© ACCA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© ACCA

© ACCA

Train the Trainer 2018

Strategic Business Reporting

(SBR)

© ACCA

To ensure that tutors feel confident that they can teach Strategic Business Reporting effectively

Objective

© ACCA

Learning outcomes

1. To build tutors’ confidence in their expertise as Strategic Business

Reporting trainers

2. To provide assistance, suggestions and recommendations around

how to teach Strategic Business Reporting

3. To equip tutors in marking and giving feedback on Strategic

Business Reporting

4. To provide assistance, suggestions and recommendations around

how to support students in revision and final preparation for

Strategic Business Reporting

© ACCA

Your agenda – what do you want from the course?

© ACCA

But before we do, just a couple of things to remember…

1. Your approach to teaching

2. Your action plan

Let’s get

started

© ACCA

To build tutors’ confidence in their expertise as Strategic Business Reporting trainers

Learning

outcome 1

© ACCA

Learning outcome 1: To build tutors’ confidence in their expertise as Strategic Business Reporting trainers

1. Know the exam

2. ACCA support resources for Strategic Business Reporting

© ACCA

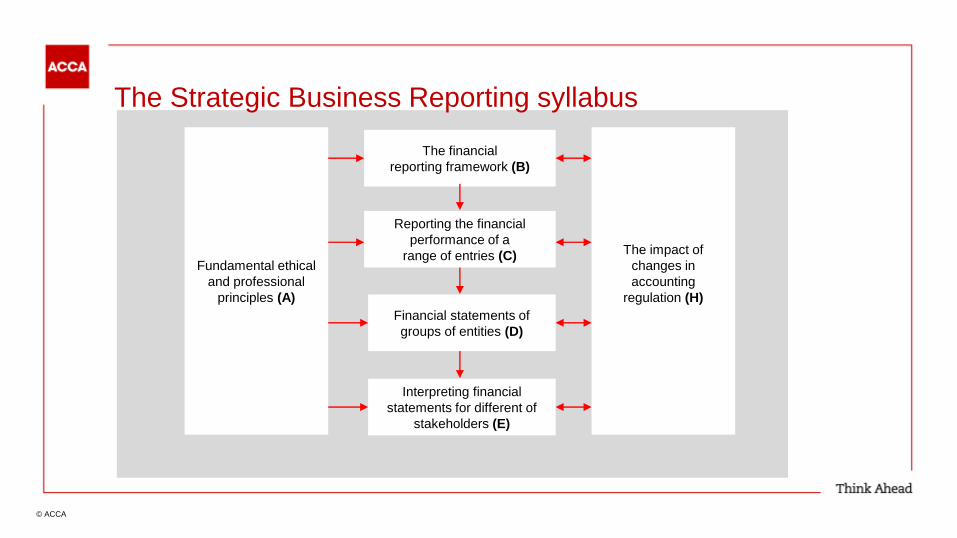

Interpreting financial

statements for different of

stakeholders (E)

Financial statements of

groups of entities (D)

The impact of

changes in

accounting

regulation (H)

The financial

reporting framework (B)

Fundamental ethical

and professional

principles (A)

Reporting the financial

performance of a

range of entries (C)

The Strategic Business Reporting syllabus

© ACCA

Exam Structure (Section A)

Questions

Section A

2 compulsory questions (50 marks, split between Q1 and Q2 can vary)

Question 1

will be based on the financial statements of group entities, or extracts thereof

(syllabus section D)

also likely to require consideration of some financial

reporting issues (syllabus section C)

Question 2

will require candidates to consider either

the reporting implications (syllabus area C) and/or (ii) the ethical

implications (syllabus area A) of specific transactions within a

scenario

Professional marks

two professional marks will be awarded in the ethical issues question in

Section A

In addition to the consideration of

the numerical aspects of group

accounting (max 25 marks), a

discussion and explanation of

these numbers will also be required

© ACCA

Exam structure (Section B)

SBR

Section B

2 compulsory questions (50 marks)

Section B questions can deal with any aspect of the syllabus but will always

include either a full question, or part of a question, that requires the appraisal of

financial and/or non-financial information from either the preparer’s or another

stakeholder’s perspective.

Question 3

Based on a modern business scenario and will require application of

accounting standards

Question

Can contain any element of the syllabus

Main focus likely to be current issues, investor issues and/or interpretation

Professional marks

• two professional marks will be awarded in the question in Section B that

requires analysis.

© ACCA

1: Insights from examiners reports

Exam skills require deeper knowledge and understanding and application of knowledge to the scenarios

Must consider the requirement verbs – numbers are not enough to respond to analyse/discuss/ critically assess

Rote learning is not enough

Very few marks available for simply repeating the requirements of standards

Candidates should be able to explain the contents of financial statements to third party users

In depth knowledge of the Conceptual Framework expected

Questions can take the perspective of a wider group of stakeholders

© ACCA

1: Insights from Learning Providers Insights November 2018

Main weaknesses in candidates answers (September 2018 session):

Unstructured answers, indicating lack of planning

Lack of precise knowledge of IFRS standards and principles of the Conceptual

Framework

Time management

© ACCA

Group activity

How would you introduce Strategic Business Reporting to students at the start of

day1 of a course?

What would you stress to students about preparing for this exam?

© ACCA

1: Introducing Strategic Business Reporting to students

Approach

Wide syllabus • Assumed knowledge from FR

• Significant amount of new content

All questions are compulsory

Cover syllabus widely

Importance of Conceptual Framework Understand the Framework and how it

underpins standards

Questions are practical Knowledge must be applied to scenarios

Questions are mainly written, with only limited

calculations

Few marks for repeating rote learned knowledge

Importance of question practice in exam style

Stakeholder perspective Consider the needs of the users of

information

© ACCA

Learning outcome 1: To build tutors’ confidence in their expertise as Strategic Business Reporting trainers

1. Knowing the exam

2. ACCA support resources for Strategic Business Reporting

© ACCA

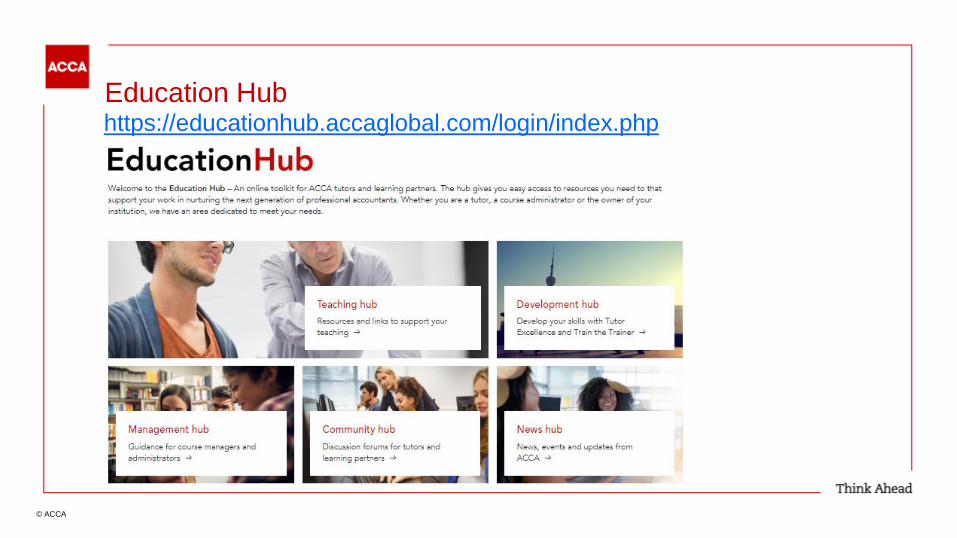

Education Hub https://educationhub.accaglobal.com/login/index.php

© ACCA

ACCA resources to support you and your students

Syllabus and study guide

Specimen Exam

Sample questions from past exams

Examining team guidance

5 minutes with the examining team

Examiner's reports

Examining team approach article

Examples of a change in approach

Recommended approach to section B of the SBR exam

© ACCA

1: Five minutes with the examining team

© ACCA

ACCA resources to support you and your students cont.

