© 2011 IFRS Foundation 1 The IFRS for SMEs Topic 1.3 Sections 1 and 2 Scope and concepts

© 2011 IFRS Foundation 1 The IFRS for SMEs Topic 1.3 Sections 1 and 2 Scope and concepts.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2011 IFRS Foundation

1The IFRS for SMEs

Topic 1.3

Sections 1 and 2

Scope and concepts

© 2011 IFRS Foundation

2

This PowerPoint presentation was prepared by IFRS Foundation education staff as a convenience for others. It has not been approved by the IASB. The IFRS Foundation allows individuals and organisations to use this presentation to conduct training on the IFRS for SMEs. However, if you make any changes to the PowerPoint presentation, your changes should be clearly identifiable as not part of the presentation prepared by the IFRS Foundation education staff and the copyright notice must be removed from every amended page .

This presentation may be modified from time to time. The latest version

may be downloaded from: http://www.ifrs.org/IFRS+for+SMEs/SME+Workshops.htm

The accounting requirements applicable to small and medium‑sized entities (SMEs) are set out in the International Financial Reporting Standard (IFRS) for SMEs, which was issued by the IASB in July 2009.

The IFRS Foundation, the authors, the presenters and the publishers do not accept responsibility for loss caused to any person who acts or refrains from acting in reliance on the material in this PowerPoint presentation, whether such loss is caused by negligence or otherwise.

© 2011 IFRS Foundation

Section 1 – scope of the IFRS for SMEs

Learning objectives– identify SMEs as defined by the IASB

(know the characteristics of SMEs)– identify which entities must not assert

compliance with the IFRS for SMEs

3

© 2011 IFRS Foundation

Section 1 – can I use the IFRS for SMEs?

Decisions on which entities are required or permitted to use the IFRS for SMEs rest with legislative and regulatory authorities and standard-setters in individual jurisdictions

4

© 2011 IFRS Foundation

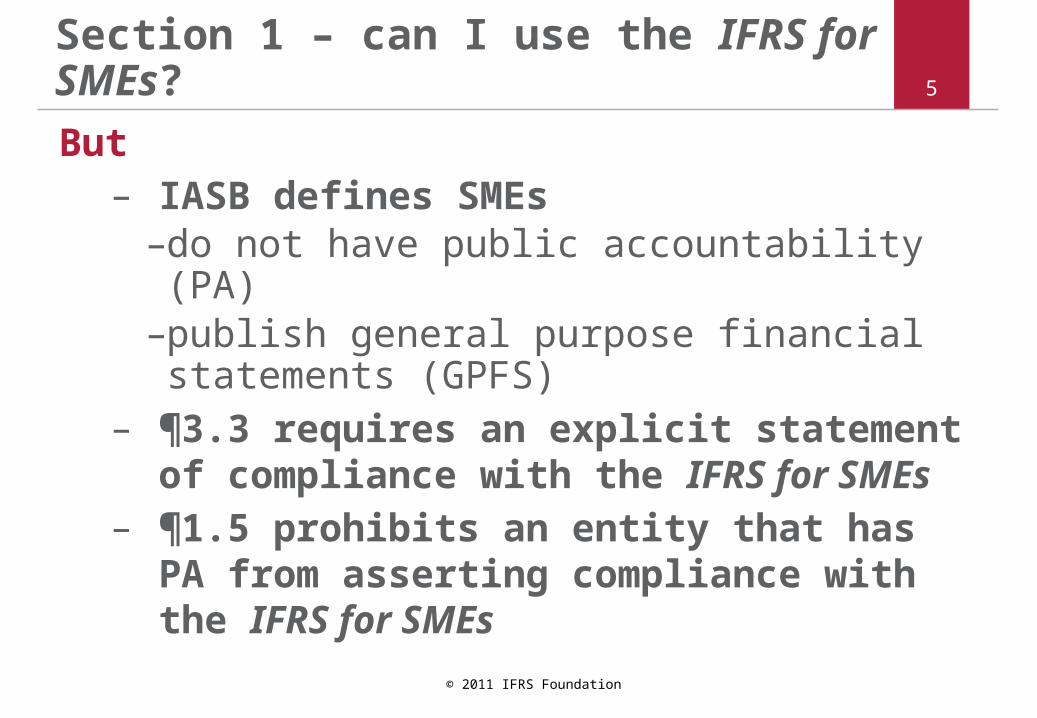

Section 1 – can I use the IFRS for SMEs?

