cost x 120%) 42,840Total Cost P 108,540

7. DSales (P25,000 / 12.5%) P200,000Less Gross Profit (P25,200 + P25,000) 50,200Cost of goods sold, actual P149,800Add: Over applied FO(P62,800 – P 63,000) 200Cost of good sold Normal P150,000FG, end 78,000FG, beg (60,000)COGM P168,000WIP, end 95,000WIP, beg (80,000)Total manufacturing cost P183,000Less: FO applied 63,000 Direct Labor (P63,000 / 75%) 84,000 (147,000)Direct Materials used P 36,000Materials, end 50,000Indirect materials 1,000Materials purchased (46,000)Materials, beg P 41,000

8. COriginal Cost (9,000 + 4,800 + P 3,750) P 17,550Additional rework cost (P1,500 + P800 + P60) 2,360Total cost after rework p 19,910Divided by units produced 5,000Unit cost P 3.982

9. DFO Applied (P 22,800 less total direct cost of P19,500) P 3,300Divided by direct labor cost (P 3,000 + P 2,500) 5,500PDR 60% of DLCTotal Mfg cost DM (3,000 + 2,000 + 6,000 + 4,500) P 15,500

DL (1,000 + 1,500 + 2,600 + 2000) 7,100FO (P 7,100 X 60%) 4,260

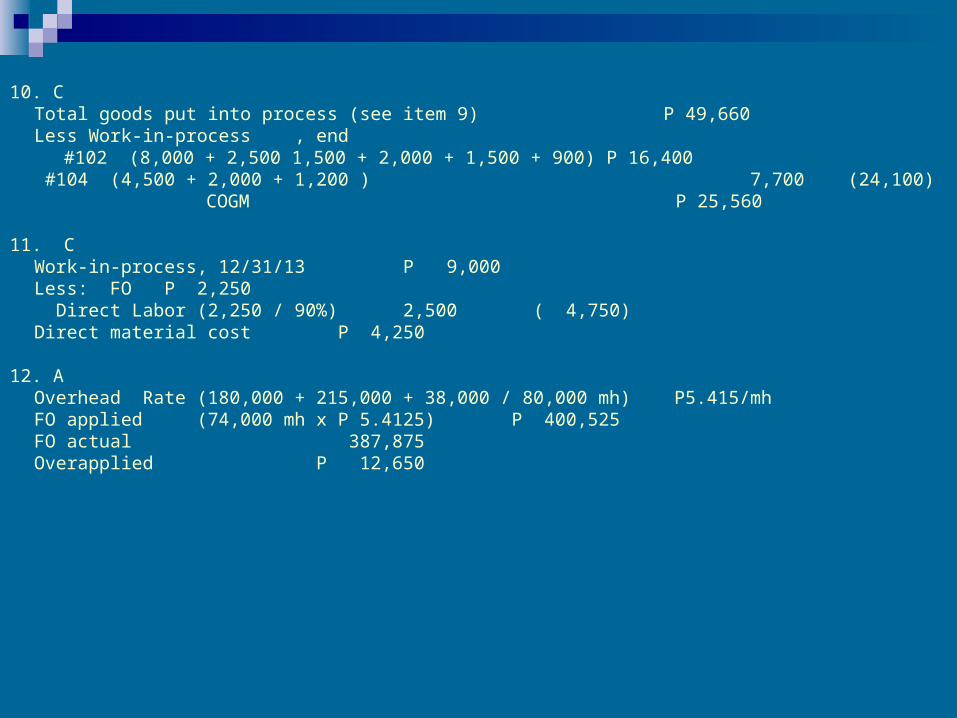

26,860add: work in process, beg 22,800total goods put into process P49,660

10. C Total goods put into process (see item 9) P 49,660Less Work-in-process , end

#102 (8,000 + 2,500 1,500 + 2,000 + 1,500 + 900) P 16,400 #104 (4,500 + 2,000 + 1,200 ) 7,700 (24,100)

COGM P 25,560

11. CWork-in-process, 12/31/13 P 9,000Less: FO P 2,250 Direct Labor (2,250 / 90%) 2,500 ( 4,750)Direct material cost P 4,250

12. AOverhead Rate (180,000 + 215,000 + 38,000 / 80,000 mh) P5.415/mhFO applied (74,000 mh x P 5.4125) P 400,525FO actual 387,875Overapplied P 12,650

Related Documents