Technical articles

Technical topics

Study support videos

Exam technique articles

BPP University English Language Support

Study support guides

Retake guides

Ethics and Professional Skills module

FAQs

© ACCA PUBLIC

Core resources for Strategic Business Reporting

Summary diagram - How to

approach Strategic Business

Reporting

Helping students step up from FR

Exam techniques for success

Read the mind of an SBR marker

(Parts 1 and 2)

© ACCA

Ethics and Professional Skills module

© ACCA

Additional ACCA resources to support tutors

Education Hub

Development – includes ACCA/BPP Tutor Excellence Programme

Community – includes SBR Tutor discussion forum

Global Learning Provider Conference resources

Learning Provider Insights

Tutor exam review panel (TERP) presentations

Teach Accounting e-zine https://www.accaglobal.com/uk/en/learning-provider/resources-tuition/teach-accounting.html

© ACCA

Resources from Approved Content Providers to support your teaching Approved Content – study texts and revision question and answer

banks

Approved Teaching Resources:

Course notes

Revision notes

Teaching guidance

Course exams

Mock exams

© ACCA

Questions Comments Feedback

© ACCA PUBLIC

Advanced Financial Reporting

LO2: Guidance on how to teach

© ACCA PUBLIC

LO2: Guidance on how to teach SBR

2.1 The step up from Financial Reporting (FR)

2.2 Course structure

2.3 Teaching the harder topics

© ACCA PUBLIC

2.1 The step up from Financial Reporting

Underpinning knowledge from FR:

Conceptual framework

Accounting for transactions in

financial statements

Analysing and interpreting financial

statements

Preparation of financial statements

© ACCA PUBLIC

Useful article

https://educationhub.accaglobal.com/course/view.php?id=114

© ACCA PUBLIC

Activity

How can we make sure students have the

assumed knowledge and skills?

© ACCA PUBLIC

LO2: Guidance on how to teach SBR

2.1 The step up from Financial Reporting (FR)

2.2 Course structure

2.3 Teaching the harder topics

© ACCA PUBLIC

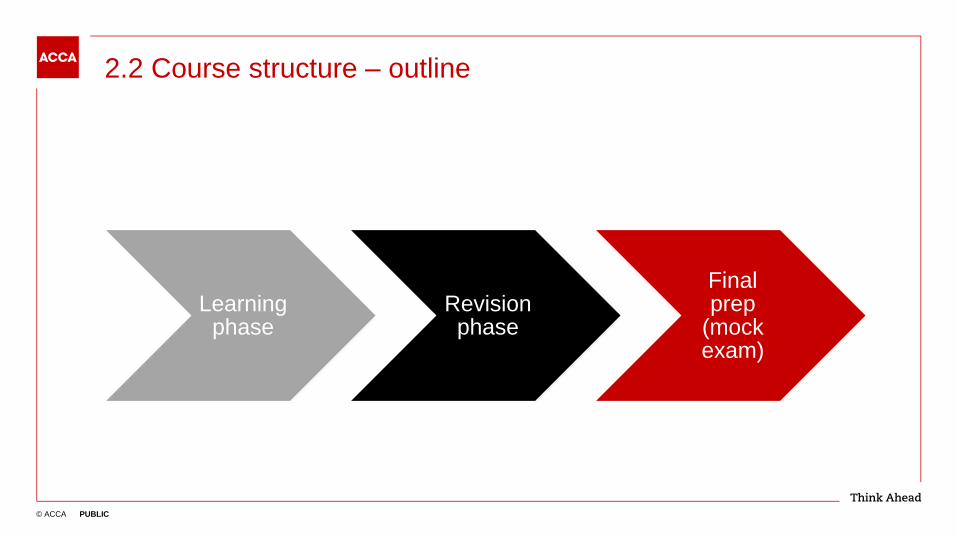

2.2 Course structure – outline

Learning phase

Revision phase

Final prep

(mock exam)

© ACCA PUBLIC

Activity

Devise an outline teaching plan

© ACCA PUBLIC

Activity

How to encourage effective self-study

© ACCA PUBLIC

LO2: Guidance on how to teach SBR

2.1 The step up from Financial Reporting (FR)

2.2 Course structure

2.3 Teaching the harder topics

a. Groups

b. Analysis and interpretation

c. Current issues

© ACCA PUBLIC

LO 2.3 (a) Detailed syllabus

D Financial statements of groups of

entities

1. Group accounting including

statements of cash flows

2. Associates and joint arrangements

3. Changes in group structures

4. Foreign transactions and entities

© ACCA PUBLIC

Learning outcome examples

Strategic Business Reporting

D1a Discuss and apply the principles behind determining whether a business combination has occurred.

D1b Discuss and apply the method of accounting for a business combination including identifying the acquirer and the

principles in determining the cost of a business combination.

© ACCA PUBLIC

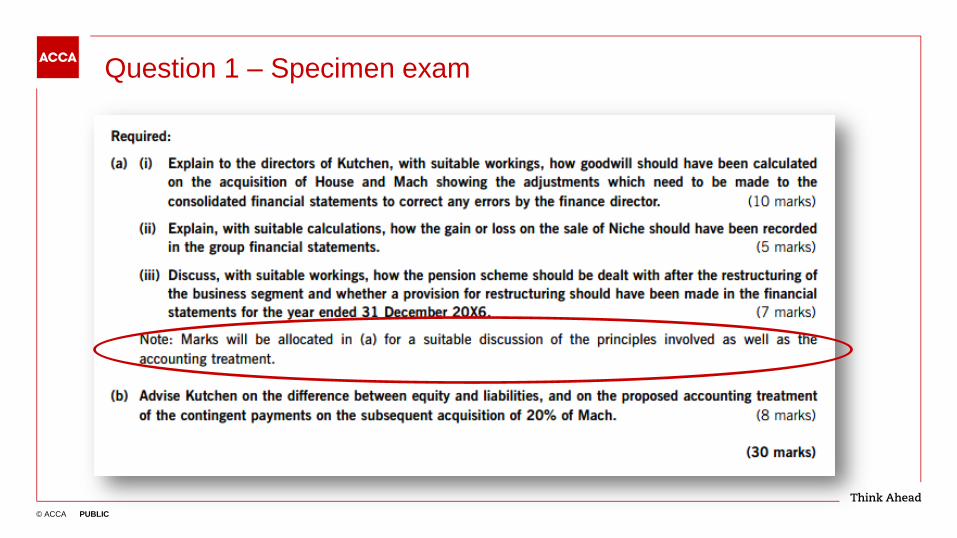

Question 1 – Specimen exam

© ACCA PUBLIC

Question 1 – Specimen exam

© ACCA PUBLIC

Effective teaching of group accounting

Points to consider:

• Brought forward knowledge from Financial Reporting (FR)

• Few marks available for calculations alone

• Emphasis on explanations

• Focus on principles

© ACCA PUBLIC

Exam focus - goodwill

Goodwill

Fair value of consideration 680

Fair value of NCI 420

1,100

Net assets at acquisition:

Share capital 200

Reserves 600

Fair value adjustments 150

(950)

Goodwill 1,050

• Different elements

• Why include contingent consideration?

• How is each element measured?

• Subsequent measurement?

• Why include NCI?

• Choice of measurement

• Impact of measurement options

• Recognition principles

• Measurement principles

• Exceptions to principles

• Subsequent accounting

• What is goodwill?

• Why is it an asset?