But– IASB defines SMEs

–do not have public accountability (PA)–publish general purpose financial

statements (GPFS)– ¶3.3 requires an explicit statement of

compliance with the IFRS for SMEs– ¶1.5 prohibits an entity that has PA

from asserting compliance with the IFRS for SMEs

5

© 2011 IFRS Foundation

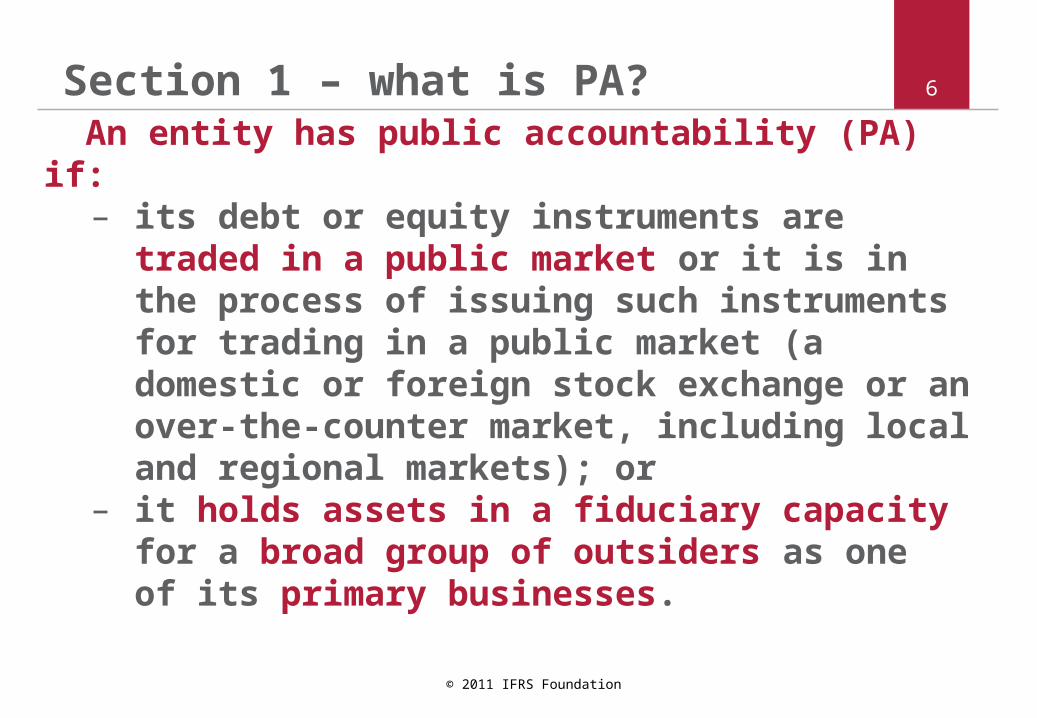

Section 1 – what is PA? An entity has public accountability (PA) if:

– its debt or equity instruments are traded in a public market or it is in the process of issuing such instruments for trading in a public market (a domestic or foreign stock exchange or an over-the-counter market, including local and regional markets); or

– it holds assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses.

6

© 2011 IFRS Foundation

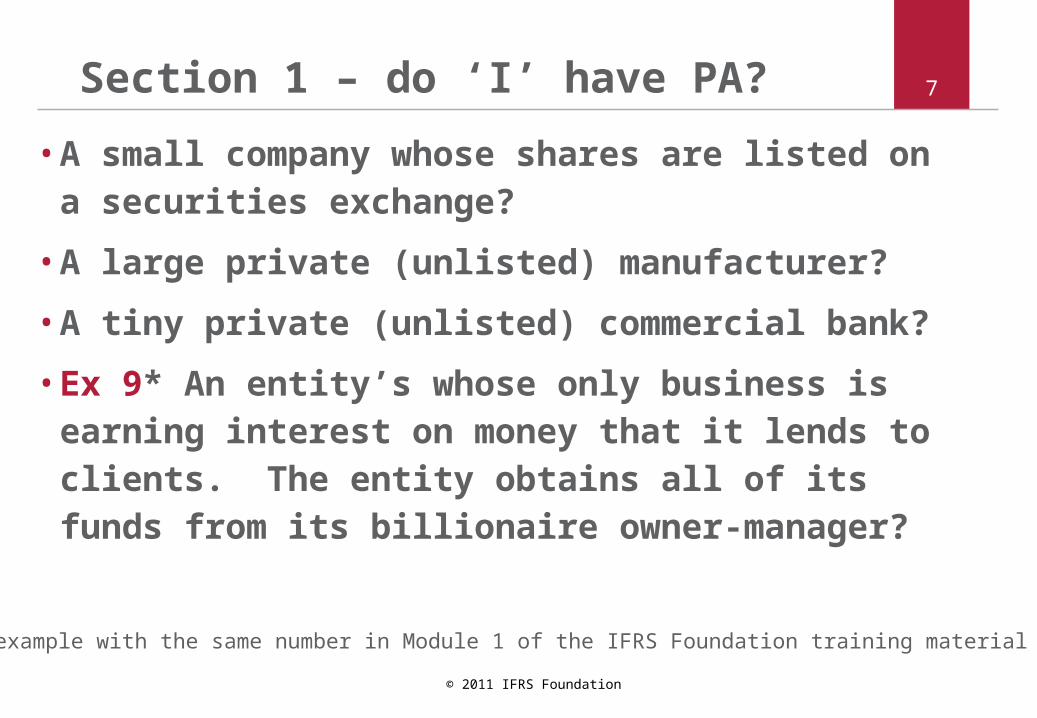

7Section 1 – do ‘I’ have PA?

• A small company whose shares are listed on a securities exchange?

• A large private (unlisted) manufacturer?

• A tiny private (unlisted) commercial bank?

• Ex 9* An entity’s whose only business is earning interest on money that it lends to clients. The entity obtains all of its funds from its billionaire owner-manager?

* see example with the same number in Module 1 of the IFRS Foundation training material

© 2011 IFRS Foundation

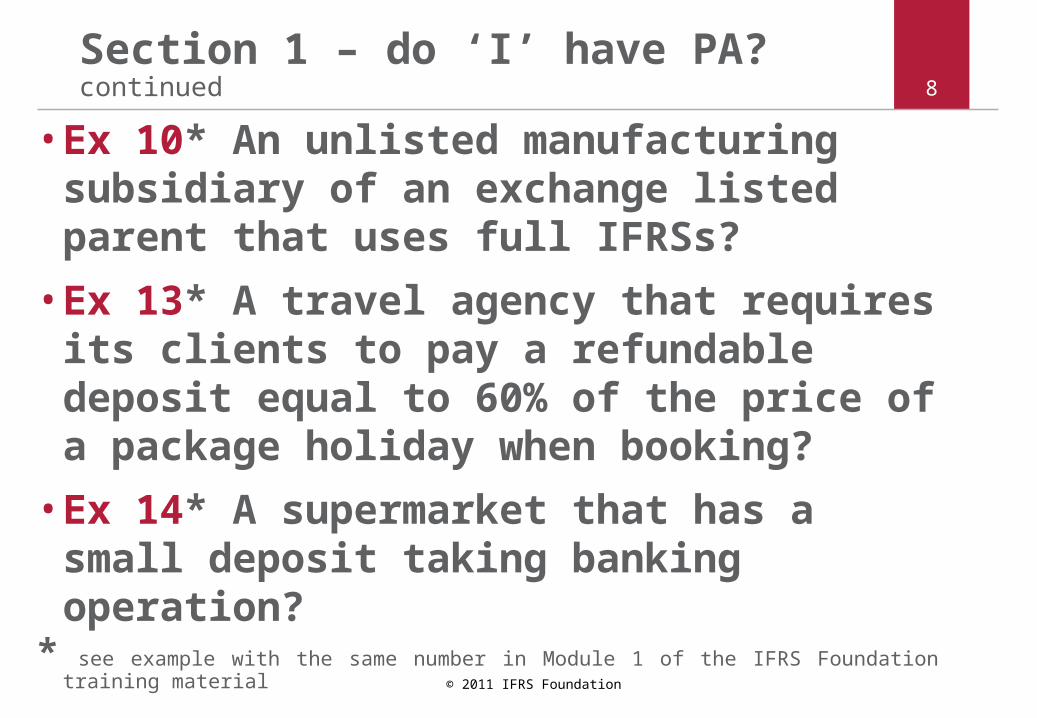

8Section 1 – do ‘I’ have PA? continued

• Ex 10* An unlisted manufacturing subsidiary of an exchange listed parent that uses full IFRSs?

• Ex 13* A travel agency that requires its clients to pay a refundable deposit equal to 60% of the price of a package holiday when booking?

• Ex 14* A supermarket that has a small deposit taking banking operation?

* see example with the same number in Module 1 of the IFRS Foundation training material

© 2011 IFRS Foundation

Section 1 – what are GPFS?

General purpose financial statements are prepared on a basis that is designed to provide useful information to a wide range of users (eg investors and creditors) who are not in a position to demand reports tailored to meet their particular needs.

9

© 2011 IFRS Foundation

Section 1 – are SMEs statements GPFS?

The objective of financial statements prepared in accordance with the IFRS for SMEs is to provide information about the entity’s financial position, performance and cash flows that is useful to a broad range of users who are not in a position to demand reports tailored to meet their particular information needs.

10

© 2011 IFRS Foundation

11Section 1 – do I have GPFS?

• Ex 4* FS prepared in compliance with tax requirements for calculating taxable income (that are different from the IFRS for SMEs) and which are sent only to the tax authorities?

• Ex 5* FS prepared on the tax basis (see above) but also sent to the entity’s bankers and the national repository. FS filed in the national repository are publicly available?

* see example with the same number in Module 1 of the IFRS Foundation training material