© ACCA PUBLIC

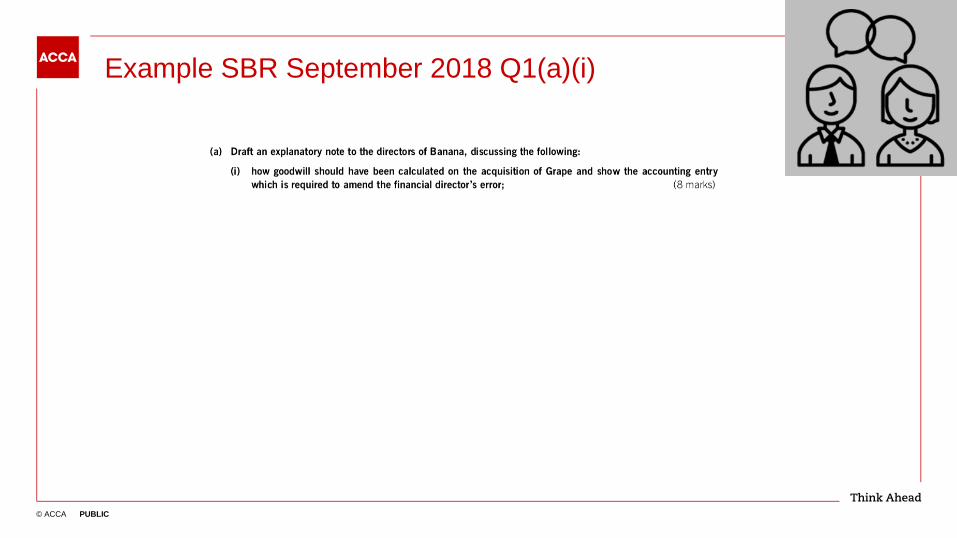

Activity SBR September 2018 Q1(a)(i)

© ACCA PUBLIC

Example SBR September 2018 Q1(a)(i)

© ACCA PUBLIC

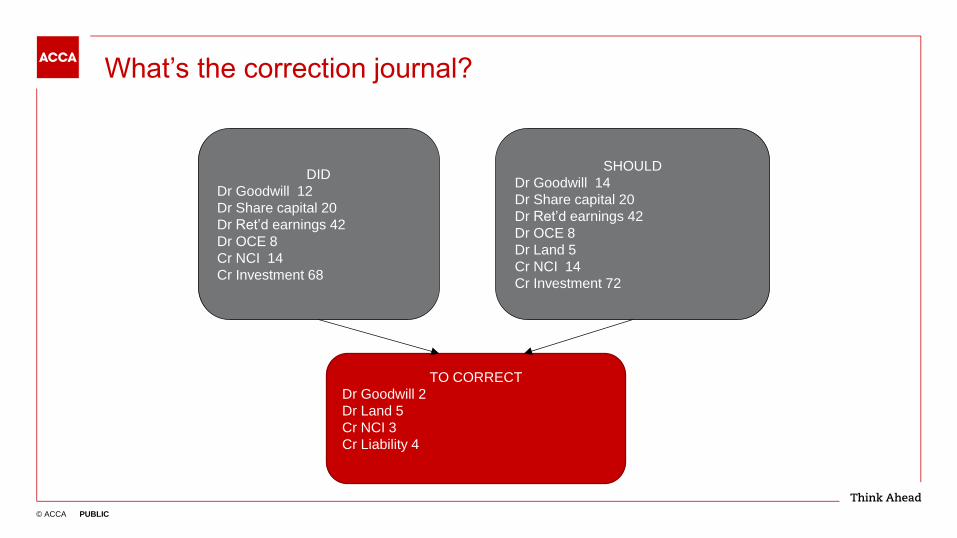

What’s the correction journal?

DID

Dr Goodwill 12

Dr Share capital 20

Dr Ret’d earnings 42

Dr OCE 8

Cr NCI 14

Cr Investment 68

SHOULD

Dr Goodwill 14

Dr Share capital 20

Dr Ret’d earnings 42

Dr OCE 8

Dr Land 5

Cr NCI 14

Cr Investment 72

TO CORRECT

Dr Goodwill 2

Dr Land 5

Cr NCI 3

Cr Liability 4

© ACCA PUBLIC

Activity Q1(a)(iii) September 2018 SBR exam

© ACCA PUBLIC

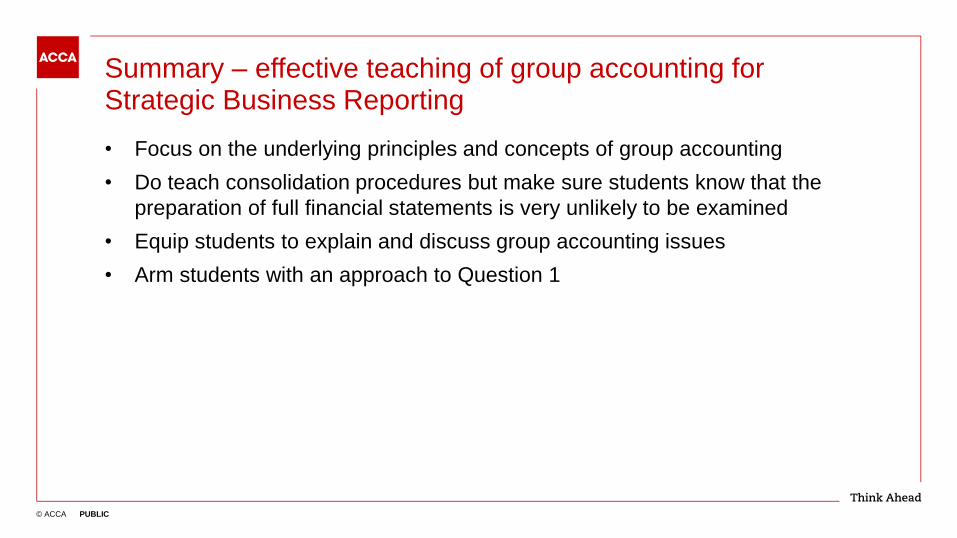

Summary – effective teaching of group accounting for Strategic Business Reporting

• Focus on the underlying principles and concepts of group accounting

• Do teach consolidation procedures but make sure students know that the

preparation of full financial statements is very unlikely to be examined

• Equip students to explain and discuss group accounting issues

• Arm students with an approach to Question 1

© ACCA PUBLIC

LO2: Guidance on how to teach SBR

2.1 The step up from Financial Reporting (FR)

2.2 Course structure

2.3 Teaching the harder topics

a. Groups

b. Analysis and interpretation

c. Current issues

© ACCA

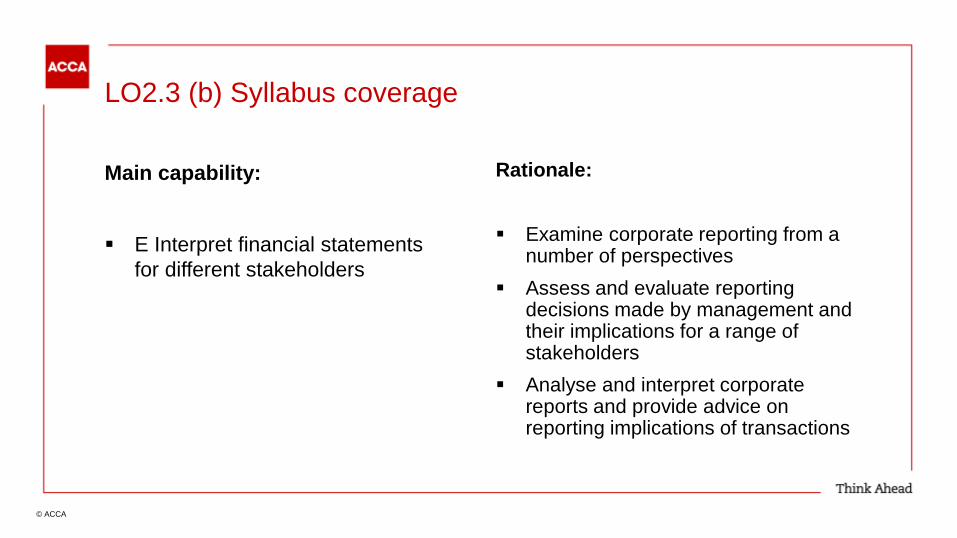

LO2.3 (b) Syllabus coverage

Main capability:

E Interpret financial statements

for different stakeholders

Rationale:

Examine corporate reporting from a number of perspectives

Assess and evaluate reporting decisions made by management and their implications for a range of stakeholders

Analyse and interpret corporate reports and provide advice on reporting implications of transactions

© ACCA

Analysis and interpretation: detailed learning outcomes

E1

a) Discuss and apply relevant indicators of financial and non-financial performance

including earnings per share and additional performance measures

b) Discuss the increased demand for transparency in corporate reports, and the

emergence of non-financial reporting standards.

c) Appraise the impact of environmental, social, and ethical factors on performance

measurement.

d) Discuss the current framework for integrated reporting (IR) including the objectives,

concepts, guiding principles and content of an Integrated Report

e) Determine the nature and extent of reportable segments

f) Discuss the nature of segment information to be disclosed and how segmental

information enhances the quality and sustainability of performance

© ACCA

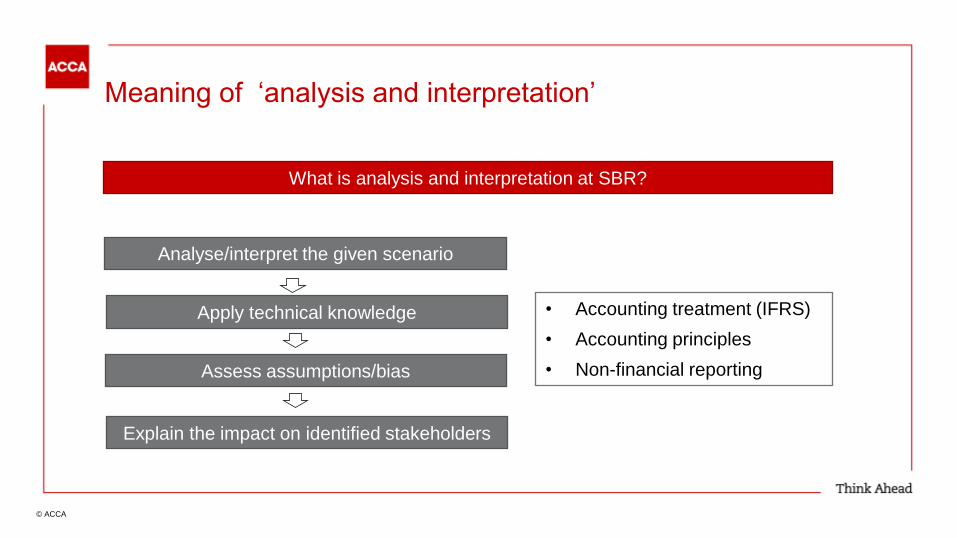

Meaning of ‘analysis and interpretation’

What is analysis and interpretation at SBR?

Analyse/interpret the given scenario

Apply technical knowledge

Assess assumptions/bias

Explain the impact on identified stakeholders

• Accounting treatment (IFRS)

• Accounting principles

• Non-financial reporting

© ACCA

Question 4(a)(ii) – Specimen exam

The directors use ‘underlying profit’ to comment on its financial performance. Underlying profit is a measure

normally based on earning before interest, tax, depreciation and amortisation (EBITDA). However, the effects

of events which are not part of the usual business activity are also excluded when evaluating performance.

The following items were excluded from net profit to arrive at ‘underlying profit’ . In 20X6, the entity had to

write off a property due to subsidence and the insurance proceeds recovered for this property were recorded

but not approved until 20X7, when the company’s insurer concluded that the claim was valid. In 20X6, the

entity considered issuing loan notes to finance an asset purchase, however, the purchase did not go ahead.

The entity incurred costs associated with the potential issue and so these costs were expensed as part of net

profit before taxation. The entity felt that the share-based payment was not a cash expense and that the value

of the options was subjective. Therefore, the directors wish to exclude restructuring charges incurred in the

year, and impairments of acquired intangible assets.

Discuss the use and the limitations of the proposed calculation of ‘underlying profit’ by rationale.

Note: Your answer should include comparative calculation of underlying profit for the years ended 31

December 20X5 and 20X6

(9 marks)