© 2011 IFRS Foundation

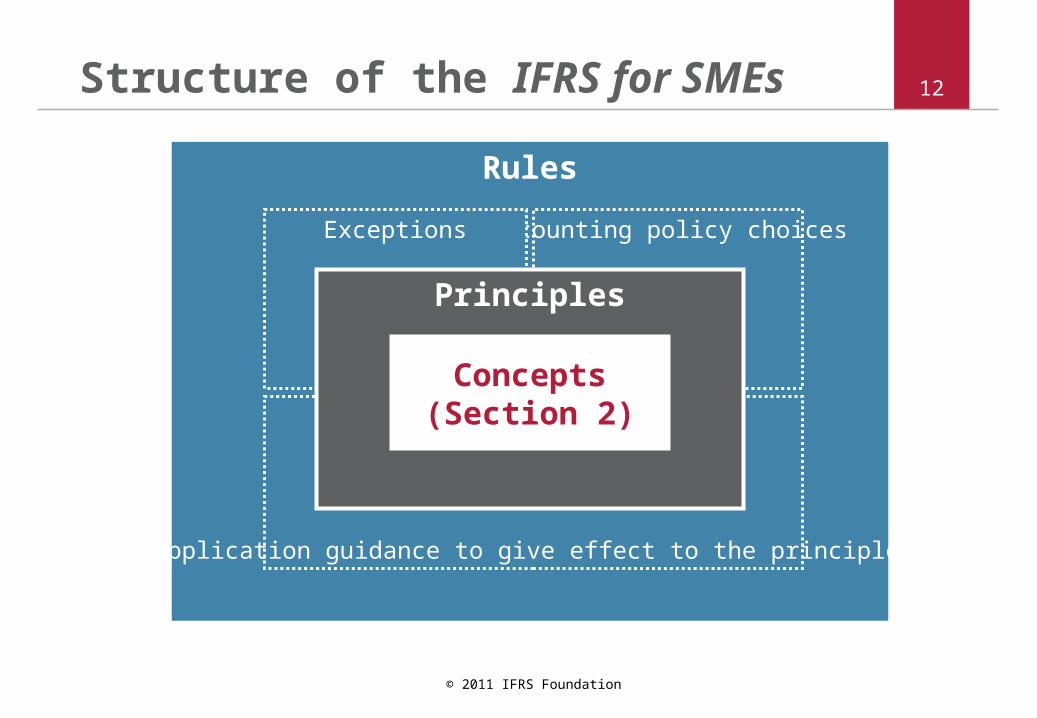

Rules

Application guidance to give effect to the principles

Accounting policy choicesExceptions

Principles

Structure of the IFRS for SMEs 12

Concepts(Section 2)

© 2011 IFRS Foundation

Section 2 Concepts and Pervasive Principles

• Objective

• Qualitative characteristics

• Elements (building blocks)

• Recognition

• Measurement

• Offsetting

13

© 2011 IFRS Foundation

Section 2 – objective

Objective of an SME’s financial statements (FS)

• to provide information about the entity’s financial position, performance and cash flows

• that is useful for economic decision-making by a broad range of users (eg investors and creditors)

• who are not in a position to demand reports tailored to meet their particular information needs

14

© 2011 IFRS Foundation

Qualitative characteristics are the attributes that make the information provided in financial statements useful to users