© ACCA

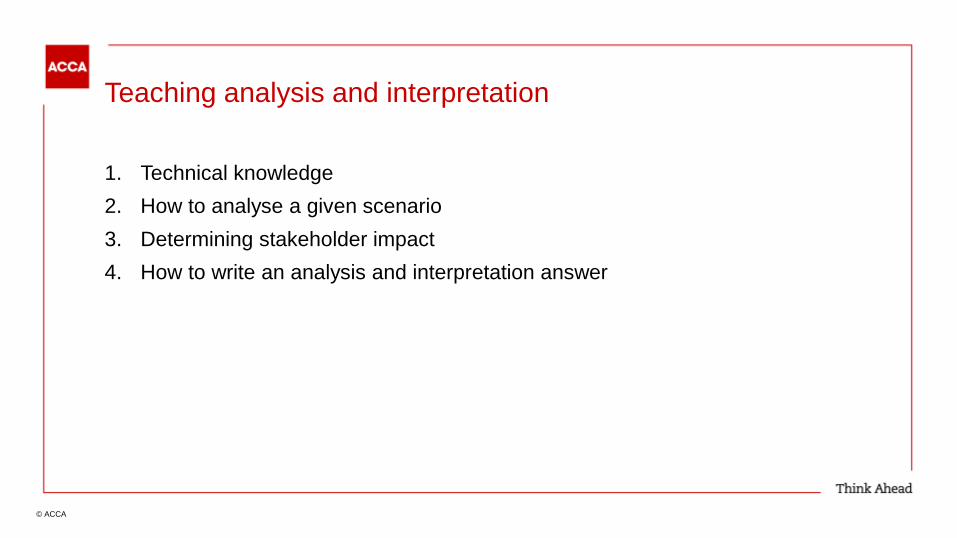

Teaching analysis and interpretation

1. Technical knowledge

2. How to analyse a given scenario

3. Determining stakeholder impact

4. How to write an analysis and interpretation answer

© ACCA

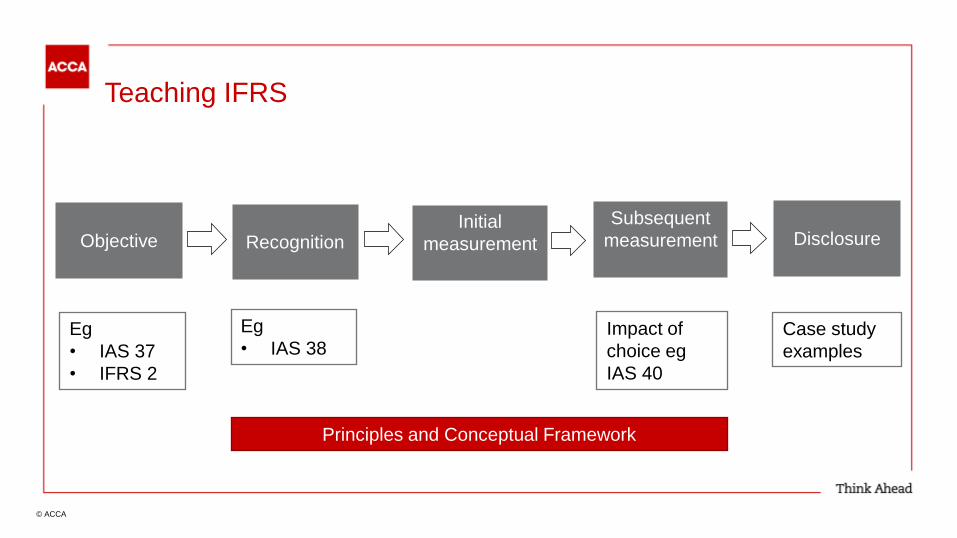

Teaching IFRS

Objective

Recognition

Initial

measurement

Disclosure

Eg

• IAS 37

• IFRS 2

Eg

• IAS 38 Impact of

choice eg

IAS 40

Subsequent

measurement

Case study

examples

Principles and Conceptual Framework

© ACCA ©ACCA

Thoughts from the examining team

1. Understand the Q

and identify the

accounting issues

2. Use principles in the

standard/framework to

plan the answer

3. Apply these principles

to the scenario to

answer the Q

© ACCA

Teaching technique

Teach the theory

Work an example

with students

Ask students to

complete an

example or

question

© ACCA

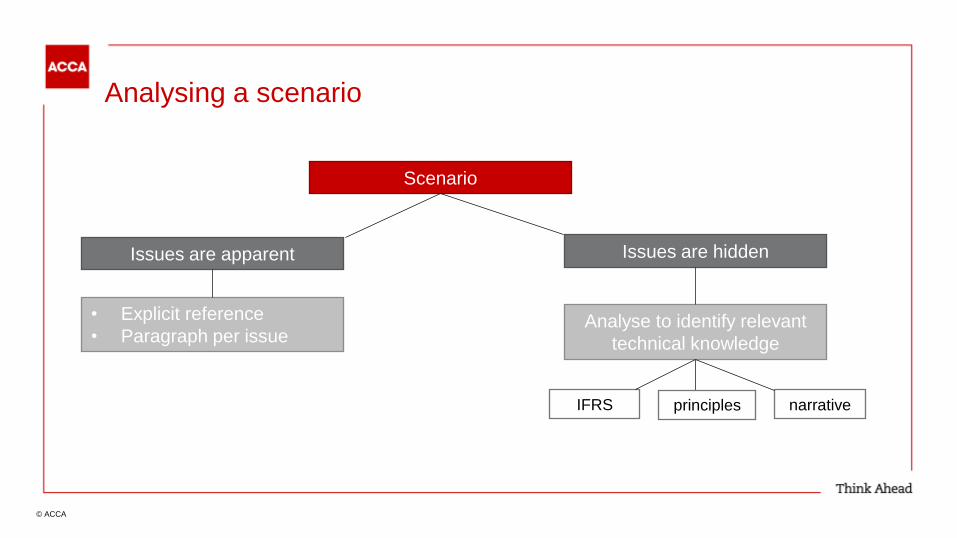

Analysing a scenario

Scenario

Issues are hidden Issues are apparent

• Explicit reference

• Paragraph per issue Analyse to identify relevant

technical knowledge

IFRS principles narrative

© ACCA

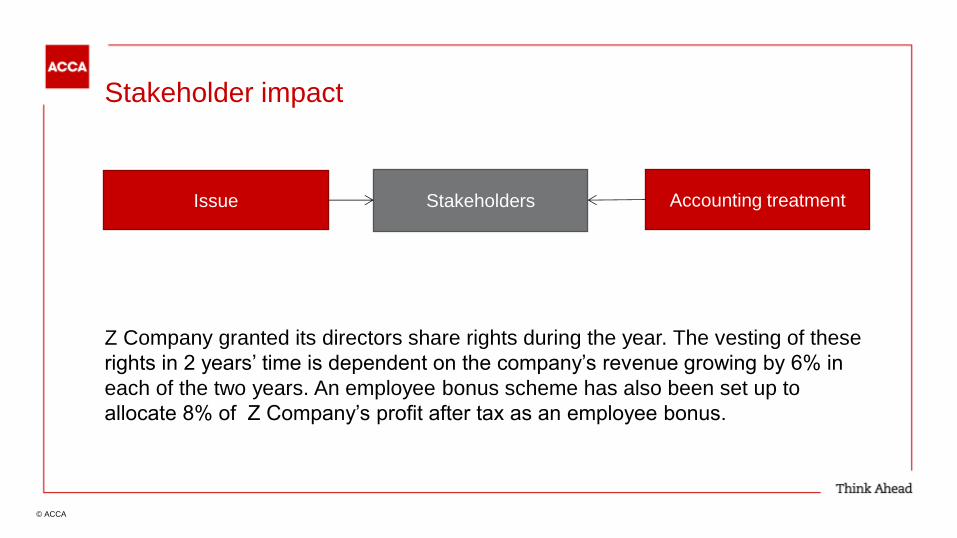

Stakeholder impact

Z Company granted its directors share rights during the year. The vesting of these

rights in 2 years’ time is dependent on the company’s revenue growing by 6% in

each of the two years. An employee bonus scheme has also been set up to

allocate 8% of Z Company’s profit after tax as an employee bonus.

Issue Stakeholders Accounting treatment

© ACCA

Stakeholder impact

Stakeholders

Investors and

potential

investors

Suppliers

Customers

Directors and

senior

management

Employees

The public Government

Lenders

Auditor

© ACCA

What’s the impact on stakeholders?

Good or bad for the stakeholder?

What action might the stakeholder take?

What would be the impact on the reporting

entity?

What action would other stakeholders take as

a result?

© ACCA

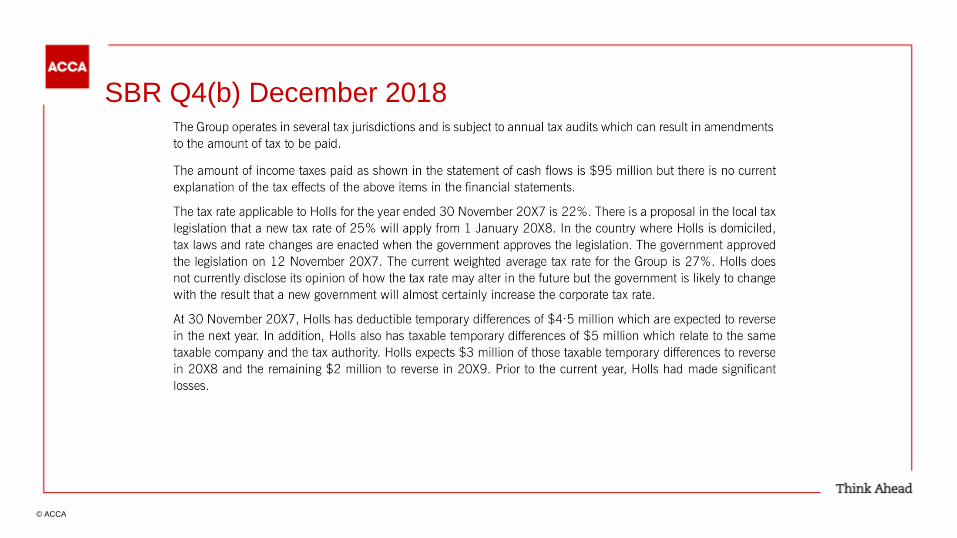

SBR Q4(b) December 2018

© ACCA

SBR Q4(b) December 2018

© ACCA

The tax reconciliation Differs from taxable profit

22% x profit

Group tax is total of individual

companies’ tax at local rate

Amounts in SPL that are not

taxable/are not relieved

• Adjustments

• Deferred tax At effective rate

© ACCA

How to prepare students for a similar question

Explain a disclosure

note

1. Identify disclosure requirements

in IFRS

2. Use examples from real

companies’ annual reports

© ACCA

Example

© ACCA

Techniques to identify issues

Read through and make note in margin/use highlighter to identify each issue

Look for

trigger words

e.g.

impairment

Consider a

list of

standards to

identify those

that are

relevant

Consider a

standard

layout of the

SOFP,

SPLOCI and

SCF

Consider what

the stakeholder

sees - the

layout of a

published

annual report –

narrative /

group accounts

/ parent

company

accounts

Consider the

content of the

Conceptual

Framework

© ACCA

Specimen exam Question 4

© ACCA

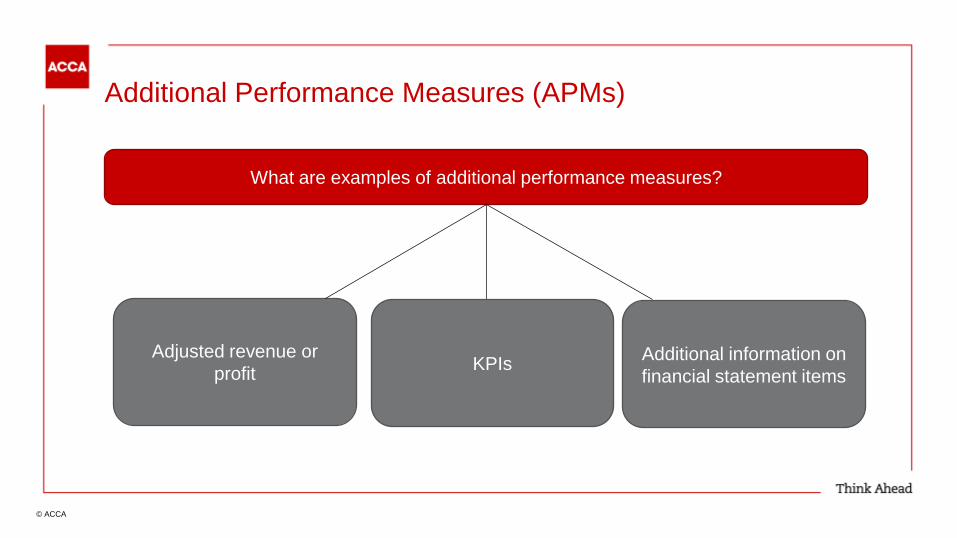

Additional Performance Measures (APMs)

What are examples of additional performance measures?