Section 2 – qualitative characteristics 15

© 2011 IFRS Foundation

Section 2 – QCs continued

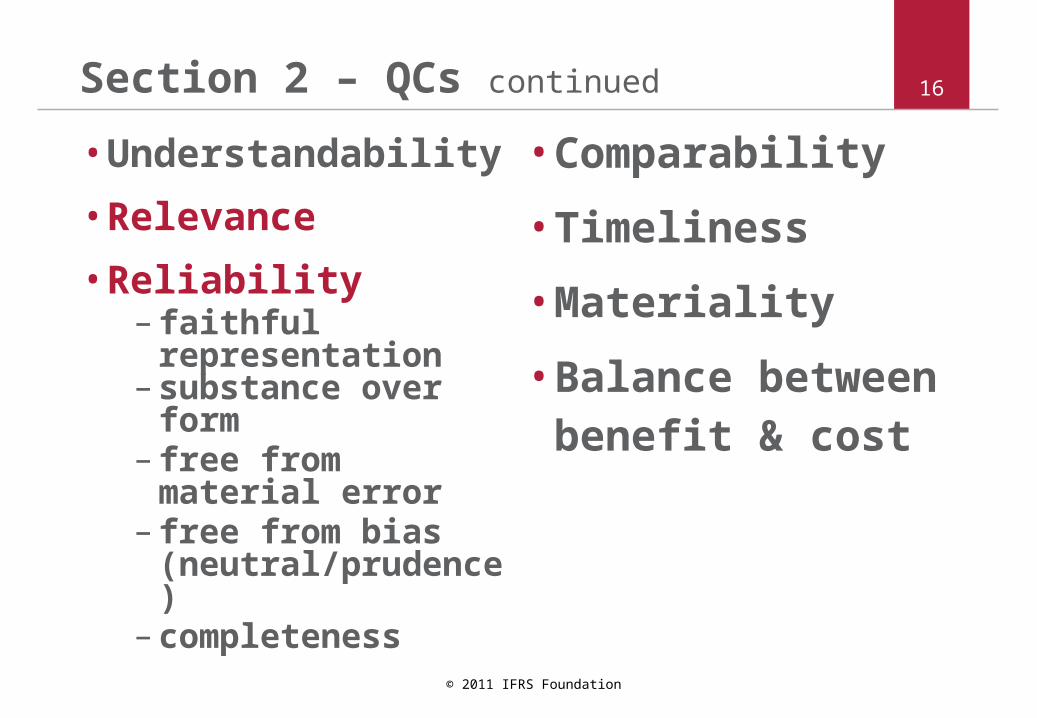

• Understandability

• Relevance

• Reliability– faithful

representation– substance over

form– free from material

error– free from bias

(neutral/prudence) – completeness

• Comparability

• Timeliness

• Materiality

• Balance between benefit & cost

16

© 2011 IFRS Foundation

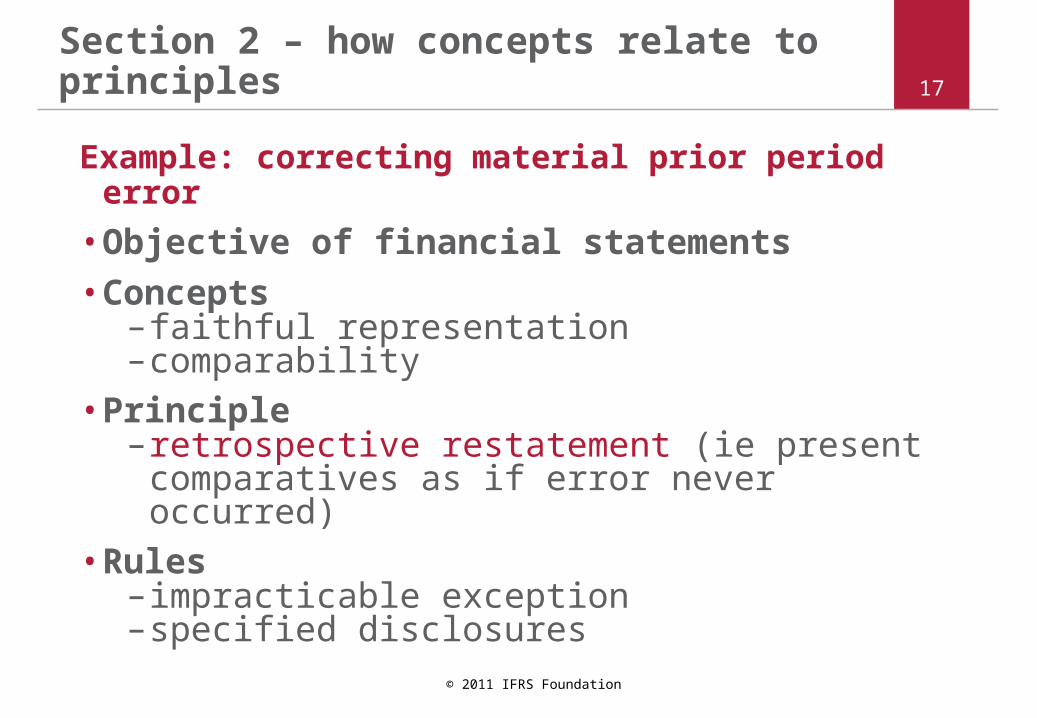

Section 2 – how concepts relate to principles

Example: correcting material prior period error

• Objective of financial statements

• Concepts– faithful representation–comparability

• Principle – retrospective restatement (ie present

comparatives as if error never occurred)• Rules

– impracticable exception–specified disclosures

17

© 2011 IFRS Foundation

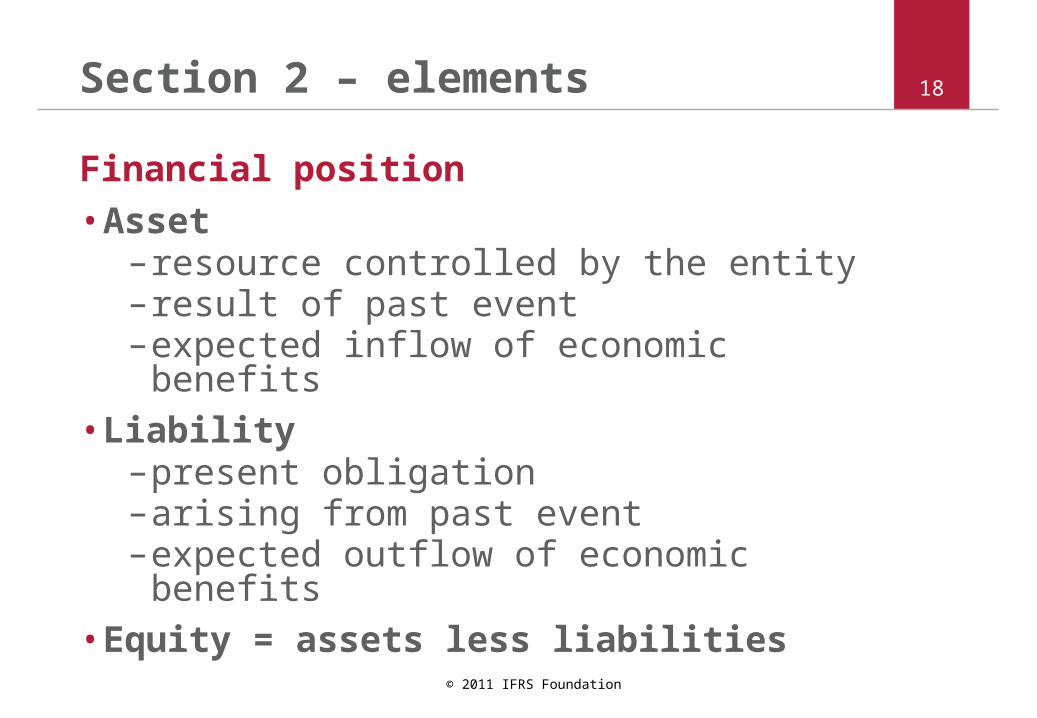

Section 2 – elements

Financial position

• Asset–resource controlled by the entity–result of past event–expected inflow of economic benefits

• Liability–present obligation –arising from past event–expected outflow of economic benefits

• Equity = assets less liabilities

18

© 2011 IFRS Foundation

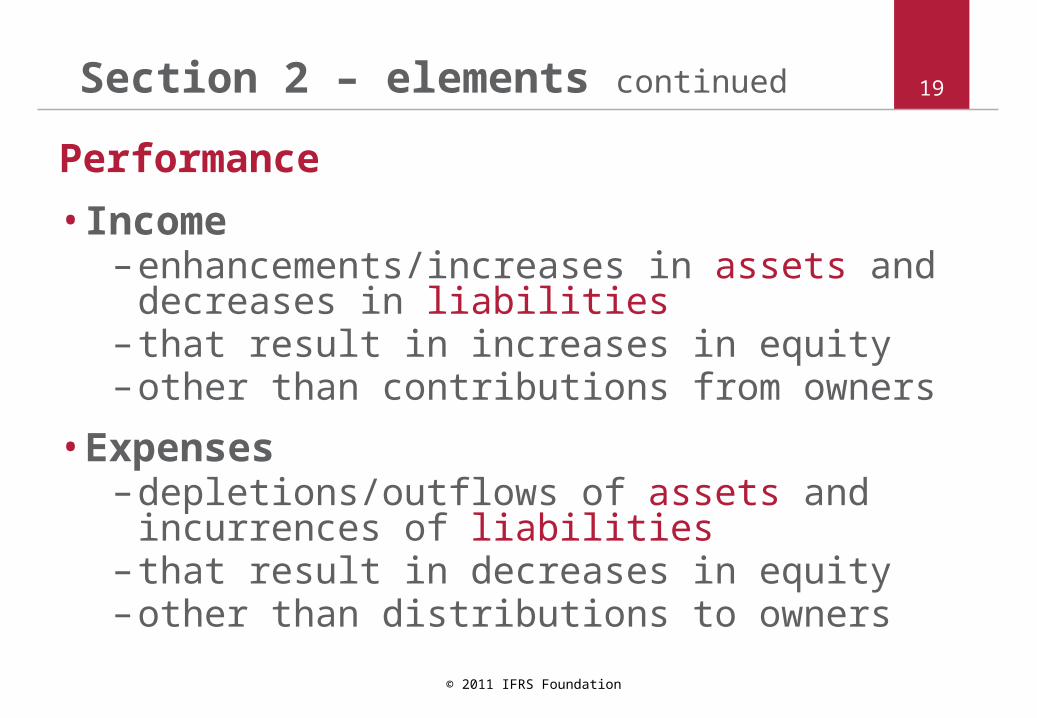

Section 2 – elements continued

Performance

• Income– enhancements/increases in assets and

decreases in liabilities – that result in increases in equity– other than contributions from owners

• Expenses– depletions/outflows of assets and incurrences of

liabilities – that result in decreases in equity– other than distributions to owners