Adjusted revenue or

profit KPIs

Additional information on

financial statement items

© ACCA

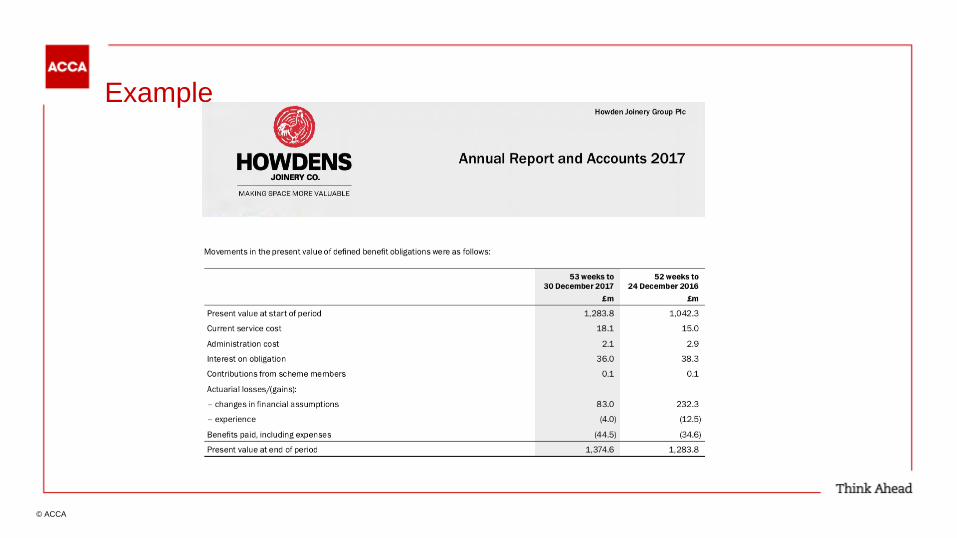

Example – annual report

*Key financial indicators

Underlying sales growth, underlying volume growth, core operating margin and free cash flow are non-

GAAP measures. For further information about these measures, and the reasons why we believe they

are important for an undertanding of the performance of the business, please refer to our commentary on

non-GAAP measures on page 26 to 28

© ACCA

Example - highlights in annual report

© ACCA

TIM Group EBITDA

© ACCA

APMs: aspects to teach

Advantages and disadvantages Evaluation

European Securities and Markets

Authority guidelines

© ACCA

Writing an answer to an analysis and interpretation question

Identify the requirement and

allocate marks to sub-

requirements both explicit and

implicit

Write answer

Deal with all sub-

requirements

Write sufficient

points

Headings Separate

paragraphs

Write succinctly

Professional

language

Write thought

process

Avoid repetition

© ACCA PUBLIC

LO2: Guidance on how to teach SBR

2.1 The step up from Financial Reporting (FR)

2.2 Course structure

2.3 Teaching the harder topics

a. Groups

b. Analysis and interpretation

c. Current issues

© ACCA PUBLIC

LO2.3 (c) Current Issues

Current syllabus

How can tutors prepare to teach?

How to teach current issues

© ACCA PUBLIC

Current Syllabus (September 2018 to June 2019)

Discuss and apply the accounting implications of the first time adoption of

new accounting standards

Identify issues and deficiencies which have led to proposed changes to an

accounting standard

Discuss the impact of current issues in corporate reporting

© ACCA PUBLIC

Current syllabus (September 2018 to June 2019) continued

Discuss the impact of current issues in corporate reporting

Revision of the conceptual framework

IASB’s Principles of Disclosure Initiative

Materiality in the context of financial reporting

Primary Financial Statements

Management commentary

Developments in sustainable reporting

© ACCA PUBLIC

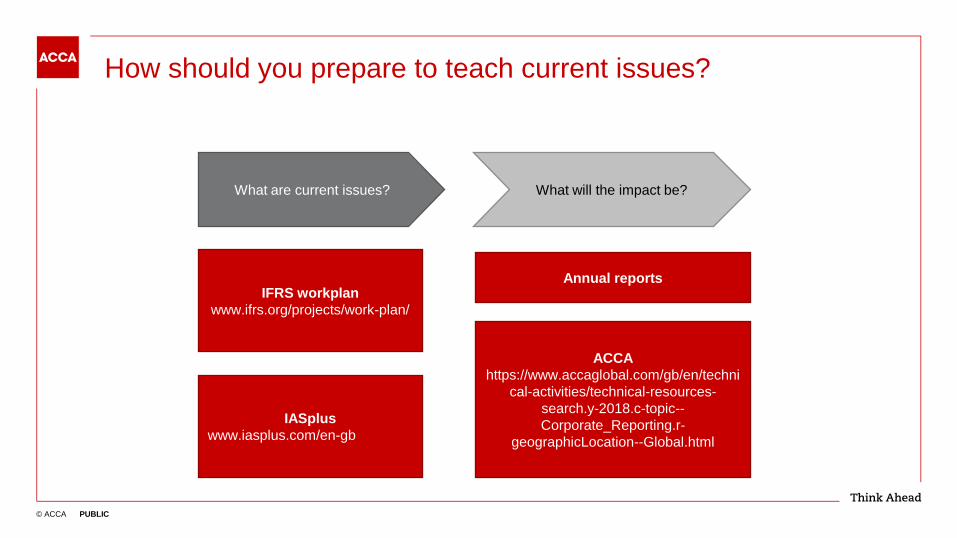

How should you prepare to teach current issues?

What are current issues? What will the impact be?

IFRS workplan

www.ifrs.org/projects/work-plan/

IASplus

www.iasplus.com/en-gb

Annual reports

ACCA

https://www.accaglobal.com/gb/en/techni

cal-activities/technical-resources-

search.y-2018.c-topic--

Corporate_Reporting.r-

geographicLocation--Global.html

© ACCA PUBLIC

How to teach current issues

Activity

How can we teach current issues in the classroom?

© ACCA PUBLIC

Using the Conceptual Framework to appraise current standards – an example

IAS 12 Income

Taxes

Qualitative criteria

Definition and

recognition of elements

Accrual accounting

© ACCA PUBLIC

Sustainability Reporting – An approach to teaching

What is a sustainability report?

Is there any guidance?

Do companies prepare sustainability

reports?

© ACCA PUBLIC

What is a sustainability report?

© ACCA PUBLIC

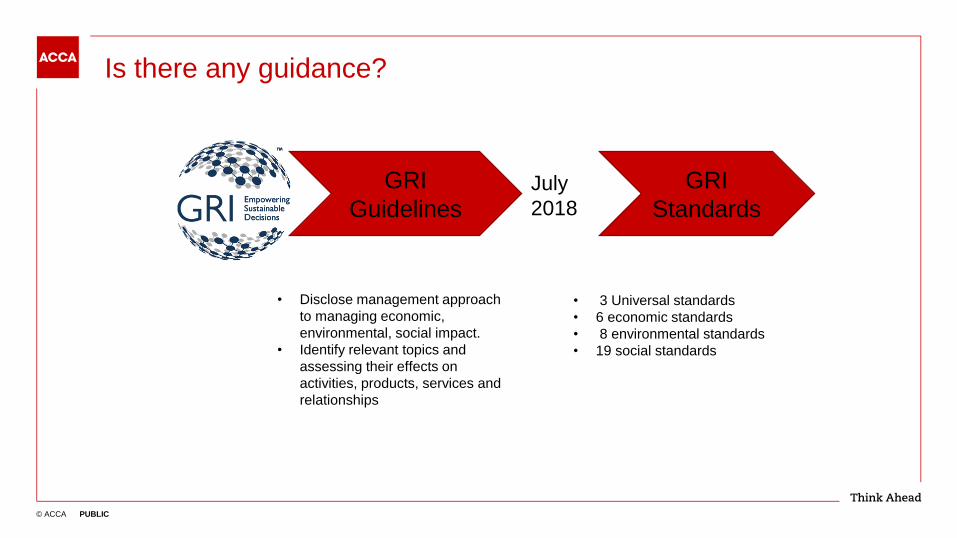

Is there any guidance?

GRI

Guidelines

GRI

Standards July

2018

• Disclose management approach

to managing economic,

environmental, social impact.

• Identify relevant topics and

assessing their effects on

activities, products, services and

relationships

• 3 Universal standards

• 6 economic standards

• 8 environmental standards

• 19 social standards

© ACCA PUBLIC

Real life example

Do you think that Vodafone report under GRI

guidelines?

© ACCA PUBLIC

Vodafone G4

© ACCA

Questions Comments Feedback

© ACCA

How SBR is marked

Learning

outcome 3

© ACCA

Learning outcome 3: How SBR is marked

1. Overview of exam marking at ACCA

2. Interactive exercise where tutors have the opportunity to practise marking

© ACCA

How SBR is marked

Learning

outcome 3

© ACCA

Learning outcome 3: How SBR is marked

1. Overview of exam marking at ACCA

2. Interactive exercise where tutors have the opportunity to practise marking

© ACCA

Who are the marking team?

Qualifications Technical

Adviser

Marking

Session Lead

Team Leader

Markers

Team Leader

Markers

Team Leader

Markers

© ACCA

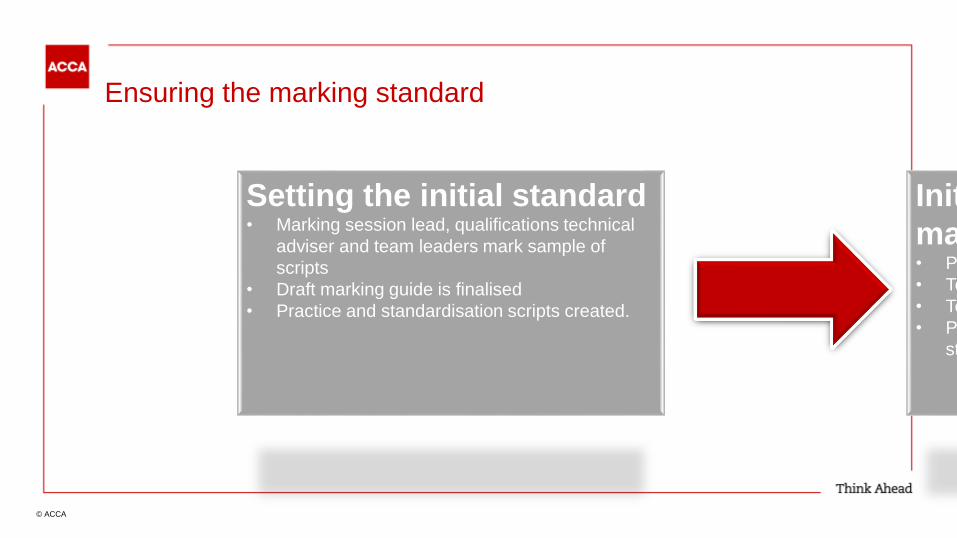

Ensuring the marking standard

Setting the initial standard • Marking session lead, qualifications technical

adviser and team leaders mark sample of

scripts

• Draft marking guide is finalised

• Practice and standardisation scripts created.

Initial standardisation of

markers • Practice to learn marking guide

• Tested on standardisation scripts

• Team leaders train as required

• Process repeats until

standard met.

Maintaining the standard

during marking • Marking session lead marks scripts

to be set as seeding

• Seeding scripts allocated

to markers

• Team Leaders check and resolve

standard drift.

© ACCA

Marking – basic principles

Suggested answers – are examples of strong answers

Credit is given for any relevant answers

No negative marking

No marks lost for poor spelling or grammar

© ACCA

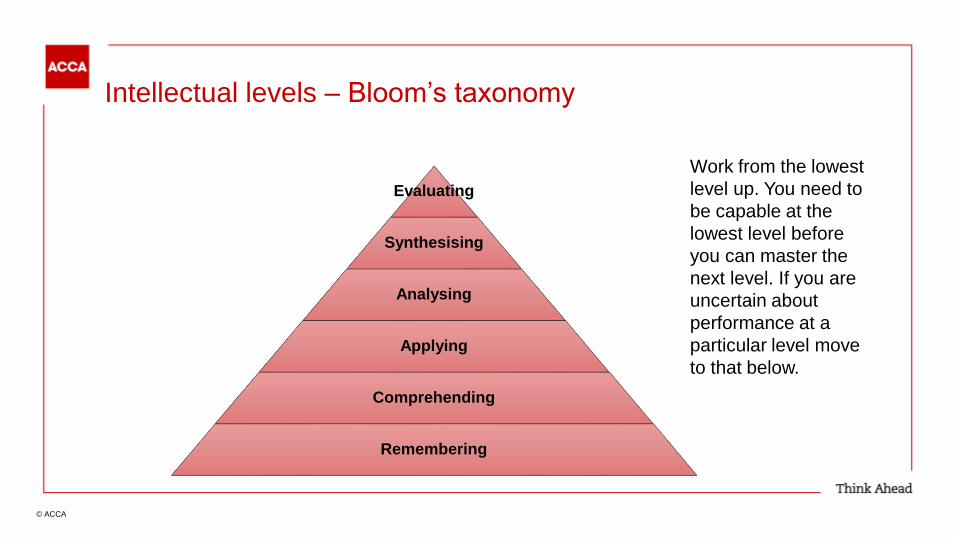

Intellectual levels – Bloom’s taxonomy

Work from the lowest

level up. You need to

be capable at the

lowest level before

you can master the

next level. If you are

uncertain about

performance at a

particular level move

to that below.

Evaluating

Synthesising

Analysing

Applying

Comprehending

Remembering

© ACCA

Marking – basic principles

Generally 1 mark per relevant point (see marking schemes

for each question)

Marking will reflect the intellectual level demanded by the

task requirements

Own figure rule

© ACCA

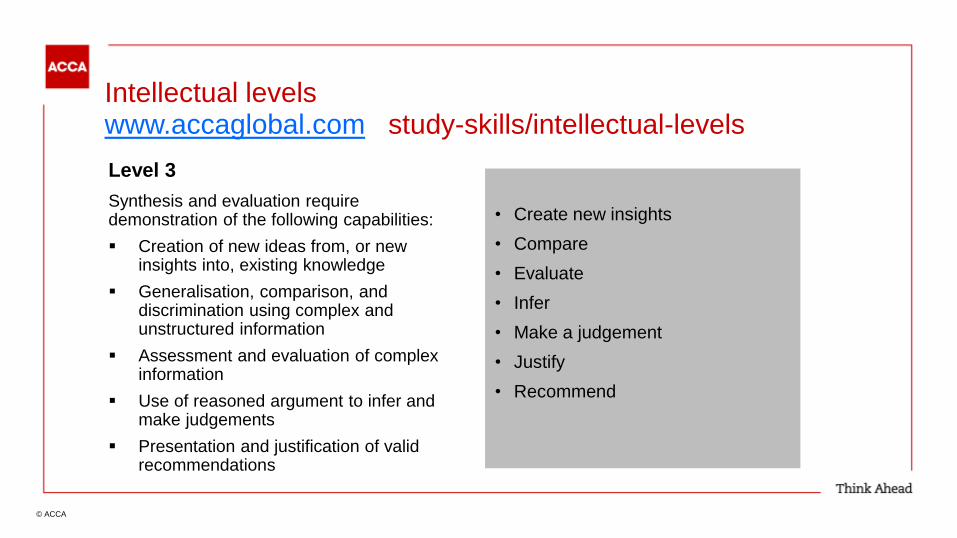

Intellectual levels www.accaglobal.com study-skills/intellectual-levels

Level 3

Synthesis and evaluation require demonstration of the following capabilities:

Creation of new ideas from, or new insights into, existing knowledge

Generalisation, comparison, and discrimination using complex and unstructured information

Assessment and evaluation of complex information

Use of reasoned argument to infer and make judgements

Presentation and justification of valid recommendations

• Create new insights

• Compare

• Evaluate

• Infer

• Make a judgement

• Justify

• Recommend

© ACCA

Learning outcome 3: How SBR is marked

1. Overview of exam marking at ACCA

2. Interactive exercise where tutors have the opportunity to

practise marking

© ACCA

Interactive exercise: your turn to mark!