19

© 2011 IFRS Foundation

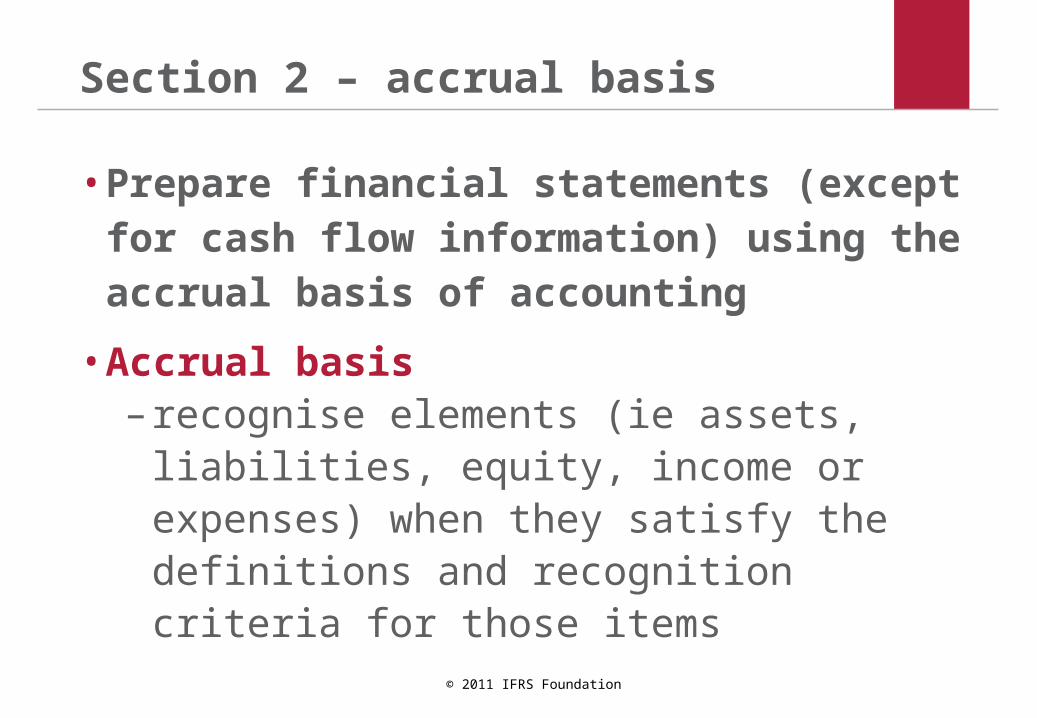

Section 2 – accrual basis

• Prepare financial statements (except for cash flow information) using the accrual basis of accounting

• Accrual basis– recognise elements (ie assets, liabilities,

equity, income or expenses) when they satisfy the definitions and recognition criteria for those items

© 2011 IFRS Foundation

Section 2 – recognition criteria

Recognise an item (element) when:

• it is probable that future economic benefit will flow to/from the entity; and

– assess probability individually unless large population of individually insignificant items then assess collectively

• the item has a cost or value that can be measured reliably

– the use of reasonable estimates–is an essential part of accounting –does not undermine the reliability of FS

21

© 2011 IFRS Foundation

Section 2 – measurement

Measurement is the process of determining the monetary amounts at which an entity measures assets, liabilities, income and expenses

• Many measurement methods in the IFRS for SMEs

• Two common measurement bases– historical cost (eg amount paid for an asset)– fair value (eg amount for which an asset could

be exchanged in arm’s length transaction)

22

© 2011 IFRS Foundation

Section 2 – measurement continued

• Most sections of the IFRS for SMEs specify a measurement base to be used

–on initial recognition–subsequently

• Some sections permit more than one measurement method (an accounting policy choice)

• In other sections measurement is circumstance driven, eg

–fair value, if it can be determined without undue cost or effort

–otherwise cost-amortisation-impairment

23

© 2011 IFRS Foundation

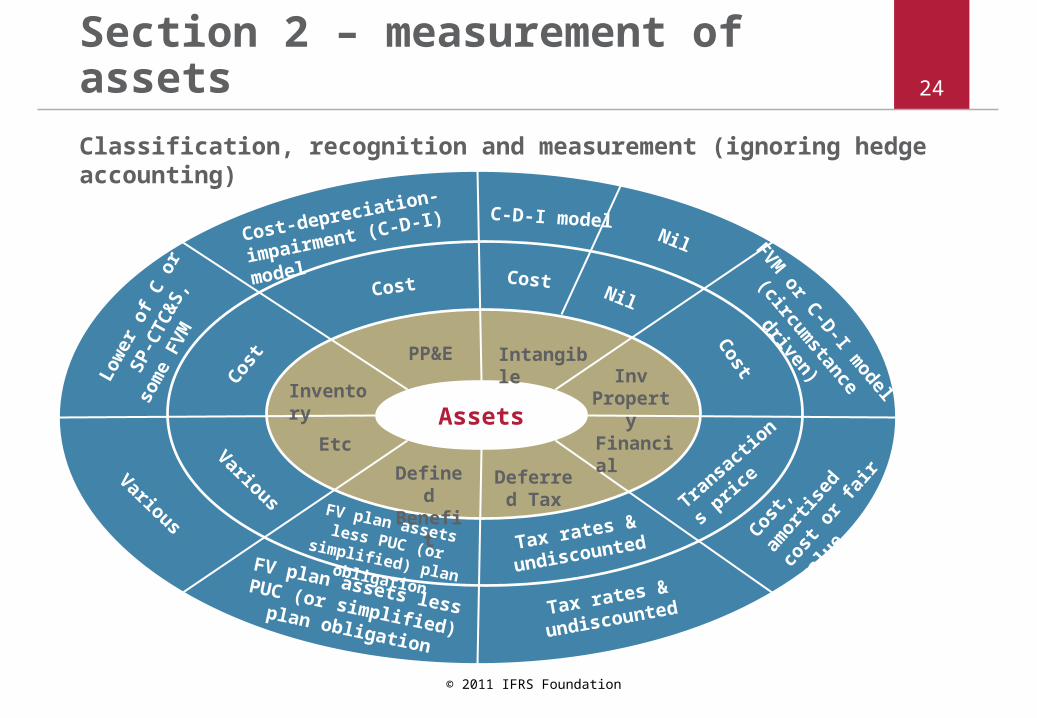

Section 2 – measurement of assets 24

Assets

Intangible

Financial

Inv Property

PP&E

Inventory

Etc

DefinedBenefit

Deferred Tax

Cost

Cost-depreciation-

impairment (C-D-I) model C-D-I model

CostNil

Nil

Low

er o

f C o

r

SP

-CTC

&S

,

som

e FV

M

Cost

Cost

FVM or C-D-I m

odel

(circumstance driven)

Transactio

ns

price

Cost,

amor

tised

cos

t

or fa

ir va

lue

Tax rates &

undiscounted

Tax rates &

undiscounted

FV plan assets less PUC (or simplified) plan obligationFV plan assets less PUC

(or simplified) plan obligation

Various

Various

Classification, recognition and measurement (ignoring hedge accounting)

© 2011 IFRS Foundation

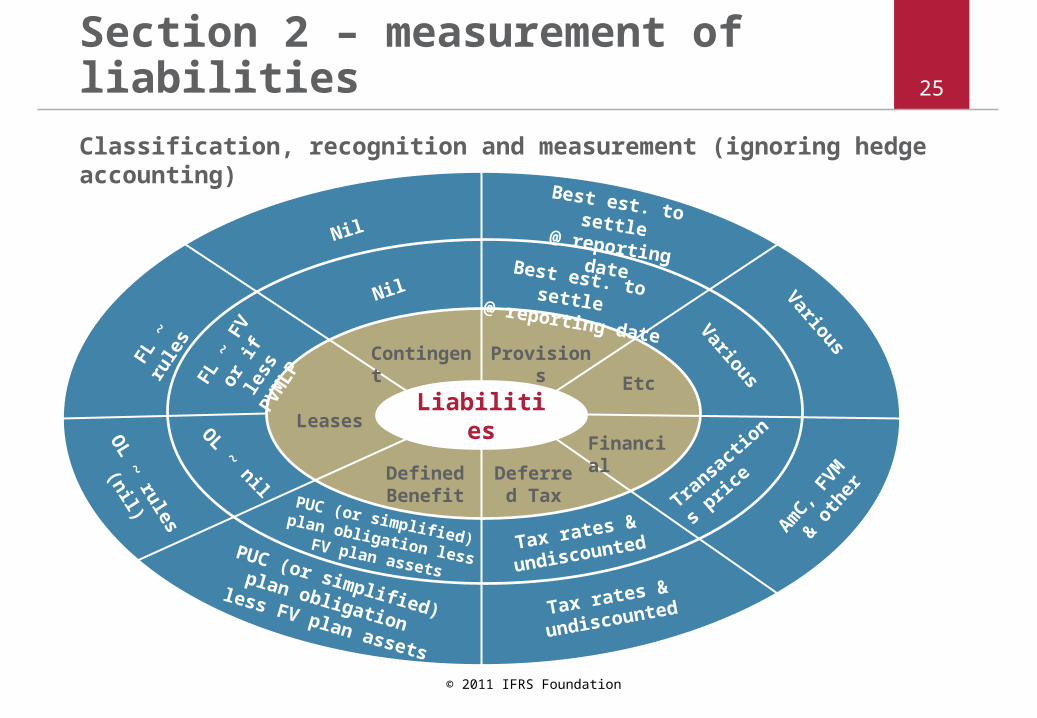

25Section 2 – measurement of liabilities

LiabilitiesFinancial

ProvisionsContingent

Leases

DefinedBenefit

Deferred Tax

Nil

NilVarious

FL ~

rul

es

OL ~ nil

Best est. to settle@ reporting date

Transactio

ns

price

AmC, F

VM

& oth

er

Tax rates &

undiscounted

Tax rates &

undiscounted

PUC (or simplified) plan obligation less FV plan assets

PUC (or simplified) plan obligation

less FV plan assets

FL ~

FV

or if

less

PVM

LP

OL ~ rules

(nil)

Best est. to settle @ reporting date

Classification, recognition and measurement (ignoring hedge accounting)

Etc

Various

© 2011 IFRS Foundation

Section 2 – absent a specific requirement

In the absence of a requirement in another section of the IFRS for SMEs that applies specifically to a transaction, other event or condition an entity’s management must use its judgement in developing an accounting policy that results in information that is relevant and reliable. …

26

© 2011 IFRS Foundation

Section 2 – absent a … continued

… In doing so management refers to:

• First, requirements and guidance dealing with similar and related issues

• Second the definitions, recognition criteria and measurement concepts and pervasive principles in Section 2

• In parallel management may also consider the requirements and guidance in full IFRSs dealing with similar and related issues

27

© 2011 IFRS Foundation

Section 2 – offsetting

An entity shall not offset assets and liabilities, or income and expenses, unless required or permitted to do so by another section of the IFRS for SMEs. However,

• measuring assets net of a valuation allowance (eg allowance for inventory obsolescence) is not offsetting

• if an entity’s normal operating activities do not include buying and selling non-current assets (including investments and operating assets) then the entity reports the profit on disposal of such items on a net basis

28

Related Documents