• Practice scripts

• Marking scheme

© ACCA

Interactive exercise: your turn to mark! The answer scripts include two answers to the following requirements:

Requirement Marks

Specimen Q1(a)

(i)

Explain goodwill calculations and error corrections 10

Specimen Q1(a)

(ii)

Explain treatment of gain/loss on sale of investment in

subsidiary

5

Specimen Q 2 Ethical and accounting implications 18

Professional marks 2

December 2018

Q3

(a) Conceptual Framework and valuation of inventory 7

(b) Treatment of reconditioning costs and impairment 8

(c) Treatment of acquisition of additional interest in a mine 10

© ACCA

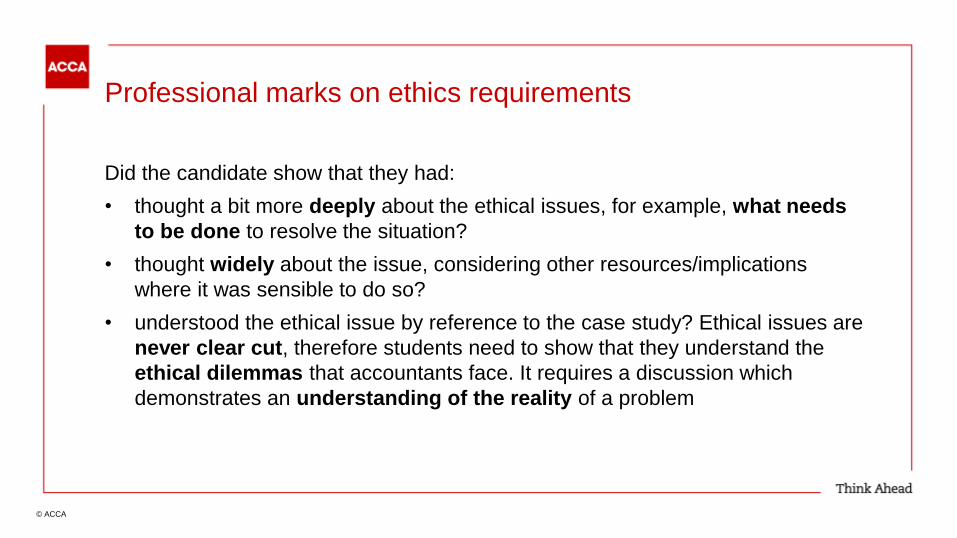

Professional marks on ethics requirements

Did the candidate show that they had:

• thought a bit more deeply about the ethical issues, for example, what needs

to be done to resolve the situation?

• thought widely about the issue, considering other resources/implications

where it was sensible to do so?

• understood the ethical issue by reference to the case study? Ethical issues are

never clear cut, therefore students need to show that they understand the

ethical dilemmas that accountants face. It requires a discussion which

demonstrates an understanding of the reality of a problem

© ACCA

Learning outcome 3: How SBR is marked

1. Overview of live exam marking at ACCA

2. Interactive exercise where tutors have the opportunity to practise marking

© ACCA PUBLIC

LO4: Supporting students in revision and final preparation for SBR

4.1 Structure of a revision course

4.2 Effective exam technique

4.3 Running a mock exam day

© ACCA PUBLIC

4.1 Overall structure of a revision course

Pre-course information

Pre-course work

Timetable

Each day

Topics

Question practice

Homework

Mock exam

On course or

a separate day

© ACCA PUBLIC

Activity - using questions

Question-based teaching is the most effective way to revise but students will be

bored if they are not given a variety of activities in class.

List the different ways that you can use questions during a revision course

© ACCA PUBLIC

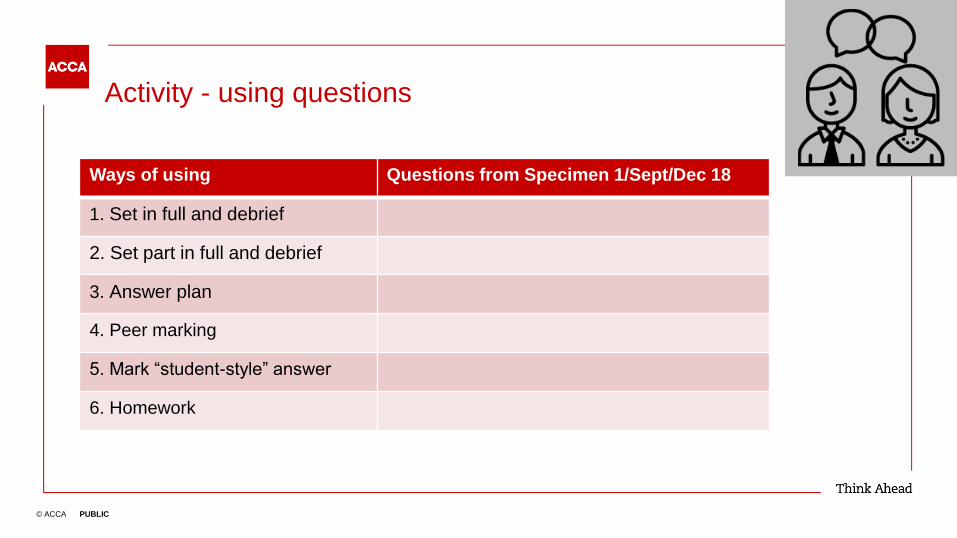

Activity - using questions

Ways of using Questions from Specimen 1/Sept/Dec 18

1. Set in full and debrief

2. Set part in full and debrief

3. Answer plan

4. Peer marking

5. Mark “student-style” answer

6. Homework

© ACCA PUBLIC

Activity

Debriefing a revision question

© ACCA PUBLIC

Debriefing a revision question

Take in and mark

Guide marking

Mark a student style answer

Rework it

Draw on examiner’s report feedback

Debrief checklist

© ACCA PUBLIC

Required:

(i) Explain the criteria in both the 2010 version of the Conceptual Framework for Financial Reporting (the Conceptual Framework) of the International Accounting Standards Board and the 2015 proposed revision to the Conceptual Framework for the recognition of an asset and whether the criteria are the same in IAS® 38 Intangible Assets. (6 marks)

(ii) Discuss the implications for Skizer’s financial statements for both the years ended 31 August 20X7 and 20X8 if the recognition criteria in IAS 38 for an intangible asset were met as regards the stakes in the development projects above. Your answer should also briefly consider the implications if the recognition criteria were not met. (5 marks)

(iii) Discuss whether the proceeds of the sale of the development project above should be treated as revenue in the financial statements for the year ended 31 August 20X8. (4 marks)

Skizer Co (September 2018 Q2a) – Debrief requirements

© ACCA PUBLIC

LO4: Supporting students in revision and final preparation for AAA

4.1 Structure of a revision course

4.2 Effective exam technique

4.3 Running a mock exam day

© ACCA PUBLIC

4.2 Inappropriate exam technique – examiner’s feedback

1. Not answering in line with the requirement verbs – analyse/discuss/critically

assess

2. Quoting accounting standards with no application or discussion

3. Numbers in isolation will not be enough

4. Poor time management – tendency to over-run on Q1

5. Poor planning - repetition of points wastes time and will not score marks

© ACCA PUBLIC

4.2 Effective exam technique

Guidance on:

Time management

Format

Content

Preparation

© ACCA PUBLIC

Activity

How to instil best exam technique practices

in our students?

© ACCA PUBLIC

Activity

Exam technique in Q1

© ACCA PUBLIC

Moyes Q1December 2018 - the requirements

© ACCA PUBLIC

LO4: Supporting students in revision and final preparation for SBR

4.1 Structure of a revision course

4.2 Effective exam technique

4.3 Running a mock exam day

© ACCA PUBLIC

4.3 Running a mock exam “day”

“Sitting a Mock Exam in the time allocated, without reference to study materials, is

the single most important element in preparing for the ACCA exam”

Readiness

Timing

“Fear factor”

Effective exam technique

Time management

Overall approach

Reflect on experience

© ACCA PUBLIC

4.3 Running a mock exam “day” – Marking and feedback

Wherever possible

Marking scheme

Debrief and commentaries

© ACCA PUBLIC

Questions?

© ACCA PUBLIC

For more information visit accaglobal.com

Related Documents